Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

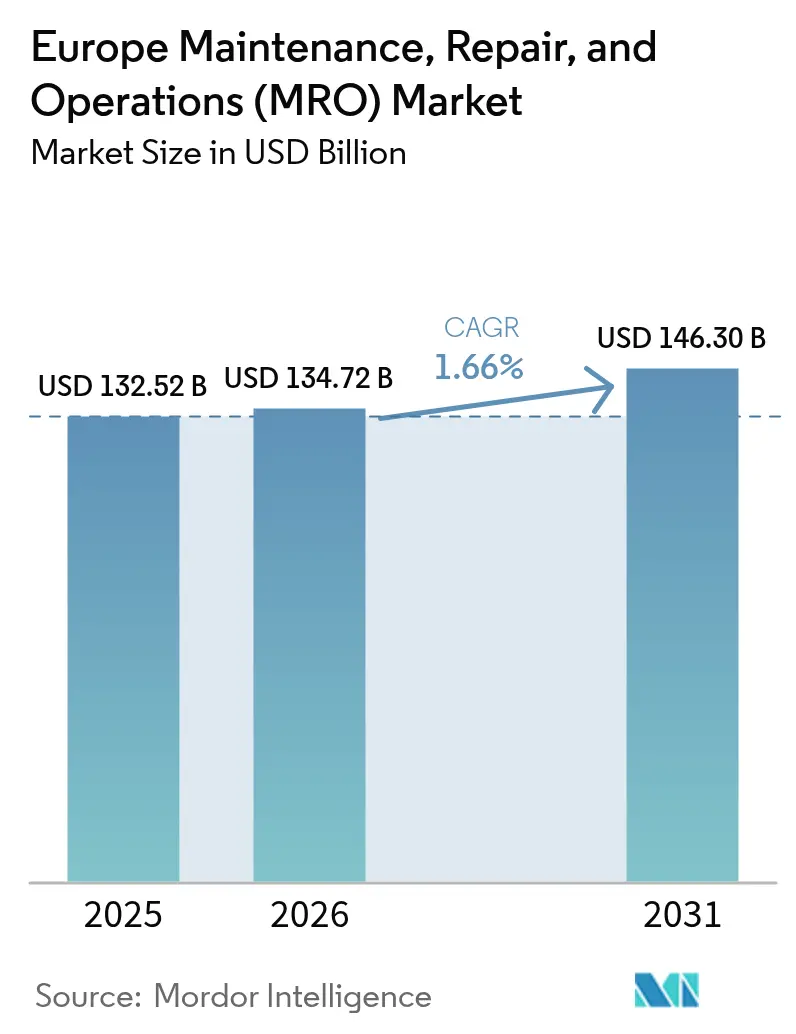

| Base Year Market Size (2025) | USD 132.52 Billion |

| Market Size (2026) | USD 134.72 Billion |

| Market Size (2031) | USD 146.3 Billion |

| Growth Rate (2026 - 2031) | 1.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Maintenance, Repair, And Operations (MRO) Market Analysis by Mordor Intelligence

The European MRO market size was valued at USD 132.52 billion in 2025 and estimated to grow from USD 134.72 billion in 2026 to reach USD 146.3 billion by 2031, at a CAGR of 1.66% during the forecast period (2026-2031). This mature yet steadily expanding trajectory stems from mandatory right-to-repair rules, circular economy legislation, and a growing reliance on data-driven maintenance strategies across the region’s diversified industrial base. Germany’s deep automation footprint, the European green-deal agenda, and heightened supply-chain resilience programs all reinforce long-term demand for integrated maintenance solutions. Rapid digitalization raises the competitive stakes for service providers who can merge mechanical, electrical, and software support into a single, coordinated offer. Meanwhile, manufacturers are shifting budget priorities from capital investments to operating expenses, accelerating the uptake of external services, and creating new revenue streams for specialized vendors. Finally, sustainability disclosures mandated by the Corporate Sustainability Reporting Directive (CSRD) intensify the requirement for life-cycle-oriented maintenance documentation, providing an extra boost to analytics-enabled service contracts.

Key Report Takeaways

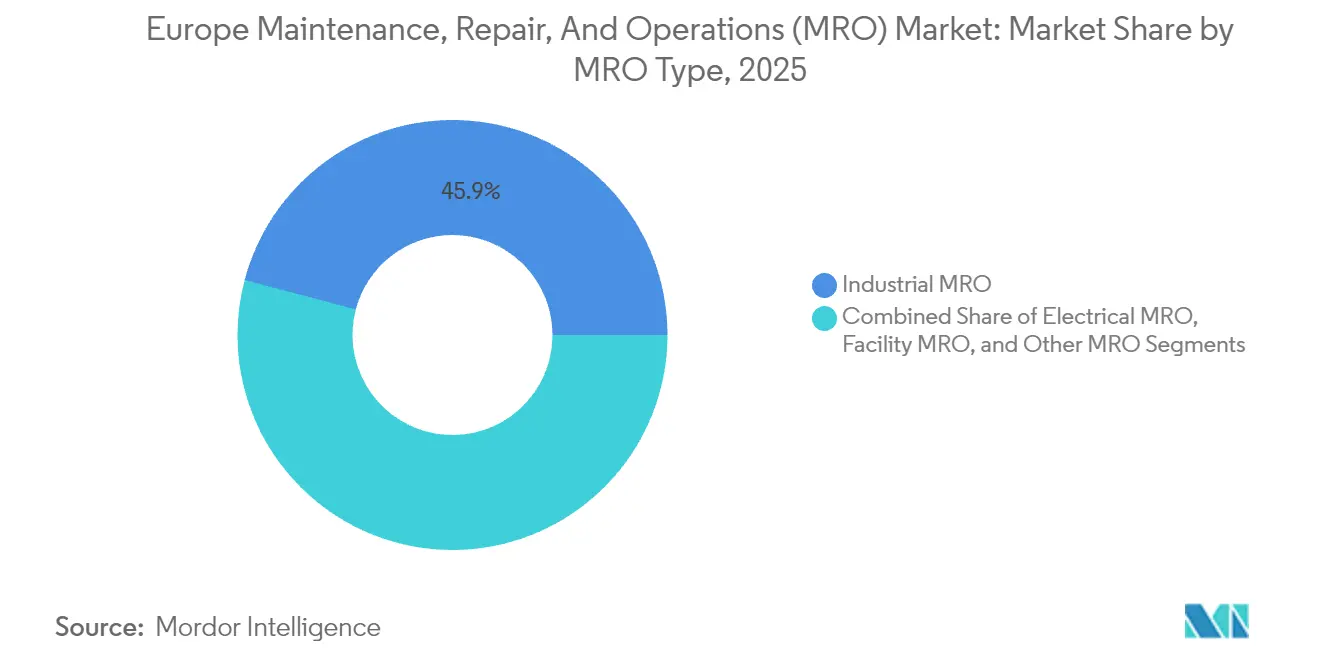

- By MRO type, Industrial MRO led with 45.88% revenue share in 2025, whereas Electrical MRO is forecast to advance at a 2.69% CAGR to 2031.

- By maintenance type, preventive routines held 57.02% of the European MRO market share in 2025, while predictive programs are projected to climb at a 6.82% CAGR through 2031.

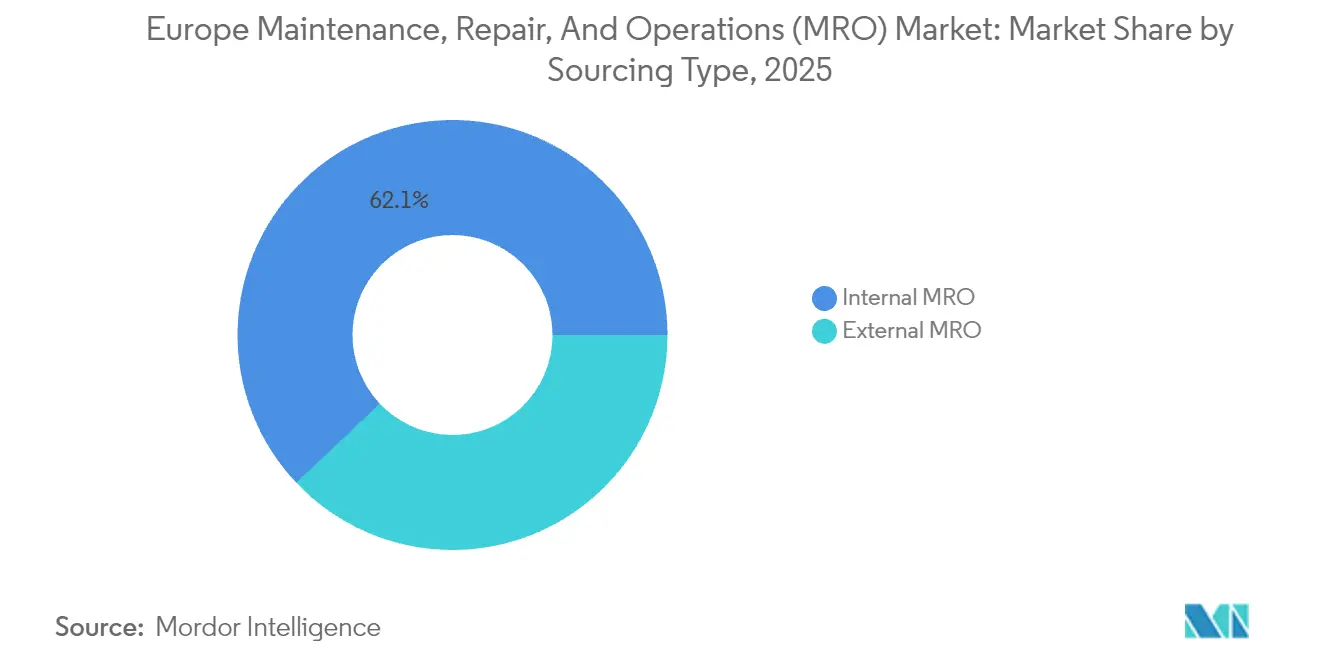

- By sourcing model, internal teams controlled 62.05% of spending in 2025; yet, external services are poised for a 6.15% CAGR, as manufacturers favor asset-light strategies.

- By end-user industry, manufacturing accounted for 31.55% of the European MRO market size in 2025, whereas the energy and utilities sector is expected to expand at a 5.21% CAGR through 2031.

- By country, Germany accounted for 38.10% of regional demand in 2025, while Spain is expected to log the fastest 4.32% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Maintenance, Repair, And Operations (MRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for predictive maintenance in European industry | +0.4% | Germany, France, the Netherlands, Nordic countries | Medium term (2-4 years) |

| Industrial automation and the need for uptime across the manufacturing base | +0.3% | Germany, Italy, the Czech Republic, and Poland | Long term (≥ 4 years) |

| Shift from capex to opex, favoring outsourced MRO contracts | +0.3% | Western Europe, early adoption in Scandinavia | Short term (≤ 2 years) |

| Sustainability legislation is driving circular and remanufactured parts | +0.3% | EU-wide, strongest in Germany, the Netherlands, and Denmark | Long term (≥ 4 years) |

| Aging aerospace and transportation fleets are demanding overhaul cycles | +0.2% | United Kingdom, France, Germany, Spain | Medium term (2-4 years) |

| E-commerce platforms optimizing MRO supply chains | +0.2% | Germany, the United Kingdom, France, Benelux | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Predictive Maintenance in European Industry

The Cyber Resilience Act requires connected-equipment manufacturers to incorporate continuous monitoring into their machines, effectively making predictive maintenance a compliance requirement.[1]European Commission, “Regulation (EU) 2024/2847 on Cybersecurity,” eur-lex.europa.eu Companies that comply early are already reducing unplanned downtime by up to 50%, a cost-saving measure that further stimulates demand for analytics-heavy MRO contracts. Germany’s government reserves EUR 2.1 billion (USD 2.26 billion) to subsidize Industry 4.0 rollouts, with 40% of that package specifically allocated for predictive infrastructure. As large OEMs increasingly require downstream suppliers to share machine health data, even mid-sized plants must adopt sensors and cloud-based analytics to remain on approved vendor lists. As the phased regulation runs until 2027, the European MRO market benefits from a staggered, multi-year investment cycle that sustains growth.

Industrial Automation and the Need for Uptime Across the Manufacturing Base

Europe’s factories operate closer to full capacity than most of their global peers, with leading German plants posting overall equipment effectiveness rates of nearly 90%. The stakes rose sharply after pandemic-era semiconductor shortages revealed how a single machine failure could ripple through entire supply networks. Automotive electrification now introduces high-voltage and battery-handling complexity, prompting firms such as Volkswagen to allocate EUR 89 billion (USD 95.8 billion) for electric-mobility infrastructure that requires specialized maintenance.[2]Volkswagen Group, “Investments in Electric Mobility,” volkswagen-group.com Czech and Polish exporters are following suit to keep pace with German benchmarks, reinforcing the region-wide priority on uptime. These dynamics draw continuous spending into the European MRO market as digital twins, smart sensors, and AI-driven diagnostics evolve from a nice-to-have to a competitive imperative.

Shift from Capex to Opex, Favoring Outsourced MRO Contracts

CSRD rules reward asset-light business models that can document lower carbon footprints and clearer cost allocation. Scandinavian manufacturers were first movers, increasing outsourced maintenance budgets by roughly one-third between 2022 and 2024 as they redeployed capital into core production. Siemens Digital Industries reports 28% year-over-year growth in external contract value, signaling a structural shift toward pay-as-you-go service models. Outsourcing also mitigates labor shortages by shifting recruitment risk to vendors, a potent incentive as Europe prepares for an estimated 145,000 technician shortfall. Consequently, specialist providers with multi-disciplinary teams and strong digital toolkits are winning longer, larger contracts across the European MRO market.

Sustainability Legislation Driving Circular and Remanufactured Parts Use

The Ecodesign for Sustainable Products Regulation mandates longer product life and material recovery, prompting companies to prioritize repairs over replacements. Denmark, the Netherlands, and Germany are showing early traction in the adoption of remanufactured parts, cutting waste while trimming maintenance costs by up to 15%. European steelmakers and component suppliers now market low-carbon or recycled-content spares, creating distinct value streams for repair-centric service providers. Over the long term, these mandates rebalance inventories toward refurbished components, deepening the skill set required of maintenance crews and broadening the scope of contracts—from standard service to complete circular economy compliance reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortage of certified technicians | -0.3% | Germany, the United Kingdom, the Netherlands, Nordic countries | Long term (≥ 4 years) |

| Volatile raw-material prices are squeezing distributor margins | -0.2% | EU-wide, especially Eastern Europe | Short term (≤ 2 years) |

| OEM data monopolies are limiting independent service access | -0.1% | Germany, France, Italy | Medium term (2-4 years) |

| Geopolitical supply-chain disruptions for critical spares | -0.2% | Eastern Europe, Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage of Certified Technicians

Europe is expected to require up to 145,000 additional maintenance technicians by 2030, resulting in a training expenditure of EUR 1.4 billion (USD 1.51 billion). Germany shoulders the heaviest burden, with 45,000 unfilled maintenance roles despite its renowned apprenticeship programs. Aviation is hit hardest because aircraft operations require lengthy certification processes; in some cases, recruits wait two years or more before they can sign off on critical tasks. The demographic reality compounds the issue: 40% of today’s maintenance workforce is over 50, which raises the urgency of replacement. Persistent scarcity raises service prices, delays repairs, and restricts the speed at which the European MRO market can scale.

Volatile Raw-Material Prices Squeezing Distributor Margins

Steel costs increased by 45% between 2022 and mid-2024, driven by energy inflation and geopolitical tensions.[3]European Steel Association, “Steel Market Developments,” eurofer.eu Titanium, palladium, and rare-earth supplies also tightened after the Russia-Ukraine conflict, inflating aerospace component costs throughout the supply chain. Smaller Eastern European vendors lack hedging capacity and therefore pass higher prices through to customers or exit the market. Energy-intensive forging and casting shops pay as much as 80% more for electricity at peak times, eroding profitability and discouraging investment in new capacity. Contract structures are shifting toward cost-plus terms, but the uncertainty still caps short-term growth within parts-dependent portions of the European MRO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By MRO Type: Electrical Specialism Outpaces Broad Industrial Base

Industrial MRO retained 45.88% of 2025 revenue owing to Europe’s vast manufacturing ecosystem and the deep integration of automation technologies that demand regular servicing. The European MRO market size for industrial plants continues to grow modestly as facilities modernize; however, the electrical segment is growing faster, driven by renewable energy rollouts and smart factory retrofits. Germany’s ramp-up of electric-vehicle charging networks alone calls for thousands of high-voltage technicians trained to both mechanical and digital standards. Although facility services like HVAC and building automation offer steady returns, emerging niches—such as the maintenance of hydrogen electrolyzers—illustrate how environmental legislation constantly extends the market’s technical frontier.

Electrical MRO’s 2.69% CAGR springs from converging trends: wider sensor deployment, grid digitalization, and stricter uptime targets for renewable assets. As more solar parks and battery-storage arrays connect to the network, preventive testing of switchgear, cables, and inverters becomes mission-critical. Hybrid service contracts, which combine mechanical fixes with software upgrades, are gaining favor, further blurring traditional category boundaries. Those who master both domains are poised to capture above-average wallet share from asset owners seeking single-source accountability across a growing array of technologies.

By Maintenance Type: Predictive Routines Transform Cost Structures

Preventive programs accounted for 57.02% of 2025 spending and remain the backbone of European reliability culture; yet, predictive analytics is rewriting the rulebook by growing at a 6.82% CAGR. Real-time data enables operators to schedule work only when indicators cross risk thresholds, thereby reducing spare parts consumption and freeing labor for more strategic tasks. Early adopters such as BMW report 40% fewer unscheduled stops, which translates into direct margin gains and stronger supply-chain credibility. Consequently, the European MRO market size allocated to sensors, cloud platforms, and AI models climbs each year.

Corrective tasks still matter because no predictive model can foresee every failure. When turbines, engines, or robotic cells break unexpectedly, downtime losses can exceed EUR 100,000 (USD 108,000) per hour. Vendors now deploy augmented-reality headsets to accelerate complex repairs, while drone inspection shrinks outage windows for high-rise or offshore assets. As the service mix shifts, providers who can pivot between data-driven forecasting and responsive crisis management will protect their revenue streams, even as predictive penetration deepens.

By Sourcing Type: External Expertise Gains Momentum

Internal teams controlled 62.05% of 2025 spend, underscoring Europe’s longstanding preference for in-house technical mastery. Nevertheless, the external portion is rising at a 6.15% CAGR, as equipment complexity outpaces corporate skill-development cycles. Asset-light, sustainability-oriented financial reporting under CSRD further nudges management toward outsourcing, particularly in high-cost Nordic economies.

External suppliers differentiate themselves by bundling uptime guarantees, inventory management, and compliance reporting into a single performance-based contract. Scale allows them to invest in niche skills, such as additive-manufactured spare production, that most plant operators cannot justify alone. Over time, partner ecosystems, rather than individual workshops, will dominate the European MRO market, mirroring trends seen earlier in IT and logistics outsourcing.

By End-User Industry: Energy Transition Sets the Pace

Manufacturing still contributed 31.55% of 2025 turnover, reflecting Europe’s dense network of automotive, chemical, and machinery plants that require constant upkeep. However, energy and utilities already post a market-leading 5.21% CAGR as the continent pours EUR 584 billion (USD 629 billion) into REPowerEU projects, which include wind, solar, and grid modernization. Turbines require gearbox checks every 6-12 months, and solar sites necessitate regular inverter calibration and cleaning to maintain optimal yield.

Aerospace remains a high-value sector due to its safety-critical processes, while the automotive industry's shift to electric drivetrains multiplies service tasks for battery handling, thermal management, and software updates. Meanwhile, nascent fields like hydrogen production and carbon capture create fresh blue-ocean prospects for agile maintenance players that can blend process, electrical, and digital know-how.

Geography Analysis

Germany’s large installed base, combined with high uptake of predictive maintenance, secures its leadership position. Widespread automation and Federal funding sustain a strong pipeline of retrofit projects that underpin the European MRO market. The United Kingdom follows, with diversified demand from aerospace engines, offshore wind farms, and rail overhauls, although post-Brexit customs formalities add cost friction to cross-border parts movements. France’s nuclear fleet and Airbus production lines ensure a steady flow of specialized maintenance requirements, while national decarbonization goals drive upgrades in HVAC and building management systems. Italy’s machinery and luxury automotive clusters prefer preventive disciplines rooted in lean manufacturing culture; yet, rising EV adoption is prompting new skills investments. Spain’s rapid growth stems from the deployment of solar and onshore wind energy across Andalusia and Castilla-La Mancha, creating an outsized demand for high-voltage electricians and blade technicians. The Rest of Europe captures Poland, the Czech Republic, and Hungary, where EU funds stimulate factory modernization and extend the European MRO market share into Central and Eastern corridors.

Supply-chain resiliency imperatives born out of the Russia-Ukraine conflict are propelling regional sourcing; many German and Austrian firms are relocating critical spare parts depots to Dutch ports and Polish free zones to cushion geopolitical shocks. Pan-European e-commerce platforms further shorten lead times, particularly for small and medium-sized enterprises. Overall, geography-specific policies, investment incentives, and changes in the energy mix produce a heterogeneous yet collectively expanding European service landscape.

Competitive Landscape

The European maintenance arena is moderately fragmented, with large aerospace specialists coexisting alongside thousands of local industrial workshops. Lufthansa Technik, Safran, and MTU Aero Engines dominate aviation engine and APU workscopes, leveraging scale and OEM alliances to secure double-digit operating margins. Industrial segments remain more fragmented but are progressing toward consolidation as vendors aggregate predictive analytics capabilities to secure global framework deals.

Technology adoption shapes competitive advantage. Service providers deploying digital twins, machine-learning prognostics, and augmented-reality repair guidance report 20-30% higher productivity compared to their peers.[4]Lufthansa Technik, “Press Releases,” lufthansa-technik.com Many independent companies lack the capital to keep pace and are therefore targets for acquisition. EasyJet’s purchase of SR Technics Malta and Sonaca’s tie-up with Aciturri illustrate the momentum toward vertical integration, ensuring aircraft operators and airframe suppliers control critical capacity.

White-space opportunities emerge in green-energy and hydrogen-infrastructure maintenance, areas where few incumbents possess deep domain knowledge. Vendors able to staff composite-blade repair teams or electrolyzer stack specialists will capture a disproportionate share as Europe scales its renewable capacity. Simultaneously, the skilled labor deficit elevates talent management to a strategic priority, prompting leaders to launch in-house academies and cross-training programs that not only lock in expertise but also enhance the employer brand.

Europe Maintenance, Repair, And Operations (MRO) Industry Leaders

Wurth Group GmbH

W.W. Grainger Inc.

Sonepar SA

Rexel SA

WESCO International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nayak Aircraft Services completed the purchase of Nordic MRO and formed Nayak-LM Nordic AB, boosting ATR turboprop coverage across Northern Europe.

- December 2024: Sonaca agreed to acquire 51% of Aciturri Aerostructures for EUR 1.1 billion (USD 1.18 billion), creating a top-three independent aerostructures group.

- July 2024: AMETEK consolidated U.K.-based AEM and France-based ANTAVIA to focus on Europe’s business-jet segment, forecast to reach USD 7.08 billion by 2030.

- June 2024: Airbus finalized an agreement with Spirit AeroSystems covering St. Nazaire and Belfast sites, with a USD 559 million consideration to reinforce program stability.

Europe Maintenance, Repair, And Operations (MRO) Market Report Scope

Maintenance, repair, and operations (MRO) items are products and materials purchased by companies that are not directly employed in their manufacturing process. These products are mostly used to keep business operations running.

Europe Maintenance, Repair, and Operations (MRO) Market is segmented by MRO Type (Industrial MRO, Electrical MRO, Facility MRO) and Country (United Kingdom, Germany, France, Spain). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By MRO Type

| Industrial MRO |

| Electrical MRO |

| Facility MRO |

| Other MRO Types |

By Maintenance Type

| Preventive |

| Predictive |

| Corrective |

By Sourcing Type

| Internal MRO |

| External MRO |

By End-user Industry

| Manufacturing |

| Aerospace |

| Automotive |

| Energy and Utilities |

| Others |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By MRO Type | Industrial MRO |

| Electrical MRO | |

| Facility MRO | |

| Other MRO Types | |

| By Maintenance Type | Preventive |

| Predictive | |

| Corrective | |

| By Sourcing Type | Internal MRO |

| External MRO | |

| By End-user Industry | Manufacturing |

| Aerospace | |

| Automotive | |

| Energy and Utilities | |

| Others | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size of the European MRO market in 2026?

The market is valued at USD 134.72 billion in 2026 and is projected to reach USD 146.3 billion by 2031.

What is the expected CAGR for Europe’s MRO services between 2026 and 2031?

The market is forecast to grow at a 1.66% CAGR over the period.

Which segment is expanding fastest within Europe’s maintenance landscape?

The Electrical MRO segment is the fastest-growing, projected to grow at a 2.69% CAGR through 2031.

Why is predictive maintenance gaining traction in Europe?

EU cybersecurity and right-to-repair mandates necessitate continuous monitoring, enabling up to 50% cost savings in unplanned downtime.

What factor most constrains market growth?

Acute shortages of certified technicians—estimated at up to 145,000 by 2030—pose the primary growth bottleneck.

Which country is expected to deliver the strongest growth rate by 2031?

Spain is forecast to post the highest national CAGR at 4.32%, driven by large-scale renewable-energy investments.

Page last updated on: