Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

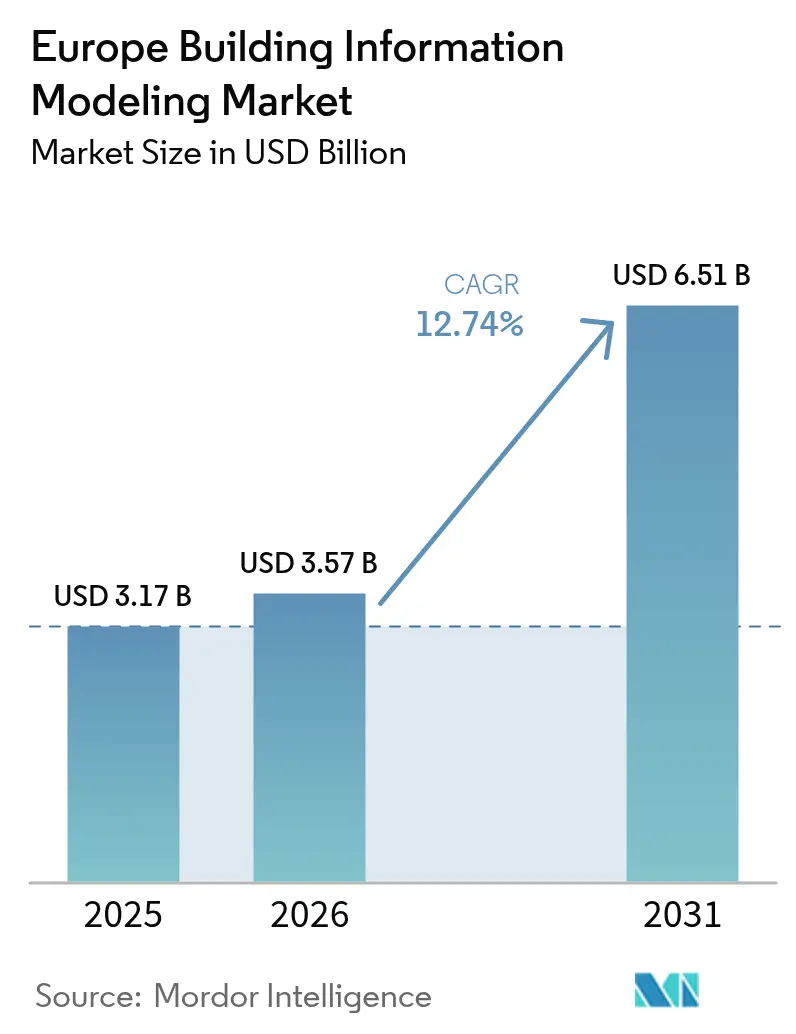

| Base Year Market Size (2025) | USD 3.17 Billion |

| Market Size (2026) | USD 3.57 Billion |

| Market Size (2031) | USD 6.51 Billion |

| Growth Rate (2026 - 2031) | 12.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Building Information Modeling Market Analysis by Mordor Intelligence

The Europe Building Information Modeling Market size was valued at USD 3.17 billion in 2025 and estimated to grow from USD 3.57 billion in 2026 to reach USD 6.51 billion by 2031, at a CAGR of 12.74% during the forecast period (2026-2031).

Accelerated digitization funding, binding regulatory mandates, and growing demand for lifecycle carbon reporting are reshaping procurement priorities and sustaining the region’s rapid growth trajectory. Government-backed incentives under the EUR 750 billion (USD 847.5 billion) Recovery and Resilience Facility continue to fast-track software investments, while large-scale public infrastructure programs and private commercial projects widen the addressable base of adopters. Cloud deployment and subscription licensing are expanding rapidly, giving smaller engineering teams affordable entry points and pushing established vendors toward open, collaborative ecosystems. Simultaneously, AI-assisted model optimization and automated clash detection shrink design lead times, enabling contractors to deliver complex, multinational projects with lower risk and higher cost certainty. Mid-sized and specialist service providers are riding this momentum by bundling technical training, project management, and data governance into turnkey packages that complement licensed software.

Key Report Takeaways

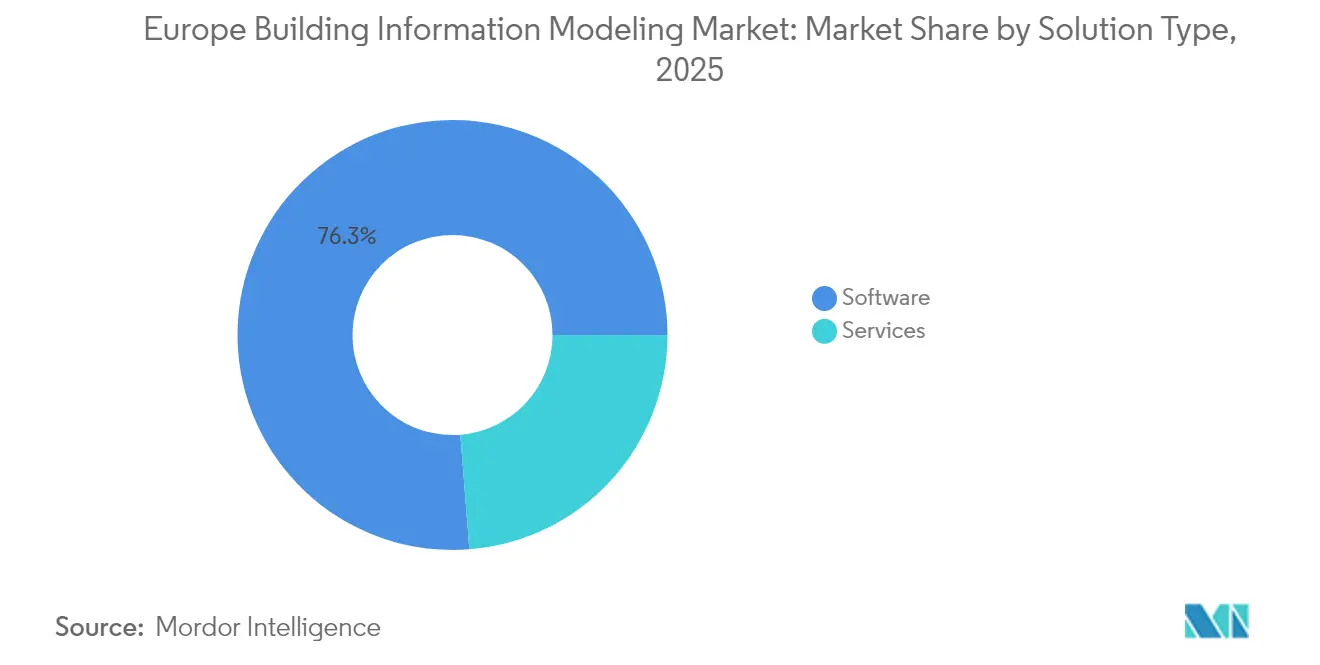

- By type, software held 76.25% of Europe BIM market share in 2025, while services posted the fastest 13.05% CAGR through 2031.

- By deployment model, on-premise accounted for 57.45% share of the Europe BIM market size in 2025 and cloud recorded the highest 13.30% CAGR outlook.

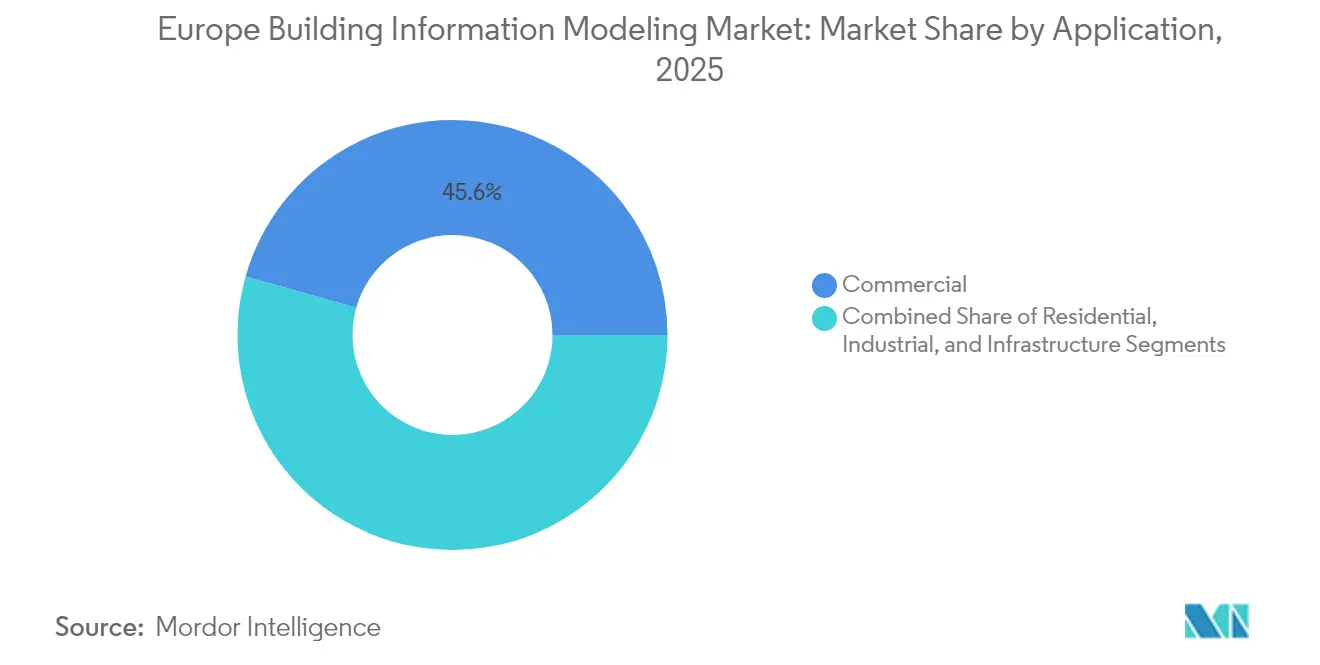

- By application, commercial construction led with 45.62% share in 2025; infrastructure is expanding at 13.32% CAGR to 2031.

- By end-user, architects and designers commanded 33.78% share in 2025, whereas facility owners and operators are projected to grow at 13.56% CAGR through 2031.

- By country, the United Kingdom captured 28.85% share in 2025 and the Netherlands shows the strongest 13.70% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Building Information Modeling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-mandated BIM adoption | +3.2% | EU-wide - strongest in United Kingdom, Germany, Netherlands | Medium term (2-4 years) |

| Accelerated digitization funding | +2.8% | EU-wide - concentrated in Southern and Eastern Europe | Short term (≤ 2 years) |

| Shift to cloud-based collaborative platforms | +2.1% | Global - early adoption in Nordics and Netherlands | Medium term (2-4 years) |

| EU Green Deal lifecycle-carbon linkage | +1.9% | EU-wide - strongest in Germany, France, Netherlands | Long term (≥ 4 years) |

| Growing offsite-modular adoption | +1.7% | Northern Europe, Germany, Netherlands, Nordics | Medium term (2-4 years) |

| AI-driven generative design | +1.3% | Technology hubs: United Kingdom, Germany, Netherlands, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-mandated BIM adoption drives procurement transformation

EU Public Procurement Directives oblige public sector owners to demand BIM-compliant deliverables, transforming tender requirements across 27 member states and promoting coordinated digital workflows.[1]German Federal Ministry of Transport, “Digital Planning and Building,” bmvi.de The United Kingdom has enforced a Level 2 mandate since 2016, while Germany requires BIM for federal transport schemes from 2020. Italy’s phased policy reaches full coverage for projects above EUR 1 million by 2025, creating firm deadlines that accelerate software purchases, staff certification, and process reengineering. These rules lift entry barriers for software and service suppliers, but they also penalize contractors that defer upskilling, effectively pushing the entire value chain toward digital maturity over the medium term.

Accelerated digitization funding reshapes investment priorities

Under the Recovery and Resilience Facility, each member state must channel at least 20% of its allocation toward digital transition, and construction digitalization qualifies as an eligible spend.[2]European Commission, “Recovery plan for Europe,” commission.europa.eu Southern and Eastern Europe receive a disproportionate share, unlocking capital for firms that historically lacked resources to migrate from 2D workflows. Because stimulus spending is time-bound to 2026, many public owners are issuing front-loaded, multi-year BIM tenders, thereby compressing deployment timelines. Vendors that can bundle cloud hosting, user training, and compliance audits within turnkey packages are capturing this surge, even as the pipeline may normalize once stimulus funds taper.

Shift to cloud-based collaborative design platforms

Cloud environments offer real-time model sharing and version control, which is vital for cross-border infrastructure such as the Scandinavian-Mediterranean rail corridor. Denmark mandates cloud-based Common Data Environments for state projects by 2025, and the Netherlands aligns with buildingSMART’s open BIM schema so stakeholders can interchange data freely. Subscription licensing reduces upfront costs and layers in analytics modules, making high-performance computing accessible to smaller subcontractors. AI-driven rule checks embedded in cloud services slash RFIs and rework, which helps contractors protect thin margins under target-cost contracts.

EU Green Deal integrates carbon reporting with BIM workflows

The Energy Performance of Buildings Directive requires digital logbooks by 2025, compelling building owners to capture embodied and operational carbon across the asset lifecycle.[3]European Commission, “Energy Performance of Buildings Directive,” energy.ec.europa.eu Software vendors now embed environmental databases and automated material quantification tools so designers can run carbon scenarios alongside cost estimates. Germany and the Netherlands extend the rule to major renovations, widening the serviceable market to heritage retrofits. Consolidation between BIM vendors and sustainability analytics specialists, exemplified by One Click LCA’s acquisition of Buildrz, signals rising demand for fully integrated design-to-operation platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront software and training costs | -2.1% | EU-wide - strongest on SME contractors in Southern and Eastern Europe | Short term (≤ 2 years) |

| Persistent skills gap among SME contractors | -1.8% | EU-wide - acute in Germany, France, Italy | Medium term (2-4 years) |

| Inconsistent national BIM maturity | -1.3% | Cross-border projects, Eastern European markets | Medium term (2-4 years) |

| Fragmented interoperability standards | -1.1% | EU-wide - multi-vendor environments | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

High implementation costs constrain SME adoption

Comprehensive BIM suites can cost more than EUR 10,000 per seat each year, and contractors must add workstation upgrades and multi-week training programs to achieve competence. These outlays deter smaller trade firms, which still form the bulk of Europe’s supply chain. Although subsidies exist, complex application procedures and co-financing requirements often sideline the smallest entities. As larger contractors push BIM deliverables down the subcontracting pyramid, SMEs without digital capacity risk being disqualified from lucrative projects, slowing homogeneous market penetration in the short term.

Persistent skills gap limits implementation effectiveness

Industry polls reveal that 42% of European construction companies cannot source enough BIM-literate staff to meet project pipelines.[4]EY Italy, “Il BIM è il protagonista della Trasformazione Digitale,” ey.com Germany, France, and Italy are especially constrained as public works accelerate. Universities and vocational institutions are adding curricula, yet a multi-year lag persists between enrollment and graduate output. Scarcity drives up salaries for certified BIM managers, raising project overheads and delaying delivery schedules. Managed-service providers partially bridge the gap, but high demand continues to outstrip available talent in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Services Illuminate Value Beyond Software

Software solutions captured 76.25% of Europe BIM market share in 2025, confirming their foundational status within design offices and contractor headquarters. However, the services segment is advancing at a 13.05% CAGR, outpacing licensed applications as owners and contractors seek expert partners who can translate regulatory mandates into BIM execution plans. The Europe BIM market size for implementation and consulting services is projected to widen as compliance auditing, change management, and CDE administration become recurring necessities. Embedded service packages attached to annual subscriptions blur boundaries, encouraging vendors to act as strategic advisors as well as software providers.

Rising project complexity and cross-border collaboration elevate demand for federated model coordination, clash resolution, and data governance documentation. Services firms offer essential guidance on ISO 19650 certification, cybersecurity, and lifecycle data handover. As public owners embed carbon tracking into tenders, consultants skilled in environmental data integration are differentiating themselves. Consequently, mergers and acquisitions such as Nemetschek’s USD 3.277 billion service-oriented spree are likely to continue as vendors chase downstream revenue.

By Deployment: Cloud Channels Democratize Access

On-premise deployments controlled 57.45% of the Europe BIM market size in 2025, favored by companies wary of data sovereignty rules, particularly in Germany. Yet cloud environments are forecast to expand 13.30% CAGR, riding new work routines shaped by pandemic-era remote collaboration. Flexible subscription plans minimize capex and embed automatic updates, drawing small subcontractors who previously relied on entry-level drafting tools.

Interoperability frameworks such as IFC 4.3 and BCF 3.0 ease data exchange, increasing comfort with off-premise storage. Nordic and Dutch public owners already require cloud-based CDEs, accelerating adoption curves. Hybrid topologies are gaining traction: sensitive data are ring-fenced on local servers while non-critical tasks flow to cloud analytics. This model balances compliance with productivity, clearing a pathway for universal connectivity across scattered supply chains.

By Application: Infrastructure Investment Fuels the Next Wave

Commercial construction applications delivered 45.62% of revenue in 2025, reflecting high-profile office and retail projects in capital cities and major economic hubs. Multidisciplinary teams rely on 3D models to coordinate complex MEP systems and façade geometries. Infrastructure, however, is sprinting ahead at a 13.32% CAGR, lifted by the Trans-European Transport Network and renewable-energy corridors. Rail, highway, and offshore wind developers use model-based scheduling and digital twins to minimize downtime and extend asset life. The Europe BIM market share for infrastructure is poised to eclipse commercial volumes within a decade if investment pipelines remain on course.

Digital twinning in airports, seaports, and bridges supports predictive maintenance and real-time operations. Gatwick Airport’s airside facilities leverage sensor-fed BIM twins for condition monitoring, underscoring the shift from design-focused models to operational intelligence systems capable of integrating IoT data streams in near real time.

By End-user: Owners Emerge as Digital Stewards

Architects and designers retained a 33.78% stake in 2025, yet facility owners and operators are growing 13.56% CAGR, signaling a fundamental pivot toward lifecycle performance rather than front-end design savings.

Mandated digital logbooks and carbon passports compel owners to budget for long-term data custodianship. Hospitals, universities, and logistics hubs increasingly request asset-linked BIM deliverables to streamline FM handover and enable predictive asset management. As a result, software workflows now integrate CAFM and BMS platforms to deliver unified dashboards, broadening the market for post-construction analytics services.

Geography Analysis

The United Kingdom contributed 28.85% of 2025 revenue and remains the anchor of the Europe BIM market, backed by its long-standing Level 2 mandate and world-leading consultant base. Flagship programs such as HS2 and Thames Tideway rely on 5D modeling to compress schedules and tighten cost control. The Building Safety Act compels high-rise operators to submit secure digital records, infusing demand for as-built models long after completion.

Germany follows closely, propelled by its Masterplan BIM and autonomous automotive manufacturing campuses that depend on integrated factory-building models. Large municipal transportation projects and energy-transition infrastructure attach strict BIM requirements, reinforcing service demand. Preference for hybrid deployments is pronounced due to strong data-privacy culture, sustaining a sizeable on-premise segment.

The Netherlands tops the growth chart with a 13.70% CAGR through 2031 as circular economy goals enforce material passports and disassembly-ready design. Digital building passports for all new builds by 2025 transform BIM files into legal records of material quantity and embedded carbon.Progressive public-sector procurement accelerates cloud adoption, enabling SMEs to access high-fidelity models via browser-based viewers without heavy hardware.

Nordic nations collectively invest in pan-regional corridors such as Fehmarnbelt, showcasing model-based regulatory review and automated compliance.

Italy’s stepped mandate coupled with EU funding narrows its adoption gap, while Spain leverages Recovery Facility grants for hospital retrofits that incorporate BIM-driven energy upgrades.

Regulatory Landscape

BIM requirements in Europe are shaped by EU public procurement practices and a growing set of EU-wide construction digitization rules. EU Public Procurement Directives have embedded BIM-compliant deliverables into tendering across member states, while national mandates continue to harden timelines, including the United Kingdoms Level 2 mandate (since 2016), Germanys BIM requirement for federal transport schemes (from 2020), and Italys phased policy reaching full coverage for projects above EUR 1 million by 2025. At the EU level, CEN/TC 442 supports standardization through EN ISO 19650 for information management and EN ISO 16739-1 (IFC) for data exchange, reinforcing the direction toward auditable and interoperable deliverables.

Rules for product and asset information are increasingly tying BIM deliverables to regulated data flows across the construction supply chain. Regulation (EU) 2024/3110 (Construction Products Regulation) entered into force on 7 January 2025 and became generally applicable on 8 January 2026, introducing a framework for digital product information flows, including Digital Product Passport concepts for construction products. Separately, the EU BIM Task Group has pushed for harmonized, vendor-neutral openBIM approaches for public procurement, including a position paper released in November 2025 that calls for minimum, aligned BIM requirements across the EU. That proposal raises expectations for Common Data Environments, information-management plans, and standardized handover data.

Value Chain Analysis

The Europe BIM value chain begins with standard setters and public-sector clients that define information requirements, then moves through software and cloud-platform providers, implementation partners, and project delivery stakeholders. European standards bodies (notably CEN/TC 442 via EN ISO 19650 and EN ISO 16739-1/IFC) and cross-government coordination through the EU BIM Task Group help set the data formats and information-management practices that vendors and service firms operationalize. Upstream software publishers and CDE vendors provide authoring tools, model coordination, and APIs, while system integrators, BIM consultants, and managed-service providers translate regulatory and client requirements into BIM execution plans, ISO 19650-aligned processes, and model governance.

Downstream, designers, engineers, general contractors, and specialist subcontractors create and exchange models, schedules, and asset data, with facility owners and operators increasingly setting requirements for lifecycle handover data and digital records. Value capture concentrates in software licensing and subscriptions, including cloud CDE administration, and in professional services such as implementation, training, and compliance audits. Adjacent workflows like reality capture, model federation, and sustainability and carbon reporting integration also support monetization. Friction points persist around cross-border interoperability and uneven national maturity, with legal BIM mandates in public procurement accelerating adoption for large public programs (about 12 as of 2024) while leaving many SMEs more dependent on prime contractors requirements and available training capacity.

Competitive Landscape

The Europe BIM market features moderate concentration: the top five suppliers account for about 55% revenue, leaving scope for mid-tier entrants and niche specialists. Autodesk, Nemetschek, and Bentley Systems anchor the field with comprehensive suites, large installed bases, and active acquisitions. Nemetschek’s dividend increase to EUR 0.55 (USD 0.622) per share underscores healthy cash flows that finance R&D in AI and open BIM. Bentley reports double-digit recurring revenue growth powered by cloud subscriptions and infrastructure-twin services.

New challengers including Speckle and Didimi pursue interoperability overlays that bridge proprietary silos, alleviating a prime pain point voiced by public agencies. hsbcad and Hexagon target vertical niches such as offsite timber and reality-capture-to-model workflows, extending BIM’s footprint to fabrication and field robotics. AI-assisted code compliance and generative design remain white-space opportunities; early pilots demonstrate cost savings, but widespread roll-out awaits validated benchmarks.

Suppliers differentiate on local language support, native compliance libraries, and ISO 19650 certification touted during public tenders. Service-centric hybrid bundles are increasing, binding software licenses to multi-year consulting retainers. This trend blurs traditional product boundaries and tilts competitive focus toward time-to-value and embedded analytics rather than feature parity alone.

Europe Building Information Modeling Industry Leaders

Autodesk, Inc.

Dassault Systèmes SE

Hexagon AB

Trimble Inc.

Bentley Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulated digital product information and public-procurement harmonization create opportunities for BIM platforms and services that can operationalize interoperable, machine-readable construction data across suppliers and projects. Regulation (EU) 2024/3110 becoming generally applicable on 8 January 2026, alongside its Digital Product Passport direction for construction products, pushes manufacturers, contractors, and project teams toward standardized data dictionaries, structured product attributes, and traceable documentation. Those requirements are increasingly expected to link to BIM objects and to support model-based procurement. This lifts demand for openBIM-aligned workflows (IFC and ISO 19650) and for service providers that can map product data, set up CDE governance, and audit deliverables for regulated documentation.

Large infrastructure programs are functioning as practical testbeds for advanced CDE and digital-twin workflows, which creates room for platform vendors and specialist integrators focused on cross-discipline collaboration and model-based delivery at scale. In June 2026, Bentley Systems tooling (including ProjectWise CDE) was used by Egis on the Seine-Nord Europe Canal project, with reported productivity gains tied to common data management and coordinated modeling practices. That use case supports continued demand for enterprise CDE rollouts on multi-stakeholder programs. Similar momentum appears in Northern and Baltic project pipelines where full BIM modeling and shared environments are being deployed for rail assets, supporting opportunities in data governance, information-exchange automation, and lifecycle handover integration, particularly as owners tighten requirements for operational digital records and asset-linked documentation.

Recent Industry Developments

- June 2026: Nemetschek and its brand Graphisoft announced an upcoming Archicad-Autodesk Forma Connection add-on aimed at improving continuity between early design and BIM authoring workflows. The announcement targets buyer demand for vendor-spanning interoperability and reduces data friction for teams running mixed toolchains across architecture and construction delivery.

- December 2025: Autodesk announced a fifth strategic partnership agreement with Royal BAM Group NV, extending a long-running collaboration focused on BIM-driven and AI-enabled construction workflows. The renewal reinforces large-contractor standardization around integrated project delivery platforms, which supports subscription and services pull-through across multi-year programs.

- June 2024: Hexagon acquired Voyansi, an AECO provider of BIM and VDC solutions, to expand its BIM solutions portfolio within Hexagon Geosystems. The acquisition broadens Hexagons software footprint around model-based delivery and complements reality-capture-driven workflows used to convert field conditions into usable BIM data.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe building information modelling market is the revenue generated from BIM software and related services that enable digital planning, design coordination, and construction lifecycle collaboration for built assets across Europe.

Scope exclusions: This sizing excludes general CAD tools that are not used for BIM workflows, as well as pure hardware-only sales such as workstations, scanners, and non-BIM sensors.

Segmentation Overview

- By Solution Type

- Software

- Services

- By Deployment Type

- On-premise

- Cloud

- By Application

- Commercial

- Residential

- Industrial

- Infrastructure

- By End-user

- Architects and Designers

- General Contractors

- Specialty Sub-contractors

- Facility Owners and Operators

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Nordics (Denmark, Sweden, Norway, Finland)

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set a reliable base, before any model assumptions were locked. We reviewed public construction output and investment signals across Europe, along with digital construction policy cues that influence adoption timing.

Key public sources used for inputs and checks included items such as Eurostat construction statistics, European Commission publications on digitalization and public procurement, national building regulation portals (where BIM mandates are published), buildingSMART and CEN materials on standards, and peer reviewed papers on BIM adoption and productivity impacts. We also cross-checked company filings, investor presentations, and reputable press for pricing direction, product mix, and services attach trends. Select paid subscriptions were used only to speed up company financials tracking, patent landscaping, and news screening. These examples are not exhaustive and many other public documents and datasets were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating adoption, pricing, and buying patterns in key European markets, and then confirming how BIM spend splits between software licenses, subscriptions, and services. We spoke with a mix of software and services providers, implementation partners, AEC users, and project stakeholders so assumptions could be corrected where desk signals were incomplete, followed by triangulation of the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 18% | |

| Mid tier: 46% | Functional/Unit leaders: 26% | |

| Smaller Players: 19% | Managers: 56% |

Market-Sizing & Forecasting

The market was first reconstructed using a top-down approach where construction activity indicators and BIM adoption signals were translated into an addressable spend pool across major European countries. Once that structure was in place, selective bottom-up checks were used to keep the totals realistic, such as supplier revenue splits where disclosed, sampled license and subscription pricing, and channel feedback on implementation and training spend.

Inputs used in the model included (as illustrative examples) construction output trends, infrastructure project pipeline signals, public sector BIM mandate coverage, cloud subscription penetration, average contract size patterns for implementation services, and renewal behavior for ongoing software seats. Where bottom-up checks had gaps (for example, private companies with limited disclosure), we used peer benchmarks and interview ranges, and then tested the sensitivity before finalizing.

For the forecast, scenario analysis was applied around mandate enforcement timelines, public infrastructure funding cycles, and cloud migration speed, and then the chosen path was aligned to expert consensus from interviews. The approach keeps the steps repeatable so updates can be made quickly when new policy or construction cycle data becomes available.

Data Validation & Update Cycle

Validation was done by comparing model outputs against independent signals such as construction spending direction, vendor reported regional momentum, and changes in procurement language tied to BIM requirements. If a country-level estimate moved outside expected ranges, the drivers were rechecked and, when needed, the related assumption was recalculated and confirmed again through follow-up outreach.

Before sign-off, the work passes through multi-step analyst review so calculation errors, unit mismatches, and currency timing issues are caught early. The report is refreshed annually, and interim updates are made when material events occur, such as major mandate changes or sharp construction cycle swings. Right before delivery, we do a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Europe Building Information Modelling Market Size Measured Against Other Published Estimates

Different published BIM market values do not always line up because the scope lines are not consistent and the pricing logic is handled differently. We also see gaps coming from the base year chosen, the set of countries counted as Europe, and how fast cloud subscriptions and services are assumed to expand.

Hardware like 3D scanners and site sensors is a common add-on in some estimates, but it sits outside Mordor Intelligence's scope for this Europe building information modelling market, which keeps the size tied to BIM software plus related services spending. Some external figures also apply aggressive subscription price uplift or assume uniform mandate-driven adoption across countries, even where procurement readiness differs, and this tends to widen the total quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.17 B (2025) | |

| Industry Publisher A | USD 6.47 B (2024) | Often reflects a broader digital construction technology basket, where adjacent hardware and wider platform spend can be blended into BIM, and the earlier base year can amplify reported scale. |

| Analytics Portal B | USD 2.44 B (2025) | Typically leans on a narrower demand pool and conservative adoption ramps, and may undercount services attach and enterprise subscription expansion in larger Western European markets. |

The comparison shows that the spread mainly comes from what is counted as BIM spend and how quickly subscription and services revenue is allowed to grow. By keeping inclusions traceable to software and services, and then pressure-testing adoption and pricing assumptions with country-level checks, the final value is easier to reconcile and repeat year to year.

Key Questions Answered in the Report

How large is the Europe BIM market in 2026?

The Europe BIM market size is USD 3.57 billion in 2026, with a 12.74% CAGR projected through 2031.

Which deployment model is growing fastest in Europe?

Cloud-based BIM platforms are expanding at 13.30% CAGR, driven by regional mandates for collaborative Common Data Environments.

What is driving BIM adoption in Southern and Eastern Europe?

Accelerated digitization funding from the EU Recovery and Resilience Facility allocates capital specifically to construction technology upgrades.

Why are facility owners investing heavily in BIM?

Digital twins and regulatory demands for energy and carbon logbooks push owners to maintain detailed lifecycle BIM records for predictive maintenance and compliance.

Which country shows the highest BIM growth rate?

The Netherlands leads with a 13.70% CAGR outlook thanks to circular economy mandates and mandatory digital building passports.

Page last updated on: