Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

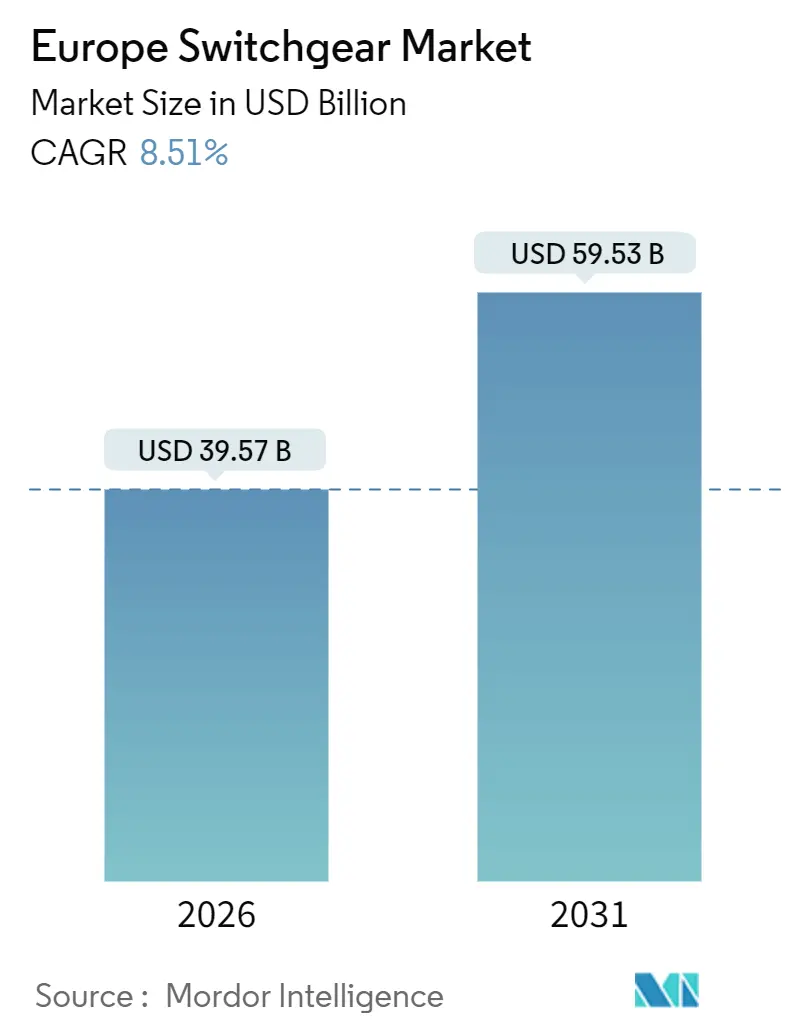

| Market Size (2026) | USD 39.57 Billion |

| Market Size (2031) | USD 59.53 Billion |

| Growth Rate (2026 - 2031) | 8.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Switchgear Market Analysis by Mordor Intelligence

The Europe switchgear market size reached USD 39.57 billion in 2026 and is projected to climb to USD 59.53 billion by 2031, advancing at an 8.51% CAGR. Continued policy pressure to replace SF₆-filled equipment, fast-tracking of renewable interconnections, and the embedding of IoT sensors inside medium- and high-voltage assemblies are the dominant growth catalysts. Investment momentum is reinforced by the European Commission’s REPowerEU schedule, which compresses grid connection lead times and accelerates the procurement of compact gas-insulated units for offshore wind platforms. Data-center build-outs across Ireland, the Netherlands, and Germany are simultaneously lifting demand for redundant N+1 switchgear architectures that guarantee 99.999% uptime. Meanwhile, utilities are piloting switchgear-as-a-service contracts to convert capital outlay into predictable operating fees, creating a parallel revenue stream for manufacturers.

Key Report Takeaways

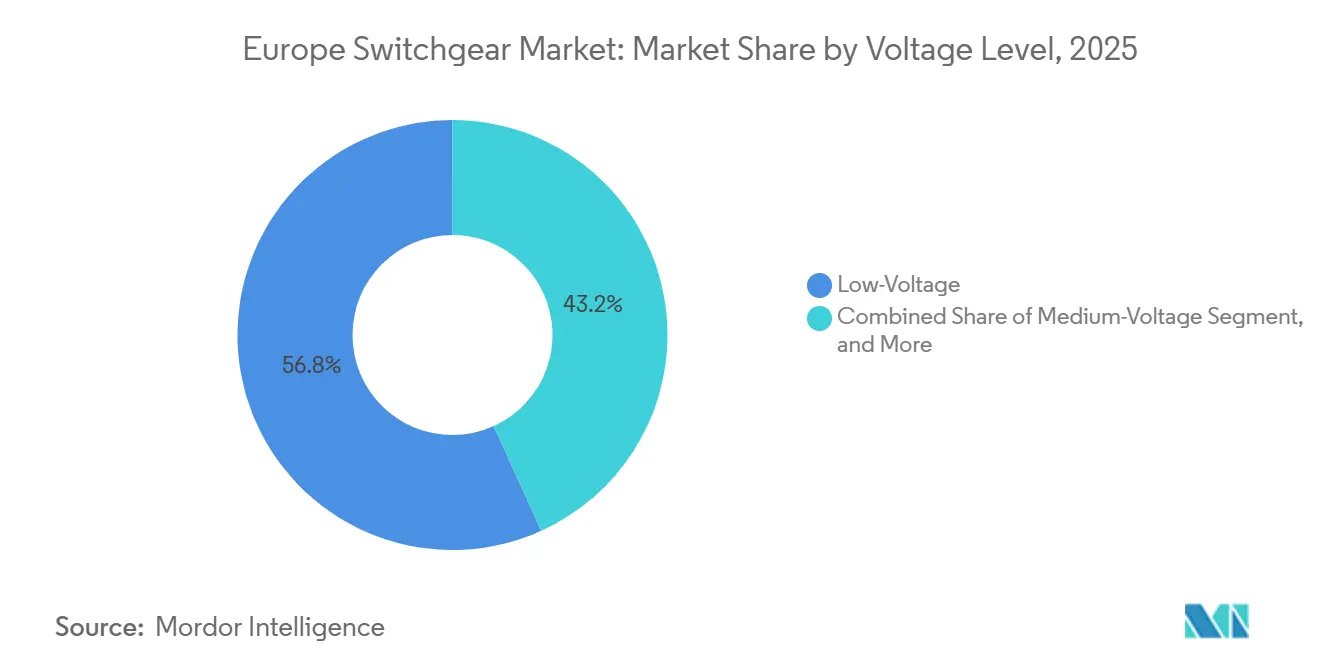

- By voltage level, low-voltage equipment accounted for 56.78% of 2025 revenue, while medium-voltage equipment is poised to expand at a 9.11% CAGR through 2031.

- By insulation type, air-insulated gear accounted for 42.39% of the Europe switchgear market share in 2025, but gas-insulated variants are forecast to grow at a 9.57% CAGR.

- By installation, indoor systems accounted for 63.91% of deployments in 2025, whereas outdoor assemblies are projected to grow at an 8.92% CAGR.

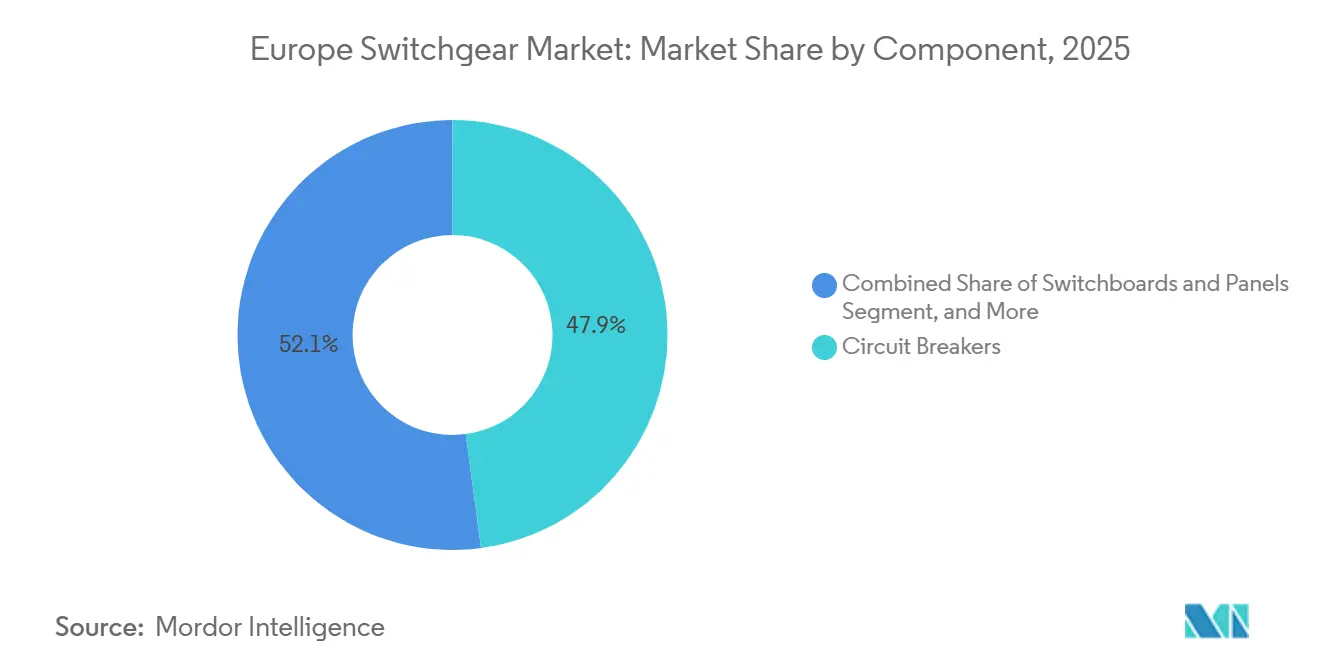

- By component, circuit breakers accounted for 47.88% of 2025 revenue, yet switchboards and panels posted the fastest 9.34% CAGR.

- By end-user, utilities led with a 36.21% share in 2025; transportation and infrastructure is the fastest-rising segment at a 9.51% CAGR.

- By geography, Germany contributed 29.19% of the 2025 value, while the United Kingdom is slated for a 9.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Edge Digitalization Push | +1.8% | Germany, United Kingdom, France, Nordic countries | Medium term (2-4 years) |

| Fast-Track Renewable Grid Connections | +2.1% | Germany, Spain, United Kingdom, Denmark | Short term (≤ 2 years) |

| Surge in Data-Center Switchgear Demand | +1.5% | Ireland, Netherlands, Germany, France | Short term (≤ 2 years) |

| Accelerated Rail Electrification Projects | +1.3% | France, Italy, Spain, Poland | Medium term (2-4 years) |

| SF₆-Free Technology Mandates | +1.6% | European Union-wide, early adoption in Germany and Nordics | Long term (≥ 4 years) |

| Rise of Micro-Utility Community Grids | +0.8% | Germany, Netherlands, Belgium, Austria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Edge Digitalization Push

Real-time monitoring modules embedded in switchgear allow utilities to detect partial-discharge spikes and temperature anomalies before a fault escalates, cutting outage duration by as much as 40%.[1]Siemens AG, “Annual Report 2025,” siemens.com National Grid ESO has required IEC 61850-compliant panels for every new connection above 11 kV since 2025, accelerating retrofit demand in aging U.K. substations. The convergence of edge computing with breaker intelligence enables dynamic load balancing without operator intervention, easing congestion at urban feeders. Cyber-security standards under the NIS-2 Directive, however, lengthen procurement by an extra 12-18 months because penetration tests and secure firmware protocols must be demonstrated before commissioning.

Fast-Track Renewable Grid Connections

The European Commission’s REPowerEU plan targets 320 GW of new solar and wind capacity by 2030, forcing network operators to halve grid connection lead times.[2]Ministry for Ecological Transition and Demographic Challenge, “Renewable Energy Approvals 2025,” miteco.gob.es Spain approved 15 GW of projects in 2025 and specifies medium-voltage switchgear with fault-ride-through logic to handle intermittent output. Germany booked a 31% rise in coastal gas-insulated orders to serve 8.2 GW of offshore wind awaiting hookup. Denmark’s Energinet invested EUR 1.2 billion (USD 1.28 billion) in 2025 to upgrade transmission gear with vacuum interrupters that eliminate SF₆ use. Integrated reactive-power compensation built into modern panels lifts unit cost 15-20%, but it avoids separate capacitor banks, trimming project footprints.

Surge in Data-Center Switchgear Demand

Hyperscale builds added 1.8 GW of IT load across Europe in 2025, with Ireland, the Netherlands, and Germany accounting for 62% of capacity.[3]European Data Centre Association, “European Data Centre Market Report 2026,” eudca.org Schneider Electric saw European data-center orders jump 28% in 2025, particularly for compact gas-insulated lines that fit tight server-hall footprints. Liquid-cooled racks are raising inrush currents sixfold, compelling operators to specify higher short-circuit ratings. AWS pledged EUR 7.8 billion (USD 8.3 billion) to expand its regional footprint and mandates IEC 62271-certified equipment with 99.999% uptime guarantees. Persistent 40- to 52-week lead times for gas-insulated units are nudging some developers toward modular air-insulated designs that ship in 24 weeks at the expense of larger footprints.

SF₆-Free Technology Mandates

The 2025 F-gas revision bans most new SF₆-filled switchgear above 24 kV, driving a 34% jump in European vacuum-interrupter orders at ABB. Eaton’s solid-dielectric line, launched in March 2025, replaces both SF₆ and vacuum chambers, appealing to urban sites with limited maintenance access. The newly published IEC 62271-203 benchmarks accelerate type tests and cut certification costs by up to 22%. Vacuum assemblies cost 25-30% more than legacy gas units at 36 kV, straining budgets in Southern and Eastern Europe. Clean-air switchgear using fluoronitrile-CO₂ blends balances cost and performance, with Siemens pilots in Italy and Spain showing dielectric strengths within 5% of those of SF₆ units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex versus Opex Savings Debate | -1.2% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Lengthy Type-Testing Lead Times | -0.9% | European Union-wide, acute in Germany and France | Medium term (2-4 years) |

| Raw-Material Price Volatility | -1.4% | European Union-wide, supply-chain exposure in Germany, Italy, Poland | Short term (≤ 2 years) |

| Cyber-Security Compliance Burden | -0.7% | Germany, France, Netherlands, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex versus Opex Savings Debate

Digitalized, SF₆-free panels cost 30-45% more upfront than legacy alternatives, leading Terna to retrofit only 12% of planned distribution substations in its 2025 budget. Iberdrola procurement committees now insist on five-year payback thresholds that many vacuum units cannot satisfy without factoring carbon-credit gains. Pilot switchgear-as-a-service contracts in the United Kingdom convert capex to opex, but regulators are undecided on whether leased assets earn a rate-based return, delaying widespread adoption. Utilities in Greece and Poland continue to favor cheaper SF₆ designs, slowing overall replacement velocity. As incentive schemes expand, however, performance-based contracts could bridge the value-perception gap.

Lengthy Type-Testing Lead Times

Copper traded between USD 8,200 and USD 10,400 per metric ton in 2025, while aluminum traded between USD 2,300 and USD 2,850, swelling medium-voltage production costs by up to 35%. Schneider Electric raised list prices by 6-8% in October 2025 to offset 180 basis points of margin erosion. Small regional suppliers lack hedging muscle and face cash-flow strain, prompting acquisitions by Tier-1 players securing raw-material pipelines. Steel enclosure prices rose 14% after carbon-border tariffs, adding EUR 800-1,200 (USD 850-1,280) per panel. Persistent volatility encourages design shifts toward aluminum-bus or composite-bus layouts, reducing copper mass by 20-25%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage Level: Medium-Voltage Gains on Industrial Electrification

Medium-voltage assemblies are tracking a 9.11% CAGR, outpacing low-voltage growth, as factory electrification and data center campuses demand higher fault-clearing ratings. ABB reported a 26% jump in European medium-voltage orders from automotive and chemical plants converting to electric furnaces. High-voltage equipment continues to serve cross-border interconnections such as the North Sea Wind Power Hub, which deploys 400 kV gas-insulated bays to conserve offshore platform real estate. Regulatory clauses in Germany’s VDE-AR-N 4110 compel assets above 1 MW to install programmable protection, nudging industrial loads from low- to medium-voltage boards.

Low-voltage frameworks still dominate residential and commercial projects where plug-and-play modules slash commissioning to 48 hours. Yet electric-vehicle hubs rated at 350 kW blur the voltage boundary, prompting some operators to choose compact 24 kV panels to curb feeder voltage drop. Hybrid medium-voltage designs that mix air busbars and vacuum interrupters trim footprint by 35%, reinforcing adoption on space-restricted brownfield sites. TenneT earmarked EUR 2.1 billion (USD 2.24 billion) for 2025 for upgrades to 72.5–245 kV lines along the Dutch-German corridor, prioritizing SF₆-free equipment. The Europe switchgear market, therefore, sees voltage-level convergence, where application rather than nominal voltage dictates equipment choice.

By Insulation Type: Gas-Insulated Captures Urban and Offshore Niches

Air-insulated gear maintained a 42.39% share in 2025 on cost advantage and ease of servicing, but gas-insulated alternatives are growing at a 9.57% CAGR because their compact footprints address premium land costs in London, Paris, and Frankfurt. Schneider Electric logged a 31% leap in gas-insulated data-center orders after launching fluoronitrile-CO₂ mixtures with a global warming potential below 1. Vacuum-insulated varieties respond directly to SF₆ bans, with German utilities replacing 1,200 panels under a federal subsidy covering 40% of incremental expense. Solid-dielectric technology, though 15-20% pricier, is more resistant to humidity and pollution on Mediterranean coasts and is therefore favored in Sicily and Cyprus.

Hybrid configurations pairing air busbars with gas breakers now account for roughly 9% of new procurements, balancing cost and density. Hitachi Energy’s 2025 hybrid launch shrank enclosure volume by half, targeting retrofits beneath city-center plazas where excavation permits are scarce. In rural Spain, utilities still prefer air-insulated bays for solar farms where land is abundant, and salt spray is minimal. The Europe switchgear market consequently maintains a mixed insulation portfolio, reflecting divergent spatial and regulatory pressures.

By Installation Type: Outdoor Gear Rides Renewable Expansion

Outdoor assemblies are expected to grow at an 8.92% CAGR, supported by wind and solar sites in remote or coastal terrain. United Kingdom offshore developers ordered 29% more outdoor 66 kV gas-insulated panels in 2025 to lighten turbine-platform loads. Natural ventilation reduces cooling costs by up to 25%, yet IP65 coatings and UV-resistant gaskets increase initial pricing. France’s RTE spent EUR 890 million (USD 950 million) on 47 outdoor substations engineered with surge arresters to counter lightning risk.

Indoor systems still account for 63.91% of volumes because urban density and fire codes demand enclosed solutions. Eaton’s 2025 arc-resistant indoor design vents pressure and limits incident energy by 85%, improving safety in hospitals and airports. Polymer-insulated busbars are shrinking indoor footprints by 30%, widening applicability to retrofits beneath office towers. Germany and the Netherlands, with substation densities above 12 units per 100 km², remain the strongholds of the Europe switchgear market.

By Component: Switchboards and Panels Lead Modular Shift

Switchboards and panels are forecast to grow at a 9.34% CAGR as modular architectures ease factory acceptance testing and enable field reconfiguration without downtime. Siemens recorded a 19% increase in European switchboard bookings after customers migrated from fixed to withdrawable designs, which expedited breaker swaps. Prefabricated skids now shorten on-site installation time from 2 months to under 3 weeks, cutting labor and lost-production costs.

Circuit breakers, still accounting for 47.88% of 2025 revenue, are evolving toward electronic trip units with Bluetooth diagnostics that feed building-management dashboards. Contactors and relays gain relevance in vehicle-charging depots where fast-cycling duty profiles prevail, while fuse switches retain cost appeal in apartments below 100 A. Legrand’s modular platform captured 62% of new panel bids in 2025, confirming a lasting tilt toward plug-and-play assemblies. The modular trend keeps the Europe switchgear market in rapid-deployment mode, favoring suppliers with flexible manufacturing lines.

By End-User: Transportation Electrification Accelerates Demand

Transportation and infrastructure applications will grow at a 9.51% CAGR as high-speed rail and metro extensions proliferate. SNCF budgeted EUR 4.2 billion (USD 4.48 billion) to electrify 1,800 km of regional rail, specifying 25 kV vacuum gear with pantograph protection. Spain’s Adif awarded contracts for 320 traction substations along the Madrid-Galicia corridor, mandating SF₆-free 36 kV units for environmental compliance.

Utilities remain the largest buyers at 36.21% share, but stretched capex forces prioritization of transmission-level upgrades over distribution replacements. Industrial plants are pursuing predictive maintenance to avert costly outages, investing EUR 1.6 billion (USD 1.71 billion) in German chemical complexes in 2025. Commercial buildings must meet near-zero-emission standards, hence specify switchgear with embedded energy meters. Residential uptake follows heat-pump adoption, up 34% in 2025, necessitating uprated service equipment. Performance-based contracts piloted by National Grid illustrate how service models can reshape the procurement landscape for the Europe switchgear market.

Geography Analysis

Germany accounted for 29.19% of the Europe switchgear market in 2025, backed by its industrial base and expanding offshore wind corridors. The Federal Network Agency approved EUR 3.8 billion (USD 4.05 billion) for 2026 transmission upgrades, 42% of which targets switchgear replacements along the North-South spine. Digital-ready panels installed by Enedis in France’s urban grids reduced outage response by 35%, illustrating tangible operational gains.

The United Kingdom will pace growth at a 9.77% CAGR through 2031, propelled by its offshore wind build-out and the requirement for smart-ready switchgear for any connection above 11 kV. Italy earmarked EUR 1.1 billion (USD 1.17 billion) for medium-voltage refresh in Sicily and Sardinia in 2025, while Spain’s 12 GW renewable surge mandates IP54 outdoor enclosures to withstand dust and heat. Nordic utilities have already replaced 840 SF₆ units through voluntary programs, accelerating the migration to vacuum and clean-air solutions.

Central and Eastern European nations such as Poland, the Czech Republic, and Romania are retiring coal plants, requiring bidirectional switchgear to accommodate distributed solar exports.

Competitive Landscape

The market shows moderate concentration: ABB, Siemens, and Schneider Electric together hold roughly half of regional revenue. By end-2025, ABB’s Ability platform linked 14,000 live panels, providing customers with six- to nine-month failure forecasts. Siemens deepened vertical integration by acquiring a German sensor firm in October 2025, guaranteeing the supply of embedded partial-discharge monitors. Schneider Electric pilots switchgear-as-a-service deals, shifting revenue toward annuity streams and boosting retention in the Europe switchgear market.

Regional specialists such as Ormazabal and Lucy Electric win on localized assembly and sub-40-week delivery schedules, expanding share in Spain, Portugal, and the United Kingdom. CG Power exploits lower Indian production costs to price 18-22% below Western competitors, though service coverage remains thin. Eaton entered the SF₆-free retrofit niche with modular vacuum inserts compatible with legacy frames, tapping utilities unwilling to replace entire panels.

Innovation intensity is rising: Hitachi Energy now embeds AI algorithms that optimize breaker timing, cutting switching losses by 12-15%. Rockwell Automation targets industrial end-users with gear natively integrated into FactoryTalk analytics, enabling plant-wide predictive maintenance. Patent activity jumped 27% in 2025, spotlighting polymer-insulated busbar technology from Mitsubishi Electric that reduces partial-discharge risk by 40%.

Europe Switchgear Industry Leaders

ABB Ltd.

Honeywell International Inc.

Rockwell Automation Inc.

Schneider Electric SE

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Siemens announced a EUR 180 million (USD 192 million) expansion of its Erlangen plant to scale SF₆-free medium-voltage production.

- November 2025: ABB landed a USD 240 million contract with TenneT for 420 kV fluoronitrile-CO₂ gas-insulated bays across 18 North Sea substations.

- October 2025: Schneider Electric rolled out EcoStruxure Switchgear Advisor, a cloud analytics suite that cut pilot-phase outages by 28%.

- September 2025: Eaton opened a EUR 95 million (USD 101 million) vacuum-interrupter assembly site in Kraków with 12,000-panel annual capacity.

Europe Switchgear Market Report Scope

The Europe Switchgear Market Report is Segmented by Voltage Level (Low-Voltage, Medium-Voltage, High-Voltage), Insulation Type (Air-Insulated, Gas-Insulated, Vacuum-Insulated, Solid-Insulated, Hybrid), Installation Type (Indoor, and Outdoor), Component (Circuit Breakers, Contactors and Relays, Fuse Switches, Switchboards and Panels), End-User (Utilities, Industrial, Commercial Buildings, Residential, Transportation and Infrastructure), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Voltage Level

| Low-Voltage |

| Medium-Voltage |

| High-Voltage |

By Insulation Type

| Air-Insulated |

| Gas-Insulated |

| Vacuum-Insulated |

| Solid-Insulated |

| Hybrid |

By Installation Type

| Indoor |

| Outdoor |

By Component

| Circuit Breakers |

| Contactors and Relays |

| Fuse Switches |

| Switchboards and Panels |

By End-User

| Utilities |

| Industrial |

| Commercial Buildings |

| Residential |

| Transportation and Infrastructure |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Voltage Level | Low-Voltage |

| Medium-Voltage | |

| High-Voltage | |

| By Insulation Type | Air-Insulated |

| Gas-Insulated | |

| Vacuum-Insulated | |

| Solid-Insulated | |

| Hybrid | |

| By Installation Type | Indoor |

| Outdoor | |

| By Component | Circuit Breakers |

| Contactors and Relays | |

| Fuse Switches | |

| Switchboards and Panels | |

| By End-User | Utilities |

| Industrial | |

| Commercial Buildings | |

| Residential | |

| Transportation and Infrastructure | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe switchgear market by 2031?

The market is expected to reach USD 59.53 billion by 2031.

Which insulation technology is growing fastest in Europe?

Gas-insulated switchgear is forecast to expand at a 9.57% CAGR as urban and offshore installations seek compact, fire-safe solutions.

Why are utilities piloting switchgear-as-a-service contracts?

These contracts shift large upfront purchases to monthly operating fees, improving cash flow while guaranteeing performance and maintenance.

How do SF₆-free mandates affect equipment selection?

The 2025 F-gas rules virtually ban new SF₆ units above 24 kV, pushing utilities toward vacuum, solid-dielectric, or clean-air alternatives despite higher capex.

Which country is likely to post the fastest growth in switchgear demand?

The United Kingdom is projected to advance at a 9.77% CAGR through 2031, driven by offshore wind interconnections and smart-grid retrofits.

What material prices most influence switchgear costs?

Copper and aluminum together account for up to 35% of medium-voltage unit costs, and price swings have forced suppliers to raise list prices and redesign busbars.

Page last updated on: