Europe Kitchen Hobs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.30 Billion |

| Market Size (2026) | USD 6.5 Billion |

| Market Size (2031) | USD 7.70 Billion |

| Growth Rate (2026 - 2031) | 3.57% CAGR |

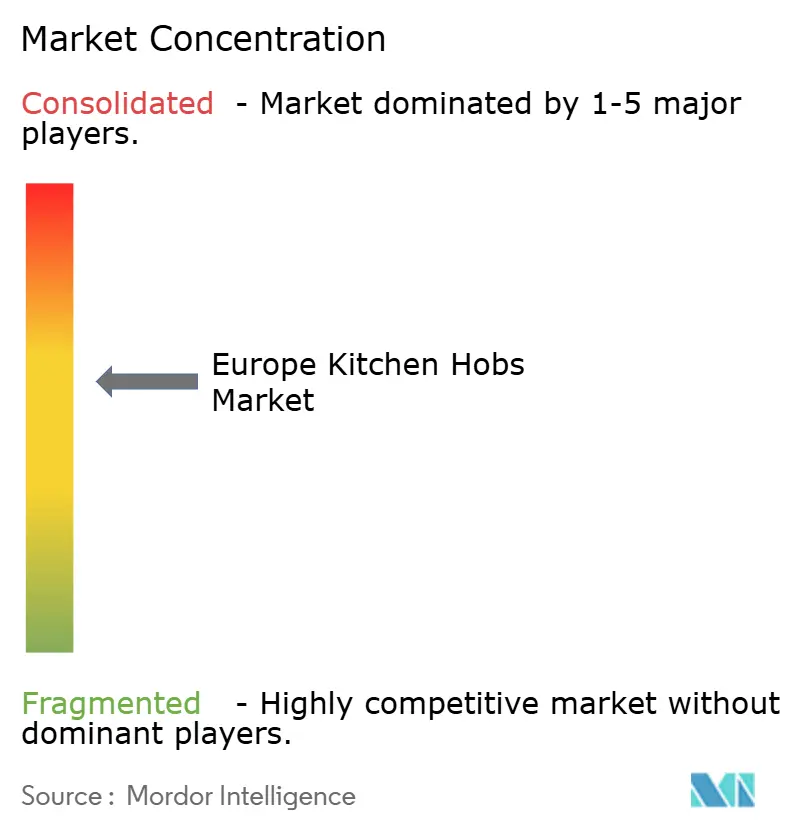

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Kitchen Hobs Market Analysis by Mordor Intelligence

The Europe kitchen hobs market size is projected to expand from USD 6.30 billion in 2025 and USD 6.5 billion in 2026 to USD 7.70 billion by 2031, registering a CAGR of 3.57% between 2026 and 2031. Energy-transition policies that penalize residential gas use, rapid consumer pivot toward high-efficiency induction technology, and widespread kitchen remodeling activity underpin the growth trajectory of the European Kitchen Hobs market. Competitive positioning remains concentrated, with the top five manufacturers capturing 60% of revenue, yet innovation cycles in smart connectivity and downdraft extraction create fresh white-space opportunities. Regional demand continues to diverge: Germany commands the largest revenue pool, while Spain advances the fastest on the back of accelerated renovation programs. At the same time, the European kitchen Hobs market is benefiting from a structural digital shift, as online channels outpace traditional stores in year-on-year growth, especially for premium built-in formats. Policy decarbonization momentum is cemented by the European Commission’s REPowerEU roadmap, which obliges Member States to file national gas-phase-out plans by end-2025 and materially lifts electric-cooking demand.

Key Report Takeaways

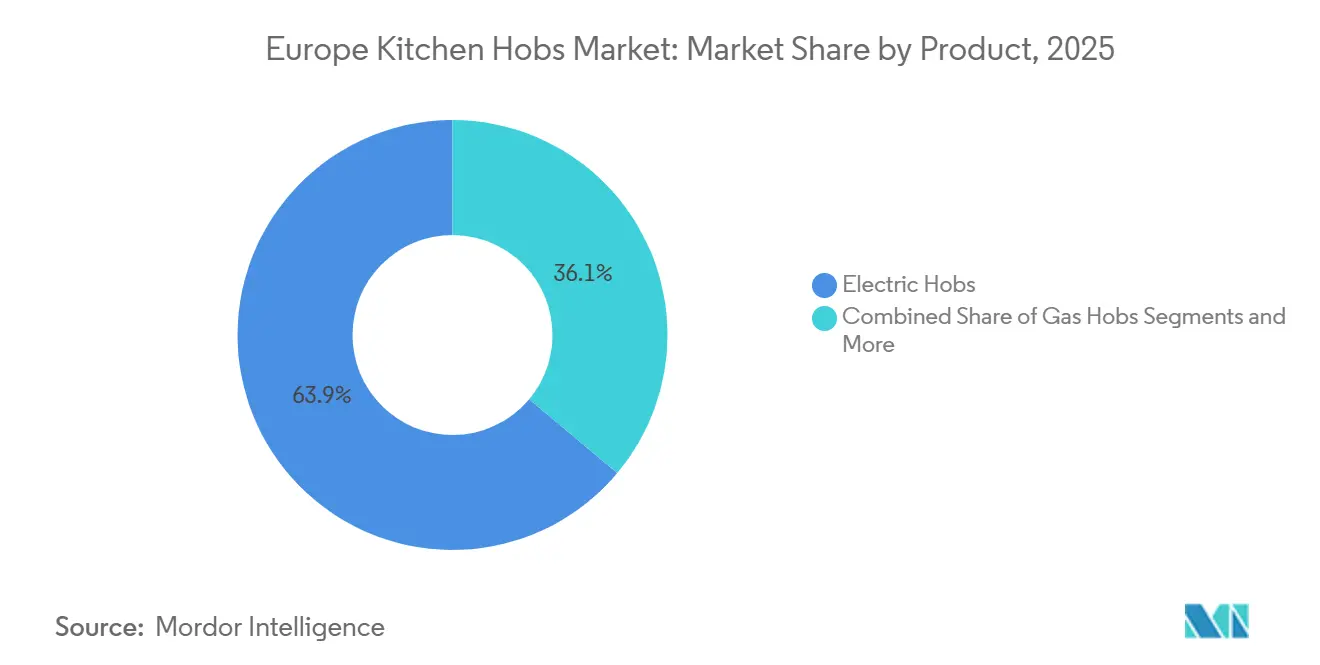

- By product, electric hobs led with 63.9% of the European kitchen hobs market share in 2025 and are projected to post a 4.40% CAGR through 2031.

- By installation type, built-in hobs captured 75% of the European kitchen hobs market share in 2025 and are set to grow at a 4.02% CAGR through 2031.

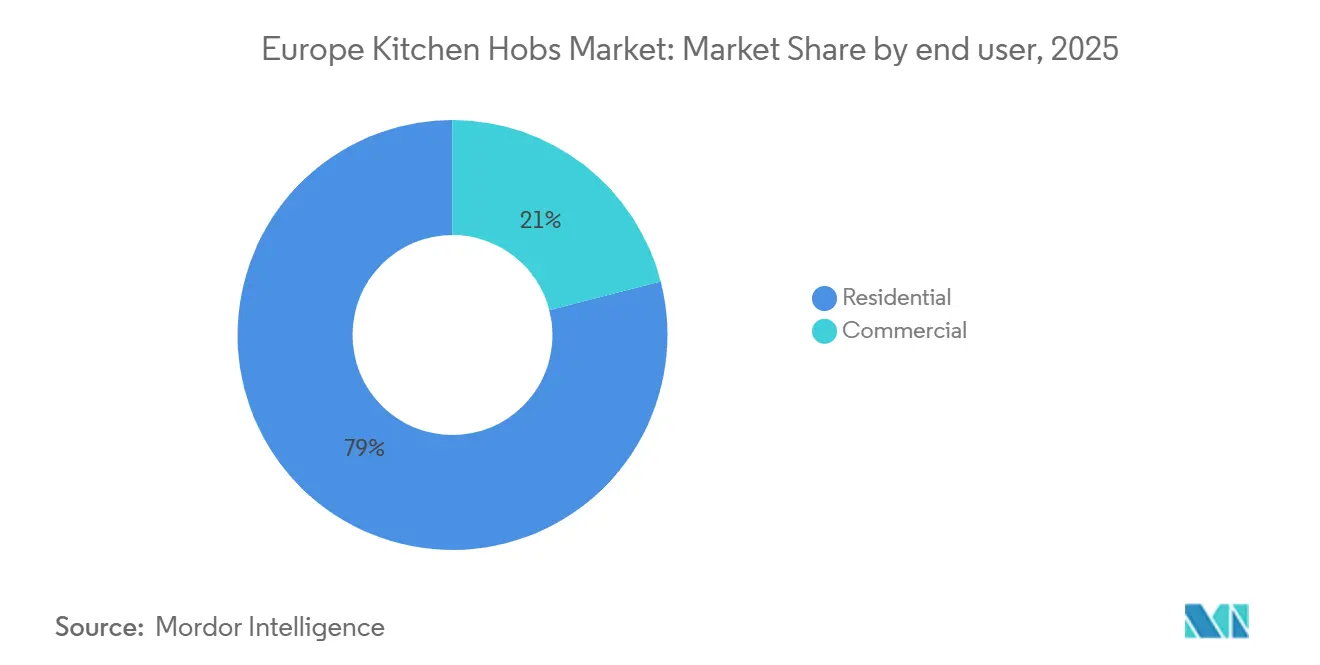

- By end user, residential accounted for 79% of the Europe kitchen hobs market size in 2025, and is forecast to expand at a 3.89% CAGR to 2031.

- By distribution channel, B2C/retail accounted for 82.3% of the European kitchen hobs market size in 2025, whereas online stores are forecast to expand at a 6.54% CAGR to 2031.

- By geography, Germany represented 22.6% of the European kitchen hobs market size in 2025, while Spain is advancing at a 5.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Kitchen Hobs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-wide incentives phasing-out gas cookers | +1.2% | Netherlands, France, Germany | Medium term (2-4 years) |

| Rapid adoption of energy-efficient induction | +0.8% | Pan-European with Nordic leadership | Short term (≤ 2 years) |

| Kitchen premiumization & design renovations | +0.6% | Germany, UK, BENELUX | Long term (≥ 4 years) |

| Surge in smart/connected built-in appliances | +0.5% | Urban centers across major EU markets | Medium term (2-4 years) |

| Online pure-play retailers expanding big-ticket sales | +0.4% | Europe-wide, led by UK & DACH region | Short to Medium term (1–3 years) |

| Corporate decarbonisation of food-service kitchens | +0.7% | Western Europe, especially France & Germany | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

EU-wide Incentives Phasing-out Gas Cookers

Member-state subsidy schemes are accelerating the transition from gas to electric cooking, exemplified by the Netherlands’ nationwide gas-boiler ban effective 2026 and France’s electrification credits embedded in its recovery plan[1]European Commission, “Roadmap Towards Ending Russian Energy Imports,” europa.eu. . Retail momentum mirrors policy action; IKEA Netherlands has fully delisted gas cooktops, underscoring retailer alignment with the energy transition. The European Commission now requires each country to submit detailed gas-phase-out strategies by December 2025, creating clear demand visibility for induction technology. Commercial kitchens are also adjusting procurement plans as corporate decarbonization targets tighten, bringing hospitality venues into the electric-cooking fold. The codified policy framework effectively enlarges the addressable base for the Europe Kitchen Hobs market, sharply tilting product-development roadmaps toward induction and downdraft electric solutions. Manufacturers leveraging EU energy-efficiency labelling to market sub-1 kWh boil-time performance are recording the strongest order backlogs.

Rapid Adoption of Energy-efficient Induction Hobs

Efficiency advantages remain the single most persuasive factor behind household migration to induction: laboratory testing shows 90% energy transfer versus 40-50% for gas. Time-to-boil trials further cement consumer perception, with induction heating 1 liter of water in 4.81 minutes compared with 9.69 minutes on gas, a differential that gains salience as electricity tariffs adopt dynamic pricing. Indoor air-quality advocacy groups have heightened scrutiny of nitrogen dioxide emissions from gas burners, a link quantified in a 2024 study estimating 40,000 premature European deaths annually[2]Guardian Staff, “Gas Stoves Linked to 40,000 Deaths in Europe Annually,” theguardian.com. . Younger, sustainability-minded demographics amplify the trend by favouring app-controlled cooktops compatible with smart-home platforms such as Bosch Home Connect and Samsung SmartThings. Nordic countries serve as the bellwether, achieving double-digit induction penetration because plentiful renewable electricity sharpens the carbon advantage. The cascading effect narrows SKU rationalization around gas and ceramic lines for several OEMs, pushing R&D budgets decisively into induction coil efficiency and power-sharing algorithms.

Kitchen Premiumization & Design-led Renovations

Post-pandemic lifestyle shifts have embedded the kitchen as the social nucleus of European homes, triggering an upswing in aesthetic-driven renovations. Flush-mount induction units such as Miele’s KMDA 7876 FL, retailing at GBP 2,929 (USD 3,660), illustrate consumer readiness to pay for integrated ventilation and frameless glass. BORA’s X Pure 2 downdraft system applies matte-black finishes and Bluetooth connectivity to create functional showpieces. Culinary content on social media further blurs the line between appliance utility and interior décor, accelerating demand for shadow-line installation and handle-less cabinetry. Builders report that built-in hobs are specified in 8 out of 10 new premium kitchens, reinforcing the Europe Kitchen Hobs market’s tilt toward integrated formats. Renovation grants under EU green-building programs sweeten upgrade economics by subsidizing high-efficiency appliances. Premiumization also dovetails with durability mandates under the 2024 Ecodesign Regulation, pushing brands to highlight recyclability along with quiet-operation ratings that resonate in open-plan spaces.

Surge in Smart/connected Built-in Appliances

Smart penetration across European households has reached 23% and is compounding at close to 14% annually, embedding connectivity as a standard purchase criterion. AEG’s AI-assisted hob, introduced at IFA 2024, employs machine-learning algorithms to calibrate temperature in real time, reducing risk of burnt pans and food wastage. Siemens’ Intelligent Kitchen Series performs automatic pan-recognition to propose cooking presets, a feature that dovetails with voice assistants for hands-free operation. Samsung’s SmartThings Energy extends functionality by orchestrating demand-response signals, allowing hobs to throttle power during high-tariff windows. IoT add-ons like recipe libraries and remote diagnostics elevate post-purchase engagement and brand loyalty, creating ancillary revenue from firmware subscriptions. Premium buyers associate connected features with futureproofing, thereby propelling ASPs higher and expanding margins within the Europe Kitchen Hobs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost vs. legacy gas/ceramic units | -0.7% | Price-sensitive markets across Eastern Europe | Short term (≤ 2 years) |

| Cookware-compatibility limitations for induction | -0.4% | Traditional cooking regions in Southern Europe | Medium term (2-4 years) |

| Installer & electrical-panel upgrade bottlenecks | -0.5% | Older housing stock across Southern & Eastern Europe | Medium term (2–4 years) |

| Stricter EU repairability rules lifting compliance cost | -0.6% | EU-27, especially affecting mid-market manufacturers | Medium to Long term (2–5 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost vs. Legacy Gas/Ceramic Units

Induction models still retail at price points 50-70% above gas alternatives, a delta that constrains adoption among households with limited disposable income in Eastern Europe. Retrofitting costs add complexity; panel upgrades from 3 kW to 6 kW can reach EUR 800 (USD 875) in older apartments. While lifecycle analyses show energy savings offsetting the premium within five years, cash-constrained buyers remain unconvinced even after rebate schemes in Germany and France. Manufacturers are experimenting with entry-level lines that sacrifice ancillary features like Wi-Fi to shave USD 108 (EUR 100) off retail tickets, but scale economics have yet to neutralize the gap fully. Retailers are softening the blow through 0% APR financing, and some utilities bundle appliance loans into electricity contracts. The price barrier is likely to moderate as high-volume coil production in Poland and Turkey drives cost deflation.

Cookware-compatibility Limitations for Induction

Induction requires ferromagnetic cookware, rendering legacy aluminium and copper pots unusable, a factor that dissuades many Southern European consumers who cherish heirloom cookware. Surveys in Italy reveal that 44% of households would need to replace half their pans to switch to induction[3] NYSERDA, “Der Kaufratgeber für Induktionskochfelder,” nyserda.ny.gov. . Cookware replacement pushes the effective conversion cost even higher, sometimes eclipsing the hob itself. Manufacturers are mitigating friction via promotional bundles: BSH offers a three-piece steel set with select Bosch models, while Ikea integrates compatible pans into kitchen packages. Cookware brands are reacting by embedding magnetic stainless-steel bases into traditional copper lines, but adoption remains gradual. Education campaigns emphasizing the “magnet test” are steadily improving awareness, and younger homebuyers, less attached to existing cookware, are adopting induction more readily.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Electric Technology Drives Market Evolution

Electric hobs secured 63.9% revenue in 2025 and are expanding at a 4.40% CAGR, the highest rate among product types in the European kitchen hobs market. Gas hobs hold 29.4% share but are retreating as regulatory pressures mount and consumers reassess indoor-air-quality risks. Ceramic variants occupy about 12.33%, serving as transitional choices for buyers wary of induction premiums yet eager to leave gas behind. Electric plate hobs persist primarily in entry-level rental stock, while niche categories such as domino modular units are benefiting from upticks in micro-apartment construction. Manufacturers are phasing out slow-selling gas SKUs, reallocating tooling to induction coil production, and doubling down on power-sharing electronics that allow several zones to draw from a single 7.4 kW circuit. Product-design language increasingly converges on frameless glass and seamless touch sliders, standardizing aesthetics across price tiers. Regulatory tailwinds bolster induction’s leadership: revised EU energy-labeling rules now deprioritize gas efficiency improvements, effectively channeling R&D into electric formats.

The segment’s performance underscores the Europe Kitchen Hobs market’s pivot from thermal combustion to magnetic energy transfer. Induction’s value proposition resonates across environmental, safety, and speed vectors, yielding higher customer-satisfaction scores in post-purchase surveys. Moreover, integration with downdraft extraction is most feasible in induction builds because the absence of open flames allows tighter proximity between the surface and the fan. Energy-monitoring features, now standard in upper-mid SKUs, push induction beyond mere cooktop status toward holistic kitchen-energy management. As manufacturing scales up, cost curves are expected to bend downward by 3-4% annually, accelerating mainstream penetration even in price-sensitive geographies.

By Installation Type: Built-in Solutions Dominate Premium Segment

Built-in hobs accounted for 75% of 2025 revenue, a dominance reinforced by European consumers’ preference for seamless kitchen aesthetics and the ubiquity of wall-to-wall countertop designs. Free-standing units, with 19.10% share, remain popular only in budget renovations and landlord-owned properties where portability and low initial cost rank higher than design cohesion. The Europe Kitchen Hobs market size for built-in variants is expected to outpace the overall average, riding on premiumization and the integration of extraction within the hob surface.

The installation type segmentation demonstrates how open-plan living catalyzes appliance evolution: downdraft hobs like Elica’s NikolaTesla combine ventilation and cooking to preserve sightlines in lounge-kitchen multipurpose areas. Built-in sales also benefit from longer replacement cycles: once flush-mounted, consumers are more inclined to upgrade within the same footprint, reinforcing brand lock-in. Professional installation services have transitioned from secondary to primary revenue streams for some retailers, generating high-margin service contracts that complement hardware sales. Manufacturers have responded by designing clip-in mounts and standardized cut-out dimensions to minimize carpenter labor, significantly widening the addressable DIY demographic. In energy-retrofit projects funded under EU Green Deal packages, built-in induction hobs are often mandatory to secure subsidies, further entrenching their dominance.

By End User: Residential Segment Dominate

The residential segment of the European kitchen hobs market accounted for 79% of the market value in 2025. In 2025, the European kitchen hobs market is experiencing significant changes, particularly in the residential segment. Homeowners are increasingly seeking solutions that simplify meal preparation and enhance the kitchen's aesthetic appeal. The momentum is further bolstered by a swift pivot to energy-efficient induction hobs and is witnessing the most rapid growth. Moreover, policies promoting electrification, notably the gas phase-out, coupled with a rising consumer appetite for smart, built-in appliances, are intensifying the replacement demand in households. Consequently, with lifestyle shifts like increased home cooking and upscale kitchen renovations, residential usage stands out as the dominant growth driver.

By Distribution Channel: Digital Transformation Accelerates

B2C/retail continue to dominate with 82.3% market share, leveraging experiential showrooms where consumers can interact with working displays and receive expert guidance. Yet the online channel is compounding at 6.54% annually, reshaping how large appliances are researched, configured, and financed. COVID-era lockdowns crystallized e-commerce habits, and virtual-reality product tours now replicate showroom experiences. Pure-player websites like AO.com and manufacturer web-shops are investing in augmented-reality apps that visualize hob placement on customers’ countertops, compressing decision cycles. The other channels segment covering warehouse clubs and direct selling adopts hybrid approaches, integrating click-and-collect options that balance online selection with in-person pickup convenience.

Digital advertising platforms allow brands to micro-target by renovation stage, resulting in higher conversion rates compared with broadcast TV. Crucially, online buyers of the European kitchen hobs market often purchase higher-ASP models because comparison engines foreground energy-efficiency metrics and lifetime electricity savings. Returns, historically a friction point for e-commerce, are contained via thorough compatibility checklists and plug-type selectors. Installation services are increasingly scheduled through API integrations with local contractors, ensuring online transactions remain hassle-free. Taken together, the channel shift is realigning marketing budgets toward SEO and content partnerships while pressuring brick-and-mortar retailers to reinvent their value proposition around experiential spaces.

Geography Analysis

Germany remains the cornerstone of the Europe kitchen hobs market with 22.6% revenue share in 2025, supported by deep manufacturing expertise and a consumer base that values engineering quality . Although unit shipments now grow in low single digits, the country sets design trends that radiate across the continent, such as flush-mounted induction with downdraft extraction. Local building codes favor energy-efficient retrofits, but saturation and tightening household budgets temper volume expansion. Spain offers a contrasting dynamic, combining a catch-up renovation cycle with EU-subsidized energy-efficiency incentives to post a 5.80% CAGR, the region’s highest. Rising tourism and hospitality refurbishment further enlarges the commercial sub-segment.

France and Italy sustain sizable volumes through culinary tradition but grapple with slower regulatory impetus on gas phase-out, stretching the transition timeline. Nonetheless, younger urban professionals in Paris, Milan, and Rome opt overwhelmingly for induction, signaling an inflection point. The United Kingdom, despite import-cost pressures from currency depreciation, is witnessing robust replacement demand driven by gas-price volatility and new building-energy standards. BENELUX countries, spearheaded by the Netherlands’ early ban on new-build gas connections, have become living laboratories for integrated induction-and-ventilation solutions. Nordic markets leverage almost-fully decarbonized electricity grids to position induction as both an environmental and economic win, achieving the highest per-capita penetration across Europe.

In Eastern Europe, the Rest-of-Europe cluster confronts affordability barriers but benefits from structural EU funds aimed at housing modernization, gradually narrowing the adoption gap. Grid-capacity upgrades and falling induction ASPs are pivotal for unlocking demand. Cross-border e-commerce platforms are shortening distribution lead times, making premium induction SKUs more accessible in secondary cities. Consequently, the regional mosaic highlights how policy frameworks, electricity-generation profiles, and income levels coalesce to dictate growth trajectories within the Europe Kitchen Hobs market.

Competitive Landscape

The European kitchen Hobs market is moderately concentrated, with the top five having a significant share of the market in 2024. BSH leverages a multi-brand architecture, Bosch, Siemens, Neff, and Gaggenau, to blanket price tiers and retail channels. Miele, Electrolux (AEG), and Whirlpool hold solid mid-teens shares, each differentiating through proprietary induction features like power-slide controls or AI-based cooking guidance. Samsung and LG, although late entrants, capitalize on home-electronics ecosystems to cross-sell connected hobs within broader smart-home bundles. Arçelik’s 2025 launch of Beko Europe underscores OEM appetite for region-specific operations that accelerate sustainability compliance.

Strategic maneuvers increasingly revolve around vertical integration to secure component supply amid semiconductor shortages. BSH has invested in European coil-winding facilities, while Electrolux broadened its Czech plant to internalize inverter-board production. Brand portfolios are converging on downdraft technologies, evidenced by Siemens’ inductionAir Plus and Whirlpool’s 36-inch Induction Downdraft showcased at KBIS 2025. Disruptors like Klarstein upend pricing conventions through direct-to-consumer e-commerce, targeting design-conscious millennials with domino and portable induction units.

Collaborations with energy-software firms are multiplying; Samsung’s SmartThings Energy partners with Italian utility Enel to pilot demand-response incentives, a trend that deepens ecosystem lock-in. Sustainability narratives have evolved from recyclable packaging to scope 3 carbon accounting, compelling OEMs to publish life-cycle assessments. Competitive intensity remains highest in the premium band, where ASPs exceed USD 1296 (EUR 1,200) and features such as zoneless induction and smart-pan recognition anchor differentiation. M&A activity is selective but strategic: Haier’s 2025 acquisition of Klima KFT, though HVAC-focused, offers cross-selling synergies in built-in kitchen channels across Central Europe.

Europe Kitchen Hobs Industry Leaders

BSH Home Appliances (Bosch, Siemens, Neff, Gaggenau)

Electrolux AB (AEG, Zanussi)

Whirlpool Corporation (Whirlpool, Indesit, Hotpoint)

Miele & Cie. KG

Arçelik A.Ş. (Beko, Grundig)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Haier completed the acquisition of KLIMA KFT in Budapest to accelerate HVAC growth in Central and Eastern Europe, transferring assets and expertise to Haier Europe Appliances Holding BV as part of the company's strategy to capture infrastructure upgrades driven by EU green transition policies.

- February 2025: Whirlpool Corporation highlighted future innovation at KBIS 2025, featuring JennAir's 36-inch Induction Cooktop with Temperature-Controlled Cooking and 30/36-inch Induction Downdraft Cooktops, signaling continued investment in premium induction technology across global markets.

- January 2025: Arçelik launched Beko Europe as a resolute business unit, positioning itself as a leading provider of sustainable home appliances in Europe, emphasizing corporate commitment to environmental sustainability and regional market focus.

- September 2025: AEG unveiled an AI-assisted cooking platform at IFA 2024, incorporating machine learning algorithms for automatic temperature adjustment and recipe guidance, representing a significant advancement in smart kitchen technology integration.

Europe Kitchen Hobs Market Report Scope

A kitchen hob, unlike regular gas stoves, is equipped with robust burners and sturdy support grills that can easily accommodate heavy utensils such as pressure cookers. These hobs are specifically designed to blend seamlessly into the kitchen countertop.

The report provides a comprehensive background analysis of the European kitchen hobs market, including an assessment of emerging trends by segments and regional markets, key market players, significant changes in market dynamics, and a market overview. The European kitchen hobs market is segmented by product, distribution channel, and geography. By product, the market is segmented into ceramic hobs, induction hobs, electric plate hobs, gas hobs, and others (stainless steel, domino hobs, and gas-on-glass hobs). By distribution channel, the market is segmented into multi-brand stores, specialty stores, online stores, and other distribution channels (manufacturing retailers, warehouse clubs, discount retailers, and direct selling companies). By geography, the market is segmented into France, the United Kingdom, Germany, Italy, Spain, and the Rest of Europe. The report offers market sizes and forecasts in value (USD) for all the above segments.

| Gas Hobs | |

| Electric Hobs | Induction Hobs |

| Radiant Hobs/Radiant Cooktops | |

| Coil Cooktops | |

| Hybrid/Combination Hobs | |

| Other Products (Domino Hobs, etc.) |

| Built-in / Integrated Hobs |

| Free-standing Hobs |

| Residential |

| Commercial |

| B2C/Retail | Offline |

| B2B (directly from the manufacturers) |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Product | Gas Hobs | |

| Electric Hobs | Induction Hobs | |

| Radiant Hobs/Radiant Cooktops | ||

| Coil Cooktops | ||

| Hybrid/Combination Hobs | ||

| Other Products (Domino Hobs, etc.) | ||

| By Installation Type | Built-in / Integrated Hobs | |

| Free-standing Hobs | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Offline |

| B2B (directly from the manufacturers) | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe Kitchen Hobs market in 2026?

The Europe Kitchen Hobs market size is expected to reach USD 6.5 billion in 2026.

What is the expected CAGR for Europe-wide kitchen hob sales through 2031?

The market is projected to grow at a 3.57% CAGR during the 2026-2031 period.

Which product segment is growing the fastest?

Electric hobs are advancing at a 4.40% CAGR, the quickest among all product categories.

Why is Spain considered the fastest-rising geography?

Spain benefits from EU-funded renovation incentives, robust housing starts, and tourism-linked commercial upgrades, yielding a 6.54% CAGR.

What factor most deters consumers from adopting induction technology?

Higher upfront equipment and installation costs remain the primary hurdle, especially in price-sensitive Eastern European markets.

Page last updated on: