Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 68.48 Billion |

| Market Size (2026) | USD 71.40 Billion |

| Market Size (2031) | USD 87.97 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Kitchen Appliances Market Analysis by Mordor Intelligence

The Europe kitchen appliances market size is expected to increase from USD 68.48 billion in 2025 to USD 71.40 billion in 2026 and reach USD 87.97 billion by 2031, growing at a CAGR of 4.26% over 2026-2031. The Europe kitchen appliances market benefits from the 2025–2027 eco-design review cycle that raises the bar for reparability and standby consumption, which in turn shapes product roadmaps and accelerates upgrade cycles. Strategic investments in AI-enabled ovens, ultra-low standby architectures, and spare-parts logistics are now core to differentiation as connectivity and repair readiness become hygiene features across brands. The regulatory pipeline is central to volume and value outcomes as the ESPR’s Digital Product Passport requirements formalize repairability and traceability, creating service-led monetization openings for early movers.

Key Report Takeaways

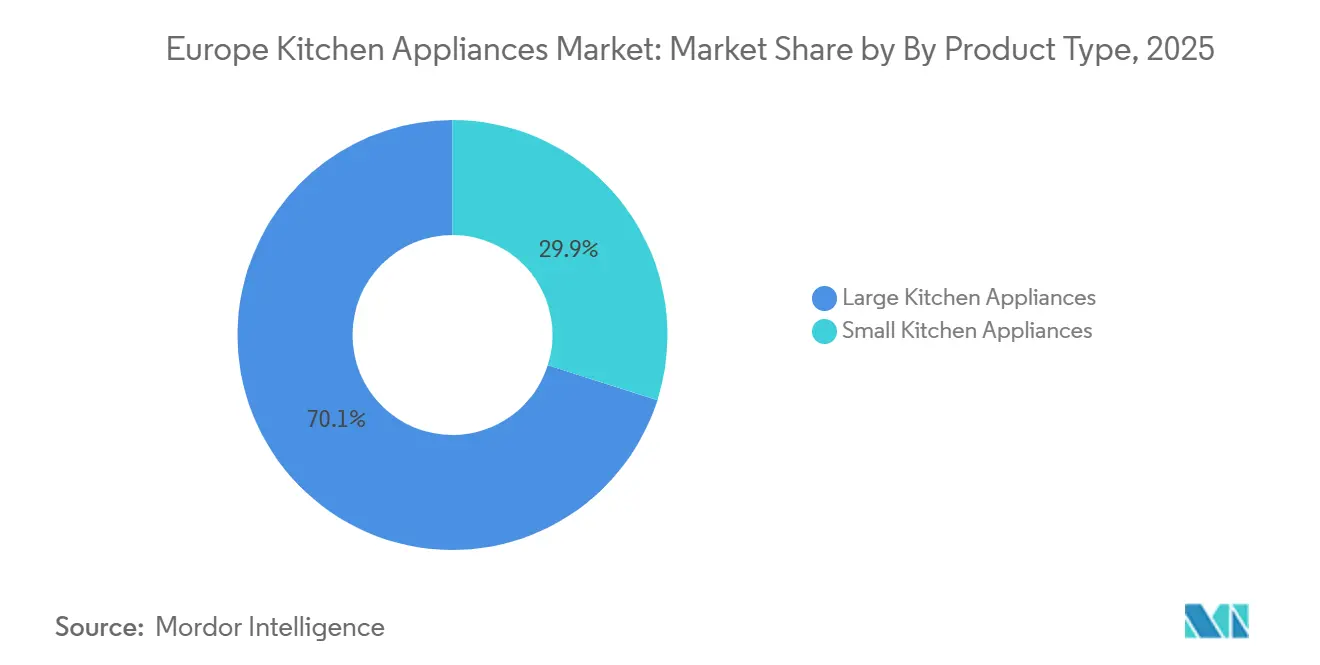

- By product, large kitchen appliances led with 70.05% revenue share in 2025 in the Europe kitchen appliances products market; small kitchen appliances are forecast to expand at a 5.65% CAGR through 2031.

- By end user, the residential segment held 70.85% share in 2025; commercial users are projected to grow at a 4.96% CAGR to 2031.

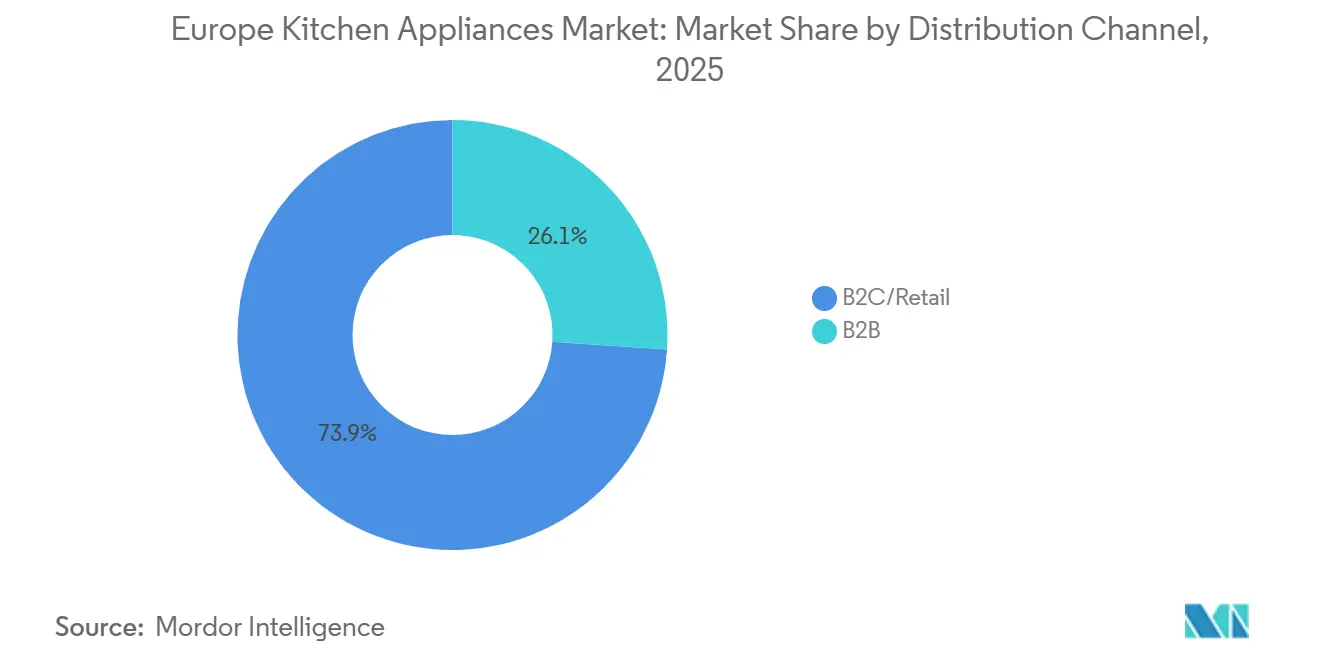

- By distribution channel, B2C/retail commanded 73.92% share in 2025 in the Europe kitchen appliances products market; online channels within retail are expected to post a 6.09% CAGR through 2031.

- By geography, Germany led with an 18.22% share in 2025; Spain is expected to record a 5.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU energy label rescaling and eco-design accelerate replacement cycles | +0.9% | Germany, France, the Netherlands, UK alignment | Medium term (2-4 years) |

| Premiumization and built-in kitchen adoption lift average selling prices | +0.7% | Germany, UK, France, BENELUX, Nordics | Long term (≥ 4 years) |

| Omnichannel access, two-person delivery, and EPREL transparency boost online conversion | +0.6% | EU-wide, notably the UK, Spain, Italy | Short term (≤ 2 years) |

| ESPR-driven circularity and Digital Product Passport enable service-led monetization | +0.4% | EU-wide pilots in France, Germany, Netherlands | Long term (≥ 4 years) |

| Air-fry functionality migration from countertop to ovens spurs oven replacements | +0.5% | Germany, UK, France, Nordics | Medium term (2-4 years) |

| Smart connected kitchens and interoperability lift feature adoption and ARPU | +0.6% | Germany, UK, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Energy Label Rescaling and Ecodesign Accelerate Replacement Cycles

The A–G energy label introduced in 2021 reshaped purchase decisions, with consumers relying on label classes to compare refrigerators, dishwashers, ovens, and hobs clearly and consistently, which drives upgrades toward Class A and B models. The European Commission’s review cycle for refrigerators and ovens extends beyond energy use to reparability, recyclability, and information display, which forces manufacturers to reengineer product architectures for both efficiency and serviceability[1]European Commission, “Energy Labelling and Ecodesign for Energy-Related Products,” European Commission, commission.europa.eu . The EPREL database and QR labels, in place since 2021, allow instant access to product data sheets and energy classes, simplifying comparisons on mobile and improving trust during online journeys. The Commission’s policy stack projects cumulative energy savings and household utility bill reductions by 2030, which adds a direct consumer incentive to replace older appliances earlier in their lifecycles. Brands investing in advanced insulation, zeolite drying, and high-efficiency motors are capturing mixed gains as regulations converge with visible performance tests and awards. The alignment of label visibility, eco-design scope, and digital transparency is lifting the Europe kitchen appliances products market through structured replacement cycles and premium mix improvements.

Premiumization and Built-In Kitchen Adoption Lift Average Selling Prices

Built-in formats continue to raise average selling prices as consumers invest in integrated aesthetics and handleless designs across ovens, dishwashers, refrigeration, and coffee systems. Product launches that combine premium materials, flush-fit integration, and smart functions target full-kitchen packages, often linking wall ovens with steam drawers and built-in coffee devices within a single design language. Premium refrigeration packages focus on larger niches, flexible temperature zones, and improved internal lighting, while promising higher energy classes under the rescaled labels to validate the investment case. Premium dishwashers and ovens with elevated finishes and AI-assisted options command higher price tiers even where unit volumes are soft, reinforcing the resilience of the affluent segment. Consistent model-line updates across built-in hobs, extractors integrated into cooktops, and concealed dishwashers support new kitchen design norms in Germany, the United Kingdom, and the Nordics. These dynamics keep the Europe kitchen appliances products market oriented toward higher ASP products that promise quieter operation, better hygiene, and seamless cabinetry integration[2]BSH Hausgeräte, “Press Releases and CES 2026 Announcements,” BSH Group, bsh-group.com .

Omnichannel Access, Two-Man Delivery, and EPREL Transparency Boost Online Conversion

Online purchasing gains credibility when paired with live consultations, fast scheduling, and reliable two-person services that install heavy units on the first visit. Logistics upgrades, including shared-user 4PL implementations and consolidated returns, cut lead times and ensure on-time delivery metrics that match or surpass in-store expectations for large appliances. Brand-owned D2C sites and social commerce integrations lift conversion and average order value by linking rich content and influencers with frictionless checkout. The EPREL QR requirement gives shoppers direct access to standardized product information, which reduces information asymmetry and builds confidence in buying higher-end models online. Brands that emphasize durability testing, energy classes, and spare-parts availability on their product pages report stronger online sell-through across categories that previously relied on in-person demos. These improvements in the discovery-to-delivery flow reinforce the European kitchen appliances products market as omnichannel setups align with regulatory transparency and upgraded last-mile capabilities[3]European Commission, “EPREL Product Database,” European Commission, energy.ec.europa.eu .

Smart Connected Kitchens and Interoperability Lift Feature Adoption and ARPU

Connectivity is shifting from a novelty to an expected baseline as interoperable standards enable cross-brand control and scenario automation. Leading ecosystems now link ovens, refrigerators, and dishwashers with leak detection, energy optimization, and guided cooking features that reduce the cognitive load on end users. Early deployments of Matter-enabled devices in North America and Europe, combined with established platforms like Home Connect and SmartThings, create a framework where AI and automation justify premium pricing. Insurance partnerships and energy tariff integrations highlight real-world savings, which have smart features such as risk-reduction and cost-management tools rather than one-off gadgets. Camera-enabled ovens that auto-recognize dishes and optimize settings increase the perceived utility of built-in formats and support higher price points. As the ESPR’s Digital Product Passport embeds requirements for lifecycle data and software updates, connectivity becomes a compliance-ready layer that advances the European kitchen appliances products market toward serviceable, updatable devices by design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged Consumer Caution and Heavy Promotions Compress Margins | -0.3% | EU-wide, more acute in Southern Europe | Short term (≤ 2 years) |

| Compliance And Component Cost Inflation Under Tighter Energy/Standby Caps | -0.2% | Europe's manufacturing hubs across Germany, Poland, Romania | Medium term (2-4 years) |

| Rising Refurbished Ecosystems Cannibalize New-Unit Sales | -0.1% | France, Germany, Netherlands | Long term (≥ 4 years) |

| Sluggish Housing Turnover And Renovation Delays Curb Built-In Upgrades | -0.2% | Germany, the United Kingdom, and France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged Consumer Caution and Heavy Promotions Compress Margins

Households display cautious spending behavior in late 2025 and early 2026, which raises the share of sales that occur during promotional windows. Retailers and brands increase discounts to maintain unit volumes, and this reduces pricing power in core categories. Some manufacturers report improved operating margins through cost efficiencies, yet they note negative price development due to promotion intensity. The balance between mixed gains in premium segments and broader discounting remains delicate, especially in markets where energy bills are stabilizing but wage growth is uneven. Premium tiers hold steadier in units and pricing, while mid-tier and entry ranges depend on seasonal events. Company disclosures confirm that cost controls help offset discounts, but persistent promotion cycles continue to weigh on profitability in the European kitchen appliances products market.

Compliance and Component Cost Inflation Under Tighter Energy/Standby Caps

Stricter standby power ceilings entering force in 2025 and tightening by 2027 require redesigns of power management, communication modules, and auto power-down features across categories. Upgrades to PMICs and connectivity modules add per-unit costs and require line retooling and additional testing time to validate compliance. The redesign cycle pushes more R&D and manufacturing coordination into 2026 for refrigerators, dishwashers, ovens, and microwaves. Larger brands invest in warehouse automation and local supply stabilization, while SMEs face capital constraints in upgrading electronics and testing infrastructure at speed. Although these policies will save energy at scale across the EU by 2030, near-term compliance spending and component volatility pressure margins. The result is disciplined feature prioritization and tighter launch sequencing, even as the Europe kitchen appliances products market benefits from the long-run efficiency gains set by law.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Large Kitchen Appliances Drive Volume, Small Appliances Lead Growth Velocity

Large kitchen appliances held 70.05% of the European kitchen appliances products market share in 2025, while small kitchen appliances advanced faster with a 5.65% CAGR through 2031. The European kitchen appliances products market is pivoting around premium dishwashers, built-in refrigeration, and induction-based cooking solutions that balance design with energy labels and water efficiency requirements. Refrigerators and freezers remain anchor products, and larger integrated models with flexible cooling zones and advanced insulation set the tone for Class A outcomes under the rescaled label. Dishwashers gain momentum through quieter operation, zeolite drying, and hygiene enhancements, supported by production and testing upgrades at leading European plants. Cooking formats show mixed volume trends, yet innovation in integrated extractors and no-preheat approaches keeps value trends favorable in hobs and ovens. As air-fry functionality migrates from countertop appliances into ovens, value per unit improves even when total oven volumes fluctuate in line with renovation cycles.

Small appliances retain a fragmented structure with coffee, air frying, blending, and food preparation as consistent demand pools tied to health and convenience themes. Coffee remains a high-frequency purchase driver, and premium manual or capsule platforms help smooth category seasonality. The European kitchen appliances products market size for small kitchen appliances is projected to expand at a 5.65% CAGR during 2026–2031 on the back of D2C, omnichannel exposure, and faster launch cycles. Air fryers plateaued in standalone units in some countries, but multi-function features and larger capacities sustain value growth as brands expand into adjacent countertop categories. Portfolio expansion that crosses into beauty, outdoor grilling, and smart recipe ecosystems creates new reasons to upgrade within brand families. Stronger packaging circularity programs in espresso and air-fry lines enhance sustainability signals without relying on green premiums to sustain demand.

By End User: Residential Dominates, Commercial Accelerates via HoReCa Recovery

Residential buyers accounted for 70.85% of 2025 demand as replacement cycles, EPREL visibility, and smart-home adoption patterns supported steady sell-through. Built-in penetration in mature markets shifts spending to higher-end packages, while entry and mid-tier buyers move to better energy classes as price gaps compress during promotions. Replacement dominates residential volumes, and energy label familiarity accelerates upgrades where the utility bill case is visible. Connectivity features and recipe ecosystems improve attach rates for premium options in ovens, refrigeration, and dishwashers. The European kitchen appliances products market size for commercial end users is projected to expand at a 4.96% CAGR through 2031, as hotels, restaurants, and cafés scale back to full operating patterns with professional coffee as a strong draw. B2B buyers converge on total cost of ownership, uptime, and service contracts, which strengthens recurring revenue profiles for vendors.

Commercial demand includes professional kitchens, micro-canteens, and boutique coffee setups that lean on subscription maintenance and predictive diagnostics. Prosumer espresso models blur the home and professional line, elevating average selling prices and strengthening aftermarket opportunities. As ESPR-linked Digital Product Passports spread, both residential and commercial buyers will see repairability, parts access, and lifecycle data as part of standard due diligence. The European kitchen appliances products industry is already adapting service footprints and spare-parts logistics to meet these needs in 2026. B2B adoption of dishwashing technologies with hygiene enhancements and faster cycles supports labor efficiency and compliance needs. The combination of energy class improvements and contract-based service models helps keep commercial trajectories above residential growth over the forecast period.

By Distribution Channel: B2C Retail Anchors, Online Surges, B2B Direct Gains Traction

B2C/Retail accounted for 73.92% of sales in 2025, with online channels inside retail posting the fastest growth at a 6.09% CAGR through 2031. Multi-brand retailers continue to anchor volumes, while brand stores and D2C websites gain on the strength of product expertise and curated demos. Logistics consolidation improves on-time delivery and supports higher first-time installation rates for heavy products. Online growth rests on reliable two-person delivery, transparent EPREL information, and structured consultations that mirror in-store experiences. The Europe kitchen appliances products market size for online channels within retail is projected to expand at a 6.09% CAGR during 2026–2031, aided by short delivery windows and integrated returns. B2B direct gains share on the back of bulk purchases by developers and large corporate buyers who value assured energy class compliance and lifecycle support.

The European kitchen appliances products industry uses hybrid models to reach fragmented SME customers through distributors while managing direct relationships with the largest retail chains. Builder partnerships around induction migration and electric upgrades open bundled selling opportunities that include ovens, hobs, and extractors with built-in configurations. As DPP requirements come into force, channel parties on lifecycle information will rise and reduce trust gaps between online and physical touchpoints. Property developers seek consistent energy performance declarations to align with evolving building standards and green financing criteria. Closer orchestration between brand showrooms, online advisors, and installation partners shrinks the gap between discovery and ownership. These patterns reinforce steady growth across the Europe kitchen appliances products market as omnichannel capabilities scale.

Geography Analysis

Germany accounted for 18.22% of the Europe kitchen appliances products market share in 2025, supported by high built-in adoption and the region’s most mature induction base. Germany’s premium tier features brands with long testing horizons and strong spare-parts commitments, which keep value share elevated despite economic headwinds. Leading manufacturers adjust local factory footprints to reflect demand patterns while maintaining German R&D and core investments in digitalization and automation. The market balance continues to favor Class A and B dishwashers and energy-efficient refrigeration solutions as label literacy remains high. Softness in housing markets weighs on some built-in upgrade plans, yet the core of demand persists due to replacements and project-led kitchen remodels. The evolution of AI-driven ovens and integrated extractors in hobs aligns well with German kitchen design norms[4]Institute for European Energy and Climate Policy (IEECP), “Research and Reports on Electrification,” IEECP, ieecp.org .

Spain shows the fastest growth at a 5.22% CAGR to 2031 as renovation cycles and electrification incentives lift replacement demand. The Europe kitchen appliances products market size for Spain is supported by kitchen refurbishments that favor induction hobs and integrated ovens. Brands planning direct-operating models in Spain expect short-term transitions followed by improved margin capture and tighter retail execution. Health and convenience themes in small appliances remain strong in Spain, given the demographic tilt toward urban households. Expanded omnichannel presence and last-mile improvements sustain online conversion for cooking and dish care. Incentive programs and building renovations reinforce demand for efficient white goods that meet current and near-term EU criteria.

The United Kingdom stabilized after earlier supply disruptions, with portfolio diversification offsetting category plateaus in air fryers. Online logistics and two-person service reliability reached consistent performance levels, supporting buy-online-install-soon journeys in large appliances. France and Italy continue to balance premium gains against broad consumer caution, with premium built-in launches from multiple brands adding resilience to value trends. Italy’s manufacturing footprint shifts eastward for some lines while service hubs expand to support circularity and spare-parts flow. The BENELUX and Nordics maintain high online touchpoints and early smart-home adoption, creating favorable conditions for connected kitchen features. Across the rest of Europe, local brands leverage cost advantages and brand familiarity to expand in Eastern markets, while larger groups consolidate portfolios under shared R&D and service programs.

Competitive Landscape

The Europe kitchen appliances products market in 2026 remains oligopolistic in large kitchen appliances, with a tight group of global and European champions holding leadership in refrigeration, dishwashing, and cooking. Small kitchen appliances are more fragmented, with specialists scaling through D2C, social commerce, and fast-moving launch calendars. BSH Hausgeräte sustains a significant footprint across German factories and international sites while investing in automation and AI-led kitchen software to amplify its Home Connect ecosystem. Beko Europe, created through the combination of Whirlpool EMEA’s major domestic appliances with Arçelik’s European operations, consolidates a multi-brand portfolio with a broad manufacturing base. Electrolux Group concentrates on premium AEG and Electrolux tiers in Europe while reporting progress on cost efficiencies in 2025 despite a promotional environment. Haier Europe builds out a regional service hub strategy to enhance spare parts logistics and reconditioning, aligned with circularity goals and connected feature adoption.

Miele targets premium positioning with sustained investments in Germany and a long-standing commitment to long-life testing and spare-parts availability. Premium coffee and prosumer crossovers from De’ Longhi’s professional brands add a high-value stream that strengthens B2B and affluent residential segments. Recent strategic moves include new factory builds, portfolio extensions, and interoperability commitments that reinforce premium and service-led positioning. BSH opened a new plant in Cairo to produce cookers for Africa and Middle Eastern markets, diversifying its manufacturing base while maintaining EU investments in automation.

Swisslog’s AutoStore implementation for Haier Europe’s Brugherio Service Hub underpins spare-parts and reconditioning logistics that align with ESPR-linked circularity objectives. Partnerships for robotic cleaning and expanding built-in accessory ecosystems signal that adjacent categories will remain part of kitchen platform strategies. These actions anchor the Europe kitchen appliances products market in 2026 as major brands align with regulatory, connectivity, and service trends across the region.

Europe Kitchen Appliances Industry Leaders

Electrolux AB

BSH Hausgerate GmbH

Haier Europe

Groupe SEB

Beko Europe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BSH Hausgeräte opened a new automated shipping facility at its Giengen site to optimize supply chains, using tailored packaging to reduce material waste and transport costs while increasing efficiency for refrigerator production. The facility aligns with investments focused on digitalization and automation across German sites.

- January 2026: SMEG announced new direct subsidiaries in New Zealand and the Middle East, bringing the Group’s direct subsidiaries to 22 worldwide and reinforcing export-led growth and service quality in high-potential regions.

- January 2026: BSH highlighted personalized AI for the kitchen at CES 2026 and reaffirmed R&D investment and digitalization priorities across 39 factories after reporting 2024 revenue growth.

- December 2025: Samsung showcased the Bespoke AI Refrigerator Family Hub with Google Gemini integration, extending AI food recognition to thousands of items, alongside new energy management features that optimize cooling performance.

Europe Kitchen Appliances Market Report Scope

The report on the European kitchen appliance market provides a comprehensive evaluation of the market, with an analysis of the segments in the market. Moreover, the report also provides the competitive profile of the key manufacturers, along with their product offerings and revenue analysis. Europe Kitchen Appliances Market is Segmented by Product (Refrigerators and Freezers, Dishwashers, Food Processors, Mixers and Grinders, Microwave Ovens, Grills and Roasters, Water Purifiers, and Other Kitchen Appliances), By Distribution Channel (Multi-Brand Stores, Specialty Stores, Online Stores, and Other Distribution Channels) and by Geography (France, United Kingdom, Germany, Italy, Spain, and Rest of Europe). The report offers market size and forecasts for the European kitchen appliances market in Value (USD billion) for all the above segments.

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (directly from the manufacturers) |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX |

| NORDICS |

| Rest of Europe |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers and Blenders | ||

| Grills and Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Countertop Ovens | ||

| Other Small Kitchen Appliances (bread makers, waffle makers, egg cookers, etc.) | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (directly from the manufacturers) | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size and outlook for the Europe kitchen appliances products market in 2026?

The Europe kitchen appliances products market size is USD 71.4 billion in 2026 and is expected to reach USD 87.97 billion by 2031 at a 4.26% CAGR.

Which product categories lead growth in the Europe kitchen appliances products market?

Large appliances anchor volume, while small kitchen appliances lead growth with a 5.65% CAGR through 2031, supported by health, convenience, and online adoption.

Which end-user segment is expanding faster in the Europe kitchen appliances market?

Commercial buyers are projected to grow faster at 4.96% CAGR through 2031, driven by HoReCa recovery and professional coffee demand, while residential remains the largest segment.

How are regulations shaping demand in the Europe kitchen appliances products market?

The A–G energy label, ecodesign, and ESPR-driven Digital Product Passports are accelerating replacements, raising reparability standards, and enabling service-led models that support long-term growth.

Which regions stand out within the Europe kitchen appliances products market?

Germany leads by value share, while Spain records the fastest growth to 2031, helped by kitchen renovations, induction migration, and improving online logistics and conversions.

Page last updated on: