Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

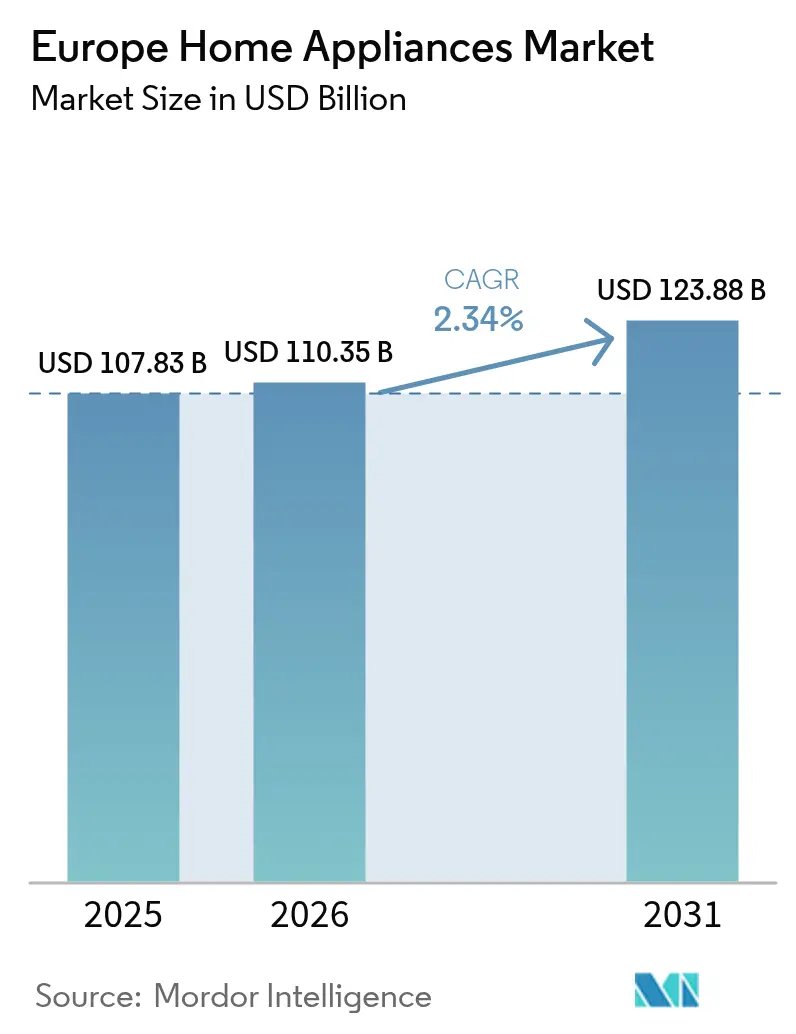

| Base Year Market Size (2025) | USD 107.83 Billion |

| Market Size (2026) | USD 110.35 Billion |

| Market Size (2031) | USD 123.88 Billion |

| Growth Rate (2026 - 2031) | 2.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Appliances Market Analysis by Mordor Intelligence

The Europe home appliances market size was valued at USD 107.83 billion in 2025 and estimated to grow from USD 110.35 billion in 2026 to reach USD 123.88 billion by 2031, at a CAGR of 2.34% during the forecast period (2026-2031). Manufacturers are shifting from volume-driven tactics toward value enhancement, emphasizing smart connectivity, embedded software, and higher energy-efficiency ratings that comply with the EU’s evolving eco-design legislation [1]European Commission, “Energy Performance of Buildings Directive Revision,” ec.europa.eu. . Regulatory alignment, particularly the Energy Performance of Buildings Directive (EPBD) revision and the forthcoming Ecodesign for Sustainable Products Regulation (ESPR), accelerates demand for products carrying better repairability scores and lower lifetime energy costs. Competitive intensity remains moderate, yet the entrance of Beko Europe following the Whirlpool-Arçelik deal increases the pressure on incumbents to invest in R&D and digital platforms. Against a backdrop of raw-material inflation and fragile supply chains, utilities’ demand-response rebates and an expanding base of single-person households continue to create tangible pockets of opportunity across Western and Central Europe.

Key Report Takeaways

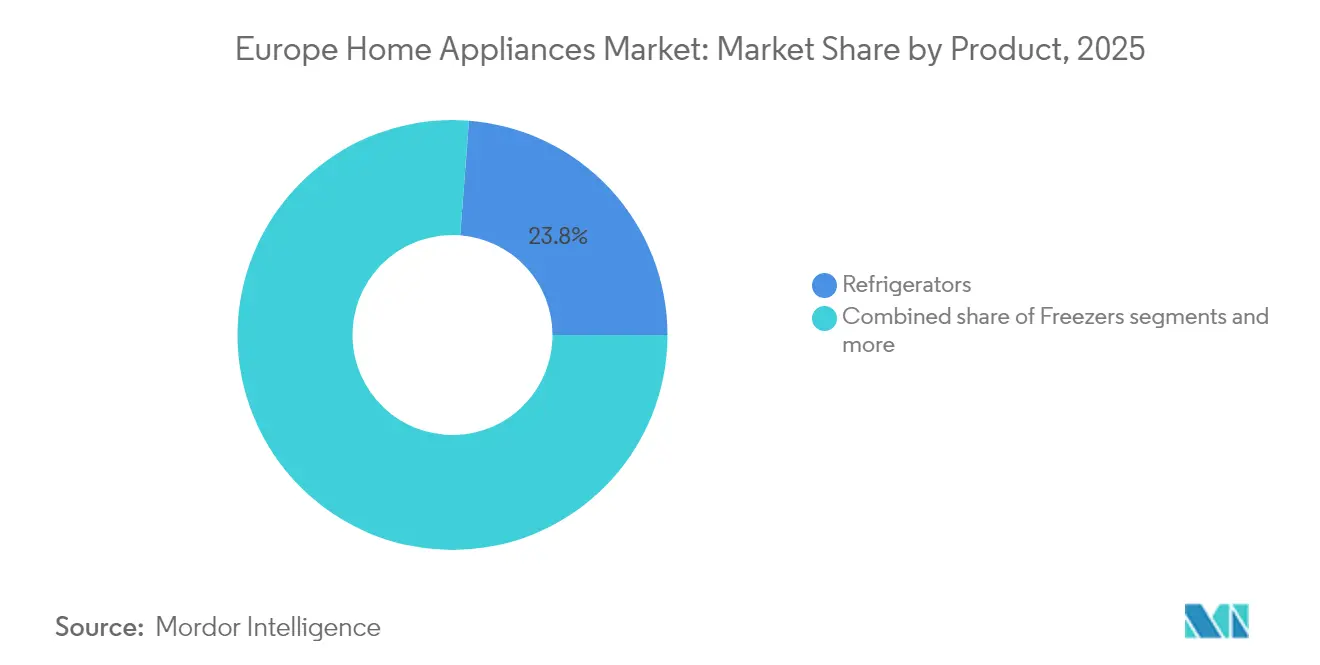

- By product type, refrigerators led with 23.78% of the Europe home appliances market share in 2025, while air fryers are projected to grow at a 4.05% CAGR through 2031.

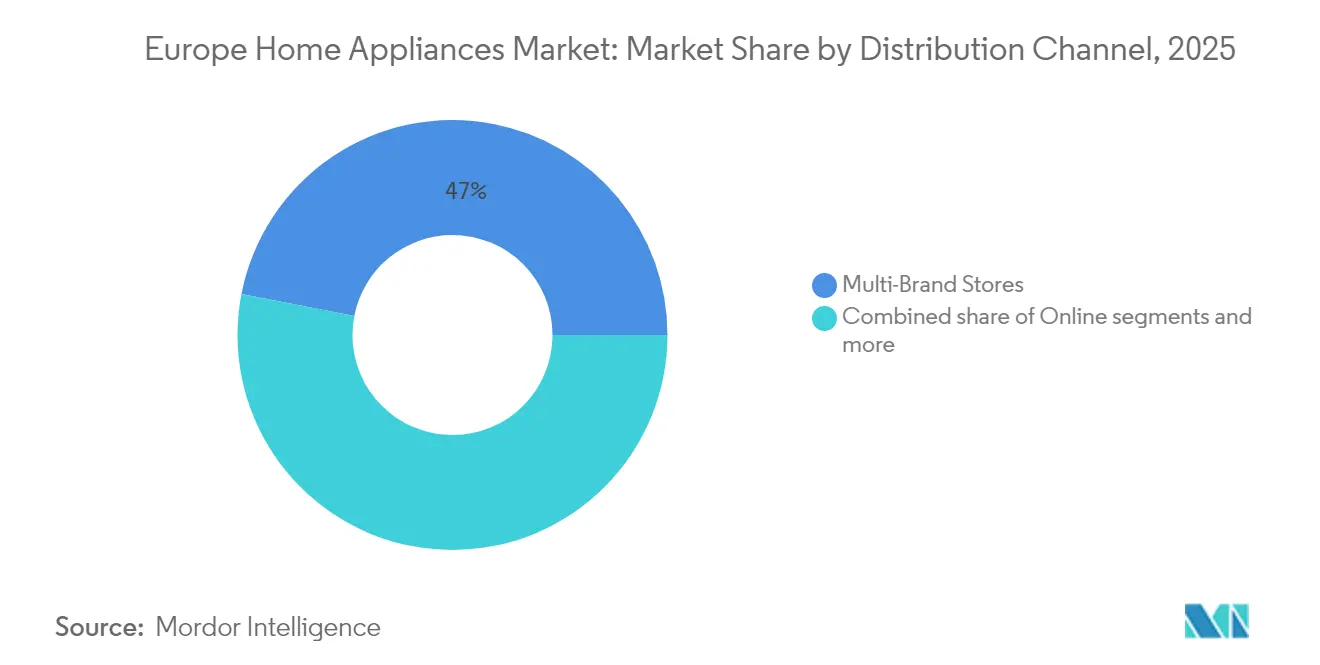

- By distribution channel, multi-brand stores held 46.95% of the Europe home appliances market size in 2025; online channels record the highest forecast growth at 4.62% CAGR to 2031.

- By geography, Germany accounted for 13.65% of the Europe home appliances market share in 2025, whereas Italy is advancing at a 3.02% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency labeling & eco-design laws | +0.8% | EU27, UK, Switzerland | Medium term (2-4 years) |

| Smart-home integration accelerating upgrades | +0.6% | Western Europe, Nordics | Short term (≤ 2 years) |

| Growth in single-person households | +0.4% | Germany, France, Nordics, urban centers | Long term (≥ 4 years) |

| Rising disposable income in CEE | +0.3% | Poland, Czech Republic, Hungary, Romania | Medium term (2-4 years) |

| Heat-pump dryer subsidies | +0.2% | Germany, Netherlands, France | Short term (≤ 2 years) |

| Utilities’ demand-response rebates | +0.2% | Germany, Netherlands, Belgium | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Labeling & EU Eco-Design Mandates

The ESPR, scheduled for full enforcement in 2026, introduces digital product passports that log energy consumption, material composition, and repairability metrics throughout an appliance’s life cycle [2]European Commission, “Ecodesign for Sustainable Products,” ec.europa.eu. . Compliance costs raise entry barriers for import-dependent brands, favoring regional manufacturers with embedded sustainability processes. Spare-parts obligations and mandated firmware updates make total cost of ownership a decisive purchase factor. ISO 14006 alignment becomes a core procurement requirement among European retailers, further reinforcing the premium that consumers attach to low-carbon footprints. Brands able to launch A-rated models ahead of statutory deadlines command price premiums and strengthen retailer partnerships.

Rapid Replacement Cycle Driven by Smart-Home Integration

Matter protocol adoption and Thread networking permit appliances to join whole-home energy-management systems, making non-connected units a bottleneck in demand-response programs offered by utilities [3]Federal Ministry for Economic Affairs and Climate Action, “Building Renovation Programs,” bmwk.de. . Functional obsolescence now arrives sooner than mechanical failure, encouraging 5- to 7-year upgrade cycles. LG’s 2024 takeover of Athom, maker of Homey hubs, illustrates a pivot from one-off sales to subscription-based energy-optimization services. Connected models deliver usage data that utilities convert into off-peak rebates, trimming payback periods for premium appliances. Northern Europe, where electricity prices remain high, leads adoption.

Rising Disposable Income in Central & Eastern Europe

Economic convergence in Central and Eastern Europe creates a distinct growth corridor where appliance penetration rates remain below Western European levels while purchasing power steadily increases. Poland's GDP per capita growth of 3.20% in 2024 and similar trajectories in Czech Republic and Hungary drive appliance market expansion as consumers upgrade from basic functionality to premium features [4]OECD, “Economic Outlook 2025,” oecd.org. . This income growth particularly benefits built-in appliance segments where kitchen renovations accompany rising living standards, creating opportunities for premium brands to establish market presence before local competitors can respond. The region's integration with EU supply chains and energy efficiency standards accelerates the adoption of Western European appliance technologies, while lower labor costs attract manufacturing investments that strengthen local market presence.

Surge in Heat-Pump Dryer Retrofits Supported by Subsidies

Government incentives across Europe specifically target heat-pump dryer adoption as part of broader electrification strategies, creating a distinct growth vector within the laundry appliance segment. Germany's BEG (Bundesförderung für effiziente Gebäude) program provides up to EUR 2,100 (USD 2,250) subsidies for heat-pump dryer installations, while France's MaPrimeRénov scheme offers similar incentives as part of whole-home energy efficiency upgrades. These programs specifically target heat-pump technology because it delivers 50% energy savings compared to conventional vented dryers while enabling integration with home heat recovery systems. The subsidy structure creates artificial demand acceleration that manufacturers leverage to build market share and achieve production scale economies before incentives phase out.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility & component gaps | -0.5% | Global, EU assembly facilities | Short term (≤ 2 years) |

| Inflation-driven consumer down-trading | -0.4% | Southern & Eastern Europe | Short term (≤ 2 years) |

| EU Right-to-Repair rules | -0.3% | EU27 | Long term (≥ 4 years) |

| Grid-capacity fees penalizing peak loads | -0.2% | Germany, Belgium, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility and Component Shortages

Persistent semiconductor shortages and raw material price volatility continue to disrupt European appliance manufacturing, with plastic resin costs rising 15-20% year-over-year in 2024 while metal prices remain elevated compared to pre-pandemic levels. This cost pressure forces manufacturers to implement selective price increases while absorbing margin compression, particularly affecting mid-market segments where price sensitivity limits pass-through capability. Supply chain resilience becomes a competitive differentiator as companies with diversified sourcing and vertical integration maintain better availability and cost control compared to those dependent on single-source suppliers.

EU "Right-to-Repair" Rules Extending Product Lifetimes

The EU's Right-to-Repair directive, fully implemented across member states in 2024, mandates 10-year spare parts availability for major appliances and introduces repairability scoring that influences consumer purchasing decisions. This regulation extends average appliance lifespans by 2-3 years, reducing replacement demand while increasing aftermarket service revenue opportunities. Manufacturers adapt by designing modular architectures that facilitate component replacement and developing service networks that can monetize extended product lifecycles through maintenance contracts and upgrade services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Air Fryers Drive Small Appliance Renaissance

Refrigerators preserved their 23.78% portion of the Europe home appliances market in 2025 as top-mounted freezer models shifted to A-class efficiency ratings that align with upcoming eco-design thresholds. In value terms, refrigerators accounted for USD 25.64 billion of the Europe home appliances market size during 2025, and the segment is tracking a 1.84% CAGR through 2031 as incremental gains from compressor and insulation advances taper. At the opposite end of the growth spectrum, air fryers are scaling from USD 2.38 billion in 2025 to an expected USD 3.02 billion by 2031, reflecting a 4.05% CAGR that outpaces every other small-appliance line. Compact form factors, oil-free cooking, and app-based recipe libraries resonate with single-person and health-conscious households, creating premium sub-segments featuring dual-zone baskets and smart-heat algorithms.

Beyond these headline categories, washing machines and dishwashers integrate turbidity and fabric-sensing technology that adjusts cycle length and resource consumption in real time. Sensor-driven models claim water savings of up to 35% versus legacy machines, an advantage reflected in higher average selling prices. Combination microwave-steam-convection ovens underscore the push toward multi-functionality, capturing space-constrained urban buyers while raising cross-category cannibalization risks. Manufacturers deploy modular platform architectures, enabling rapid SKU proliferation without duplicating engineering expense. Over the forecast horizon, premiumization remains the principal value lever, offsetting the deceleration of pure replacement demand triggered by Right-to-Repair regulations.

By Distribution Channel: Online Acceleration Reshapes Retail Landscape

Multi-brand stores retained 46.95% of the Europe home appliances market share in 2025, yet channel fundamentals are tilting online as digitally native retailers deploy virtual-demo tools and flexible delivery windows. The Europe home appliances market size generated through e-commerce touched USD 18.28 billion in 2025 and is positioned to exceed USD 23.98 billion by 2031 at a 4.62% CAGR. Direct-to-consumer storefronts amplify manufacturer control over pricing, product launches, and customer data, enabling tailored after-sales services such as subscription detergents for auto-dose washers.

Physical showrooms pivot toward experiential selling, integrating augmented-reality kitchen planners and on-site installation services. Exclusive brand outlets gain momentum for built-in portfolios, where appliance-cabinet alignment requires professional guidance. Warehouse clubs and regional specialty chains differentiate via financing bundles and extended warranties. The emergent omnichannel model hinges on unified inventory visibility across touchpoints, pushing retailers to overhaul legacy ERP architectures. Order-fulfillment optimization, including micro-fulfillment centers inside city limits, trims last-mile costs and supports same-day delivery promises on large-format goods.

Geography Analysis

Western Europe contributed more than 69% of the Europe home appliances market in 2025, with Germany alone capturing 13.65% share on the strength of its manufacturing base and high household incomes. Smart-home penetration surpasses 50% in German urban centers, leading to elevated attach rates for voice-enabled refrigerators and AI-driven laundry pairs. The United Kingdom shows resilient spend on premium built-ins as post-Brexit logistics bottlenecks ease and housing-renovation activity normalizes.

Italy is the standout growth engine, advancing at a 3.02% CAGR through 2031 amid generous Superbonus tax credits that subsidize energy-efficient appliance purchases as part of home retrofits. Italian consumers favor design-oriented finishes and customizable hardware, giving premium brands pricing power. France and Spain leverage building-renovation incentives to sustain mid-single-digit value growth despite cautious consumer sentiment.

Central and Eastern Europe offer the most compelling volume upside. Poland’s appliance shipments climbed 6.90% in 2025 as rising wages converged with EU energy-efficiency mandates. Czech Republic and Hungary exhibit similar trajectories, underpinned by automotive-sector wage gains that lift discretionary spending. Cross-border e-commerce accelerates feature adoption as consumers tap Western inventory assortments. These markets double as near-shoring locations, cushioning Western supply chains against Asia-Pacific risks.

Competitive Landscape

In 2024, the Europe home appliances market was moderately consolidated, with the top five vendors collectively holding a significant share of the market. BSH Hausgeräte led the field, supported by its strong engineering capabilities and vertically integrated component supply chain, which helped mitigate the impact of global chipset shortages. Whirlpool transferred its EMEA operations to Beko Europe in April 2024, creating a EUR 5.5 billion (USD 5.90–5.95 billion) revenue company that combines Turkish manufacturing efficiencies with Western design and distribution strengths. Electrolux focused its investments on higher-margin built-in appliances to enhance profitability. Meanwhile, SMEG and Miele maintained their positions in the premium segment, emphasizing distinctive design and dedicated in-house service networks.

Strategic focus tilts toward software-defined appliances that harvest usage data, unlocking predictive-maintenance services and utility partnerships. LG’s acquisition of Athom positions the Korean brand as a software-centric challenger that monetizes AI-enabled routines beyond hardware margin. Incumbents intensify R&D around heat-pump compression, leveraging patent portfolios to sustain efficiency leadership in anticipation of stricter eco-design tiers. M&A momentum is likely to persist as tier-two vendors seek scale to fund compliance and digital-platform investments.

Emerging disruptors exploit direct-to-consumer logistics and subscription models that bundle small appliances with consumables. Though their revenue remains low in absolute terms, they influence channel standards around unboxing, delivery speed, and return convenience. Incumbents respond with white-label fulfillment arms and last-mile partnerships to match customer expectations built by e-commerce pure-plays.

Europe Home Appliances Industry Leaders

Whirlpool Corp.

BSH Hausgeräte GmbH

Electrolux AB

Haier Smart Home (Candy/Hoover)

Dyson Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Midea Group completed the acquisition of Teka Group (excluding Teka Rus LLC) to strengthen its European presence and enlarge its premium portfolio.

- February 2025: Whirlpool unveiled the KitchenAid premium collection at KBIS 2025, offering customizable Juniper and Black Ore finishes.

- June 2024: LG Electronics acquired an 80% stake in Dutch smart-home platform Athom, adding the Homey ecosystem to its AI-home portfolio.

- April 2024: Whirlpool finalized the creation of Beko Europe in partnership with Arçelik A.Ş., retaining a 25% stake while reallocating resources toward the Americas and India.

Europe Home Appliances Market Report Scope

A complete background analysis of the European home appliances market, including an assessment of the emerging market trends by segment, significant changes in the market dynamics, and the market overview, is provided. Major Appliances is segmented into Refrigerators, Freezers, Dishwashing Machines, Washing Machines, and Cookers and Ovens, Other Major Appliances. Small Appliances is segmented into Vacuum Cleaners, Coffee Machines, Irons, Toasters, Grills and Roasters, and Other Small Appliances. Distribution Channel is segmented into Multibrand Stores, Exclusive Stores, Online, and Other Distribution Channels. The market is segmented by Country into Germany, Poland, France, Italy, and the Rest of Europe. The report offers market size and forecasts for the European home appliances market in value (USD million) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi and Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills and Roasters | |

| Electric Kettles | |

| Juicers and Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi and Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills and Roasters | ||

| Electric Kettles | ||

| Juicers and Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Region | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

How large is the Europe home appliances market in 2026?

The Europe home appliances market size reached USD 110.35 billion in 2026 and is projected to rise to USD 123.88 billion by 2031.

Which product segment holds the largest market share across Europe?

Refrigerators led with a 23.78% share of the Europe home appliances market in 2025, reflecting strong replacement demand for energy-efficient models.

Why are air fryers growing faster than other categories?

Air fryers combine oil-free cooking with compact form factors that appeal to single-person and health-focused households, resulting in a 4.05% CAGR outlook through 2031.

Which distribution channel is expanding the fastest?

Online sales are increasing at a 4.62% CAGR as manufacturers push direct-to-consumer storefronts and retailers deploy virtual demos and flexible delivery options.

What factors make Italy the fastest-growing European market?

Superbonus tax credits for energy-efficient renovations and a rebound in household spending drive Italy’s 3.02% CAGR, outpacing other geographies through 2031.

How will EU eco-design rules influence appliance innovation?

From 2026, digital product passports and stricter repairability scores will push manufacturers toward modular, software-defined designs that meet tougher sustainability benchmarks.

Page last updated on: