Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

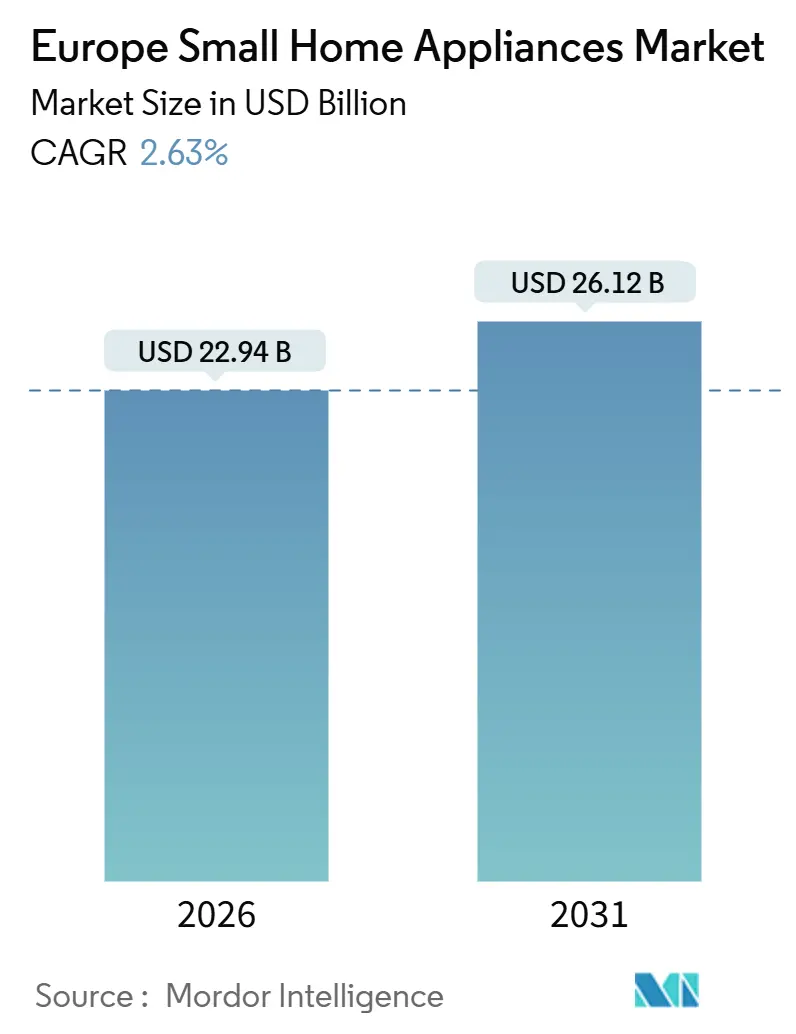

| Market Size (2026) | USD 22.94 Billion |

| Market Size (2031) | USD 26.12 Billion |

| Growth Rate (2026 - 2031) | 2.63% CAGR |

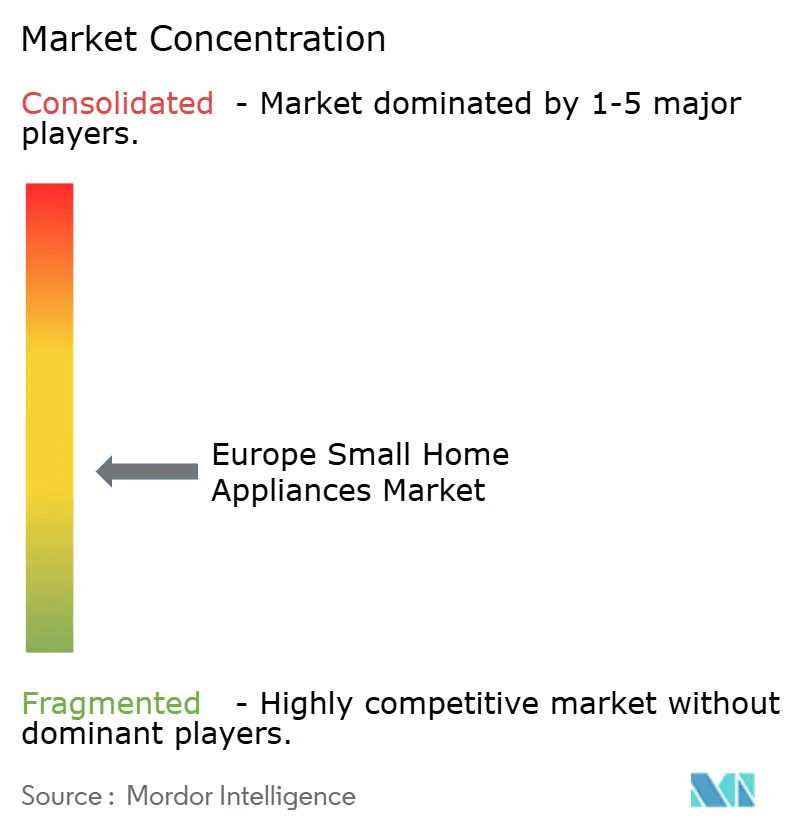

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Small Home Appliances Market Analysis by Mordor Intelligence

The Europe Small Home Appliances Market size is estimated at USD 22.94 billion in 2026, and is expected to reach USD 26.12 billion by 2031, at a CAGR of 2.63% during the forecast period (2026-2031).

The growth profile reflects a shift from ownership-focused volume to access-based value, as EU product sustainability rules introduce digital product passports and lifecycle security obligations that change how products are designed, sold, and serviced. Replacement cycles averaging 5 to 6 years are now the dominant cycle driver rather than first-time penetration, and this aligns with the measured headline expansion. Germany remains an anchor country on the back of energy-efficiency economics, while the Nordics advance faster due to digital infrastructure that supports rapid adoption of connected and IoT-enabled appliances[1]Eurostat, “Internet-connected devices are widely used in the EU,” Eurostat, ec.europa.eu.. Products follow a two-speed path as coffee makers hold the largest revenue pool while air fryers post the fastest value growth, and distribution dynamics favor omnichannel models in which multi-brand stores lead but online gains the most share.

Key Report Takeaways

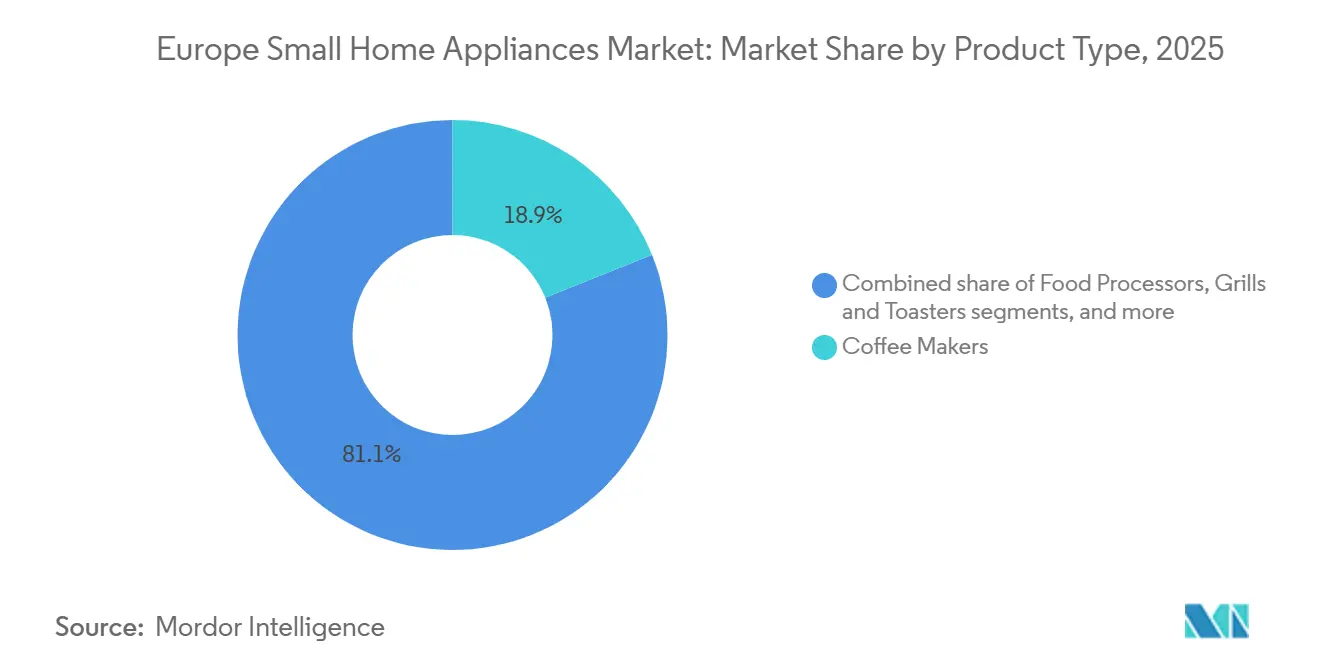

- By product type, coffee makers led with 18.92% of the Europe small home appliances market share in 2025, while air fryers are projected to expand at a 2.93% CAGR through 2031.

- By distribution channel, multi-brand stores held 48.51% of the Europe small home appliances market share in 2025, while online recorded the highest projected CAGR at 3.63% through 2031.

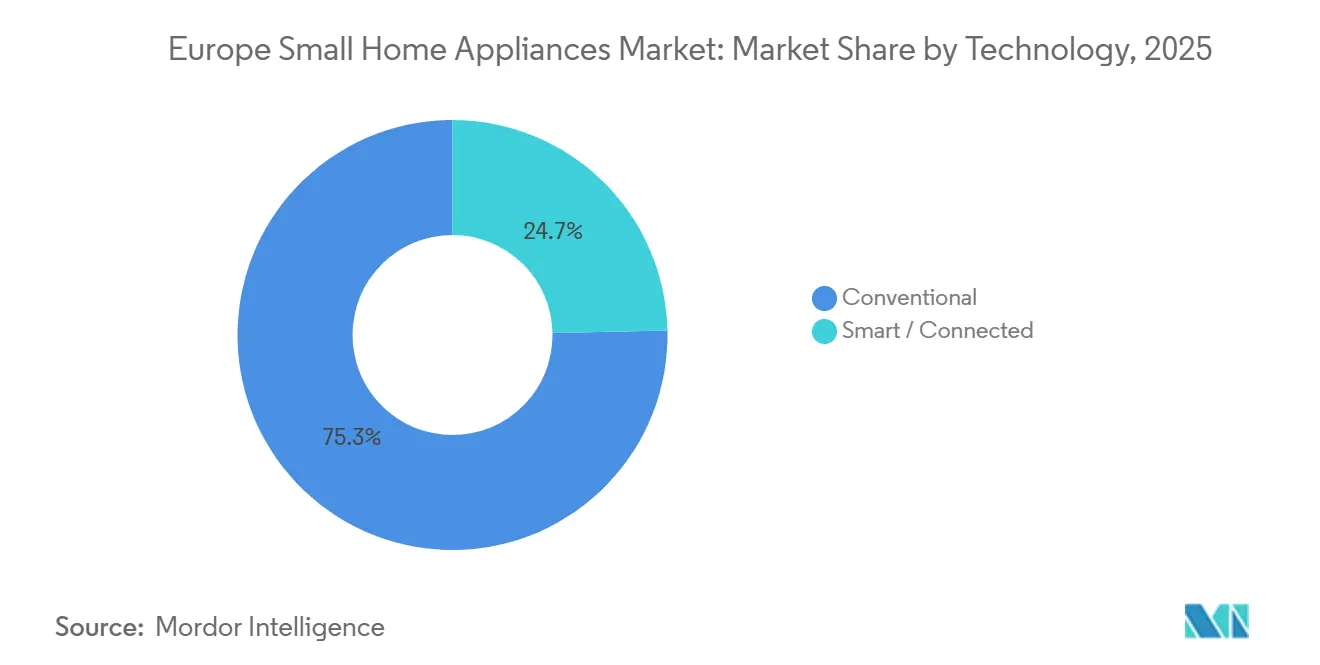

- By technology, the conventional segment accounted for 75.33% of the Europe small home appliances market share in 2025, while smart or connected appliances are projected to grow at a 3.27% CAGR through 2031.

- By geography, Germany held 19.73% of the Europe small home appliances market share in 2025, while the Nordics are forecast as the fastest-growing region at a 3.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Small Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce penetration surge | +0.6% | Global, with the United Kingdom and Nordic early movers; Germany and France accelerating | Medium term (2-4 years) |

| Rising disposable income and premiumization | +0.5% | Western Europe, CEE post-2027 | Long term (≥ 4 years) |

| Stringent EU energy-efficiency regulations | +0.8% | EU27 plus United Kingdom following parallel A-G rescaling | Short term (≤ 2 years) |

| Growth of repair-as-a-service platforms | +0.3% | France leading; Germany, Austria, Netherlands rolling out by 2027 | Long term (≥ 4 years) |

| Appliance subscription and rental models | +0.2% | Germany, Austria, Spain, Netherlands; Samsung and LG expanding pan-Europe | Medium term (2-4 years) |

| AI-powered food-waste reduction functions | +0.4% | BENELUX, Nordics, Germany; Southern Europe lagging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Penetration Surge

E-commerce captured a rising share of the Europe small home appliance sales by 2025, compressing the channel shift into a shorter window as consumers increased digital research, price comparison, and post-sale support online. United Kingdom shoppers demonstrate the highest pre-purchase digital engagement among non-essential categories, which leads to sustained online sales gains even when store traffic is healthy. Nordic digital habits accelerate the adoption of connected appliances as Sweden reports high monthly online shopping participation and Denmark sustains very high internet-connected device usage, which reduces friction at checkout and onboarding for connected devices. The EU’s Radio Equipment Directive cybersecurity requirements for wireless devices took effect for compliance beginning August 2025, and this strengthens consumer trust in connected appliances while favoring scaled online platforms that centralize compliance documentation[2] CSA Group, “EU RED Cybersecurity Requirement Take Effect August 1, 2025,” CSA Group, csagroup.org. In this environment, the Europe small home appliances market benefits from omnichannel retail that blends showroom experiences with online inventory availability and rapid delivery. Online growth in turn amplifies product discovery for rapid innovation cycles in categories such as air fryers and robotic vacuums, which reinforces the channel’s structural share gains.

Stringent EU Energy-Efficiency Regulations

The European Union strengthened its product policy framework to reduce household energy consumption and extend product lifetimes, which directly promotes upgrades from older units to higher-efficiency models. The Ecodesign for Sustainable Products Regulation entered into force in 2024 and introduces digital product passports, durability, repairability, and information requirements that apply across nearly all goods, including small household appliances. Updated ecodesign and energy label measures for household tumble dryers have been effective from July 1, 2025, banning non-heat-pump dryers and projecting cumulative energy savings of 15 TWh and 1.7 Mt CO₂eq by 2040, which reshapes SKU portfolios toward efficient designs[3]European Commission, “New measures for more energy efficient household tumble dryers from 1 July,” European Commission, energy.ec.europa.eu. The A–G rescaled energy labels are now the standard and make efficiency differences visible at the point of sale, which accelerates conversion to top-class models in most EU markets. These rules complement national subsidy programs and utility incentives that improve household payback periods for efficient appliances, which support replacement demand in high-tariff markets. As a result, the Europe small home appliances market continues to benefit from policy-driven upgrades and clearer consumer information on the shelf and online.

Appliance Subscription and Rental Models

Subscription and rental models are building a presence as consumers seek flexibility and lower upfront costs for premium products, which can improve lifetime value for suppliers when retention exceeds two to three years. Leading brands are preparing pan-European subscription offerings that link connected devices to predictive maintenance, which reduces downtime and service costs versus non-connected fleets. Integration with smart-home ecosystems such as SmartThings allows remote diagnostics and energy optimization that become part of the subscription value proposition for households that value convenience. The Right to Repair framework reinforces rental economics by requiring fair access to spare parts and repairs over multiple years, which lowers refurbishment costs for fleet operators and extends product life. By improving affordability and serviceability, these models expand access to higher-end features for renters, students, or mobile workers and widen the addressable base for the Europe small home appliances market.

AI-Powered Food-Waste Reduction Functions

Commercial kitchen deployments show that AI-enabled waste monitoring can meaningfully reduce food waste and procurement costs, and consumer versions are beginning to adapt those functions. Peer-reviewed evidence from hospitality use cases indicates significant waste reductions and cost savings, which demonstrates a performance baseline for household adaptation once the cost structure aligns. Consumer-grade smart appliances package internal cameras, on-device AI, and app-based recommendations to manage expiration dates and cooking choices, though initial premiums remain material relative to conventional models. Compact form factors that solve single tasks, such as efficient boiling or guided portioning, help buyers perceive clear payback, which shortens adoption cycles in price-sensitive segments. Policy targets to cut household food waste by 2030 can support future subsidy designs and nudge features into mainstream price points, which would expand addressability within the Europe small home appliances market. As brands blend AI with energy-saving modes, feature sets that deliver measurable utility are likely to sustain willingness to pay.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost volatility | -0.7% | EU-wide manufacturing base; Germany and Italy exposed | Short term (≤ 2 years) |

| Data privacy and cybersecurity concerns | -0.3% | Germany, Netherlands; EU-wide CRA and RED | Long term (≥ 4 years) |

| Regulatory push for right-to-repair inflating warranty costs | -0.5% | France early; EU27 by July 2026 | Medium term (2-4 years) |

| Emerging second-hand marketplaces are cannibalizing new sales | -0.4% | United Kingdom large scale; Germany, Netherlands growing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Concerns

The EU Cyber Resilience Act creates a single framework for cybersecurity in connected products, with fines up to EUR 15 million (USD 16.2 million) or 2.5% of global turnover for serious violations, which raises engineering and compliance costs for smart appliances. Wireless devices sold in the EU must also meet Radio Equipment Directive cybersecurity rules, including protections for personal data and authentication safeguards, which expand testing and certification steps before market entry. Insurer-linked programs that reduce premiums in exchange for real-time device data are emerging, but many households hesitate to share sensor streams, which slows opt-in for connected features that could otherwise grow faster. Brands now highlight on-device processing and privacy-by-design to reassure buyers and avoid adoption barriers in privacy-conscious markets. Over time, security maturity and transparent data policies can convert privacy risk into a differentiator, but in the near term, these obligations temper the speed of connected adoption in the Europe small home appliances market.

Regulatory Push for Right-to-Repair Inflating Warranty Costs

The EU Right to Repair Directive requires manufacturers to repair covered products at reasonable prices for several years after purchase and extends the legal guarantee by 12 months when goods are repaired within the guarantee period, which increases after-sales obligations and reserves. The framework also discourages parts pairing and similar restrictions, which pushes design toward modularity and standardized interfaces that can add unit costs for small appliances. National implementations such as Spain’s long parts-availability timelines and France’s repairability index add layers that extend product lifecycles and shift demand toward repair rather than replacement for durable models. For suppliers with established European service networks, these rules can create barriers to entry and advantage scale, while also compressing accessory and replacement-driven revenue in some categories. In the short run, the additional costs can weigh on prices and promotions, while in the medium term the Europe small home appliances market adapts through design changes, service partnerships, and circular programs that fit the new rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Air Fryers Propel Health-Centric Shift

Coffee makers accounted for 18.92% of category revenue in 2025, the largest product share in the Europe small home appliances market. At the same time, air fryers are the fastest-growing product with a 2.93% CAGR through 2031, underpinned by app-enabled recipes and dual-zone designs now available below EUR 150 (USD 162). Feature innovation concentrates on multi-functionality to justify mid-tier pricing, including dual-basket platforms and guided cooking that compress learning curves for new users. As average selling prices rise and consumers shift to larger capacities, value growth outpaces unit growth, which sustains the contribution to the Europe small home appliances market. Premium small appliances continue to expand at the top end as brands invest in aesthetics and automation, for example, high-end hair care and top-spec coffee equipment that target affluent households willing to pay for performance and design.

Vacuum cleaners remain a core family as robotics evolves from convenience to automation through self-maintenance and AI-based object recognition, which supports higher prices. Robot vacuum platforms with docking systems that wash and dry mops and empty dustbins extend intervals between user interventions, which shifts demand toward integrated stations priced well above entry-level models. Mature categories such as kettles, toasters, and blenders show slower growth due to high penetration and longer replacement cycles, while brands reposition for premium subsegments that deliver higher margins and more differentiated use cases. As Chinese entrants target budget tiers with connected features, European incumbents respond by pushing upmarket and leveraging service, repairability, and brand trust to defend share within the Europe small home appliances industry. The net effect is a polarized product landscape where mid-range innovation drives volume while high-end feature sets and materials sustain price ladders across categories.

By Distribution Channel: Omnichannel Blurs Traditional Boundaries

Multi-brand stores held 48.51% of 2025 distribution, reflecting the role of showroom experiences and assisted selling for complex products and bundled add-ons. Flagship and gallery formats from leading manufacturers allow shoppers to test interoperability and see predictive maintenance interfaces before purchase, which sustains conversion even when much of the research occurs online. Retailers increasingly deploy in-store digital catalogs and kiosks that connect to extended online assortments with home delivery, which blurs attribution between offline and online sales but keeps the full assortment accessible on-site. This omnichannel model fits the Europe small home appliances market, where shoppers value hands-on evaluation yet complete purchases through whichever channel offers speed, price, or availability advantages.

Online channels deliver the fastest growth at a projected 3.63% CAGR through 2031, lifted by convenience, rapid delivery options, verified reviews, and better price transparency across borders. The United Kingdom sets the tone with very high pre-purchase digital engagement that influences product discovery and brand comparison at scale, while the Nordics convert high device usage into digital purchasing habits. Exclusive brand outlets serve premium buyers who seek specialist advice, but their share remains niche relative to the broader base of shoppers who prefer multi-brand choice or online convenience. As subscriptions and rentals expand, they add a new route that ties products to service outcomes, which complements retail channels and widens access within the Europe small home appliances industry.

By Technology: Matter Protocol Unlocks Smart Adoption

Conventional technology accounted for 75.33% of revenue in 2025 and remains the default choice for cost-focused households, landlords, and senior consumers who prefer straightforward operation and lower upfront prices. This segment benefits from ubiquity and familiarity, especially in rentals where simple appliances help avoid connectivity issues and support requests. The Europe small home appliances market continues to see steady conventional demand even as connected features diffuse, since many tasks do not require connectivity for clear user value. Over time, energy efficiency and durability improvements flow into conventional lines as policy and competition improve baseline specifications.

Smart or connected small appliances are projected to grow at a 3.27% CAGR as Matter interoperability matures and reduces ecosystem lock-in, which removes a major adoption barrier present during earlier smart-home cycles. BSH began shipping Matter-enabled cooling lines in 2025, and other brands are rolling out connected portfolios for vacuum cleaning, cooking, and small kitchen appliances across Europe. Haier Europe’s hOn platform surpassed 10 million connected users, which signals the scale now reachable for appliance-linked services and energy features in the region. Regulatory cybersecurity requirements under the RED and Cyber Resilience Act add costs and testing steps but also raise trust in connected devices, which helps sustain adoption across the Europe small home appliances market. Brands now emphasize on-device processing and security provenance as differentiators, which aligns connected innovation with the region’s privacy expectations.

Geography Analysis

Germany accounted for a 19.73% share of the Europe small home appliances market size in 2025, reflecting its scale and the energy-efficiency case for replacing older models. Urban households with limited space prefer compact and multi-function formats that combine performance and small footprints, which support categories like air-fryer ovens and premium coffee makers. Germany’s policy framework and the EU’s rescaled A–G energy labels influence buyer choices toward efficient models and away from legacy classes, especially for appliances with meaningful energy footprints. Product launches that feature interoperability and energy-saving modes typically start in Germany and roll through major EU markets, which accelerates the feedback loop between innovation and adoption. Brands in the mid-price tier have grown quickly by combining feature parity with affordable pricing, which captures households that want smart functions without premium pricing.

The Nordics post the fastest projected growth with a 3.18% CAGR through 2031, supported by high device penetration and digital shopping habits that make discovery and adoption of connected appliances easier. Sweden’s high online shopping frequency and Denmark’s high device connectivity form a favorable context for smart and energy-aware products that can link to tariffs and usage data. Nordic buyers emphasize sustainability and warranty length, which supports brands that can document durability, repairability, and lifecycle support under EU rules that increasingly value circular design. Robotic vacuum penetration is high in the region and leads to adoption in small appliance connectivity, which favors rapid iteration of AI-based navigation and maintenance features. The region’s digital acceleration and premium inclinations make it a proving ground for connected small appliances in the Europe small home appliances market.

The United Kingdom remains an important European market where remote and hybrid work patterns since 2024 have lifted in-home usage of small appliances, which supports shorter replacement cycles in specific categories. Air fryers continue to gain share due to health and energy considerations, and seasonal events like Black Friday trigger sharp volume spikes that pull adoption forward. France, Italy, and Spain jointly account for a sizable share of regional demand with divergent policy and enforcement contexts that shape energy class mix and spare parts practices. Italy’s use of strong incentives for efficiency upgrades supports above-average growth among Western European markets, while Spain’s parts availability obligations reinforce the region’s circular design direction. BENELUX favors premiumization due to affluent consumers and sustainability preferences, and Central-Eastern Europe benefits from income convergence that lifts volume in mid-tier lines. Across Europe, regulation, digital habits, and disposable income trends combine to set a steady growth path for the Europe small home appliances market.

Competitive Landscape

The Europe small home appliances market is moderately fragmented, with no single brand dominant across all categories, and share leadership varies by product and price tier. European incumbents such as BSH, Groupe SEB, Electrolux, De’Longhi, and Dyson rely on brand equity, service networks, and early adoption of interoperability standards to defend premium positions that emphasize repairability and long-term support[4]BSH Hausgeräte GmbH, “BSH increases turnover to 15.3 billion euros in 2024,” BSH, press.bsh-group.com. Asian challengers, including SharkNinja, Midea, Xiaomi, Samsung, and ECOVACS, expand by offering strong functionality at competitive prices and by moving fast on new formats and SKUs. M&A and partnerships broaden portfolios and strengthen local capabilities, which intensifies competition and compresses time-to-market for new features.

Strategic moves are concentrated in three themes. First, interoperability and AI-led experiences are now core roadmap items for leading brands, as shown by BSH’s Matter-enabled launches and Samsung’s AI device lineup that links performance, energy savings, and app ecosystems. Second, circularity and right-to-repair requirements drive investment in refurbishment programs and parts logistics, which entrenches service moats for brands with European networks. Third, subscription-ready offerings and rental pilots open recurring-revenue models that can produce higher lifetime value in connected categories underpinned by diagnostics and remote support. These moves collectively raise the innovation bar while keeping regulatory fit central to product and service design for the Europe small home appliances market.

Company examples underline the pace of change. Midea’s acquisition of Teka adds strong European brands and channel access to complement scaled manufacturing, improving its product pyramid from entry to premium. SharkNinja reported European net sales above USD 1.7 billion in 2024 and is accelerating local presence to support growth in mid-priced categories like air fryers and floor care. Groupe SEB began a multi-year program to restore profitable growth by 2027 through recurring savings and higher investment in innovation and AI, aiming to balance price pressure with product differentiation. Dyson continues to push premium device miniaturization and AI features across vacuum, air, and hair care lines, which anchors its design-led positioning. Together, these moves demonstrate how product innovation, compliance leadership, and channel execution shape competitive outcomes across the European small home appliances market.

Europe Small Home Appliances Industry Leaders

Groupe SEB

BSH Hausgeräte GmbH

Koninklijke Philips N.V.

De'Longhi S.p.A.

Dyson Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Electrolux Group announced the division of its Business Area Europe, Asia-Pacific, Middle East, and Africa into separate Region EMEA and Region APAC structures effective 2025 to strengthen regional capabilities and customer focus.

- September 2025: BSH Home Appliances Group and ECOVACS Group announced a strategic partnership to develop innovative solutions for integrated floor cleaning, specifically robotic vacuum cleaners, presenting the world's first built-in vacuum and mopping robot that disappears invisibly behind the kitchen front at IFA 2025, combining BSH's European market presence with ECOVACS's AI-driven robotics expertise.

- April 2025: Midea Group completed the acquisition of Teka Group (excluding Teka Rus LLC) for undisclosed terms, integrating the century-old German-founded brand specializing in household appliances like ovens, cooktops, sinks, and faucets to exponentially boost market penetration of its brands (Teka, Küppersbusch, Intra) across Europe, leveraging Midea's Fortune Global 500-ranked manufacturing scale and R&D capabilities.

- March 2025: Samsung Electronics unveiled its 2025 Bespoke AI Home Appliances lineup, including the Bespoke AI Jet Ultra cordless stick vacuum cleaner, claiming powerful suction with AI Cleaning Mode 2.0 that classifies cleaning environments to auto-adjust suction and brush speed, reducing battery power while extending runtime, shipping Europe-wide in Q2 2025.

Europe Small Home Appliances Market Report Scope

Small appliances, defined as portable kitchen devices designed for worktops, offer a greater variety compared to standard large appliances. They can be relocated or stored to optimize space and significantly impact kitchen aesthetics, making design a key consideration for consumers. Unlike large appliances, their necessity varies by household, reflecting diverse preferences. Consequently, the appearance of small appliances influences purchasing decisions, as they contribute to both functionality and the overall ambiance of the kitchen environment.

The Europe Small Home Appliances Market Report is segmented by product type (coffee makers, food processors, grills & toasters, electric kettles, juicers & blenders, air fryers, vacuum cleaners, electric rice cookers, other small home appliances), distribution channel (multi-brand stores, exclusive brand outlets, online, other distribution channels), technology (conventional, smart/connected), and geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The market forecasts are provided in terms of value (USD).

By Product Type

| Coffee Makers |

| Food Processors |

| Grills & Toasters |

| Electric Kettles |

| Juicers & Blenders |

| Air Fryers |

| Vacuum Cleaners |

| Electric Rice Cookers |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Technology

| Conventional |

| Smart / Connected |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product Type | Coffee Makers |

| Food Processors | |

| Grills & Toasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Other Small Home Appliances | |

| By Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Technology | Conventional |

| Smart / Connected | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the European small home appliances market?

The European small home appliances market is estimated to reach USD 22.94 billion in 2026 and is forecast to reach USD 26.12 billion by 2031 at a 2.63% CAGR.

Which product category leads and which grows the fastest in Europe?

Coffee makers lead with 18.92% revenue share in 2025, while air fryers are the fastest-growing product with a 2.93% CAGR through 2031.

Which channels and technologies are shaping demand most?

Multi-brand stores lead with 48.51% share in 2025, while online delivers the fastest growth, and conventional technology holds 75.33% share as smart or connected appliances grow at 3.27% CAGR.

Which countries or regions in Europe stand out?

Germany leads with a 19.73% share in 2025, and the Nordics post the fastest growth with a 3.18% CAGR through 2031.

How are EU regulations influencing product design and sales?

ESPR, energy label rescaling, the tumble dryer update, and the Right to Repair Directive push durability, efficiency, repairability, and cybersecurity, which favor efficient and connected designs and drive replacement and service innovation.

Where are companies focusing on competing effectively?

Key moves include Matter-enabled interoperability, AI-powered features, circular programs for refurbishment and repair, and subscription-ready offerings that link devices to diagnostics and energy features.

Page last updated on: