Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

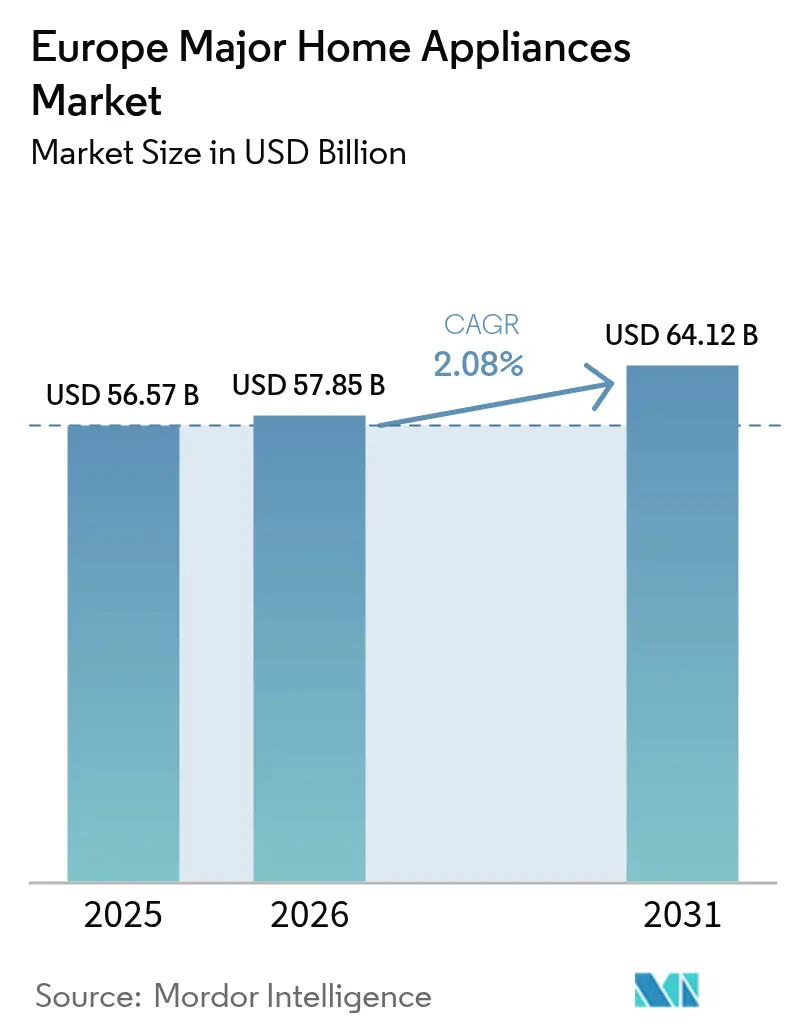

| Base Year Market Size (2025) | USD 56.57 Billion |

| Market Size (2026) | USD 57.85 Billion |

| Market Size (2031) | USD 64.12 Billion |

| Growth Rate (2026 - 2031) | 2.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Major Home Appliances Market Analysis by Mordor Intelligence

The Europe major home appliances market size is projected to be USD 56.57 billion in 2025, USD 57.85 billion in 2026, and reach USD 64.12 billion by 2031, growing at a CAGR of 2.08% from 2026 to 2031. Energy-efficiency regulation is compressing replacement windows, with the EU energy label rescale and tighter Ecodesign thresholds accelerating A-class adoption across core categories in early-adopter markets[1]European Commission, “EU Energy Labelling and Ecodesign,” European Commission, europa.eu. Electrification policies and gas phase-out mandates in several member states are redirecting spending toward induction cooktops and premium built-ins, while Spain leads forecast growth on the back of Green Deal co-financing and sustained heatwave-driven demand for efficient cooling. Connectivity is becoming a practical differentiator as Matter-certified appliances remove gateway friction and integrate with dynamic tariffs, which aligns with demand-response programs rolling out under national smart-meter plans. Compliance obligations from the EU Cyber Resilience Act and the Carbon Border Adjustment Mechanism raise lifecycle and material costs, reinforcing a shift toward higher-value segments where software, energy optimization, and circular design support defensible margins.

Key Report Takeaways

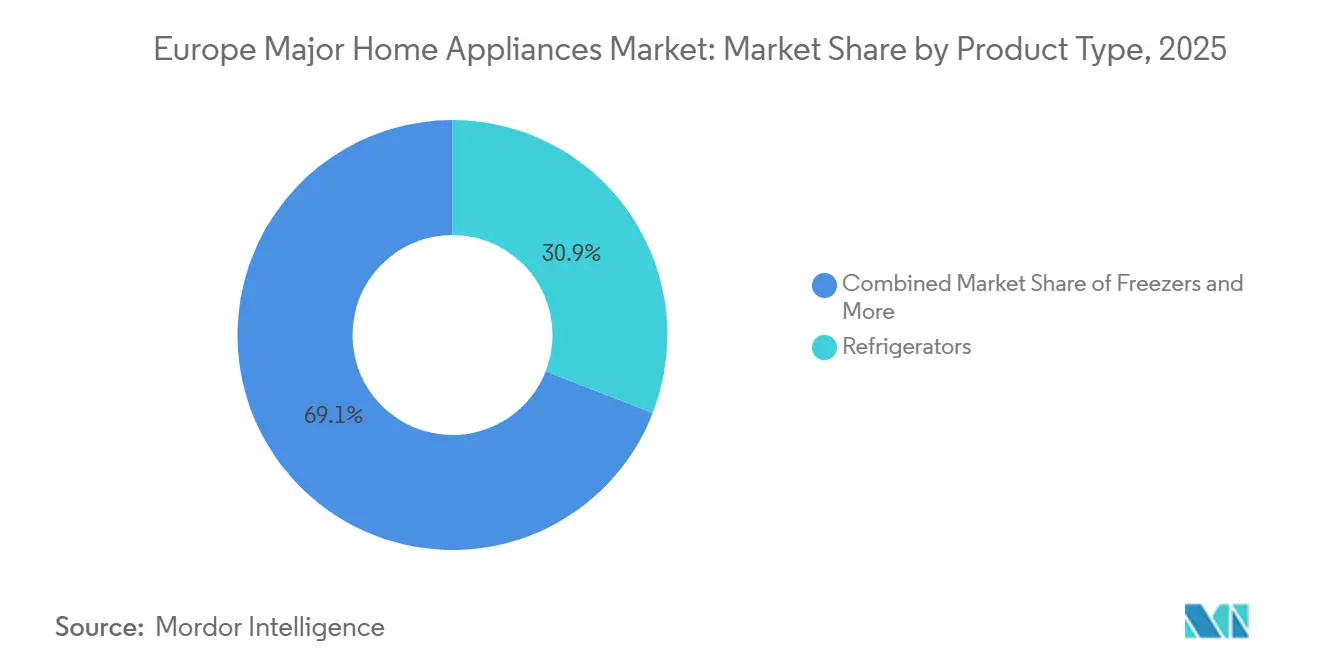

- By product type, refrigerators led with 30.96% revenue share in 2025, while microwave ovens are projected to expand at a 2.15% CAGR through 2031.

- By distribution channel, multi-brand stores accounted for 45.78% of sales in 2025, while online channels recorded the highest projected CAGR at 3.12% through 2031.

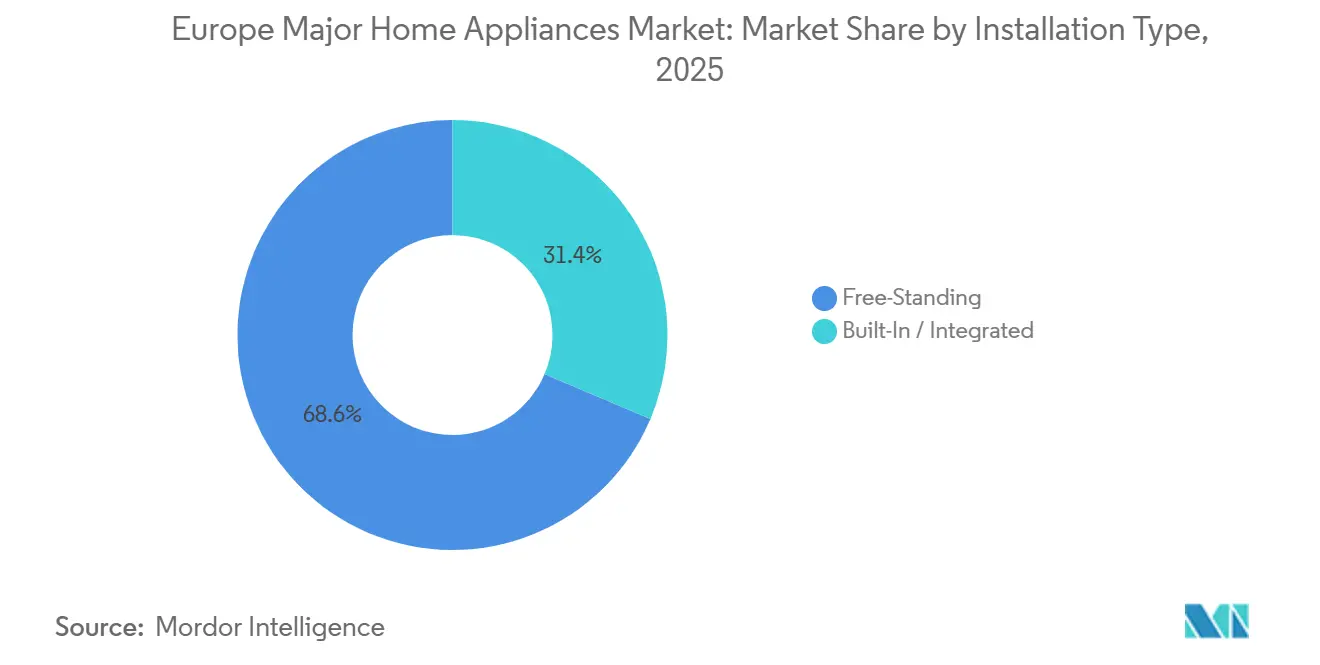

- By installation type, free-standing appliances held 68.62% of the 2025 volume, while built-in or integrated units are forecast to grow at a 2.62% CAGR to 2031.

- By technology, conventional appliances retained 83.92% of 2025 volume, while smart connected alternatives are projected to advance at a 3.41% CAGR through 2031.

- By geography, Germany held 24.05% of 2025 revenue, while Spain is forecast to post the fastest national CAGR at 3.74% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU energy label rescales, and tighter Ecodesign rules accelerate the replacement of legacy appliances | +0.6% | Germany, France, the Nordics, with spill-over to Southern Europe | Medium term (2-4 years) |

| Electrification and gas phase-out in new buildings lift induction/cooktops and built-in demand | +0.5% | Netherlands, Germany, France, Spain | Medium term (2-4 years) |

| E-commerce maturity with stable, high online penetration sustains omnichannel major-appliance sales | +0.3% | United Kingdom, Nordics, BENELUX, expanding in Southern Europe | Short term (≤ 2 years) |

| Smart/connected attach rates rise on interoperability and demand-side programs | +0.4% | Germany, France, United Kingdom, Nordics, with broader EU rollout | Medium term (2-4 years) |

| Digital Product Passports (ESPR) push lifecycle data, favoring connected platforms | +0.3% | Pan-European from 2026-2027 with early adoption in Germany, the Netherlands, and France | Medium term (2-4 years) |

| Dynamic tariffs/demand response adoption shifts laundry and dish cycles to smart MDAs | +0.2% | Germany, Sweden, and Spain, with an EU-wide smart-meter rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Energy Label Rescale and Tighter Ecodesign Rules Accelerate Replacement of Legacy Appliances

The EU energy label rescale that returned categories to an A to G scale, combined with tighter Ecodesign thresholds phased in through 2025, has nudged households to replace older units earlier than planned as the performance gap becomes clearer at the point of sale. In France, the share of A-rated dishwashers rose from 6% of volume in 2024 to 11% in 2025 as consumers targeted models with about 45% lower energy consumption than E-rated alternatives amid elevated electricity bills. In Germany, ZVEI reported a 2024 washing-machine unit uplift as households traded in 11 to 15-year-old models for newer designs that still deliver double-digit efficiency gains even at mid-tier ratings. Brands have repositioned around verified efficiency and lower embedded emissions, with domestic manufacturing and low-CO₂ materials featuring prominently in new lines to align with consumer preferences and procurement criteria[2]BSH Group, “Sustainability and Low-CO₂ Manufacturing Initiatives,” BSH Group, bsh-group.com. The Ecodesign for Sustainable Products Regulation will add Digital Product Passports to washing machines, dishwashers, and dryers from 2026 to 2027, which will favor models that disclose lifecycle data and support circular practices across repairs and take-back. Together, these policy shifts reinforce price-to-performance value for efficient appliances, which supports premium attach in categories with high energy savings over the ownership period.

Electrification And Gas Phase-Out in New Buildings Lift Induction Cooktops and Built-In Demand

Gas restrictions and electrification mandates are changing kitchen specifications in Northwestern Europe and beyond, boosting induction hobs and coordinated built-in suites as developers and renovators move to all-electric configurations[3]International Energy Agency, “Electrification of Heating and Cooking in Europe,” International Energy Agency, iea.org. The Netherlands enforces a nationwide gas-boiler ban from 2026, while Germany’s Buildings Energy Act steers heating and, by extension, kitchen systems toward renewable energy alignment to simplify compliance and permitting. France tightened its RE2020 requirements for collective housing in 2025, and guidance favors electric solutions that help meet stricter carbon-intensity thresholds in new builds. Induction’s thermal efficiency advantage over gas makes the operating cost case more compelling as retail energy-price ratios converge, which supports upgrades in both residential and hospitality settings as subsidy-linked retrofits scale. Installer partnerships and point-of-sale financing are extending from heating to kitchen electrification projects, creating coordinated upgrade paths that attach high-efficiency cooktops to broader home energy packages. These dynamics sustain a steady premium mix shift in cooking that complements high-end refrigeration and dish solutions integrated into modern kitchen designs.

Smart Connected Attach Rates Rise on Interoperability and Demand-Side Programs

Interoperability has moved from a promise to a product reality as Matter-certified models connect across Apple, Google, Amazon, and Samsung ecosystems without hubs, reducing friction and increasing the appeal of smart white goods. The CSA-IOT roadmap has expanded the certified device base, while national policies on dynamic tariffs and smart-meter rollout create practical use cases such as time-of-use scheduling for laundry and dishwashing. In France, connected penetration increased through 2025 across cooling and cooking, reflecting rising interest in energy dashboards, remote diagnostics, and features that coordinate around household routines. Sweden’s widespread adoption of dynamic hourly contracts has demonstrated significant bill savings when households shift cycles to off-peak windows, and this experience is informing utility incentives in other EU states. OpenADR’s latest specification integrates with widely used IoT protocols, positioning smart appliances as demand-response endpoints as grid operators scale flexibility programs throughout the decade. OEM platforms that quantify consumption and automate load shifting are converting usage data into service revenue and retention, which supports margins in premium lines that anchor the Europe major home appliances market.

Digital Product Passports ESPR Push Lifecycle Data Favoring Connected Platforms

The Ecodesign for Sustainable Products Regulation introduces Digital Product Passports for washing machines, dishwashers, and dryers between 2026 and 2027, embedding material composition, recycled content, repairability, spare-part timelines, and disassembly guidance into product data accessible via QR codes. Battery Passport implementation has provided a template for attribute depth and traceability, and its approach to state-of-health and supply-chain diligence is informing appliance-sector data schemas. Corporate sustainability reporting and public procurement frameworks are already encouraging DPP-ready products in B2B tenders across hospitality and real estate, which pulls connected and modular designs into shortlists. The Critical Raw Materials Act will extend disclosures to permanent magnets used in large home appliances in 2027, creating another data field that supports circular recovery and design for disassembly. OEMs that publish disassembly manuals, part availability, and modular certifications gain visibility advantages on retail platforms that score repairability and lifetime support, strengthening conversion in ESG-conscious segments. Connected platforms can capture and update DPP data natively through firmware and cloud logs, which lowers compliance friction relative to conventional SKUs and adds a modest growth tailwind for higher-spec models within the Europe major home appliances market.

Restraints Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-of-living pressures and elongated replacement cycles mute discretionary upgrades | -0.5% | Pan-European, acute in Italy, France, Spain | Short term (≤ 2 years) |

| Weak housing starts/renovation delays hit built-in/integrated categories | -0.4% | Germany, France, Italy | Medium term (2-4 years) |

| Cyber Resilience Act compliance raises cost/complexity for connected appliances | -0.2% | Pan-European from December 2027 | Medium term (2-4 years) |

| CBAM-driven steel/aluminum cost pass-through pressures margins | -0.3% | Pan-European with downstream exposure post-2028 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-of-Living Pressures and Elongated Replacement Cycles Mute Discretionary Upgrades

Inflation shocks from 2022 to 2024 reduced discretionary budgets and extended appliance replacement intervals, which constrained short-term upgrade cycles for big-ticket categories. In France, durable-goods spending growth lagged energy costs through 2023, reflecting tighter consumer wallets and a heightened focus on basic efficiency over premium extras. Spanish proximity retailers reported that most households still purchased an appliance in 2024, yet average tickets declined as shoppers traded down in specifications and sought promotions, which compressed value growth even when volumes held up. The housing cycle added further drag, with mortgage rates and project cost inflation delaying kitchen renovations across several large markets and shifting purchases toward essential replacements. Industry data also showed that European unit demand in 2024 was below recent peaks, and consumers’ greater willingness to repair within warranty windows moderated the pace of new-unit adoption. Premium brands responded by extending warranty propositions and promoting long-life components, which supports confidence but also stretches replacement intervals in a price-sensitive environment.

Weak Housing Starts Renovation Delays Hit Built-In Integrated Categories

Residential completions across Europe fell to multiyear lows in 2025, with the sharpest declines in Germany, reducing the installation base for built-in kitchens and the coordinated suites that typically attach to new housing supply. Built-in’s exposure is magnified because a high share of purchases coincides with new construction or major remodels, so delays in permits and projects directly ripple into slower category turns even when free-standing demand is steady. France’s built-in segment softened in 2025 amid political uncertainty and sluggish housing starts, which weighed on cooking and refrigeration. Germany’s built-in volumes showed limited resilience on the strength of replacements in existing stock, but the gains were modest versus the levels achieved during prior housing upcycles when completions were materially higher. Across Italy and nearby markets, developers and homeowners faced higher labor and input costs that pushed some renovation plans to later years, compressing near-term throughput for integrated formats. Although policy initiatives such as the Energy Performance of Buildings Directive point to a stronger pipeline later in the decade, the timing and national execution will shape how quickly built-in demand normalizes for the Europe major home appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refrigerators Anchor Share, Microwaves Lead Growth on Compact Innovation

Refrigerators captured 30.96% of the Europe major home appliances market share in 2025, reflecting their non-discretionary status and steady replacement cadence within multi-appliance households. Premium refrigerators added momentum with larger formats and food-management features that reduce waste and sharpen energy performance, which strengthens the category’s role as a value anchor in coordinated kitchen upgrades. The Europe major home appliances market continues to see brands invest in connected cold appliances that integrate vision systems and inventory tools, which aligns with consumer interest in convenience and operating-cost control[4]Samsung Electronics, “Refrigeration and Connected Feature Innovations,” Samsung, samsung.com. Dishwasher upgrades in France and washing-machine replacements in Germany during 2024 to 2025 also signaled a broader energy-efficiency pivot that supports premium attachment across refrigeration lines in multi-brand kitchen solutions as sustainability metrics influence household choices and public procurement, refrigerator lines that publish lifecycle and repairability data gain shelf visibility online and in-store, creating a soft pull for models that bundle transparency with lower total cost of ownership.

Microwave ovens are the fastest-growing product line, with a 2.15% CAGR projected through 2031 for the Europe major home appliances market size as compact combination models replace traditional ovens in space-constrained urban homes. Multifunctional designs that blend microwave, convection, and steam functions address urban kitchen layouts and support energy savings for small-batch cooking, which reinforces the uptake beyond entry-level tiers. Washing machines benefited from sustained upgrades to higher-efficiency classes and the rollout of AI features that tune water and detergent usage, which improved perceived value during a period of cautious spending. Dishwashers gained share where right-to-repair and repairability indices are visible to consumers at the point of sale, and smart scheduling features that align with time-of-use tariffs further strengthened conversion in early dynamic-tariff markets. Induction cooktops continued to take share from gas in markets with electrification policies, and hobs with integrated extraction added design-led appeal in open-plan renovations, supporting the premium segment of the Europe major home appliances market.

By Distribution Channel: Multi-Brand Stores Leverage Expertise, Online Gains on Logistics Innovation

Multi-brand stores accounted for 45.78% of sales in 2025, supported by in-store advisory and coordinated installation that simplifies complex purchases such as built-in kitchens. Demonstration zones, hands-on evaluation, and installation planning underpin attachment rates across premium lines, which helps physical retail sustain influence within the Europe major home appliances market even as digital discovery rises. Retailers that invest in marketplace operations and augmented visualization tools have expanded reach and improved conversion for suite-based bundles, with Spain’s largest specialist chain citing online marketplace transactions as a meaningful share of its digital mix in 2025. Trade-in and refurbishment programs linked to major store networks are also helping value-focused consumers manage budgets, which supports a circular channel that complements new-unit turnover.

Online channels are projected to grow at a 3.12% CAGR to 2031 within the Europe major home appliances market as logistics networks standardize white-glove delivery and retailers narrow delivery windows across borders. Search for algorithms on leading platforms now surface repairability and part-availability signals that reward OEMs publishing disassembly and service information, which aligns with ESPR-driven transparency and boosts conversion for modular designs. Payment options such as buy-now-pay-later ease the premium gap between A-class and legacy classes, which supports upgrades where running-cost savings are salient in household budgets. Data feedback from online service interactions allows OEMs to refine designs and cut warranty incidents over successive cycles, which sustains margins in segments that monetize predictive maintenance and energy coaching features.

By Installation Type: Free-Standing Dominates, Built-In Premiumizes Despite Weak New-Build

Free-standing appliances held 68.62% of 2025 volume as households favored lower upfront costs and simpler installation, which remains decisive for renters and secondary-home buyers across key geographies. Price transparency online keeps pressure on free-standing lines, and aggressive promotions from challengers with extended warranties stimulate value-tier competition inside the Europe major home appliances market. Manufacturers continue to refresh free-standing models with updated Eco programs and noise-reduction improvements, signaling that even non-connected lines must demonstrate measurable benefits to defend share. As ESPR and DPP timelines approach, brands are extending documentation and parts availability to free-standing models, which helps sustain resale value and reduce barriers to purchase for budget-conscious buyers.

Built-in or integrated appliances are projected to grow at a 2.62% CAGR through 2031 for the Europe major home appliances market size as premium kitchen renovations proceed in resilient customer segments. Germany’s built-in category showed replacement-led gains even as new-build construction dropped to the lowest levels since 2015, highlighting the importance of upgrades in existing stock. In France, built-in experienced a pause during 2025 due to policy uncertainty and soft housing starts, yet integrated hobs with downdraft extraction continued to serve design-led urban projects. As DPP requirements take hold, integrated models that surface lifecycle, repairability, and recycled content data should maintain visibility in commercial projects and affluent residential purchases across the Europe major home appliances industry.

By Technology: Conventional Holds Volume, Smart Connected Surges on Matter and Demand-Response

Conventional appliances retained 83.92% of 2025 volume, reflecting price sensitivity and the prioritization of basic functionality in entry and mid tiers. Manufacturers apply platform strategies across brands and trims to lower cost and integrate standard Eco programs, which sustains competitiveness while energy classes improve under Ecodesign. Value-conscious buyers still emphasize upfront price, but policy-driven attention to efficiency and repairability is broadening the appeal of models that show lower lifetime cost even without connectivity. The Europe major home appliances market continues to blend conventional units with targeted smart features in upper trims where measurable savings and convenience appeal justify premiums.

Smart connected appliances are projected to grow at a 3.41% CAGR through 2031 as Matter certification enables cross-brand operation and simplifies setup for households with mixed ecosystems. France’s connected penetration rose through 2025 in both cooling and cooking, helped by clear value communication and features such as remote diagnostics, consumable tracking, and guided programs. Germany mandated dynamic tariffs for large suppliers and set ambitious smart-meter milestones, which create a favorable backdrop for automated scheduling and utility-linked incentives. Sweden’s widespread dynamic-tariff adoption illustrates the savings potential when cycles move to off-peak periods, and this experience is guiding broader EU demand-response programs where open standards like OpenADR integrate with home platforms. OEM cloud dashboards now reduce service calls through predictive maintenance and convert energy insights into subscription revenue, which supports premium-line margins and strengthens retention in the Europe major home appliances market. Regulatory alignment, including the EU Code of Conduct for Energy Smart Appliances and the Cyber Resilience Act, is standardizing interoperability and security update windows, which moves connectivity from novelty to requirement in selected buyer segments.

Geography Analysis

Germany held 24.05% of the Europe major home appliances market share in 2025, supported by a large addressable base and strong brand preferences in premium lines despite a housing slump that constrained built-in demand. Unit growth in washing machines and dishwashers during 2024 reflected a tilt toward efficient replacements in existing housing stock as households prioritized lower operating costs. Dynamic-tariff mandates and accelerating smart-meter rollout have created a favorable framework for automated scheduling of laundry and dish cycles, which reinforces the value of connected features in upper trims. Traditional retail remains important, but omnichannel experiences are expanding as large specialists enhance digital tools to capture research-online and buy-in-store behaviors. These patterns underscore how efficiency policy and pricing signals guide product mix even when macro headwinds dampen overall spending in the Europe major home appliances market.

Spain is projected to deliver the fastest national CAGR at 3.74% to 2031 as electrification programs and tourism-linked retrofits support kitchen upgrades and efficient cooling. Heatwaves elevated awareness of inverter-driven cooling solutions and smart thermostats, while Green Deal-linked co-financing supported appliance packages that attach to solar deployments in coastal hospitality hubs. The leading specialist retailer reported higher revenue in 2025 with growth attributed to marketplace expansion and in-store digital tools that visualize coordinated suites, highlighting how omnichannel design improves attachment and conversion in Spain. The proximity channel also grew and maintained a significant share with thousands of points of sale, which indicates that service and installation convenience carry weight even as online options mature. Overall, Spain’s alignment of policy tailwinds and retailer capability is a distinct bright spot within the Europe major home appliances market.

France recorded a 2025 contraction in large appliances by value as political uncertainty and a slow housing pipeline delayed built-in projects, although several small-appliance niches expanded on convenience and wellness trends. Efficiency consciousness continued to rise, and A-rated dishwasher sales more than doubled their share year over year, which demonstrates sustained interest in lower running costs and repairability at the category level. Elsewhere in Europe, the United Kingdom, BENELUX, and the Nordics contributed steady growth supported by mature e-commerce behaviors and high smart-meter penetration that enable demand-response features in connected appliances. Italy’s connected-home ecosystem expanded in 2025, yet per-capita spending remained below the EU average, suggesting a runway for connected white goods as user education and interoperability improve. Across the Rest of Europe, rising incomes and the spread of modern retail formats are improving access and financing options, which support first-time purchases and upgrades as retailers extend services across new metro areas.

Competitive Landscape

The Europe major home appliances market features a moderately consolidated set of leaders, with BSH Hausgeräte, Beko Europe, Electrolux Group, Haier Europe, and Miele together holding about 40% of revenue, while competition remains active across price tiers and channels. Asian challengers increase pressure by acquiring premium brands and supplying extended warranties at aggressive prices, which compresses entry and mid-tier margins and pushes incumbents toward software-backed differentiation. Incumbents are deepening platform capabilities that convert usage data into predictive maintenance and energy coaching, which adds recurring service revenue and raises switching costs in premium lines. These platform strategies work alongside regulatory alignment on interoperability and security, anchoring connected attach as a central lever for value creation within the Europe major home appliances market.

Strategic moves from 2024 to 2026 reshaped the supply base and compliance posture. Beko Europe launched as a joint venture combining extensive European manufacturing capacity and a large workforce, aiming for cost reduction and improved profitability across the region. Midea expanded its European footprint with the acquisition of a premium German brand parent, which strengthened its positioning in built-ins and widened its access to affluent segments. LG acquired Dutch platform Athom to accelerate cross-brand integration in its ThinQ ecosystem, and BSH released the first Matter-certified refrigerator globally, which demonstrated fast execution on interoperable smart-home standards. These bets connect directly to the regulatory arc under ESPR and the Cyber Resilience Act, which reward transparent lifecycle data and durable security update support.

Operational discipline and channel mix optimization are top priorities as input inflation and promotions stress profitability. Electrolux reported lower revenue for Q4 2025 and announced a 2026 reorganization to reduce complexity, citing persistent promotional intensity even as operating margins improved year over year. Specialist retailers are scaling omnichannel capabilities to meet coordinated-installation demand and monetize marketplace listings, while circular plays such as trade-in partnerships and refurbishment programs open new customer segments without cannibalizing premium lines. OEMs are also rebalancing production footprints and pursuing light-weighting in steel-intensive categories to cushion the effect of CBAM-related material costs, with early product redesigns already reducing metal content while maintaining performance targets. As CBAM phases in and CRA compliance deadlines approach, firms that integrate compliance with product value propositions are better positioned to defend margins in the Europe major home appliances market.

Europe Major Home Appliances Industry Leaders

BSH Hausgerate GmbH

AB Electrolux

Haier Europe (Candy/Hoover)

Miele & Cie. KG

Beko Europe B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Samsung Electronics Europe and Instacart unveiled AI Vision-enabled refrigerators that support in-app grocery ordering across France, Germany, and the United Kingdom.

- January 2026: Samsung Germany expanded its Certified Re-Newed program to France and the United Kingdom for flagship smartphones to strengthen refurbished propositions and brand reach.

- October 2025: Miele announced a 25-year motor warranty for washing machines and dryers sold in Germany, aligning with extended product-longevity commitments.

- January 2025: BSH Hausgeräte launched the Bosch Serie 100 refrigerator, the first globally certified Matter-enabled appliance compatible with major smart-home ecosystems.

Europe Major Home Appliances Market Report Scope

A complete background analysis of Europe's Major Home Appliances Market, which includes an assessment of the market dynamics, emerging trends in the segments and regional markets, and insights into various product and application types. Also, it analyses the key players and the competitive landscape in the Europe major home appliance market. Europe's Major Home Appliances Market is segmented by Product (Refrigerators, Freezers, Dishwashers, Clothes dryers, Washing Machines, Large Cooking Appliances, and Others), and by Distribution Channel (Supermarkets, Specialty Stores, Online, and Other Distribution Channels). The report offers market size and forecasts for Europe's major home appliances market in value (USD Million) for all the above segments.

By Product Type

| Refrigerators |

| Freezers |

| Washing Machines |

| Dishwashers |

| Cooktops & Ranges |

| Microwave Ovens |

| Air Conditioners |

| Others (Electric Hobs) |

By Distribution Channel

| Multi-Brand and Exclusive Brand Stores (EBOs) |

| Hypermarkets & Supermarkets |

| Online / E-commerce Platforms |

| Direct-to-Consumer (D2C) & Subscription Models |

By Installation Type

| Free-Standing |

| Built-In / Integrated |

By Technology

| Conventional Appliances |

| Smart / Connected Appliances |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Product Type | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Cooktops & Ranges | |

| Microwave Ovens | |

| Air Conditioners | |

| Others (Electric Hobs) | |

| By Distribution Channel | Multi-Brand and Exclusive Brand Stores (EBOs) |

| Hypermarkets & Supermarkets | |

| Online / E-commerce Platforms | |

| Direct-to-Consumer (D2C) & Subscription Models | |

| By Installation Type | Free-Standing |

| Built-In / Integrated | |

| By Technology | Conventional Appliances |

| Smart / Connected Appliances | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe major home appliances market?

The Europe major home appliances market size is valued at USD 57.85 billion in 2026, and reach USD 64.12 billion by 2031, growing at a CAGR of 2.08% from 2026 to 2031.

Which product categories are leading and growing fastest in the Europe major home appliances market?

Refrigerators led with 30.96% revenue share in 2025, while microwave ovens are projected to grow the fastest with a 2.15% CAGR through 2031.

How are regulations shaping demand in the Europe major home appliances market?

The EU energy label rescale and ESPR Digital Product Passports accelerate efficient replacements and favor connected platforms, while the Cyber Resilience Act and CBAM increase compliance and material costs that reinforce premiumization.

Which channels and installation types are gaining traction in the Europe major home appliances market?

Multi-brand stores led in 2025 due to advisory and installation services, while online is the fastest-growing channel; free-standing dominates volumes, and built-in is growing on premium kitchen renovations.

Where are the strongest geographic opportunities in the Europe major home appliances market?

Spain is projected to post the fastest national CAGR at 3.74% to 2031, supported by electrification programs and hospitality retrofits, while Germany remains the largest market by share at 24.05%.

How is connectivity changing the competitive playbook in the Europe major home appliances market?

Matter-certified appliances, dynamic tariffs, and demand-response integrations are driving smart adoption and enabling OEMs to monetize energy coaching and predictive maintenance, supporting premium-line margins and retention.

Page last updated on: