Europe Insurance Brokerage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

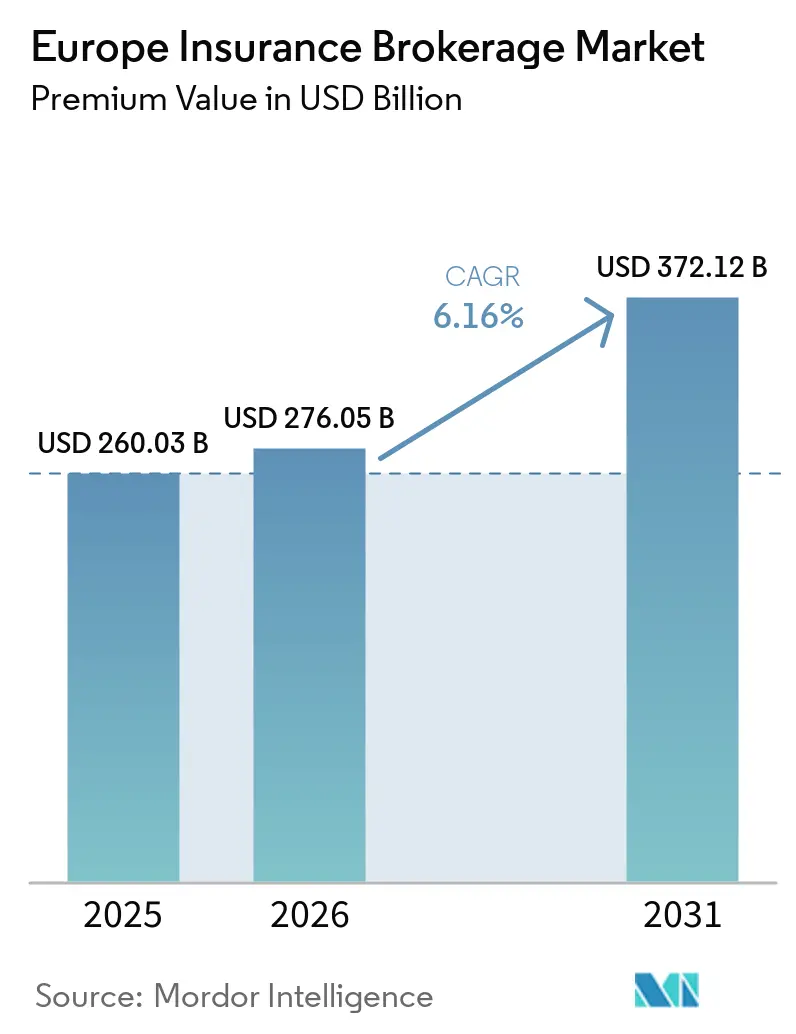

| Base Year Market Size (2025) | USD 260.03 Billion |

| Market Size (2026) | USD 276.05 Billion |

| Market Size (2031) | USD 372.12 Billion |

| Growth Rate (2026 - 2031) | 6.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Insurance Brokerage Market Analysis by Mordor Intelligence

The Europe Insurance Brokerage Market size in terms of premium value is projected to expand from USD 260.03 billion in 2025 and USD 276.05 billion in 2026 to USD 372.12 billion by 2031, registering a CAGR of 6.16% between 2026 to 2031.

Robust demand for cyber-risk advisory, rapid adoption of embedded insurance, and resilient SME economic activity underpin this trajectory, even as fee compression and talent scarcity introduce headwinds. Intensifying regulatory requirements under the Insurance Distribution Directive (IDD), Solvency II review, and the Digital Operational Resilience Act (DORA) are simultaneously raising compliance costs and creating high-margin consulting opportunities that favor technically proficient intermediaries. Digital transformation continues to reshape customer acquisition economics, with broker–insurtech partnerships delivering application-programming-interface (API) connectivity that supports real-time quotation and policy binding. Consolidation among both carriers and intermediaries persists, driven by private-equity roll-ups and strategic acquisitions that bolster specialty-line capabilities and geographic reach. Against this backdrop, brokers that invest in data analytics, regulatory expertise, and multi-channel distribution remain best positioned to defend margins while capturing cross-border growth.

Key Report Takeaways

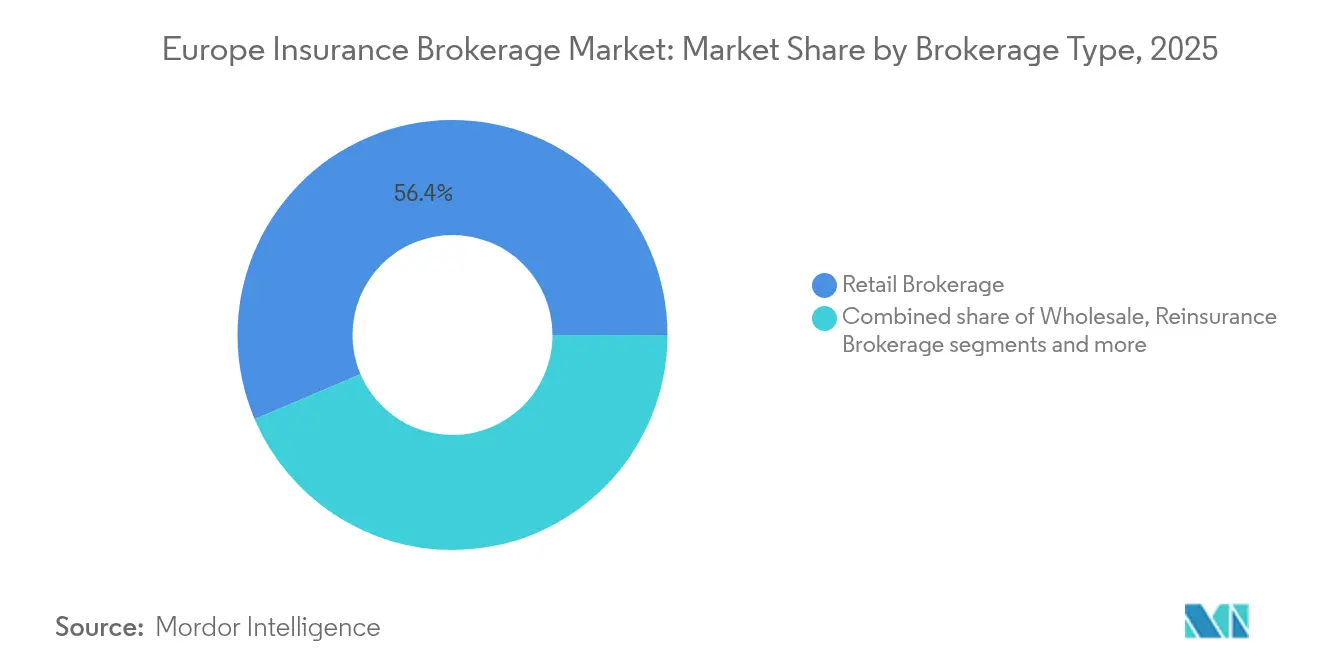

- By brokerage type, retail brokerage led with 56.40% of the Europe insurance brokerage market share in 2025, while reinsurance brokerage posted the fastest acceleration at a 5.05% CAGR through 2031.

- By client type, small and medium-sized enterprises accounted for 46.10% of the Europe insurance brokerage market size in 2025 and are projected to grow at a 6.03% CAGR to 2031.

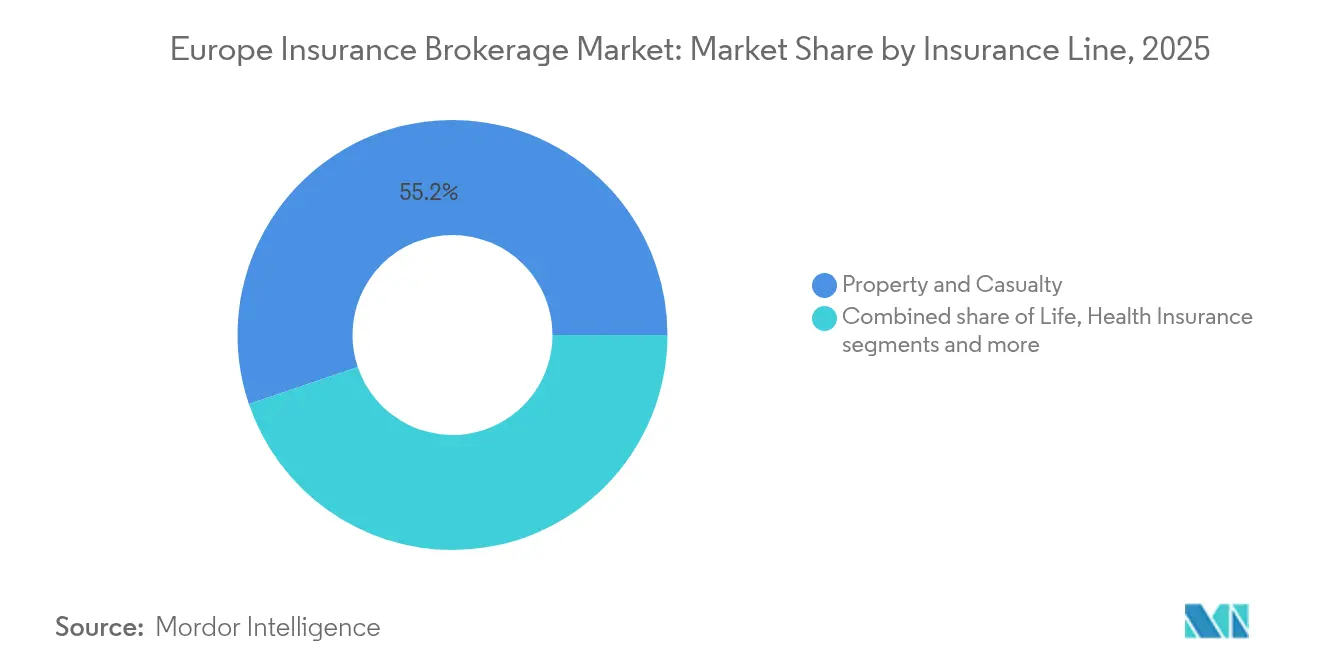

- By insurance line, property & casualty held 55.20% of Europe insurance brokerage market share in 2025, whereas specialty lines are projected to expand at a 6.74% CAGR through 2031.

- By distribution channel, traditional face-to-face still represented 56.10% of the Europe insurance brokerage market size in 2025; digital and online platforms are advancing at a 7.62% CAGR for the forecast period.

- By geography, the United Kingdom retained a 28.15% share of the Europe insurance brokerage market in 2025, while the NORDICS region records the fastest forecast growth at a 5.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on insurance brokerage market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Insurance Brokerage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-insurance advisory demand | +1.8% | United Kingdom, Germany, Netherlands | Medium term (2–4 years) |

| Regulatory complexity (IDD, Solvency II, DORA) | +1.2% | All EU member states | Long term (≥ 4 years) |

| SME demand for tailored cover | +1.5% | Western Europe; spill-over to Central & Eastern Europe | Medium term (2–4 years) |

| Insurtech partnerships | +1.1% | United Kingdom, Nordics | Short term (≤ 2 years) |

| Embedded-insurance distribution | +0.9% | Germany, Netherlands, France | Medium term (2–4 years) |

| EU Green Deal climate-related parametric products | +0.7% | Northern Europe, Alpine region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cyber-Insurance Advisory

Organizations across Europe are upgrading risk-transfer strategies as ransomware incidents surge and legislative scrutiny intensifies under DORA, effective January 2025[1]European Insurance and Occupational Pensions Authority, “Digital Operational Resilience Act Overview,” eiopa.europa.eu. Cyber premiums rose 35% during 2024, yet insurer capacity remains tight, prompting brokers to structure layered, parametric, and captive-fronted programs tailored to sector-specific exposures. SMEs, which remain 60% underinsured for digital risks, represent a fertile advisory pool that rewards firms capable of translating technical vulnerabilities into appropriate indemnities. Brokerages are recruiting chief information security officers and penetration-testing specialists to bridge knowledge gaps and secure underwriting data credibility. Standardized frameworks such as ISO 27001 and forthcoming NIS2 rules further expand consulting revenue because clients require proof of compliance alignment for policy issuance. Talent bottlenecks, however, inflate salary costs and prolong onboarding, marginally tempering the tailwind.

Increasing Regulatory Complexity

The 2025 Solvency II review tightens capital disclosure while the IDD elevates conduct-of-business obligations, compelling brokers to maintain granular product-suitability records that small carriers and SMEs often lack. These layers of oversight generate incremental advisory fees as intermediaries map risk appetite to carrier solvency positions and ensure multi-jurisdictional compliance. The United Kingdom’s Consumer Duty framework solidifies this trend by mandating fair-value assessments and clear remuneration disclosure, reinforcing the value proposition of brokers with embedded compliance expertise. At the same time, duplicated reporting and audit procedures raise overheads that smaller firms struggle to absorb, accelerating acquisition interest from scale players looking to spread fixed costs. Brokers capitalize on regulatory arbitrage by structuring cross-border programs that exploit variance in premium taxes and capital-relief rules, yet emerging pan-EU alignment under DORA may gradually narrow such opportunities.

Expansion of the SME Sector

SMEs contributed 46.42% to the Europe insurance brokerage market in 2024 and will expand faster than any other client group through 2030 as supply-chain fragility, cyber threats, and trade realignment heighten insurance awareness. Policy-density gaps, particularly in continental Europe, are narrowing as banks and digital marketplaces embed commercial coverage at the point of invoice financing, logistics booking, or software subscription. Brokers that invest in modular products and automated triage tools shorten quoting cycles, improving retention while lifting cross-sell ratios for ancillary lines such as trade credit and directors’ and officers’ (D&O) liability. The EU Artificial Intelligence Act is poised to create a fresh compliance burden, making professional liability extensions for algorithmic errors an emerging niche. Nonetheless, uneven digital literacy among micro-businesses could slow penetration unless intermediaries deploy intuitive self-service platforms supported by multilingual advisory chatbots.

Insurtech Partnerships Enhancing Customer Experience

Incumbent brokers increasingly pursue minority stakes or joint ventures with software-as-a-service underwriting engines and digital brokers to retain relevance with mobile-first consumers. API integration speeds quote-to-bind from days to minutes and delivers dynamic pricing that reflects telematics, weather feeds, or supply-chain analytics. Embedded-insurance pilots such as the 2024 launch of mobility cover inside German telecom billing demonstrate how brokers can monetize high-frequency customer touchpoints without surrendering advisory depth. These alliances also generate granular customer data that improves loss-ratio forecasting and informs tailor-made risk-mitigation services. However, dependence on third-party technology raises operational-resilience obligations under DORA, compelling careful vendor-risk governance. Margin-sharing agreements must also be balanced against potential cannibalization of traditional high-commission channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee compression from online comparison platforms | -1.4% | UK, Germany, Netherlands with spillover to France | Short term (≤ 2 years) |

| GDPR limits on data-driven cross-selling | -0.8% | EU-wide, strongest impact in Germany, France | Medium term (2-4 years) |

| Insurer consolidation reduces broker bargaining power | -0.6% | Global, with concentrated impact in UK, Germany | Long term (≥ 4 years) |

| Talent shortage in specialty-risk advisory | -0.9% | EU-wide, most acute in UK, NORDICS | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fee Compression From Online Comparison Platforms

Price-aggregator websites have eroded commission rates for personal lines and commoditized segments by offering real-time premium grids that enable straight-through purchasing. Insurers aiming for sub-15% expense ratios channel more volume directly to digital-first distributors, cutting traditional intermediaries out of the value chain. Transparency rules under IDD and Consumer Duty reinforce client bargaining power by obliging brokers to disclose remuneration and demonstrate fair value. As a result, negotiated base commissions for standard motor and home policies in some EU markets fell by as much as 150 basis points during 2024. Premium-rich advisory segments like cyber and trade credit offer insulation, yet cross-subsidization becomes harder as profit pools shrink on commoditized lines. Brokers counter by differentiating through value-added services, risk engineering, claims advocacy, and data analytics, though scaling these services across diverse micro-segments remains challenging.

Talent Shortage in Specialty-Risk Advisory

Retirement deferrals by senior practitioners, combined with a sparse mid-career cohort, leave firms exposed to knowledge-transfer gaps. Cyber risk, marine renewable energy, and structured reinsurance placements are among the hardest roles to staff, with some positions remaining unfilled for over nine months[2]Chartered Insurance Institute, “Insurance Workforce Skills Report 2025,” cii.co.uk. The apprenticeship model that traditionally developed technical competence weakened during the pandemic as remote work curtailed on-the-job learning. Post-Brexit visa restrictions further restrict access to non-EU technical talent, particularly actuaries and engineers. Rising wage competition among brokers, carriers, and technology vendors inflates cost-to-serve, threatening profitability on resource-intensive placements. Firms respond with graduate-rotational schemes, accelerated professional-qualification sponsorship, and retention bonuses, but success is uneven and time-consuming, keeping capacity constrained in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Brokerage Type: Demand for Reinsurance Expertise Outpaces Retail Dominance

Retail brokerage generated 56.40% of the European insurance brokerage market size in 2025 on the back of deep client relationships and multichannel servicing capabilities. Nevertheless, reinsurance brokerage is predicted to expand at a 5.05% CAGR through 2031, energizing overall growth as climate-driven catastrophe severity prompts cedents to seek sophisticated capital-management solutions. Reinsurance specialists monetize advanced stochastic-modeling and alternative-risk-transfer advisory, often commanding higher fee yields than retail placements. Wholesale brokers remain pivotal for surplus-line cover and multi-territory programs, especially where local capacity constraints intersect with complex compliance requirements. Bancassurance brokerage, though smaller in absolute terms, is regaining momentum as banks leverage payment and balance-sheet data to upsell bundled coverage and increase non-interest income.

Reinsurance brokerage is accelerating, with growth projected to rise from 3.8% (2019–2024) to 5.05%, driven by increased catastrophe-bond issuance, parametric solutions, and greater demand for carrier capital relief. Meanwhile, retail insurance margins are under pressure as digital aggregators compress commission spreads on standard products, prompting a shift toward advisory-heavy specialties. Wholesale intermediaries are gaining from the globalization of supply chains, which require cross-border certificate issuance and localized claims support. However, broader macroeconomic headwinds may dampen premium growth across markets. Bancassurance is set to expand as open-banking regulations boost data availability, allowing insurers to embed personalized offers within everyday financial transactions.

By Client Type: SMEs Anchor Forward Momentum

Small and medium-sized enterprises currently represent 46.10% of the European insurance brokerage market share and are projected to clock a 6.03% CAGR over the forecast horizon. Geopolitical disruptions and cybercrime spikes have heightened risk awareness, catapulting demand for business-interruption, trade-credit, and cyber-liability policies. Brokers that introduce modular policy architectures and digital self-serve platforms shorten onboarding, an advantage when courting cost-sensitive micro-enterprises. Large corporations sustain resilient premium pools but exert fee pressure by internalizing elements of risk management and running competitive tenders among mega-brokers. Public-sector entities rely on brokers for climate-resilience funding structures and catastrophe-response frameworks, bolstering demand for alternative-risk-transfer counsel.

The SME segment is growing rapidly, boosted by EU recovery-fund investments that support digitization grants and expose businesses to new cyber risks requiring coverage. Start-ups within platform ecosystems are driving demand for innovative policies, including contingent-labor liability and intellectual property protection. At the individual level, more customers are turning to direct-to-consumer channels for motor and home insurance, squeezing broker margins in the small-account space. As a result, brokerages are refocusing on advisory-rich services tied to professional indemnity, key-person coverage, and voluntary benefits. These offerings are increasingly aligned with the needs of entrepreneurial clients and their evolving risk profiles.

By Insurance Line: Specialty Classes Drive Innovation

Property & casualty lines retained 55.20% of the Europe insurance brokerage market size in 2025, fueled by corporate motor fleets and commercial property exposures. Specialty lines cyber, marine, pet, and travel are forecast to outpace the core at a 6.74% CAGR through 2031, propelled by evolving risk taxonomies and regulatory mandates. Cyber insurance remains the standout, its European gross written premiums expanding 35% in 2024 amid escalating ransomware sophistication. Marine renewable-energy projects and offshore wind construction inject additional specialty momentum as the continent accelerates decarbonization. Life-insurance brokerage sees moderate growth via simplified-issue products integrated into mortgage and savings platforms, whereas health-insurance intermediation benefits from cross-border telemedicine and private-medical plans among mobile professionals.

Parametric climate-linked covers, spearheaded by Nordic carriers, exemplify product innovation that brokers can scale across the agriculture and tourism sectors. Structured environmental-liability wrappers accompany green-bond issuances, providing another fee niche. Yet capacity for high-limit cyber or catastrophe pools remains finite, pressuring brokers to syndicate placements across multiple carriers or reinsurance markets. As underwriting sophistication rises, data-quality management and actuarial analytics become decisive competitive assets. Regulatory scrutiny around ESG disclosures is also prompting insurers and brokers to enhance transparency in both product design and portfolio reporting.

By Distribution Channel: Digital Gains Accelerate

Traditional face-to-face channels still account for 56.10% of the Europe insurance brokerage market size, underlining client reliance on personal advisory for complex and high-value placements. Digital and online platforms, however, are advancing at a 7.62% CAGR as embedded-insurance APIs integrate cover into non-insurance customer journeys. Affinity programs housed within professional associations and membership clubs leverage trust networks to distribute niche products at lower acquisition cost. Bancassurance partnerships are being reinvented; banks leverage transaction data to generate hyper-personalized offers, reinforcing cross-sell potential while elevating compliance duties under Consumer Duty.

The pandemic-era pivot to virtual communications accelerated policy digitization, collapsing sales-cycle duration for small commercial and personal-accident products. Brokers extend portal functionality to claims triage and risk-prevention advice, boosting retention. Nonetheless, omni-channel coherence remains critical because clients often initiate digitally but seek human intervention for coverage customization. Investments in customer-relationship-management (CRM) platforms and cybersecurity controls are therefore rising, especially as DORA sharpens operational-resilience expectations. As digital touchpoints proliferate, brokers are also leveraging AI-driven insights to personalize offerings and anticipate client needs more proactively.

Geography Analysis

In 2025, the United Kingdom accounted for 28.15% of Europe's insurance brokerage market, leveraging London's position as a global hub for specialty risks and the Lloyd's marketplace. However, the post-Brexit environment has introduced challenges, particularly with passporting arrangements. To address these issues, brokers have strengthened their EU-based subsidiaries and pursued treaty placements through Brussels-based entities. Germany and France follow closely behind in market share, driven by their strong industrial sectors, which require advanced engineering and liability insurance solutions. Spain and Italy are also experiencing growth, supported by EU Green Deal funding that focuses on infrastructure resilience. This funding has increased demand for parametric weather insurance and construction all-risk policies.

The Nordic countries, Sweden, Denmark, Finland, and Norway, are showing the fastest growth in the region, with a projected compound annual growth rate (CAGR) of 5.81% through 2031. These nations benefit from high levels of digital literacy and regulatory alignment, which facilitate the adoption of insurtech solutions and the seamless cross-border passporting of insurance products. In the Benelux region, countries are capitalizing on trade-corridor insurance, which supports logistics operations between ports and their surrounding areas. This focus on logistics has created opportunities for specialized insurance products tailored to the needs of these trade corridors.

Central and Eastern Europe, while historically underpenetrated, are now catching up as foreign direct investment drives an increased need for risk transfer solutions. The European Insurance and Occupational Pensions Authority (EIOPA) is promoting supervisory convergence to enhance market integration across the region. However, localized tax regulations continue to pose challenges, requiring customized structuring for multinational insurance programs. These developments highlight the evolving dynamics of the European insurance brokerage market and the diverse factors influencing its growth.

Mordor Intelligence provides coverage of the insurance brokerage market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

Europe’s insurance brokerage market remains moderately concentrated: the top five firms, Marsh McLennan, Aon, Willis Towers Watson, Arthur J. Gallagher, and Howden Group, held a combined half share in 2024. Scale affords these leaders privileged access to carrier capacity, investment in proprietary data platforms, and talent recruitment budgets that smaller peers find difficult to match. Marsh McLennan reinforced its retail footprint with the USD 7.75 billion acquisition of McGriff Insurance Services, exemplifying a shift toward large-ticket strategic buys aimed at deepening specialty penetration[4]Reinsurance News, “Marsh McLennan Acquires McGriff for USD 7.75 Billion,” reinsurancene.ws. Howden Group’s continued continental expansion through bolt-ons in Spain and Eastern Europe illustrates private-equity-backed appetite for regional specialists possessing cultural know-how and niche product skills.

Private-equity roll-ups remain a defining feature, particularly in the United Kingdom and Benelux, where fragmented agency networks present abundant targets. Deal multiples compressed slightly in 2024 as financing costs rose, but competition for cyber-specialist and MGA capabilities kept valuations resilient. Technology investment differentiates market leaders; several large brokers deploy cloud-native placement platforms that reduce turnaround time and enable carrier panel selection based on real-time appetite signals. Regulatory-compliance prowess is turning into a defensible moat, with DORA and Consumer Duty elevating the complexity bar for emerging players. Yet talent shortages in analytics and climate modeling could hinder even well-capitalized firms unless recruitment pipelines diversify.

Carrier consolidation introduces countervailing power: mergers among European insurers shrink broker panels and toughen commission negotiations. To preserve bargaining power, brokers co-create specialty MGAs, harnessing underwriting authority to retain a larger slice of economics while satisfying capacity constraints within carrier partners. Collaboration with technology vendors to operationalize predictive-risk-prevention services, such as IoT sensor deployments in manufacturing plants, further differentiates offerings beyond mere placement. Over the forecast horizon, firms that align digital, advisory, and regulatory competencies will consolidate gains, while subscale generalists risk margin erosion or forced exit. As competition intensifies, strategic talent acquisition, particularly in data science, compliance, and sector-specific underwriting, will become a key determinant of long-term broker success.

Europe Insurance Brokerage Industry Leaders

Marsh & McLennan Companies (Marsh)

Aon plc

Willis Towers Watson (WTW)

Arthur J. Gallagher & Co.

Hyperion Insurance Group (Howden)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Zurich Insurance Group acquired a significant minority stake (just under 50%) in London-based Icen Risk for approximately USD 194 million, targeting M&A-focused insurance, including warranty & indemnity coverage, with plans to expand into North America and large European markets, including Germany.

- September 2024: Marsh McLennan agreed to acquire McGriff Insurance Services for USD 7.75 billion, expanding U.S. retail brokerage presence and signaling continued large-scale consolidation in the global insurance brokerage market via cross-border transactions by leading brokers seeking specialty lines capabilities and enhanced client relationships.

- August 2024: ERGO, O2 Telefónica, and Telefónica Insurance launched an embedded insurance product, "O2 Care | Mobility," throughout Germany at USD 5.25 (EURO 4.99) monthly, featuring mobility guarantee for rental car breakdowns and bicycle flats, demonstrating embedded insurance distribution integrated into telecommunications billing and digital customer journeys.

- July 2024: Brown & Brown Inc. entered agreement to acquire Quintes Holding B.V., one of the largest independent insurance brokers in the Netherlands, serving approximately 200,000 customers across broking, MGA, and pensions divisions with 700 insurance professionals across 18 Dutch locations, expanding Brown & Brown's European footprint and Dutch market presence.

Europe Insurance Brokerage Market Report Scope

The report includes a detailed note on the importance of insurance brokers across various insurance products in the region. An understanding of the present status of the European insurance markets to correlate that with the evolving brokerage firms' business models across the region, detailed market segmentation, current market trends, changes in market dynamics, and growth opportunities. In-depth analysis of the market size and forecast for the various segments. The report offers market size and forecasts in value (USD billion) for all the above segments.

| Retail Brokerage |

| Wholesale Brokerage |

| Reinsurance Brokerage |

| Bancassurance Brokerage Services |

| Individuals |

| Small & Medium-Sized Enterprises (SMEs) |

| Large Corporations |

| Public Sector Entities |

| Life Insurance |

| Health Insurance |

| Property & Casualty (Motor, Home, Commercial, Liability) |

| Specialty Lines (Cyber, Pet, Marine, Travel) |

| Traditional Face-to-Face |

| Digital / Online Platforms |

| Affinity & Embedded Partnerships |

| Bancassurance Partnerships |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Brokerage Type | Retail Brokerage |

| Wholesale Brokerage | |

| Reinsurance Brokerage | |

| Bancassurance Brokerage Services | |

| By Client Type | Individuals |

| Small & Medium-Sized Enterprises (SMEs) | |

| Large Corporations | |

| Public Sector Entities | |

| By Insurance Line | Life Insurance |

| Health Insurance | |

| Property & Casualty (Motor, Home, Commercial, Liability) | |

| Specialty Lines (Cyber, Pet, Marine, Travel) | |

| By Distribution Channel | Traditional Face-to-Face |

| Digital / Online Platforms | |

| Affinity & Embedded Partnerships | |

| Bancassurance Partnerships | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe insurance brokerage market in 2026?

The market generated USD 276.05 billion in 2026 and is projected to reach USD 372.12 billion by 2031.

Which segment is growing fastest within European brokerage?

Reinsurance brokerage is forecast to grow at a 5.05% CAGR, outpacing other brokerage types.

Why are SMEs critical for brokers’ future growth?

SMEs already account for nearly half of brokered premiums and are expected to expand at a 6.03% CAGR as cyber and supply-chain risks intensify.

How is digital distribution reshaping brokerage economics?

Digital and online platforms are projected to grow at a 7.62% CAGR, lowering acquisition costs while pressuring traditional commission structures.

Which geography shows the highest growth momentum?

The Nordics region leads with a forecast 5.81% CAGR, buoyed by advanced digital infrastructure and supportive regulation.

What is driving consolidation among European brokers?

Scale economies in compliance, technology investment, and talent acquisition motivate large players to absorb regional specialists and MGAs.

Page last updated on: