Europe Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

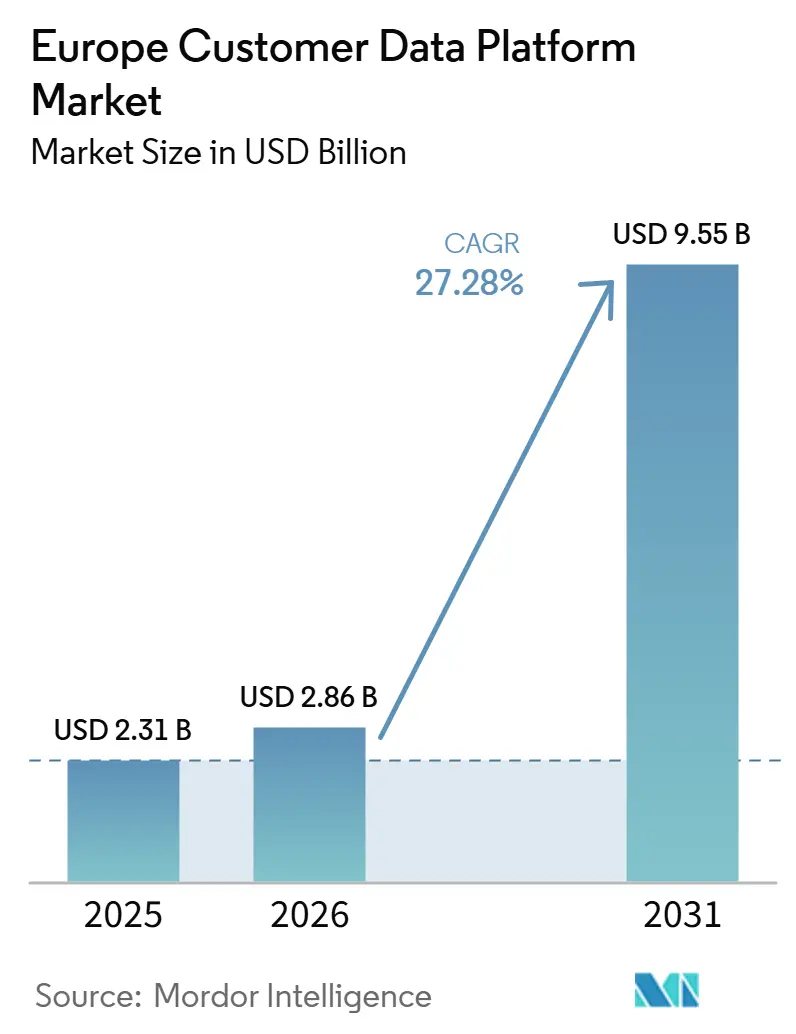

| Base Year Market Size (2025) | USD 2.31 Billion |

| Market Size (2026) | USD 2.86 Billion |

| Market Size (2031) | USD 9.55 Billion |

| Growth Rate (2026 - 2031) | 27.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Customer Data Platform Market Analysis by Mordor Intelligence

The Europe customer data platform market size was valued at USD 2.31 billion in 2025 and is forecast to reach USD 9.55 billion by 2031, expanding at a CAGR of 27.28% over 2026-2031. The Europe customer data platform market is moving from basic profile unification toward systems that support real-time activation, predictive decisions, and stricter consent handling across channels. GDPR enforcement has made first-party data architecture a business priority because enterprises now need systems that can support personalization goals and compliance requirements at the same time. Demand is also shifting toward flexible deployment models, especially hybrid and warehouse-centered setups, because many European enterprises want stronger control over customer data residence and processing. Competition in the Europe customer data platform market remains strongest at the enterprise tier, where large suite vendors benefit from installed CRM and ERP relationships, while regional specialists compete through privacy-focused design and identity resolution strength. The next phase of growth is likely to come from organizations that delayed adoption earlier, including SMEs, healthcare operators, and public sector entities that now face clearer operational reasons to modernize customer data infrastructure.

Key Report Takeaways

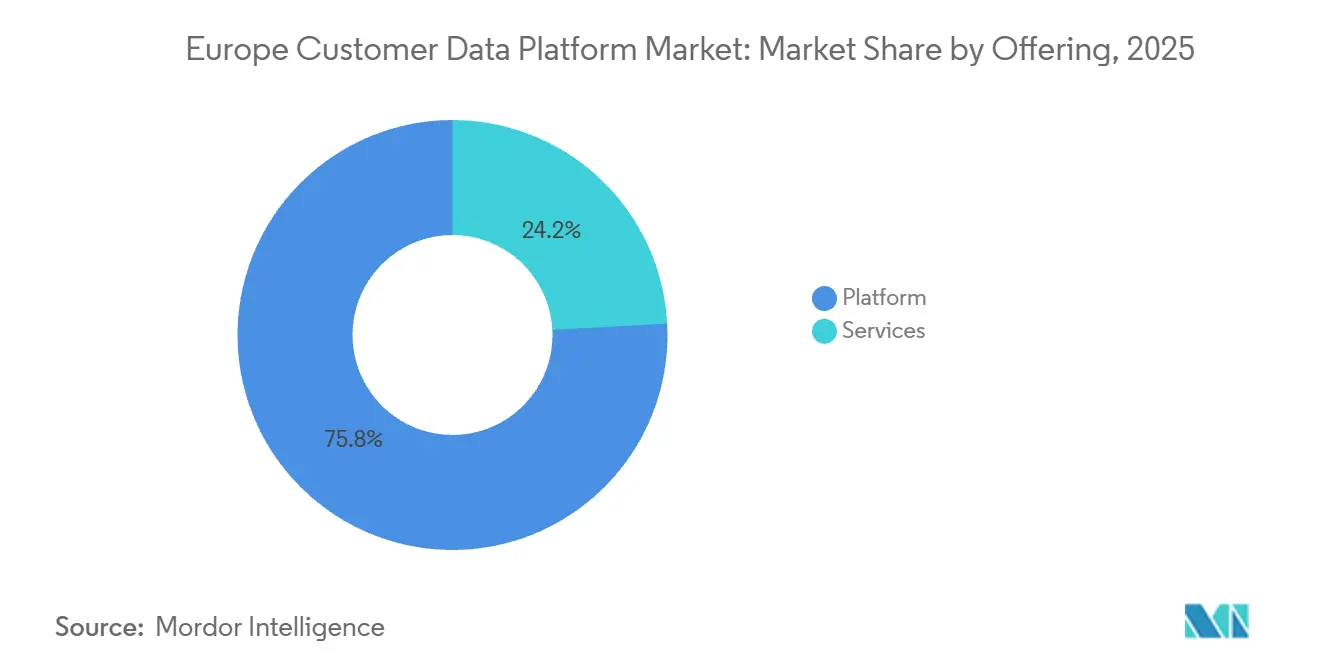

- By offering, platform held 75.84% of the Europe customer data platform market share in 2025, while services is projected to expand at 29.94% CAGR through 2031.

- By deployment mode, cloud captured 59.62% share in 2025, while hybrid is projected to grow at 31.08% CAGR through 2031.

- By organization size, large enterprises held 70.88% share in 2025, while SMEs are projected to expand at 31.26% CAGR through 2031.

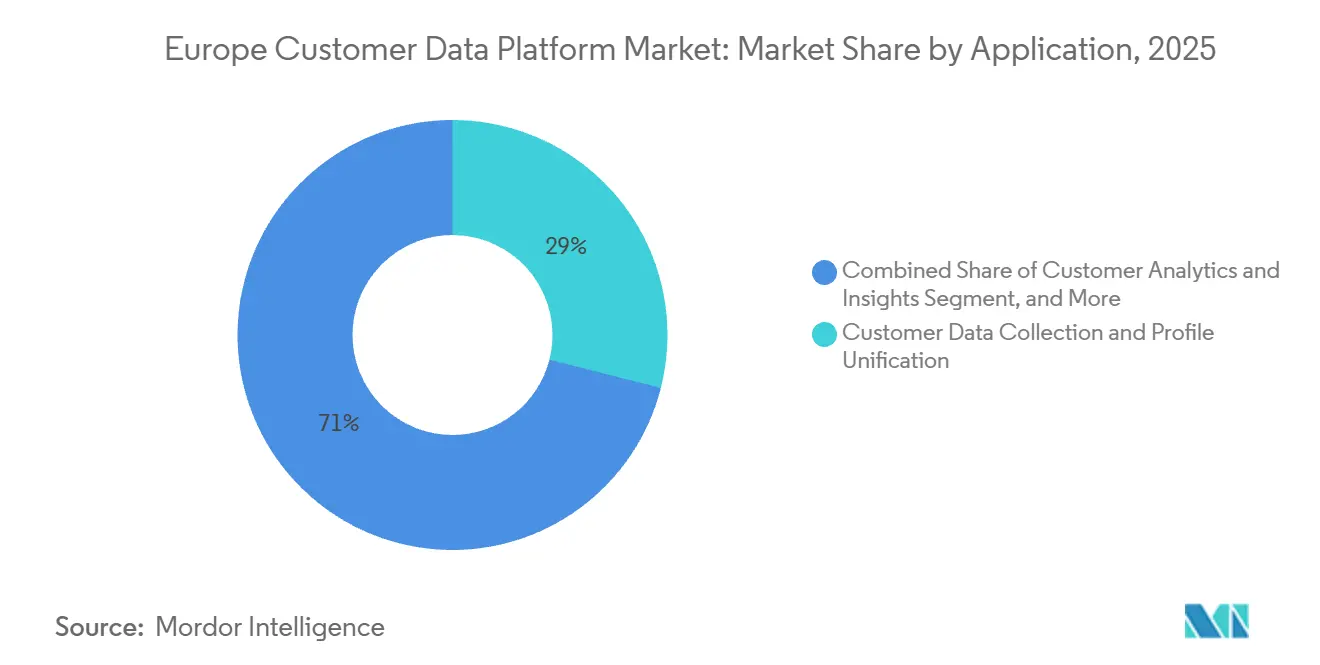

- By application, customer data collection and profile unification accounted for 28.96% share in 2025, while customer analytics and insights is projected to grow at 32.18% CAGR through 2031.

- By end-user industry, retail and e-commerce led with 23.84% of the Europe customer data platform market share in 2025, while healthcare and life sciences is projected to expand at 32.44% CAGR through 2031.

- By geography, the United Kingdom accounted for 20.74% share of the Europe customer data platform market size in 2025, while Spain is projected to expand at 31.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven First-Party Data Modernization | +6.8% | EU-wide, strongest in Germany, France, Netherlands | Long term (≥ 4 years) |

| AI-Led Journey Orchestration and Predictive Segmentation | +5.9% | UK, Germany, Nordics, spill-over to BeNeLux | Medium term (2-4 years) |

| Real-Time Identity Resolution for Omnichannel Activation | +4.6% | UK, Germany, Nordics, DACH core | Medium term (2-4 years) |

| Composable and Warehouse-Native CDP Adoption | +4.1% | DACH region, UK, Nordics, spill-over to BeNeLux | Medium term (2-4 years) |

| Third-Party Cookie Decommissioning | +3.2% | EU-wide, early enforcement pressure in France and Germany | Short term (≤ 2 years) |

| Consent-Aware Personalization at Scale | +2.5% | EU-wide, strongest in France and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven First-Party Data Modernization Redefines Data Infrastructure

GDPR enforcement has turned customer data management into a long-cycle infrastructure decision across the European customer data platform market. Enterprises are no longer treating compliance as a separate legal workflow because consent capture, data retention, and profile activation now sit inside the same operating model. This has increased interest in CDPs that can document user permissions, support deletion requests, and preserve auditable records without forcing teams into manual workarounds. It also changes who influences vendor selection, because data protection officers, legal teams, and security functions now shape procurement alongside marketing and technology teams. In the Europe customer data platform market, this shift favors platforms that can show compliance discipline at the architecture level rather than through later customization.

AI-Led Journey Orchestration and Predictive Segmentation Reshape Activation Economics

The Europe customer data platform market is also benefiting from a shift toward AI-led campaign orchestration and predictive segmentation. Buyers are placing greater value on systems that can shorten the time between signal capture and action, especially when customer journeys span web, mobile, paid media, loyalty, and service channels. Adobe launched CX Enterprise Coworker in April 2026 on Adobe Experience Platform, with Real-Time CDP serving as the data layer for agentic customer experience workflows.[1]Adobe, “Adobe Unveils CX Enterprise Coworker to Build Agentic-Enabled Workflows for Customer Experience Orchestration,” Adobe Newsroom, news.adobe.com SAP also expanded its Google Cloud partnership in April 2026 to bring multi-agent AI capabilities into SAP Engagement Cloud and SAP Customer Experience, with marketing identified as the first commercial use case. These moves support a wider pattern in the Europe customer data platform market, where buyers increasingly judge CDPs by how well they connect customer data to automated decisioning. Better orchestration can reduce manual campaign work while improving segmentation precision, which strengthens the case for investment in a market where spending approvals often face close governance review.

Real-Time Identity Resolution Becomes the Differentiating Data Layer

Identity resolution remains one of the most contested capabilities in the Europe customer data platform market because it determines how much value enterprises can extract from fragmented customer touchpoints. The challenge is sharper in Europe because strict privacy conditions and uneven consent rates reduce the usefulness of third-party identifiers in many digital environments. Transcend noted that analytics cookie consent rates often fall within a 40% to 70% range, which leaves a meaningful share of web traffic outside conventional tracking models.[2]Transcend, “Identity Resolution for Enterprises, How to Scale Without the Privacy Risk,” Transcend, transcend.io Databricks launched CustomerLake in June 2026 with identity, audience building, and campaign automation embedded in its lakehouse environment, showing how identity functions are moving closer to the core data layer. For the Europe customer data platform market, the practical result is clear, privacy-aware first-party identity graphs are becoming an operating requirement rather than a premium feature.

Composable and Warehouse-Native CDP Adoption Accelerates Across European Enterprises

Composable architecture is gaining traction in the Europe customer data platform market because many enterprises want to activate customer data without duplicating sensitive records into vendor-controlled systems. This preference is strongest in DACH and other sovereignty-conscious markets, where storage location, processing control, and PII minimization carry direct weight in procurement. The CDP Institute reported in January 2026 that composable and warehouse-native vendors recorded 7.8% organic employment growth, compared with 1.3% for the broader industry. Hightouch has also argued that warehouse-native designs better fit European GDPR requirements because they reduce the need to copy personal data into separate application storage. In the Europe customer data platform market, that architectural argument is now tied as much to compliance and internal control as to engineering flexibility. It also helps explain why hybrid deployment models are rising even while cloud remains the largest installed format.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy CRM, ERP, and MarTech Integration Burden | -3.8% | EU-wide, pronounced in Southern and Eastern Europe | Long term (≥ 4 years) |

| Data Minimization and Cross-Border Transfer Constraints | -3.1% | EU-wide, cross-border between EU and non-EU jurisdictions | Long term (≥ 4 years) |

| Talent Gaps in Privacy Engineering and Data Activation | -2.4% | Eastern Europe, smaller EU markets | Medium term (2-4 years) |

| High Cost of Identity Graph Maintenance and Data Quality Remediation | -1.9% | Global, with pronounced impact on European SMEs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy CRM, ERP, and MarTech Integration Burden Slows Deployment Cycles

Integration remains one of the clearest limits on growth in the Europe customer data platform market. Many enterprises still hold customer records across older ERP systems, CRM installations, marketing tools, and regional databases that were never designed to operate as a single real-time environment. This issue is especially difficult in organizations built through acquisitions, where overlapping data models and inconsistent identifiers create long implementation cycles. The burden raises total ownership costs and delays time to usable activation, which matters in procurement settings where technology and marketing budgets are reviewed separately. Even when a CDP supports real-time capabilities, its value can stay constrained if source systems still depend on batch exports and manual reconciliation.

Data Minimization and Cross-Border Transfer Constraints Limit Activation Scope

Data minimization rules also place a structural limit on how broadly enterprises can build and activate unified profiles in the Europe customer data platform market. Teams must justify why each attribute is collected, retained, and used, which adds continuous coordination between engineers, privacy counsel, and operational stakeholders. Publicis Groupe announced an agreement in May 2026 to acquire LiveRamp for USD 2.2 billion, a move that drew attention to the strategic importance of identity and data collaboration in regulated environments. At the same time, cross-border data handling remains sensitive because controllership, processor roles, and transfer frameworks can change the compliance profile of an activation workflow. These conditions narrow the practical scope of some cross-market use cases, particularly when European customer data must be connected with systems or campaigns outside EU jurisdiction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Dominance Masks an Accelerating Services Shift

Platform commanded 75.84% of the Europe customer data platform market size in 2025, which reflects the established role of full-suite vendors in enterprise procurement. Salesforce, Adobe, Oracle, and SAP benefit from installed relationships in CRM, marketing automation, and enterprise applications, which makes the platform purchase easier to justify within existing technology estates. That installed base also supports renewal momentum because buyers often prefer tighter integration over introducing a separate specialist tool into a complex stack. The scale of platform demand shows that many enterprises still want a central operating layer rather than a loose collection of point solutions. It also shows that the Europe customer data platform market still rewards vendors that can package identity, segmentation, and activation inside a broader commercial software relationship.

Services is forecast to grow at 29.94% CAGR through 2031, which makes it the faster-moving side of the offering mix. This growth reflects the reality that many deployments need more than software access, because organizations must still configure identity rules, connect consent systems, engineer pipelines, and validate activation logic. As composable models spread, the work often shifts from license-led buying toward implementation, integration, and managed activation support. Compliance reviews also add service demand because enterprises increasingly expect deployment partners to understand audit requirements, security controls, and data governance standards. In the Europe customer data platform industry, the rising services share signals a more operational phase of adoption, where value depends on execution quality as much as on product selection.

By Deployment Mode: Hybrid Architectures Signal a Warehouse-First Future

Cloud captured 59.62% share in 2025, confirming that it remained the default route for new implementation across the Europe customer data platform market. Cloud still appeals because it shortens deployment cycles, reduces infrastructure ownership, and supports easier scaling across business units and channels. It is especially relevant for organizations that want faster activation without building every integration internally. Even so, cloud leadership does not mean a fully outsourced data model is becoming universal across Europe. The market is moving toward more selective architecture choices, where organizations separate activation speed from storage control.

Hybrid is projected to expand at 31.08% CAGR through 2031, which makes it the fastest-growing deployment mode. The appeal of hybrid architecture is strongest where enterprises want to keep core customer records in internal or controlled environments while still connecting them to real-time engagement tools. On-premises setups remain relevant in BFSI and government, where security policy, contract legacy, and data residency rules can slow public cloud migration. Tealium extended its hybrid proposition in May 2026 with AI at the Edge, and AI Decisioning features aimed at processing signals closer to the data collection layer. The Europe customer data platform market is therefore not moving away from cloud, but toward cloud models that preserve stronger enterprise control over where personal data sits and how it is activated.

By Organization Size: Large Enterprises Anchor Revenue While SMEs Drive Faster Expansion

Large enterprises held 70.88% of the Europe customer data platform market in 2025, showing how strongly first-generation adoption favored organizations with larger budgets and deeper technical resources. Early CDP programs often required extensive systems integration, identity design, governance alignment, and change management, which naturally matched larger companies better than smaller firms. Large enterprises also had stronger reasons to invest early because they managed broader customer touchpoint networks across geographies, brands, and channels. Their scale made profile unification and cross-channel orchestration more valuable, even when deployment was costly and complex. This revenue concentration explains why major suite vendors remain most powerful in the enterprise tier of the Europe customer data platform market.

SMEs are forecast to grow at 31.26% CAGR through 2031, making them the fastest-growing organization size segment. Growth is being supported by cloud-native deployment models, managed services, and simpler user interfaces that reduce the technical threshold for adoption. Smaller companies are increasingly able to buy packaged analytics, segmentation, and activation capabilities without assembling large in-house data engineering teams. The wider availability of GDPR-aware, subscription-based platforms also makes adoption more practical for firms that need compliance support but cannot fund a full custom stack. In the Europe customer data platform industry, this shift suggests that volume growth will increasingly come from smaller buyers even if large enterprises continue to anchor the largest contract values.

By Application: Analytics Overtakes Data Collection as the Primary Value Proposition

Customer data collection and profile unification accounted for 28.96% share in 2025, which shows that the foundational CDP use case still held the largest installed position. Most organizations still need a reliable layer for gathering, cleaning, and aligning records before they can activate data consistently across journeys. This base use case remains essential because weak profile quality can undermine every downstream function, from segmentation to measurement. It also keeps demand steady for platforms that can organize fragmented customer records across channels and business units. In the Europe customer data platform market, the installed strength of this application reflects the fact that many enterprises are still formalizing core data governance before moving into more advanced activation.

Customer analytics and insights is projected to grow at 32.18% CAGR through 2031, which makes it the fastest-growing application in the Europe customer data platform market. That pattern shows buyers are shifting budget toward systems that can predict value, score churn, improve audience quality, and tie marketing activity more directly to commercial outcomes. Organizations that have already solved much of the aggregation problem are now placing higher value on intelligence generation and decision support. This also changes the buying center because analytics teams, revenue leaders, and customer experience groups gain more influence once the platform becomes a decision engine instead of a storage layer alone. The Europe customer data platform industry is therefore moving from collection-led adoption toward analytics-led differentiation, with consent and preference management becoming a more visible budget line around that transition.

By End-User Industry: Retail Anchors Current Revenue While Healthcare Expands Fastest

Retail and e-commerce held 23.84% share in 2025, which made it the largest end-user segment in the Europe customer data platform market. The segment naturally generates high customer data intensity because brands must connect behavior across websites, apps, loyalty programs, stores, marketplaces, and campaign channels. That operating environment makes profile unification and audience activation easier to justify than in sectors with fewer commercial touchpoints. Retail buyers also face immediate pressure to improve conversion, retention, and personalization, which aligns closely with the original CDP value proposition. As a result, retail remains the clearest volume anchor for the Europe customer data platform market.

Healthcare and life sciences is projected to expand at 32.44% CAGR through 2031, the fastest rate among end-user industries. Growth reflects rising digital health activity, stronger focus on compliant patient and consumer engagement, and greater need for governed first-party data environments. The healthcare opportunity is also being shaped by policy direction in Europe, which is pushing institutions and commercial players toward more structured electronic data exchange and consent-aware infrastructure. BFSI remains another important demand center because customer data workflows sit close to compliance, fraud monitoring, and personalized service models. IT and telecom, media and entertainment, and government are also broadening the opportunity set, which reduces the long-term revenue dependence of the Europe customer data platform market on retail alone.

Geography Analysis

The United Kingdom held 20.74% of the Europe customer data platform market share in 2025, which made it the largest national market in the region. The country benefits from a dense concentration of retail, financial services, media, and advertising-linked enterprises that have invested in digital engagement stacks over multiple years. It also has a deeper managed-services ecosystem than many neighboring markets, which helps enterprises implement and operate CDP programs at scale. Germany followed as the next large market, supported by a substantial enterprise base and strong digitization activity, but with more cautious deployment preferences around data control. Across the Europe customer data platform market, the UK and Germany set much of the pace for enterprise adoption, yet they do so through different operating priorities.

Spain is projected to expand at 31.92% CAGR through 2031, which makes it the fastest-growing geography in the Europe customer data platform market. This faster growth reflects a lower installed base combined with rising digitization across retail, banking, and tourism, which creates room for new deployments rather than only replacement demand. France remains strategically important because strong regulatory enforcement and high digital marketing activity both increase the need for consent-aware customer data infrastructure. The Nordics continue to stand out for digital maturity and for early interest in warehouse-native and composable CDP models, especially among data-oriented retail and financial institutions. These regional differences show that the Europe customer data platform market is not following a single adoption pattern, because some countries are led by compliance urgency while others are led by architectural preference.

The Netherlands and Italy remain meaningful parts of the Europe customer data platform market, though each is shaped by different conditions around enterprise maturity, digital advertising intensity, and sector mix. Switzerland is smaller in volume but strategically relevant for financial services deployments, while Russia remains more isolated from the broader Western vendor ecosystem because of sanctions and localization factors. Central and Eastern European countries such as Poland, the Czech Republic, Hungary, and Romania represent a developing frontier where lower current penetration leaves room for future demand growth. Together, these markets broaden the long-term addressable base of the Europe customer data platform market beyond the largest Western European economies.

Competitive Landscape

The Europe customer data platform market shows moderate concentration at the top and much looser structure across the broader field. Salesforce, Adobe, Oracle, and SAP continue to shape enterprise competition because they can connect CDP functions with installed CRM, ERP, service, and marketing software relationships. That suite advantage makes switching harder and also allows these vendors to position the CDP as part of a wider transformation program rather than as a standalone tool purchase. Their influence is strongest in large accounts, where governance complexity and integration needs make established platform relationships more valuable. This gives the Europe customer data platform market a two-level structure, concentrated in the enterprise tier and more fragmented in the mid-market.

Strategic moves in 2026 show how quickly the competitive field is shifting. Adobe launched CX Enterprise Coworker in April 2026, extending its Real-Time CDP into agentic customer experience orchestration across the full lifecycle. SAP expanded its Google Cloud partnership in April 2026 to bring multi-agent AI into SAP customer experience workflows, with marketing named as the initial commercial use case.[3]SAP, “SAP and Google Cloud Expand Partnership to Deploy Multi-Agent AI,” SAP News Center, news.sap.com Databricks entered the competitive layer more directly in June 2026 with CustomerLake, bringing Customer 360, identity, audience building, and campaign automation into its lakehouse environment. Publicis also agreed in May 2026 to acquire LiveRamp for USD 2.2 billion, highlighting the rising strategic value of identity and data collaboration assets around customer activation. These developments suggest the Europe customer data platform market is no longer defined only by classic CDP vendors, because infrastructure platforms, agencies, and ecosystem providers are moving closer to the same value pool.

At the same time, specialist players remain relevant where privacy-native design, identity precision, or warehouse-first deployment are stronger buying criteria. That leaves room for vendors such as Zeotap and other regional specialists to compete where enterprises want tighter alignment with European data handling expectations. Oracle also strengthened its position in April 2026 after being named a Leader for its Fusion Cloud Unity Data Platform, which it framed around unifying customer, account, and operational data in one layer.[4]Oracle, “Oracle Named a Leader in the Gartner Magic Quadrant for Customer Data Platforms,” Oracle, oracle.com The next competitive dividing line in the Europe customer data platform market is likely to center on how well vendors connect governed first-party data with AI-driven activation without weakening enterprise control over sensitive information.

Europe Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

SAP SE

Bloomreach

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Databricks launched CustomerLake at the Data and AI Summit in San Francisco, introducing an agentic CDP natively embedded in its lakehouse. The platform combines Customer 360, identity resolution, audience building, and campaign automation within a single governed environment. Early adopters include HP, AB InBev, Virgin Atlantic, and Adidas, with the launch challenging standalone CDP vendors by bundling agentic AI and identity infrastructure at the data platform layer.

- May 2026: Publicis Groupe entered into an agreement to acquire LiveRamp, a global data collaboration platform, for a total enterprise value of USD 2.2 billion in an all-cash transaction at USD 38.50 per share. LiveRamp connects more than 25,000 publisher domains and 500+ technology partners across 14 markets. The transaction is expected to close before year-end 2026, subject to regulatory and shareholder approvals, and positions Publicis as a leader in AI-era data co-creation.

- April 2026: SAP and Google Cloud announced a strategic partnership to deploy multi-agent AI across SAP Engagement Cloud and SAP Customer Experience using Gemini Enterprise models. The integration enables orchestration of AI agents accessing unified data across both ecosystems, with marketing as the initial commercial use case and availability targeting H2 2026.

- April 2026: Adobe launched CX Enterprise Coworker, an agentic AI customer experience orchestration system built on Adobe Experience Platform, integrating Real-Time CDP, Customer Journey Analytics, and Journey Optimizer. The system is architectured on open standards including Model Context Protocol and Agent2Agent, embedding autonomous AI across the full customer lifecycle for brands operating at enterprise scale.

Europe Customer Data Platform Market Report Scope

The Europe Customer Data Platform (CDP) market comprises software platforms and associated services that collect, unify, manage, and activate customer data from multiple online and offline sources to create persistent, unified customer profiles. These platforms enable organizations to deliver personalized, privacy-compliant, and omnichannel customer experiences through capabilities such as identity resolution, audience segmentation, real-time data activation, customer journey orchestration, analytics, and consent management.

The Europe Customer Data Platform Market Report is Segmented by Offering (Platform, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries), and Geography (Germany, United Kingdom, France, Italy, Spain, Netherlands, Switzerland, Russia, Nordics, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Platform |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Switzerland |

| Russia |

| Nordics |

| Rest of Europe |

| By Offering | Platform |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Switzerland | |

| Russia | |

| Nordics | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe customer data platform market size through 2031?

The Europe customer data platform market size was USD 2.31 billion in 2025 and is forecast to reach USD 9.55 billion by 2031, with a 27.28% CAGR over 2026-2031.

Which segment leads by offering in Europe customer data platforms?

Platform led the market with 75.84% share in 2025. Services is growing faster, with a projected 29.94% CAGR through 2031.

Which deployment model is expanding fastest across Europe customer data platforms?

Hybrid is the fastest-growing deployment mode with a projected 31.08% CAGR through 2031. Cloud remained the largest model in 2025 with 59.62% share.

Which application is creating the strongest growth momentum in Europe customer data platforms?

Customer analytics and insights is projected to grow at 32.18% CAGR through 2031. This shows the market is shifting from basic data assembly toward decision support and activation intelligence.

Which end-user group offers the biggest opportunity in Europe customer data platforms?

Retail and e-commerce remained the largest end-user segment with 23.84% share in 2025. Healthcare and life sciences is the fastest-growing segment, with a projected 32.44% CAGR through 2031.

Which countries matter most in the Europe customer data platform market?

The United Kingdom held the largest national share at 20.74% in 2025, while Spain is projected to grow fastest at 31.92% CAGR through 2031. Germany, France, the Nordics, the Netherlands, and Italy also remain important growth markets.

Page last updated on: