Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

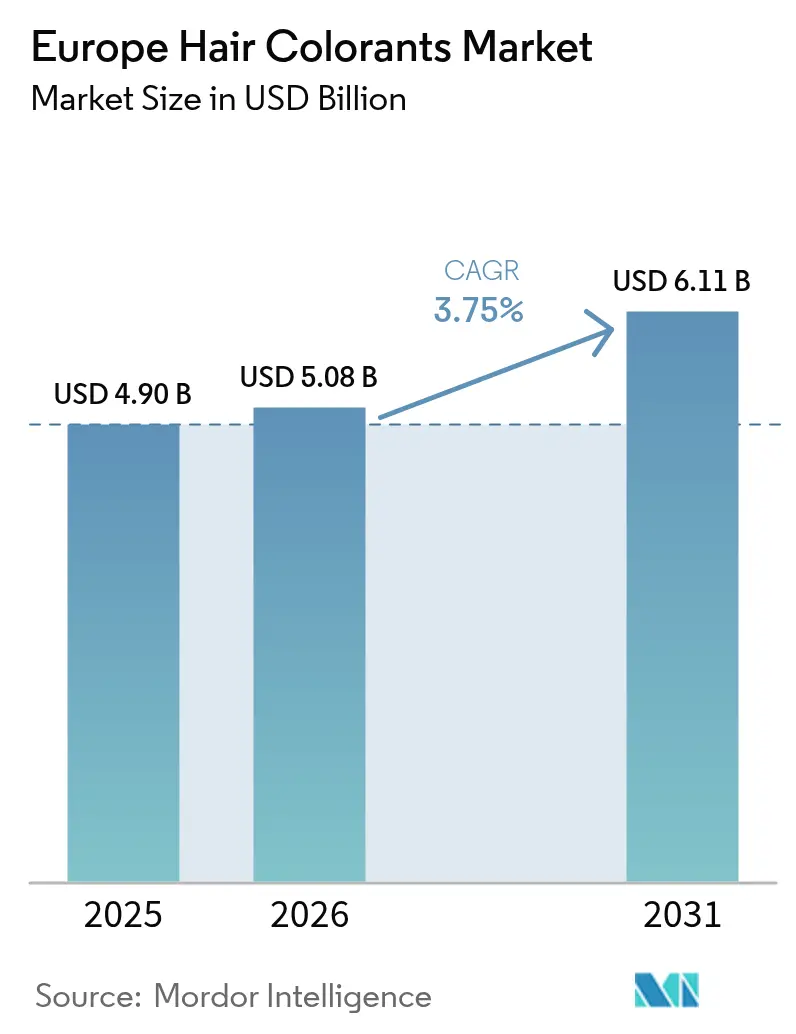

| Base Year Market Size (2025) | USD 4.90 Billion |

| Market Size (2026) | USD 5.08 Billion |

| Market Size (2031) | USD 6.11 Billion |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

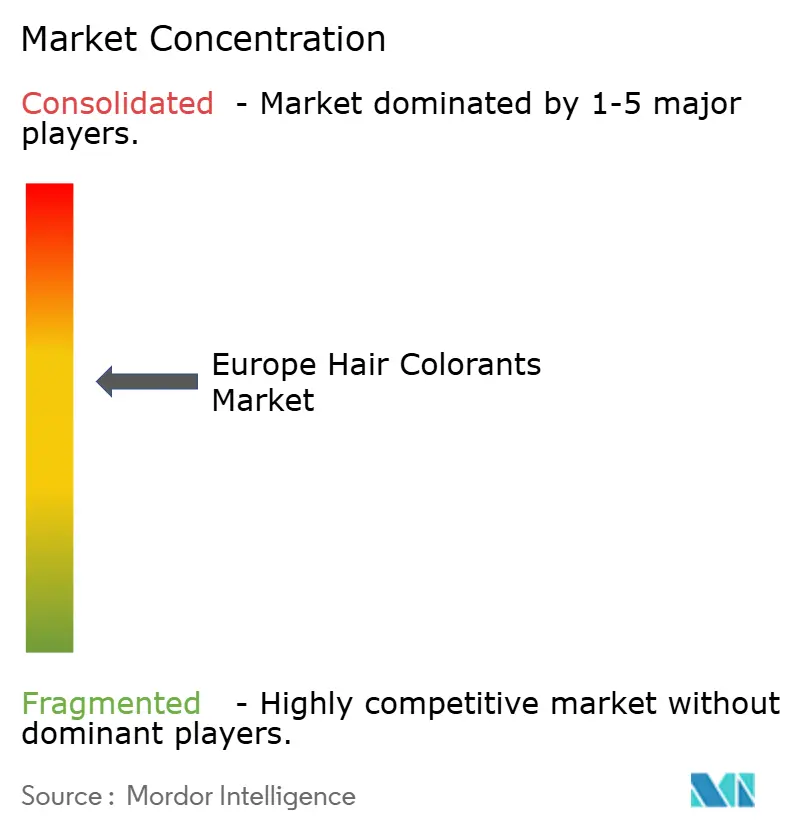

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Hair Colorants Market Analysis by Mordor Intelligence

The Europe hair colorant market size was valued at USD 4.90 billion in 2025 and estimated to grow from USD 5.08 billion in 2026 to reach USD 6.11 billion by 2031, at a CAGR of 3.75% during the forecast period (2026-2031). Urbanization, an aging population, and increasing beauty awareness are driving this growth. Additionally, premiumization, the expansion of digital retail, and a focus on ingredient transparency are contributing to higher average selling prices. The growing adoption of hair coloring by men for grooming and styling further supports market expansion. Innovations have introduced more natural, organic, and ammonia-free hair colorants, addressing consumer concerns about chemical exposure and environmental impact. Germany leads in sales with an extensive retail network, while the United Kingdom surpasses its peers due to strong e-commerce penetration and influencer-driven premium demand. Permanent shades remain the most popular choice among consumers, but temporary formats are experiencing the fastest growth, fueled by social media-driven experimentation. Online retailers and direct-to-consumer brands are gaining market share by utilizing personalized color-matching tools that streamline consumer decision-making and improve conversion rates.

Key Report Takeaways

- By product type, permanent colorants led with 48.35% of the European hair colorant market share in 2025; temporary colorants are projected to post the fastest 4.67% CAGR through 2031.

- By category, conventional formulations held 85.12% revenue share in 2025, while organic alternatives are on track to expand at a 4.40% CAGR to 2031.

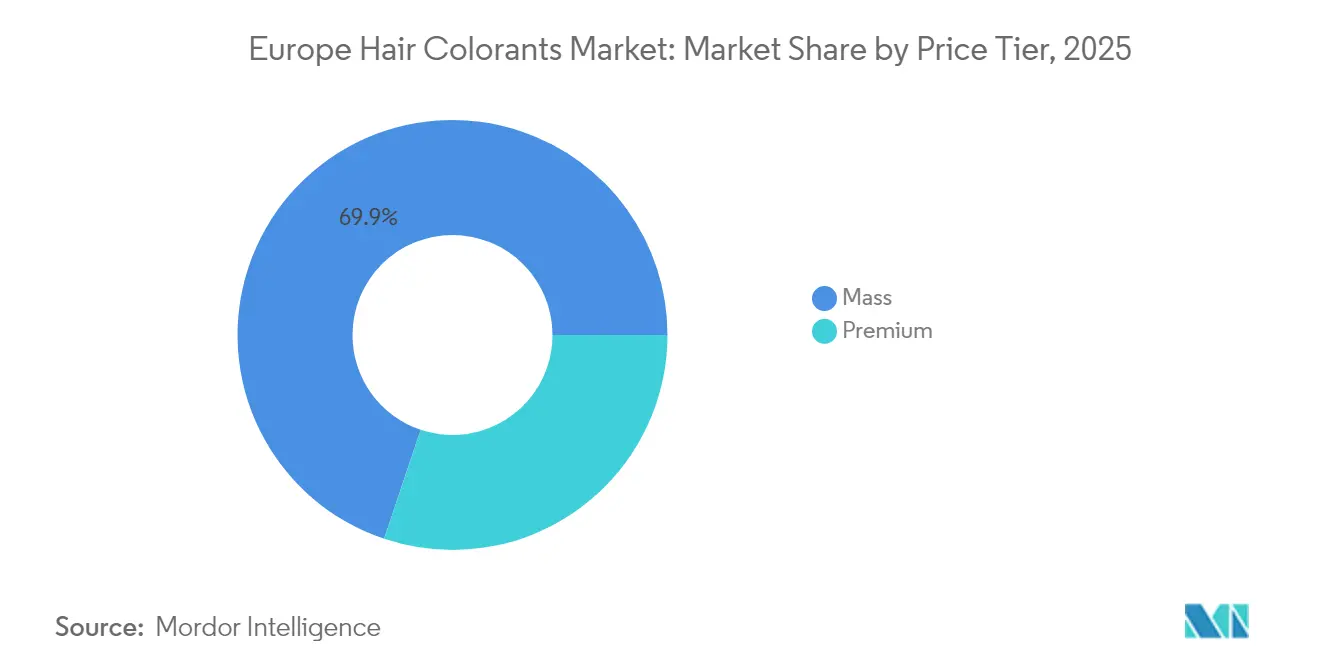

- By price tier, mass products accounted for 69.85% of the European hair colorant market size in 2025, and premium lines are forecast to advance at a 4.95% CAGR.

- By distribution, specialist retailers captured 39.45% of sales in 2025, whereas online retail is positioned for a 5.32% CAGR up to 2031.

- By geography, Germany contributed 21.15% of the 2025 value; the United Kingdom is expected to be the fastest-growing country at 4.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Hair Colorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer focus on personal grooming | +0.8% | Europe-wide, strongest in Germany, France, Italy | Medium term (2-4 years) |

| Rising demand for natural and organic formulations | +0.6% | Nordic countries, Germany, Netherlands | Long term (≥ 4 years) |

| Aging population boosting grey-coverage demand | +0.9% | Italy, Portugal, Bulgaria (highest elderly shares) | Long term (≥ 4 years) |

| Social media and influencer impact | +0.5% | United Kingdom, France, Spain (high digital engagement) | Short term (≤ 2 years) |

| Increasing popularity of DIY at-home hair coloring | +0.4% | Northern Europe, urban centers | Medium term (2-4 years) |

| Product innovation and customization | +0.3% | Germany, France, United Kingdom (innovation hubs) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing consumer focus on personal grooming

European consumers are increasingly prioritizing appearance-enhancing products, showcasing a stronger inclination to invest in beauty solutions. This trend extends beyond clinical treatments to include premium hair colorants designed to deliver salon-quality results in the comfort of home. It reflects a broader transformation in consumer behavior, where personal grooming has evolved into a form of self-expression and a way to boost confidence, moving beyond its traditional role of basic upkeep. The growing influence of social media has further normalized beauty treatments, creating a psychological shift that encourages higher spending on appearance-related products. This trend is particularly evident among the 19-34 age group, which has recorded the highest increase in the adoption of aesthetic treatments. In 2024, 16% of Europe's population was under 15 years old, as reported by the Population Reference Bureau[1]Source: Population Reference Bureau, "World Population Data Sheet 2024", prb.org. This young demographic's growth is set to drive a steady demand for these products. Recognizing this opportunity, European brands are innovating to bridge the gap between professional and consumer markets. A notable example is L'Oréal's Colorsonic device, which automates the mixing and application process, enabling users to achieve salon-like precision and results at home.

Rising demand for natural and organic formulations

European consumers are placing greater emphasis on natural ingredients, influenced by regulatory frameworks such as the European Green Deal and the Corporate Sustainability Due Diligence Directive, which require supply-chain traceability and environmental accountability. Consequently, the EU's natural cosmetics segment is growing faster than conventional formulations, reflecting consumers' preference for products that align with sustainability values. Regulatory pressures further reinforce this trend. For example, the ECHA's classification of tea tree oil as a reproductive toxicant Category 1B demonstrates how safety scrutiny can restrict traditional natural ingredients, prompting reformulation toward botanicals verified as safe. In 2024, European importers purchased natural cosmetic ingredients valued at EUR 2.221 million, with developing countries contributing 33% of this value[2]Source: Center for the Promotion of Imports from Developing Countries, "What is the demand for natural ingredients for cosmetics on the European market", cbi.eu. This highlights significant supply-chain investments in sustainable sourcing. Suppliers providing certified organic, fair-trade, or UEBT-verified ingredients are gaining competitive advantages, while conventional manufacturers are being pushed to reformulate their products. Companies like Kemon are responding by offering products containing up to 70% natural-origin ingredients, calculated according to ISO 16128 standards, positioning natural content as a key differentiator.

Aging population boosting grey-coverage demand

Europe's demographic transformation creates sustained demand for grey-coverage solutions, with 21.6% of the EU population aged 65+ in 2024, according to Eurostat[3]Source: Eurostat, "Population structure and aging", ec.europe.eu. Italy stands out with 24.3% of its population in this age group, followed closely by Portugal at 24.1%, making these countries significant demand hubs for age-specific hair care formulations. Furthermore, Greece, Italy, Portugal, and Slovakia have experienced a median age increase, signaling a notable acceleration in market growth within these regions. This demographic transformation is not limited to grey coverage alone but also includes products designed to address broader age-related hair concerns, such as thinning, changes in hair texture, and increased scalp sensitivity. In response to these evolving needs, Henkel's Schwarzkopf has introduced its Keratin Root products, which provide 100% grey coverage in just 10 minutes. These products are specifically formulated with bond-enforcing systems to cater to the unique requirements of mature hair. The industry is also witnessing a shift toward the development of gentler chemical formulations that minimize scalp irritation while ensuring effective and reliable coverage. Additionally, European manufacturers are redefining the positioning of grey-coverage products. Rather than marketing them solely as tools for concealing age, these products are increasingly being promoted as lifestyle enhancers that empower individuals to embrace aging with confidence. This shift reflects changing societal attitudes toward aging, emphasizing personal empowerment and self-expression over traditional notions of age concealment.

Social media and influencer impact

Beauty brands are significantly transforming hair colorant purchasing decisions by leveraging digital platforms. They are utilizing livestreaming and short-form video content to enhance product discovery and foster deeper sales engagement. Social media plays a pivotal role in inspiring consumers visually, particularly for temporary and semi-permanent hair color formulations. These formulations allow users to experiment with trends without committing to long-term changes, making them highly appealing. This shift goes beyond traditional influencer marketing, encompassing user-generated content where consumers share their transformation results. Such content provides authentic social proof, often leading to the viral popularity of specific shades and techniques. A notable example of this strategy is Clairol's "It's So Me" campaign, launched in March 2024. The campaign featured a diverse lineup of global influencers who highlighted self-expression through hair color while demonstrating specific product applications. This approach has particularly resonated with younger demographics, who view hair color as an extension of their digital identity and self-presentation. Consequently, there is a rising demand for hair color formulations that are photogenic and perform well under various lighting conditions. In response to this trend, European brands are innovating by developing Instagram-optimized shades designed to stand out on social media platforms. They are also partnering with micro-influencers who showcase authentic usage scenarios, further enhancing the appeal and relatability of their products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergic reactions and tighter European Union chemical rules | -0.7% | Europe-wide, strictest in Nordic countries | Short term (≤ 2 years) |

| Presence of counterfeit and substandard products | -0.4% | Italy, France, Spain (major import hubs) | Medium term (2-4 years) |

| Pigment supply-chain volatility | -0.5% | Global impact, affecting all EU markets | Short term (≤ 2 years) |

| Price sensitivity in certain markets | -0.3% | Eastern Europe, economically pressured regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Allergic reactions and tighter European Union chemical rules

European hair colorant manufacturers face increasing compliance costs and restricted ingredient options due to stricter regulations. From September 2025, the EU will enforce a ban on 20 new CMR substances, requiring widespread reformulation across the industry. For example, trimethylbenzoyl diphenylphosphine oxide will transition from permitted use to a complete ban. The Scientific Committee on Consumer Safety continues to review hair dye substances, with HC Yellow No. 16 now subject to concentration limits of 1% in oxidative dyes and 1.5% in non-oxidative formulations, reflecting ongoing regulatory oversight. These regulations disproportionately affect smaller manufacturers, who may lack the resources for extensive reformulations, potentially leading to market consolidation favoring larger, well-funded companies. Additionally, the regulatory framework includes stricter packaging and labeling requirements, with enhanced traceability mandates increasing operational complexity and costs throughout the supply chain.

Presence of counterfeit and substandard products

Counterfeit beauty products undermine legitimate market growth. France experiences the highest absolute losses in the cosmetics sector, reflecting the economic impact of counterfeit goods on legitimate businesses. The rapid expansion of e-commerce platforms has further exacerbated the issue by providing counterfeit distributors with new avenues for operation. Criminals have adopted sophisticated methods, such as shipping low-cost packaging separately and assembling the counterfeit products within the EU, to bypass border detection mechanisms. Among the various product categories, hair colorants are particularly susceptible to counterfeiting due to their complex formulations, which make it difficult for consumers to verify authenticity. This vulnerability not only raises safety concerns but also erodes consumer trust in the category. The situation is further aggravated as counterfeiters exploit supply-chain disruptions and price volatility to flood the market with substandard products. These inferior goods not only undercut the pricing of legitimate products but also pose significant risks to consumer safety and damage the reputation of established brands. The combined impact of these factors underscores the urgent need for enhanced enforcement measures and industry collaboration to combat the growing counterfeit threat effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Permanents Lead, Temporaries Accelerate

Permanent colorants hold a 48.35% market share in 2025, highlighting European consumers' preference for durable solutions that deliver complete grey coverage and vibrant color changes. For many mature consumers, particularly women, covering grey hair is crucial to maintaining a youthful and natural appearance, with studies showing significantly higher adoption rates among women than men. However, temporary colorants are the fastest-growing segment, with a projected 4.67% CAGR through 2031. This growth is driven by a desire for experimentation and a low-commitment approach to hair coloring, reflecting the influence of fast-changing social media trends. This divergence in growth trends indicates a shift in consumer behavior: while traditional permanent solutions remain popular, there is increasing demand for flexible and reversible color options. Semi-permanent colorants offer a middle ground, providing moderate longevity without the commitment of permanent formulations. Meanwhile, bleachers and highlighters cater to specialized needs, enabling bold color transformations and accent techniques.

Schwarzkopf Professional's Chroma ID launch exemplifies the industry's response to the growing temporary segment. This product features a semi-permanent system designed for both salon express services and at-home maintenance, with a 5-15 wash cycle and a quick 3-10 minute development time. Meeting modern consumer demands for gentler yet effective solutions, the product incorporates a vegan formulation and FibreBond technology. The rapid growth of the temporary segment reflects a broader cultural shift, where consumers, inspired by social media, increasingly embrace experimentation and self-expression, normalizing frequent color transformations and changes in appearance.

By Category: Conventional Dominance Faces Organic Challenge

Conventional formulations hold an 85.12% market share in 2025, benefiting from well-established performance attributes and cost advantages that appeal to price-sensitive consumers across Europe. These conventional ingredients provide consistent coloration, reliable grey coverage, and durability, essential features for mass-market consumers. At the same time, organic alternatives are growing at a 4.40% CAGR (2026-2031), driven by regulatory pressures and increasing consumer demand for natural ingredients aligned with sustainability values. As organic formulations improve their performance and regulations further restrict synthetic options, the dominance of conventional products is expected to decline. This category split reflects the broader European consumer landscape: affluent demographics prioritize premium purchases influenced by health and environmental concerns, while cost-conscious consumers in the mass market continue to favor conventional products.

European regulations are increasingly supporting organic formulations by imposing restrictions on synthetic substances and implementing stricter labeling requirements to emphasize natural content. The European Unions classification of several substances into CMR categories 1A, 1B, or 2 adds pressure on conventional manufacturers to reformulate their products or face market exclusion. This evolving market dynamic also creates opportunities for hybrid formulations. By combining synthetic performance with natural positioning, manufacturers can cater to both segments while ensuring compliance with regulatory requirements.

By Price: Mass Market Stability, Premium Acceleration

Premium segments are projected to grow at a 4.95% CAGR through 2031, surpassing the mass market. This growth highlights a rising consumer preference for high-quality formulations that offer superior performance and brand prestige. In 2025, mass-market products hold a significant 69.85% share, driven by competitive pricing and extensive distribution. However, their growth rates trail behind premium segments as consumers increasingly prioritize quality over cost in discretionary beauty spending. This divergence reflects the European market's evolution, where established consumers seek unique experiences, while price-sensitive segments continue to demand functional solutions. The premium segment's growth aligns with Euromonitor's "renovation" trend, which emphasizes brands adopting premiumization strategies to attract younger demographics and justify higher price points through improved formulations and packaging.

L'Oréal's EUR 1.288 billion investment in research and development in 2024 exemplifies the innovation required to sustain premium positioning. Such investments enable brands to leverage technological advancements and performance differentiation to support premium pricing. L'Oréal's Melasyl launch, developed over 18 years and supported by 121 scientific studies, addresses localized pigmentation concerns and establishes intellectual property advantages that reinforce its premium pricing strategy. Additionally, digital distribution channels have significantly contributed to premium growth by fostering direct-to-consumer relationships and enabling personalized marketing strategies, which validate higher price points through tailored solutions. The evolving price segmentation indicates ongoing polarization, with premium brands capturing value-driven consumers, while mass-market players focus on accessibility and affordability.

By Distribution Channel: Specialists Hold, Online Surges

Specialist retailers hold a 39.45% market share in 2025, driven by their strong customer relationships and expertise in providing professional consultation services. These retailers feature a wide selection of hair colorants, including advanced professional, natural, and ammonia-free formulations, along with niche and trending brands that are typically unavailable in supermarkets and general retail outlets. Online retail channels are growing at a significant 5.32% CAGR (2026-2031), transforming the European hair colorant distribution landscape. This growth aligns with the broader adoption of e-commerce, as seen in Zalando's AI-powered expansion of beauty offerings across 25 European markets, which improves product discovery and purchase conversion rates. Supermarkets and hypermarkets ensure mass-market accessibility, while convenience stores cater to impulse purchases and provide coverage in underserved areas. Additionally, direct-to-consumer platforms and subscription services offer alternative touchpoints, bypassing traditional retail intermediaries.

Brands that effectively create engaging digital content and utilize social media to drive traffic and conversions are well-positioned to benefit from this online growth. However, this shift presents challenges for traditional specialist retailers, who must adopt omnichannel strategies that integrate physical consultations with digital convenience. Regulatory compliance also plays a critical role in shaping channel strategies. Online platforms, in particular, must comply with EU cosmetics regulations by ensuring accurate product labeling and safety information, adding operational complexity that favors established players with strong compliance capabilities.

Geography Analysis

Germany holds a dominant 21.15% share of the European hair colorant market in 2025, leveraging its position as the continent's largest economy and population. The German market thrives on a strong retail infrastructure, high disposable incomes, and well-established beauty consumption habits that cater to both mass-market and premium segments. However, challenges persist, with Douglas AG highlighting declining consumer sentiment and reduced purchasing power as factors limiting growth in Germany's beauty sector. The market's maturity allows brands to implement sophisticated segmentation strategies, targeting specific demographics and price points through established distribution networks. Additionally, Germany's regulatory framework, aligned with EU standards, benefits established players while posing challenges for smaller competitors lacking resources for extensive regulatory compliance.

Although smaller in size compared to its continental peers, the United Kingdom is the fastest-growing region, with a projected 4.42% CAGR through 2031. This growth is driven by factors such as rapid digital adoption, which fosters direct-to-consumer relationships, and premium positioning strategies that bypass traditional retail constraints. The United Kingdom's post-Brexit regulatory alignment with European Union cosmetics standards ensures market access while creating opportunities for innovative product development and marketing approaches. France and Italy maintain strong market positions, supported by their rich beauty traditions and established luxury status, which drive growth in the premium segment. In Spain, market dynamics reflect broader Southern European trends, where economic challenges heighten price sensitivity, while an aging population increases demand for grey-coverage products.

Eastern European markets, led by Poland, exhibit growth potential fueled by rising disposable incomes and increasing adoption of beauty products. However, price sensitivity continues to favor mass-market formulations over premium alternatives. The diverse nature of European markets offers opportunities for tailored strategies that address local preferences, regulatory requirements, and economic conditions. This geographic diversity enables efficient distribution and marketing strategies while intensifying competition in major markets, driving innovation, and exerting pricing pressures across the industry.

Competitive Landscape

The European hair colorant market exhibits moderate concentration with fragmented competitive dynamics, where established multinational players leverage scale advantages while specialized brands capture niche segments through innovation and targeted positioning. The market increasingly emphasizes technology-driven differentiation. For example, in January 2025, L'Oréal collaborated with IBM to develop generative AI models, enhancing formulation processes with a focus on sustainability and personalization. Additionally, strategic acquisitions are redefining the competitive landscape. In July 2025, L'Oréal expanded its professional haircare portfolio by acquiring Color Wow, while Henkel's acquisition of Vidal Sassoon in Greater China highlighted its geographic expansion strategy.

Industry leaders in the European hair colorants market include L'Oréal SA, Henkel AG and Co. KGaA, Coty Inc., Kao Corporation, and Revlon Inc. These companies prioritize product innovation, particularly in creating natural and ammonia-free formulations to meet the growing demand from health-conscious consumers. They are adopting omnichannel distribution strategies by partnering with online platforms while maintaining a strong presence in salons and retail stores. Their strategic initiatives include significant investments in research and development, sustainable packaging, and digital marketing campaigns aimed at attracting younger demographics.

Opportunities exist in specialized areas such as multicultural beauty formulations, sustainable packaging solutions, and personalized color matching technologies that address unmet consumer needs. Emerging players are leveraging digital-first strategies and direct-to-consumer models to bypass traditional distribution challenges while building loyal communities around specific product categories or demographic groups. This competitive environment drives continuous innovation in formulation chemistry, application technology, and consumer experience design. Companies are building extensive patent portfolios to protect their intellectual property. Regulatory compliance creates barriers that favor well-capitalized companies capable of managing complex substance restrictions and safety testing requirements. This dynamic limits market entry for smaller competitors who may lack the regulatory expertise and financial resources to navigate evolving EU cosmetics regulations and REACH restrictions.

Europe Hair Colorants Industry Leaders

-

L'Oréal S.A.

-

Revlon, Inc.

-

Coty Inc.

-

Kao Corporation

-

Henkel AG and Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Coloraqua has debuted its innovative water-based hair color in the United Kingdom. This redefined hair color prioritizes a clean, water-based formula, promising not only vibrant and long-lasting results but also emphasizing the health of both hair and scalp.

- June 2024: L'Oréal has entered into an agreement to acquire Color Wow, a premium professional haircare brand. This acquisition strengthens L'Oréal's Professional Products Division by adding award-winning solutions for frizz control, thickening, and volumizing, which have received strong stylist endorsements.

- January 2025: L'Oréal collaborated with IBM to develop generative AI models, enhancing formulation processes with a focus on sustainability and personalization.

- January 2025: Schwarzkopf Professional and Lakmé have collaborated to introduce a revolutionary ammonia-free hair color. This advanced range delivers exceptional results while ensuring hair health remains uncompromised.

Europe Hair Colorants Market Report Scope

Hair colorants provide a range of commercial products capable of coloring the hair in various shades and tints, ranging from very light blonde to black, passing through a range of tones, like golden ash, reddish, mahogany, violet, etc. The European hair colorants market is segmented by product type, distribution channel, and country. By product type, the market is further segmented into bleachers, highlighters, permanent colorants, semi-permanent colorants, and other product types. By distribution channel, the market is further segmented into supermarkets and hypermarkets, convenience stores, specialist retailers, online retail stores, and other distribution channels. Also, the study analyzes the hair colorants market in emerging and established markets across Europe, including the United Kingdom, Germany, France, Spain, Italy, Russia, and the Rest of Europe. For each segment, market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Bleachers |

| Highlighters |

| Permanent Colorants |

| Semi-Permanent Colorants |

| Temporary Colorants |

By Category

| Conventional |

| Organic |

By Price

| Mass |

| Premium |

By Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialist Retailers |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Belgium |

| Poland |

| Netherlands |

| Rest of Europe |

| By Product Type | Bleachers |

| Highlighters | |

| Permanent Colorants | |

| Semi-Permanent Colorants | |

| Temporary Colorants | |

| By Category | Conventional |

| Organic | |

| By Price | Mass |

| Premium | |

| By Distribution Channels | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialist Retailers | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe hair colorant market in 2026?

It is valued at USD 5.08 billion and is projected to reach USD 6.11 billion by 2031.

Which product category is growing fastest?

Temporary colorants are expanding at a 4.67% CAGR, benefiting from social-media-driven experimentation.

Why is the United Kingdom outpacing other countries in growth?

The UK leverages high e-commerce penetration and influencer marketing, yielding a 4.42% CAGR through 2031.

How are EU chemical regulations affecting manufacturers?

Bans on 20 new CMR substances effective September 2025 compel costly reformulation and favor scale players with strong research..

Page last updated on: