Europe Food Contract Manufacturing And Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

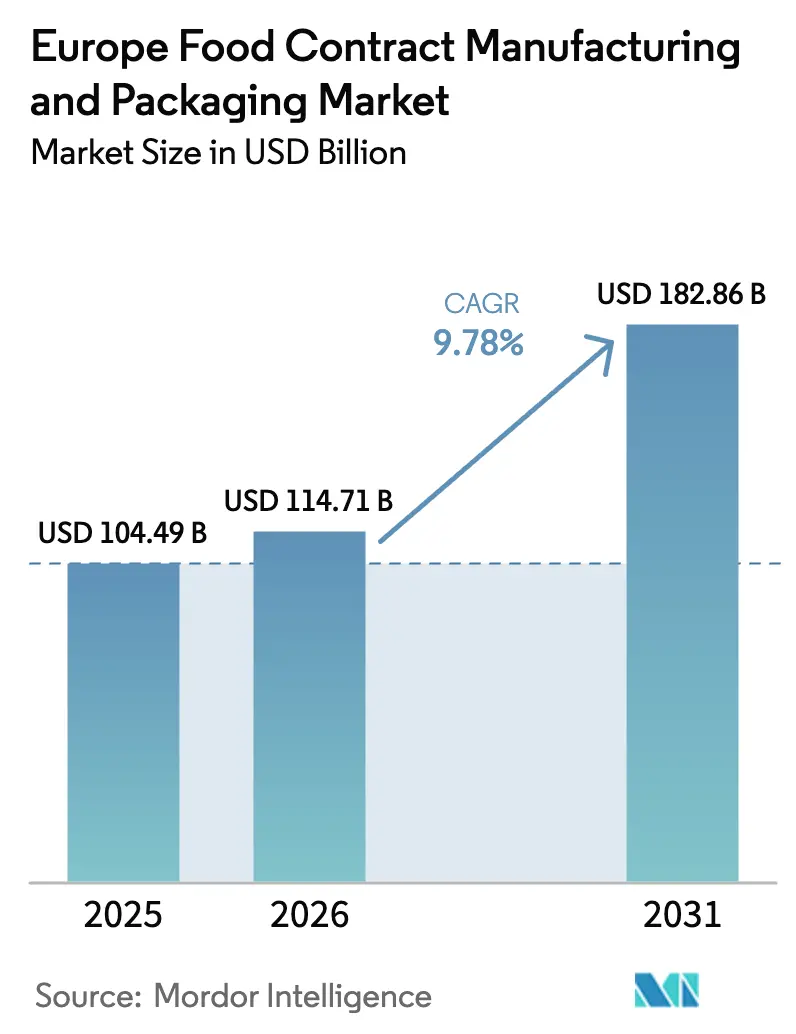

| Base Year Market Size (2025) | USD 104.49 Billion |

| Market Size (2026) | USD 114.71 Billion |

| Market Size (2031) | USD 182.86 Billion |

| Growth Rate (2026 - 2031) | 9.78% CAGR |

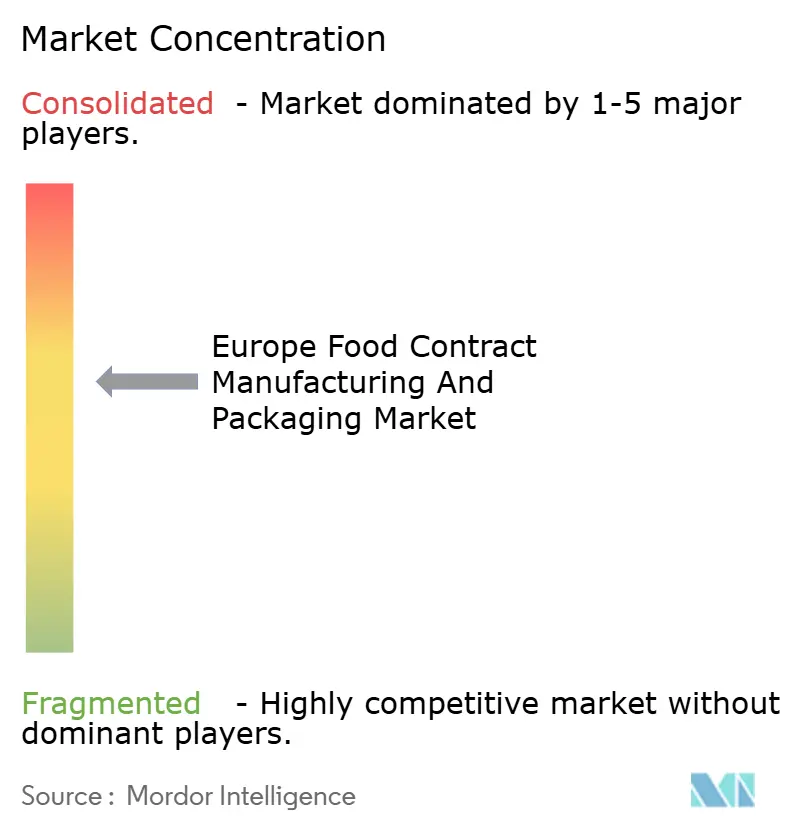

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Food Contract Manufacturing And Packaging Market Analysis by Mordor Intelligence

The Europe food contract manufacturing and packaging market size was valued at USD 104.49 billion in 2025 and estimated to grow from USD 114.71 billion in 2026 to reach USD 182.86 billion by 2031, at a CAGR of 9.78% during the forecast period (2026-2031). This rapid expansion is underpinned by brand owners shifting fixed assets off the balance sheet, tightening EU sustainability rules that favor specialized partners, and retailer pressure for agile private-label production. Processing and manufacturing services continue to anchor volumes, yet higher-margin custom formulation capabilities outpace the overall Europe food contract manufacturing and packaging market in growth as brands search for innovation speed. Digital factories, lower-carbon packaging formats, and allergen-controlled zones differentiate suppliers that can respond quickly to frequent SKU rotations. Meanwhile, volatile energy pricing and recycled-content mandates introduce compliance costs that only the most automated facilities can absorb without eroding margins.

Key Report Takeaways

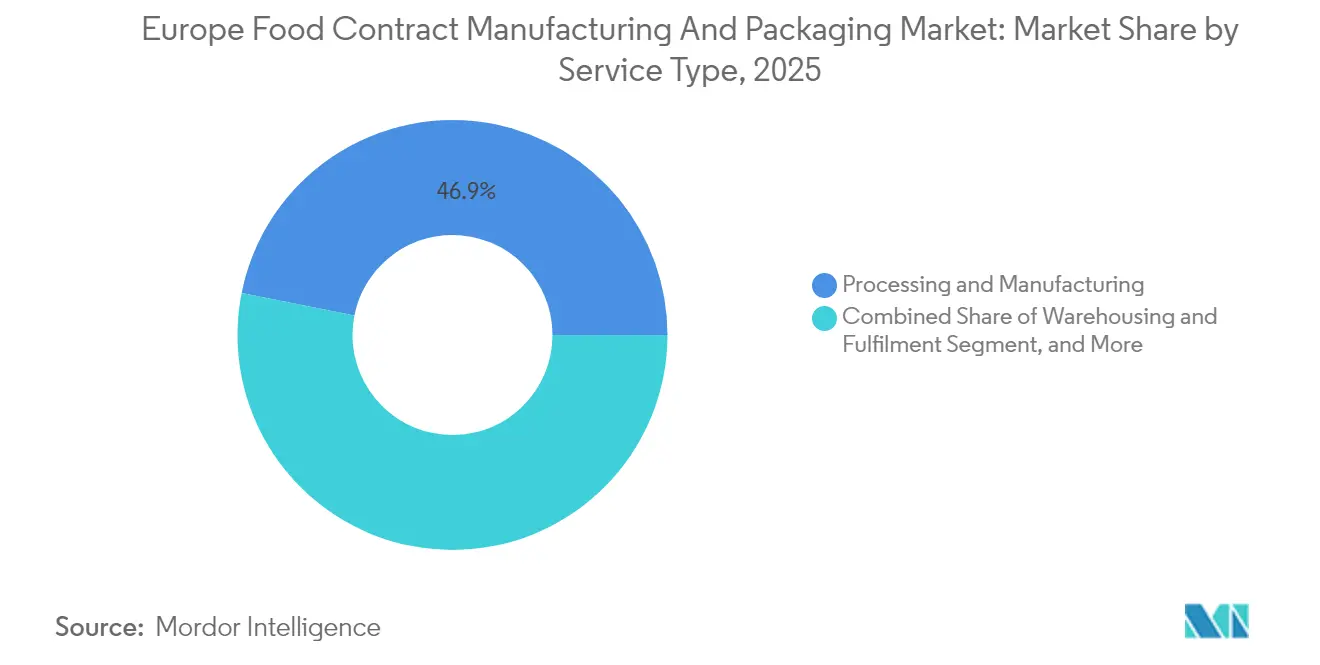

- By service type, processing and manufacturing led with 46.88% of the Europe food contract manufacturing and packaging market share in 2025; custom formulation and R&D is projected to expand at a 10.18% CAGR through 2031.

- By end-use industry, bakery and confectionery captured 29.85% of the Europe food contract manufacturing and packaging market size in 2025, while functional and nutraceutical products are forecast to grow at 10.98% CAGR to 2031.

- By packaging format, flexible solutions commanded 58.02% share of the Europe food contract manufacturing and packaging market in 2025 and are advancing at a 12.21% CAGR through 2031.

- By geography, Germany accounted for 27.95% share in 2025; Spain registers the fastest trajectory, rising at a 11.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Food Contract Manufacturing And Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Contract-manufacturers investing in allergen-free and plant-based lines | +1.8% | Germany, Netherlands, UK | Medium term (2-4 years) |

| Retail private-label expansion seeking flexible capacity | +2.1% | Germany, France, UK | Short term (≤ 2 years) |

| Digitalisation and cloud-connected factories improving line-changeover speeds | +1.5% | Germany, Netherlands, France | Medium term (2-4 years) |

| E-commerce meal-kit boom demanding fulfilment-ready packaging | +1.3% | UK, Germany, Netherlands | Short term (≤ 2 years) |

| EU Green Deal incentives for low-carbon packaging operations | +1.7% | EU-wide | Long term (≥ 4 years) |

| Commercialisation of upcycled ingredients supplying new value streams | +1.4% | Netherlands, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Contract-Manufacturers Investing in Allergen-Free and Plant-Based Lines

Facilities dedicated to allergen-free and plant-based production are scaling across Europe in response to stricter oversight from national food safety agencies. Mars allocated USD 140.4 million to modernize eight French sites in 2024, installing segregated air-handling and storage systems that eliminate cross-contact risk. Early movers secure multi-year contracts from brands that lack capital for specialized retrofits. The conversion cycle spans 18–24 months, temporarily tightening outsourced capacity but ultimately lifting overall throughput once finished. Demand is buoyed by a surge in vegan product launches and by public health authorities linking lifestyle diseases to overconsumption of animal proteins. For contract manufacturers, plant-protein texturization lines offer premium fees that offset the higher utility and certification expenses associated with allergen management. As a result, this trend lifts both revenue density and bargaining power within the Europe food contract manufacturing and packaging market.

Retail Private-Label Expansion Seeking Flexible Capacity

European grocers now use private-label margins to shield consumers from inflation shocks, driving unprecedented volatility in production schedules. NewPrinces’ USD 1 billion acquisition of Carrefour Italia in 2025 affirms the strategic value of in-house and contracted capacity that can handle multi-temperature portfolios. Retailers increasingly issue quarterly bid cycles rather than annual tenders, rewarding contractors that demonstrate sub-24-hour changeover. Flexible capacity contracts, typically 12–18 months in length, now include variable-volume clauses that shift inventory risk back to manufacturers. Those able to amortize frequent start-ups through digital twin scheduling and rapid sanitization protocols capture disproportionate wallet share in the Europe food contract manufacturing and packaging market.

Digitalization and Cloud-Connected Factories Improving Line-Changeover Speeds

AUTOMATED guided vehicles, predictive maintenance dashboards, and cloud-based recipe management are shrinking downtime from hours to minutes. MULTIVAC’s EUR 100 million (USD 117.2 million) Factory 2 in Germany integrates driverless transport and automated process chains that lift overall equipment effectiveness by up to 30%. Cloud connectivity allows quality teams to trace deviations in real time, slashing waste and accelerating release approvals. For brand owners, the ability to run micro-batches without penalty is a key selection criterion when outsourcing functional and nutraceutical products. Consequently, digitally mature plants advance from price-taker status to strategic co-innovation partners within the Europe food contract manufacturing and packaging market.

E-Commerce Meal-Kit Boom Demanding Fulfillment-Ready Packaging

Meal-kit subscriptions require portion-controlled packs that maintain freshness for 48-hour delivery windows. HelloFresh’s automated fulfillment hubs rely on contract packers capable of integrating temperature indicators and step-by-step instructions in a single SKU. Packaging lines engineered for secondary assembly, placing sauces, proteins, and produce into corrugated inserts, secure long-term contracts as urban penetration plateaus and rural deliveries grow. Material choices favor light-gauge films paired with renewable insulation, aligning with PPWR recyclability thresholds. Contract manufacturers that co-locate cold-storage and pick-and-pack services command premium conversions per square meter, reinforcing their share of the Europe food contract manufacturing and packaging market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compression of brand owner price margins passed to contractors | -1.9% | EU-wide | Short term (≤ 2 years) |

| Tightening EU Single-Use Plastics and PPWR rules raising compliance costs | -1.4% | EU-wide | Medium term (2-4 years) |

| Heightened food-safety liability driven by Listeria/Allergen recalls | -1.2% | EU-wide, particularly Germany, France | Short term (≤ 2 years) |

| Volatile energy and logistics prices disrupting production planning | -1.6% | Germany, UK, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Compression of Brand Owner Price Margins Passed to Contractors

Food inflation peaked at 5.1% in the United Kingdom during 2025, prompting retailers to cap shelf prices and force suppliers to absorb input spikes. Electricity and gas tariffs doubled versus 2020 baselines, eroding contribution margins on energy-intensive cooking and drying lines.[1]Department for Environment, Food & Rural Affairs, “United Kingdom Food Security Report 2024,” gov.uk While tier-one contractors negotiate pass-through clauses or hedge energy, mid-sized firms face a margin squeeze that dampens capital spending. Constrained cash flow slows automation upgrades, widening performance gaps inside the Europe food contract manufacturing and packaging market.

Tightening EU Single-Use Plastics and PPWR Rules Raising Compliance Costs

The PPWR stipulates 10% minimum recycled content for beverage cartons by 2030 and sharply restricts multilayer films that impede sorting. Elopak’s PPWR-compliant cartons illustrate the expense of redesign and certification costs that many small contractors cannot shoulder. Capital investment bursts ahead of regulatory deadlines, drives up equipment lead times, and inflates project budgets. Some niche packers exit PET or multilaminate categories altogether, trimming available capacity just as demand for recyclable formats accelerates, putting upward pressure on tolling rates in the Europe food contract manufacturing and packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Processing Maintains Scale Advantage

Processing and manufacturing held 46.88% of the Europe food contract manufacturing and packaging market share in 2025, underscoring its role as the volume backbone for private-label staples. Its scale benefits allow contractors to leverage bulk ingredient procurement and continuous-flow machinery, keeping unit costs competitive for branded and retailer customers. Simultaneously, the custom formulation and R&D segment is forecast to grow at a 10.18% CAGR through 2031, signaling brand owner urgency to commercialize differentiated concepts without building in-house pilot plants. The Europe food contract manufacturing and packaging market size for custom formulation services is thus expected to swell as clinical-substantiated nutraceuticals and clean-label emulsions move from lab to shelf within a single quarterly cycle.

Advances in micro-batch encapsulation, such as ACG’s personalized capsule platform, illustrate how contractors monetize formulation IP through premium fee structures. Warehousing and fulfillment services benefit from rising direct-to-consumer flows, but pricing remains volume-linked, placing a strategic emphasis on real-time inventory visibility to optimize cube utilization. Packaging services face margin uplift as EU recyclability mandates require continuous redesign and regulatory validation, a complexity most brand owners prefer to outsource. Overall, the Europea food contract manufacturing and packaging market continues to tilt toward contractors capable of bundling formulation, processing, and compliant packaging into a single turnkey proposition..

By End-Use Industry: Functional Products Outpace Legacy Categories

Bakery and confectionery led with 29.85% share of the Europe food contract manufacturing and packaging market in 2025, buoyed by premium chocolate lines and artisanal sourdough formats. The category relies on temperature-controlled enrobing and high-shear mixing that many small brands cannot afford, reinforcing outsourcing necessity. Meanwhile, functional and nutraceutical products are projected to expand at an 10.98% CAGR, driven by aging demographics and preventive health spending. The Europe food contract manufacturing and packaging market size for functional SKUs is set to widen further as novel-food approvals for botanical extracts shorten under the updated EFSA framework.

IRCA’s investment in high-protein chocolate chips typifies how contractors pivot specialty capacity toward performance nutrition. Dairy production leverages continuous fermentation upgrades to meet demand for Greek-style yogurt and plant-based alternatives, though margin volatility from whey and almond raw materials tempers segment profitability. Convenience and ready meals grow steadily as dual-income households trade cooking time for portion-controlled formats, securing consistent throughput for multi-tray retort lines. Emerging industries from insect protein burgers to cell-grown chicken nuggets seek pilot-scale partners to validate recipes ahead of regulatory clearance, ensuring a pipeline of high-margin prototypes for Europe’s most innovative contractors.

By Packaging Format: Flexible Films Consolidate Leadership

Flexible solutions captured 58.02% of the Europe food contract manufacturing and packaging market in 2025, propelled by e-commerce parcel weight limits and consumer preference for resealable pouches. The format’s 12.21% CAGR through 2031 outstrips rigid options as mono-material laminates satisfy PPWR recyclability thresholds without sacrificing barrier performance. Saica Group’s paper-based multipack for Mondelez shows how kraft substrates combined with bio-coatings deliver shelf-life parity to plastic while lowering CO₂ footprints.

Rigid cans and jars fight back via lightweighting and post-consumer recycled content, as seen in Sonoco’s 88% recyclable paper-can supplied to Lorenz in August 2025. Bottles integrate tethered caps and sleeve perforations to pass deposit-return criteria, though capital costs for blow-mold upgrades deter small converters. Trays pivot toward mono-PP or PET structures with functional coatings, exemplified by Südpack’s Pure Line flowpacks that cut emissions 27% while maintaining high-oxygen barriers. As brand owners juggle shelf aesthetics with end-of-life obligations, contractors that can run both flexible and next-generation rigid lines capture wider wallet share across the Europe food contract manufacturing and packaging market.

Geography Analysis

Germany commanded 27.95% of the Europe food contract manufacturing and packaging market in 2025, reflecting world-class engineering talent and adjacency to major consumer hubs. MULTIVAC’s EUR 100 million (USD 117.2 million) Wolfertschwenden expansion embeds Industry 4.0 protocols that reinforce the nation’s leadership in precision food machinery. Spanish revenues, while smaller in absolute terms, are forecast to rise at a 11.83% CAGR through 2031 as Kraft Heinz’s EUR 70 million (USD 82.07 million) capacity addition boosts domestic employment and export readiness.

The United Kingdom leans on premium and organic positioning to offset post-Brexit supply chain friction, with DEFRA data revealing that 30% of corrugated inputs still cross EU borders. France attracts confectionery investment on the back of Mars’ multi-site expansion aimed at net-zero manufacturing. Italy leverages culinary heritage to secure niche co-packing contracts for sauces and ready-meals, while smaller Central and Eastern European states court greenfield projects through tax holidays. Collectively, regional specialization underpins a resilient yet dynamic landscape within the broader Europe food contract manufacturing and packaging market.

Germany’s entrenched industrial base, combined with advanced automation, secures its position as the operational hub of the Europe food contract manufacturing and packaging market. Factory density supports cluster economies, enabling shared cold-chain logistics and pooled labor training programs that raise overall productivity. Federal subsidies for renewable heat and waste-water recovery further tilt investments toward domestic upgrades rather than offshoring. The presence of equipment majors, including packaging-line OEMs, ensures rapid maintenance turnaround, a decisive factor for high-speed confectionery and dairy fillers.

Spain’s ascent reflects favorable wage differentials, strategic Mediterranean port access, and government grants that offset capital costs for greenfield plants. Kraft Heinz’s new site illustrates how multinational brands choose Spain as a launchpad for southern European and North African distribution. Regional clusters in Catalonia and Andalusia now offer integrated ingredient sourcing, packaging, and cold-chain corridors, shrinking lead times for ready-meal exporters. Energy from expanding solar capacity mitigates electricity price volatility, enhancing competitiveness for energy-intensive bake and snack operations.

The United Kingdom contends with rules-of-origin documentation and sanitary checks that extend inbound ingredient lead times. Contractors respond by dual-sourcing EU and domestic materials, inflating inventory and working-capital needs. Simultaneously, government grants for automation under the Made Smarter program spur robotics adoption in mixing, portioning, and case-packing. France enjoys deep dairy expertise and consumer preference for premium chocolate, drawing continuous investment in allergen-controlled lines that service global luxury brands. Italy’s artisan reputation secures co-exports for sauce, pesto, and filled pasta, while Central-Eastern Europe alloys lower labor costs with EU market access, making it a magnet for entry-level production runs. This mosaic of capabilities fosters intra-regional supply agility that undergirds the long-term vitality of the Europe food contract manufacturing and packaging market.

Regulatory Landscape

Food contract manufacturing and packaging in Europe operates under a combined food safety and packaging compliance stack, with food contact materials governed by Regulation (EC) 1935/2004 and Good Manufacturing Practice requirements under Regulation (EC) 2023/2006. For plastic food contact materials, Regulation (EU) No 10/2011 drives substance authorization and Declaration of Compliance expectations across converters and co-packers, while the European Commission continues list maintenance through updates such as Regulation (EU) 2026/245 (February 2026) amending Annex I of the plastics Union list.

Packaging sustainability compliance has tightened through Regulation (EU) 2025/40 (Packaging and Packaging Waste Regulation, PPWR), which entered into force in February 2025 and applies from 12 August 2026. In parallel, bisphenol controls have become more prescriptive via Commission Regulation (EU) 2024/3190, supported by corrective Regulation (EU) 2026/250 (February 2026), with transitional market placement allowances for certain BPA-related single-use final food contact articles running up to 20 July 2026. These timelines accelerate reformulation of coatings, inks, and barrier layers and increase documentation and change-control requirements for outsourced packers.

Value Chain Analysis

The value chain spans upstream agricultural and ingredient suppliers, food processors and brand owners, contract manufacturers and co-packers (processing, blending, filling, secondary assembly, and warehousing/fulfilment), packaging material suppliers (films, cartons, cans, closures, labels), and processing and packaging machinery OEMs. Industry bodies and coordinators, including the European Commission agri-food industrial ecosystem framework, FoodDrinkEurope, EUROPEN, EPPA, EUROPAMA, and the European Co-Packers Association (ECPA), help align best practices, while competent authorities enforce food safety and food contact material rules that require chain-of-custody and compliance documentation to move from packaging producers through co-packers to retailers.

Midstream scale and specialization are increasingly built through acquisitions and site additions that tighten integration between ingredients and outsourced production. FERM FOOD acquiring Orkla's former site in Skovlund, Denmark (effective 1 April 2026) expands fermented ingredients capacity to 20,000 tonnes per year, while Schouten Europe acquiring Bobeldijk Food Group in June 2026 expands private-label plant-based capacity. Compliance pull-through from PPWR application starting August 2026 reinforces demand for packaging-material collaboration (design-for-recycling, PFAS-free structures) and elevates the role of machinery and process automation providers in enabling faster changeovers and more auditable production runs.

Competitive Landscape

The Europe food contract manufacturing and packaging market exhibits moderate concentration, with the top five players collectively estimated to hold just under 45% of regional revenue. Industry leaders differentiate through scale, digital maturity, and sustainability credentials. Hearthside, for example, integrates real-time OEE dashboards that feed directly into customer portals, offering transparency that smaller firms cannot match. CordenPharma’s EUR 900 million (USD 1,055.2 million) peptide expansion underscores the strategic value of deep technical specialization, enabling premium pricing for clinical-grade nutraceuticals.

New entrants seize white space by focusing on fiber-based packaging or allergen-free confectionery. Papacks’ molded fiber bottle prototype achieves a 90% carbon reduction relative to PET, positioning the company as a go-to partner for zero-plastic initiatives.[3]Deniz Ataman, “Papacks bets on fiber bottles,” FoodNavigator-USA, foodnavigator-usa.com Automation catalyzes consolidation; mid-tier packers unable to fund robotics retrofits increasingly accept acquisition offers from private-equity-backed platforms seeking geographic roll-ups. Regulatory complexity becomes a barrier to entry, cementing the advantage of incumbents with embedded compliance teams and ISO-certified quality management systems. As procurement teams award multi-category, multi-year contracts, the purchasing power of brand owners ushers in performance-based fee structures that reward throughput, scrap minimization, and carbon intensity metrics.

Strategic alliances emerge between ingredient suppliers and co-packers to lock in demand for novel proteins and functional additives. Example: a leading oat-milk concentrate maker grants exclusive processing rights to a German packer in exchange for guaranteed minimum volumes across Benelux retail chains. Such vertical collaborations tighten the supply web and raise switching costs, thereby reinforcing share stability across the Europe food contract manufacturing and packaging market.

Europe Food Contract Manufacturing And Packaging Industry Leaders

Romix Foods Limited

Aimia Foods Ltd

Alphapak International Limited

A and S Packing Company Limited

Alexir Co-Packers Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

PPWR implementation creates near-term whitespace for contractors that can deliver compliant, fulfillment-ready packaging at scale, especially for flexible and fiber-forward solutions, while meeting food contact material documentation needs across multi-country supply chains. Regulation (EU) 2025/40 applies from 12 August 2026 and includes food-contact PFAS thresholds from that date, and the European Commission is also tasked with standardization and harmonized labeling workstreams, including a mandate to request a home-compostability standard by 12 February 2026 and implementing acts for harmonized material-composition labels by 12 August 2026. Contractors that can qualify alternative barrier systems, manage recycled-content traceability, and run short lead-time SKU rotations with auditable controls are positioned to take on redesign, revalidation, and re-launch workloads that brand owners and retailers are pushing outward.

Capacity and capability investments across ingredients and formulation-adjacent manufacturing also broaden the outsourcing pipeline for functional foods, sports nutrition, and premium confectionery inputs that often require specialized handling and packaging formats. FrieslandCampina Ingredients completed a Borculo (Netherlands) expansion in March 2026 that doubled capacity for whey protein isolate and milk fat globule membrane ingredients, Symrise opened an upgraded food and beverage site near Barcelona in April 2026 with new large-scale mixing capacity for powdered solutions, and Cargill announced EUR 56 million across three Belgian sites in June 2026 spanning edible oils, gourmet chocolate, and an extrusion pilot plant. These additions increase the volume of high-value ingredients and semi-finished bases moving through European supply chains, supporting opportunities for contract manufacturers and co-packers that can integrate formulation-to-pack, allergen control, and compliant, retailer-ready packaging within a single operating footprint.

Recent Industry Developments

- July 2026: Lappi Labels and Flexible Packaging acquired Portuguese flexible packaging provider Alempack, expanding the group footprint across Spain and Portugal and strengthening industrial capacity in doypack and flowpack formats. The added scale supports higher-volume contract packaging programs and improves response time for brands shifting toward recyclable flexible structures under tightening EU packaging rules.

- September 2025: BioTechUSA tripled protein bar production capacity and launched two premium lines, expanding throughput in sports nutrition manufacturing. The step-up in specialized capacity supports faster private-label and branded innovation cycles in functional and nutraceutical products, a key growth pocket for outsourced production.

- August 2024: AB Mauri UK and Ireland acquired specialty blending business Romix Foods, keeping the existing management team in place. The deal strengthens blending and dry-mix capabilities that feed into contract manufacturing and packing programs, supporting more integrated ingredient-to-pack offerings for bakery and adjacent food categories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned in Europe from outsourced food manufacturing and outsourced food packaging services that brand owners and retailers contract out to specialist service providers, including related service activities that are sold as part of the contract.

Scope exclusions: We exclude in-house food production and packaging done within the brand owner or retailer, along with upstream raw material sales that are not part of a contract service fee.

Segmentation Overview

- By Service Type

- Processing and Manufacturing

- Packaging

- Warehousing and Fulfilment

- Custom Formulation and R&D

- By End-Use Industry

- Bakery and Confectionery

- Dairy Products

- Convenience and Ready Meals

- Functional and Nutraceutical Products

- Other End-Use Industries

- By Packaging Format

- Flexible

- Pouches and Sachets

- Bags

- Other Flexible Packaging

- Rigid

- Bottles and Jars

- Cans

- Pallets

- Cartons

- Other Rigid Packaging

- Flexible

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries and to build the first pass of volume and value indicators by country and food category. We reviewed public sources such as Eurostat production and structural business statistics, UN Comtrade trade flows for packaged foods and key packaging materials, the European Commission pages on food labeling and packaging waste rules, and national statistics offices for food manufacturing output and price indices.

To keep the model tied to real company activity, we also used annual reports and investor presentations of large food producers and packaging service providers, along with reputable press and association updates on capacity expansions, sustainability conversions, and outsourcing trends. Where public financial splits were limited, we used paid subscriptions for company financials and news intelligence, plus an import and export shipment-level database to sanity-check cross-border flows of packaged food products. These sources are not exhaustive, and many other public documents and data points were consulted to collect, validate, and clarify assumptions.

Primary Interviews and Surveys

Primary interviews and surveys were run to confirm what is typically outsourced versus kept in-house, and to test the pricing logic used for service contracts across major European countries. We spoke with a mix of contract manufacturers, contract packers, ingredient and packaging procurement teams, and brand-side operations leaders, so gaps from desk research could be closed and key assumptions cross-checked across Western and Southern Europe.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | |

| Mid tier: 49% | Functional/Unit leaders: 39% | |

| Smaller Players: 14% | Managers: 47% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build that reconstructs the outsourced demand pool from Europe food output and packaging conversion activity, and then allocates the share that is typically handled by third-party service providers. At the same time, we use selective bottom-up checks, such as sampled provider revenue roll-ups, channel checks on common contract types, and simple ASP x volume approximations for high-visibility packaging formats, which are then used to adjust totals where needed.

The main inputs in the model include food manufacturing output by country, private-label penetration and co-manufacturing reliance, packaging mix shifts (flexible versus rigid), average contract packaging and co-packing service rates, energy and labor cost passthrough behavior, and regulatory-driven redesign cycles tied to packaging waste and labeling requirements. For forecasting, we used scenario analysis supported by primary expert views on outsourcing intensity, capacity additions, and price reset frequency in service contracts, and then stress-tested results using recent inflation and production index trends. When company-level splits were not available, revenue was inferred using observable capacity signals, typical utilization ranges, and validated service scopes, and then the estimates were normalized to avoid double counting across bundled contracts.

Data Validation & Update Cycle

Before results are finalized, outputs are checked against independent signals such as country-level food production value, packaging activity indicators, and visible contract manufacturing and packaging capacity movements. Any sharp changes are re-tested by revisiting the underlying drivers, and follow-up calls are triggered when a data point conflicts with multiple interview inputs, or when new policy timelines change service demand.

A multi-step review is used so assumptions, calculations, and country splits are checked by another analyst prior to sign-off. The report is refreshed annually, and interim updates are made when material events occur, such as major site expansions, large contract wins, or sudden cost shocks. Right before delivery, we run a final update pass so clients receive the most current view supported by traceable inputs.

Mordor Intelligence's Europe Food Contract Manufacturing and Packaging Market Size Versus Other Published Estimates

Published values for this market can look far apart because the word contract is treated differently across studies, and some also mix in adjacent service lines that are not always sold as a distinct outsourcing fee. Differences also come from how analysts treat bundled contracts, what currency timing is used, and whether the estimate is updated after a large contract shift or a regulation-driven packaging redesign.

Some estimates widen the scope by adding general packaging services and broader logistics activities for food products across Europe. In Mordor Intelligence, the value is counted when a third-party provider earns revenue for food contract manufacturing and contract packaging services, with warehousing and fulfillment included only when it is contracted and billed as part of the same service engagement.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 114.71 B (2026) | |

| Industry Database A | USD 123.90 B (2026) | Often bundles broader packaging services and outsourced logistics for food, which can pull in activity not tied to food co-manufacturing or contract packaging fees, and it may not net out overlaps when one provider subcontracts part of the work. |

| Trade Journal B | USD 98.40 B (2025) | Typically focuses on co-manufacturing revenue only, leaving out a large share of contract packaging, rework, and compliance-driven relabeling services, and it can apply conservative service-rate assumptions that lag recent contract repricing. |

The table shows that the spread is mainly explained by scope choices and how bundled service contracts are treated in the math. By tying the total to outsourced service revenues and then checking it against visible production and packaging activity indicators, we keep the estimate repeatable, and we reduce the risk of over-counting adjacent services or missing contract packaging value that is material in Europe.

Key Questions Answered in the Report

What is the current value of the Europe food contract manufacturing and packaging market?

The market is valued at USD 114.71 billion in 2026 and is forecast to reach USD 182.86 billion by 2031.

Which service segment is growing fastest across European outsourcing?

Custom formulation and R&D services are projected to grow at a 10.18% CAGR through 2031 as brands seek rapid innovation.

Which packaging format dominates contract packing in Europe?

Flexible formats lead with 58.02% share in 2025 and are expected to expand at a 12.21% CAGR, driven by e-commerce and sustainability mandates.

Which country shows the highest growth rate in European food contract manufacturing?

Spain is forecast to record a 11.83% CAGR through 2031 following significant capacity investments.

How do EU sustainability regulations impact contractors?

The PPWR and Green Deal require recycled content and carbon reduction, pushing contractors to invest in recyclable materials and low-carbon operations.

What recent investments signal confidence in the sector?

High-profile projects include Kraft Heinz’s EUR 70 million (USD 82.07 million) Spanish plant and MULTIVAC’s EUR 100 million (USD 117.2 million) German expansion, both completed or announced in 2024-2025.

Page last updated on: