Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

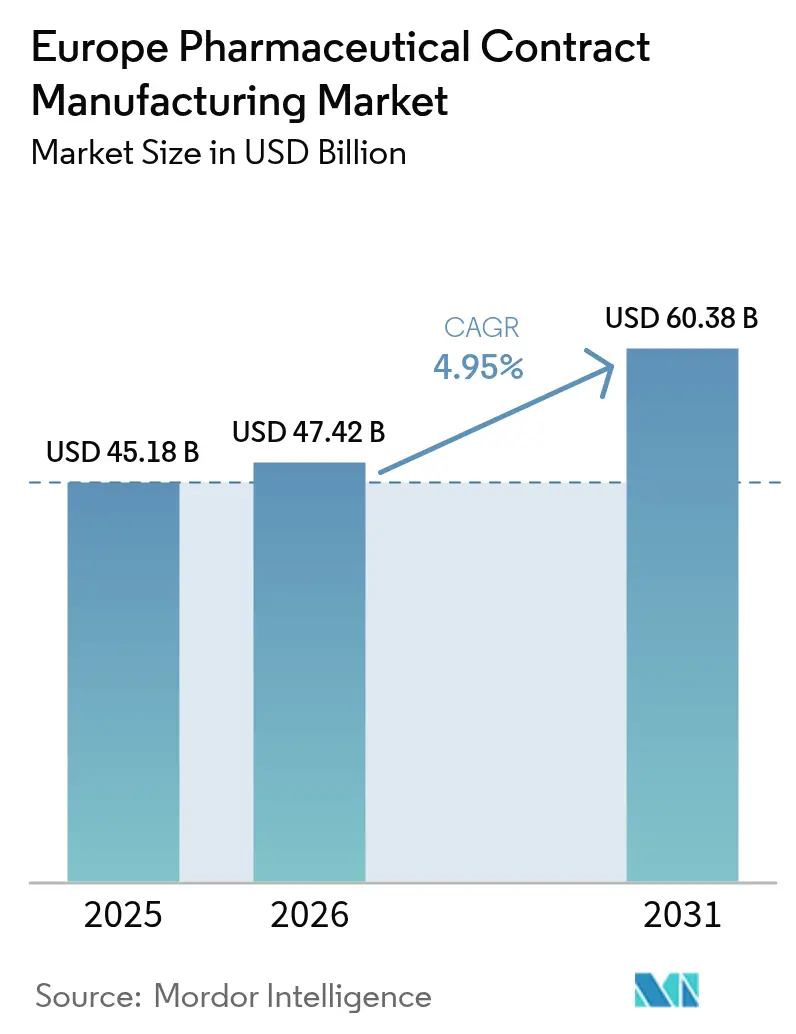

| Base Year Market Size (2025) | USD 45.18 Billion |

| Market Size (2026) | USD 47.42 Billion |

| Market Size (2031) | USD 60.38 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

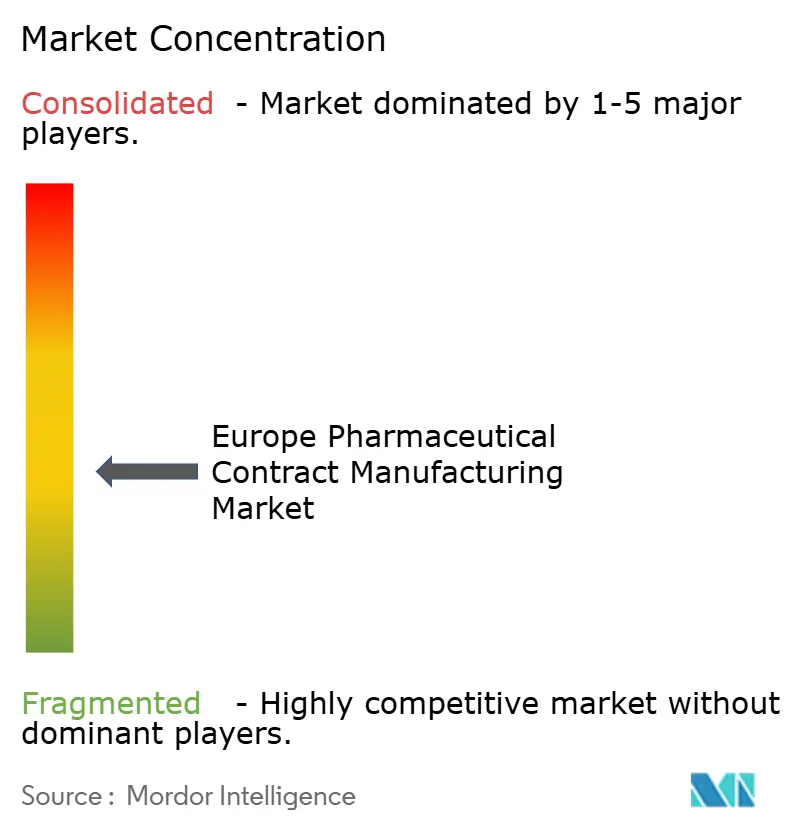

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Pharmaceutical Contract Manufacturing Market Analysis by Mordor Intelligence

The pharmaceutical contract manufacturing market size in Europe was valued at USD 45.18 billion in 2025 and estimated to grow from USD 47.42 billion in 2026 to reach USD 60.38 billion by 2031, at a CAGR of 4.95% during the forecast period (2026-2031). Steady outsourcing by large and mid-size drug makers, combined with regulatory initiatives such as the EU Health Technology Assessment Regulation, continues to elevate demand for specialized biologics and highly potent API capacity across the region. Active Pharmaceutical Ingredient (API) manufacturing remains the cornerstone revenue contributor, while finished dosage formulation (FDF) projects accelerate on the back of innovative delivery formats and serialization mandates. Germany retains its position as the primary production hub, yet Spain’s incentive-rich environment is catalyzing the fastest expansion in manufacturing footprints. Strategic acquisitions, typified by Lonza’s purchase of Roche’s Vacaville site and Catalent’s integration into Novo Holdings, have reinforced integrated service platforms that compress development timelines and broaden one-stop-shop capabilities.

Key Report Takeaways

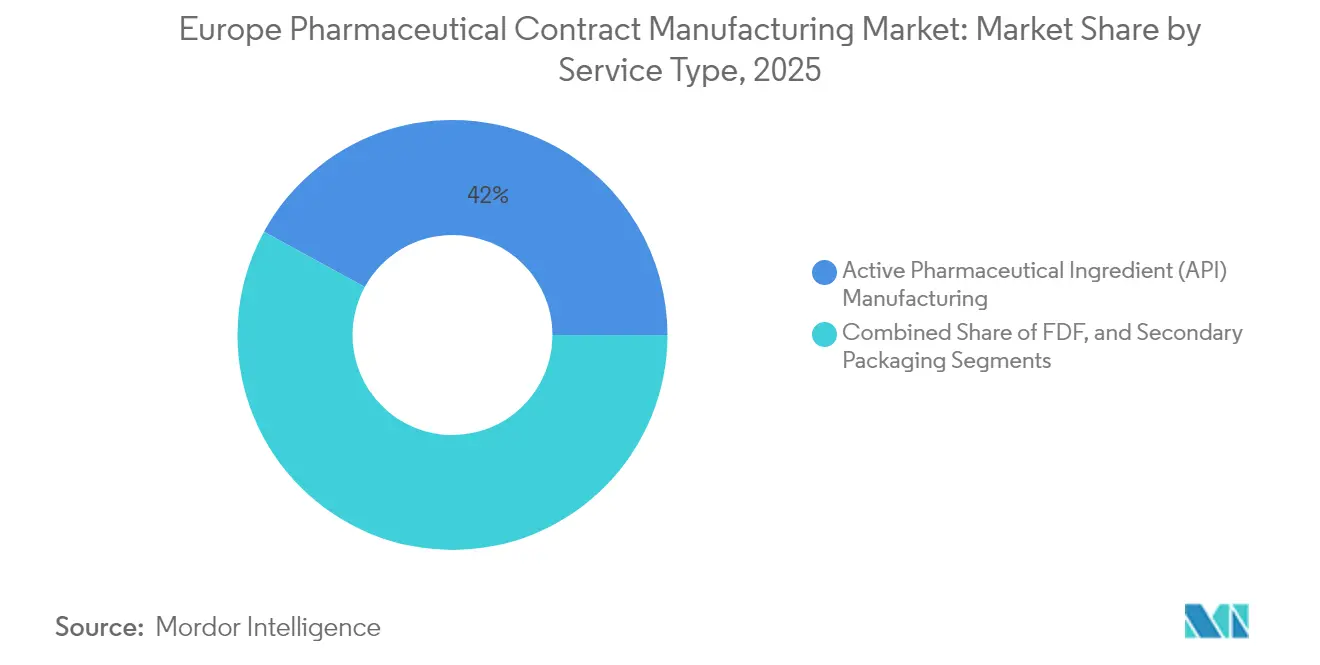

- By service type, API manufacturing led with 42.02% of the pharmaceutical contract manufacturing market share in 2025, whereas FDF services are growing at a 6.67% CAGR through 2031.

- By molecule type, small molecules accounted for 58.12% of the pharmaceutical contract manufacturing market size in 2025; highly potent APIs are projected to expand at a 7.02% CAGR to 2031.

- By therapeutic area, oncology held 28.31% revenue share in 2025, while respiratory applications registered the highest forecast CAGR at 5.91% through 2031.

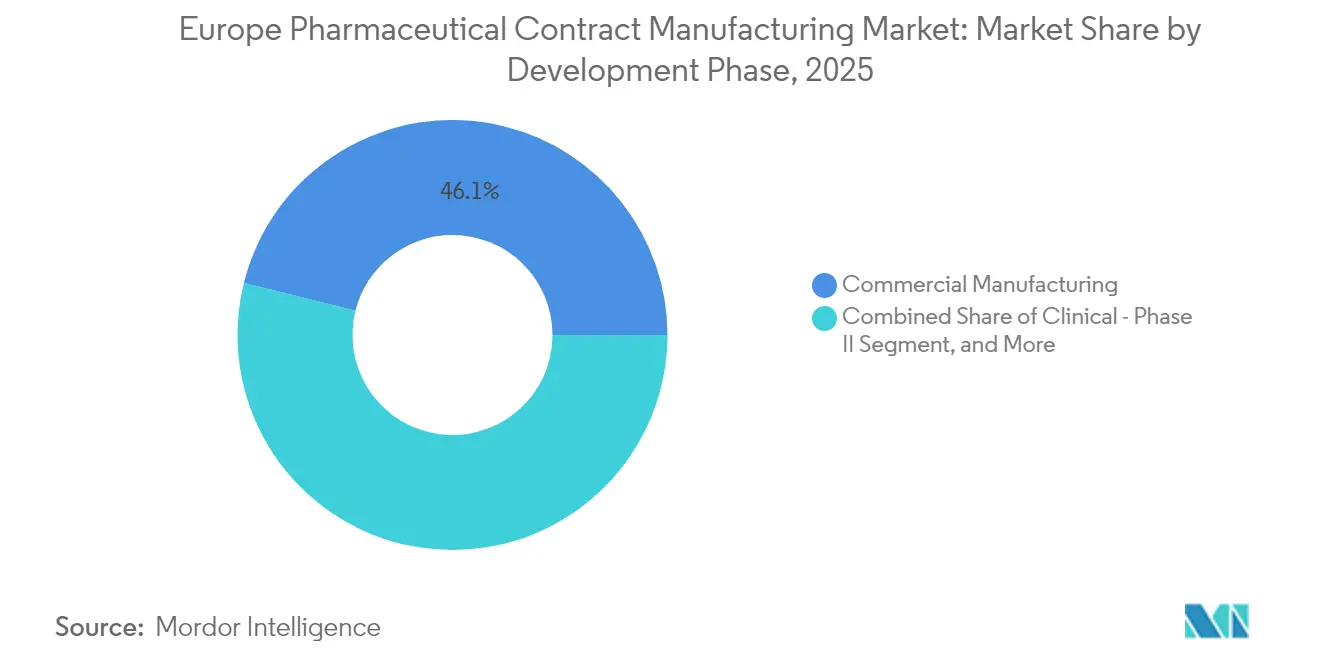

- By development phase, commercial manufacturing controlled 46.11% of the pharmaceutical contract manufacturing market share in 2025, yet Phase II clinical work is growing at a 7.1% CAGR to 2031.

- By end-client type, Big Pharma commanded 50.88% share in 2025, whereas small and mid-size pharma engagements are rising at a 6.88% CAGR through 2031.

- By geography, Germany captured 22.41% share of the pharmaceutical contract manufacturing market size in 2025; Spain is advancing at 6.92% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Pharmaceutical Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing outsourcing volume by EU pharma majors | +1.2% | Germany, France, UK core markets | Medium term (2-4 years) |

| Growing biologics and HPAPI pipeline complexity | +1.8% | Global, concentrated in Germany and Switzerland | Long term (≥ 4 years) |

| Contract-friendly EU tax incentives and grants | +0.9% | Spain, Italy, Eastern Europe focus | Short term (≤ 2 years) |

| CDMO M&A unlocking one-stop-shop capabilities | +1.1% | Pan-European with UK-Germany axis | Medium term (2-4 years) |

| On-demand manufacturing tech gaining traction | +0.7% | Germany, Netherlands, Denmark leaders | Long term (≥ 4 years) |

| Near-shoring driven by supply-chain security clauses | +0.6% | EU-wide, particularly Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Biologics and HPAPI Pipeline Complexity

Rising demand for monoclonal antibodies, bispecifics, and antibody-drug conjugates is pushing CDMOs to invest in large-scale single-use bioreactors, high-containment suites, and advanced purification trains that few facilities can match. [1]Samsung Biologics, “Samsung Biologics Reports First Quarter 2025 Financial Results,” samsungbiologics.com Samsung Biologics’ USD 1.4 billion multiyear contract with a European sponsor and the 180,000-liter expansion of Plant 5 exemplify the premium tied to specialized capacity. Digital twin systems are being deployed across European plants to enable predictive maintenance and real-time batch analytics, reducing failure rates and shortening tech-transfer cycles. These capital-heavy upgrades raise barriers to entry, concentrating pharmaceutical contract manufacturing market capacity among a handful of technologically advanced providers. As biologic payloads gain potency, compliance with updated EU GMP Annex 1 standards further differentiates operators equipped with isolators, restricted-access barrier systems, and robust contamination control strategies.

Increasing Outsourcing Volume by EU Pharma Majors

Regional drug makers continue divesting non-core sites while locking in long-term supply agreements with CDMOs that can ensure capacity, quality, and regulatory alignment. Sanofi’s facility transfer to Thermo Fisher illustrates a broader pivot that allows originators to redeploy capital toward R&D and commercialization. The Critical Medicines Act encourages multi-site European production to mitigate supply risks, prompting pharmaceutical companies to split portfolios across several contract partners. Outsourcing decisions now extend beyond cost, encompassing cyber-resilient data exchange, serialization compliance, and post-approval change management support. CDMOs that can bundle early-phase development, tech transfer, commercial supply, and regulatory liaison functions benefit from higher wallet share and deeper client lock-in.

Contract-friendly EU Tax Incentives and Grants

The EUR 1 billion IPCEI Med4Cure initiative and other country-level tax credits reduce payback periods on green-field biologics and sterile-fill investments. [2]European Commission, “Important Projects of Common European Interest,” commission.europa.eu Spain’s fiscal incentives are directly linked to its 7.01% CAGR leadership, enabling mid-tier CDMOs to upgrade containment lines for highly potent formulations. Clean Industrial Transition grants favor continuous-manufacturing installations that lower carbon footprints and energy intensity. Incentive structures also encourage collaborations between academia and CDMOs, accelerating technology adoption in niche modalities such as nucleic acid therapeutics and peptidomimetics.

CDMO M&A Unlocking One-Stop-Shop Capabilities

Ownership shifts have produced integrated networks capable of hosting discovery chemistry, IND-enabling toxicology, process development, and global commercial supply under unified quality systems. The consolidation wave compresses vendor lists for pharmaceutical sponsors seeking coordinated global launches, while also driving harmonization of digital quality-management platforms. Post-merger entities are investing in end-to-end data lakes that amalgamate batch, deviation, and release metrics, enabling AI-driven process control and predictive release testing. This scale and data integration underpin higher service premiums and foster entry barriers for stand-alone niche providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EU energy prices pressuring margins | -0.6% | Germany, Netherlands, Belgium most affected | Short term (≤ 2 years) |

| Capacity utilisation gaps in small-molecule plants | -0.4% | UK, Italy, France legacy facilities | Medium term (2-4 years) |

| Talent shortage in aseptic processing specialists | -0.5% | Germany, Switzerland, UK core markets | Long term (≥ 4 years) |

| Inflation-linked CDMO input contracts limiting price passthrough | -0.3% | Pan-European, particularly smaller CDMOs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising EU Energy Prices Pressuring Margins

Escalating power tariffs have added close to EUR 1 billion in incremental annual costs for European generics manufacturers alone. [3]European Central Bank, “Energy Shocks and Corporate Investment Decisions,” ecb.europa.eu Energy-intensive unit operations such as lyophilization and high-temperature HPAPI syntheses face acute margin compression, especially in Germany, where industrial electricity prices remain elevated. CDMOs respond by accelerating heat-recovery retrofits, procuring long-term renewable-energy PPAs, and piloting continuous processes that lower energy per kilogram output. Smaller providers lacking capital for energy-efficiency upgrades risk being priced out of competitive bids.

Capacity Utilization Gaps in Small-Molecule Plants

Legacy batch reactors built for blockbuster volumes are increasingly under-loaded as pipelines tilt toward niche oncology and orphan therapies. The capital required to retrofit continuous-flow or high-potency suites often exceeds available cash flows for facilities in Italy, France, and the UK. As utilization dips below the 60% break-even mark, owners resort to either niche-service pivots (e.g., controlled-substance APIs) or consolidation. CDMOs with modern multipurpose assets pick up incremental demand, reinforcing the shift in pharmaceutical contract manufacturing market revenue toward agile, high-containment providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: API Manufacturing Leads Despite FDF Growth

API manufacturing contributed 42.02% of 2025 revenue, underlining its anchor role in the pharmaceutical contract manufacturing market size. Projects involve complex multi-step chemistries, biocatalysis, and high-containment work that sustain premium pricing. Recent demand spikes in antiviral and oncology payloads have pushed European CDMOs to debottleneck kilolab through commercial kilo-scale assets while integrating real-time release testing to curtail cycle times.

FDF work, though currently smaller, is projected to outpace overall market growth at 6.67% CAGR on the back of patient-friendly oral thin films, autoinjectors, and inhaled formulations. Serialization rules under the Falsified Medicines Directive drive added packaging revenues, while Annex 1’s sterile-drug revisions prompt investments in isolator-based filling lines. The interplay between bulk-drug and dosage manufacturing strengthens bundled contracting, further consolidating pharmaceutical contract manufacturing market opportunities within multi-service providers.

By Molecule Type: Small Molecules Dominate While HPAPI Commands Premium

The pharmaceutical contract manufacturing market share for small molecules stood at 58.12% in 2025, reflecting Europe’s entrenched synthetic-chemistry heritage and extensive reactor infrastructure. Continuous-flow retrofits have trimmed solvent consumption and cycle times, helping older assets remain competitive amid escalating energy costs.

Highly-potent API programs grow at 7.02% CAGR as oncology and targeted therapies proliferate. Investments in negative-pressure suites, glove-box isolators, and advanced dust-collection systems are mandatory to meet Occupational Exposure Limit thresholds below 10 µg/m³. Large-molecule biologics projects command longer timelines but deliver durable revenue streams due to multi-year tech-transfer complexity and higher regulatory scrutiny, reinforcing the blended portfolio approach of leading CDMOs.

By Therapeutic Area: Oncology Leadership Faces Respiratory Challenge

Oncology retained 28.31% share of 2025 demand, driven by continuous innovation in cytotoxics, antibody-drug conjugates, and checkpoint inhibitors. Specialized containment, high-pressure chromatography, and toxin-linker chemistries define the capability moat in this segment.

Respiratory therapeutics, expected to grow at 5.91% CAGR, benefit from pandemic-accelerated investments in inhalable biologics and next-generation dry-powder devices. CDMOs with integrated device-drug assembly lines can command higher margins, expanding the pharmaceutical contract manufacturing market footprint into combination-product territory.

By Development Phase: Commercial Manufacturing Dominance Challenged by Clinical Growth

Commercial supply still accounts for 46.11% of the pharmaceutical contract manufacturing market size, reflecting mature brands and biosimilar volumes. Multi-year supply contracts stabilize cash flows, allowing CDMOs to finance capacity upgrades for emerging modalities.

Phase II programs, growing at 7.1% CAGR, signal a vibrant biotech funding environment and faster regulatory feedback loops. Flexible single-use bioreactors and modular cleanrooms enable CDMOs to switch between pilot and low-volume commercial batches, reducing scale-up risk and aligning capacity with demand uncertainty.

By End-Client Type: Big Pharma Stability Meets Mid-Size Innovation

Big Pharma held 50.88% of 2025 revenue by leveraging preferred-provider arrangements that secure slot reservations across multiple sites. These clients push for integrated digital quality systems and global change-control harmonization.

Small and mid-size pharma companies, growing at a 6.88% CAGR, increasingly outsource complex chemistry and biologics as they focus on asset-light discovery models. CDMOs offering development-through-commercial continuity gain share, reinforcing a virtuous cycle of capacity expansion and deeper expertise within the pharmaceutical contract manufacturing market.

Geography Analysis

Germany generated 22.41% of 2025 revenue, anchored by deep chemical engineering talent, stringent regulatory oversight, and proximity to industry headquarters. However, elevated energy costs are forcing operators to accelerate efficiency retrofits, negotiate renewable-energy PPAs, and pilot continuous manufacturing to safeguard gross margins.

Spain, clocking a 6.92% CAGR, leverages aggressive tax breaks, streamlined construction permits, and access to Spanish-speaking workforce pools for expansion into Latin American supply chains. CDMOs cluster around Catalonia and Madrid, focusing on biologics fill-finish and inhalation products, thereby broadening the pharmaceutical contract manufacturing market reach into emerging segments.

The UK, France, Italy, and Eastern Europe collectively account for the remaining share. Post-Brexit UK maintains MHRA alignment with EU GMP, enabling seamless batch release into the single market via mutual recognition pathways. France benefits from over EUR 1.87 billion in 2024-2025 investments by major innovators to expand monoclonal antibody output. Italy exploits mature generics expertise and competitive labor costs, while Poland, Hungary, and Czechia attract brown-field conversions of legacy plants into high-containment suites supported by EU structural funds.

Competitive Landscape

European CDMOs exhibit moderate consolidation, with the top five providers controlling just over 50% of total revenues. Lonza’s USD 1.2 billion Vacaville site purchase expands large-scale mammalian capacity, while Catalent’s integration into Novo Holdings accelerates capital deployment into continuous-manufacturing lines and advanced delivery technologies.

Technology remains the core differentiator. Operators are adopting MES-integrated continuous chromatography, PAT-enabled in-line release, and cloud-based deviation analytics to shorten cycle times and slash rework. Digital twins underpin predictive maintenance that boosts asset uptime by 8-12%, directly improving capacity availability within the pharmaceutical contract manufacturing market.

White-space opportunities persist in cell and gene therapy viral-vector manufacturing, high-potency oral solids, and sterile-lyophilized biologics. Smaller, agile entrants focus on modular clean-room pods and micro-batch continuous reactors, positioning themselves as overflow partners for large CDMOs. The ability to manage dual-sourcing mandates and navigate diverse EU subsidy regimes remains pivotal for sustained growth.

Europe Pharmaceutical Contract Manufacturing Industry Leaders

Fareva Holding SA

Recipharm AB

Boehringer Ingelheim Group

Aenova Group

Famar SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Thermo Fisher Scientific and Sanofi expanded their strategic partnership through Thermo Fisher’s acquisition of Sanofi’s sterile manufacturing site in Ridgefield, New Jersey.

- April 2025: Samsung Biologics launched Plant 5 operations, adding 180,000 L of bioreactor capacity and announcing a USD 1.4 billion contract with a European drug maker.

- April 2025: Thermo Fisher Scientific unveiled a USD 2 billion U.S. manufacturing investment plan to reinforce healthcare supply chains.

- March 2025: Thermo Fisher Scientific agreed to buy Solventum’s Purification & Filtration business for USD 4.1 billion.

Europe Pharmaceutical Contract Manufacturing Market Report Scope

Pharmaceutical contract manufacturing involves outsourcing the production of pharmaceutical products to specialized third-party manufacturers and handles various stages of drug production, including APIs, synthesis, formulation development, and finished dosage form manufacturing.

The European pharmaceutical contract manufacturing market is segmented by service type (active pharmaceutical ingredient (API) manufacturing, finished dosage formulation (FDF) development and manufacturing (solid dose formulation, liquid dose formulation, and injectable dose formulation), and secondary packaging), and by country (United Kingdom, Germany, France, Italy, and Rest of Europe).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Active Pharmaceutical Ingredient (API) Manufacturing | |

| Finished Dosage Formulation (FDF) Development and Manufacturing | Solid Dose Formulation |

| Liquid Dose Formulation | |

| Injectable Dose Formulation | |

| Secondary Packaging |

By Molecule Type

| Small Molecule |

| Large Molecule / Biologics |

| Highly-Potent APIs (HPAPI) |

| Advanced Therapies (Cell and Gene) |

By Therapeutic Area

| Oncology |

| Cardiovascular |

| CNS Disorders |

| Infectious Diseases |

| Respiratory |

| Other Therapeutic Area |

By Development Phase

| Pre-clinical |

| Clinical - Phase I |

| Clinical - Phase II |

| Clinical - Phase III |

| Commercial Manufacturing |

By End-Client Type

| Big Pharma |

| Small and Mid-size Pharma |

| Virtual / Biotech Start-ups |

| Generics Manufacturers |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Service Type | Active Pharmaceutical Ingredient (API) Manufacturing | |

| Finished Dosage Formulation (FDF) Development and Manufacturing | Solid Dose Formulation | |

| Liquid Dose Formulation | ||

| Injectable Dose Formulation | ||

| Secondary Packaging | ||

| By Molecule Type | Small Molecule | |

| Large Molecule / Biologics | ||

| Highly-Potent APIs (HPAPI) | ||

| Advanced Therapies (Cell and Gene) | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular | ||

| CNS Disorders | ||

| Infectious Diseases | ||

| Respiratory | ||

| Other Therapeutic Area | ||

| By Development Phase | Pre-clinical | |

| Clinical - Phase I | ||

| Clinical - Phase II | ||

| Clinical - Phase III | ||

| Commercial Manufacturing | ||

| By End-Client Type | Big Pharma | |

| Small and Mid-size Pharma | ||

| Virtual / Biotech Start-ups | ||

| Generics Manufacturers | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the European pharmaceutical contract manufacturing market?

The market is valued at USD 47.42 billion in 2026 and is expected to reach USD 60.38 billion by 2031.

Which service segment generates the largest revenue?

API manufacturing holds the highest share at 42.02% of 2025 revenue.

Which European country is expanding contract manufacturing capacity the fastest?

Spain is registering the highest growth, forecast at a 6.92% CAGR between 2026-2031.

Which therapeutic area drives the greatest manufacturing demand?

Oncology leads, accounting for 28.31% of 2025 contract manufacturing demand.

Why are biologics significant for European CDMOs?

Complex biologics such as monoclonal antibodies demand specialized containment and single-use capacity, enabling CDMOs to capture premium pricing.

How is consolidation reshaping the competitive landscape?

High-profile acquisitions like Lonza-Roche and Novo Holdings-Catalent have created integrated service platforms that compress development timelines and deepen client relationships.

Page last updated on: