Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

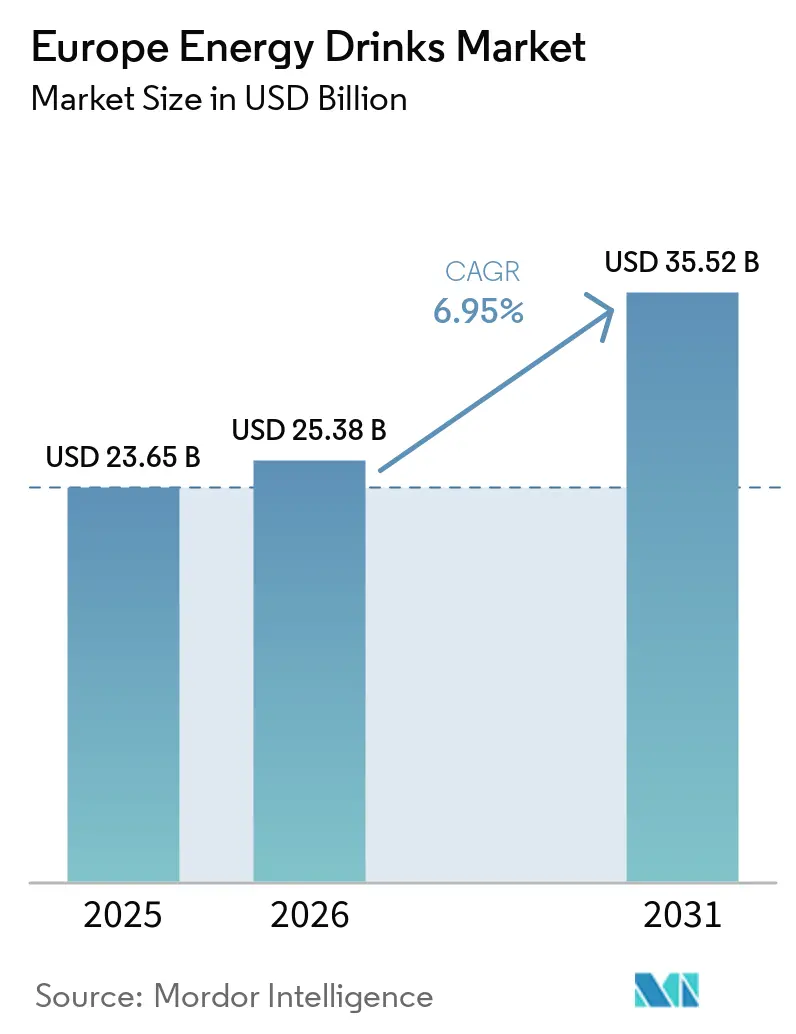

| Base Year Market Size (2025) | USD 23.65 Billion |

| Market Size (2026) | USD 25.38 Billion |

| Market Size (2031) | USD 35.52 Billion |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

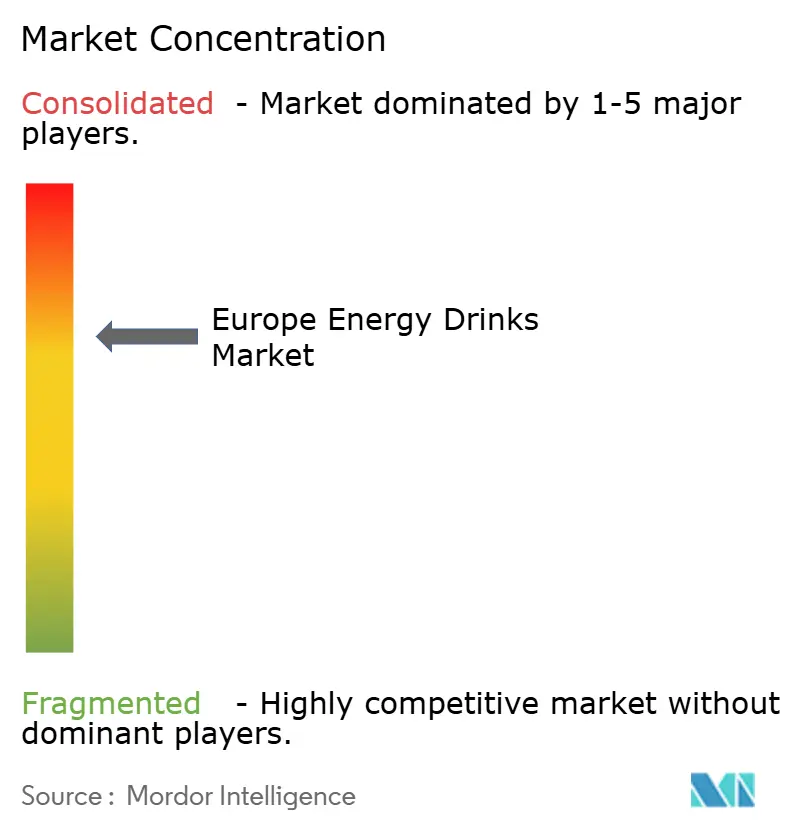

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Energy Drinks Market Analysis by Mordor Intelligence

The Europe energy drinks market size is projected to be USD 23.65 billion in 2025, USD 25.38 billion in 2026, and reach USD 35.52 billion by 2031, growing at a CAGR of 6.95% from 2026 to 2031. Once primarily favored for late-night boosts, energy drinks are now being embraced for daytime productivity, fitness recovery, and overall wellness, broadening their appeal beyond just students. The market's growth is also supported by evolving consumer preferences for functional beverages that cater to active lifestyles and health-conscious choices. In response to EU sugar taxes and caffeine labeling mandates, there's a pronounced shift towards sugar-free formulations, prompting leading brands to accelerate product reformulations. Premium plant-based caffeine sources like yerba mate and guayusa not only command price premiums but also resonate with sustainability objectives, aligning with the European Commission's Farm to Fork Strategy. Additionally, the increasing focus on eco-friendly packaging solutions is driving innovation in the market. Meanwhile, a shortage of aluminum cans has tightened supply chains and inflated packaging costs, nudging some brands to pivot to glass formats, despite the added burden of higher freight expenses.

Key Report Takeaways

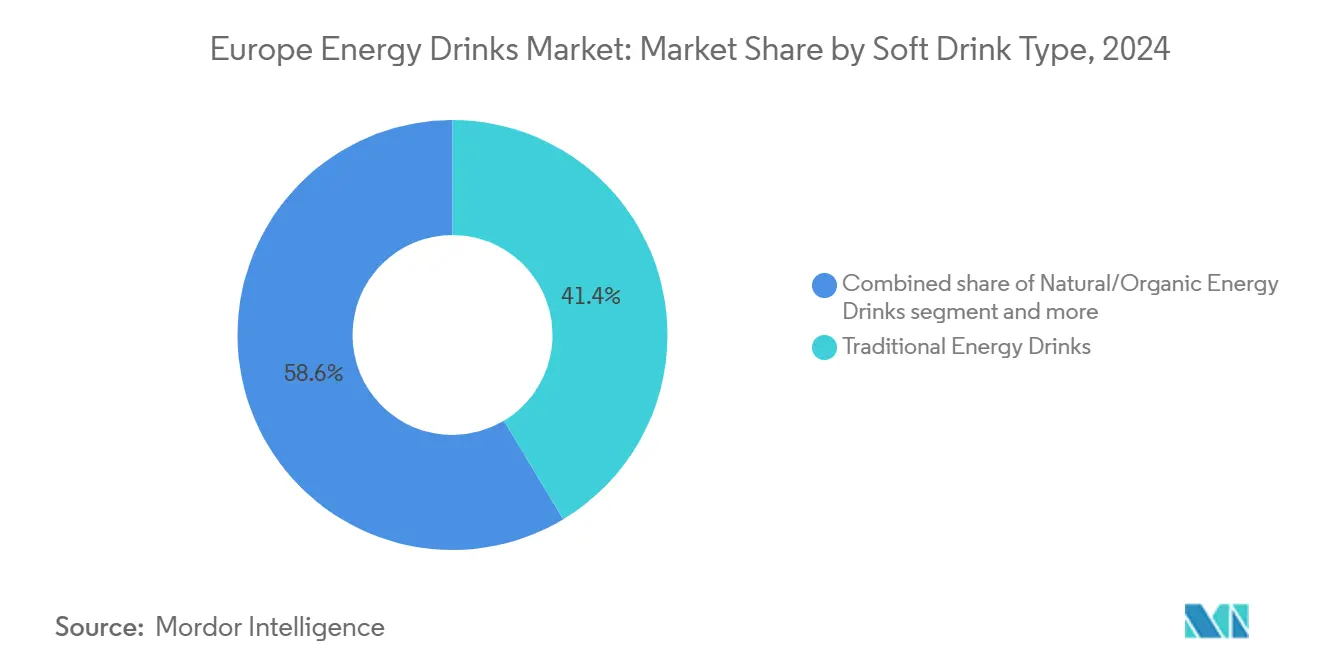

- By type, traditional energy drinks led the European energy drinks market with 41.38% share in 2025, while natural and organic variants are expanding at an 8.69% CAGR through 2031.

- By packaging type, metal cans commanded 53.64% share of the European energy drinks market size in 2025, yet glass bottles are set to grow at an 8.15% CAGR to 2031.

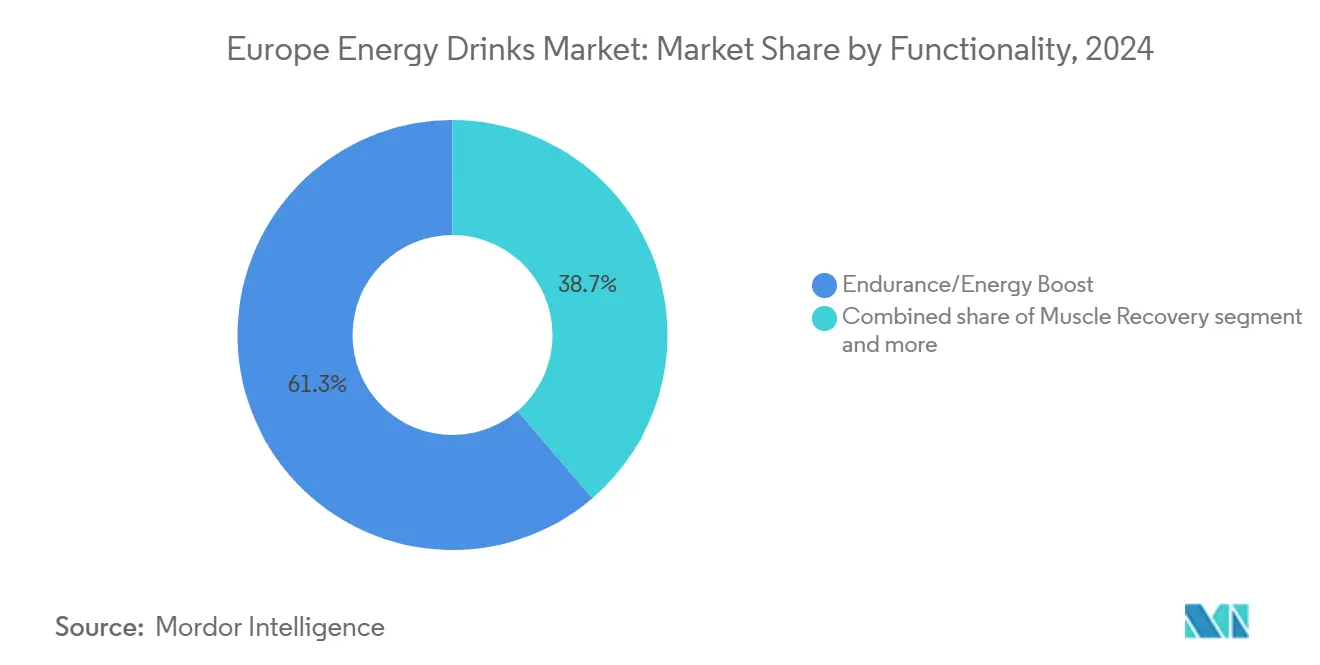

- By functionality, endurance and energy-boost products accounted for 61.28% share of the European energy drinks market size in 2025, while muscle-recovery beverages are advancing at an 8.24% CAGR through 2031.

- By distribution, retail channels held 80.25% of Europe energy drinks market share in 2025, whereas HoReCa is projected to post a 7.28% CAGR to 2031.

- By geography, Germany captured 16.85% revenue share in 2025; Poland is forecast to record the fastest 7.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Energy Drinks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Sugar Tax-Prompted Shift to Sugar-Free Energy Drinks | +1.2% | Western Europe (UK, France, Belgium), with spillover to Nordics | Medium term (2-4 years) |

| Gen Z and E-Sports Fueled Consumption Surge | +1.5% | Global, with concentration in Germany, UK, Poland, Netherlands | Short term (≤ 2 years) |

| Rise in Convenience and E-Commerce Channels | +0.9% | Pan-European, with accelerated adoption in Spain, Italy, France | Medium term (2-4 years) |

| Boom in Premium Plant-Based Caffeine Options Like Yerba Mate and Guayusa | +0.8% | Nordics (Sweden, Denmark), Germany, Netherlands, urban centers across Western Europe | Long term (≥ 4 years) |

| Launch of Nootropic-Enhanced Energy-Plus Beverages | +0.7% | Germany, UK, Netherlands, with early traction in urban millennial and Gen Z cohorts | Medium term (2-4 years) |

| Cost Advantages in Central-Eastern Europe Manufacturing | +0.6% | Poland, Hungary, Czech Republic, with export flows to Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Sugar Tax-Prompted Shift to Sugar-Free Energy Drinks

Fiscal measures targeting sugar-sweetened beverages have driven swift reformulation cycles across Europe. By 2025, twelve European Union member states had implemented sugar taxes. The World Health Organization reported that all European countries enforcing soft-drink excise duties also include energy drinks in their scope[1]Source: World Health Organization, “Soft-Drink Fiscal Measures in Europe,” who.int. The UK's Soft Drinks Industry Levy, introduced in 2018 and expanded in 2024, led Red Bull to release a zero-sugar variant, which now accounts for over 40% of its UK sales. France's tiered tax system, which imposes penalties on beverages containing more than 5 grams of sugar per 100 milliliters, prompted Monster Beverage Corporation to reformulate its core product line with sucralose and acesulfame potassium by mid-2024. In the same year, Belgium and the Netherlands adopted similar frameworks, creating a complex regulatory environment. This situation primarily benefits multinational brands with the R&D resources to develop region-specific products. Meanwhile, smaller regional players, unable to reformulate, face margin pressures or market exits, consolidating market share among the top five brands.

Gen Z and E-Sports Fueled Consumption Surge

Demographic shifts are redefining consumption patterns, placing flavor innovations in the spotlight. Red Bull, with a global presence, supports over 800 athletes and 250 e-sports teams, with a strong focus on Europe's League of Legends and Counter-Strike tournaments. Similarly, Monster Energy secures title sponsorships across various esports franchises. These partnerships are transforming passive viewers into active consumers: 2024 Nielsen data shows that 18-24-year-olds in Germany and Poland consume energy drinks an average of 3.2 times per week, double the frequency of the 35-44 age group. Gen Z increasingly prefers energy drinks offering functional benefits beyond caffeine, such as B-vitamins, taurine, and cognitive enhancers. This trend drove the Q1 2024 launch of Monster Energy's Green Zero Sugar in 16 European markets, featuring 160 mg of caffeine along with L-carnitine and ginseng. Reflecting the changing marketing dynamics, e-sports arenas in the Netherlands and Sweden now host branded lounges where fans can try exclusive flavors, creating a direct marketing loop that bypasses traditional retail channels.

Rise in Convenience and E-Commerce Channels

Omnichannel distribution is eroding the dominance of hypermarkets and supermarkets. Retail channels held 80.25% of market share in 2025, yet convenience stores and online platforms are expanding at 7.28% through 2031, driven by impulse purchases and subscription models. Amazon's Subscribe and Save program in Germany and the UK offers 15% discounts on recurring energy-drink orders, locking in habitual consumers and generating predictable revenue streams for brands. Spain and Italy, historically reliant on hypermarket promotions, witnessed a 22% year-over-year increase in e-commerce energy-drink sales during 2024 as delivery apps like Glovo and Deliveroo integrated beverage SKUs into 30-minute fulfillment windows. Convenience stores in Poland and Belgium expanded cooler space for energy drinks by an average of 18% in 2024, prioritizing single-serve cans over multipacks to capture on-the-go consumption. This shift pressures brands to invest in direct-store-delivery networks and digital marketing, raising customer-acquisition costs but improving velocity.

Boom in Premium Plant-Based Caffeine Options Like Yerba Mate and Guayusa

Natural caffeine sources are establishing a premium niche in the market. Guayusa, an Amazonian holly leaf boasting 90 mg of caffeine per 8-ounce serving and rich in polyphenols, made its mark in 12 new product launches across Europe in 2024, with a notable concentration in Sweden, Germany, and the Netherlands. Traditionally enjoyed in South America, yerba mate has found a foothold in Europe, championed by brands like Mateina and Club-Mate, marketing it as a smoother alternative to synthetic caffeine. These premium formulations, priced 25-35% higher than conventional energy drinks, resonate with health-conscious millennials who prioritize clean labels. The European Commission's Farm to Fork Strategy, which promotes organic and sustainably sourced ingredients, bolsters the regulatory landscape for plant-based caffeine. Yet, challenges loom: guayusa's cultivation is predominantly in Ecuador, and yerba mate, harvested in Argentina and Brazil, grapples with climate-induced volatility, hindering immediate volume expansion.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter EU Caps on Caffeine, Taurine, and Youth Advertising | -0.8% | Pan-European, with strictest enforcement in UK, Nordics, Baltics | Short term (≤ 2 years) |

| Rising Cardiovascular and Sugar-Linked Health Risks | -0.6% | Western Europe (Germany, UK, France), with spillover to Southern Europe | Medium term (2-4 years) |

| Aluminum Can Shortages Driving Up Packaging Expenses | -0.5% | Global, with acute impact in Germany, UK, France, Italy | Short term (≤ 2 years) |

| Cannibalization from RTD Cold-Brew Coffee | -0.4% | Urban centers in Germany, UK, Netherlands, Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tighter EU Caps on Caffeine, Taurine, and Youth Advertising

Regulatory frameworks are tightening the permissible formulation envelope. The European Food Safety Authority sets a 200 mg single-dose caffeine cap and a 400 mg daily limit for adults, while children are restricted to 3 mg per kilogram of body weight[2]Source: European Food Safety Authority, “Caffeine Limits in Beverages,” efsa.europa.eu. EU Regulation 1169/2011 mandates warning labels on beverages surpassing 150 mg of caffeine per liter. Additionally, Lithuania, Latvia, Poland, Romania, Hungary, and Bulgaria have outright bans on sales to minors. In 2025, the UK government proposed extending these age restrictions to those under 16, a move set to heavily impact the UK energy drinks market. Meanwhile, Sweden is mulling over point-of-sale ID checks for energy drinks. Such regulations are reshaping marketing strategies: Red Bull found itself under an EU antitrust probe in November 2025, accused of using exclusivity clauses to limit retailers from stocking rival brands. With advertising bans on youth-targeted campaigns, brands are shifting focus to adults, but this pivot diminishes their reach among the 18-24 age group, which constitutes 35% of the category's volume. Moreover, compliance costs for labeling adjustments and age-verification systems inflate operating expenses by 2-3%, a significant strain for smaller entities.

Rising Cardiovascular and Sugar-Linked Health Risks

Public-health researchers are increasing their focus on energy drinks, particularly those with high caffeine and sugar content. The European Food Safety Authority (EFSA) has identified excessive energy drink consumption as a factor in cases of arrhythmia and hypertension, particularly among individuals with existing cardiovascular conditions. A 2024 study published in the European Heart Journal reported that individuals aged 18-35 who consumed more than two energy drinks daily experienced an average rise of 4.5 mmHg in systolic blood pressure and an increase of 7 beats per minute in heart rate. The World Health Organization's 2025 report on non-communicable diseases highlighted energy drinks as a contributor to increasing obesity rates in Eastern Europe, where sugar-sweetened variants remain widespread. These findings have strengthened advocacy groups' efforts to push for stricter regulations, with several European parliaments considering outright bans on energy drink sales to minors. While brands are shifting toward sugar-free reformulations, consumer perceptions remain slow to evolve. A 2024 survey in Germany found that 42% of respondents still associate energy drinks with health risks, regardless of their sugar content.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sugar-Free Variants Reshape Portfolio Mix

In 2025, traditional energy drinks, led by Red Bull's original formulation and Monster Energy's core line, held a 41.38% market share. However, natural and organic energy drinks are projected to grow at 8.69% through 2031, driven by a consumer shift toward clean-label ingredients. Within the traditional category, sugar-free and low-calorie variants are the fastest-growing sub-segment, supported by EU sugar taxes and reformulation mandates. Brands like Rockstar and Burn Energy launched zero-sugar SKUs in 2024 to meet this demand. Energy shots, popularized by 5-hour Energy in North America, remain niche in Europe, capturing less than 5% of the volume due to caffeine restrictions and limited retail presence. Other energy drinks, such as functional waters and lightly carbonated blends, attract health-conscious consumers but face challenges scaling due to limited brand equity and marketing resources.

Natural and organic energy drinks, using plant-based caffeine from guayusa, yerba mate, and green tea, command a 25-35% price premium over traditional options. Targeting millennials in Germany, Sweden, and the Netherlands, these products align with the European Commission's Farm to Fork Strategy promoting organic sourcing but face supply-chain constraints limiting growth. Monster Beverage Corporation's Green Zero Sugar, launched in 16 European markets in Q1 2024, bridges traditional and natural segments by combining synthetic caffeine with botanical extracts, appealing to consumers seeking taste and clean labels. Navigating EFSA's caffeine limits and Regulation 1169/2011's labeling requirements adds complexity but offers differentiation in a competitive market.

By Packaging Type: Sustainability Mandates Accelerate Glass Adoption

In 2025, metal cans accounted for 53.64% of the packaging market, valued for their recyclability, portability, and carbonation retention. Glass bottles are expected to grow at 8.15% through 2031, driven by premiumization and sustainability trends. PET bottles, with a 20% volume share, cater to multipacks and value-tier products but face criticism over single-use plastics. This has led brands to adopt recycled PET (rPET) with 50-100% post-consumer content. Aseptic packages, such as Tetra Pak cartons and pouches, face consumer concerns about product quality but offer cost advantages for private-label brands in discount channels. Disposable cups, mainly used in HoReCa settings, represent less than 3% of the volume and are under pressure from the EU's Single-Use Plastics Directive.

In 2024, aluminum can shortages extended lead times to 16-20 weeks and increased packaging costs by 15-20%, prompting brands to shift to glass despite higher costs. Hell Energy and Vitamin Well introduced 250 ml glass bottles in Sweden and Germany in 2024, positioning them as premium alternatives for on-premise consumption in bars and restaurants. Glass's recyclability and inert properties appeal to eco-conscious consumers, but its weight raises freight costs by 30-40%, limiting distribution to regional markets. Ball Corporation and other manufacturers are investing over EUR 1 billion in new European facilities by 2026, but capacity growth lags demand, keeping prices high and driving packaging innovation. Brands with long-term can-supply agreements gain an edge, while smaller players risk stock-outs during peak demand.

By Functionality: Muscle Recovery Gains Traction Among Fitness Enthusiasts

In 2025, energy and endurance formulations dominated with a 61.28% market share, driven by caffeine, taurine, and B-vitamins for quick energy boosts suited to work, study, and nightlife. Muscle-recovery drinks, featuring BCAAs, creatine, and electrolytes, are growing at 8.24% through 2031, merging with sports nutrition and appealing to gym-goers for post-workout recovery. Cognitive enhancement and immune support claims are emerging, supported by nootropic ingredients like L-theanine and lion's mane mushroom. Celsius Holdings markets its European line as thermogenic and cognitive-enhancing, combining guarana-derived caffeine with green tea extract, while Ghost Energy uses cognizin citicoline for mental clarity.

The European Food Safety Authority has not approved health claims linking nootropics or muscle-recovery ingredients to specific benefits, limiting on-pack messaging and pushing brands to rely on influencer marketing and clinical-trial references online. In 2024, Monster Beverage Corporation launched Reign Total Body Fuel in the UK, targeting fitness enthusiasts with 300 mg caffeine, BCAAs, and CoQ10, but faced regulatory scrutiny for exceeding EFSA's 200 mg caffeine guideline per dose. Germany and the UK lead in muscle-recovery beverage adoption, with these products accounting for 8% of total energy-drink volume in 2024, up from 4% in 2023. Brands that navigate regulations and establish clinical credibility are set to capture share from traditional sports drinks, which lack the caffeine consumers now associate with energy.

By Distribution Channel: HoReCa Rebounds as Nightlife Recovers

In 2025, retail channels held 80.25% of the distribution share, led by supermarkets and hypermarkets, followed by convenience stores and online platforms. The HoReCa sector, including bars, restaurants, and nightclubs, is set to grow at 7.28% through 2031, recovering from pandemic closures and driven by on-premise consumption at e-sports arenas and music festivals. Convenience and grocery stores in Poland and Belgium grew 18% year-over-year in 2024, fueled by single-serve can sales and expanded cooler space, leveraging impulse purchases and extended hours. Online retail platforms, such as Amazon and direct-to-consumer channels, increased their retail volume share from 8% in 2023 to 12% in 2025, supported by subscription models and 30-minute delivery apps integrating beverage SKUs.

Supermarkets and hypermarkets, traditionally strong due to promotional pricing and multipacks, face challenges from e-commerce and convenience channels offering faster turnover and lower inventory costs. Red Bull and Monster Beverage Corporation invest heavily in direct-store-delivery networks for cooler placement and visibility, while smaller brands, reliant on third-party distributors, struggle with limited retail influence. HoReCa's recovery remains uneven: nightlife venues in Spain and Italy returned to pre-pandemic levels by mid-2024, but Germany and France lag due to cautious consumers and reduced disposable income among younger demographics. In the Netherlands and Sweden, e-sports arenas feature branded lounges where fans sample exclusive flavors, creating direct marketing ecosystems that bypass traditional retail and boost margins.

Geography Analysis

In 2025, Germany accounted for 16.85% of regional revenue, driven by Red Bull's home advantage, extensive convenience-store presence, and a consumer preference for energy drinks as productivity boosters. Strict advertising regulations limiting youth-targeted campaigns have led brands to focus on adult demographics through sponsorships of professional and e-sports teams. In 2024, Monster Beverage Corporation expanded into 5,000 additional German retail outlets, targeting fitness enthusiasts with its Reign Total Body Fuel and Ultra variants, emphasizing zero sugar and functional benefits. Poland is projected to grow at 7.85% through 2031, supported by low labor costs attracting contract manufacturing, a youthful population with rising disposable income, and Hell Energy's strong regional presence via its Hungarian production facility. The United Kingdom, France, and Spain collectively contribute over 30% of market value but face challenges from sugar taxes and proposed age restrictions limiting youth access.

Russia, once a key market, experienced volatility due to geopolitical tensions and supply chain disruptions. However, domestic brands like Adrenaline Rush retained market share through localized production and competitive pricing against Western imports. Despite a combined population under 30 million, the Netherlands and Belgium excel in energy drink consumption, driven by health-conscious consumers adopting natural and organic variants and paying premiums for clean labels. Sweden, home to Nocco and Vitamin Well, serves as a testing ground for premium formulations that later expand to Germany and the UK, leveraging Scandinavian consumers' preference for functional ingredients and sustainability. Italy and the Rest of Europe, including Portugal, Greece, and Eastern European markets (excluding Poland and Russia), remain underpenetrated, with energy drinks comprising less than 5% of total beverage volume. However, urbanization and growing e-commerce infrastructure present long-term growth potential in these regions.

Central-Eastern Europe is reshaping supply chains with its manufacturing advantages. In 2024, Poland and Hungary attracted over USD 150 million in beverage-production investments, including expansions by Mutalo Group and contract packers for private-label brands. Labor costs in these regions are 40% lower than in Western Europe, while electricity prices for aluminum can production are EUR 0.08 per kilowatt-hour compared to EUR 0.14 in Germany, reducing packaging costs by 12-15%. These savings allow regional players to price products 10-20% lower than multinationals while maintaining margins. However, logistics costs to Western markets and quality perception gaps limit premium-tier penetration. European Commission's cohesion funds supporting infrastructure in Central-Eastern Europe further enhance manufacturing investments, ensuring a structural cost advantage through the forecast period[3]Source: European Commission, “Farm to Fork Strategy,” ec.europa.eu.

Competitive Landscape

The European energy drinks market showcases moderate consolidation. Red Bull GmbH and Monster Beverage Corporation together account for over 50% of the market volume. However, they are feeling the heat from regional players like Hell Energy, Vitamin Well, and Nocco. These challengers are carving out their niche by offering localized flavors, competitive pricing, and direct-to-consumer sales. In a move highlighting the scrutiny on market leaders, the European Union launched an antitrust investigation into Red Bull in November 2025, focusing on the company's exclusivity agreements with retailers. This increased oversight could pave the way for smaller brands to gain shelf space. Reflecting a trend of consolidation, PepsiCo shelled out USD 3.85 billion for Rockstar in January 2025, while Keurig Dr. Pepper's acquisition of Ghost, ranging between USD 990 million and USD 1.65 billion in October 2024, underscores the push by multinationals to scale up amidst rising input costs and regulatory challenges.

Targeting the female demographic, Celsius Holdings acquired Alani Nu for USD 1.8 billion in February 2025, emphasizing clean-label products. Meanwhile, Carlsberg's GBP 3.3 billion (around USD 4.2 billion) purchase of Britvic in July 2024 marks its foray into the lucrative world of functional beverages, expanding its portfolio beyond traditional beer offerings, as reported by the Wall Street Journal. New players like Congo Brands, the force behind Prime Energy and Alani Nu, are shaking up the scene. They've harnessed the power of influencer collaborations and exclusive drops to create a buzz on social media, steering clear of conventional advertising.

Ghost Energy, making its UK debut in September 2025, is riding on Keurig Dr. Pepper's distribution clout. They're zeroing in on the gaming and fitness sectors, boasting transparent labels and flavors inspired by pop culture. There's untapped potential in muscle-recovery and nootropic-enhanced drinks. Here, the murky waters of health claim regulations offer a golden chance for brands ready to invest in clinical studies and engage with the EFSA. While many brands still lean on traditional retail methods, there's a noticeable gap in tech adoption. Most haven't embraced data-driven demand forecasting or dynamic pricing, presenting a golden opportunity for tech-savvy newcomers to streamline inventory and cut down on waste. As aluminum can production ramps up and supply constraints ease by late 2026, the competitive landscape is set to heat up. This will lower entry barriers, allowing private-label brands to stake their claim in the value-tier segments.

Europe Energy Drinks Industry Leaders

Monster Beverage Corporation

PepsiCo, Inc.

Red Bull GmbH

Suntory Holdings Limited

Vitamin Well Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Nutrabolt unveiled its limited-edition, sugar-free drink, C4 Ultimate Energy x Godzilla. This Sour Blue Razzilla flavor boasts 300mg of caffeine, derived from the Tri-Stim blend (Caffeine, TeaCrine, Dynamine), ensuring sustained energy. The launch, bolstered by multi-channel marketing, influencer partnerships, and activations at the NACS Show, seamlessly fuses pop culture with performance.

- September 2025: Mahou San Miguel made its debut in the energy drink arena with "Refeel" in Spain. Aiming at the rapidly expanding low-calorie market, this 100% natural beverage, flavored with mango and pineapple, boasts plant-based caffeine and contains fewer than 20 calories per 10cl. It's conveniently available through supermarkets, delivery platforms, and company-owned stores.

- June 2025: Ghost Energy Drink rolled out a revamped 500ml variant in the UK through Prolife. This version, featuring 160mg of caffeine (25% less than its US counterpart), substitutes VitaCholine for the previously used NeuroFactor/alpha-GPC. It comes in four enticing flavors: Blue Raspberry, Cherry Limeade, Original, and Sour Warheads Watermelon.

- January 2025: Celsius, one of the largest energy drink brands in the US, made its foray into the UK market. Partnering with Suntory Beverage & Food GB&I, Celsius aimed at grocers, independent outlets, and convenience stores, starting February 3. Their zero-sugar cans, packed with vitamins C, B5, B6, and B12, offer a medley of fruit flavors: Peach Vibe, Fantasy Vibe (orange), Cosmic Vibe, and Sunset Vibe (mango-passionfruit).

Europe Energy Drinks Market Report Scope

Energy Shots, Natural/Organic Energy Drinks, Sugar-free or Low-calories Energy Drinks, Traditional Energy Drinks are covered as segments by Soft Drink Type. Glass Bottles, Metal Can, PET Bottles are covered as segments by Packaging Type. Off-trade, On-trade are covered as segments by Distribution Channel. Belgium, France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom are covered as segments by Country.By Type

| Traditional Energy Drinks |

| Sugar-free or Low-calories Energy Drinks |

| Natural/Organic Energy Drinks |

| Energy Shots |

| Other Energy Drinks |

By Packaging Type

| PET Bottles |

| Glass Bottles |

| Metal Can |

| Aseptic packages |

| Disposable Cups |

Fucntionality

| Endurance/Energy Boost |

| Muscle Recovery |

| Other |

By Distribution Channel

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Type | Traditional Energy Drinks | |

| Sugar-free or Low-calories Energy Drinks | ||

| Natural/Organic Energy Drinks | ||

| Energy Shots | ||

| Other Energy Drinks | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Metal Can | ||

| Aseptic packages | ||

| Disposable Cups | ||

| Fucntionality | Endurance/Energy Boost | |

| Muscle Recovery | ||

| Other | ||

| By Distribution Channel | HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms