Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

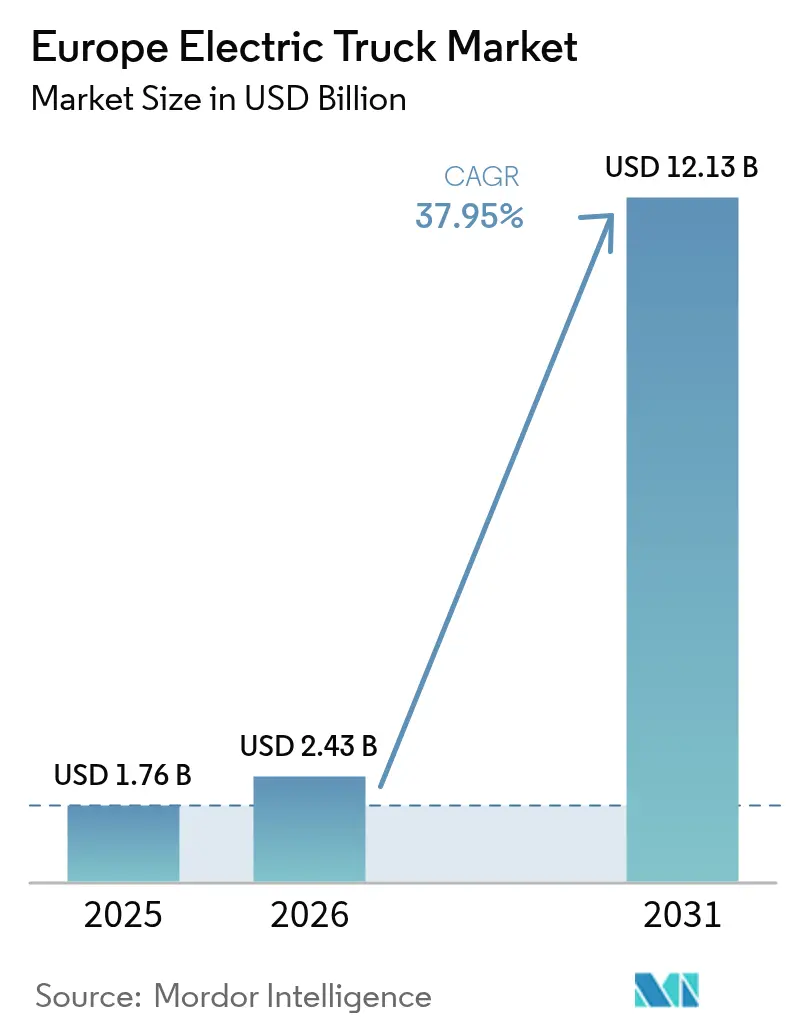

| Base Year Market Size (2025) | USD 1.76 Billion |

| Market Size (2026) | USD 2.43 Billion |

| Market Size (2031) | USD 12.13 Billion |

| Growth Rate (2026 - 2031) | 37.95% CAGR |

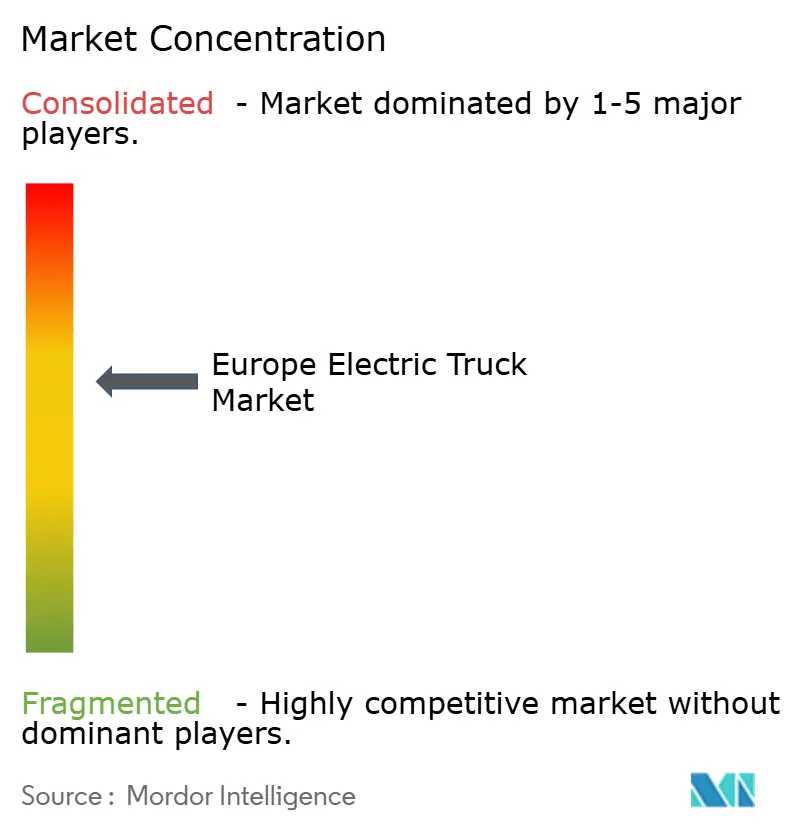

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Electric Truck Market Analysis by Mordor Intelligence

The European electric truck market size is expected to grow from USD 1.76 billion in 2025 to USD 2.43 billion in 2026 and is forecast to reach USD 12.13 billion by 2031 at 37.95% CAGR over 2026-2031. This steep growth path is driven by the European Union’s binding CO₂-reduction targets, falling battery pack prices, and the rapid build-out of megawatt-class charging corridors. Together, these forces shift electric trucks from pilot projects to mainstream fleet assets, especially in high-utilization logistics routes. Regulatory deadlines compel manufacturers to ramp output, while corporate sustainability pledges translate into firm purchase orders that stabilize demand and spur scale economies. At the same time, improvements in battery energy density, rising renewable-power penetration, and innovative financing models narrow the remaining total-cost-of-ownership premium versus diesel, further accelerating adoption across regional and long-haul applications. As a result, the European electric truck market is moving from early-adopter clusters to a broad commercial footprint that touches every major freight corridor on the continent.

Key Report Takeaways

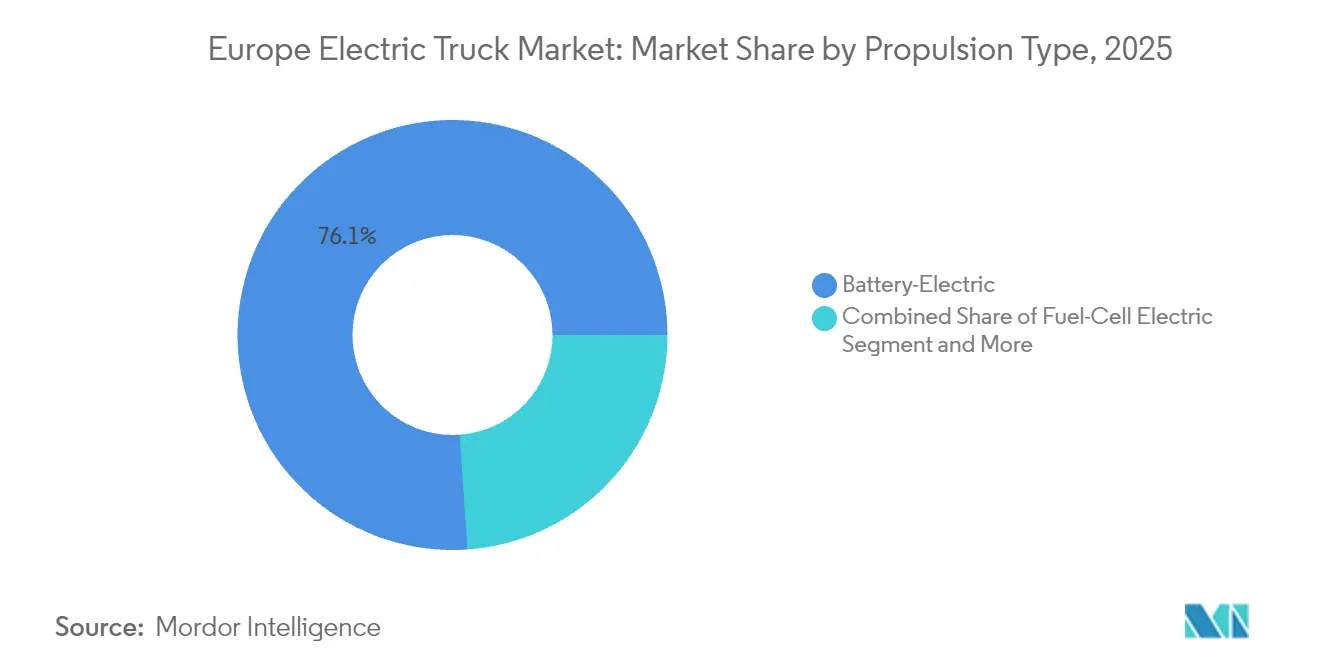

- By propulsion type, battery-electric systems commanded 76.12% of the European electric truck market size in 2025, whereas fuel-cell variants are advancing at a 42.75% CAGR to 2031.

- By truck type, heavy-duty models above 12 tons held a 47.05% share of the European electric truck market size in 2025, while tractor-trailers are expected to record the fastest trajectory at 39.05% CAGR through 2031.

- By battery type, NMC chemistry led with 69.62% of the European electric truck market size in 2025; LFP cells are poised to expand at a 41.35% CAGR to 2031.

- By battery capacity, the 50-250 kWh bracket accounted for 55.38% share of the European electric truck market size in 2025, while packs above 250 kWh are expected to grow at a 40.95% CAGR.

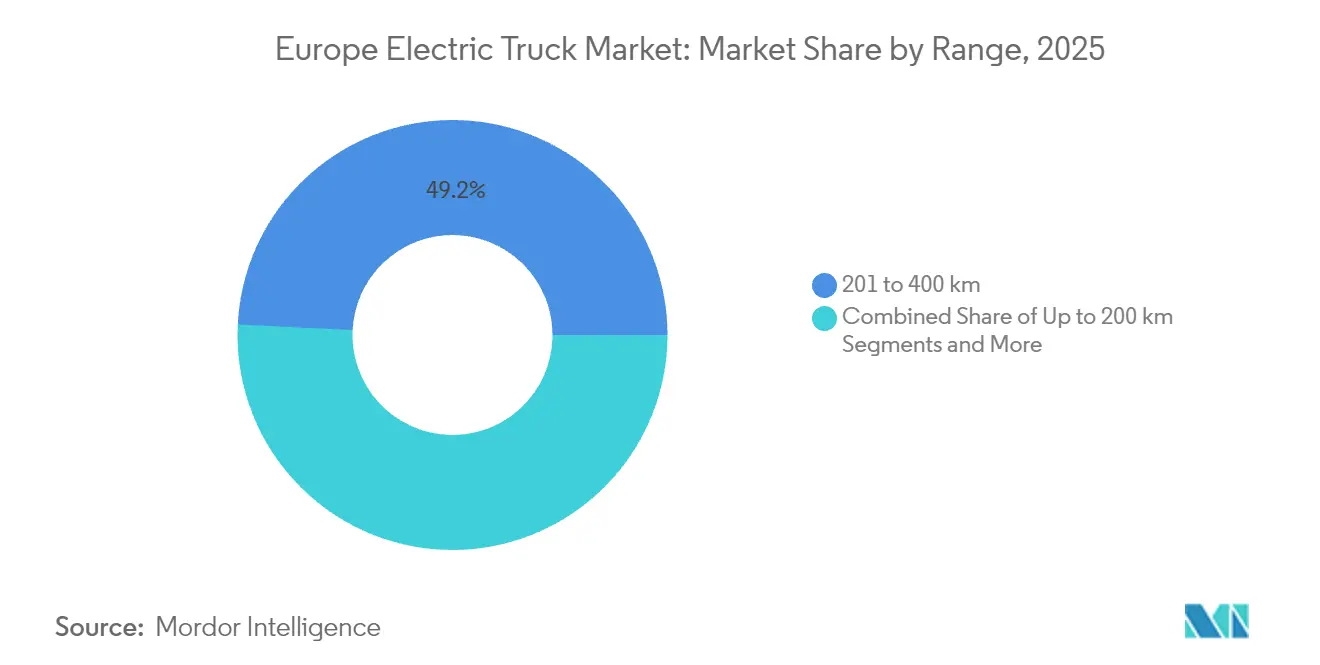

- By range, the 201-400 km class dominated with 49.22% of the European electric truck market size in 2025, whereas trucks exceeding 400 km range are expected to post a 41.6% CAGR through 2031.

- By application, logistics and parcel delivery led with 52.15% share of the European electric truck market size in 2025; construction and mining are expected to be the fastest 42.4% CAGR to 2031.

- By geography, Germany captured 30.78% of the European electric truck market size in 2025; Norway marks the highest 41.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Electric Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emission Standards and ZEV Mandates | +6.2% | Germany, France, Netherlands, Sweden | Medium term (2-4 years) |

| Battery-Pack Cost Declines | +5.8% | Germany, Sweden, Netherlands, Norway | Short term (≤ 2 years) |

| Corporate Fleet-Decarbonization | +4.9% | Germany, UK, France, Netherlands | Medium term (2-4 years) |

| Purchase Incentives and Toll Exemptions | +3.1% | Norway, Netherlands, Germany, UK | Short term (≤ 2 years) |

| Megawatt-Charging Corridors | +2.7% | Germany, Netherlands, Sweden, Denmark | Long term (≥ 4 years) |

| Truck-As-A-Service Financing | +1.9% | Germany, UK, France, Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU CO₂ Emission Standards and 2040 ZEV Sales Mandate

Binding CO₂ reduction targets make zero-emission trucks a legal requirement rather than a voluntary sustainability choice. Interim 2030 and 2035 benchmarks provide a clear volume signal that enables manufacturers to justify multi-billion-dollar electrification investments. Fleet operators face steep non-compliance penalties, propelling procurement toward battery-electric and fuel-cell models at scale. National policies such as Germany’s emission-free urban zones tighten the compliance net further, ensuring that the European electric truck market gains momentum well before the 2040 deadline.[1]European Commission, “CO₂ Emission Standards for Heavy-Duty Vehicles,” ec.europa.eu

Rapid Battery-Pack Cost Declines

In 2024, battery pack prices dropped by 20%, settling at USD 115 per kilowatt-hour (kWh)[2]European Alternative Fuels Observatory, "Electric Vehicle Battery Packs Experience Record Price Drop in 2024", alternative-fuels-observatory.ec.europa.eu. Cost parity with diesel emerges first in high-mileage logistics fleets that cover more than 80,000 km annually, where fuel savings offset capital premiums. Wider adoption of LFP chemistry cuts raw-material exposure, boosts cycle life beyond 4,000 charges, and further lowers total ownership cost. European gigafactory build-outs shorten supply chains and anchor regional content, reinforcing the scale economies that sustain the steep learning curve.

Corporate Fleet-Decarbonization Commitments

Consumer-facing multinationals and industrial shippers embed Scope 3 emission targets into procurement scorecards, locking in future demand for electric trucks. Sustainability reporting requirements and investor scrutiny create pricing tolerance that outweighs higher sticker costs, especially when electric options secure customer relationships and brand reputation. The resulting demand pipeline extends beyond last-mile e-commerce into bulk freight, refrigerated transport, and specialty haulage, broadening the Europe electric truck market far beyond its early niche.

Purchase Incentives and Road-Toll Exemptions

Vehicle grants of up to 20% in the United Kingdom and full road-toll waivers in Norway directly lower the cost hurdle for fleet buyers. Toll exemptions alone can save a long-haul operator more than EUR 20,000 per truck per year in high-density corridors, greatly improving cash flow. As incentives combine with declining battery costs, the break-even horizon versus diesel shortens to three to four years for regional routes, a timeline acceptable to most leasing structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Vehicle Cost Vs. Diesel | -4.3% | Poland, Spain, Italy, Belgium | Short term (≤ 2 years) |

| Sparse Public Charging Infrastructure | -3.6% | Poland, Spain, Italy, France | Medium term (2-4 years) |

| Grid-Capacity Constraints | -2.8% | Germany, Netherlands, UK, France | Long term (≥ 4 years) |

| Maintenance Skill Shortage | -2.1% | Poland, Spain, Italy, Belgium | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Vehicle Cost Versus Diesel

Electric trucks still carry a 40-60% sticker premium compared with diesel, a barrier for price-sensitive operators in Central and Southern Europe. The premium reflects battery costs, low production volumes, and technology complexity, though rapid cost declines suggest this restraint will diminish significantly by 2027-2028. Limited access to cheap financing amplifies the issue for small fleets. However, truck-as-a-service models and government incentives increasingly neutralize this disadvantage by converting capital expenditure into operational expense structures that better align with cash flow patterns.

Sparse Public HDV-Ready Charging Infrastructure

The public charging infrastructure for heavy-duty vehicles across Europe is currently inadequate. This shortfall significantly restricts the utilization of electric trucks to short and well-defined routes, creating substantial barriers to the widespread adoption of electric vehicles for long-haul transportation. Without a robust network of charging stations, long-distance journeys become impractical, stalling the shift toward more sustainable and environmentally-friendly freight solutions. A lack of standardized megawatt charging systems and the interdependence between infrastructure and vehicle deployment further delay progress. However, the Milence joint venture by Volvo, Daimler, and TRATON aims to install 1,700 chargers by 2027, signaling a strong industry commitment to overcoming these barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Battery-Electric Dominance Accelerates

Battery-electric trucks held 76.12% of the European electric truck market size in 2025, while fuel-cell models track the steepest 42.75% CAGR through 2031. The initial dominance arises from a dense charging-station footprint, proven reliability in parcel delivery and regional freight, and lower operating costs for fleets that rack up daily mileage. Over the forecast period, hydrogen refueling networks extend across Scandinavia and Germany, catalyzing fuel-cell uptake in heavy haul and temperature-sensitive commodities that demand high uptime and quick turnarounds. Plug-in hybrids occupy a narrowing transition niche as zero-emission zoning rules begin to exclude combustion back-up modes entirely.

Fleet use-case alignment will continue to favor battery-electric formats in city and short regional corridors because overnight depot charging remains the simplest infrastructure model. Fuel-cell traction intensifies in routes exceeding 600 km per day, especially where payload penalties from large battery packs would otherwise erode revenue per trip. As battery-energy density improves and charging curves steepen, a measurable share of current fuel-cell prospect routes may flip to pure battery solutions, underscoring the dynamic nature of competition inside the Europe electric truck market.

By Truck Type: Heavy-Duty Leadership Faces Tractor-Trailer Challenge

Heavy-duty rigid trucks over 12 tons currently deliver 47.05% of Europe's electric truck market size in 2025. Their predictable hub-and-spoke logistics cycles maximize battery utilization and justify depot-charging investment. From 2026 onward, the tractor-trailer segment shows the fastest ramp, with a 39.05% CAGR as megawatt chargers roll out on the pan-European freight network and advanced thermal management maintains pack longevity under long-haul duty cycles. Light trucks up to 3.5 tons continue experiencing steady adoption in dense urban zones governed by emission-free mandates. Medium-duty specials such as garbage compactors or crane-equipped chassis see growing municipal interest, but at lower annual volume.

The competitive theater is intensifying around heavy-duty tractors, where newcomers from China and emerging European startups pitch integrated hardware-plus-software stacks that promise lower total cost. Legacy OEMs respond with modular platforms optimized for both regional and cross-border applications, aiming to protect service-network advantages. As a result, the European electric truck market will witness fast price discovery in the tractor segment, setting reference points for the rest of the portfolio.

By Battery Type: NMC Dominance Challenged by LFP Innovation

NMC cells commanded 69.62% of Europe's electric truck market size in 2025 due to their superior gravimetric energy density, a critical factor for payload-sensitive freight. However, LFP chemistry’s cost advantage, cobalt-free supply chain, and excellent cycle life have sparked a 41.35% CAGR, signaling a large-scale pivot for standard-range models. Solid-state prototypes remain in pilot programs, targeting post-2030 volume launches at energy densities above 450 Wh/kg, a step change that could unlock lighter long-haul packs and higher residual values.

The chemistry mix inside the European electric truck market will increasingly split by duty cycle: high-mileage, metro-regional trucks lean toward LFP for lower operating cost and deeper discharge resilience, while ultra-long-range tractors and refrigerated trailers retain NMC or move to advanced solid-state options once commercialized. OEM purchasing strategies now include dual-sourcing from regional gigafactories to mitigate raw-material volatility, sharpening competition among cell suppliers.

By Battery Capacity: Mid-Range Optimization Dominates

Packs rated 50-250 kWh captured 55.38% of Europe's electric truck market size in 2025, matching the 200-400 km daily mission typical for European regional logistics. Above-250 kWh systems track a 40.95% CAGR as OEMs equip tractors for two-shift operations and long-haul segments that demand minimal recharging downtime. Sub-50 kWh micro-packs retain relevance in niche vehicles such as low-speed municipal shuttles and specialized port haulers.

Pack sizing decisions within the European electric truck market increasingly hinge on a holistic energy strategy that balances depot power capacity, grid reinforcement costs, and route scheduling. Fleet data analytics help operators right-size batteries, avoiding unnecessary weight and cost while still guaranteeing operational resilience. Over-the-air telemetry feeds allow dynamic range predictions, enabling smaller packs without compromising service levels.

By Range: Regional Applications Lead Long-Haul Expansion

The 201-400 km range band delivered 49.22% of Europe's electric truck market size in 2025, hitting the sweet spot for one-shift distribution loops that top up overnight. Vehicles exceeding 400 km range accelerate at a 41.6% CAGR as charging nodes proliferate along the TEN-T network and as battery density pushes usable energy beyond 800 kWh without sacrificing payload. Sub-200 km utilities keep a steady share in refuse collection and postal services, benefitting from predictable depot returns.

As charging downtime falls below regulatory driver rest periods, the operational penalty of refueling electric trucks disappears. Consequently, the European electric truck market will witness a progressive share shift toward the 400-700 km class, where diesel still holds sway today. OEM road-testing of megawatt-enabled trucks in Germany, the Netherlands, and Sweden shows consistent energy cost advantages that will accelerate this inflection.

By Application: Logistics Leadership Drives Construction Growth

Logistics and parcel fleets generated 52.15% of Europe's electric truck market unit sales in 2025, propelled by e-commerce demand and city access rules. Construction and mining fleets, although smaller, record the fastest 42.4% CAGR as contractors electrify equipment to gain permits in zero-emission urban zones. Municipal services, utilities, and retail distribution adopt electric trucks at a steady pace, leveraging fleet commonality benefits.

E-commerce giants and third-party logistics providers act as anchor customers, signing multi-hundred-unit framework agreements that stabilize production runs. Construction-sector momentum relies on the deployment of off-grid charging solutions at worksites and on combined vehicle-machinery electrification packages that share power infrastructure.

Geography Analysis

Germany led the European electric truck market with a 30.78% stake in 2025, owing to an advanced supplier base, early purchase incentives, and dense charging coverage. German federal grants of up to EUR 40,000 per truck, coupled with state-level toll exemptions on select Autobahn segments, create a compelling economic case for fleet turnover. Large integrated logistics groups like DHL and DB Schenker have set fleet transition targets that synchronize truck procurement with depot charging upgrades. The strong domestic manufacturing cluster further lowers delivery lead times and ensures parts availability, reinforcing operator confidence.

Norway charts the fastest pathway, posting a 41.9% CAGR through 2031. Full VAT waivers, registration-fee relief, and permanent toll exemptions virtually erase the electric-diesel upfront differential. Abundant hydropower keeps electricity costs low, anchoring total-cost-of-ownership leadership across both urban and regional duty cycles. The National Transport Plan earmarks dedicated HDV charging hubs every 60 km on arterial routes by 2027, removing the range barrier for north-south haulage. The policy package positions Norway as a living laboratory that illustrates the long-term potential of the Europe electric truck market under ideal incentive structures.

Elsewhere, the United Kingdom accelerates adoption via grant funding and Low Emission Zone enforcement, while the Netherlands leverages unparalleled charger density and port-centric logistics demand. France integrates industrial policy by subsidizing domestic battery production alongside vehicle incentives. Italy and Spain focus on EU cohesion-fund grants to build public truck chargers, whereas Poland’s rapidly expanding e-commerce sector seeds future demand despite current infrastructure gaps. Sweden and Denmark make progress by coupling renewable-energy surplus with cross-border freight corridors, and Belgium acts as a strategic charging crossroads linking Atlantic and Central European routes.

Competitive Landscape

The European electric truck market is moderately concentrated, leading to intense but focused rivalry. AB Volvo holds the front position, capitalizing on an early start in serial production and a wide dealer footprint that extends service coverage into secondary freight corridors. Daimler Truck follows, banking on a diversified powertrain portfolio that spans battery and fuel-cell variants as well as flexible financing packages.

Strategic alliances play a pivotal role in defending market positions. Volvo, Daimler, and TRATON co-invest in the Milence charging network, ensuring that their heavy-duty customers find brand-agnostic megawatt charging across Europe’s busiest lanes. Concurrently, joint development of software-defined truck operating systems accelerates time-to-market for digital fleet services, a key differentiator as vehicle operating systems evolve into profit centers.

Competitive pressure intensifies from new entrants. Chinese manufacturers scale aggressively into light and medium segments, offering price-competitive chassis plus integrated telematics subscriptions. Technology-driven players integrate autonomous stack development with electric drivetrains, targeting hub-to-hub long-haul corridors where driver-cost savings can reach up to 30%. These challengers force incumbents to sharpen value propositions that extend beyond mechanical reliability into energy cost management, over-the-air updates, and truck-as-a-service models.

Europe Electric Truck Industry Leaders

-

Scania AB

-

Renault Trucks

-

Daimler Trucks AG

-

MAN Truck and Bus

-

AB Volvo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Daimler Truck has rolled out 14 eActros 600 electric trucks for long-haul operations across Germany, proving their commercial viability on routes exceeding 500 km.

- June 2025: Tesla has confirmed that it is preparing to introduce the Tesla Semi to customers in Europe, marking new competition in the heavy truck market.

- December 2024: Einride has launched daily autonomous electric freight operations on Swedish public roads, integrating electrification with autonomy for commercial logistics.

- October 2024: Volvo Group and Daimler Truck launched a joint venture, establishing a software-defined truck platform to support future digital services.

Europe Electric Truck Market Report Scope

Electric trucks can be defined as commercial vehicles powered by a pack of batteries, and they are used for the transportation of cargo. In electric trucks, motors inside have fewer parts moving compared to a diesel truck and don't need multi-speed transmissions, reducing the vehicle's maintenance cost and improving reliability with almost zero noise pollution.

The European electric truck market covers the latest trends and technological development in the electric bus market in European countries. The report's scope covers segmentation based on propulsion type, truck, application, and country. By Propulsion type, the market is segmented into a plug-in hybrid, fuel cell electric, and battery electric. By truck type, the market is segmented into light truck, medium-duty truck, and heavy-duty truck. By application, the market is segmented into logistics, municipal, and other applications. By country, the market is segmented into Germany, the United Kingdom, France, Italy, the Netherland, Spain, and the Rest of Europe. For each segment, market sizing and forecasting are based on value (USD million).

By Propulsion Type

| Battery-Electric |

| Fuel-Cell Electric |

| Plug-in Hybrid |

By Truck Type

| Light Truck (Up to 3.5 t) |

| Medium-Duty Truck (3.6 to 12 t) |

| Heavy-Duty Truck (Above 12 t) |

| Tractor-Trailer |

By Battery Type

| Lithium-Nickel-Manganese-Cobalt Oxide (NMC) |

| Lithium-Iron-Phosphate (LFP) |

| Others (NCA, LTO, solid-state prototypes) |

By Battery Capacity

| Less Than 50 kWh |

| 50 to 250 kWh |

| Above 250 kWh |

By Range

| Up to 200 km (urban) |

| 201 to 400 km (regional) |

| Above 400 km (long-haul) |

By Application

| Logistics and Parcel |

| Municipal Services (Waste, Street-sweep) |

| Construction and Mining |

| Retail and FMCG Delivery |

| Utility and Other Industrial |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Netherlands |

| Spain |

| Sweden |

| Norway |

| Denmark |

| Belgium |

| Poland |

| Rest of Europe |

| By Propulsion Type | Battery-Electric |

| Fuel-Cell Electric | |

| Plug-in Hybrid | |

| By Truck Type | Light Truck (Up to 3.5 t) |

| Medium-Duty Truck (3.6 to 12 t) | |

| Heavy-Duty Truck (Above 12 t) | |

| Tractor-Trailer | |

| By Battery Type | Lithium-Nickel-Manganese-Cobalt Oxide (NMC) |

| Lithium-Iron-Phosphate (LFP) | |

| Others (NCA, LTO, solid-state prototypes) | |

| By Battery Capacity | Less Than 50 kWh |

| 50 to 250 kWh | |

| Above 250 kWh | |

| By Range | Up to 200 km (urban) |

| 201 to 400 km (regional) | |

| Above 400 km (long-haul) | |

| By Application | Logistics and Parcel |

| Municipal Services (Waste, Street-sweep) | |

| Construction and Mining | |

| Retail and FMCG Delivery | |

| Utility and Other Industrial | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Netherlands | |

| Spain | |

| Sweden | |

| Norway | |

| Denmark | |

| Belgium | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe Electric Truck Market?

The Europe Electric Truck Market size is expected to reach USD 2.43 billion in 2026 and grow at a CAGR of 37.95% to reach USD 12.13 billion by 2031.

What is the current Europe Electric Truck Market size?

In 2026, the Europe Electric Truck Market size is expected to reach USD 2.43 billion.

Who are the key players in Europe Electric Truck Market?

Volvo Group, Renault Trucks, Scania AB, Daimler and MAN trucks are the major companies operating in the Europe Electric Truck Market.

What years does this Europe Electric Truck Market cover, and what was the market size in 2025?

In 2025, the Europe Electric Truck Market size was estimated at USD 1.76 billion. The report covers the Europe Electric Truck Market historical market size for years: 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Europe Electric Truck Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

How fast will electric trucks scale in European heavy-duty freight?

The segment for tractors above 12 tons is projected to climb at a 39.05% CAGR to 2031, fueled by megawatt charging corridors and tightening CO₂ caps.

Which country today buys the most electric trucks?

Germany leads with 30.78% of 2025 unit registrations thanks to strong incentives and extensive charging infrastructure.

What range do regional electric trucks typically cover?

The 201-400 km category holds 49.22% share, offering enough daily mileage for one-shift distribution with overnight depot charging.

Which battery chemistry is set to gain share fastest?

LFP cells are forecast to grow at a 41.35% CAGR to 2031 as fleets prioritize lower cost and long cycle life.

What is the biggest cost hurdle for operators?

The residual 40-60% upfront price premium versus diesel remains the top barrier, especially for smaller fleets in price-sensitive markets.

Page last updated on: