Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

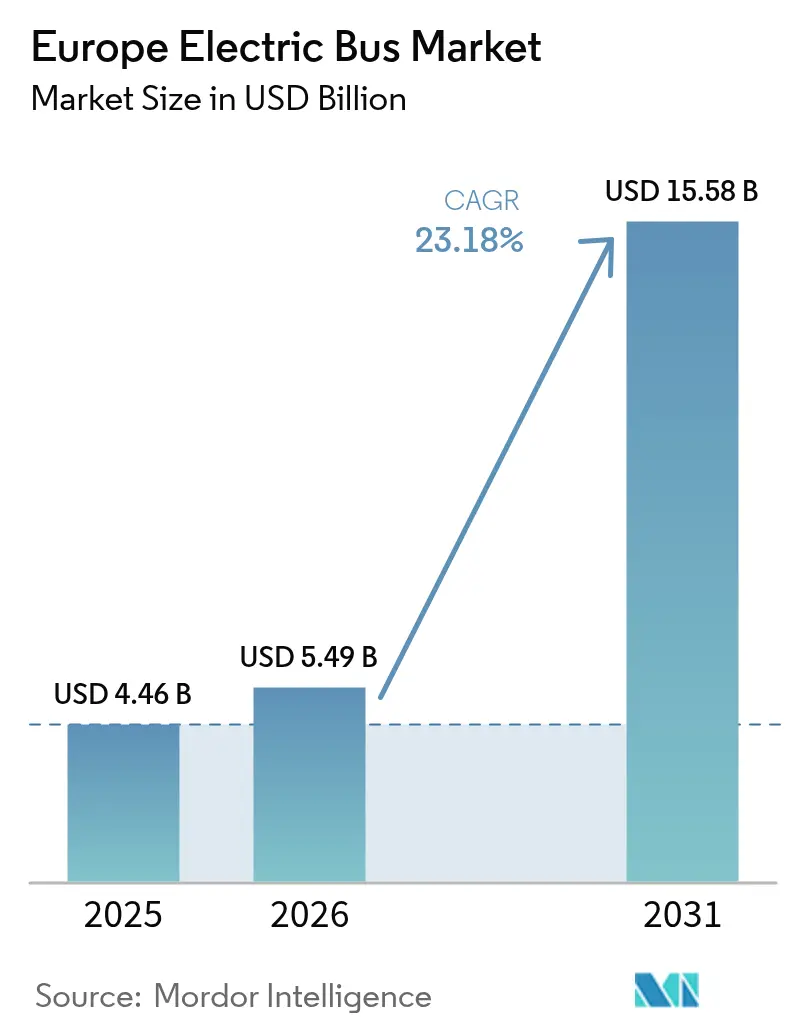

| Base Year Market Size (2025) | USD 4.46 Billion |

| Market Size (2026) | USD 5.49 Billion |

| Market Size (2031) | USD 15.58 Billion |

| Growth Rate (2026 - 2031) | 23.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electric Bus Market Analysis by Mordor Intelligence

The Europe electric bus market size was valued at USD 4.46 billion in 2025 and estimated to grow from USD 5.49 billion in 2026 to reach USD 15.58 billion by 2031, at a CAGR of 23.18% during the forecast period (2026-2031). Aggressive EU-level CO₂ standards, expanding clean-vehicle procurement quotas, and widening gaps in total cost of ownership versus diesel have converged to make battery-electric buses the default option for municipal fleets. Operators increasingly favor electrification because battery prices continue to fall, charging infrastructure is backed by a EUR 1 billion EU funding stream, and ETS-2 carbon pricing is set to raise diesel fuel costs from 2027. The Europe electric bus market, therefore, combines regulatory certainty with improving economics and rising corporate appetite for sustainability branding, reinforcing the investment cycle.

Key Report Takeways

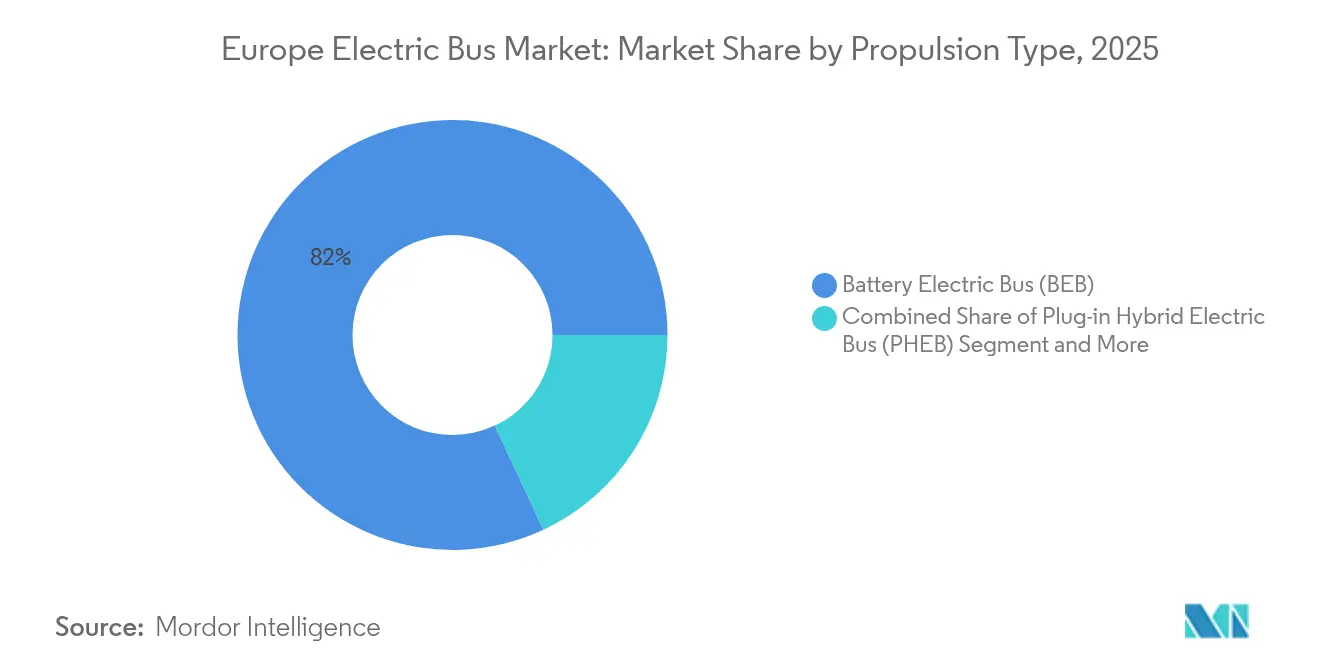

- By propulsion type, battery-electric buses led with 81.95% revenue share in 2025; the segment is also forecast to post the fastest growth at 24.10% CAGR through 2031.

- By battery chemistry, LFP captured 48.75% of the Europe electric bus market share in 2025 and is advancing at 24.60% CAGR through 2031.

- By bus length, 9-14 m standard models commanded 54.85% of the Europe electric bus market size in 2025; articulated and double-decker formats are advancing at 23.95% CAGR through 2031.

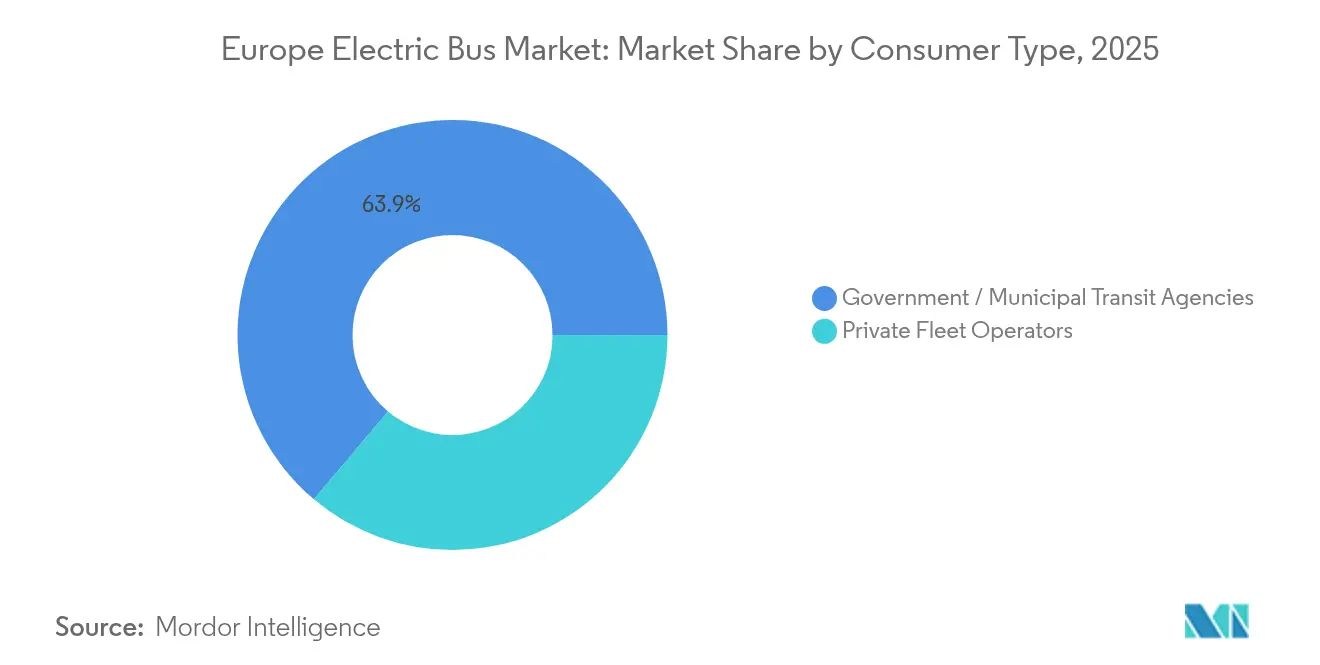

- By consumer type, government and municipal agencies held 63.85% share of the Europe electric bus market size in 2025, whereas private operators recorded the highest projected CAGR at 26.75% to 2031.

- By application, intra-city urban transit accounted for a 67.95% share of the Europe electric bus market size in 2025, while intercity and regional transit is expected to expand at 25.10%.

- By geography, Germany led with 18.35% Europe electric bus market share in 2025; Italy is the fastest-growing national market at 29.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Electric Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling Total-Cost-of-Ownership Versus Diesel After 2026 | +6.8% | Led by Netherlands, Nordic countries | Medium term (2-4 years) |

| EU Clean-Vehicles Directive Compliance Deadlines | +4.2% | EU-wide, strongest in Germany, France | Medium term (2-4 years) |

| Battery-as-a-Service Contracts Lowering Capex Risk | +3.9% | Western Europe, expanding to Central Europe | Medium term (2-4 years) |

| National Zero-Emission Public-Procurement Quotas | +3.5% | EU core markets, emerging in Eastern Europe | Short term (≤ 2 years) |

| Escalating EU Carbon-Pricing Under ETS-2 Boosts Diesel Operating Costs | +2.8% | EU-wide implementation from 2027 | Long term (≥ 4 years) |

| On-Site Depot Battery-Storage Shaving Peak-Demand Charges | +2.1% | Germany, Netherlands, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Falling Total Cost of Ownership Versus Diesel After 2026

Battery prices fell sharply in 2024 on wider LFP adoption, cutting pack costs by about 20% compared with NMC. When maintenance savings and ETS-2 carbon charges are added, an electric bus purchased in 2025 is projected to reach TCO parity with a diesel unit within four years of service. Early deployments of the Mercedes-Benz eCitaro in Berlin and Utrecht reveal annual maintenance savings exceeding 30% thanks to fewer drivetrain wear parts. Fleet operators are now standardizing three-shift duty cycles that push electric utilization above 96%, which accelerates payback. Such economics underpin private-sector confidence and explain why venture funding for specialized e-bus operators climbed 18% in 2025 [1]“eCitaro Total Cost Savings Data Sheet,” Daimler Truck AG, daimlertruck.com.

EU Clean-Vehicles Directive Deadlines

Binding procurement targets under the Clean-Vehicles Directive remove uncertainty for city transport agencies, prompting multi-year tenders that bundle vehicle supply and charging solutions. Germany’s Saubere-Fahrzeuge-Beschaffungs-Gesetz lifts required clean-vehicle purchases to 65% for 2026-2030, half of which must be zero-emission. Similar transpositions in France and Spain are clustering demand into large, predictable tranches that let manufacturers optimize production lines and reduce per-unit costs. National flexibility to pool targets across contracting authorities also raises purchasing power, helping smaller cities gain volume discounts. As a result, more than 49% of new EU city buses were already zero-emission in 2024, a share expected to exceed 70% by 2027 [2]“Half of EU City-Bus Sales Were Zero-Emission in 2024,” Transport & Environment, transportenvironment.org.

National Zero-Emission Public-Procurement Quotas

Member states surpassing EU minimums further concentrate demand. The United Kingdom earmarked GBP 500 million to place 1,200 zero-emission buses on the road by 2026, directly stimulating domestic plants in Scarborough and Falkirk. Sweden’s public tenders require operators to reach 95% electric fleets by 2027, compelling firms such as Nobina to secure multi-hundred-unit contracts in advance. Finland channels low-cost debt from the Nordic Investment Bank to bridge municipal funding gaps, accelerating uptake in mid-sized cities. These national quotas create regional hubs of operational knowledge, which then spill into neighboring markets through cross-border operator groups [3]“EUR 13.2 Million Loan for Finnish E-Bus Fleet,” Nordic Investment Bank, nib.int.

On-Site Depot Battery-Storage Shaving Peak-Demand Charges

Transit agencies increasingly treat depots as grid-interactive assets. In Hamburg and Rotterdam, co-located stationary batteries cut demand charges by up to 30% when electric buses fast-charge simultaneously during nightly pull-ins. Smart-charging software staggers plug-in cycles to coincide with renewable power peaks, easing utility strain and unlocking low-tariff windows. Partnerships such as Siemens-OMV provide turnkey energy-management packages that bundle solar PV, battery-storage containers, and megawatt-scale chargers into a single service contract. Revenue stacking through ancillary grid services adds another line item to project cash flow, improving bankability for private financiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Connection Bottlenecks at Legacy Depots | -3.8% | Germany, Italy, dense EU urban nodes | Short term (≤ 2 years) |

| Shortage of Certified High-Voltage Technicians | -2.7% | Eastern Europe, emerging in West | Long term (≥ 4 years) |

| Residual-Value Uncertainty for First-Gen Buses | -2.4% | EU-wide leasing markets | Medium term (2-4 years) |

| Potential EU Tariffs on Chinese E-Buses | -1.9% | EU-wide trade policies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Bottlenecks at Legacy Depots

Upgrading substations and cabling at sites built for diesel fleets remains slow because utilities face long permitting backlogs. Operators in Milan and Munich report waits of 18 months or more for 2-MW connections, forcing interim reliance on mobile chargers that limit overnight energy intake. The European Commission’s Action Plan for Grids identifies a 60% increase in electricity demand by 2030, yet many city centers have little spare cabling capacity to handle clustered charging. Delays can push back contract start dates and inflate depot conversion budgets, cooling near-term delivery schedules despite healthy order books.

Residual-Value Uncertainty for First-Generation E-Buses

Buses delivered between 2020 and 2023 carry batteries whose capacity and chemistry may fall short of upcoming EU recycled-content rules. Lessors, therefore, struggle to estimate resale values, prompting shorter lease terms and higher residual guarantees that shift risk back to operators. Solaris and Volvo have responded with extended battery warranties, but a secondary-market pricing curve has yet to stabilise. Operators worry that residual-value gaps could widen when long-range, fast-charging second-generation buses dominate auctions after 2027, adding a financing premium to current procurements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Battery-Electric Becomes the Standard

Battery-electric technology controlled 81.95% of the Europe electric bus market in 2025, driven by regulatory mandates and the maturing supply chain that reduce purchase price gaps. Strong policy backing, simpler drivetrains, and falling battery costs support a 24.10% CAGR for the segment through 2031. Fuel-cell buses remain a strategic hedge for routes exceeding 400 km daily, but scarce hydrogen refueling sites restrict widespread adoption. Plug-in hybrids now serve mostly in transitional contracts where depot upgrades are incomplete.

Manufacturers are standardizing power electronics and thermal-management systems across their electric and hydrogen lines, which lowers development expense. Solaris is executing a 130-unit hydrogen order for Bologna while maintaining battery-electric production at volume, ensuring flexibility if policy signals shift. Because heavy municipal subsidies target zero tailpipe emissions rather than a specific technology, fleet managers continue to pick battery-electric options for near-term compliance and cost reliability, cementing segment leadership for the next five years.

By Battery Chemistry: LFP Extends Lead on Safety and Cost

Lithium-iron-phosphate packs captured 48.75% Europe electric bus market share in 2025 and lead the category with the fastest projected expansion of 24.60% CAGR through 2031, driven by cost advantages and superior thermal stability that resonate with operator safety and economic priorities. The chemistry’s cycle life of 4,000+ charge events helps operators plan for 12-year asset lives without mid-life battery swaps, cutting lifetime capex. Renault’s decision to source LFP modules from CATL’s Hungarian plant illustrates OEM confidence in European supply security. Lithium nickel manganese cobalt oxide remains the chemistry of choice for articulated buses that need high energy density, but rising cobalt prices and ESG scrutiny create headwinds.

Europe electric bus market size gains tied to LFP are reinforced by EU Battery Regulation recycled-content quotas that are easier to meet with iron-based cathodes. Operators in Helsinki and Vienna report battery warranty claims trending lower than early NMC fleets, signaling reduced technical risk. Over the forecast horizon, sodium-ion research may add yet another low-cost chemistry, but commercial scale is unlikely before 2030, leaving LFP dominant.

By Bus Length: Standard Models Anchor Urban Networks

Standard 9-14 m buses held 54.85% of Europe electric bus market size in 2025, reflecting efficient maneuverability in historic city layouts and capacity for 70-90 passengers. Operators appreciate that these vehicles fit existing depot bays and charge within night-shift windows without expensive infrastructure upgrades.

Articulated and double-decker models post the quickest growth, 23.95% CAGR, because they serve dense corridors in London, Copenhagen, and Barcelona. Higher upfront price is offset by greater passenger-kilometers per driver, supporting favourable labor economics. Mini-bus formats under 9 m continue to fill niche airport or rural feeder roles where demand is thin, yet fleet numbers remain modest relative to core city trunks.

By Consumer Type: Private Operators Close the Gap

Government agencies still dominate with a 63.85% share because their procurement cycles align with political climate commitments and grant programs. However, private fleet operators show the strongest momentum, logging 26.75% CAGR to 2031. This trend reflects franchising models in countries such as Sweden, where public authorities set service standards but outsource operations under long-term contracts that reward low emissions.

Large private groups like Arriva and Keolis benefit from multi-country scale and can amortise training and telematics investment over thousands of vehicles. Venture-funded newcomers are also entering premium intercity coach segments, attracted by falling battery costs and route profitability. As financing houses grow comfortable with Battery-as-a-Service structures, private ownership of electric buses is expected to overtake municipal ownership on new registrations after 2029, further diversifying the competitive field.

By Application: Inter-City Services Unlock New Range Potential

Although intra-city urban operations accounted for 67.95% of usage in 2025, while improvements in battery energy density are unlocking inter-city and regional services at a 25.10% CAGR. Daimler’s eIntouro prototype posts a 500 km range, eliminating one mid-route charge stop on many regional lines. National coach operators in Austria and Portugal have begun pilot runs that report 90% lifetime CO₂ savings compared with Euro VI diesels, strengthening investor narratives.

Airport shuttle operators also transition rapidly because predictable timetables simplify charging logistics. Meanwhile, tourism-focused services in southern Italy and the Greek islands evaluate rooftop solar-assisted charging to mitigate grid constraints. By 2030, the share of Europe's electric bus market deployments on inter-city routes is projected to double, indicating significant upside for long-range models.

Geography Analysis

Germany maintained 18.35% of the Europe electric bus market share in 2025, thanks to a federal subsidy that reimburses up to 80% of the cost difference between electric and diesel models. The domestic footprint of Daimler, MAN, and Solaris subsidiaries accelerates local content compliance, encouraging cities such as Hamburg and Berlin to place bulk orders extending to 2030. Public-private partnerships also fund charging depots with surplus capacity that neighboring municipalities can access, spreading infrastructure costs.

Italy is poised for the fastest growth, 29.90% CAGR, under a EUR 50 million incentive scheme backed by EU recovery plans. Fleet expansions in Rome, Milan, and Naples aim to meet looming air-quality deadlines while stimulating domestic body assemblers. Italian transit agencies often select joint procurement frameworks that aggregate demand across provinces, enhancing tender volumes and lowering per-vehicle prices.

The United Kingdom continues to deploy large fleets under its GBP 500 million Zero-Emission Bus Regional Areas program, recording 40% year-on-year growth in 2024. Scotland achieves especially high penetration because island and rural councils value noise reduction and stable electricity pricing. France leverages domestic producers such as Iveco Bus to maintain competitive pricing and secure export contracts in francophone Africa, indirectly strengthening the local supply chain. Nordic countries already run near-saturated electric penetration, yet they continue to pilot emerging technologies such as inductive road charging, ensuring that lessons from extreme-climate operations feed back into continental best practices.

Competitive Landscape

The Europe electric bus market displays moderate concentration. Top suppliers include Mercedes-Benz, MAN, Volvo, Solaris, and BYD. Traditional OEMs leverage decades-old dealer networks, which reassure operators about parts availability and residual-value support. Solaris differentiates through early hydrogen expertise, winning mixed-technology tenders that hedge future policy swings.

Chinese entrant BYD continues to build presence through joint ventures that localize assembly, softening potential tariff exposure. Its alliance with Alexander Dennis in the United Kingdom produces double-deckers tailored to tight London clearances, undercutting European rivals on price while meeting local-content rules. Meanwhile, Scania strengthened vertical integration in 2025 by deepening battery cell collaboration with Northvolt, seeking cost and supply security.

Across the European electric bus industry, competitive advantage is shifting from hardware margins to lifecycle services. Mercedes-Benz’s OMNIplus five-year battery warranties bundle telematics, driver training, and energy-management software, thus locking in long-term revenue streams. Volvo and VDL now offer depot-electrification engineering alongside vehicle deliveries, capturing infrastructure spending that may exceed bus cost over a ten-year horizon. Digital fleet-optimization platforms further wedge into value capture, with telematics providers partnering directly with financiers to underwrite performance guarantees.

Europe Electric Bus Industry Leaders

MAN Truck & Bus

Solaris Bus & Coach sp. z o.o.

Volvo Buses

Mercedes-Benz Group AG

BYD Auto Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: MAN Truck & Bus premiered the Lion's Coach E with up to 650 km range and 375 kW CCS charging, marking Europe’s first series-production electric coach.

- May 2025: VAG Nuremberg added 31 Mercedes-Benz eCitaro G articulated units to its urban fleet, supporting high-capacity corridors.

- April 2025: Solaris won 170-bus contracts in Sweden, including 89 units for Nobina Sverige and 81 for VR Sverige AB, consolidating its Nordic footprint.

- February 2025: Go-Ahead placed its inaugural electric bus order with Volvo, expanding the OEM’s position in the UK regional market.

Europe Electric Bus Market Report Scope

The European Electric Bus Market is segmented by Propulsion type (Battery Electric Bus, Plug-in Hybrid Electric Bus, and Fuel Cell Electric Bus), By battery type (Lithium-ion, Nickel-metal hydride battery (NiMH), and Others), By Consumer Type (Government and Fleet Operators), and by Country. The report offers the market size and forecasts in Value (USD billion) for all the above segments.

The Europe Electric Bus Market covers the latest electric bus demand trends, technological development, latest government policies, battery technologies, etc. It also covers the market share of major electric bus manufacturers across Europe.

By Propulsion Type

| Battery Electric Bus (BEB) |

| Plug-in Hybrid Electric Bus (PHEB) |

| Fuel-Cell Electric Bus (FCEB) |

By Battery Chemistry

| Lithium-Iron-Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt Oxide (NMC) |

| Nickel-Metal Hydride (NiMH) |

| Others (Sodium-ion, Solid-state) |

By Bus Length

| Less than 9 m |

| 9-14 m (Standard) |

| Above 14 m (Articulated/Double-decker) |

By Consumer Type

| Government / Municipal Transit Agencies |

| Private Fleet Operators |

By Application

| Intra-city Urban Transit |

| Inter-city & Regional |

| Airport & Shuttle Services |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Norway |

| Poland |

| Sweden |

| Finland |

| Belgium |

| Switzerland |

| Rest of Europe |

| By Propulsion Type | Battery Electric Bus (BEB) |

| Plug-in Hybrid Electric Bus (PHEB) | |

| Fuel-Cell Electric Bus (FCEB) | |

| By Battery Chemistry | Lithium-Iron-Phosphate (LFP) |

| Lithium Nickel Manganese Cobalt Oxide (NMC) | |

| Nickel-Metal Hydride (NiMH) | |

| Others (Sodium-ion, Solid-state) | |

| By Bus Length | Less than 9 m |

| 9-14 m (Standard) | |

| Above 14 m (Articulated/Double-decker) | |

| By Consumer Type | Government / Municipal Transit Agencies |

| Private Fleet Operators | |

| By Application | Intra-city Urban Transit |

| Inter-city & Regional | |

| Airport & Shuttle Services | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Norway | |

| Poland | |

| Sweden | |

| Finland | |

| Belgium | |

| Switzerland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current Europe electric bus market size?

The Europe electric bus market size stands at USD 5.49 billion in 2026 and is projected to grow to USD 15.58 billion by 2031.

How fast is the Europe electric bus market expected to grow?

The market is forecast to expand at a 23.18% CAGR between 2026 and 2031, underpinned by strict EU clean-transport mandates and falling battery costs.

Which propulsion technology dominates European deployments?

Battery-electric buses dominate 81.95% of new registrations, thanks to mature charging networks and superior total cost of ownership.

Which country is the largest market for electric buses in Europe?

Germany leads with an 18.35% share due to generous federal subsidies and strong domestic manufacturing capacity.

Page last updated on: