Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

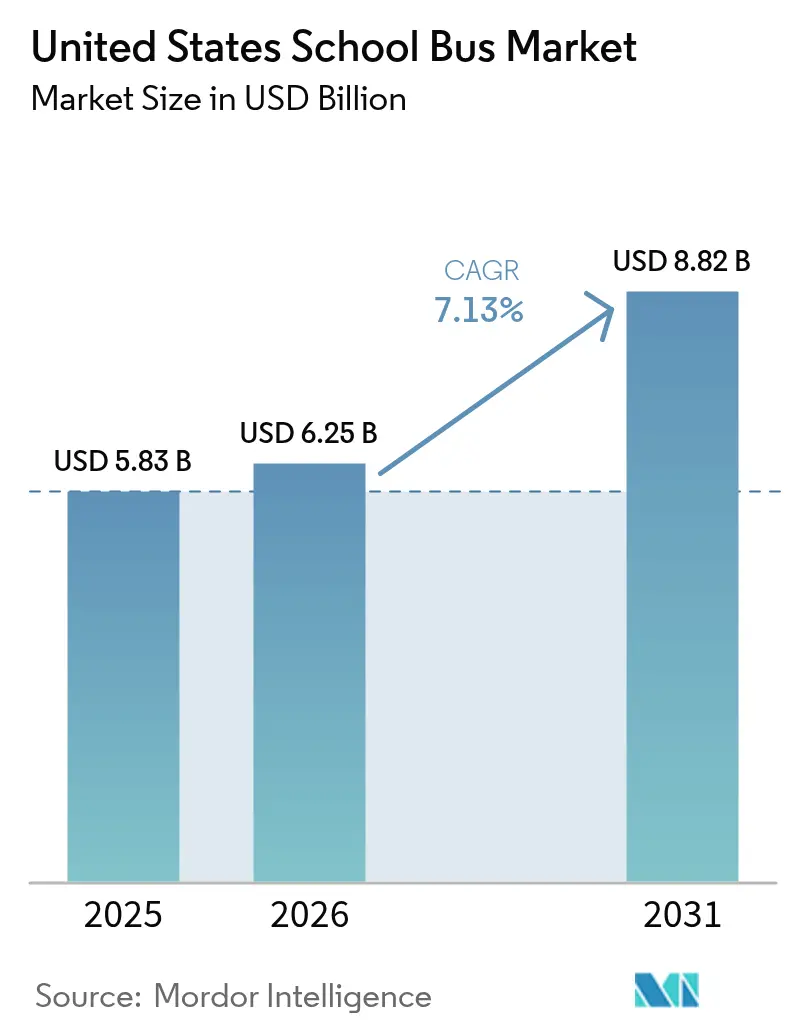

| Base Year Market Size (2025) | USD 5.83 Billion |

| Market Size (2026) | USD 6.25 Billion |

| Market Size (2031) | USD 8.82 Billion |

| Growth Rate (2026 - 2031) | 7.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States School Bus Market Analysis by Mordor Intelligence

The United States school bus market size was valued at USD 5.83 billion in 2025 and estimated to grow from USD 6.25 billion in 2026 to reach USD 8.82 billion by 2031, at a CAGR of 7.13% during the forecast period (2026-2031). With technological advancements, the emergence of electric school buses on roads underscores a dedication to environmental care and the future of younger generations. The swift transition towards battery-electric vehicles and innovative low-NOx solutions is poised to boost the adoption of electric school buses significantly. Simultaneously, stricter NHTSA safety mandates and state-level zero-emission purchase deadlines are advancing replacement decisions that might otherwise have been deferred. Industry participants are therefore balancing near-term chassis shortages, technician training gaps, and uneven charging infrastructure with longer-term opportunities such as vehicle-to-grid revenue streams and depot-based micro-grids that materially reduce total cost of ownership.

Key Report Takeaways

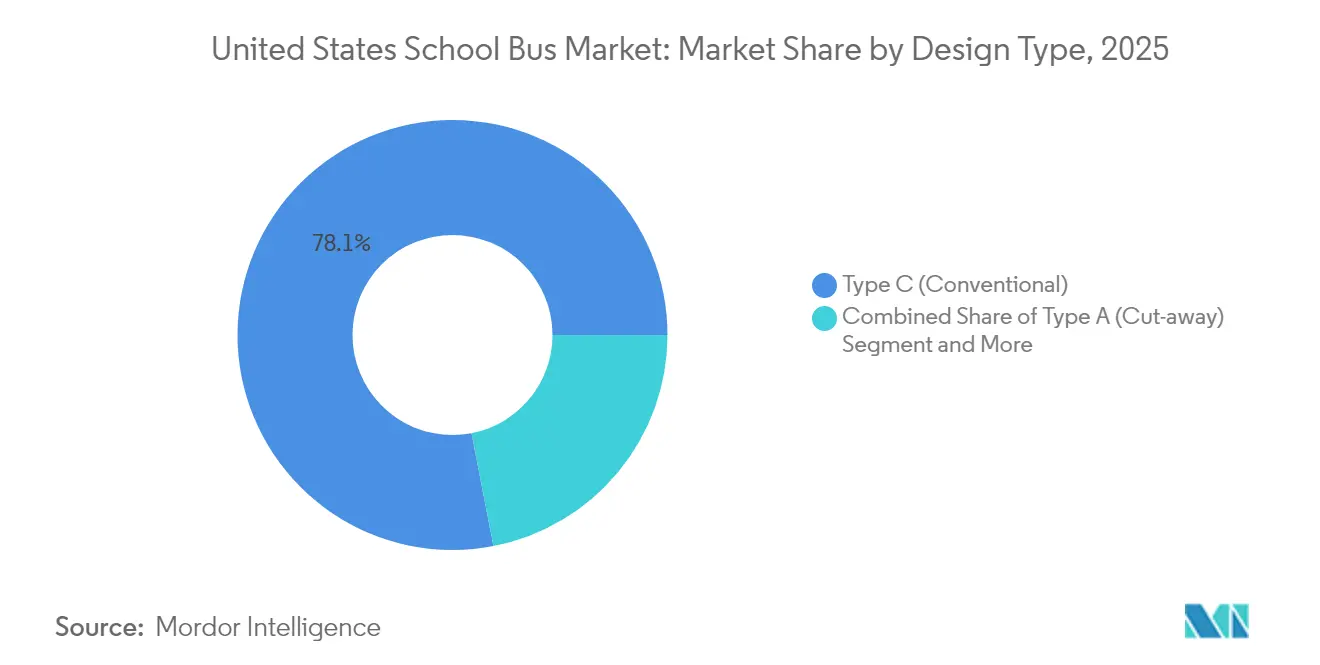

- By design type, Type C (conventional buses) led the United States school bus market with 78.05% of the market share in 2025, advancing at an 8.05% CAGR to 2031.

- By powertrain, internal-combustion models retained an 88.40% share of the United States school bus market size in 2025, whereas battery-electric and hybrid variants are expanding at a 37.09% CAGR through 2031.

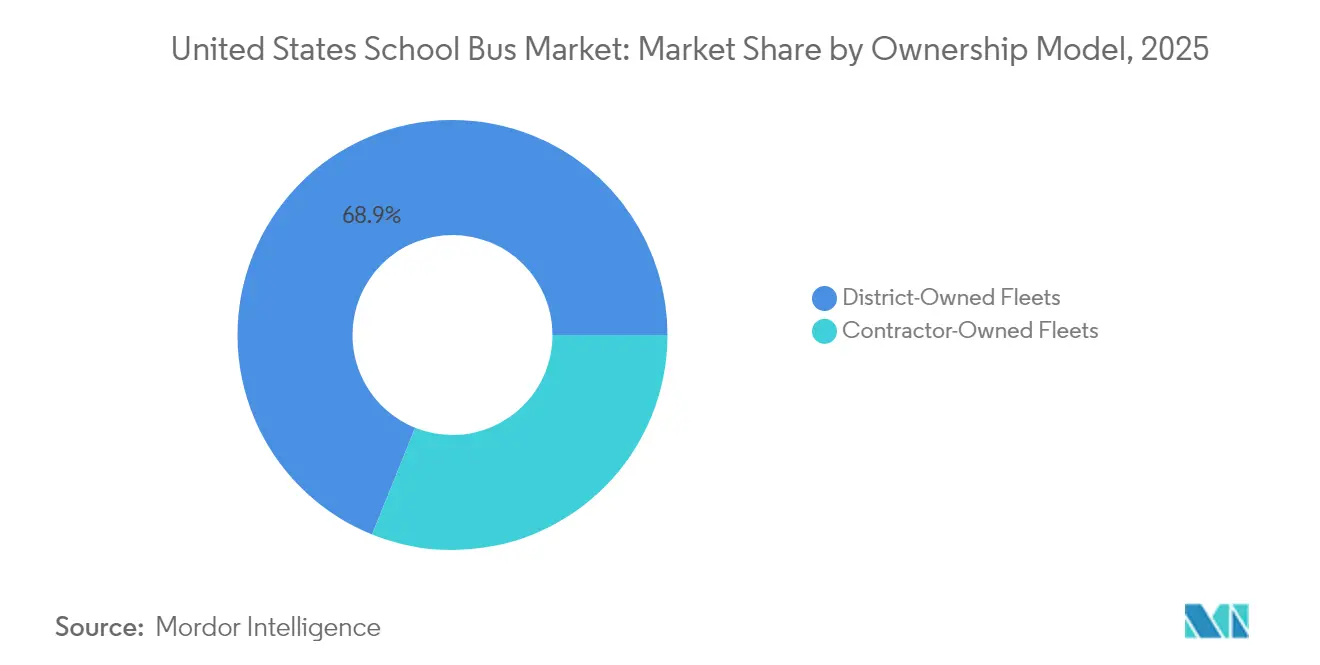

- By ownership model, district-controlled fleets held 68.90% of the United States school bus market in 2025, while contractor-owned operations are forecast to post a 7.76% CAGR during 2026-2031.

- By seating capacity, mid-size (30-60-seat) buses accounted for a 56.60% share of the United States school bus market size in 2025, and smaller (less than 30-seat) buses are projected to grow at an 7.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States School Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPA Clean Bus Funding Boost | +2.1% | National; disadvantaged communities | Medium term (2-4 years) |

| Aging Fleet Drives Bus Demand | +1.8% | National; acute in Midwest and rural districts | Long term (≥ 4 years) |

| Safety Mandates Accelerate Fleet Renewal | +1.3% | Nationwide; stronger in Northeast | Short term (≤ 2 years) |

| Low-NOx Fuel Demand Rises | +0.9% | California, Texas, Northeast corridor | Medium term (2-4 years) |

| V2G Revenue Potential for Schools | +0.7% | California, New York, select pilots | Long term (≥ 4 years) |

| Micro-grids Lower Electric TCO | +0.4% | Sun Belt; utility-partnership regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Funding Surge via EPA Clean School Bus Program

The EPA Clean School Bus Program has altered procurement economics by offsetting up to 80% of incremental costs for battery-electric models, prompting districts to accelerate replacement schedules beyond normal depreciation cycles. Priority scoring directs 45% of funds to low-income and tribal communities, creating adoption clusters in markets that have historically faced limitations due to low tax bases. This wave of subsidized demand is expected to peak before the program sunsets in 2026, compressing procurement windows and intensifying competition for production slots. OEMs and battery suppliers are therefore expanding domestic capacity while forging utility partnerships to streamline charging deployments.

Aging National Fleet (Above 11 yrs) Pushing Replacement Demand

Average bus age now exceeds 11 years, well beyond the Federal Transit Administration’s 12-year or 500,000-mile guidance, creating a backlog of sigiifcnat amount of buses units that must be cycled out within five years. Deferred maintenance costs are escalating, particularly in the Midwest, where harsh winters accelerate corrosion. Electric models cost roughly USD 0.40 per mile to maintain versus USD 0.70 for diesel, allowing life-cycle savings to offset higher purchase prices over 12 years [1]U.S. Department of Energy, “Medium- and Heavy-Duty Vehicle Factsheet,” energy.gov. Rural systems with the oldest fleets are exploring propane or CNG bridges while evaluating grants for electrification infrastructure. OEMs are responding with modular electrified chassis that reuse existing Type C layouts, shortening the learning curve for district mechanics. This alignment of end-of-life timing and incentive availability underpins the robust growth outlook for the United States school bus market.

Stringent On-Board Safety Mandates Accelerating Fleet Renewal

NHTSA’s ongoing revisions to Federal Motor Vehicle Safety Standards are compelling districts to phase out buses built before 2020, especially those lacking modern child-restraint anchors, enhanced glazing, and improved emergency exits. The agency’s 2024 denial of Blue Bird’s FMVSS 217 exemption request underscored regulators’ willingness to impose retrofit costs that can reach USD 15,000 per vehicle, accelerating retirements [2]National Highway Traffic Safety Administration, “Denial of Blue Bird Petition,” nhtsa.gov. Proposed FMVSS 305a rules further raise the bar for electric crashworthiness and post-crash battery isolation, favoring OEMs with deeper compliance engineering budgets. Complementary enforcement tools, such as high-definition stop-arm cameras, have cut violation rates by 40%, reinforcing public pressure for safer, newer fleets. As districts weigh legal liability and insurance premiums, safety compliance is becoming nearly as influential as propulsion choice in replacement decisions.

Low-NOx “Other Fuels” Demand in Non-Attainment Counties

Air-quality rules in ozone-non-attainment zones are sustaining demand for compressed natural gas and propane buses that cut NOx emissions at lower capital cost than electrics. South Coast Air Quality Management District’s Rule 1195 obliges fleet additions to be alternative-fueled, helping CNG capture double-digit shares in Southern California. Texas districts in Houston and Dallas are transitioning to propane, which offers a price discount compared to electric options, providing immediate fiscal relief and achieving 50% savings on fuel costs compared to diesel. Innovative portable CNG refueling trailers deployed in rural Kern County extend adoption beyond pipeline networks. These interim fuels allow districts to meet near-term NOx targets as they plan multi-year charging rollouts, reinforcing a heterogeneous propulsion mix in the United States school bus market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Rural Charging Infrastructure | -1.4% | Rural Midwest and Mountain West | Medium term (2-4 years) |

| E-Bus High Cost Persists | -0.9% | Rural and fiscally constrained districts | Short term (≤ 2 years) |

| High-Voltage Technician Scarcity | -0.7% | Nationwide; rural bias | Long term (≥ 4 years) |

| Medium-Duty Chassis Bottlenecks | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sparse Rural Charging Infrastructure

Rural districts face a five-to-ten-fold deficit in public charging density compared with urban areas, complicating route planning for long daily runs. While Illinois’ Williamsfield Schools overcame the hurdle via a campus microgrid that now meets 94% of energy needs, most rural systems lack the technical staff or utility partnerships to replicate the model. The Infrastructure Investment and Jobs Act allocated USD 1.25 billion for rural EV infrastructure. However, project lead times exceed immediate replacement cycles, resulting in timing misalignments. Until Level 3 chargers become more widely available, diesel and propane will remain important fallback options, tempering overall electrification momentum in the United States school bus market.

High Upfront Cost Of E-Buses Despite Incentives

Despite rebates covering up to 80% of the incremental costs, districts still face an average premium of USD 156,000 when purchasing battery-electric vehicles over diesel ones. This financial strain has led to bond-issue defeats in several counties across New York. The state projects its zero-emission mandate will come with a hefty USD 8.9 billion price tag, a challenge for many localities already grappling with budget constraints and in need of new revenue streams. While repowering existing chassis for USD 110,000-180,000 presents a more economical solution, the adoption has been hampered by ambiguous federal crash-test standards. Meanwhile, energy-as-a-service financing models offer a potential respite, but they require advanced procurement skills that are often lacking in smaller districts, further complicating affordability issues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Design Type: Conventional Dominance Amid Gradual Modernization

Type C (conventional) buses anchored the United States school bus market in 2025 with 78.05% share, and the segment is expected to deliver an 8.05% CAGR through 2031 as districts favor its blend of maneuverability and seating capacity. The United States school bus market size for this design is therefore poised to rise steadily as replacement cycles align with incentive windows that subsidize battery-electric retrofits. OEMs are fortifying Type C platforms with updated driver-assistance suites, while maintaining frame dimensions familiar to maintenance staff. Upgrade packages include electronic stability control and 360-degree camera systems that simplify driver training and reduce insurance premiums.

A parallel modernization wave is unfolding in Type D transit-style configurations, which cater to consolidated routes requiring 90-passenger capacity. Thomas Built’s Saf-T-Liner EFX2 launch in March 2025 added rollover-enhanced body structures and lane-departure warnings, signaling an industry shift toward mass-transit safety norms. As districts consolidate depots and extend route lengths, Type D demand is projected to outpace historical averages, though limited production slots may constrain near-term deliveries. At the smaller end, Type A and B buses serve special-needs transport and tight urban corridors. While they remain niche in unit volume, a surge in individualized education programs is boosting growth prospects, especially for electric variants that can operate quietly during early-morning pickup windows.

By Powertrain Type: Electric Disruption Within Diesel Dominance

Internal-combustion engines captured 88.40% of the United States School Bus Market size in 2025, yet the segment’s share is forecast to shrink as battery-electric deployments accelerate under federal funding schemes. The United States school bus market size for electric models is set to climb rapidly, given their 37.09% CAGR through 2031. Diesel retains an edge in remote geographies where winter resilience and fuel availability remain paramount. Nevertheless, OEMs are integrating lower-NOx engines and idle-reduction systems to extend diesel relevance amid environmental scrutiny.

Electric momentum is particularly strong in states with zero-emission purchase mandates and utility demand-response incentives. Hybrid powertrains occupy a small but strategic niche, offering districts a transitional pathway that mitigates range anxiety while providing fuel savings of 20-30%. Propane and CNG models underpin compliance in ozone-non-attainment counties, their adoption bolstered by lower acquisition prices and familiar fueling infrastructure. Collectively, this diverse propulsion mix underlines why the United States school bus market remains simultaneously mature and transformative.

By Ownership Model: District Control Amid Contractor Growth

District-owned fleets represented 68.90% of the United States School Bus Market size in 2025, reflecting administrators’ desire for direct oversight of safety, legal liability, and labor relations. Yet contractor-operated services are expanding at a 7.76% CAGR during the forecast period, as electrification complexity intensifies capital needs and technical know-how. Outsourcing allows districts to shift fleet-renewal risk and leverage economies of scale in charging infrastructure. National Express School’s acquisition by I Squared Capital highlights growing private-equity interest in consolidating a fragmented segment to unlock purchasing leverage and data-driven route optimization.

Meanwhile, driver shortages, employment is down 15.1% since 2019, are forcing districts to rethink value propositions such as pay scales and scheduling flexibility, areas where large contractors can often outperform local fleets. This dynamic ensures that the United States school bus market will balance public ownership preference against private-sector efficiency gains throughout the decade.

By Seating Capacity: Mid-Size Preference With Small Bus Momentum

Mid-size buses (30-60 seats) commanded 56.60% of the United States School Bus Market size in 2025, aligning with average U.S. route lengths of 32 miles and standard loading dock dimensions. The segment’s dominance will persist because its versatile capacity minimizes per-student costs while preserving maneuverability in suburban cul-de-sacs. However, smaller (below 30-seat) bus models are gaining ground at an 7.89% CAGR, propelled by special-needs services and micro-routing strategies that emerged from COVID-19 social-distancing protocols. The United States school bus market share for these compact designs is therefore climbing steadily, with manufacturers such as Lion Electric introducing 200-mile-range minibuses that solve rural distance constraints.

Large (60-plus-seat) designs traditionally favored in population-dense districts now benefit from extended-range Type D electrics offering 300 miles between charges, a specification that enables single-shift coverage of most rural loops. Whether small, medium, or large, federal safety standards apply equally, disproportionately burdening low-volume segments with testing costs. Established OEMs mitigate this impact through shared component architectures, allowing the entire seating spectrum to evolve in tandem with emerging technologies and regulations.

Geography Analysis

California remains the epicenter of school-bus electrification, having secured funding for more than 2,300 zero-emission units through combined state and federal programs in June 2025. The state’s Assembly Bill 579 bans diesel purchases beyond 2035 and allocates an extra USD 500 million in grants, ensuring continued leadership in charging innovation and fleet deployments. New York follows closely; its Environmental Bond Act provides USD 500 million to bridge remaining cost gaps ahead of the 2027 zero-emission purchase deadline . Even amid voter rejections of some bond issues, the mandate’s legal force is compelling districts to accelerate grant applications and vendor negotiations. Together, these two states account for more than one-third of nationwide electric orders, reinforcing coastal dominance in early-phase market traction.

Texas illustrates a different trajectory, favoring propane and CNG because of abundant local fuel supply and more gradual infrastructure rollouts. Houston and Dallas districts leverage existing natural-gas networks to comply with ozone-attainment goals at lower capital cost, demonstrating why the United States school bus market accommodates multiple propulsion pathways. The Midwest and Mountain West grapple with sub-zero winters and long rural routes, factors that historically hinder battery adoption. However, pilot programs in Montana show modern battery-thermal systems can maintain performance in −20 °C conditions, gradually dispelling cold-weather skepticism.

Rural districts nationwide rely heavily on federal prioritization for disadvantaged communities, which channels 45% of Clean School Bus funds into regions previously sidelined by limited tax bases. The Southeast is increasingly investing in propane solutions while monitoring solar-charging pilots that could enable leapfrogging straight to electric when conditions mature. Collectively, these regional dynamics underscore that no single technology will uniformly dominate; rather, local policy, grid capability, and resource availability will dictate adoption patterns in the United States school bus market.

Competitive Landscape

The market is moderately concentrated: Blue Bird, Thomas Built Buses, and IC Bus together hold a significant share, yet disruptive entrants are redrawing competitive boundaries. Thomas Built’s partnership with Proterra for 800-V packs and eAxles reflects a strategic bet on vertically integrated component ecosystems that optimize range and maintenance profiles. IC Bus, meanwhile, leverages Navistar’s parent company alliances to bundle telematics and over-the-air diagnostics, differentiating on uptime.

Electric-only specialists pursue market share through aggressive technology roadmaps but face capital-intensive hurdles. Lion Electric sought creditor protection in 2025 and refocused exclusively on school buses, illustrating cash-flow volatility when ramping manufacturing at multiple sites. GreenPower Motor Company secured a USD 5 million revolving credit line from Export Development Canada that underwrites expansion at its West Virginia facility, aiming to supply Eastern states rapidly without incurring shipping premiums from West Coast plants. Beyond OEMs, powertrain suppliers and charging-infrastructure developers are forging alliances such as Daimler-Proterra that blur traditional value-chain boundaries and pivot competition toward software-defined vehicles, energy services, and life-cycle guarantees.

Service capability is emerging as a key competitive differentiator in the United States school bus market. High-voltage technician scarcity propels OEMs to offer turnkey maintenance contracts bundled with workforce-training modules. Dealers in rural geographies are investing in mobile repair fleets equipped with battery diagnostics, a feature particularly valued by districts with limited in-house expertise. Financing innovation represents another battleground; subscription-style models that wrap vehicles, chargers, and energy costs under one invoice are gaining traction, positioning capital-heavy investors as de facto competitors to legacy manufacturers.

United States School Bus Industry Leaders

Blue Bird Corporation

Collins Bus Corporation

Navistar Inc. (IC BUS)

Lion Electric Company

Daimler Truck North America LLC (Thomas Built)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Micro Bird launched its G5e electric school bus, boasting a remarkable 200-mile range that sets a new benchmark for Type A buses. This pioneering bus offers an environmentally friendly solution for student transport, merging efficiency with state-of-the-art technology.

- March 2025: Thomas Built Buses has finalized its transition to the Type D model with the introduction of the Saf-T-Liner EFX2. The company has consolidated its production operations at Archdale and integrated advanced safety features into the new model.

- January 2025: Thomas Built Buses unveiled its second-generation Jouley electric bus, marking a significant stride in sustainable transportation. Now featuring Proterra’s state-of-the-art 800-V battery technology and the robust 14Xe eAxle, this revamped Jouley promises an unparalleled driving experience, seamlessly blending sleek design with advanced engineering for eco-conscious travelers.

- October 2024: GreenPower launched four colorful school buses in Arizona, California, and West Virginia. With operations in South Charleston gaining momentum, six more eco-friendly buses are en route to their destinations.

United States School Bus Market Report Scope

By Design Type

| Type A (Cut-away) |

| Type B |

| Type C (Conventional) |

| Type D (Transit-Style) |

By Powertrain Type

| Internal Combustion Engine (IC Engine) |

| Hybrid and Electric |

By Ownership Model

| District-Owned Fleets |

| Contractor-Owned Fleets |

By Seating Capacity

| Less than 30 Seats |

| 30–60 Seats |

| Above 60 Seats |

| By Design Type | Type A (Cut-away) |

| Type B | |

| Type C (Conventional) | |

| Type D (Transit-Style) | |

| By Powertrain Type | Internal Combustion Engine (IC Engine) |

| Hybrid and Electric | |

| By Ownership Model | District-Owned Fleets |

| Contractor-Owned Fleets | |

| By Seating Capacity | Less than 30 Seats |

| 30–60 Seats | |

| Above 60 Seats |

Key Questions Answered in the Report

How big is the United States school bus market in 2026?

The United States School Bus Market size is expected to reach USD 6.25 billion in 2026.

What is driving demand for electric school buses in the United States?

Federal subsidies under the EPA Clean School Bus Program and state zero-emission mandates are sharply lowering acquisition costs while tightening fleet-age and safety rules push districts to replace older diesel models.

Which school bus design holds the largest share today?

Type C (Conventional Buses) lead with 78.05% share and remain popular for their balance of capacity and maneuverability.

Why are rural districts slower to adopt electric buses?

Sparse charging infrastructure and higher upfront costs limit feasibility despite available federal incentives.

Page last updated on: