Europe E-commerce Watch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.53 Billion |

| Market Size (2026) | USD 9.07 Billion |

| Market Size (2031) | USD 12.37 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

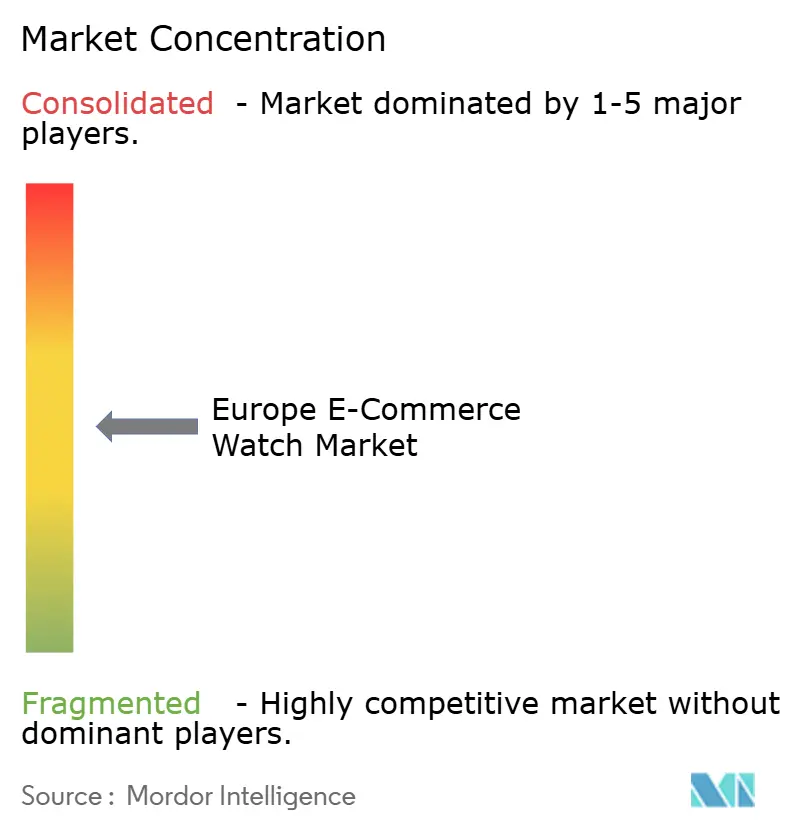

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe E-commerce Watch Market Analysis by Mordor Intelligence

The Europe E-commerce Watch Market size is expected to grow from USD 8.53 billion in 2025 to USD 9.07 billion in 2026 and is forecast to reach USD 12.37 billion by 2031 at 6.39% CAGR over 2026-2031. Strong broadband infrastructure enables seamless online shopping experiences across desktop and mobile platforms, while increased mobile commerce adoption reflects evolving consumer shopping behaviors and digital maturity. Consumer trust in high-value online transactions, particularly for luxury timepieces, continues to drive market growth for both traditional watchmakers and digital-first brands. The integration of advanced health monitoring features in smartwatches, such as heart rate tracking, sleep analysis, stress monitoring, blood oxygen measurement, and detailed fitness metrics, maintains consistent consumer interest and drives adoption. The market's growth is further supported by premium positioning across various price segments, the increasing popularity of gender-neutral design trends in both traditional and smart timepieces, and sustained demand for authenticated pre-owned timepieces from established luxury brands, which appeals to both collectors and value-conscious consumers.

Key Report Takeaways

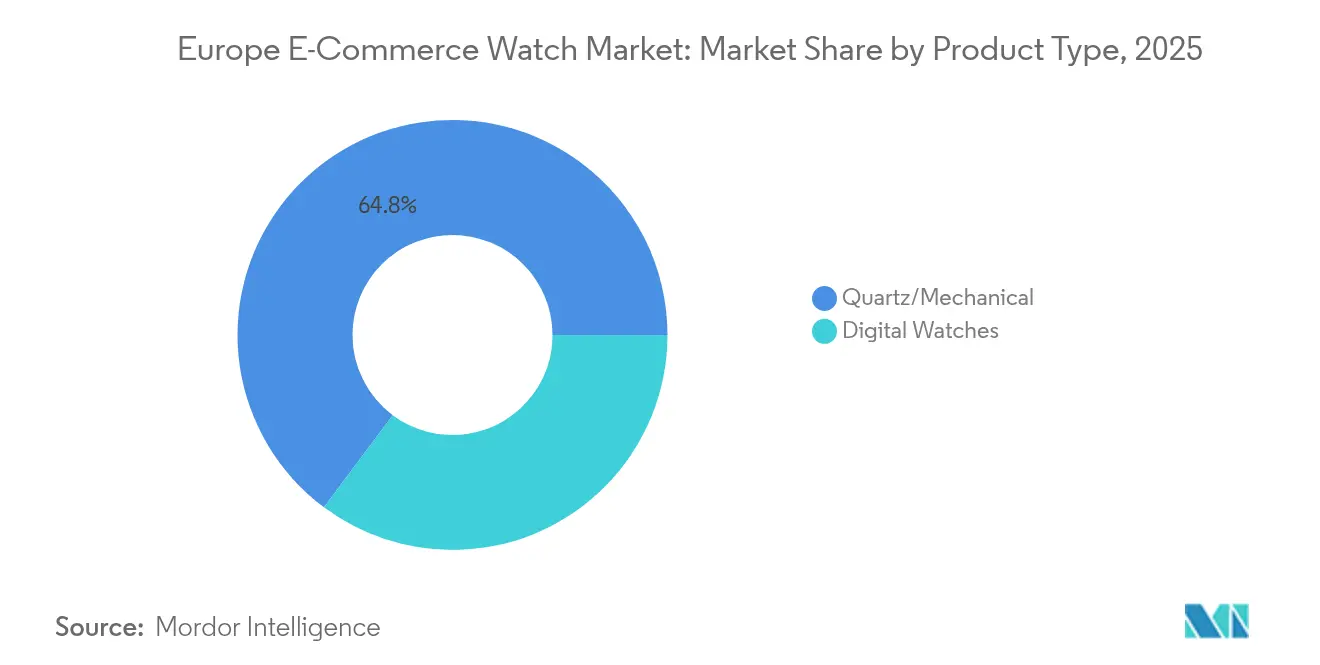

- By product type, quartz/mechanical watches held 64.80% of the European e-commerce watch market share in 2025, while digital watches are set to expand at a 6.75% CAGR to 2031.

- By category, the mass segment accounted for 67.96% share of the European e-commerce watch market size in 2025, while the premium segment is forecast to grow at 7.13% CAGR through 2031.

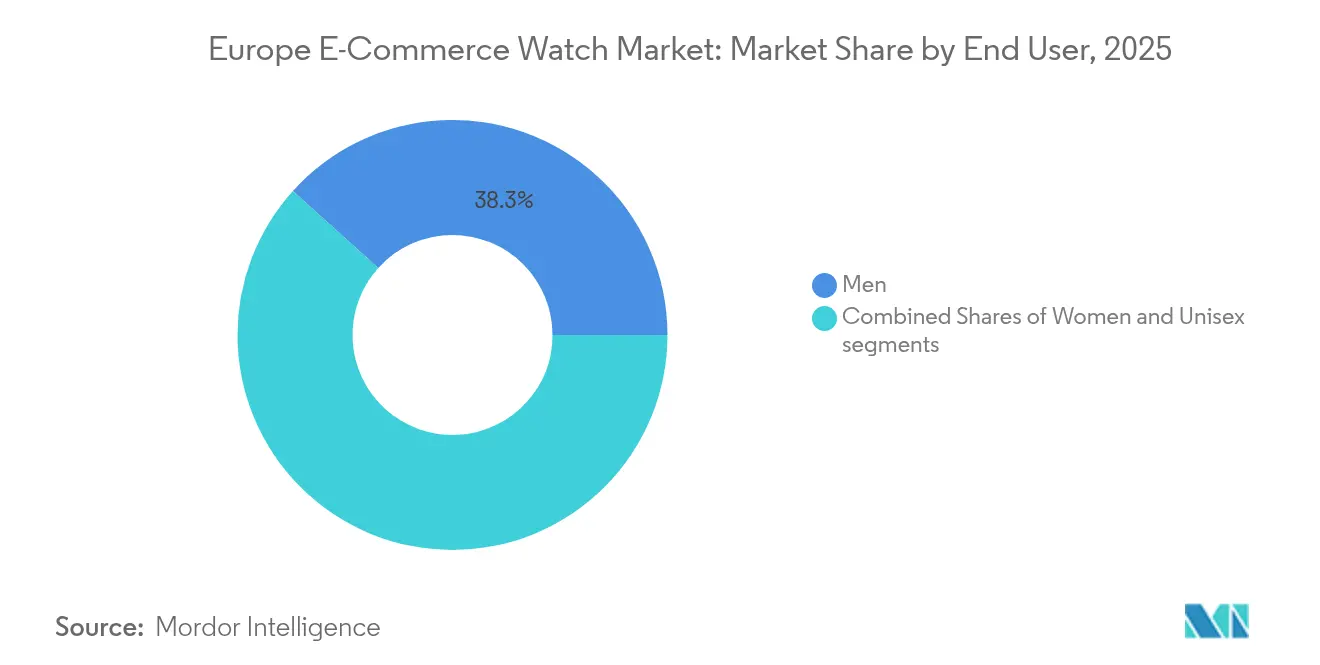

- By end user, men led with 38.31% share in 2025, whereas unisex models are advancing at a 7.48% CAGR during 2026-2031.

- By platform, third-party marketplaces dominated with 81.04% revenue share in 2025 and are pacing ahead at an 8.07% CAGR.

- By geography, the United Kingdom contributed 20.41% market share in 2025, while Spain is poised for an 8.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe E-commerce Watch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible and diverse payment options | +1.2% | Western Europe, Nordic countries | Short term (≤ 2 years) |

| Promotion and discounts enticing consumer to make purchase | +0.8% | Southern Europe, Eastern Europe | Short term (≤ 2 years) |

| Technological advancement | +1.5% | Germany, United Kingdom, Netherlands | Medium term (2-4 years) |

| Growing smartphone and internet penetration | +0.9% | Eastern Europe, Southern Europe | Medium term (2-4 years) |

| Influence of social media platforms and celebrity endorsements | +1.1% | Western Europe, United Kingdom | Short term (≤ 2 years) |

| Rising demand for premium and luxury watches | +1.3% | Western Europe, Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Flexible and Diverse Payment Options

Payment flexibility has become a key factor in sales conversion, with companies like Payabl reporting that 43% of European consumers abandon purchases due to complex checkout processes, limited payment options, and insufficient payment authentication methods [1]Payabl, “The State of European Checkout 2024”, www.payabl.com. PayPal maintains a dominant position with 50% usage across Europe, offering consumers a trusted and secure payment method through its robust fraud protection and buyer protection policies. Mobile payment preferences are transforming European retail, as card payments increase and cash usage decreases across all age groups, driven by the convenience, security, and speed of digital transactions, along with the growing integration of contactless payment technologies. This shift benefits luxury watch e-commerce, where transaction values frequently exceed consumers' single-payment thresholds, necessitating flexible payment solutions such as installment plans, digital wallets, and buy-now-pay-later options that accommodate high-value purchases. The European Payments Initiative's development of unified payment systems aims to reduce cross-border transaction barriers by standardizing payment processes, regulations, and settlement mechanisms, allowing smaller watch retailers to compete with established marketplace platforms in the international market while ensuring compliance with regional payment standards and security protocols.

Technological Advancement

Smartwatch manufacturers are incorporating AI coaching, advanced biosensors, and digital identification features into their devices. The AI coaching functions deliver personalized fitness recommendations, workout guidance, and real-time performance analysis using individual user data and activity patterns. Samsung recorded a 74% increase in unit sales during Q1 2025, demonstrating robust consumer demand for connected wellness devices. Swiss manufacturers are implementing blockchain-based certificates for authenticity verification and secondary market trading. These certificates establish a transparent ownership record and combat counterfeiting in the luxury watch segment, while documenting service history and maintenance records. The addition of advanced health monitoring capabilities, including non-invasive glucose measurement and sleep tracking, has transformed smartwatches from fitness trackers into comprehensive health management tools. Sleep monitoring includes analysis of sleep phases, breathing patterns, heart rate variability, and customized recommendations for sleep quality improvement. These technological developments are driving growth in the market, especially in premium and health-focused segments, as consumers seek devices offering comprehensive health insights and preventive care features.

Influence of Social Media Platforms and Celebrity Endorsements

Social media platforms like Instagram, TikTok, and YouTube have transformed watch enthusiasts into influential content creators who provide comprehensive product reviews, technical specifications, historical context, movement analysis, brand comparisons, and hands-on demonstrations that shape consumer purchasing decisions. Regular engagement between content creators and their followers through comments and live Q&A sessions enhances credibility and perceived expertise in luxury timepieces. Traditional brand ambassadors and celebrity endorsements continue to generate aspirational value and market interest during new product launches, special editions, and limited releases. Video content featuring detailed product unboxings, wrist shots, movement demonstrations, macro photography, strap changes, real-time auction streams, and price trend analysis drives consumers to online marketplaces, increasing transaction velocity and market participation in the European online watch market.

Rising Demand for Premium and Luxury Watches

European consumers view luxury watches as both heirloom pieces and investment assets. According to the Federation of the Swiss Watch Industry, certain watch models were traded at up to 200% of their retail value on authorized platforms in 2024 [2]Federation of the Swiss Watch Industry, “Statistics 2024”, www.fhs.swiss. The pre-owned market, enhanced by secure payment systems, digital authentication certificates, and trusted intermediary services, enables younger professionals to enter the luxury watch market. This accessibility, combined with stringent verification processes and secure transaction mechanisms, helps maintain value stability and market confidence in the European e-commerce watch segment. The digital infrastructure supporting these transactions includes blockchain-based ownership tracking, professional authentication services, and insured shipping options, further strengthening the market's credibility. The integration of advanced verification technologies and secure payment gateways has also reduced counterfeit risks and fraud incidents, making the European pre-owned watch market more reliable for both buyers and sellers. Additionally, the market benefits from established partnerships between authorized dealers, auction houses, and digital platforms, creating a robust ecosystem for luxury watch trading.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit products | -1.4% | National, particularly Eastern Europe | Long term (≥ 4 years) |

| Logistical challenges in fulfillment and delivery | -0.9% | Cross-border Europe, remote regions | Medium term (2-4 years) |

| Competition from brick-and-mortar stores and alternative retail channels | -1.1% | Western Europe, established luxury markets | Medium term (2-4 years) |

| Rising production and operational costs | -0.7% | Manufacturing hubs, supply chain dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of Counterfeit Products

The proliferation of counterfeit watches threatens brand integrity and consumer trust in the watch market. E-commerce platforms face increasing difficulty in maintaining marketplace accessibility while protecting brands, as counterfeiters utilize sophisticated social media marketing and direct-to-consumer distribution channels. The rise in counterfeit trade has led to significant revenue losses for legitimate watch manufacturers and retailers, while also compromising consumer safety through substandard materials and manufacturing processes. In 2024, Chrono24 introduced an authenticity verification program to combat counterfeit products, implementing advanced digital authentication technologies and expert verification processes. However, advanced counterfeiting techniques continue to challenge authentication processes, with counterfeiters adopting high-quality materials and replicating serial numbers. The European Union's Digital Services Act implementation establishes comprehensive regulatory frameworks for online platforms, which may enhance counterfeit identification and removal procedures through mandatory due diligence requirements and improved cooperation between platforms and rights holders.

Competition from Brick-and-Mortar Stores

Traditional retail channels dominate luxury watch sales, especially for high-value purchases where customers prefer physical product interaction and personalized service. Authorized dealers offer comprehensive manufacturer-backed warranties, extensive after-sales support, and authentic brand experiences that online platforms cannot fully replicate. These dealers provide specialized expertise, authentication services, and detailed product knowledge, creating a trusted environment for significant purchases. In December 2023, a EUR 91.6 million fine imposed on Rolex by French authorities for restricting online sales illustrates the complex conflict between maintaining strict brand control and expanding digital distribution channels. Physical stores are evolving into sophisticated experiential spaces that showcase brands through interactive displays, personalized consultations, and immersive brand storytelling while supporting online sales channels. Luxury watch retailers are adopting comprehensive omnichannel approaches that combine digital product discovery with in-store purchases, offering virtual try-ons, detailed product configurations, and seamless inventory access to attract younger consumers while preserving their premium market position.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Quartz/Mechanical Segment Shows Dominance While Digital Innovation Accelerates

The Europe E-commerce Watch Market maintains a 64.80% of revenue in 2025 for quartz and mechanical watches, while projecting a 6.75% CAGR for digital watches through 2031. The market growth stems from connected wearables offering comprehensive health monitoring systems, integrated payment capabilities, and advanced AI-powered features, particularly attracting consumers under 35. Mechanical watches maintain their market position through collectors who value their exceptional longevity, intricate craftsmanship, and investment potential. The digital watch segment is expected to double by 2030, as heritage timepieces sustain their value through limited production numbers, historical significance, and verified authenticity.

The smartwatch segment expands through consistent product updates, technological innovations, and strategic mobile carrier partnerships. European mobile providers enhance adoption by integrating sophisticated payment applications and offering bundled service packages. Traditional watch manufacturers respond by developing hybrid models that combine advanced digital functionality with classical design elements and traditional watchmaking expertise. The certified pre-owned mechanical watch market demonstrates stability through established online platforms and trusted authentication processes, indicating sustained demand and market maturity in the European online watch market.

By Category: Premium Segment Outpaces Mass Market Growth

Mass watches represent 67.96% of the 2025 turnover in the Europe E-commerce Watch Market, while premium watches demonstrate a robust CAGR of 7.13%. Consumer preferences are increasingly shifting toward investing in single high-quality timepieces instead of multiple lower-priced watches, which has significantly increased average transaction values across the market. The segment's sustained growth is driven by carefully controlled annual production volumes, transparent and structured waiting list systems, and exceptional craftsmanship that meets museum-grade standards.

The mass-market segment maintains substantial sales volumes through strategic promotional activities and seasonal discount events, ensuring accessible price points for new customers entering the market. The certified pre-owned market serves as a vital alternative acquisition channel for premium timepieces, substantially reducing waiting times compared to authorized boutiques. The European online market for premium watches continues to expand, benefiting from sophisticated cross-border shipping infrastructure and comprehensive warranty services standardized across European territories.

By End User: Men's Watch Holds Largest Market While Unisex Segment Captures Generational Shift

Men's watches maintain a 38.31% market share while the unisex watch segment is expected to grow at a CAGR of 7.48% through 2031, driven by millennial and Gen Z preferences for flexible sizing options. These demographics increasingly seek timepieces that transcend traditional gender boundaries. Customization features, including interchangeable dials, straps, and modular bracelets, enable personalization beyond traditional gender classifications. The European online watch market has adapted to this trend by implementing advanced search functionality that prioritizes fit measurements over gender-specific categories, allowing consumers to filter watches based on precise lug-to-lug measurements and case dimensions.

Established collector networks, heritage collections, and traditional product lines support the men's watch segment growth. The women's segment shows consistent growth, correlating with increased female representation in executive positions and growing purchasing power. However, unisex watches represent the fastest-growing category, with manufacturers focusing on versatile 36-40 mm case sizes that accommodate diverse wrist measurements. This shift in design philosophy reflects the market's evolution toward size-inclusive offerings that prioritize individual fit preferences over gender-specific categorization in the European e-commerce watch market.

By Platform Type: Third-Party Marketplaces Dominate Digital Commerce

Third-party portals account for 81.04% of online watch sales in 2025 and are projected to maintain an 8.07% CAGR through 2031. These platforms lead the market through their comprehensive product selection, including new and pre-owned timepieces across price segments, robust buyer protection programs with authenticity guarantees and return policies, and integrated financing options with installment payments. The Digital Services Act implementation requires major platforms to verify business sellers through documentation and regular audits, increasing transparency for premium watch buyers in the European market.

Brand-owned storefronts maintain their market position through controlled pricing and brand-focused digital experiences. While marketplaces provide extensive reach, brands face platform commissions and direct price competition from multiple sellers. To address this, brands release products on their websites first before distributing remaining inventory to marketplaces. Platforms like Chrono24 establish their market presence by authenticating timepieces through certified experts, providing digital certificates with ownership history, and offering escrow services. These service enhancements increase customer retention and generate higher transaction values in the market

Geography Analysis

The United Kingdom holds 20.41% of transaction value in the European e-commerce watch market, supported by established logistics networks, high credit-card adoption rates, and significant luxury market presence. London's financial sector maintains strong discretionary spending and attracts international tourists seeking tax-free shopping, contributing to cross-border sales. The dominance of global luxury brands and high consumer trust in online authentication services further boost the United Kingdom's online watch transactions.

Spain projects an 8.45% CAGR through 2031, driven by increasing middle-class wealth, high smartphone penetration, and government support for digital enterprises. According to World Bank data , the GDP per capita increased from USD 27,233.9 in 2020 to USD 35,297 in 2024 in Spain. The integration of virtual try-on technology in Spanish e-commerce platforms improves fit confidence and conversion rates. Generation Z's preference for statement accessories drives premium watch demand in the market. Additionally, collaborations with fashion influencers and local celebrities are helping online platforms tap into younger demographics.

Germany, France, and Italy represent established markets with strong brand recognition. French consumers demonstrate among the highest luxury spending per capita globally. Germany's technical culture supports demand for precision timepieces, while Italian retailers offer specialized collections from independent watchmakers. The Netherlands and Sweden benefit from complete digital integration, with widespread debit card use and efficient parcel delivery systems generating high average order values. Eastern European countries, including Poland, demonstrate double-digit volume growth from smaller bases, benefiting from Europe logistics networks that reduce delivery times. These market characteristics maintain regional growth in the European online watch market.

Competitive Landscape

The European online watch market exhibits moderate competitive intensity, characterized by a fragmented structure. Traditional Swiss manufacturers, such as Rolex, maintain their pricing power through limited production and heritage-focused brand narratives. Technology companies such as Apple and Samsung compete by offering advanced biometric features and integrated ecosystems, which expand the market's consumer base. Online marketplace platforms, particularly in the authenticated luxury resale segment, serve as key intermediaries influencing product discovery and price transparency. The coexistence of legacy craftsmanship and tech-driven innovation highlights the evolving preferences of Europe's diverse watch-buying audience.

Market players demonstrate varied strategic approaches. Rolex reduced production by 2% in 2024 to maintain exclusivity, while Apple focused on developing blood-pressure monitoring capabilities for its 2025 models. Chrono24 implemented blockchain-based authentication certificates to combat counterfeit products. Samsung established partnerships with major European telecommunications providers to integrate its health applications. These initiatives reflect ongoing competition for market presence and customer retention in the European e-commerce watch market.

The market presents several growth opportunities. Gender-neutral watch collections gain popularity among younger consumers, while environmentally conscious features, including recycled materials and carbon-neutral delivery options, attract sustainability-focused customers. Service-based offerings, such as maintenance subscriptions and guaranteed trade-in programs, help strengthen customer relationships. Companies that effectively combine flexible payment options, authentication services, and efficient international shipping position themselves to increase their market share. Brands that proactively adapt to shifting lifestyle trends and ethical consumption values are well-positioned for long-term growth.

Europe E-commerce Watch Industry Leaders

Apple Inc.

Huawei Technologies Co. Ltd.

Fossil Group Inc.

Rolex SA

The Swatch Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Huawei launched HUAWEI WATCH 5, featuring the HUAWEI TruSense System with Multi-sensing X-TAP Technology and Distributed Sensor Module. The system enables health monitoring through fingertip measurements, providing accurate and rapid health data. The watch includes gesture controls with "Double Slide" and "Double Tap" functions for user interaction.

- April 2025: Luminox, the Swiss watchmaker, launched the Navy SEAL 4230 Series. The watch incorporates design elements that reflect the operational requirements of Navy SEALs and special forces units. This updated version of the Luminox Navy SEAL watch emphasizes durability and precision in extreme conditions.

- March 2025: Edinburgh-based UNA Watch secured GBP 300,000 in investment from SFC Capital to develop its modular GPS sports watch. The company plans to use the funding to enhance its product development, expand its team, and accelerate market entry. The modular design allows users to customize their watch features according to their specific athletic needs and preferences.

- February 2025: Amazfit has introduced the Active 2 smartwatch in Europe. The device features a 1.32'' AMOLED display with a round dial protected by 2.5D tempered glass, differing from its predecessor's square design. The Active 2, targeted at athletes and fitness enthusiasts, offers comprehensive features at a price point significantly lower than premium smartwatches.

Europe E-commerce Watch Market Report Scope

A watch is a portable timekeeping device worn on the wrist that is designed to keep track of time and often includes additional features such as a date display, stopwatch functionality, alarms, and sometimes even advanced features like fitness tracking or GPS capabilities. E-commerce watch refers to the online retailing and purchasing of watches through electronic commerce platforms, such as websites or mobile applications.

The North American e-commerce watch market is segmented based on product type, platform type, and geography. Based on product type, the market is segmented as quartz/mechanical and smart. By platform type, the market is segmented into third-party retailers and the company's own website. By geography, the report analyses the major economies of countries in the region like the United Kingdom, Germany, Spain, France, Italy, Russia, and the Rest of Europe.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Quartz/Mechanical | |

| Digital Watch | Smart Watches |

| Other Digital Types |

| Mass |

| Premium |

| Men |

| Women |

| Unisex |

| Third-Party Marketplace |

| Company-Owned Platform |

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Quartz/Mechanical | |

| Digital Watch | Smart Watches | |

| Other Digital Types | ||

| By Category | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| Unisex | ||

| By Platform Type | Third-Party Marketplace | |

| Company-Owned Platform | ||

| By Country | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the size of the European E-commerce watch market in 2026?

The market stands at USD 9.07 billion in 2026.

How fast is the market expected to grow through 2031?

It is projected to expand at a 6.39% CAGR, reaching USD 12.37 billion by 2031.

Which product segment shows the highest growth momentum?

Digital watches, led by smartwatches, are advancing at a 6.75% CAGR to 2031.

Which European country is forecast to grow the fastest?

Spain leads with an expected 8.45% CAGR over the forecast period.

Page last updated on: