Market Overview

| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

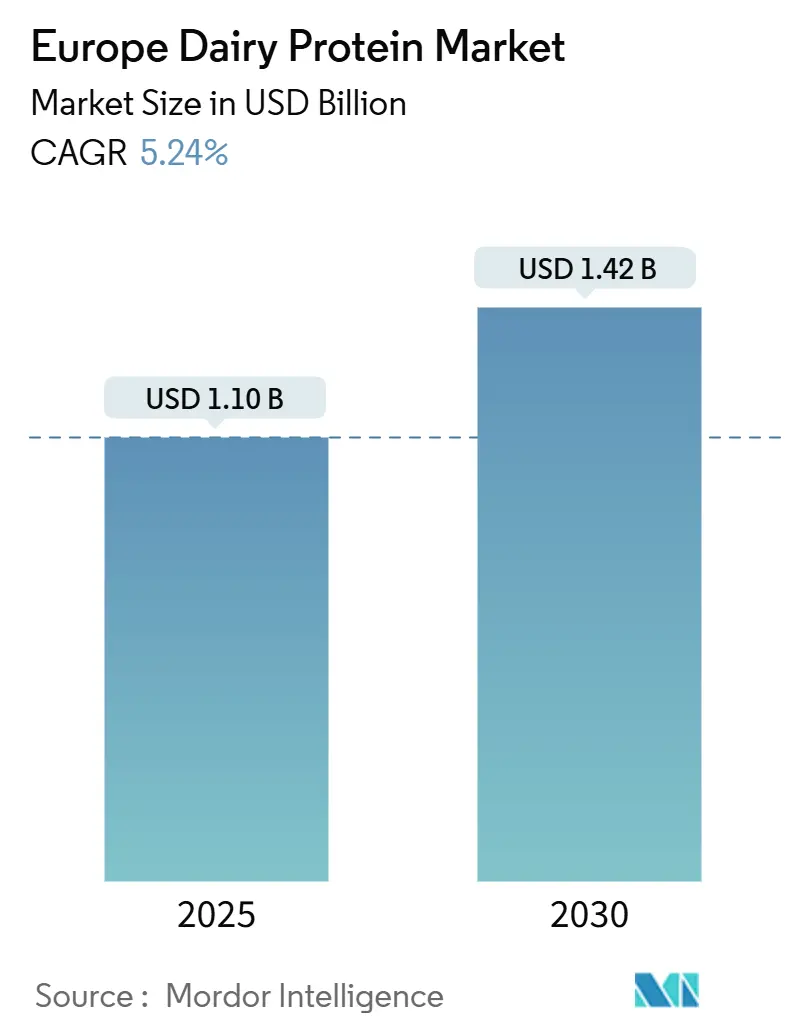

| Market Size (2025) | USD 1.10 Billion |

| Market Size (2030) | USD 1.42 Billion |

| Growth Rate (2025 - 2030) | 5.24% CAGR |

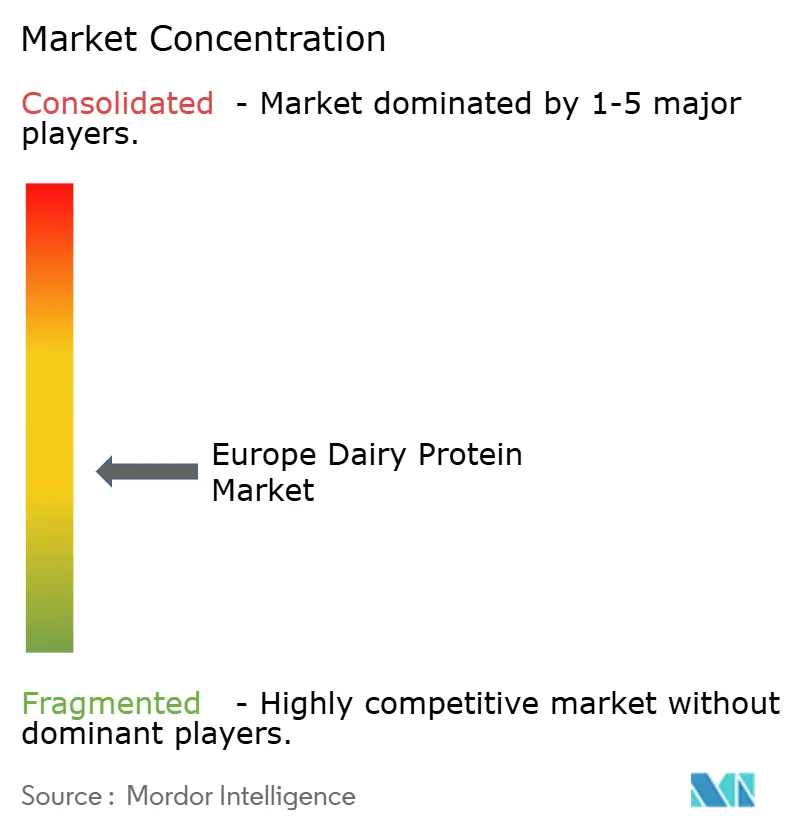

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Dairy Protein Market Analysis by Mordor Intelligence

The European Dairy Protein Market is valued at USD 1.10 billion in 2025 and is projected to reach USD 1.42 billion by 2030, registering a CAGR of 5.24% during the forecast period (2025-2030). The rising adoption of high-protein diets among the aging population and increasing demand for functional and sports nutrition products are driving the European dairy protein market. The market's expansion is supported by the growing middle-class population and increased consumption of health drinks and protein-based diets. The European dairy industry maintains a strong position in meeting consumer demands for clean labels and convenience in production, while adapting to sustainability initiatives through hybrid formulations that combine dairy and plant proteins. However, the market faces challenges from the growing popularity of plant-based alternatives and increasing instances of lactose intolerance. The industry's response to these challenges includes investment in research and development to improve protein digestibility and reduce allergenicity in dairy products. Additionally, manufacturers are focusing on innovative processing technologies to enhance the functional properties of dairy proteins, making them more suitable for various food applications. European dairy protein producers are also emphasizing transparency in their supply chains and implementing sustainable practices to maintain consumer trust and market competitiveness. Despite the challenges, the market is expected to maintain its growth trajectory, driven by continuous innovation, increasing health consciousness among consumers, and the adaptability of manufacturers to evolving market demands.

Key Report Takeaways

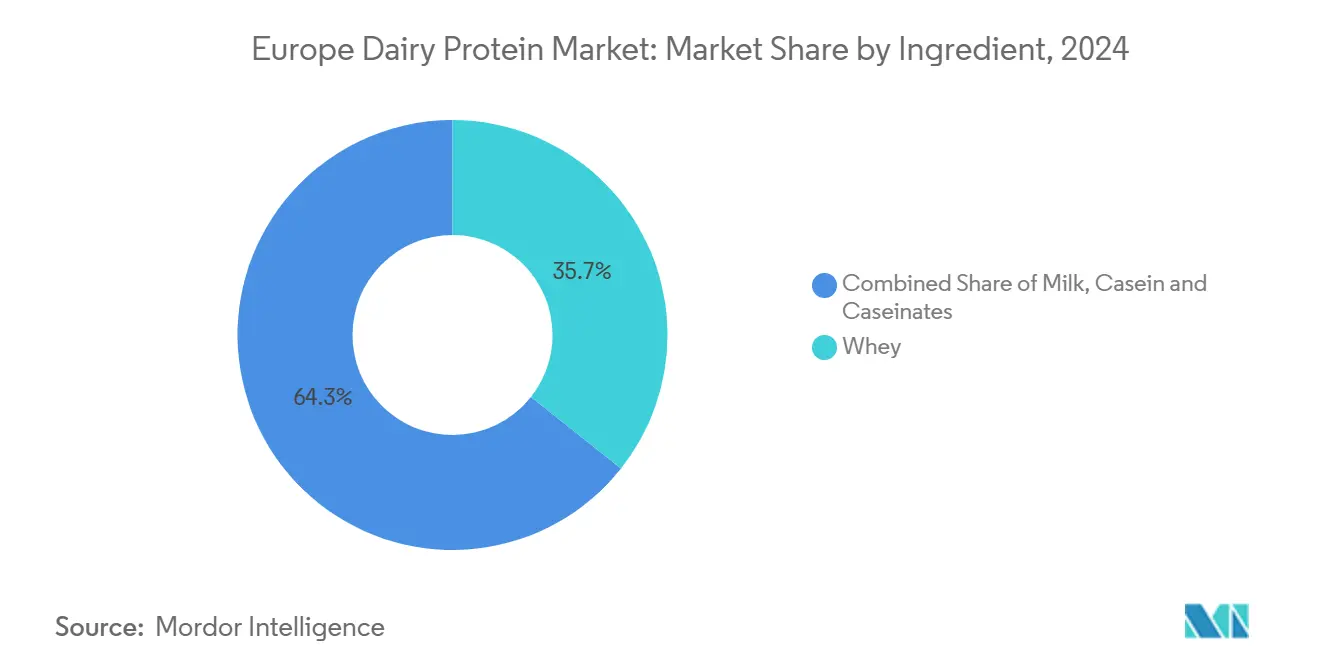

- By ingredient, whey protein concentrates held 35.66% of the European dairy protein market share in 2024; milk protein isolates are projected to expand at a 8.23% CAGR through 2030.

- By form, powder format captured 79% of the European dairy protein market size in 2024, whereas liquid (RTD) offerings are growing at a 10.40% CAGR to 2030.

- By nature, the conventional segment commanded 93% of the market in 2024; while the organic segment is advancing at an 11.26% CAGR between 2025-2030.

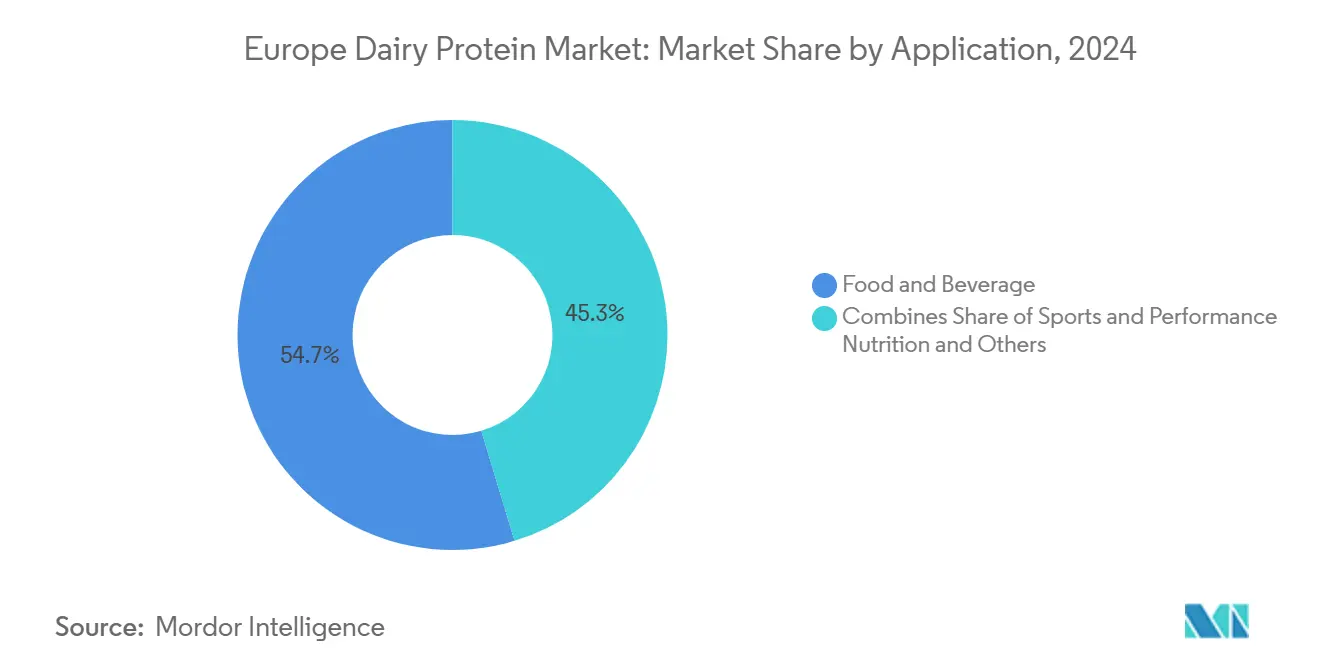

- By application, food and beverage accounted for 54.66% share in 2024, while sports and performance nutrition leads future growth at a 9.13% CAGR.

- By geography, Germany led with 25% of the European dairy protein market share in 2024, and Spain records the fastest projected CAGR of 7.20% to 2030

Europe Dairy Protein Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising adoption of high-protein diets among aging europeans | +1.8% | Germany, UK, France, Italy | Medium term (2-4 years) |

| Clean-label demand in infant and clinical nutrition | +1.2% | Germany, France, UK, Netherlands | Medium term (2-4 years) |

| Growth of hybrid (plant-dairy) formulations driving protein innovation | +0.9% | Germany, Netherlands, UK, France | Long term (≥4 years) |

| Rising demand for functional and sports nutrition | +1.5% | Spain, UK, Germany, Italy | Short term (≤2 years) |

| Technological advancements in protein processing | +1.1% | Germany, Netherlands, Denmark, France | Medium term (2-4 years) |

| Sustainable production practices supporting market growth | +0.8% | EU-wide, stronger in Nordics and Germany | Long term (≥4 years) |

Source: Mordor Intelligence

Rising adoption of high-protein diets among aging europeans

The aging demographic trend in Europe is a significant driver of dairy protein market expansion. Research demonstrates that elderly individuals have increased protein requirements, with the European Food Safety Authority (EFSA) establishing a Population Reference Intake (PRI) of 0.83 g protein/kg body weight per day. The PROT-AGE Study Group, supported by the European Union Geriatric Medicine Society, recommends even higher protein consumption: 1.0-1.2 g per kilogram daily for individuals over 65, and 1.2-1.5 g/kg for those with existing health conditions. According to recent Eurostat data from January 2024, the EU population stands at 449.3 million, with more than one-fifth being 65 years or older[1]Source: Eurostat, "Population Structure and Ageing," ec.europa.eu. The European Commission has identified sedentary elderly populations as particularly vulnerable to protein deficiency, creating substantial opportunities for protein-fortified dairy products. This demographic shift has prompted dairy manufacturers to develop specialized product lines targeting older consumers' nutritional needs. The increasing awareness of protein's role in maintaining muscle mass and preventing sarcopenia in older adults has further stimulated market growth.

Clean-label demand in infant and clinical nutrition

Clean-label dairy proteins are experiencing increasing demand in the European market, particularly in infant nutrition products. Parents seek products with simple, recognizable ingredients, prompting manufacturers to reformulate with clean-label dairy proteins. The trend also influences clinical nutrition products, where healthcare providers and patients prefer transparent ingredient declarations and natural protein components. The European Commission's regulations on infant formula composition provide specific guidelines for ingredients and additives. With 3.67 million babies born in the European Union in 2023, according to Europe's Fertility Statistics, this substantial infant population drives demand for natural, minimally processed dairy protein ingredients in baby formula and infant nutrition products[2]Source: European Commission, "Fertility Statistics", ec.europa.eu. Manufacturers are responding to this demand by investing in research and development to create innovative dairy protein formulations that meet both regulatory requirements and consumer preferences for clean-label products. Additionally, the growing awareness of the nutritional benefits of dairy proteins continues to support the expansion of the clean-label dairy protein market in infant nutrition.

Growth of hybrid (plant-dairy) formulations

Hybrid formulations that combine dairy and plant proteins allow dairy manufacturers to embrace sustainability trends while utilizing their established production capabilities. Kerry Group's Smug hybrid range, introduced in July 2024, features blended dairy products that deliver reduced saturated fat content and lower CO2 emissions[3]Source: Kerry Group, “Kerry Group Half Year Results 2024,” kerrygroup.com. These innovative hybrid products appeal to health-conscious consumers and address the declining dairy consumption trends in Europe. The products enable dairy companies to engage with younger demographics while delivering the functional benefits and familiar taste profiles that purely plant-based alternatives struggle to achieve. The hybrid approach represents a strategic middle ground, allowing companies to maintain their dairy heritage while adapting to evolving consumer preferences.

Rising demand for functional and sports nutrition

Increasing consumer focus on functional and sports nutrition products is driving significant growth in the European dairy protein market. The rising health consciousness among Europeans, coupled with a growing fitness culture, has led to higher consumption of protein-rich supplements and functional foods. Athletes, fitness enthusiasts, and health-conscious individuals are incorporating dairy protein products into their daily routines for muscle recovery and maintenance. The market is further strengthened by the expanding demographic of active aging populations seeking protein-rich nutrition, as well as the superior digestibility and complete amino acid profile of dairy proteins. In response to this market demand, FrieslandCampina Ingredients launched Nutri Whey ProHeat in March 2025, specifically designed to meet the performance and active nutrition market needs. This trend is particularly evident in major European markets such as Germany, the UK, and France, where sports participation and gym memberships continue to rise.

Restraints Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing popularity of plant-based and vegan alternative proteins | -1.3% | Germany, UK, Netherlands, Sweden | Long term (≥4 years) |

| Rising lactose intolerance and allergies | -0.8% | Southern Europe, UK, Germany | Medium term (2-4 years) |

| Price fluctuations and raw material volatility | -0.7% | EU-wide, higher in Germany and France | Short term (≤2 years) |

| Supply chain disruptions impact european dairy protein market | -1.0% | EU-wide, particularly Eastern Europe | Short term (≤2 years) |

Source: Mordor Intelligence

Growing popularity of plant-based and vegan alternative proteins

The shift toward plant-based and vegan protein alternatives presents a significant challenge to the dairy protein market. Consumer adoption of vegan and flexitarian diets, especially among younger demographics, has reduced the demand for traditional dairy proteins. This transition is driven by environmental sustainability concerns, animal welfare considerations, and the perceived health advantages of plant-based options. Food manufacturers have responded by developing protein alternatives from soy, pea, and other plant sources. Improvements in plant protein processing technology have enhanced the taste and texture of these alternatives. The increased retail availability and competitive pricing of plant-based proteins create additional pressure on traditional dairy protein products in the European market. This market shift represents a significant restraint for dairy protein manufacturers, requiring them to adapt their strategies to maintain their market position.

Price fluctuations and raw material volatility

Price volatility in the European dairy protein market continues to escalate, driven by supply shortages in whey protein concentrates and isolates. The Euro's appreciation has diminished profit margins for European dairy producers, affecting their global market position. According to USDA there was a significant dairy herd reductions in France, Germany, the Netherlands, and Belgium during 2024, primarily due to elevated input costs, drought conditions, and bluetongue virus outbreaks. Price volatility has created challenges for manufacturers who face uncertain cost structures while maintaining product quality and meeting delivery obligations. The situation is further complicated by China's anti-subsidy investigation into European Union dairy exports, which could disrupt established trade patterns. Price instability has compelled manufacturers to diversify their sourcing strategies and enhance production efficiency. Additionally, market participants have increased their emphasis on long-term contract negotiations and risk management approaches.

Segment Analysis

By Ingredient: Whey Dominates While Milk Isolates Surge

Whey Protein Concentrates maintain the largest market share at 35.66% in 2024. This dominance stems from their versatility in food applications and cost-effectiveness compared to isolates. The segment's position is strengthened by its integration with cheese production, providing operational efficiencies for dairy processors. Milk Protein Isolates represent the fastest-growing segment with a projected CAGR of 8.23% (2025-2030). This growth is attributed to their superior amino acid profile and functional properties in premium applications. Improvements in filtration and separation technologies have enhanced product quality while reducing production costs for high-purity isolates.

The Casein and Caseinates segment maintains significant market presence, particularly in cheese analogues and processed foods, though with slower growth than whey and milk protein segments. Hydrolyzed proteins are increasing in demand across categories, particularly in clinical nutrition and infant formula applications, due to their enhanced digestibility and reduced allergenicity. The market for hydrolyzed proteins benefits from increasing consumer awareness about protein absorption rates and digestive health. Manufacturers are responding to this trend by expanding their hydrolyzed protein product portfolios and investing in research and development to improve production processes.

Note: Segment Shares of all individual segments will be available upon report purchase

By Form: Powder Versatility Meets Liquid Convenience

Powder formats account for 79.00% of the European dairy protein market in 2024. This dominance is attributed to their longer shelf life, efficient transportation, and versatile applications. The powder segment maintains its market leadership through cost-effective formulation processes and accurate protein concentration control in end products. The Liquid (RTD) segment is expected to grow at a CAGR of 10.40% during 2025-2030, emerging as the fastest-growing format. This growth is driven by increasing consumer demand for convenient, ready-to-consume products, particularly in sports nutrition and functional beverages.

Manufacturers are implementing advanced technologies to overcome protein stability challenges in liquid formats. These innovations enable the production of ready-to-drink beverages with enhanced texture and reduced viscosity at neutral pH. The technological advancements address traditional formulation constraints in ready-to-drink applications, supporting the liquid segment's growth. As technology continues to evolve, liquid formats are gradually expanding their market presence alongside traditional powder formats.

By Nature: Organic Growth Outpaces Conventional Base

The conventional segment holds 93.00% of the European dairy protein market in 2024, supported by established supply chains and cost-effective traditional dairy production methods. This segment maintains its position through economies of scale and efficient processing technologies that ensure consistent quality at competitive prices. The organic segment, while smaller, is growing at a CAGR of 11.26% (2025-2030), exceeding the market's overall growth rate. This expansion stems from heightened consumer focus on environmental sustainability, animal welfare, and organic products' health advantages.

The organic segment maintains strong growth momentum despite challenges from higher prices and inflationary pressures on consumer purchasing power. Research demonstrates that organic milk contains higher concentrations of beneficial fatty acids and antioxidants compared to conventional milk, supporting the premium pricing of organic dairy proteins. The EU's robust regulatory framework for organic agriculture, combined with these documented quality differences, provides a strong foundation for the organic segment's continued expansion.

By Application: Food and Beverage Base Supports Sports Nutrition Growth

The food and beverage segment holds 54.66% market share in 2024, leading the European dairy protein market. Dairy products and desserts represent the largest sub-segment, where dairy proteins serve functional and nutritional purposes. The bakery and confectionery sector incorporates dairy proteins to enhance texture, extend shelf life, and increase nutritional value. The beverage category, particularly protein-enriched milk and yogurt drinks, exhibits significant growth as manufacturers respond to consumer demand for convenient protein delivery formats.

Sports and performance nutrition is projected to grow at a CAGR of 9.13% during 2025-2030, driven by increasing consumer awareness of protein's role in muscle recovery and athletic performance. The segment's growth reflects improvements in protein quality and absorption efficiency, as manufacturers develop specialized dairy protein ingredients for sports nutrition products. The market has diversified beyond protein powders to include ready-to-drink options and protein-enhanced hydration products combining electrolytes with dairy proteins.

In September 2024, Arla Foods launched the 'Go High in Protein' campaign to support dairy manufacturers in developing high-protein products. The campaign features the Arla Foods Ingredients Nutrilac® ProteinBoost range of patented microparticulated whey proteins, containing essential amino acids. This initiative addresses technical challenges in creating high-protein dairy products while maintaining taste and texture quality.

Note: Segment Shares of all individual segments will be available upon report purchase

Geography Analysis

Germany maintains its position as the largest market for dairy proteins in Europe with a 25% share in 2024, leveraging its robust dairy processing infrastructure and strong domestic demand for protein-enriched products. The country's leadership stems from investments in processing technology and an established distribution network that connects producers with domestic and export markets. The German market demonstrates high innovation in specialized protein ingredients for clinical nutrition and sports applications, supported by its food technology research capabilities.

Spain is emerging as the fastest-growing market with a projected CAGR of 7.20% (2025-2030), driven by increasing consumer awareness of protein's health benefits and the expansion of the sports nutrition segment. The Spanish market benefits from rising health consciousness and the growing adoption of high-protein diets for weight management and active lifestyles. Local production capacity investments and expanded distribution channels for specialized protein products support this growth.

The United Kingdom and France represent substantial markets with diverse application profiles, with the UK focusing on sports nutrition and France specializing in infant formula and clinical nutrition applications. Italy integrates dairy proteins into traditional food products, while the Netherlands and Belgium function as processing and distribution hubs for the European market. Russia shows growth potential in conventional dairy proteins, despite regulatory and geopolitical market access challenges. These regional variations reflect different consumer preferences, regulatory environments, and industrial capabilities across Europe.

Competitive Landscape

The European dairy protein market exhibits moderate fragmentation, with mid-sized cooperatives and multinational corporations like Agrial Group, Arla Foods Amba, Kerry Group Plc, and Glanbia Plc holding significant market positions. These companies are implementing vertical integration strategies to secure raw material supply while developing specialized products for high-growth application segments.

Market participants are investing in proprietary processing technologies to enhance product differentiation, particularly in areas of heat stability, solubility, and sensory attributes. This focus on technological advancement is exemplified by FrieslandCampina's March 2024 announcement of a EUR 30 million investment in its German production facilities, aimed at developing innovative dairy protein products and implementing sustainable manufacturing processes.

The market presents opportunities in hybrid protein formulations that combine dairy and plant sources, as well as specialized ingredients for the clinical nutrition segment. Industry consolidation continues as companies seek economies of scale and broader geographic presence to address margin pressures. Technological capabilities have become a crucial factor in maintaining competitive advantage in this evolving market landscape.

Europe Dairy Protein Industry Leaders

-

Glanbia plc

-

Agrial Group

-

Arla Foods Amba

-

FrieslandCampina Ingredients

-

Kerry Group Plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Fonterra launched MyNZMP Link, a digital sales platform that provides 24-hour access to dairy ingredients for European buyers. The e-commerce platform allows European ingredient buyers to purchase whey protein concentrate and lactose directly from the company's regional warehouses.

- March 2025: Verley launched three animal-free whey protein powders: FermWhey Native for sports nutrition, FermWhey MicroStab for beverages and dairy, and FermWhey Gel for dairy and cheese products.

- November 2024: Arla Foods Ingredients developed Lacprodan DI-3092, a whey protein hydrolysate containing 10g of protein per 100ml, compared to the standard 6-7g in similar products, for use in peptide-based medical nutrition applications.

- November 2024: Arla Foods Ingredients acquired Volac's Whey Nutrition business, which provided the company with additional whey supply capacity to address increasing market demand.

Europe Dairy Protein Market Report Scope

The European dairy protein market has been segmented based on ingredient, form, nature, application, and Geography. The market is segmented based on ingredient into milk and whey. They are further divided into isolates, concentrates, and hydrolyzed. By form, the market is segmented into powder and liquid. By nature, it is divided into conventional and organic. By application, the market is segmented into food & beverage (bakery & confectionery, dairy products & desserts, and beverages), sports & performance nutrition, infant & early-life nutrition, and other applications. Also, the study provides an analysis of the dairy protein market in the emerging and established markets across the region, including Germany, the United Kingdom, France, Spain, Italy, Belgium, the Netherlands, Russia, and the Rest of Europe. The market sizing has been done in value terms in USD for all the abovementioned segments.

| By Ingredient | Milk | Isolate | |

| Concentrates | |||

| Hydrolyzed | |||

| Whey | Concentrates | ||

| Isolates | |||

| Hydrolyzed | |||

| Casein and Caseinates | |||

| By Form | Powder | ||

| Liquid | |||

| By Nature | Conventional | ||

| Organic | |||

| By Application | Food and Beverage | Bakery and Confectionery | |

| Dairy Products and Desserts | |||

| Beverages | |||

| Sports and Performance Nutrition | |||

| Infant and Early-Life Nutrition | |||

| Elderly Nutrition and Medical Nutrition | |||

| Other Applications | |||

| Geography | Germany | ||

| France | |||

| United Kingdom | |||

| Spain | |||

| Netherlands | |||

| Italy | |||

| Sweden | |||

| Poland | |||

| Belgium | |||

| Rest of Europe | |||

By Ingredient

| Milk | Isolate |

| Concentrates | |

| Hydrolyzed | |

| Whey | Concentrates |

| Isolates | |

| Hydrolyzed | |

| Casein and Caseinates |

By Form

| Powder |

| Liquid |

By Nature

| Conventional |

| Organic |

By Application

| Food and Beverage | Bakery and Confectionery |

| Dairy Products and Desserts | |

| Beverages | |

| Sports and Performance Nutrition | |

| Infant and Early-Life Nutrition | |

| Elderly Nutrition and Medical Nutrition | |

| Other Applications |

Geography

| Germany |

| France |

| United Kingdom |

| Spain |

| Netherlands |

| Italy |

| Sweden |

| Poland |

| Belgium |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current Europe dairy protein market size and how fast is it growing?

The Europe dairy protein is valued at USD 1.10 billion in 2025 and is forecast to reach USD 1.42 billion by 2030, advancing at a 5.24% CAGR.

Which country leads the Europe dairy protein market in revenue?

Germany contributes 25.00% of the total revenue in 2024. The country's strong industrial base and technological advancement drive significant market growth.

Why are Liquid (RTD) gaining share in Europe dairy protein form?

The liquid (Ready-to-Drink) segment is expected to grow at a CAGR of 10.40%, driven by increasing consumer demand for convenient, ready-to-consume products.

Which Ingredient type is expected to grow at a fastest CAGR?

Milk Protein Isolates is expected to grow at a CAGR of 8.23% for the forecast period.

Page last updated on: June 20, 2025