Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

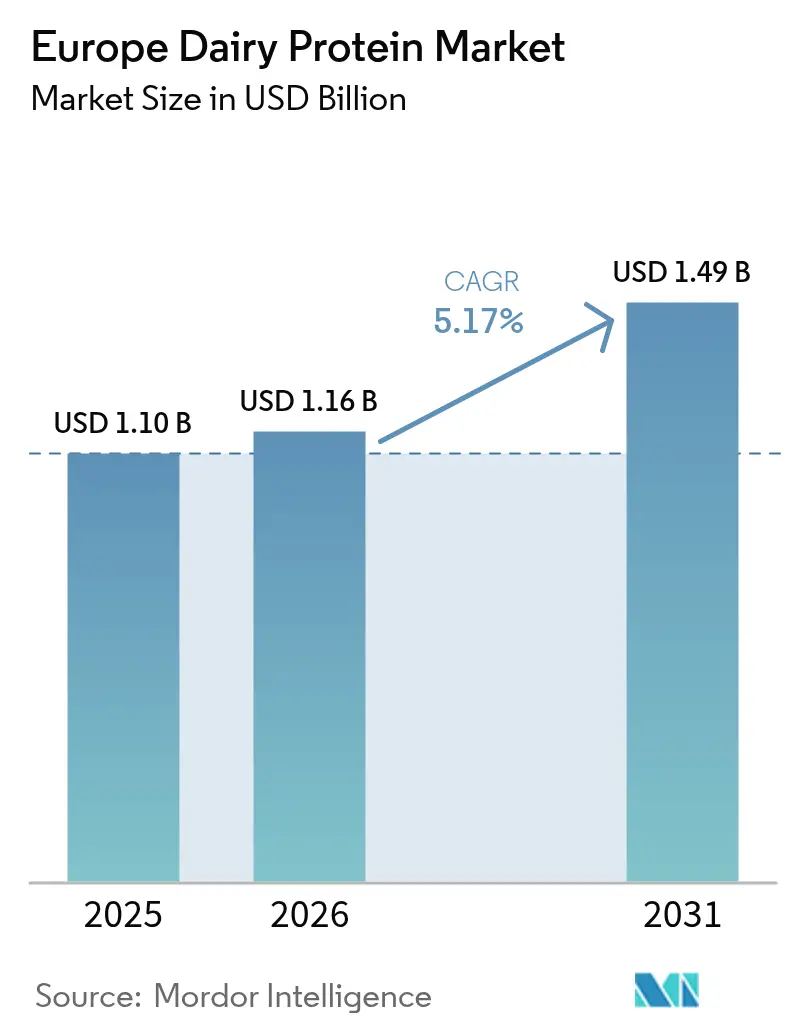

| Base Year Market Size (2025) | USD 1.10 Billion |

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

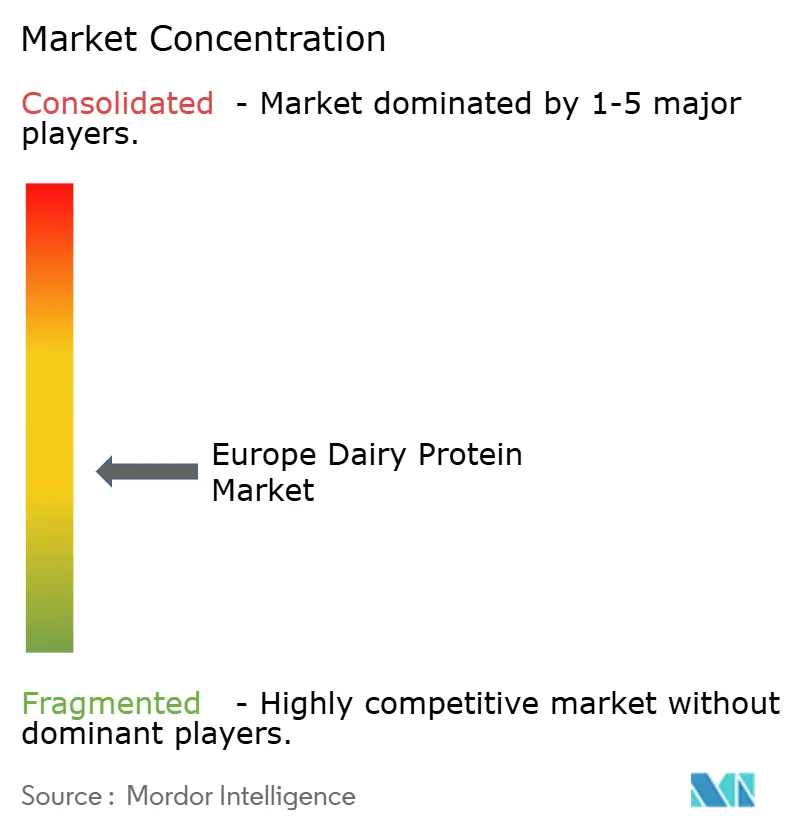

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Dairy Protein Market Analysis by Mordor Intelligence

The European Dairy Protein Market size was valued at USD 1.10 billion in 2025 and estimated to grow from USD 1.16 billion in 2026 to reach USD 1.49 billion by 2031, at a CAGR of 5.17% during the forecast period (2026-2031). The market's expansion is supported by the growing middle-class population and increased consumption of health drinks and protein-based diets. The European dairy industry maintains a strong position in meeting consumer demands for clean labels and convenience in production, while adapting to sustainability initiatives through hybrid formulations that combine dairy and plant proteins. However, the market faces challenges from the growing popularity of plant-based alternatives and increasing instances of lactose intolerance. The industry's response to these challenges includes investment in research and development to improve protein digestibility and reduce allergenicity in dairy products. Additionally, manufacturers are focusing on innovative processing technologies to enhance the functional properties of dairy proteins, making them more suitable for various food applications. European dairy protein producers are also emphasizing transparency in their supply chains and implementing sustainable practices to maintain consumer trust and market competitiveness. Despite the challenges, the market is expected to maintain its growth trajectory, driven by continuous innovation, increasing health consciousness among consumers, and the adaptability of manufacturers to evolving market demands.

Key Report Takeaways

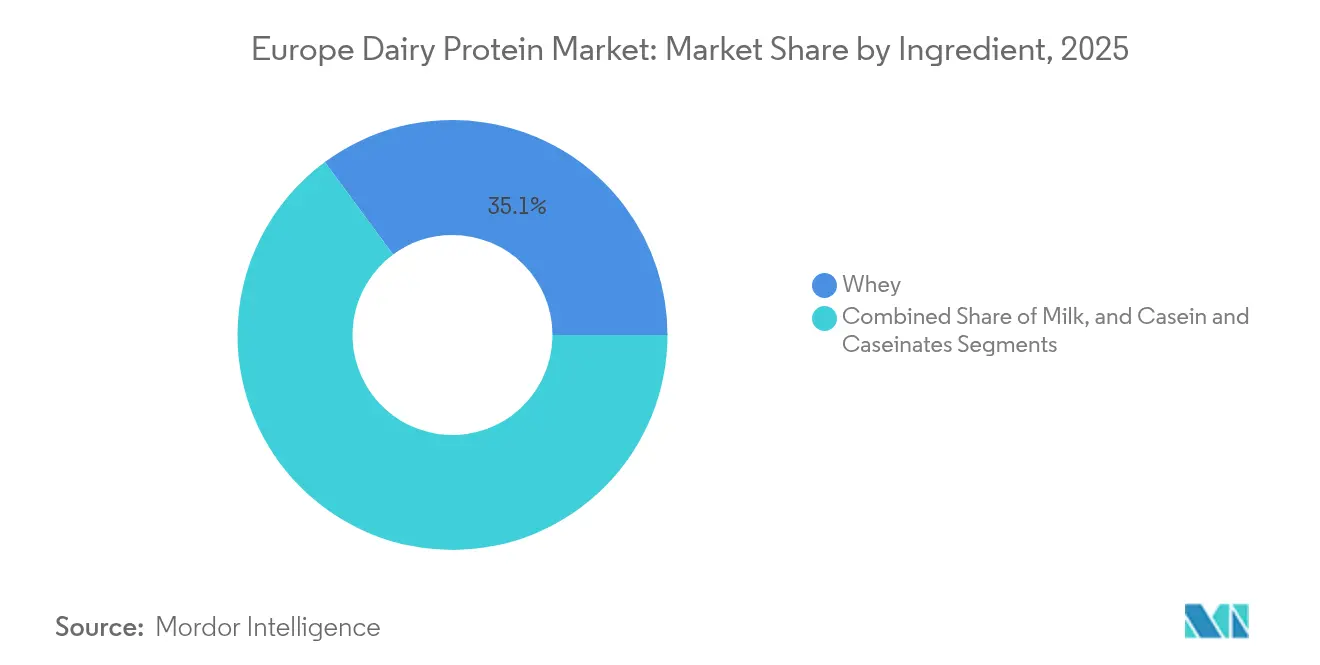

- By ingredient, whey protein concentrates held 35.12% of the European dairy protein market share in 2025; milk protein isolates are projected to expand at a 8.12% CAGR through 2031.

- By form, powder format captured 78.35% of the European dairy protein market size in 2025, whereas liquid (RTD) offerings are growing at a 9.95% CAGR to 2031.

- By nature, the conventional segment commanded 92.45% of the market in 2025; while the organic segment is advancing at an 10.72% CAGR between 2026-2031.

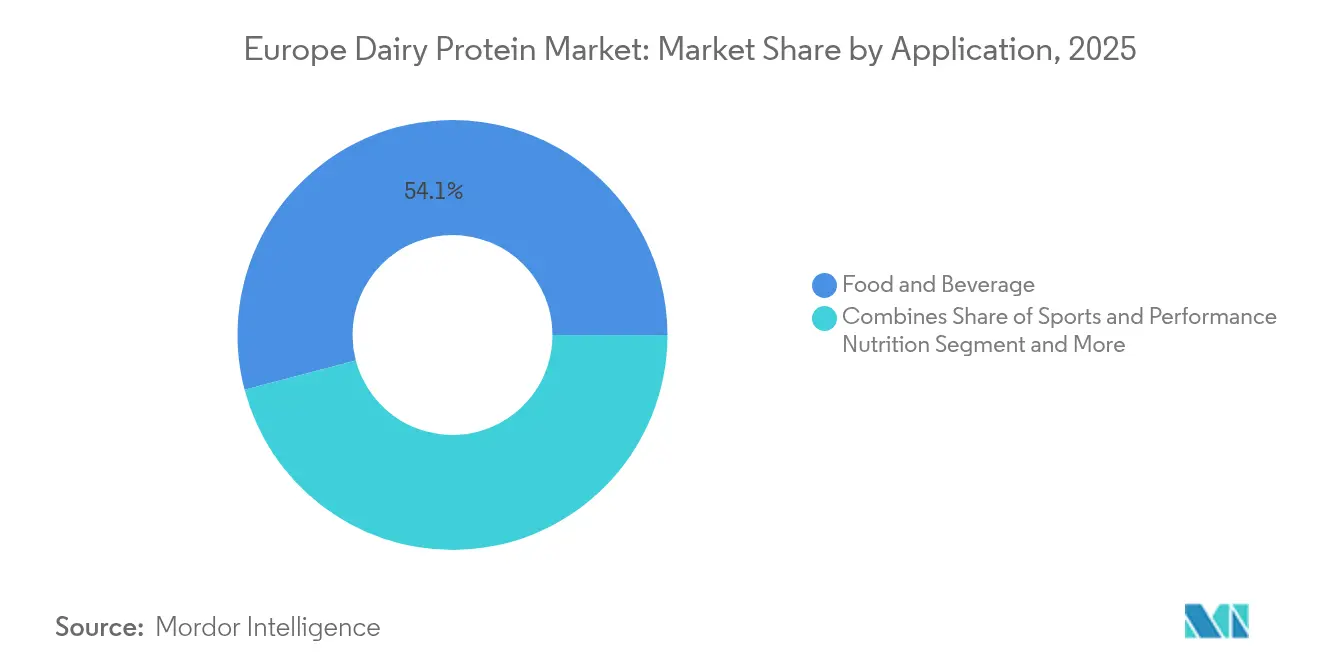

- By application, food and beverage accounted for 54.10% share in 2025, while sports and performance nutrition leads future growth at a 8.78% CAGR.

- By geography, Germany led with 24.65% of the European dairy protein market share in 2025, and Spain records the fastest projected CAGR of 6.93% to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Dairy Protein Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising adoption of high-protein diets among aging europeans | +1.8% | Germany, UK, France, Italy | Medium term (2-4 years) |

| Clean-label demand in infant and clinical nutrition | +1.2% | Germany, France, UK, Netherlands | Medium term (2-4 years) |

| Growth of hybrid (plant-dairy) formulations driving protein innovation | +0.9% | Germany, Netherlands, UK, France | Long term (≥4 years) |

| Rising demand for functional and sports nutrition | +1.5% | Spain, UK, Germany, Italy | Short term (≤2 years) |

| Technological advancements in protein processing | +1.1% | Germany, Netherlands, Denmark, France | Medium term (2-4 years) |

| Sustainable production practices supporting market growth | +0.8% | EU-wide, stronger in Nordics and Germany | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of high-protein diets among aging europeans

The aging demographic trend in Europe is a significant driver of dairy protein market expansion. Research demonstrates that elderly individuals have increased protein requirements, with the European Food Safety Authority (EFSA) establishing a Population Reference Intake (PRI) of 0.83 g protein/kg body weight per day. The PROT-AGE Study Group, supported by the European Union Geriatric Medicine Society, recommends even higher protein consumption: 1.0-1.2 g per kilogram daily for individuals over 65, and 1.2-1.5 g/kg for those with existing health conditions. According to recent Eurostat data from January 2024, the EU population stands at 449.3 million, with more than one-fifth being 65 years or older[1]Source: Eurostat, "Population Structure and Ageing," ec.europa.eu. The European Commission has identified sedentary elderly populations as particularly vulnerable to protein deficiency, creating substantial opportunities for protein-fortified dairy products. This demographic shift has prompted dairy manufacturers to develop specialized product lines targeting older consumers' nutritional needs. The increasing awareness of protein's role in maintaining muscle mass and preventing sarcopenia in older adults has further stimulated market growth.

Clean-label demand in infant and clinical nutrition

Clean-label dairy proteins are experiencing increasing demand in the European market, particularly in infant nutrition products. Parents seek products with simple, recognizable ingredients, prompting manufacturers to reformulate with clean-label dairy proteins. The trend also influences clinical nutrition products, where healthcare providers and patients prefer transparent ingredient declarations and natural protein components. The European Commission's regulations on infant formula composition provide specific guidelines for ingredients and additives. With 3.67 million babies born in the European Union in 2023, according to Europe's Fertility Statistics, this substantial infant population drives demand for natural, minimally processed dairy protein ingredients in baby formula and infant nutrition products[2]Source: European Commission, "Fertility Statistics", ec.europa.eu. Manufacturers are responding to this demand by investing in research and development to create innovative dairy protein formulations that meet both regulatory requirements and consumer preferences for clean-label products. Additionally, the growing awareness of the nutritional benefits of dairy proteins continues to support the expansion of the clean-label dairy protein market in infant nutrition.

Growth of hybrid (plant-dairy) formulations

Hybrid formulations that combine dairy and plant proteins allow dairy manufacturers to embrace sustainability trends while utilizing their established production capabilities. Kerry Group's Smug hybrid range, introduced in July 2024, features blended dairy products that deliver reduced saturated fat content and lower CO2 emissions[3]Source: Kerry Group, “Kerry Group Half Year Results 2024,” kerrygroup.com. These innovative hybrid products appeal to health-conscious consumers and address the declining dairy consumption trends in Europe. The products enable dairy companies to engage with younger demographics while delivering the functional benefits and familiar taste profiles that purely plant-based alternatives struggle to achieve. The hybrid approach represents a strategic middle ground, allowing companies to maintain their dairy heritage while adapting to evolving consumer preferences.

Rising demand for functional and sports nutrition

Increasing consumer focus on functional and sports nutrition products is driving significant growth in the European dairy protein market. The rising health consciousness among Europeans, coupled with a growing fitness culture, has led to higher consumption of protein-rich supplements and functional foods. Athletes, fitness enthusiasts, and health-conscious individuals are incorporating dairy protein products into their daily routines for muscle recovery and maintenance. The market is further strengthened by the expanding demographic of active aging populations seeking protein-rich nutrition, as well as the superior digestibility and complete amino acid profile of dairy proteins. In response to this market demand, FrieslandCampina Ingredients launched Nutri Whey ProHeat in March 2025, specifically designed to meet the performance and active nutrition market needs. This trend is particularly evident in major European markets such as Germany, the UK, and France, where sports participation and gym memberships continue to rise.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing popularity of plant-based and vegan alternative proteins | -1.3% | Germany, UK, Netherlands, Sweden | Long term (≥4 years) |

| Rising lactose intolerance and allergies | -0.8% | Southern Europe, UK, Germany | Medium term (2-4 years) |

| Price fluctuations and raw material volatility | -0.7% | EU-wide, higher in Germany and France | Short term (≤2 years) |

| Supply chain disruptions impact european dairy protein market | -1.0% | EU-wide, particularly Eastern Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing popularity of plant-based and vegan alternative proteins

The shift toward plant-based and vegan protein alternatives presents a significant challenge to the dairy protein market. Consumer adoption of vegan and flexitarian diets, especially among younger demographics, has reduced the demand for traditional dairy proteins. This transition is driven by environmental sustainability concerns, animal welfare considerations, and the perceived health advantages of plant-based options. Food manufacturers have responded by developing protein alternatives from soy, pea, and other plant sources. Improvements in plant protein processing technology have enhanced the taste and texture of these alternatives. The increased retail availability and competitive pricing of plant-based proteins create additional pressure on traditional dairy protein products in the European market. This market shift represents a significant restraint for dairy protein manufacturers, requiring them to adapt their strategies to maintain their market position.

Price fluctuations and raw material volatility

Price volatility in the European dairy protein market continues to escalate, driven by supply shortages in whey protein concentrates and isolates. The Euro's appreciation has diminished profit margins for European dairy producers, affecting their global market position. According to USDA there was a significant dairy herd reductions in France, Germany, the Netherlands, and Belgium during 2024, primarily due to elevated input costs, drought conditions, and bluetongue virus outbreaks. Price volatility has created challenges for manufacturers who face uncertain cost structures while maintaining product quality and meeting delivery obligations. The situation is further complicated by China's anti-subsidy investigation into European Union dairy exports, which could disrupt established trade patterns. Price instability has compelled manufacturers to diversify their sourcing strategies and enhance production efficiency. Additionally, market participants have increased their emphasis on long-term contract negotiations and risk management approaches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Whey Dominates While Milk Isolates Surge

Whey Protein Concentrates maintain the largest market share at 35.12% in 2025. This dominance stems from their versatility in food applications and cost-effectiveness compared to isolates. The segment's position is strengthened by its integration with cheese production, providing operational efficiencies for dairy processors. Milk Protein Isolates represent the fastest-growing segment with a projected CAGR of 8.12% (2026-2031). This growth is attributed to their superior amino acid profile and functional properties in premium applications. Improvements in filtration and separation technologies have enhanced product quality while reducing production costs for high-purity isolates.

The Casein and Caseinates segment maintains significant market presence, particularly in cheese analogues and processed foods, though with slower growth than whey and milk protein segments. Hydrolyzed proteins are increasing in demand across categories, particularly in clinical nutrition and infant formula applications, due to their enhanced digestibility and reduced allergenicity. The market for hydrolyzed proteins benefits from increasing consumer awareness about protein absorption rates and digestive health. Manufacturers are responding to this trend by expanding their hydrolyzed protein product portfolios and investing in research and development to improve production processes.

By Form: Powder Versatility Meets Liquid Convenience

Powder formats account for 78.35% of the European dairy protein market in 2025. This dominance is attributed to their longer shelf life, efficient transportation, and versatile applications. The powder segment maintains its market leadership through cost-effective formulation processes and accurate protein concentration control in end products. The Liquid (RTD) segment is expected to grow at a CAGR of 9.95% during 2026-2031, emerging as the fastest-growing format. This growth is driven by increasing consumer demand for convenient, ready-to-consume products, particularly in sports nutrition and functional beverages.

Manufacturers are implementing advanced technologies to overcome protein stability challenges in liquid formats. These innovations enable the production of ready-to-drink beverages with enhanced texture and reduced viscosity at neutral pH. The technological advancements address traditional formulation constraints in ready-to-drink applications, supporting the liquid segment's growth. As technology continues to evolve, liquid formats are gradually expanding their market presence alongside traditional powder formats.

By Application: Food and Beverage Base Supports Sports Nutrition Growth

The food and beverage segment holds 54.10% market share in 2025, leading the European dairy protein market. Dairy products and desserts represent the largest sub-segment, where dairy proteins serve functional and nutritional purposes. The bakery and confectionery sector incorporates dairy proteins to enhance texture, extend shelf life, and increase nutritional value. The beverage category, particularly protein-enriched milk and yogurt drinks, exhibits significant growth as manufacturers respond to consumer demand for convenient protein delivery formats.

Sports and performance nutrition is projected to grow at a CAGR of 8.78% during 2026-2031, driven by increasing consumer awareness of protein's role in muscle recovery and athletic performance. The segment's growth reflects improvements in protein quality and absorption efficiency, as manufacturers develop specialized dairy protein ingredients for sports nutrition products. The market has diversified beyond protein powders to include ready-to-drink options and protein-enhanced hydration products combining electrolytes with dairy proteins.

By Nature: Organic Growth Outpaces Conventional Base

The conventional segment holds 92.45% of the European dairy protein market in 2025, supported by established supply chains and cost-effective traditional dairy production methods. This segment maintains its position through economies of scale and efficient processing technologies that ensure consistent quality at competitive prices. The organic segment, while smaller, is growing at a CAGR of 10.72% (2026-2031), exceeding the market's overall growth rate. This expansion stems from heightened consumer focus on environmental sustainability, animal welfare, and organic products' health advantages.

The organic segment maintains strong growth momentum despite challenges from higher prices and inflationary pressures on consumer purchasing power. Research demonstrates that organic milk contains higher concentrations of beneficial fatty acids and antioxidants compared to conventional milk, supporting the premium pricing of organic dairy proteins. The EU's robust regulatory framework for organic agriculture, combined with these documented quality differences, provides a strong foundation for the organic segment's continued expansion.

Geography Analysis

Germany maintains its position as the largest market for dairy proteins in Europe with a 24.65% share in 2025, leveraging its robust dairy processing infrastructure and strong domestic demand for protein-enriched products. The country's leadership stems from investments in processing technology and an established distribution network that connects producers with domestic and export markets. The German market demonstrates high innovation in specialized protein ingredients for clinical nutrition and sports applications, supported by its food technology research capabilities.

Spain is emerging as the fastest-growing market with a projected CAGR of 6.93% (2026-2031), driven by increasing consumer awareness of protein's health benefits and the expansion of the sports nutrition segment. The Spanish market benefits from rising health consciousness and the growing adoption of high-protein diets for weight management and active lifestyles. Local production capacity investments and expanded distribution channels for specialized protein products support this growth.

The United Kingdom and France represent substantial markets with diverse application profiles, with the UK focusing on sports nutrition and France specializing in infant formula and clinical nutrition applications. Italy integrates dairy proteins into traditional food products, while the Netherlands and Belgium function as processing and distribution hubs for the European market. Russia shows growth potential in conventional dairy proteins, despite regulatory and geopolitical market access challenges. These regional variations reflect different consumer preferences, regulatory environments, and industrial capabilities across Europe.

Regulatory Landscape

The European dairy protein market operates under the EU food safety framework, with the European Commission providing risk management and EFSA handling risk assessment. Additional controls apply when proteins are used in sensitive applications such as infant and medical nutrition. For novel or highly processed fractions that fall under Regulation (EU) 2015/2283 (Novel Foods), EFSA scientific opinions and subsequent Commission implementing acts determine whether and how an ingredient can be marketed. Authorizations can also be applicant-specific, with time-limited data protection.

Infant and follow-on formula applications are governed by compositional rules under Commission Delegated Regulation (EU) 2016/127. The pathway from an EFSA opinion to legislative updates shapes which protein hydrolysates can be used and under what specifications. In January 2025, EFSA issued an opinion confirming the nutritional safety and suitability of a specific whey-derived protein hydrolysate for infant and follow-on formulas. In January 2026, the European Commission adopted amendments to integrate specific protein hydrolysates into compositional requirements, tightening documentation, specification control, and compliance obligations for suppliers serving early-life nutrition.

Value Chain Analysis

The European dairy protein value chain begins with raw milk production and cooperative milk collection, then moves into primary dairy processing, notably cheese manufacturing, which generates whey streams as co-products. Protein fractionation follows through membrane filtration, ion exchange, and in some cases chromatography, with the resulting fractions dried into commercial powders and further processed into liquid and RTD-ready ingredient formats. Integrated cooperatives and multinational processors such as Arla, FrieslandCampina, Lactalis, and Glanbia play a central role, since they can secure milk pools, capture whey at scale, and invest in specialized fractionation assets that differentiate concentrates, isolates, and hydrolysates for food, sports nutrition, infant nutrition, and medical nutrition applications.

Capacity is concentrated in Ireland, the Netherlands, France, Germany, and Denmark, where large-scale filtration and spray-drying infrastructure supports export-oriented supply. Storage and distribution nodes are also prominent in the Netherlands, Belgium, and northern Germany. Downstream, specialty ingredient distributors and solution providers such as Brenntag, IMCD, and Azelis help manufacturers access these ingredients through logistics, documentation, and application know-how, especially for technically demanding formats like heat-stable beverages and clinical nutrition formulations.

Competitive Landscape

The European dairy protein market exhibits moderate fragmentation, with mid-sized cooperatives and multinational corporations like Agrial Group, Arla Foods Amba, Kerry Group Plc, and Glanbia Plc holding significant market positions. These companies are implementing vertical integration strategies to secure raw material supply while developing specialized products for high-growth application segments.

Market participants are investing in proprietary processing technologies to enhance product differentiation, particularly in areas of heat stability, solubility, and sensory attributes. This focus on technological advancement is exemplified by FrieslandCampina's March 2024 announcement of a EUR 30 million investment in its German production facilities, aimed at developing innovative dairy protein products and implementing sustainable manufacturing processes.

The market presents opportunities in hybrid protein formulations that combine dairy and plant sources, as well as specialized ingredients for the clinical nutrition segment. Industry consolidation continues as companies seek economies of scale and broader geographic presence to address margin pressures. Technological capabilities have become a crucial factor in maintaining competitive advantage in this evolving market landscape.

Europe Dairy Protein Industry Leaders

-

Glanbia plc

-

Agrial Group

-

Arla Foods Amba

-

FrieslandCampina Ingredients

-

Kerry Group Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Investment is concentrating on higher-value whey and bioactive fractions for sports and performance, medical, and early-life nutrition, along with technologies that improve purity, stability, and process yields. FrieslandCampina Ingredients completed a strategic expansion at its Borculo site in March 2026, doubling production capacity for high-quality whey protein isolate and milk fat globule membrane (MFGM). It also announced an investment program exceeding EUR 90 million in May 2026 to expand and upgrade whey protein ingredient capacity across its Dutch network (Bedum, Veghel, and Workum). In Germany, DMK Group disclosed a EUR 55 million program at Edewecht in May 2026, including a new WPC80 facility with stated 7,000-tonne capacity plus packaging and logistics additions. It commissioned a EUR 25 million lactoferrin plant at Altentreptow in June 2026 using chromatography infrastructure, highlighting a shift away from commodity output toward specialized, premium protein ingredients.

Opportunities also appear in adjacent innovation tracks that complement conventional dairy proteins rather than replace them. This includes EU-funded low-carbon production approaches and sustainability upgrades integrated into new capacity by incumbent processors. The HYDROCOW project (EIC-supported and listed on the European Commission CORDIS platform) commenced in 2026 to develop a net-zero carbon dairy protein production platform using engineered hydrogen-oxidizing bacteria (Xanthobacter sp. SoF1) to convert CO2 into food-grade protein, providing an R&D pathway that can affect ingredient roadmaps and partnership structures. With EU dairy supply volatility cited by industry and public sources, including herd reductions in several producing countries during 2024, and with stricter end-market requirements in infant and medical nutrition, customers are placing more weight on suppliers that combine scale access to whey streams, advanced purification capability, and verifiable quality and traceability systems.

Recent Industry Developments

- June 2026: FrieslandCampina Ingredients completed the strategic expansion of its Borculo facility, doubling production capacity for high-quality whey protein isolate and milk fat globule membrane (MFGM). The additional output strengthens supply for premium nutrition applications that require higher purity and consistent functionality, supporting more differentiated portfolios versus commodity whey ingredients.

- May 2025: Fonterra launched MyNZMP Link, a digital sales platform providing 24-hour access to dairy ingredients for European buyers. By enabling direct purchasing of items such as whey protein concentrate from regional warehouses, the platform streamlines procurement and can shorten replenishment cycles for formulators managing volatile input availability.

- November 2024: Arla Foods Ingredients acquired Volac's Whey Nutrition business, adding whey supply capacity to support rising demand for whey-based protein ingredients. The deal increased Arla Foods Ingredients' ability to secure raw material streams and broaden its offering for sports, performance, and specialized nutrition customers in Europe.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe dairy protein market covers the value of dairy-derived protein ingredients sold in the region, mainly whey proteins, caseins, and milk protein concentrates or isolates, in forms used by food, beverage, nutrition, and related manufacturers.

Scope exclusions: We exclude plant-based proteins, lactose and permeates, and generic milk powder shipments when they are not sold as protein ingredients.

Segmentation Overview

-

By Ingredient

-

Milk

- Isolate

- Concentrates

- Hydrolyzed

-

Whey

- Concentrates

- Isolates

- Hydrolyzed

- Casein and Caseinates

-

Milk

-

By Form

- Powder

- Liquid

-

By Nature

- Conventional

- Organic

-

By Application

-

Food and Beverage

- Bakery and Confectionery

- Dairy Products and Desserts

- Beverages

- Sports and Performance Nutrition

- Infant and Early-Life Nutrition

- Elderly Nutrition and Medical Nutrition

- Other Applications

-

Food and Beverage

-

Geography

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base around milk supply, dairy processing, and trade flows that shape ingredient availability across Europe. We relied on public datasets such as Eurostat and FAOSTAT for production and utilization indicators, UN Comtrade for import-export reporting, national agriculture ministries for local supply context, and Codex Alimentarius or similar official food standards sources to confirm definitions and reporting boundaries.

Along with those, we reviewed company annual reports, investor presentations, association websites, and reputable press coverage to map product positioning and application demand across sports nutrition, infant nutrition, and everyday food fortification. Where needed for cross-checking revenues and shipment signals, we used paid subscriptions for company financials and intelligence, and shipment-level import-export data, while keeping assumptions tied to observable indicators. The desk sources mentioned here are illustrative only, and many other public and internal references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions on where demand is coming from and how pricing moves in practice across key European markets. We spoke with a mix of ingredient suppliers, processors, distributors, and downstream buyers in food, beverage, and nutrition, and we revisited specific conversations when some responses looked inconsistent with trade signals or reported capacity changes.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | |

| Mid tier: 54% | Functional/Unit leaders: 29% | |

| Smaller Players: 14% | Managers: 58% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool built from Europe dairy ingredient usage, where milk collection and processing volumes are translated into protein ingredient availability, then adjusted using trade balances and application-level adoption. After that, the totals are corroborated through selective bottom-up checks, including sampled supplier revenues by protein line, distributor channel checks, and volume-by-average-selling-price builds for common grades, which are then used to correct overcounts that appear inconsistent with grade mix.

Key inputs used in the model include dairy protein import and export values, milk production and utilization indicators, processing capacity and utilization signals, application mix shifts (for example, sports nutrition versus mainstream food), and observed price movement by product grade and concentration. When a direct data point was missing for a country or sub-category, we filled gaps using ratio-based proxies tied to milk output, trade shares, and interview-confirmed consumption patterns, and then the roll-up was rechecked for realism.

For forecasting, we relied on scenario analysis supported by simple trend logic on the main drivers, followed by expert checks on how quickly adoption and pricing can move. Assumptions were aligned to expected dairy supply conditions, consumer nutrition demand, and planned capacity changes, with those items reviewed during interviews.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including trade flows, capacity direction, and revenue sanity checks, before numbers were signed off. Any large variance versus the expected relationship between volume and pricing triggered an extra review, and in some cases respondents were re-contacted to confirm whether the change came from mix, contract timing, or a true demand shift.

The model goes through multi-step internal checks so that calculation logic, units, and currency treatments are consistent across countries and years. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's Europe Dairy Protein Market Estimate Compared With Other Published Estimates

Published market sizes for Europe dairy protein can look far apart, even when they appear to describe the same space, because the product boundary and the unit of measurement are not always aligned. Differences also come from how each publisher handles ingredient versus finished product value, and from whether the number is built from supply signals, demand signals, or a mix of both.

The biggest gap drivers here are scope and what gets counted as dairy protein, since some estimates widen the basket to include broader dairy ingredients or count finished nutrition products that only contain protein. A second driver is the year and currency treatment, where average prices and conversions can materially change the value in a market that is sensitive to commodity-linked inputs. Finally, refresh cadence matters because capacity additions and trade shifts can change apparent availability quickly, and the estimate stays narrower by excluding lactose and permeates and focusing on commercial dairy protein ingredients, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.10 B (2025) | |

| Global Consultancy A | USD 3.74 B (2024) | Uses a broader milk protein framing that can capture a wider set of protein streams and adjacent ingredient value, and it anchors to a different base year, which shifts price and conversion effects. |

| Industry Publisher B | USD 6.57 B (2022) | Positions the space as dairy protein ingredients more broadly, which can pull in a larger ingredient basket and application coverage, and it uses an earlier base year when pricing and trade mix were different. |

The spread in values is mostly explained by how wide the product basket is and whether the number reflects only protein ingredients or a wider ingredients universe. By keeping the count tied to clearly defined dairy protein ingredient streams and checking the result against trade and capacity signals, the final number remains repeatable and easier to reconcile year to year.

Key Questions Answered in the Report

What is the current Europe dairy protein market size and how fast is it growing?

The Europe dairy protein is valued at USD 1.16 billion in 2026 and is forecast to reach USD 1.49 billion by 2031, advancing at a 5.17% CAGR.

Which country leads the Europe dairy protein market in revenue?

Germany contributes 24.65% of the total revenue in 2025. The country's strong industrial base and technological advancement drive significant market growth.

Why are Liquid (RTD) gaining share in Europe dairy protein form?

The liquid (Ready-to-Drink) segment is expected to grow at a CAGR of 9.95%, driven by increasing consumer demand for convenient, ready-to-consume products.

Which Ingredient type is expected to grow at a fastest CAGR?

Milk Protein Isolates is expected to grow at a CAGR of 8.12% for the forecast period (2026-2031).

Page last updated on: