Germany Non-Dairy Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

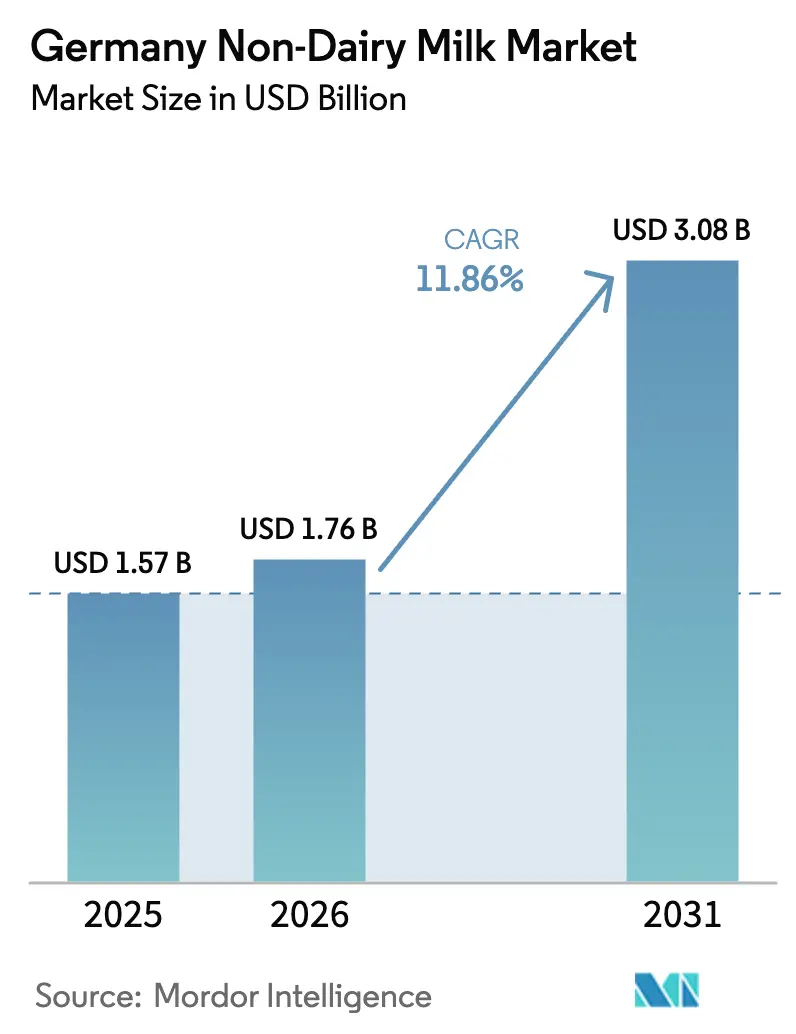

| Base Year Market Size (2025) | USD 1.57 Billion |

| Market Size (2026) | USD 1.76 Billion |

| Market Size (2031) | USD 3.08 Billion |

| Growth Rate (2026 - 2031) | 11.86% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Non-Dairy Milk Market Analysis by Mordor Intelligence

The German non-dairy milk market size was valued at USD 1.57 billion in 2025 and estimated to grow from USD 1.76 billion in 2026 to reach USD 3.08 billion by 2031, at a CAGR of 11.86% during the forecast period (2026-2031). Robust demand stems from shifting dietary preferences, official guidance that legitimizes fortified plant-based beverages, and innovation that lowers environmental footprints. Urban flexitarian consumers drive early adoption, while high lactose-intolerance prevalence in northern regions converts medically motivated shoppers. Retailers nurture the category by dedicating shelf zones and scaling private-label lines, which tighten price gaps with dairy milk. Meanwhile, partnerships between dairy cooperatives and plant-based specialists accelerate capacity expansion and cost optimization, positioning the German non-dairy milk market as a bellwether for broader European transitions.

Key Report Takeaways

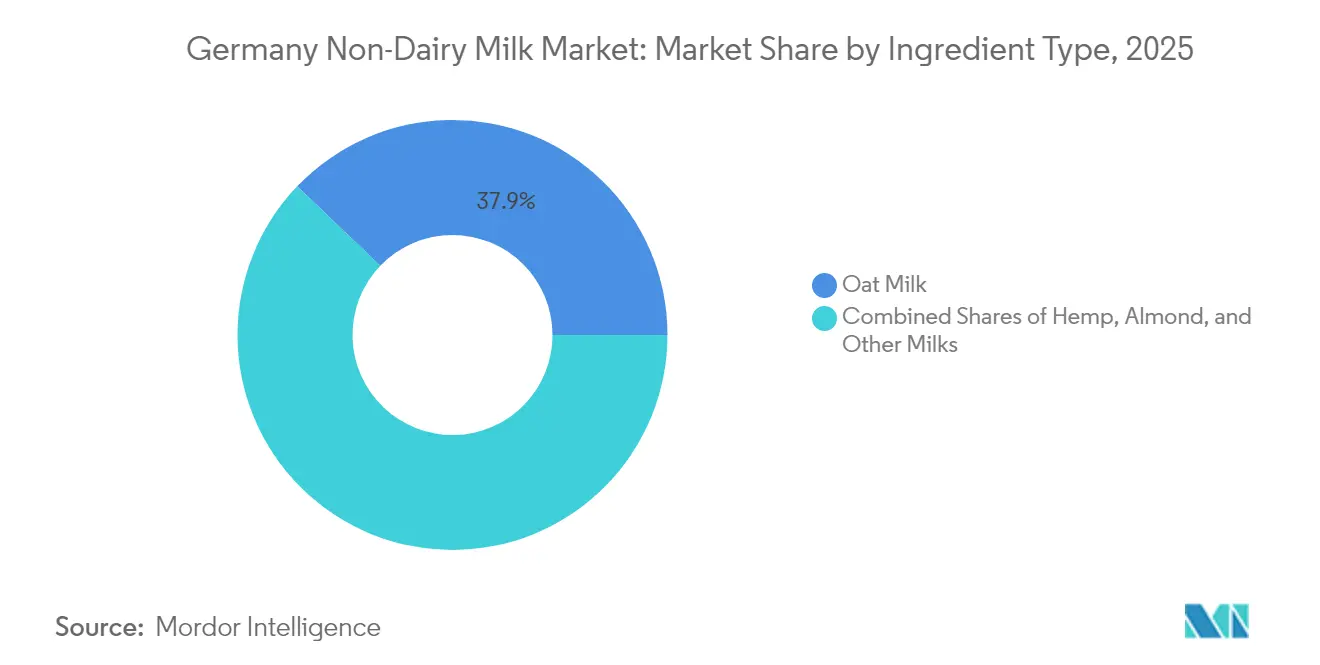

- By product type, oat milk led with 37.85% of Germany non non-dairy milk market share in 2025, while hemp milk is advancing at a 18.55% CAGR through 2031.

- By packaging, cartons accounted for 44.55% of the German non-dairy milk market size in 2025; pouches record the highest projected CAGR at 15.95% to 2031.

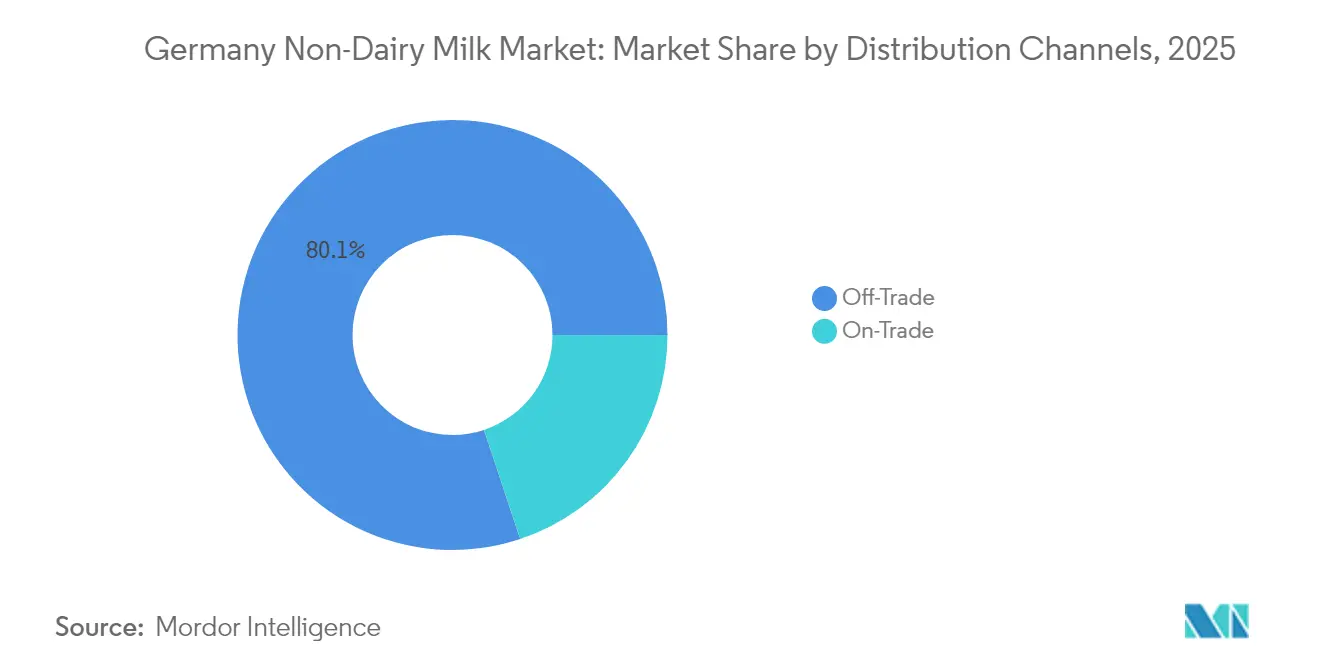

- By distribution channel, off-trade outlets held 80.10% revenue share of the German non-dairy milk market in 2025, and the segment is set to grow at a 14.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Non-Dairy Milk Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing health consciousness and demand for low-cholesterol, lactose-free, and allergen-friendly alternatives | +2.8% | National, with early gains in urban centers | Medium term (2-4 years) |

| High prevalence of lactose intolerance | +1.9% | National, concentrated in Northern Germany | Short term (≤ 2 years) |

| Expanding vegan, vegetarian, and flexitarian populations | +2.1% | National, with higher adoption in Berlin, Hamburg, Munich | Medium term (2-4 years) |

| Continuous product innovation | +2.4% | National, with R&D centers in Bavaria and North Rhine-Westphalia | Long term (≥ 4 years) |

| Endorsement of plant milk in national nutrition guidelines | +1.6% | National policy implementation | Short term (≤ 2 years) |

| Robust retail infrastructure with strong growth in off-trade channels | +1.4% | National, with accelerated expansion in smaller cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Health Consciousness and Demand for Low-Cholesterol, Lactose-Free, and Allergen-Friendly Alternatives

German consumers are increasingly prioritizing functional health benefits over simply matching the taste of dairy milk, creating opportunities in the market for fortified and specialized formulations. The 2024 Nutrition Report by the Federal Ministry of Food and Agriculture[1]Federal Ministry of Agriculture, Food and Home Affairs, "the BMEL Nutrition Report 2024", www.bmleh.de highlights that more than 50% of German consumers actively choose reduced-sugar and low-fat processed food variants, while nearly 20% specifically seek reduced-salt options. This health-conscious behavior extends beyond basic nutrition to include allergen avoidance. German food safety authorities have reported a growing awareness of multiple food sensitivities, which is influencing dairy consumption patterns. This trend is further supported by endorsements from the medical community. For instance, the German Nutrition Society (DGE) has incorporated plant-based protein recommendations into its official dietary guidelines, positioning non-dairy alternatives as nutritionally equivalent to traditional options rather than niche substitutes. Additionally, the Federal Institute for Risk Assessment (BfR) ensures clear allergen labeling standards through its regulatory influence, enabling consumers to make informed decisions about lactose-free and allergen-friendly products.

High Prevalence of Lactose Intolerance

In Germany, 15-20% of adults experience lactose intolerance, presenting a notable market opportunity that includes both diagnosed cases and individuals with mild, undiagnosed symptoms. Studies indicate that lactose malabsorption is more common in Northern Germany, with genetic research linking higher prevalence rates to regions with historically lower dairy consumption, as reported by BfR[2]BfR, “Allergeninformationen,” bfr.bund.de. Enhanced diagnostic capabilities have enabled the medical community to better identify lactose intolerance. At the same time, public awareness campaigns by health organizations have educated individuals on symptom identification and dietary management. German healthcare providers are increasingly recommending plant-based milk alternatives as a primary intervention for lactose-sensitive patients, emphasizing health benefits over taste preferences. This medical backing distinguishes the German market from others, where non-dairy milk adoption is often driven by lifestyle choices rather than health needs.

Expanding Vegan, Vegetarian, and Flexitarian Populations

As reported by the German Federal Ministry of Food and Agriculture, 8% of German consumers identify as vegetarian, while 2% identify as vegan. Over the last four years, the share of individuals purchasing vegetarian and vegan alternatives has increased by 10 percentage points. The flexitarian trend—where individuals intentionally reduce, rather than completely eliminate, animal products—has become the fastest-growing dietary segment. Currently, 39% of German consumers report buying plant-based products more frequently. This behavioral change highlights a rising focus on animal welfare and environmental sustainability, supported by government efforts to promote plant-based protein consumption in line with national climate goals. Data from the Good Food Institute Europe shows that 65% of German respondents support the approval of cultured meat technologies, provided they are deemed safe by authorities. This reflects a growing openness to innovative protein sources beyond traditional plant-based options. Urban areas such as Berlin, Hamburg, and Munich exhibit higher adoption rates, forming geographic clusters of early adopters that influence broader market acceptance patterns.

Continuous Product Innovation

German companies are leading Europe's innovation in non-dairy milk technology, driving advancements in packaging, formulation, and production. Veganz has developed a revolutionary 2D-printing technology for milk alternatives, transforming the industry. This technology enables on-demand preparation, removes the need for refrigeration, and reduces packaging waste by 94% and transportation emissions by 90%. Research projects such as PULSE2CHEESE and DARE2CYCLE, led by the Fraunhofer Institute, highlight a strong institutional focus on plant-based dairy alternatives. Supported by government funding, these initiatives aim to create meltable cheese alternatives from legumes and establish circular biorefinery platforms. The innovation ecosystem is further strengthened by partnerships like the Frischli-Brüggen joint venture, which combines traditional dairy processing expertise with oat milling to produce advanced oat drinks. Moreover, the EU's Novel Foods framework facilitates the inclusion of approved functional ingredients, such as plant proteins, human milk oligosaccharides, and microalgae oils, in dairy analogue formulations.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher price point of non-dairy milk | -1.8% | National, particularly affecting price-sensitive segments | Short term (≤ 2 years) |

| Complex regulatory requirements | -1.2% | EU-wide, with German-specific implementation challenges | Long term (≥ 4 years) |

| Supply chain volatility affecting key raw materials | -1.5% | Global supply chains affecting German production | Medium term (2-4 years) |

| Shelf life limitations and perceived freshness concerns | -0.9% | National, concentrated in traditional dairy regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Price Point of Non-Dairy Milk

Price premiums of 50-100% over conventional dairy milk create challenges for adoption, particularly among price-sensitive consumers, limiting market penetration in lower-income groups. Research from Verbraucherzentrale highlights significant price differences: premium organic non-dairy alternatives are priced above €2.00 per liter, while conventional milk costs between €0.75 and €1.20. These price gaps are driven by production cost structures, including higher raw material costs, specialized processing, and smaller production scales, which prevent economies of scale compared to established dairy operations. However, strategic partnerships, such as the Frischli-Brüggen joint venture, focus on cost optimization through vertical integration and shared infrastructure. Price sensitivity analysis indicates that achieving price parity with dairy milk could expand the addressable market by 25-30%, emphasizing the critical role of cost reduction for market leaders.

Complex Regulatory Requirements

Non-dairy milk manufacturers face increased market entry barriers and operational challenges due to the EU and German regulatory frameworks. The EU Novel Foods Regulation (2015/2283) mandates comprehensive safety assessments for innovative ingredients. Specifically, provisions for dairy analogs define maximum usage levels and impose labeling requirements, as outlined by the EU Commission. In Germany, despite strong consumer demand for organic alternatives, the prohibition on fortifying organic plant-based drinks—enforced under EU organic regulations—raises nutritional adequacy concerns, hindering organic product development. Hemp-based products are subject to additional scrutiny, with the Federal Office for Agriculture and Food (BLE) ensuring compliance with the 0.3% THC threshold for industrial hemp varieties. Additionally, labeling restrictions prohibit the use of dairy-related terminology, requiring alternative descriptors that may reduce consumer recognition and purchase intent. Allergen declaration requirements further complicate the formulation of multi-ingredient products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Hemp Milk Drives Innovation Despite Oat Dominance

In 2025, oat milk holds a leading 37.85% market share, driven by German consumers' preference for locally-sourced ingredients and its superior functionality in coffee applications. This segment has established itself as a premium alternative, offering a sensory experience comparable to dairy milk. Advances in processing technology have further enhanced its appeal by improving creaminess and reducing off-flavors. Major German retailers now consider oat milk a mainstream product. For instance, REWE has introduced Berief Food's organic oat drinks, while Penny has launched Veganz's innovative sheet-form oat milk. Meanwhile, hemp milk is the fastest-growing segment, with a projected 18.55% CAGR through 2031, fueled by the German government's recent easing of industrial hemp cultivation regulations, which have removed previous barriers.

Hemp milk is gaining traction as a high-protein, omega-rich alternative, appealing to health-conscious consumers seeking functional nutrition benefits. In 2024, regulatory changes in Germany, such as the removal of the restrictive "Missbrauchsklausel" and the approval of indoor hemp cultivation, have facilitated easier sourcing and processing of hemp ingredients, as noted by the Bundestag. Research from Lower Saxony highlights hemp milk's environmental benefits, showing a 51.7% reduction in global warming potential and 200 times lower land use compared to bovine milk, strengthening its sustainability-focused marketing. Soy, almond, and coconut milk segments maintain stable positions in the market. Soy benefits from well-established supply chains and high protein content, while almond and coconut milks cater to premium and specialty markets, respectively. The Federal Office for Consumer Protection and Food Safety (BVL) ensures consistent quality standards across all product categories.

By Packaging Type: Innovation Challenges Traditional Carton Leadership

In 2025, cartons hold a leading 44.55% share of the packaging market, leveraging their strong consumer acceptance and compatibility with retail infrastructure, which ensures extensive distribution across Germany. Traditional systems like Tetra Pak not only provide extended shelf life but also align with German consumers' preference for bulk purchases, while reducing cold chain demands for retailers. However, innovative pouch formats are experiencing the fastest growth, with a notable 15.95% CAGR, driven by sustainability efforts and space-saving benefits that appeal to environmentally conscious consumers and cost-focused retailers. Veganz's groundbreaking 2D-printed sheet technology is transforming the industry by eliminating conventional packaging. This approach enables products to be reconstituted from printed sheets, reducing packaging waste by 94% and storage requirements by 85%.

Bottle packaging targets premium and specialty markets, particularly for organic and artisanal products that benefit from the perceived quality of glass packaging and justify higher price points. Research shows a strong preference among German consumers for glass packaging, despite potential environmental trade-offs, with reusable glass bottles receiving the highest preference in choice experiments. While can packaging remains confined to specific applications and niche products, other formats are expanding, including Veganz's Mililk Drops for foodservice and specialized pouches for concentrated formulations. Regulatory pressures from packaging waste regulations are driving innovation toward sustainable materials and reduced packaging intensity, supporting the growth of alternative formats that minimize environmental impact while preserving product quality.

By Distribution Channels: Off-Trade Dominance Reflects Consumer Preferences

In 2025, off-trade channels hold an 80.10% market share, highlighting German consumers' preference for home consumption and their inclination toward bulk purchasing and brand comparison shopping. Supermarkets and hypermarkets, including leading chains such as REWE, EDEKA, and the Schwarz Group, are expanding plant-based sections and forming strategic partnerships with innovative manufacturers. REWE's exclusive launch of Berief Food's organic oat drinks and Penny's introduction of Veganz Milk products illustrate retailers' focus on category growth and brand differentiation. Convenience stores and specialist retailers address specific consumer needs, with organic shops and health food stores maintaining a premium position for specialized products that deliver higher margins.

Online retail is experiencing rapid growth within the off-trade segment, driven by established e-commerce platforms and direct-to-consumer strategies from innovative manufacturers. The off-trade channel is forecasted to grow at a 14.98% CAGR through 2031, supported by expanding retail infrastructure and the mainstream adoption of plant-based alternatives. While on-trade channels represent a smaller volume, they are essential for product trials and influencing consumer preferences through applications in restaurants, cafes, and institutional settings. Veganz's exclusive partnership with Develey highlights the strategic importance of professional channels in enhancing brand visibility and shaping consumption patterns. Regulatory oversight from food safety authorities ensures consistent quality standards across all distribution channels, while organic certification requirements add complexity to supply chain management, particularly for premium product segments.

Geography Analysis

Germany's non-dairy milk market highlights regional differences influenced by demographic, cultural, and economic factors. Northern regions such as Hamburg, Schleswig-Holstein, and Lower Saxony experience higher rates of lactose intolerance, driving a medically-driven demand for plant-based alternatives and establishing a market that goes beyond lifestyle preferences. Urban centers like Berlin, Munich, and Hamburg lead in adopting innovative products and dominate the premium segment. These cities have a higher concentration of vegetarian, vegan, and flexitarian consumers who prioritize sustainability and animal welfare in their purchasing decisions.

According to the Federal Ministry of Food and Agriculture, over 75% of German consumers value seasonality and regional origin, creating opportunities for locally-sourced plant-based ingredients, including regionally-grown oats, nuts, and legumes. Bavaria and Baden-Württemberg, traditionally known for dairy consumption, are transitioning toward plant-based alternatives, supported by strong organic food movements and growing environmental awareness. These regions benefit from well-established food processing infrastructure and renowned research institutions like the Fraunhofer Institute, which drive advancements in plant-based dairy technologies through government-funded initiatives.

North Rhine-Westphalia, with its industrial strength, offers manufacturing and logistics capabilities that enable large-scale production and distribution. Companies such as Tofutown operate significant manufacturing facilities in the region, serving both domestic and export markets. In eastern states, younger demographics and urbanization are fostering adoption, though price sensitivity drives demand for affordable private-label options over premium brands. State-level food safety authorities ensure consistent enforcement of EU and federal standards across regions, while organic certification bodies maintain quality standards that support premium positioning in environmentally-conscious areas.

Competitive Landscape

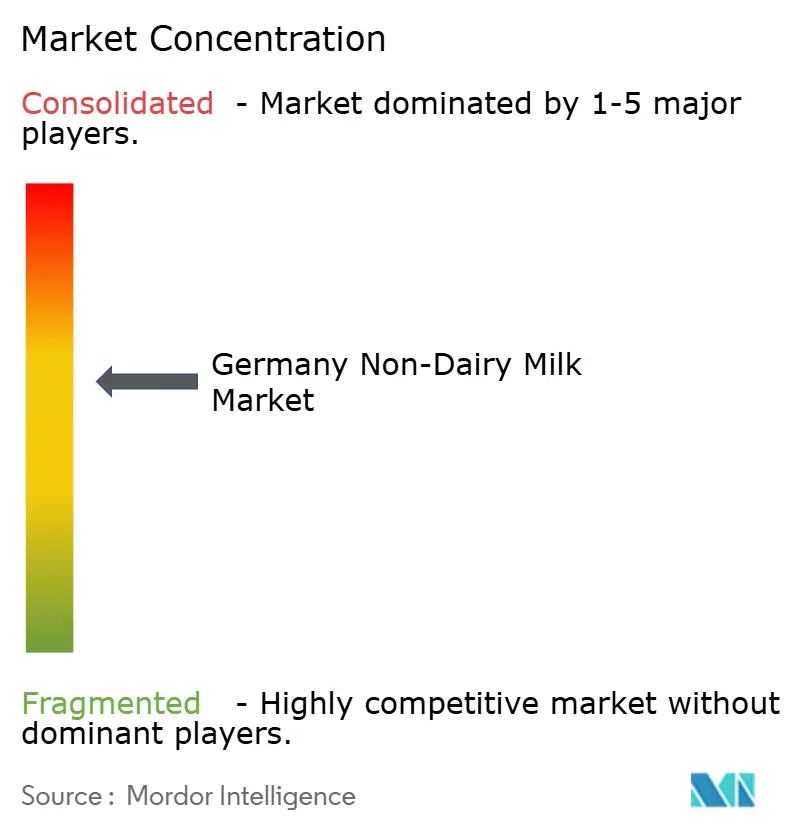

Germany's non-dairy milk market, with a competitive intensity rating of 6 out of 10, reflects a moderately concentrated industry where established multinational corporations coexist with innovative domestic startups and expanding private-label offerings. The market dynamics highlight strategic positioning across diverse price tiers and product categories. In the premium segment, innovation-driven companies such as Veganz and Oatly maintain a stronghold, while private-label products from major retailers like REWE's Vemondo, Lidl's Simply V, and Aldi's Gut Bio are increasingly gaining traction in the mass-market segment.

Competitive strategies in this market focus on technological advancements, sustainability credentials, and functional benefits, moving beyond traditional price-based competition. This approach creates significant opportunities for companies that can effectively integrate innovation with scalable production capabilities. Collaborations between traditional dairy companies and plant-based specialists signify a broader industry acknowledgment of a permanent shift in consumer preferences rather than a passing trend. For example, the Frischli-Brüggen joint venture combines extensive dairy processing expertise with specialized oat milling capabilities, offering a competitive edge in terms of production efficiency and product quality. Additionally, international expansion strategies, such as Veganz's manufacturing agreements with Jindilli Beverages for the North American and Australian markets, demonstrate the confidence of German companies in their technological expertise and brand positioning to compete on a global scale.

The market also presents untapped opportunities in functional and fortified product segments, precision fermentation technologies, and sustainable packaging innovations that address environmental concerns while ensuring product integrity. Regulatory frameworks, including oversight by competition authorities, play a crucial role in maintaining fair market access and preventing anti-competitive practices. Meanwhile, EU Novel Foods regulations create entry barriers that favor established players with the regulatory knowledge and financial resources necessary for compliance investments.

Germany Non-Dairy Milk Industry Leaders

-

AlnaturA Produktions - und Handels GmbH

-

Danone SA

-

Oatly Group AB

-

The Hain Celestial Group Inc.

-

Blue Diamond Growers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Oatly Group launched BaristaMatic, a new Barista-style oat milk product specifically formulated for fully automatic coffee machines used in commercial settings like restaurants and coffee kiosks.

- July 2025: Oat;y Group launched a ready-to-drink matcha latte oat milk. The Matcha Latte Oat Drink features a sweet matcha flavor complemented by a hint of vanilla, perfectly blended with Oatly’s signature creamy oat base.

- January 2025: Veganz Group launched high-quality vegan organic oat milk in Germany. The product is made from European wholegrain oatmeal. Oat milk is free from lactose, milk protein, and any soya components.

- June 2024: Waitrose launched fresh oat milk from Lancashire-based brand Oato. Oato’s fresh Barista-style oat milk comes in one-liter bottles designed to resemble traditional cow’s milk packaging.

Germany Non-Dairy Milk Market Report Scope

Almond Milk, Cashew Milk, Coconut Milk, Hazelnut Milk, Hemp Milk, Oat Milk, Soy Milk are covered as segments by Product Type. Off-Trade, On-Trade are covered as segments by Distribution Channel.| Almond Milk |

| Cashew Milk |

| Coconut Milk |

| Hazelnut Milk |

| Hemp Milk |

| Oat Milk |

| Soy Milk |

| Others |

| Cans |

| Pouches |

| Cans |

| Bottles |

| Others |

| Off Trade | Supermarkets & Hypermarkets |

| Convenience Stores | |

| Specialist Retailers | |

| Online Retail | |

| Other Channels | |

| On-Trade |

| Product Type | Almond Milk | |

| Cashew Milk | ||

| Coconut Milk | ||

| Hazelnut Milk | ||

| Hemp Milk | ||

| Oat Milk | ||

| Soy Milk | ||

| Others | ||

| Packaging Type | Cans | |

| Pouches | ||

| Cans | ||

| Bottles | ||

| Others | ||

| Distribution Channels | Off Trade | Supermarkets & Hypermarkets |

| Convenience Stores | ||

| Specialist Retailers | ||

| Online Retail | ||

| Other Channels | ||

| On-Trade | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms