Europe Confectionery Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

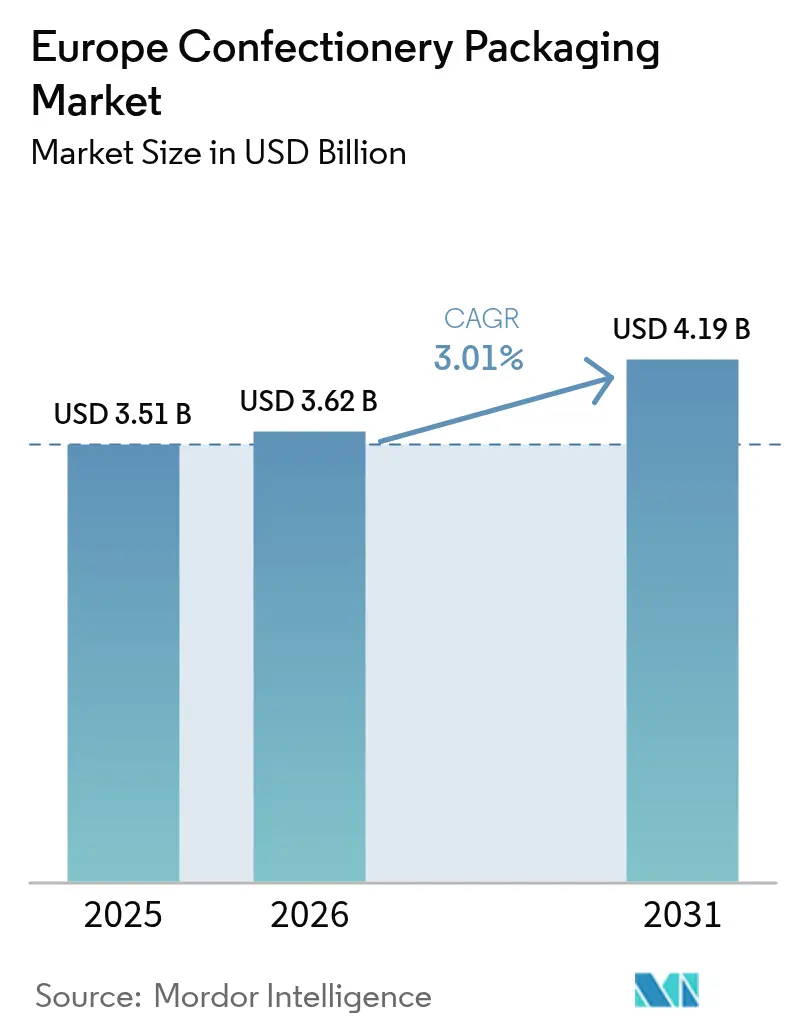

| Base Year Market Size (2025) | USD 3.51 Billion |

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 4.19 Billion |

| Growth Rate (2026 - 2031) | 3.01% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Confectionery Packaging Market Analysis by Mordor Intelligence

Europe confectionery packaging market size in 2026 is estimated at USD 3.62 billion, growing from 2025 value of USD 3.51 billion with 2031 projections showing USD 4.19 billion, growing at 3.01% CAGR over 2026-2031. Demand expands as premiumisation drives smaller pack launches, while sustainability legislation accelerates the pivot toward recyclable mono-material solutions that match classic barrier performance. Brand owners redesign shelf-ready secondary packs to curb in-store labour costs, and they invest in e-commerce-optimised multipacks that endure tougher distribution environments. Regulatory milestones such as the EU Packaging and Packaging Waste Regulation (PPWR) and the coming Digital Product Passport re-shape material choices, data requirements, and investment priorities. Finally, persistent spikes in cocoa prices, which sailed beyond USD 12,000/ton in 2024, amplify the need for portion-controlled formats that guard margins through shelf-life optimisation

Key Report Takeaways

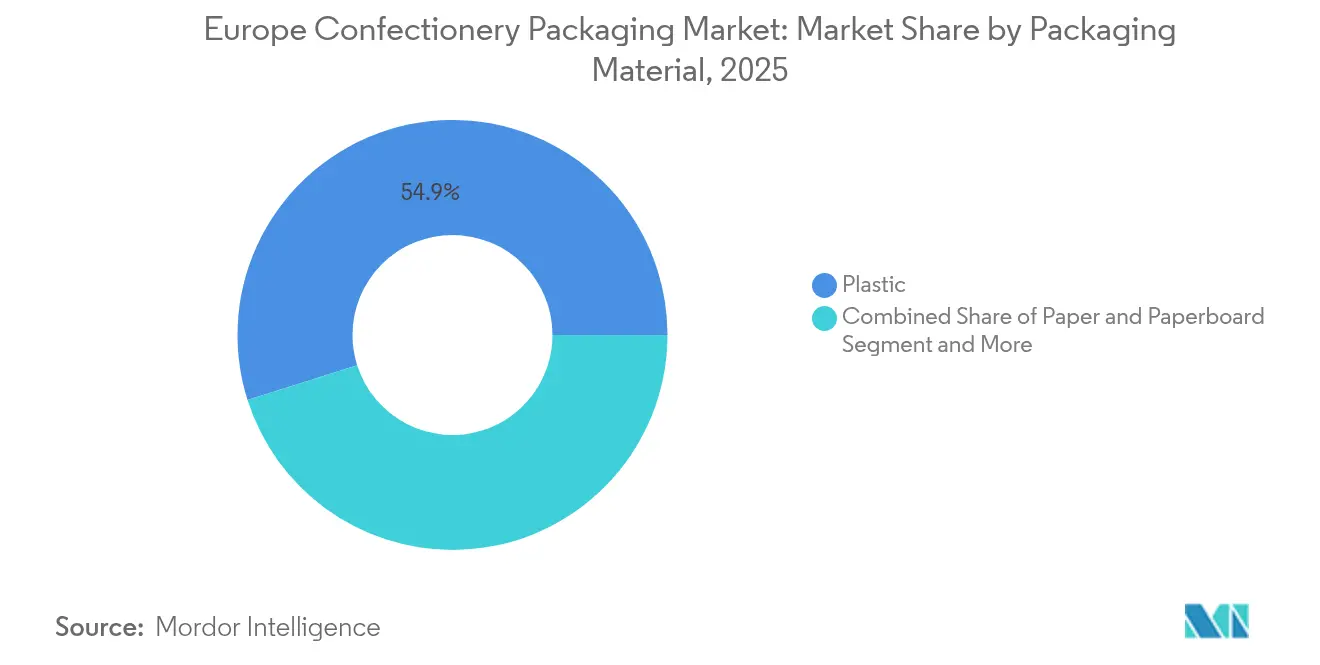

- By packaging material, plastic maintained 54.88% of the Europe confectionery packaging market share in 2025, whereas bioplastic and compostable films are set to post the fastest 6.02% CAGR through 2031.

- By packaging format, flexible solutions led with 54.31% Europe confectionery packaging market share in 2025; the segment is expected to advance at a 4.28% CAGR to 2031.

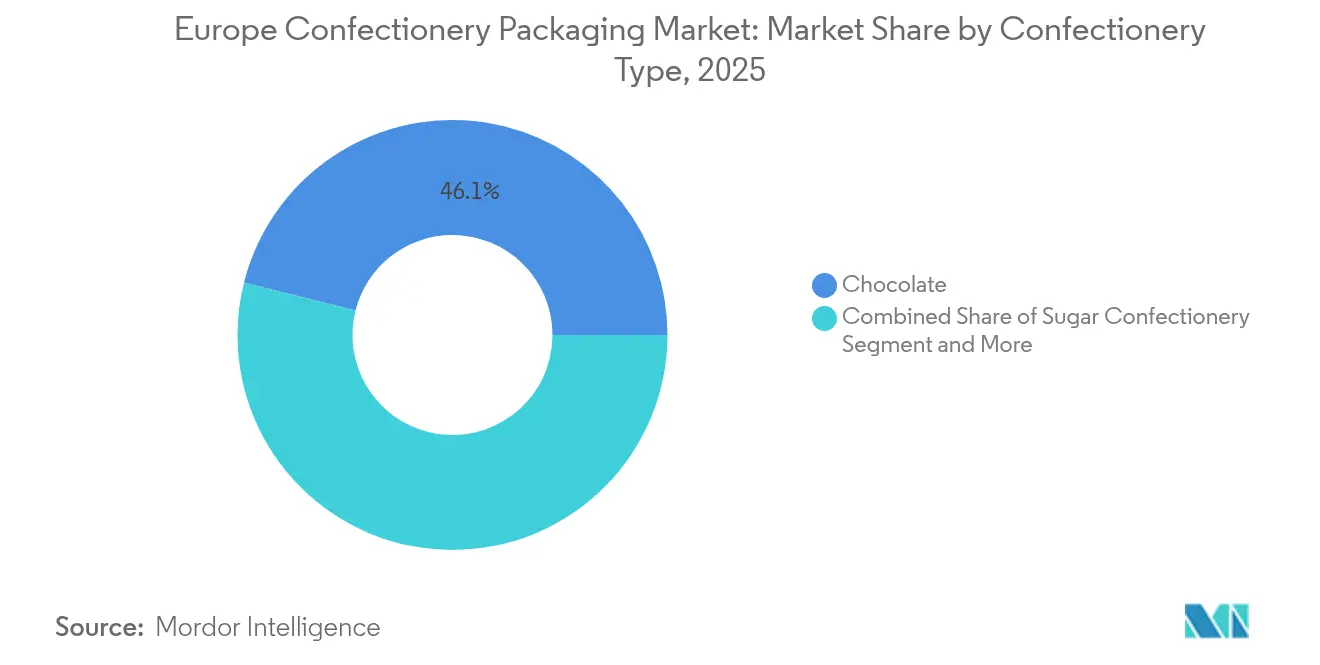

- By confectionery type, chocolate held 46.07% of the Europe confectionery packaging market size in 2025 while sugar confectionery is projected to expand at a 6.86% CAGR during 2026-2031.

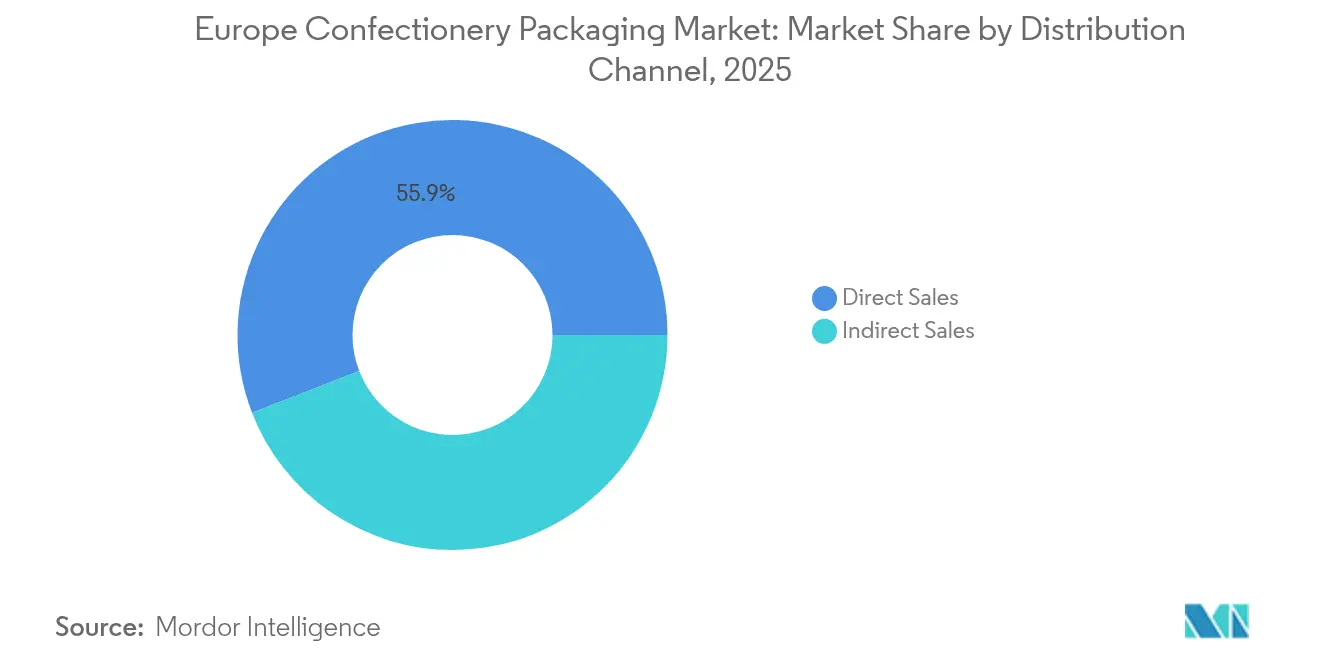

- By distribution channel, direct sales captured 55.88% of the Europe confectionery packaging market share in 2025, yet indirect channels are set to climb at a 4.57% CAGR on e-commerce momentum.

- By country, Germany commanded 22.23% revenue share in 2025, but Spain is forecast to deliver the highest 7.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on confectionary packaging market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Confectionery Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation-led smaller pack launches | +0.8% | Western Europe, with early adoption in Germany and France | Medium term (2-4 years) |

| Sustainability-driven shift to recyclable mono-material flexibles | +0.9% | EU-wide, strongest in Nordic countries and Netherlands | Long term (≥ 4 years) |

| Shelf-ready secondary packs that cut in-store labour costs | +0.5% | UK, Germany, France with retail consolidation | Short term (≤ 2 years) |

| E-commerce-optimised confectionery multipacks | +0.7% | Western Europe, expanding to Eastern Europe | Medium term (2-4 years) |

| Biopolymer barrier films reaching commercial cost parity | +0.6% | Germany, Netherlands, Scandinavia | Long term (≥ 4 years) |

| Smart-pack coding for EU Digital Product Passport compliance | +0.4% | EU-wide implementation by 2027 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumisation-led Smaller Pack Launches

Consumer willingness to trade up for artisanal products is pushing brand owners to develop sophisticated small-format packs that justify higher unit prices while curbing calorie intake. Mondelez and Saica debuted a paper-based multipack that reinforces premium cues and aligns with recyclability goals. Chocolate makers need high-barrier structures to protect flavour in reduced volumes, prompting Amcor to roll out AmFiber Performance Paper for high-margin segments.[1]Amcor, “AmFiber Performance Paper Packaging,” amcor.com Precision dosing lines and advanced sealing units now support economically viable small-batch runs, giving suppliers of flexible equipment an edge. Retailers benefit from portion-controlled packs that fit front-of-store displays, and consumers gain clarity on calorie counts, underscoring the driver’s broad relevance across the Europe confectionery packaging market.

Sustainability-driven Shift to Recyclable Mono-material Flexibles

End-of-life mandates under PPWR and consumer eco-preferences are steering brands away from complex laminates toward mono-material films that still hit oxygen and moisture targets. Amcor’s AmPrima line achieved a 92% recyclability score while preserving critical barrier levels in a recent Lorenz Snacks deployment.[2]Packaging Europe Staff, “Amcor and Lorenz Snacks collaborate on ‘recycle-ready’ snack packaging,” packagingeurope.comCorporate pledges Cadbury’s 80% recycled content for sharing bars exemplifies the trend lock in long-term demand for circular polymers. Brands that master mono-material design gain a marketing lift and regulatory head start, whereas late adopters confront higher compliance costs and risk shelf-de-listing. The shift therefore represents the most powerful growth lever in the Europe confectionery packaging market.

Shelf-ready Secondary Packs That Cut In-store Labour Costs

Retail consolidation raises pressure on store efficiency, making shelf-ready solutions that bypass back-room unpacking attractive to grocers. Purpose-built trays ease replenishment, slash labour minutes, and enhance visual merchandising. Packaging suppliers integrate perforations and display windows into corrugated or rigid plastic outers without compromising transit protection. Adoption began in the UK and Germany and now spreads into France as retailers standardise store formats. Manufacturers see faster shelf activation, limiting out-of-stock events and sustaining velocity, which supports steady uptake across the Europe confectionery packaging market.

E-commerce-optimised Confectionery Multipacks

Online confectionery spending hit 4.7% of German food retail by 2025, accelerating design priorities that favour crush resistance and thermal stability over traditional in-aisle appeal. Subscription programmes amplify demand for durable outer cases and right-sized inner flow wraps that curb dimension-based shipping fees. Brands experiment with QR codes for delivery confirmation and freshness alerts, adding traceability layers ahead of the Digital Product Passport. Suppliers who blend protective engineering with lightweight mono-materials stand to expand share within the Europe confectionery packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Impending PFAS and BPA bans raising conversion costs | -0.7% | EU-wide, particularly affecting food contact applications | Short term (≤ 2 years) |

| Proposed EU PPWR 95% recyclability target by 2030 | -0.5% | EU-wide implementation with varying national enforcement | Medium term (2-4 years) |

| Higher freight rates hurting glass container economics | -0.3% | Western Europe, particularly affecting premium segments | Short term (≤ 2 years) |

| Sugar-reduction regulations dampening seasonal gift volumes | -0.4% | EU-wide, with stricter implementation in Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Impending PFAS and BPA Bans Raising Conversion Costs

The 2026 ban on PFAS in food contact materials caps individual compounds at 25 ppb, forcing converters to reformulate barriers and adhesives. Large groups expect EUR 50–100 million (USD 58.55 - 117.09 million) in conversion spending for line retrofits and verification testing.[3]Food Packaging Forum, “European Council adopts final provisions of PPWR,” foodpackagingforum.orgSmaller firms shoulder proportionally steeper burdens and may exit high-barrier niches, tightening supply in the short term. Suppliers with certified PFAS-free portfolios secure premium pricing and gain share within the Europe confectionery packaging market.

Proposed EU PPWR 95% Recyclability Target by 2030

The 95% threshold obliges brand owners to redesign multi-layer chocolate wraps that currently rely on aluminium or EVOH for shelf-life performance. Development costs could surpass EUR 200 million (USD 234.19 million) for broad portfolios. Variable national enforcement complicates planning, and certification bottlenecks risk delaying launches. Ventures that already master mono-material science will outpace rivals across the Europe confectionery packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: Bioplastics Drive Innovation Despite Plastic Dominance

Plastic maintained a 54.88% stake in the Europe confectionery packaging market in 2025 thanks to well-understood barriers and cost advantages. Yet bioplastic and compostable films outpace at a 6.02% CAGR, marking the hottest growth pocket as regulation and eco-signals strengthen. Rigid PET cups and tubs retain relevance for portion control, while flexible BOPP and PE films anchor multipack flow wraps. The emergence of mono-material barrier films supports recyclability compliance without trading off shelf-life, shifting procurement towards suppliers that master sophisticated extrusion. The Europe confectionery packaging market size for bioplastic formats is on track to expand swiftly as PLA prices converge with fossil polymers.

Corbion’s forecasted PLA recovery plus early commercial launches signal that cost parity is achievable before 2028. PFAS restrictions intensify R&D in fluorine-free barriers leveraging EVOH and bio-coatings. Paperboard players upscale dispersion-coated papers for grease-resistant wraps, although performance limits still confine usage to low-moisture candies. Metal tins persevere in souvenir gifting due to perceived heritage value despite freight inflation. Collectively these shifts confirm that material choice is now led by recyclability metrics more than traditional cost benchmarks across the Europe confectionery packaging market.

By Packaging Format: Flexible Solutions Adapt to Sustainability Demands

Flexible packs commanded 54.31% revenue in 2025 and still post a healthy 4.28% CAGR through 2031, reflecting unmatched material yield and logistic efficiency. Flow wraps, pouches, and twist wraps score favourably under Extended Producer Responsibility schemes, lowering per-unit eco-fees. Rigid formats defend premium niches where shelf impact and protection justify heavier materials. The Europe confectionery packaging market size for flexible mono-material solutions is poised to widen as barrier performance improvements align with 95% recyclability targets.

Amcor’s 92% recyclable flexible structure for snacks demonstrates functional parity with traditional laminates. Digital printing convergence enables seasonal or influencer-driven graphics without long set-ups, suiting social media campaigns. Smart sensors embedded in flexible films provide temperature excursion alerts, bolstering e-commerce value propositions. Consequently, converters that marry lightweight films with intelligent features are best placed to capture incremental share in the Europe confectionery packaging market.

By Confectionery Type: Sugar Confectionery Accelerates Amid Health Trends

Chocolate retained 46.07% category share in 2025, yet its packaging faces pressure from soaring cocoa costs that spur manufacturers to optimise gram weight. Portion-controlled wraps with high-barrier layers lengthen shelf-life, mitigating shrinkage from heat spikes. Concurrently sugar confectionery records a 6.86% CAGR to 2031 as brands infuse functional ingredients and lower sugar counts, expanding acceptable daily consumption occasions. The Europe confectionery packaging market share tilts marginally toward sugar confectionery as viral novelties such as freeze-dried candy unlock EUR 2.2 billion (USD 2.58 billion) in incremental value.

Gum stays a stable niche requiring oxygen-barrier blister packs, while medicated confectionery employs child-resistant closures under tightening pharma-adjacent rules. Seasonal assortments decline modestly under sugar-reduction policies, yet premium gift boxes endure in high-income segments. Smart codes that verify ingredient provenance and allergen data begin to appear on sugar-free chewy candy, illustrating how health trends and digital mandates converge inside the Europe confectionery packaging market.

By Distribution Channel: Indirect Sales Gain E-commerce Momentum

Direct manufacturer-to-retailer flows took 55.88% share in 2025, but indirect models that include marketplaces, subscription services, and specialised fulfilment post a stronger 4.57% CAGR through 2031. Online baskets mix multiple brands, necessitating protective secondary packaging that survives parcel networks. The Europe confectionery packaging market size tied to e-commerce parcels rises in tandem with click-and-collect and last-mile innovations.

German online food penetration reached 4.7% in 2025, and similar double-digit gains are reported across the Netherlands and Poland. Packaging now emphasises edge-crush strength and insulation liners for summer shipping. QR codes on outer cartons enable real-time tracking, improving first-attempt delivery success. These functional upgrades confirm that indirect channel growth reshapes performance criteria inside the Europe confectionery packaging market.

Geography Analysis

Germany’s leadership in the Europe confectionery packaging market rests on automation depth and early adoption of recyclable mono-materials. The food segment booked 2.1% sales growth in 2024 and is on track to widen e-commerce penetration beyond 5% by 2026, creating a robust pipeline for e-commerce-ready packs. Converters invest in AI vision systems that cut waste and certify barrier integrity, ensuring compliance with the forthcoming Digital Product Passport. Germany’s policy support for circular plastics accelerates post-consumer feedstock availability, reinforcing domestic supply resilience.

Spain provides the sharpest expansion vector as confectionery producers add capacity near Mediterranean ports, tapping both EU and North African demand. Lower energy prices and government incentives attract line installations that prioritise biopolymer films and smart-print capabilities. Packaging lines integrate modular fillers flexible enough to switch between chocolate bars and sugar candies, optimising asset utilisation. The Europe confectionery packaging market benefits as Spanish converters scale volumes that lower unit costs for sustainable substrates.

France, the UK, Italy, the Netherlands, and Central-Eastern Europe round out the regional picture. French prestige brands demand high-end rigid boxes with eco-certified linings, and the country’s luxury gift culture props premium average selling prices. UK converters grapple with rules-of-origin bureaucracy but recover by specialising in quick-turn custom runs for DTC brands. Italian converters blend design aesthetics with functional bio-barriers, while Dutch firms leverage port-centric recycling hubs to secure rPET and rPP for closed-loop supply. Central-Eastern Europe receives investment from multinational groups such as Valeo Foods, which recently acquired Slovak biscuit maker I.D.C. for EUR 200 million (USD 234.19 million) to deepen regional reach. These varied strengths sustain continent-wide growth in the Europe confectionery packaging market.

Competitive Landscape

The Europe confectionery packaging market features moderate fragmentation: top global groups hold meaningful shares, yet niche specialists flourish through agile innovation. Amcor, Mondi, and Huhtamaki pursue vertical integration, running polymer plants, converting lines, and recycling centres that assure supply security. The announced all-stock merger of Amcor and Berry Global will form a USD 24 billion packaging leader with unprecedented scale in flexibles and healthcare, signalling a new consolidation wave.

Strategic priorities span circular materials, smart printing, and AI-enabled quality systems. Smurfit WestRock reported Q1 2025 net sales of USD 7.66 billion and targets USD 400 million in synergies, illustrating EBITDA leverage from network optimisation. Crown Holdings beat Q1 earnings expectations on robust European beverage can demand, showing that metal packaging retains a resilient specialty niche. Patent filings by Lactips for edible water-soluble films illustrate disruptive potential from new materials science.

Emerging innovators carve out share in biopolymer barriers and smart-label printing. ALPLA targets 700,000 tonnes of recycling output by 2030, betting on integrated rPET loops. Constantia Flexibles showcases compostable wraps that meet confectionery oxygen requirements at FACHPACK 2024. Private equity fosters roll-ups such as Carton Pack’s purchase of Clifton Packaging, expanding flexible footprint in the UK. On balance, competitive intensity is anchored in R&D muscle, recyclate access, and digital capability.

Europe Confectionery Packaging Industry Leaders

Amcor Plc

Mondi Group

Huhtamaki Oyj

Smurfit Westrock

Crown Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mars’ USD 36 billion acquisition of Kellanova enters an extended EU antitrust probe that may reshape confectionery sourcing patterns.

- May 2025: Smurfit WestRock posts USD 7.66 billion Q1 2025 sales and USD 1.25 billion adjusted EBITDA as synergy capture advances.

- February 2025: Mondelez moves Cadbury sharing bars to 80% recycled plastic via Amcor partnership, covering 300 million packs across the UK and Ireland.

- February 2025: EU Packaging and Packaging Waste Regulation takes legal effect, setting recyclability and PFAS benchmarks enforceable from Aug 2026.

Europe Confectionery Packaging Market Report Scope

The study tracks the demand for the end-packaging products used for selling confectionery items in Europe. As one of the major markets in the world, the region has been at the forefront of innovation in confectionery packaging, mainly driven by the end-user preference for sustainable solutions and regulations. The scope is limited to the countries with the analysis provided in the study. The major material types and packaging products considered in the scope of work include Paper and Paperboard (Secondary packs, wrappers, and multi-packs), Plastic (wraps, films, pouches, etc.), Metal Containers, Glass Bottles, and Jars. Further, the study also analyses the impact of COVID-19 on the market, and the same has been considered for the current market estimations and future market projections. The country and the confectionery type market share are arrived based on the percentage of the confectionery market in Europe, as the confectionery packaging market is tracked based on demand correlated to the confectionery demand.

| Plastic | Rigid (PET, PP, PS) |

| Flexible (BOPP, PE, PLA) | |

| Paper and Paperboard | |

| Metal | |

| Glass | |

| Bioplastic and Compostable Films |

| Flexible |

| Rigid |

| Chocolate |

| Sugar Confectionery |

| Gum |

| Others (Seasonal, Medicated) |

| Direct Sales |

| Indirect Sales |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Rest of Europe |

| By Packaging Material | Plastic | Rigid (PET, PP, PS) |

| Flexible (BOPP, PE, PLA) | ||

| Paper and Paperboard | ||

| Metal | ||

| Glass | ||

| Bioplastic and Compostable Films | ||

| By Packaging Format | Flexible | |

| Rigid | ||

| By Confectionery Type | Chocolate | |

| Sugar Confectionery | ||

| Gum | ||

| Others (Seasonal, Medicated) | ||

| By Distribution Channel | Direct Sales | |

| Indirect Sales | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe confectionery packaging market?

The Europe confectionery packaging market size reached USD 3.62 billion in 2026 and is forecast to reach USD 4.19 billion by 2031.

Which packaging material is growing fastest in Europe’s confectionery segment?

Bioplastic and compostable films are expanding at a 6.02% CAGR through 2031, outpacing all other materials.

Why are mono-material flexibles gaining traction?

They meet strict EU recyclability rules while now matching legacy barrier performance, allowing brands to hit sustainability targets without sacrificing shelf-life.

Which European country offers the highest growth potential for confectionery packaging?

Spain is projected to grow at an 7.63% CAGR to 2031 due to rising manufacturing capacity and export momentum.

Page last updated on: