Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.56 Billion |

| Market Size (2026) | USD 5.71 Billion |

| Market Size (2031) | USD 6.52 Billion |

| Growth Rate (2026 - 2031) | 2.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cosmetic Packaging Market Analysis by Mordor Intelligence

The Europe cosmetic packaging market size is projected to be USD 5.56 billion in 2025, USD 5.71 billion in 2026, and reach USD 6.52 billion by 2031, growing at a CAGR of 2.69% from 2026 to 2031. Regulatory pressure from the European Union Packaging and Packaging Waste Regulation is steering brand owners toward refillable formats and mono-material designs, forcing converters to retool legacy lines. E-commerce shipments are rising, so brands prioritize protective aesthetics that minimize dimensional-weight fees while elevating unboxing experiences. Gen-Z consumers favour minimalist, recyclable packaging, accelerating demand for clear polypropylene and polyethylene tubes. Recycled-content thresholds and extended producer responsibility fees are already higher than raw-material costs for some non-recyclable tubes in Germany and France, so converters that master lightweighting and digital printing are gaining contract renewals.

Key Report Takeaways

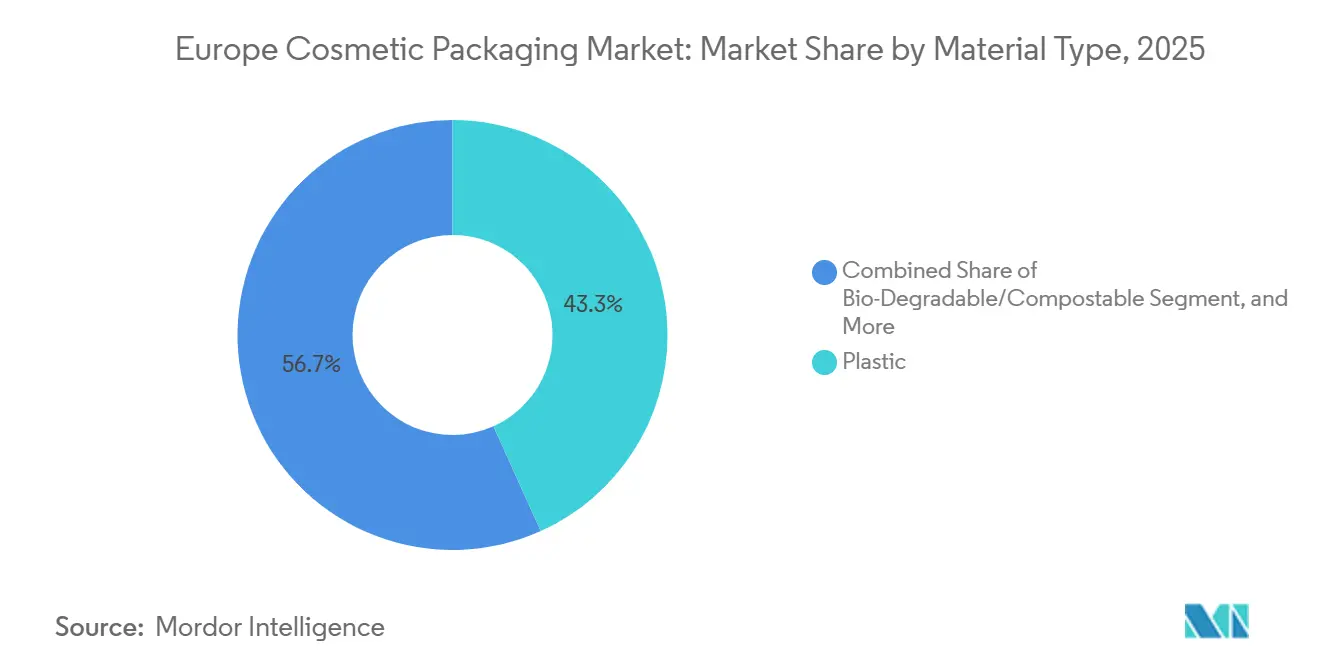

- Plastic retained 43.26% of the 2025 material share, while bio-degradable and compostable alternatives are the fastest growers at a 3.34% CAGR through 2031.

- Bottles and jars led with 29.84% of revenue in 2025, whereas flexible pouches and sachets are advancing at a 3.21% CAGR to 2031.

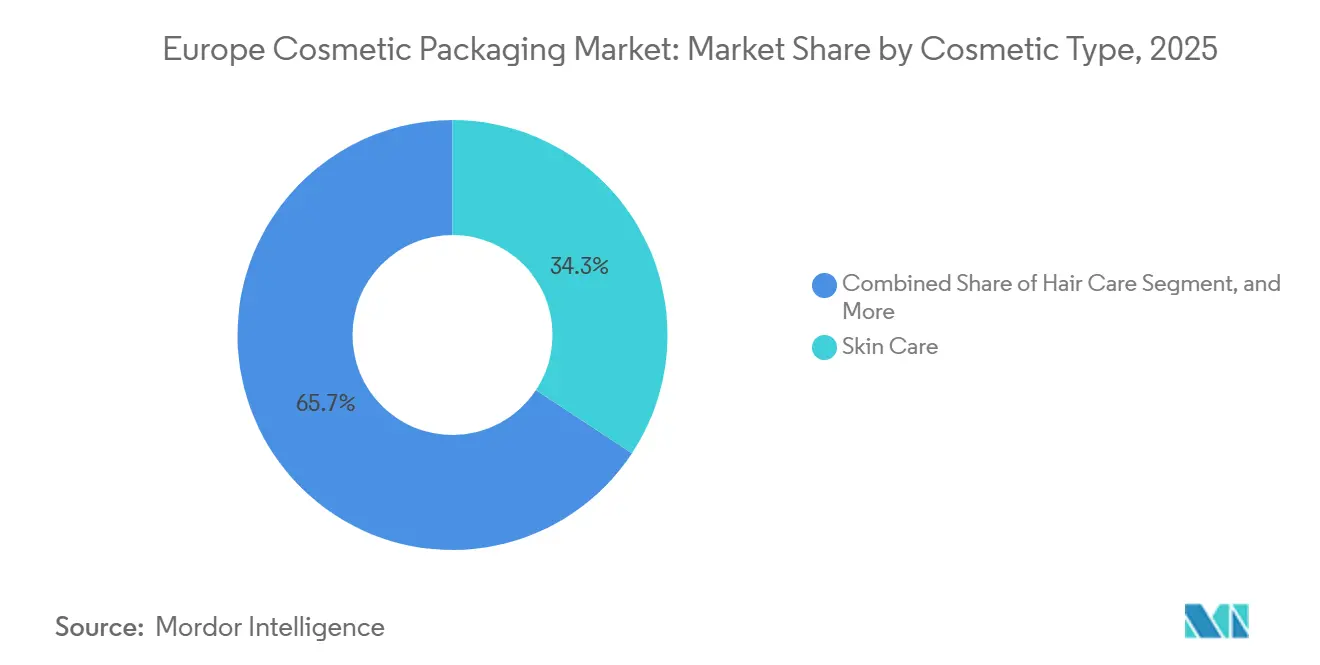

- Skin care captured 34.27% of demand in 2025, yet hair care is projected to expand at a 3.87% CAGR, the quickest among cosmetic types.

- Indirect channels held 71.59% of distribution in 2025, but direct-to-consumer platforms are forecast to rise at a 3.55% CAGR.

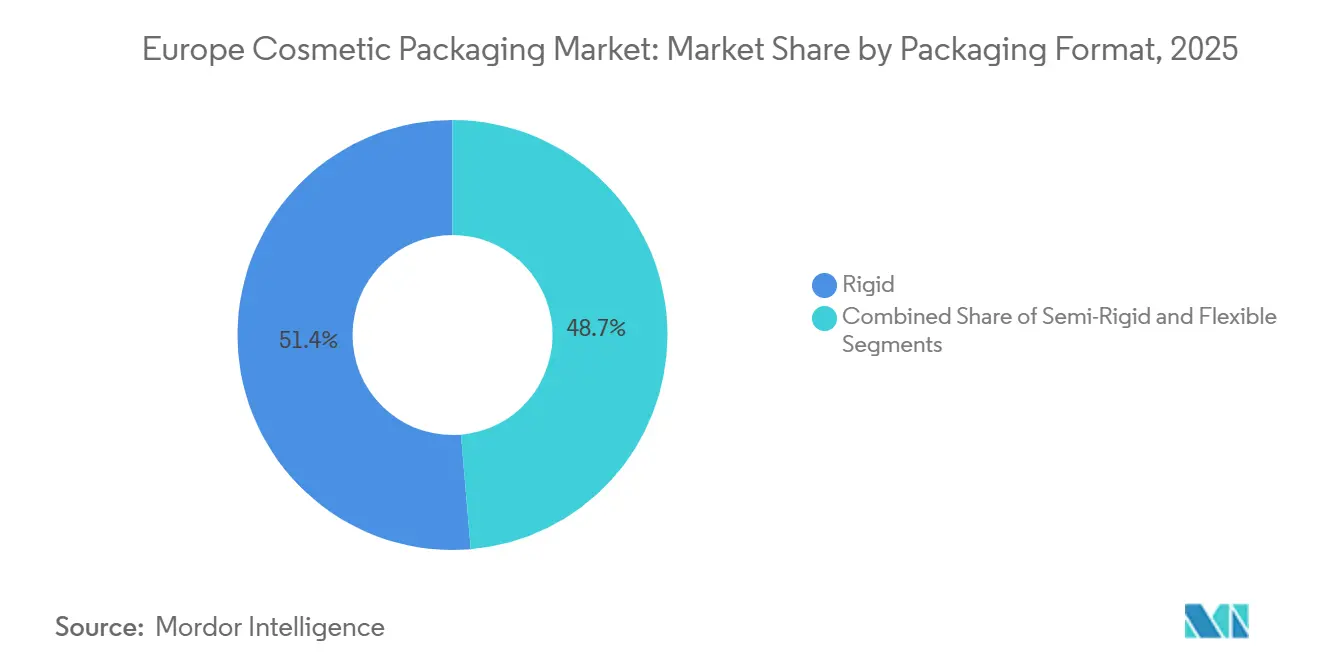

- Rigid formats accounted for 51.35% of 2025 volume, while flexible formats are set to post a 3.42% CAGR through 2031.

- Recyclable designs commanded 46.49% of sustainability share in 2025, whereas bio-based content formats are on track for a 2.91% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Cosmetic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Packaging and Packaging-Waste Regulation Push | +0.60% | Germany, France, Netherlands, Belgium, with spillover to Italy and Spain | Medium term (2-4 years) |

| Surge in Refillable and Reusable Formats | +0.50% | France, Germany, United Kingdom, expanding to Nordics and Benelux | Medium term (2-4 years) |

| E-commerce Led Demand for Protective Aesthetics | +0.40% | Pan-European, with concentration in United Kingdom, Germany, France | Short term (≤ 2 years) |

| Gen-Z Preference for Minimalist, Mono-Material Designs | +0.30% | Urban centers across Germany, United Kingdom, France, Netherlands | Medium term (2-4 years) |

| Microplastic Restriction Shifting Material Mix | +0.30% | EU-wide, with early enforcement in France, Germany, Netherlands | Long term (≥ 4 years) |

| On-Demand 3D-Printed Packaging for Indie Brands | +0.20% | Germany, United Kingdom, France, Italy (indie-brand hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Packaging and Packaging-Waste Regulation Push

Full enforcement in 2025 obliges all cosmetic packs to be recyclable or reusable by 2030 with interim recycled-content targets of 25% for PET bottles by 2027 and 30% by 2030.[1]European Commission, “Regulation 2024/1234 on Packaging and Packaging Waste,” EUR-LEX.EUROPA.EU Brands are redesigning multi-layer laminates into single-material tubes, which requires plasma-coating investments many mid-tier converters cannot fund alone.[2]Gerresheimer AG, “Investor Presentation 2025,” GERRESHEIMER.COM Extended producer responsibility fees now rival material costs for non-recyclable formats, doubling landed prices and accelerating interest in refillable systems. Transparent PET now earns lower fees than dark variants, challenging prestige firms that relied on opaque black to signal luxury. Early movers in Germany and the Netherlands report faster line-qualification approvals from retailers, securing priority shelf space ahead of laggards.[3]Quadpack Industries, “Market Insights 2025,” QUADPACK.COM

Surge in Refillable and Reusable Formats

Refillable packaging represented 15% of new European cosmetic launches in 2025, nearly double 2023 levels. France’s AGEC law mandates a 10% refillable share by weight by 2027, spurring magnetic-closure compacts and twist-lock lipstick cases that accept in-store or subscription cartridges. Gerresheimer’s modular glass jar lets consumers keep an outer shell and replace an inner liner, cutting 60% of material over five cycles. Economics work best for high-turnover creams depleted within three months, while low-usage eye shadow struggles to recoup the initial premium. Limited retail refill stations under 20% of European drugstores restrain uptake outside urban hubs, so brands embed NFC chips to reward repeat refills and maintain engagement.[4]Cosmetics Europe, “Industry Survey 2025,” COSMETICSEUROPE.EU

E-commerce Led Demand for Protective Aesthetics

Online sales rose to 28% of European cosmetic revenue in 2025, positioning packaging as a damage-prevention and brand-story medium. Dimensional-weight pricing pushes nested tube-and-carton designs that shrink void space. AptarGroup’s 2025 pump line locks during transit and cut leakage-related returns that once accounted for 12% of e-commerce complaints. Custom-printed interiors, magnetic boxes, and QR-linked tutorials now replace shelf visibility. Glass needs moulded corrugated inserts costing an extra USD 0.12 per unit but have dropped breakage to below 1%. Tamper-evident seals and serialized labels also deter counterfeits rising on third-party marketplaces.

Gen-Z Preference for Minimalist Mono-Material Designs

Consumers aged 18-27 supplied 31% of 2025 spend, with 68% ranking recyclability over ornate aesthetics. Brands are eliminating secondary cartons for tubes, trimming material outlay up to 20%. Mono-material polyethylene tubes avoid multi-resin EPR penalties and improve curb side stability. Quadpack’s 2025 lipstick case achieved 40% higher recycling rates than metal-plastic hybrids in German pilots. Clear polypropylene compacts with limited printing broadcast ingredient transparency that resonates with this cohort. Luxury houses must now balance legacy opulence with minimalist expectations to safeguard brand equity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Differential for Bio-Based Polymers | -0.40% | Pan-European, with acute pressure in price-sensitive segments across Spain, Italy, Eastern Europe | Medium term (2-4 years) |

| Intra-EU rPET Supply Shortages | -0.30% | Germany, France, Netherlands, Belgium (high-demand markets) | Short term (≤ 2 years) |

| Energy Price Volatility Impacting Glass Furnaces | -0.20% | Glass production hubs in Germany, France, Czech Republic, Poland | Short term (≤ 2 years) |

| Escalating EPR Fees for Non-Recyclable Formats | -0.20% | Germany, France, Netherlands, Belgium, with gradual rollout to Southern and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High-Cost Differential for Bio-Based Polymers

Bio-based polyethylene and polypropylene traded 20-35% above fossil alternatives during 2025, limiting uptake to premium brands able to absorb the gap. The region’s bio-plastic capacity sits below 80 000 t annually, so broader adoption would outstrip supply if more than 15% of converters switch simultaneously. Processing windows are tighter, driving scrap rates three points higher during line changeovers. Regulatory clarity on mass-balance accounting will not arrive until late 2026, postponing volume commitments. Consumer willingness to pay an 8-12% green premium fails to fully offset converter cost increases, making multi-year offtake contracts essential to close the margin gap.

Intra-EU rPET Supply Shortages

Demand exceeded available cosmetic-grade rPET by roughly 45 000 t in 2025 as beverage bottlers secured priority access to collected flake. Converters imported bales from Turkey and the United Kingdom, adding 12-18% to landed resin costs. German deposit-return systems recover 92% of bottles yet channel most material back to beverages, leaving cosmetic suppliers undersupplied. Chemical recycling capacity remains below 30 000 t, and early output is contracted to food bottles needing highest purity. Brands hedge by locking multi-year rPET contracts at fixed premiums or trailing aluminium and glass to avoid PET altogether, though these substitutes bring weight and breakage trade-offs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Regulatory Pressure Spurs Compostable Uptake

In the European cosmetic packaging market, plastics accounted for 43.26% of the material revenue in 2025. This dominance is attributed to its versatility, cost-effectiveness, and widespread use across various cosmetic product categories. Glass, benefiting from its infinite recyclability and premium appeal, secured about 22% of the market share. It remains a preferred choice for fragrances and high-end creams, where aesthetics and sustainability are key considerations.

Forecasted to grow at a rate of 3.34% CAGR, bio-degradable and compostable resins are set to expand the fastest. These materials are gaining traction as brands proactively address environmental concerns and prepare for potential microplastic bans. By securing EN 13432-certified supply contracts, companies are ensuring compliance with stringent regulations while promoting sustainable practices. This shift is steering the European cosmetic packaging industry towards a more diverse range of feedstocks, reducing dependency on traditional materials. Aluminum tubes, with an impressive 76% collection rate, solidify their significance in both sunscreen and color cosmetic segments. Their high recyclability and durability make them a reliable choice for brands aiming to meet sustainability goals. Suppliers showcasing multi-material agility, capable of transitioning from plastic to glass without the need for new tooling, gain a crucial edge as Extended Producer Responsibility (EPR) fees become more stringent. This adaptability allows them to cater to evolving market demands while minimizing operational disruptions

By Product Type: Flexible Pouches Rise on Parcel Economics

In 2025, bottles and jars dominated the European cosmetic packaging market, accounting for 29.84% of the revenue. These packaging formats remain popular due to their durability, reusability, and ability to preserve product integrity. Following closely, tubes and sticks made up roughly 24% of the market, highlighting consumers' preference for the portability of creams and balms. The convenience offered by these formats, especially for on-the-go usage, continues to drive their demand.

Flexible pouches and sachets are on the rise, boasting a 3.21% CAGR through 2031. Their lighter weights not only reduce shipping costs but also align with lower carbon targets, making them an attractive option for environmentally conscious brands and consumers. This trend suggests a potential shift in the European cosmetic packaging market's focus towards high-barrier laminates, which offer enhanced protection and sustainability benefits. While pumps and droppers, essential for oxygen-sensitive serums, see robust demand, brands are increasingly leaning towards metal-spring-free designs to simplify recycling and meet sustainability goals. Additionally, decoration services, particularly digital printing, are reaping higher margins as converters assist indie labels in distinguishing themselves in the bustling online marketplace. The ability to offer customized and visually appealing designs has become a key differentiator for brands aiming to capture consumer attention in a competitive digital landscape.

By Cosmetic Type: Hair Care Accelerates on Salon-Quality Shift

In the European cosmetic packaging market, skin care accounted for 34.27% of the market's value in 2025. This dominance is driven by the increasing consumer focus on premium and sustainable packaging solutions, as well as the rising demand for products that cater to specific skin concerns. Meanwhile, color cosmetics captured approximately 26%, bolstered by the rising popularity of refillable palettes among Gen-Z users, who prioritize eco-friendly and customizable options.

Hair care, growing at the fastest pace with a 3.87% CAGR, sees salon-grade treatments transitioning online. This shift is fueled by the convenience of at-home treatments and the growing preference for professional-quality products. It boosts the demand for airless pumps, which help preserve formulas by preventing contamination, and enhances the market share for flexible refill pouches in Europe, which offer both sustainability and cost efficiency. Fragrance brands are turning to solid sticks housed in paper tubes, a move aimed at reducing transport emissions and appealing to environmentally conscious consumers. Additionally, niche segments like men's grooming are opting for minimalist polypropylene, aligning with both cost-effectiveness and sustainability goals. This trend reflects the increasing demand for functional yet eco-friendly packaging solutions in the men's grooming category.

By Distribution Channel: Direct Sales Shape Protective Features

In 2025, indirect retail accounted for 71.59% of the distribution in Europe's cosmetic packaging market. Lines selling directly to consumers are expanding at a 3.55% CAGR. This growth is driving the adoption of tamper-evident seals and QR codes, which not only foster brand loyalty but also support premium pricing. These elements are pivotal in shaping the size of Europe's cosmetic packaging market, emphasizing value over mere volume.

The increasing focus on direct-to-consumer channels is also encouraging brands to invest in innovative packaging solutions that enhance customer experience and ensure product authenticity. Subscription services are opting for standardized bottles to enhance their pick-and-pack efficiency, which helps streamline operations and reduce logistical complexities. Additionally, omnichannel packaging formats, designed for both shelf display and parcel delivery, are helping to reduce SKU proliferation and cut down on inventory costs. These formats are particularly beneficial for brands aiming to maintain consistency across physical and online retail channels, ensuring seamless integration and improved supply chain efficiency.

By Packaging Format: Flexible Gains from Lightweight Incentives

In the European cosmetic packaging market, rigid vessels commanded a 51.35% share in 2025, driven by their durability and ability to preserve product integrity, making them a preferred choice for premium cosmetic brands. Semi-rigid tubes accounted for 28%, offering a balance between aesthetics and material efficiency, which appeals to both manufacturers and consumers seeking visually appealing yet functional packaging solutions.

As refill programs gain traction, aligning with Gen-Z's low-waste principles, flexible formats are set to grow at a 3.42% CAGR. This shift is recalibrating the market size allocations in favor of laminate producers, who are increasingly innovating to meet sustainability demands. Stand-up pouches, now sporting glossy finishes, challenge the notion of flexibles being perceived as inferior by enhancing their visual appeal and shelf presence. Additionally, reduced Extended Producer Responsibility (EPR) fees translate to tangible savings for brand finance teams, further incentivizing the adoption of flexible packaging. Moreover, advancements in barrier parity are increasingly swaying choices away from glass, provided the product chemistry permits, as these improvements ensure product safety and longevity while reducing environmental impact.

By Sustainability Attribute: Recyclability Dominates Base Expectations

In 2025, recyclable packs held a dominant 46.49% share in Europe's sustainability-focused cosmetic packaging market. This highlights the growing consumer and industry preference for environmentally friendly packaging solutions, driven by increasing regulatory pressures and awareness of sustainability goals.

Luxury brands in Paris and Milan are turning to sugar-cane polyethylene, propelling bio-based content containers to a projected 2.91% CAGR. This shift not only enhances the market share of renewable feedstocks in Europe's cosmetic packaging arena but also reflects the strategic efforts of premium brands to align with eco-conscious consumer demands and differentiate themselves in a competitive market. Refillable options account for about 18%, with NFC-enabled components monitoring reuse cycles, providing brands with valuable data on consumer behavior and sustainability practices. Retailers eyeing eco-label rollouts are favoring multi-attribute designs that blend recycled resin with bio-content, giving these designs a competitive edge in procurement. Such designs cater to the dual objectives of meeting sustainability standards and appealing to environmentally conscious consumers, further driving innovation in the cosmetic packaging market.

Geography Analysis

Germany anchored the 2025 Europe cosmetic packaging market with the region’s strictest recycling mandates and 92% PET bottle collection. Domestic converters like Gerresheimer deploy digital printing to service indie labels that demand low minimums. France follows, driven by luxury houses shifting to refillable lipstick cases to meet AGEC requirements. The United Kingdom ranks third as post-Brexit divergence complicates cross-channel compliance for pan-European brands.

Italy and Spain are expanding above the regional average as Mediterranean shoppers select artisanal products in aluminium tubes and paperboard cartons, which boosts flexible and compostable adoption rates. Scandinavian countries lead refill-system pilots, aided by carbon-pricing policies that incentivize lightweight mono-material formats. Eastern Europe attracts capacity investments because labour savings offset longer transport routes, supporting localized supply for Western demand.

Regulatory heterogeneity persists, with Germany enforcing tougher recycled-content thresholds, France emphasizing reusability, and the United Kingdom initiating unique EPR fee structures. Converters with modular lines capable of quick resin or closure swaps secure continental contracts, demonstrating that agility underpins share gains in a fragmented policy landscape.

Competitive Landscape

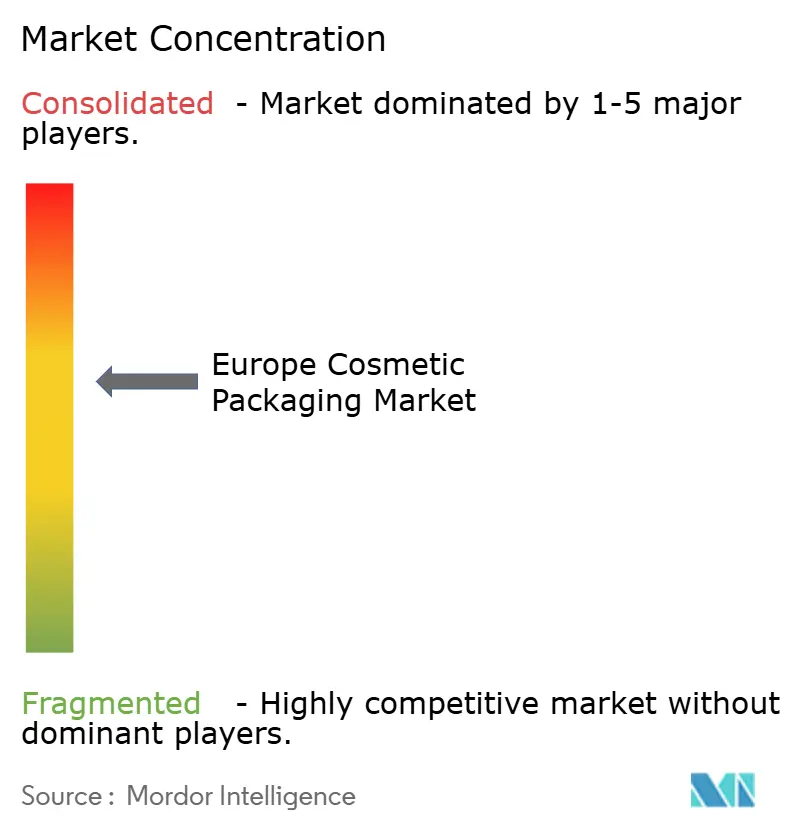

The top five converters held roughly 38% of 2025 revenue, indicating moderate concentration inside the Europe cosmetic packaging market. Amcor’s 2025 acquisition of a Polish flexible plant secures rPET access and accelerates mono-material tube rollouts. AptarGroup launched an airless pump using 50% recycled polypropylene to meet premium serum needs.

Mid-tier players like Quadpack and Coverpla specialize in refillable systems and on-demand 3D-printed closures that big suppliers find hard to scale profitably, carving out niches with indie brands. Digital printing halves lead times from 12 to six weeks in German and Dutch plants, a critical win when direct-to-consumer labels chase trend cycles.

Emerging startups test seaweed films and mycelium closures for ultra-premium lines yet remain subscale. Patent filings prioritize mono-material pumps and NFC-enabled tamper seals, signalling that traceability and design-for-recycling will define the next competitive frontier.

Europe Cosmetic Packaging Industry Leaders

Amcor PLC

Albéa Group

Hcp Packaging Co., Ltd.

AptarGroup Inc.

Cosmopak

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Marchesini Group showcased integrated powder filling lines for cosmetics at Pharmintech in Milan and reaffirmed its USD 1.13 billion revenue ambition.

- March 2025: Calaso partnered with ESTAL to broaden access to 100% recycled glass packaging for small and mid-sized beauty brands.

- January 2025: Venator raised titanium dioxide pigment prices by EUR 300 per tonne across Europe, Africa, and the Middle East, citing sustained energy cost pressures.

- November 2024: PSB Industries completed the Quadpack-Texen combination to create the fifth-largest global cosmetic packaging manufacturer.

Europe Cosmetic Packaging Market Report Scope

The Europe Cosmetic Packaging Market Report is Segmented by Material Type (Plastic, Glass, Metal, Paper and Paperboard, Bio-Degradable/Compostable), Product Type (Bottles and Jars, Tubes and Sticks, Folding Cartons, Pump, Dispenser and Droppers, Caps, Closures and Applicators, Flexible Pouches and Sachets), Cosmetic Type (Skin Care, Hair Care, Color Cosmetics, Fragrances, Other Cosmetic Types), Distribution Channel (Direct Sales, Indirect Sales), Packaging Format (Rigid, Semi-Rigid, Flexible), Sustainability Attribute (Recyclable, Reusable/Refillable, Bio-Based Content ≥30%, Compostable), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Plastic |

| Glass |

| Metal |

| Paper and Paperboard |

| Bio-Degradable/Compostable |

By Product Type

| Bottles and Jars |

| Tubes and Sticks |

| Folding Cartons |

| Pump, Dispenser and Droppers |

| Caps, Closures and Applicators |

| Flexible Pouches and Sachets |

By Cosmetic Type

| Skin Care |

| Hair Care |

| Color Cosmetics |

| Fragrances |

| Other Cosmetic Types |

By Distribution Channel

| Direct Sales Channel |

| Indirect Sales Channel |

By Packaging Format

| Rigid |

| Semi-Rigid |

| Flexible |

By Sustainability Attribute

| Recyclable |

| Reusable/Refillable |

| Bio-Based Content ?30 % |

| Compostable |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Material Type | Plastic |

| Glass | |

| Metal | |

| Paper and Paperboard | |

| Bio-Degradable/Compostable | |

| By Product Type | Bottles and Jars |

| Tubes and Sticks | |

| Folding Cartons | |

| Pump, Dispenser and Droppers | |

| Caps, Closures and Applicators | |

| Flexible Pouches and Sachets | |

| By Cosmetic Type | Skin Care |

| Hair Care | |

| Color Cosmetics | |

| Fragrances | |

| Other Cosmetic Types | |

| By Distribution Channel | Direct Sales Channel |

| Indirect Sales Channel | |

| By Packaging Format | Rigid |

| Semi-Rigid | |

| Flexible | |

| By Sustainability Attribute | Recyclable |

| Reusable/Refillable | |

| Bio-Based Content ?30 % | |

| Compostable | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How fast is packaging demand growing for hair care in Europe cosmetic packaging?

Hair-care applications are projected to expand at a 3.87% CAGR through 2031 as salon-quality treatments shift online and require airless pumps and refill pouches.

Which sustainability attribute dominates current European cosmetic packs?

Recyclability leads with 46.49% of sustainability share in 2025 as mechanical recycling systems for PET, glass, and aluminum are well established.

Why are flexible pouches gaining traction among beauty brands?

Lightweight pouches cut shipping costs, meet low-carbon targets, and align with refill programs, posting a 3.21% CAGR through 2031.

What regulation is driving material redesign in Europe cosmetic packaging?

The EU Packaging and Packaging Waste Regulation mandates all cosmetic packages be recyclable or reusable by 2030 and sets recycled-content thresholds for PET bottles.

Which countries hold the largest share of Europe cosmetic packaging spending?

Germany, France, and the United Kingdom together accounted for more than half of 2025 regional revenue.

What is the main restraint on bio-based polymer adoption?

Bio-polyethylene and polypropylene still cost 20-35% more than fossil grades, limiting use to premium brands unless multi-year supply contracts offset the gap.

Page last updated on: