Canada Combine Harvesters Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.01 Billion |

| Growth Rate (2026 - 2031) | 4.00% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Combine Harvesters Market Analysis by Mordor Intelligence

The Canada combine harvesters market size is projected to expand from USD 0.81 billion in 2025 to USD 0.83 billion in 2026 and further to USD 1.01 billion by 2031, registering a 4.0% CAGR between 2026 and 2031. Farm consolidation on the prairies, immediate-expensing tax policy, and autonomous-ready machinery are reshaping replacement cycles and pushing average machine power above 450 horsepower. Labor shortages, 28,200 unfilled positions in 2024[1]Source: Government of Canada, “CIMM – Labour Shortages,” https://www.canada.ca, raise demand for 45- to 50-foot headers that close harvest windows shortened by wildfire smoke and early frost. Precision-agriculture bundles, now standard on premium models, add significantly to per-unit costs yet deliver rapid payback within a short period through optimized input usage. Prairie operators continue to dominate purchases as they replace aging Class 8 and 9 fleets with autonomous-ready Class 10 platforms capable of harvesting wider swaths in a single pass. Competitive intensity remains elevated despite high market concentration, as leading suppliers compete to integrate telematics and autonomy features that lock customers into proprietary upgrade ecosystems.

Key Report Takeaways

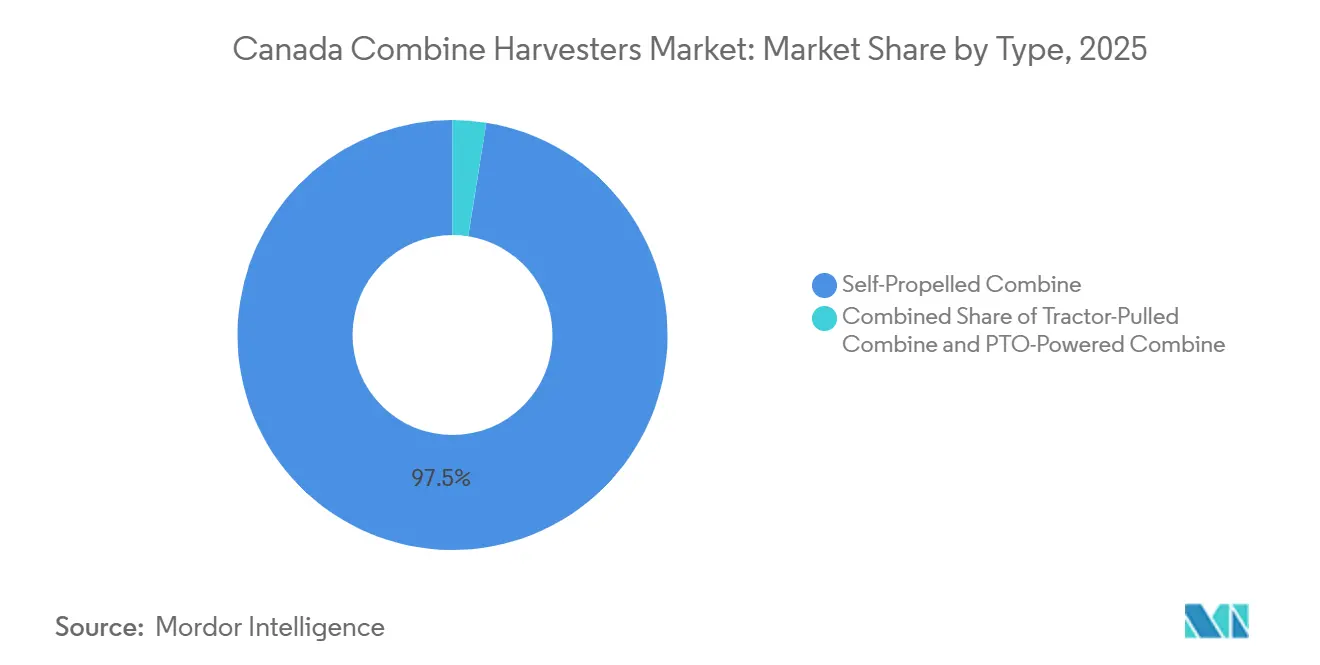

- By type, self-propelled combine harvesters dominated the Canada combine harvesters market size, accounting for 97.5% share in 2025, while PTO-powered combine harvesters are projected to grow at the fastest CAGR of 4.2% during 2026–2031.

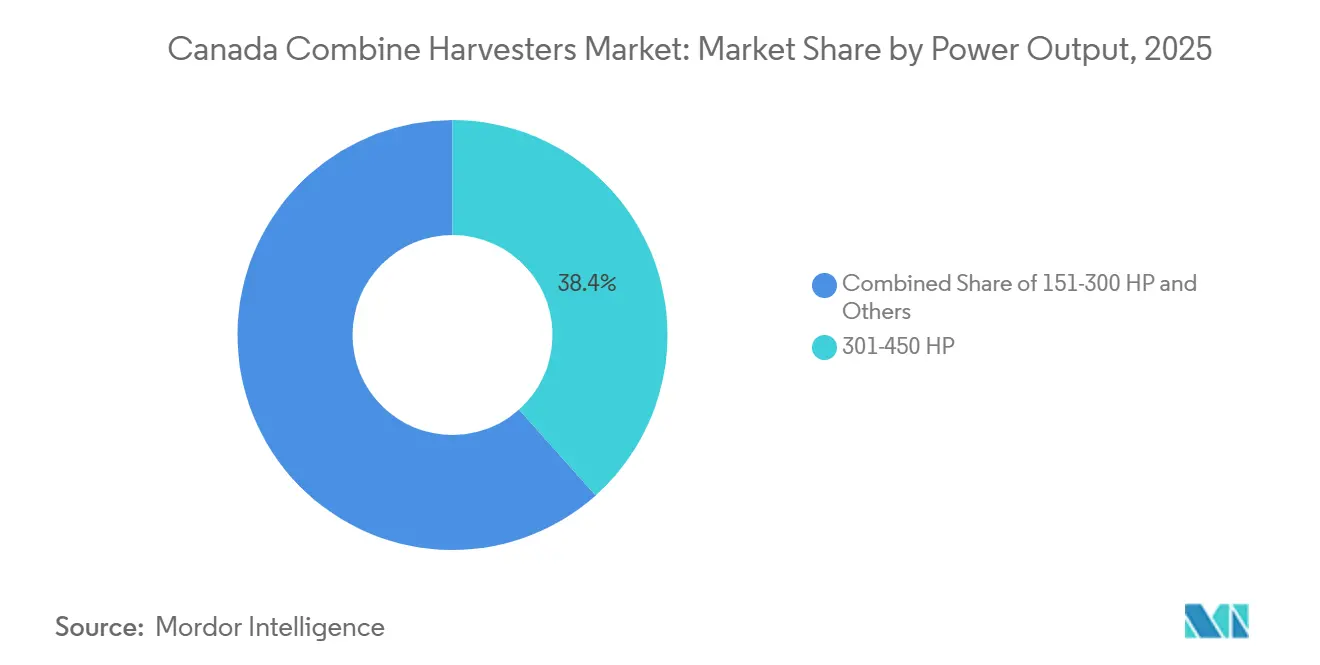

- By power output, 301–450 HP machines led with a 38.4% of Canada combine harvesters market share in 2025, whereas above 450 HP combine harvesters are estimated to register the fastest CAGR of 6.5% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Combine Harvesters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet-replacement cycle on consolidated prairie farms | + 1.20% | Saskatchewan, Manitoba and Alberta with spillover to Ontario | Medium term (2–4 years) |

| Precision-agriculture adoption | + 0.90% | National, strongest in the prairies and Ontario corn belt | Long term (≥4 years) |

| Federal financing incentives | + 0.70% | National, concentrated in the prairies | Short term (≤2 years) |

| Labor shortages driving greater than 45-foot header demand | + 0.60% | Prairies, emerging in Quebec mixed farms | Medium term (2–4 years) |

| Combine-as-a-service contractor models | + 0.40% | Saskatchewan and Alberta, expanding to Manitoba | Long term (≥4 years) |

| Autonomous-ready retrofit momentum | + 0.50% | Prairie early adopters, Ontario following | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fleet-Replacement Cycle on Consolidated Prairie Farms

Larger acreages accelerate the replacement cycle of high-horsepower machines, creating a predictable demand pulse every 10–12 years. Average prairie farm size climbed to 1,784 acres in 2024[2]Source: Statistics Canada, “Census of Agriculture,”, https://www.statcan.gc.ca, concentrating grain output among fewer operators who run multiple combine harvesters to cover 5,000–8,000 acres each season. Engine-hour thresholds fall faster under those workloads, and most owners trade Class 8 or 9 combine harvesters once operating hours exceed 2,500, to avoid drivetrain failures during harvest. The current 2024–2026 window is the tail end of a replacement cycle that began with the 2013–2014 grain-price spike, and immediate expensing rules accelerated buying by cutting after-tax costs about 25%. Deferred maintenance during the pandemic kept some fleets alive, smoothing replacements into 2027. Trade-in values for 2015-vintage models fell significantly in 2025 as buyers pursued factory-fresh, tax-advantaged units. Dealers benefit from predictable secondary-market inventory, while OEMs lock future service revenue through extended-warranty packages. The dynamic underpins steady demand even as total farm counts drift lower.

Precision-Agriculture Adoption

Connected sensors have shifted from optional to mandatory on premium combine harvesters. Deere’s 2026 S7 ships with HarvestLab 3000 NIR sensors that capture protein and moisture data in real time and feed them to Operations Center analytics, which then recommend variable-rate inputs for the next crop year. Case IH FieldOps overlays yield data on satellite imagery to pinpoint underperforming zones, enabling growers to tweak seeding density and hybrid choice before the following season. Adoption rates were significantly higher among farms with more than 2,000 acres in 2024, spurred by lender requirements. Farm Credit Canada conditions loans above USD 500,000 on evidence of data-driven management[3]Source: Canadian Agricultural Policy Institute, “Digital Agriculture Adoption in Canada,” Capi-Icpa.ca. University of Saskatchewan trials show a 4.2% yield lift when seeding prescriptions follow combine maps, driving ROI within two seasons. Operators buying premium technology bundles pay more per unit but gain faster payback through fuel and input savings. As data ecosystems mature, software subscriptions create high-margin recurring revenue for OEMs. The connectivity imperative also raises switching costs, reinforcing brand loyalty.

Federal Financing Incentives

Budget 2024 introduced 100% immediate expensing for eligible equipment, letting Canadian-controlled private corporations deduct the entire cost of a combine harvester in year one rather than over eight years. At a combined tax rate, a major equipment purchase yields substantial after-tax savings. The rule triggered a surge in fourth-quarter orders, with a significant share of deals citing immediate expensing as the primary driver. Although the cap sunsets after 2027, the incentive pulled forward replacements, lowering average fleet age and embedding newer, tech-heavy models in the installed base. Dealers booked record early-delivery schedules, but the policy may depress subsequent orders as front-loaded demand normalizes. Still, the tax benefit has reset farmer expectations around viable engine-hour retirement thresholds.

Labor Shortages Driving Greater Than 45-Foot Header Demand

Canada recorded 28,200 unfilled agricultural jobs in 2024, with grain farms posting a 14.7% vacancy rate. Operators compensate by choosing 45- to 50-foot draper headers that cut acreage per pass and let a single driver cover more ground. Linamar Corporation subsidiary MacDon increased the share of 45-foot-plus headers in its Canadian shipments, reflecting a clear shift toward wider cutting widths. Farms adopting wide headers are able to complete harvest faster, freeing equipment for custom-harvest work and improving cash flow. The trend is also visible in mixed farming regions where labor shortages persist. However, wider headers require greater operator skill to maintain cut quality at higher speeds. To address this, OEMs are bundling automation features such as header-height and lateral-tilt control, supporting adoption despite workforce constraints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost and interest rates | −0.8% | National, acute in Ontario and Quebec where debt-to-asset exceeds 18% | Short term (≤2 years) |

| Commodity-price volatility | −0.6% | Prairies and Ontario corn belt | Medium term (2–4 years) |

| Rural 5G coverage gaps limiting telematics | −0.3% | Saskatchewan, Alberta and Northern Ontario | Long term (≥4 years) |

| Wildfire-smoke induced downtime | −0.2% | Western provinces and Manitoba | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Interest Rates

Average Class 9 combine prices have risen significantly in recent years, driven by precision agriculture bundles, advanced engine standards, and higher input costs such as steel and electronics. Meanwhile, the Bank of Canada’s 3.75% policy rate holds equipment-loan rates at 6.5%–7.2% for strong credits and up to 9.8% for borrowers with high leverage[4]Source: Bank of Canada, “Interest Rates and Bond Yields,” Bankofcanada.ca. Mid-size farms are particularly affected, as they face affordability constraints while also encountering high contractor costs. As a result, some operators are delaying purchases until financing conditions improve, which is softening near-term demand despite continued buying by larger farms. OEM financing programs offer some flexibility, but higher overall carrying costs continue to limit new equipment adoption.

Wildfire-Smoke Induced Downtime

Western Canada logged 12 consecutive days above 150 µg/m³ PM2.5 in 2024, exceeding safe thresholds for combined engines and operators[5]Source: Environment and Climate Change Canada, “Wildfire Smoke and Air Quality Health Index,” Canada.ca. Farmers are replacing air filters more frequently than standard intervals, increasing maintenance requirements and operating costs per machine. Lost field days force either higher-moisture harvests, leading to additional drying expenses, or unharvested acreage that results in significant financial losses. Climate trends indicate more frequent smoke events, prompting OEMs to develop enhanced filtration and cooling systems that add cost and complexity with uncertain returns. As a result, downtime pressures return on investment and reduce near-term upgrade appetite, particularly among smaller growers with limited flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Self-Propelled Dominance Anchors Value

Self-propelled combine harvesters seized a commanding 97.5% share of the Canada combine harvesters market size in 2025, dwarfing tractor-pulled units and PTO-powered machines that together held the remaining share. Their dominance is driven by the ability to cover 150–200 acres per day on prairie farms, far exceeding the 40–60 acres achieved by tractor-pulled variants. Tractor-pulled combine harvesters persist in small mixed operations across Quebec and Ontario, while PTO machines remain a micro-niche in dairy-grain holdings where lower purchase cost is prioritized over speed.

PTO-powered combine harvesters are estimated to grow at a 4.2% CAGR through 2031, driven by their low entry cost, while tractor-pulled models lag as custom harvesting services reduce demand. Autonomous-ready self-propelled platforms are projected to expand steadily, supported by retrofit solutions that enable one operator to manage multiple machines. Dealers report increasing inclusion of automation-ready wiring in self-propelled sales, indicating continued momentum in the premium segment.

By Power Output: High-Horsepower Machines Lead Value and Growth

Combine harvesters in the 301–450 horsepower class controlled the largest 2025 slice at 38.4%, followed by units rated above 450 horsepower, with the 151–300 horsepower tier next, and sub-150 horsepower models accounting for the smallest share. Mid-power Class 7 and 8 machines appeal to farms of moderate size that must balance header width with maneuverability under road limits. High-power Class 9 and 10 platforms are gaining traction on large prairie operations seeking wider headers to manage operational delays.

Above-450-horsepower combine harvesters are set to rise fastest at a 6.5% CAGR through 2031, supported by tax incentives that improve the affordability of high-value equipment. The 301–450 horsepower segment follows, driven by upgrades linked to precision agriculture features. The 151–300 horsepower class shows steady growth due to continued demand from mixed farming operations, while sub-150 horsepower models remain stagnant as regulatory compliance increases costs and limits adoption.

Geography Analysis

Prairie Provinces contributed the majority of the 2025 Canada combine harvesters market value, reflecting their dominance in national grain and oilseed acreage. Saskatchewan accounted for the largest share of national combine sales, supported by extensive cropland availability and large average farm sizes. Manitoba followed with its diversified crop mix, while Alberta maintained a significant share despite operational disruptions from wildfire smoke delays.

Ontario represented a moderate share of demand, driven by extensive corn and soybean cultivation, smaller field sizes, and a high reliance on custom harvesters. Quebec accounted for a smaller portion amid dairy-grain rotations that extend combine replacement cycles, while Atlantic Canada maintained limited demand centered on cereal production in Prince Edward Island. British Columbia’s Peace River region contributed a niche share, favoring tracked undercarriages for hilly terrain conditions.

Regional growth through 2031 is estimated to remain strongest in Saskatchewan due to pulse-crop expansion and increasing adoption of autonomous harvesting technologies, followed by Manitoba. Alberta is projected to witness comparatively slower growth due to smoke and water constraints. Ontario is anticipated to record steady growth supported by soybean and corn equipment upgrades, while Quebec and Atlantic Canada are estimated to advance at a more moderate pace. OEMs continue optimizing inventory management and service hub networks around prairie regions to meet rapid parts and maintenance requirements from large-scale harvesting contractors.

Competitive Landscape

The market is concentrated yet fiercely innovative. Deere & Company leads the market, leveraging advanced hardware integrated with cloud-based platforms that connect equipment into a unified data ecosystem. CNH Industrial N.V. follows with a dual-brand strategy, offering differentiated machines for large-scale and mixed farming operations. AGCO Corporation maintains its position through partnerships focused on autonomous retrofit solutions that lower adoption barriers.

Claas KGaA mbH strengthens its presence with high-performance machines designed for challenging field conditions, while Kubota Corporation expands through strategic alliances, offering cost-competitive alternatives to premium models. Other players such as SDF Group, Rostselmash Group, Mahindra & Mahindra Ltd., Yanmar Holdings Co., Ltd., Gomselmash OJSC, and Weichai Lovol Intelligent Agricultural Technology CO., LTD contribute to competitive diversity across price and performance segments. Disruptors, including Tribine Industries, Inc., along with niche equipment providers like Wintersteiger AG and ALMACO, target specialized and technology-driven segments.

Competition is increasingly shifting toward uptime guarantees, digital integration, and subscription-based revenue models rather than just machine performance. Advanced diagnostic platforms help reduce downtime and improve operational efficiency, while compliance with industry standards favors established players. As automation evolves, software ecosystems are estimated to deepen customer lock-in and reinforce the dominance of leading companies.

Canada Combine Harvesters Industry Leaders

AGCO Corporation

CLAAS KGaA mbH

Kubota Corporation

CNH Industrial N.V.

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Deere & Company announced updates to its X9 and S7 combine harvesters, integrating advanced automation features that optimize machine settings and ground speed in real time using sensors and predictive technologies. These enhancements improve harvesting efficiency, with the development also supporting adoption in markets such as Canada, where large-scale harvesting solutions are increasingly required.

- March 2025: AGCO Corporation and Trimble’s PTx Trimble OutRun autonomous grain-cart retrofit received the Davidson Prize, highlighting advancements in autonomous harvesting technology. The solution enables a single operator to manage both combine and grain cart operations, improving efficiency and reducing labor dependency in large-scale farming.

- January 2025: Deere & Company. committed USD 48 million to renovate 385,000 square feet of manufacturing space at its Harvester Works facility, along with an additional USD 101 million in advanced equipment and processes to support X9 combine production. This investment enhances capacity for high-performance harvesters, aligning with demand in Canada, where large-scale farms require high-throughput, wide-header machines for efficient harvesting.

Canada Combine Harvesters Market Report Scope

Combine harvesters are agricultural machines designed to efficiently harvest, thresh, separate, and clean grain crops.

The Canada Combine Harvesters Market Report is segmented by type, including self-propelled combine, tractor-pulled combine, and PTO-powered combine, and by power output, including less than 150 HP, 151–300 HP, 301–450 HP, and above 450 HP. The market forecasts are provided in USD.

| Self-Propelled Combine |

| Tractor-Pulled Combine |

| PTO-Powered Combine |

| Less Than 150 HP |

| 151- 300 HP |

| 301- 450 HP |

| Above 450 HP |

| By Type | Self-Propelled Combine |

| Tractor-Pulled Combine | |

| PTO-Powered Combine | |

| By Power Output | Less Than 150 HP |

| 151- 300 HP | |

| 301- 450 HP | |

| Above 450 HP |

Key Questions Answered in the Report

How large is the Canada combine harvesters' market in 2026?

The Canada combine harvesters market size is estimated at USD 0.83 billion in 2026, on track to reach USD 1.01 billion by 2031 at a 4.0% CAGR .

Which power output leads combine sales in Canada?

The 301–450 HP machines led with a 38.4% of Canada combine harvesters market share in 2025 due to balanced power and efficiency.

What is the fastest combine harvester type segment?

PTO-powered combine harvesters are projected to grow at the fastest CAGR of 4.2% during 2026–2031, driven by low cost and accessibility.

Why are prairie provinces dominant buyers?

Saskatchewan, Manitoba, and Alberta command the majority of spending due to their concentration of grain and oilseed acreage and large-scale farming operations that justify high-horsepower equipment.

Page last updated on: