Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

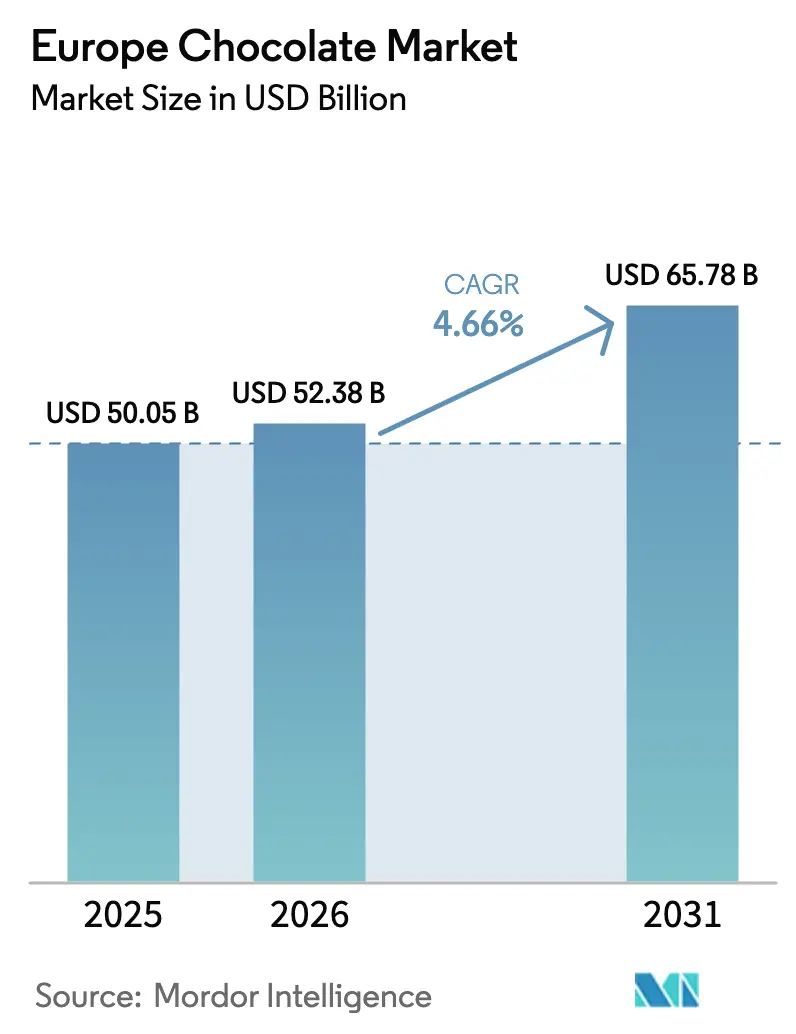

| Base Year Market Size (2025) | USD 50.05 Billion |

| Market Size (2026) | USD 52.38 Billion |

| Market Size (2031) | USD 65.78 Billion |

| Growth Rate (2026 - 2031) | 4.66% CAGR |

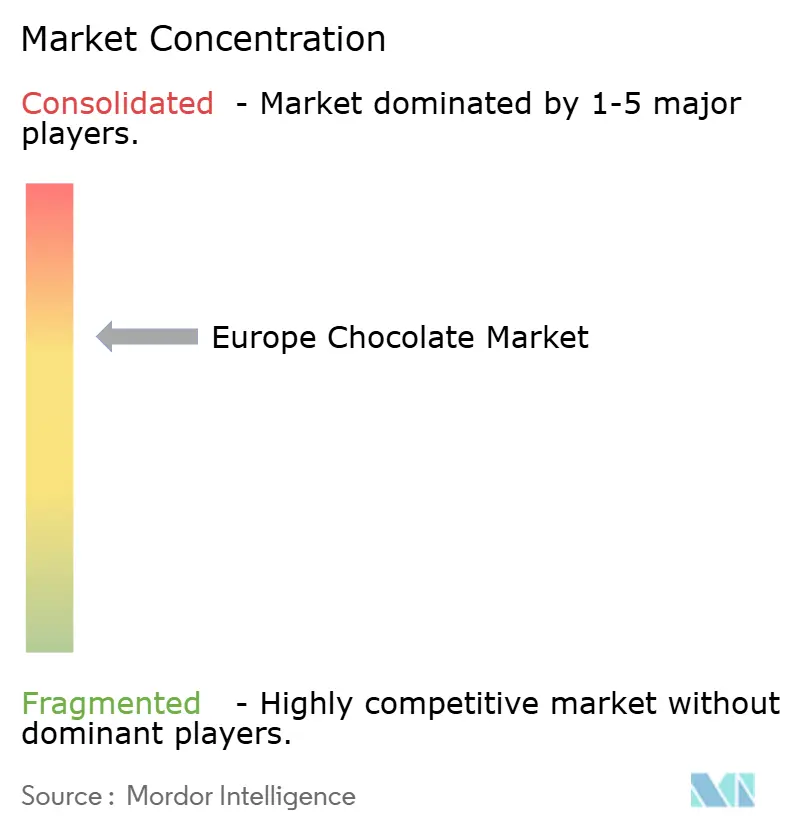

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Chocolate Market Analysis by Mordor Intelligence

The Europe Chocolate Market was valued at USD 50.05 billion in 2025 and is projected to grow from USD 52.38 billion in 2026 to USD 65.78 billion by 2031, registering a CAGR of 4.66% during the period 2026-2031. This growth indicates a shift in the market, with chocolate evolving from a traditional indulgence product to a premium, purpose-driven offering that aligns with modern consumer preferences. Manufacturers are focusing on higher cocoa content, reduced sugar, clean-label formulations, and functional benefits to meet consumer demand for healthier options, emphasizing attributes such as antioxidant content and lower glycemic impact. Additionally, sustainability, ethical sourcing, and supply chain transparency have become essential for building consumer trust and supporting premium pricing strategies. The market is further influenced by ingredient and flavor innovations, as brands explore new textures, sensory experiences, and alternative raw materials to maintain consumer interest in a mature market.

Key Report Takeaways

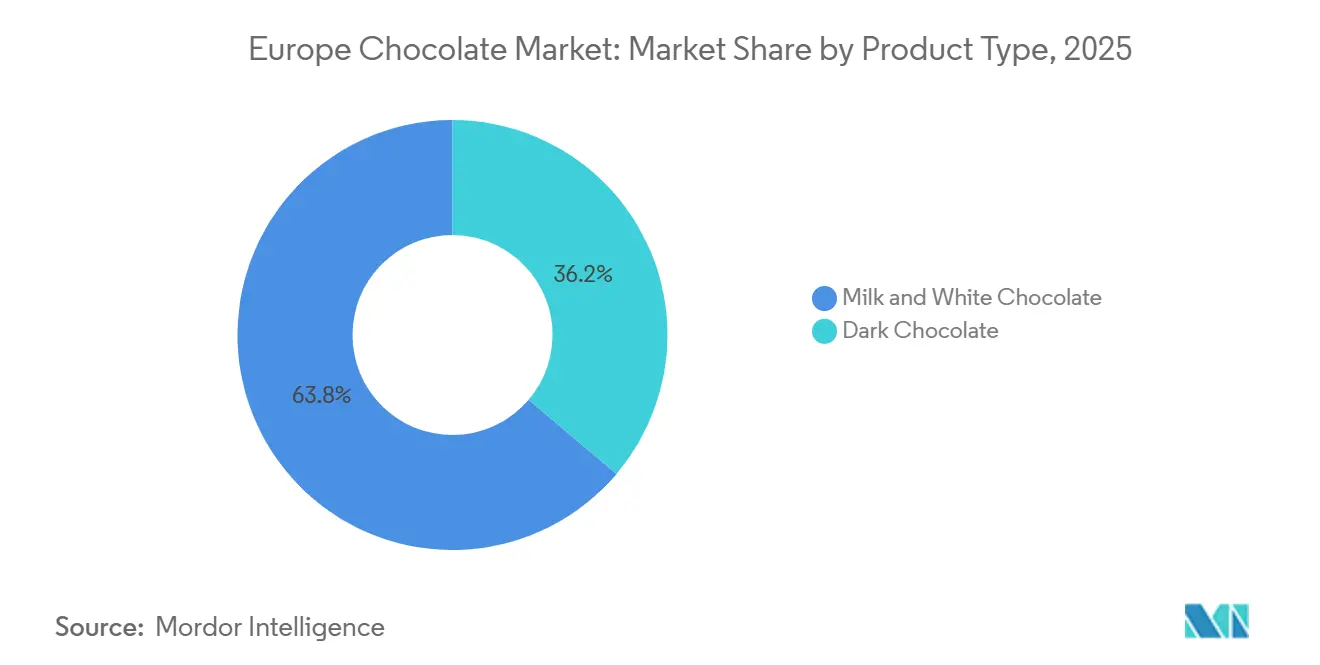

- By product type, milk and white chocolate captured 63.81% of the Europe chocolate market share in 2025; dark chocolate is advancing at a 5.23% CAGR to 2031.

- By form, tablets and bars commanded 49.09% of the Europe chocolate market size in 2025, while pralines and truffles recorded the fastest growth at a 4.71% CAGR through 2031.

- By price range, the mass tier held a 77.23% share in 2025, while premium chocolate posted the highest forecast growth at a 6.23% CAGR.

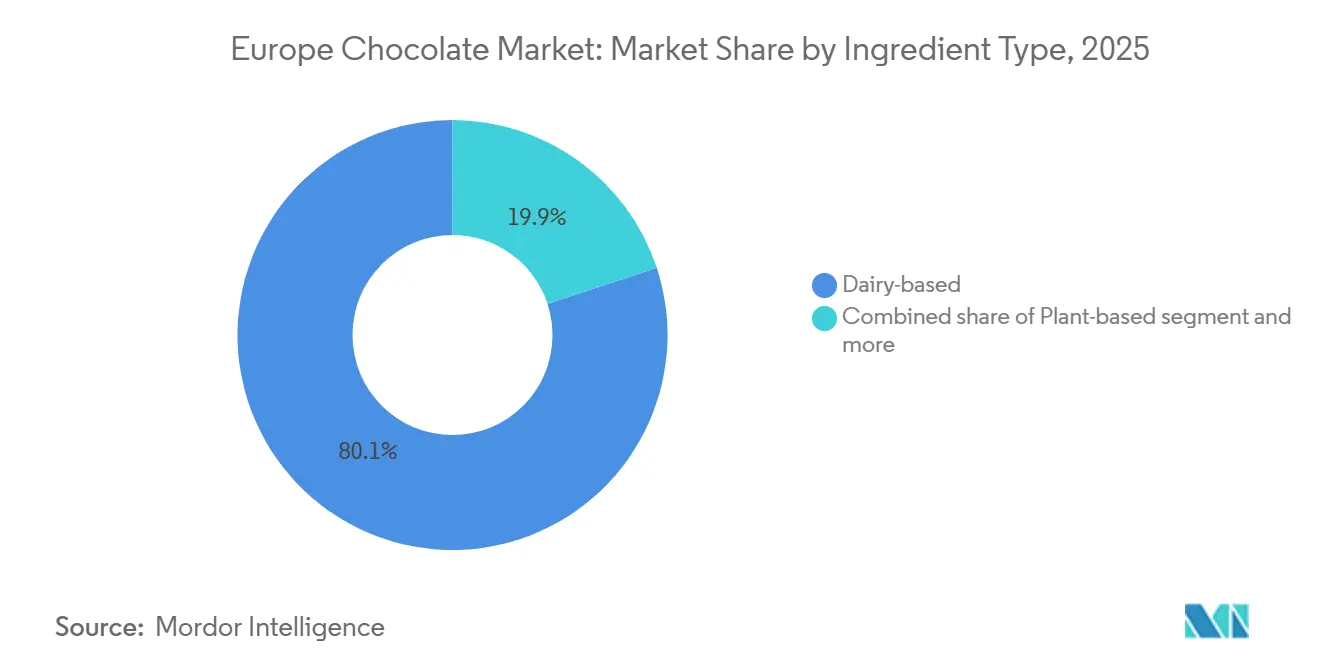

- By ingredient type, dairy-based variants dominated with 80.07% share in 2025, whereas plant-based chocolate is projected to grow at a 6.42% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 42.78% of sales in 2025, while online retail is expected to grow at a CAGR of 7.05% through 2031.

- By geography, the United Kingdom led with 24.52% revenue share in 2025, whereas Spain is forecast to expand at a 6.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and wellness trends | +0.8% | Western Europe (United Kingdom, Germany, France), with spillover to Nordics | Medium term (2-4 years) |

| Seasonal and cultural consumption patterns | +0.4% | Global, with peaks in Belgium, Switzerland, United Kingdom during Easter and Christmas | Short term (≤ 2 years) |

| Flavor and ingredient innovation | +0.6% | Urban centers across Germany, France, United Kingdom; early adoption in Scandinavia | Medium term (2-4 years) |

| Ethical and sustainable sourcing | +0.7% | Northern Europe (Netherlands, Germany, United Kingdom), expanding to Southern Europe | Long term (≥ 4 years) |

| Craft and single-origin chocolate trend | +0.5% | France, United Kingdom, Germany; emerging in Spain, Italy | Medium term (2-4 years) |

| Personalization and customization | +0.3% | E-commerce hubs in United Kingdom, Germany, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health and wellness trends

Health and wellness trends are emerging as a significant driver of growth in the chocolate market, influencing product development and consumer preferences across key markets. Manufacturers are increasingly adjusting their product portfolios to include polyphenol-rich dark chocolates and sugar-reduced formulations. This shift aligns with the growing consumer perception that higher cocoa content and reduced sugar intake offer health benefits, such as cardiovascular support and improved glycemic control. This trend highlights a broader movement toward functional indulgence, where consumers seek products that not only deliver taste and indulgence but also promote overall well-being. For example, health-conscious consumers are showing a strong preference for dark chocolates with higher cocoa percentages, organic certifications, and clean-label ingredients. In response, manufacturers are innovating with fortified chocolates, portion-controlled options, sugar alternatives, and enhanced formulations to meet evolving consumer demands.

Seasonal and cultural consumption patterns

Seasonal and cultural consumption patterns are significant structural drivers of the European chocolate market, deeply rooted in regional traditions and social practices. Chocolate holds a prominent role in major festive occasions such as Christmas, Easter, and Valentine’s Day, where gifting and shared consumption substantially boost demand across both mass-market and premium segments. In countries like the United Kingdom, Germany, France, and Italy, seasonal chocolate products, including Easter eggs, Advent calendars, and limited-edition gift boxes, are integral to celebration traditions, leading to predictable annual demand surges. Manufacturers align product launches, packaging innovations, and promotional campaigns with these calendar-driven events to ensure sustained sales momentum beyond regular consumption. Additionally, cultural norms surrounding hospitality, gifting, and indulgence further reinforce chocolate’s position as a socially accepted and emotionally significant treat, particularly in Western Europe.

Flavor and ingredient innovation

Flavor and ingredient innovation is becoming a significant growth driver in the European chocolate market, as manufacturers adapt to changing consumer demands for sustainability, novelty, and functional differentiation. European consumers are increasingly looking for unique taste experiences, alternative ingredients, and environmentally sustainable formulations, encouraging chocolate producers to go beyond traditional cocoa-based recipes. Innovations now include exotic flavor infusions, hybrid textures, reduced-sugar formulations, and alternative raw materials, allowing brands to stand out in a mature and competitive market. For example, in November 2025, Barry Callebaut partnered with cocoa-free chocolate start-up Planet A Foods, reflecting the industry's strategic move toward ingredient diversification. Planet A Foods’ ChoViva brand offers a cocoa-free chocolate alternative made from locally sourced crops such as sunflower seeds, addressing concerns related to cocoa supply volatility, sustainability, and climate risks. This collaboration highlights how innovation is expanding beyond flavor enhancement to redefine the fundamental composition of chocolate.

Ethical and sustainable sourcing

Ethical and sustainable sourcing is a significant growth driver in the European chocolate market, as consumers place greater emphasis on environmental responsibility, social impact, and transparency within the cocoa value chain. European buyers are increasingly aware of issues such as deforestation, child labor, fair farmer compensation, and climate resilience. This has led chocolate manufacturers to adopt certified and traceable sourcing practices as part of their core strategies. The trend is particularly evident in the United Kingdom, where consumer awareness of ethical certifications is well established. According to the Centre for the Promotion of Imports (CBI), Rainforest Alliance has the highest certification brand awareness in the United Kingdom at 58%, highlighting the impact of sustainability labels on purchasing decisions [1]Source: Promotion of Imports (CBI), "The European market potential for certified cocoa", cbi.eu. Consequently, chocolate producers are increasingly utilizing certifications such as Rainforest Alliance, Fairtrade, and organic labels to build consumer trust, strengthen brand credibility, and support premium pricing. Additionally, sustainable sourcing contributes to long-term supply security, enabling manufacturers to address risks associated with climate change and regulatory requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw material prices and supply risks | -0.9% | Global, with acute impact on Western Europe (Germany, United Kingdom, France) | Short term (≤ 2 years) |

| Stringent regulatory and compliance burdens | -0.6% | Europe-wide, with disproportionate impact on SMEs in Belgium, Netherlands, Italy | Medium term (2-4 years) |

| Supply chain disruptions | -0.4% | United Kingdom (Brexit-related), Southern Europe (logistics bottlenecks) | Short term (≤ 2 years) |

| Consumer skepticism over ingredients | -0.3% | Northern Europe (Germany, Netherlands, Scandinavia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile raw material prices and supply risks

Volatile raw material prices and supply risks pose a significant challenge to the European chocolate market, as cocoa procurement remains highly vulnerable to climatic, geopolitical, and structural issues in major producing regions. Cocoa prices have shown sharp fluctuations due to factors such as extreme weather events, climate change-induced yield variability, crop diseases, aging cocoa trees, and chronic underinvestment in West African farms, which collectively account for the majority of global cocoa production. These disruptions limit supply availability and increase input costs for chocolate manufacturers, thereby compressing profit margins and reducing pricing flexibility, particularly for mass-market and mid-range product segments. Furthermore, increased regulatory pressure in Europe regarding deforestation-free supply chains, traceability requirements, and sustainability compliance adds to sourcing complexity and cost burdens. Smaller manufacturers and private-label producers are especially affected, as they have limited hedging capabilities and weaker negotiating power compared to multinational companies.

Stringent regulatory and compliance burdens

Stringent regulatory and compliance requirements present a significant challenge for the European chocolate market, as manufacturers must navigate one of the most complex and dynamic food regulatory landscapes globally. Chocolate producers in Europe are required to adhere to strict food safety regulations, labeling requirements, nutritional disclosures, and ingredient usage standards, including rules related to allergens, sugar content, additives, and novel ingredients. Additionally, compliance obligations increasingly extend to areas such as sustainability, traceability, and ethical sourcing, influenced by frameworks like deforestation-free supply chain regulations, due diligence requirements, and stricter scrutiny of cocoa sourcing practices. These regulatory demands lead to higher compliance costs, increased documentation efforts, reformulation expenses, and longer time-to-market, particularly for functional, fortified, or plant-based chocolate products, which must meet stringent health and nutrition claim substantiation standards. Smaller and mid-sized manufacturers face greater challenges due to limited regulatory expertise and financial resources, while larger companies must continuously adapt their product portfolios to comply with varying regulations across multiple European jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Chocolate Gains on Health Pivot

Milk and white chocolate maintain a dominant position in the European chocolate market, accounting for approximately 63.81% of total sales. This reflects strong consumer preferences and established brand equity. The dominance is primarily attributed to the taste familiarity and broad acceptance of milk chocolate, whose creamy, smooth, and balanced flavor profile appeals to a wide demographic, including children, adults, and the elderly. Cultural traditions and seasonal consumption patterns, such as Christmas gifting, Easter chocolate eggs, and other European holidays, further reinforce its popularity due to its mild and universally liked taste. Additionally, major brands continue to innovate within this segment by introducing value-added variants, such as caramel-filled, nut-enhanced, and fortified milk chocolates, catering to both indulgence-seeking and health-conscious consumers.

Dark chocolate is emerging as one of the fastest-growing segments in the European chocolate market, with a projected CAGR of 5.23% through 2031. This growth reflects a shift in consumer preferences toward healthier and premium indulgences. The increasing health consciousness among European consumers drives this trend, as dark chocolate is associated with benefits such as antioxidants, cardiovascular support, and lower sugar content compared to milk chocolate. Furthermore, the premiumization trend significantly contributes to this growth, with consumers willing to pay higher prices for high-cocoa, single-origin, or artisanal dark chocolate products that offer unique taste experiences and a sense of sophistication.

By Form: Tablets Dominate but Pralines Premiumize

Tablets and bars hold a significant share of 49.09% in the European chocolate market, underscoring their sustained popularity and widespread consumer appeal. This segment's dominance is largely attributed to its versatility and convenience. Tablets and bars are easy to consume, portion, and share, making them suitable for everyday snacking, gifting, and on-the-go consumption. Consumers are drawn to the extensive variety of flavors, textures, and fillings available in this format, ranging from classic milk chocolate bars to options with nuts, caramel, or fruit infusions, catering to diverse taste preferences and fostering consumer loyalty. Additionally, their affordability and widespread availability across supermarkets, hypermarkets, convenience stores, and online platforms ensure high accessibility, further solidifying their market leadership.

Pralines and truffles are among the fastest-growing segments in the European chocolate market, with a projected CAGR of 4.71% through 2031. This growth is primarily fueled by their premium and gifting appeal, as these products are often associated with luxury, craftsmanship, and indulgence. European consumers increasingly seek high-quality, artisanal chocolate experiences, and pralines and truffles meet this demand by offering rich flavors, innovative fillings, and visually appealing designs. The segment also benefits from the strong gifting culture and seasonal occasions such as Christmas, Valentine’s Day, and Easter, during which premium boxed assortments are highly favored.

By Price Range: Mass Market Holds Volume, Premium Captures Value

Mass-market chocolate continues to lead the European chocolate market, accounting for 77.23% of total sales in 2025. This dominance is driven by its widespread accessibility, affordability, and consistent consumer demand. The segment appeals to a broad demographic by offering everyday indulgence at competitive price points, ensuring high consumption volumes across various age groups. Established brands play a significant role in this dominance, leveraging long-standing recognition and trust among European consumers. These brands provide familiar flavors, textures, and packaging that align with traditional consumption habits. Additionally, mass-market chocolate benefits from extensive distribution networks, ensuring strong availability and visibility throughout the region.

Premium chocolate is witnessing significant growth in the European market, with a projected CAGR of 6.23% through 2031. This growth is fueled by increasing consumer preference for high-quality, indulgent, and artisanal products. Unlike mass-market chocolate, premium offerings cater to consumers seeking unique taste experiences, superior ingredients, and sophisticated branding. These products often feature single-origin cocoa, higher cocoa content, or innovative flavor combinations. The segment also benefits from the growing culture of gifting and seasonal indulgence, with premium assortments, truffles, and specialty bars being popular choices for occasions such as Christmas, Valentine’s Day, and other European festivals. Furthermore, health-conscious trends have supported the segment's growth, as consumers increasingly view high-cocoa dark or minimally processed chocolates as a more wholesome indulgence, combining enjoyment with potential antioxidant benefits.

By Ingredient Type: Dairy Dominates, Plant-Based Surges

In 2025, dairy-based chocolate maintains its leading position in the European chocolate market, accounting for a substantial 80.07% share of total sales. This dominance is attributed to its widespread consumer familiarity, creamy texture, and versatile taste profile. The segment appeals to a wide consumer base due to its balanced sweetness and smooth texture, making it a popular choice for everyday snacking, gifting, and indulgence. Historical consumption patterns, strong brand recognition, and the extensive availability of classic milk chocolate products across supermarkets, hypermarkets, convenience stores, and online retail platforms further reinforce its market leadership. Additionally, manufacturers continue to innovate within this category by introducing variations such as nut-filled, caramel, flavored, or fortified chocolates, which sustain consumer interest and drive repeat purchases.

Plant-based chocolate is emerging as one of the fastest-growing segments in the European chocolate market, with a projected CAGR of 6.42% through 2031. This growth is driven by increasing health consciousness and ethical awareness among European consumers. Many consumers are seeking alternatives to traditional dairy-based products due to lactose intolerance, dietary preferences, or environmental concerns, leading to a rising demand for vegan and plant-based chocolates made from ingredients such as almond, oat, soy, and coconut milk. The segment's growth is further supported by the trend of premiumization, as manufacturers offer high-quality, ethically sourced plant-based chocolate options that align with the gifting and indulgence culture prevalent in Europe.

By Distribution Channel: Supermarkets Anchor, Online Accelerates

In 2025, supermarkets and hypermarkets continue to dominate the European chocolate market, accounting for 42.78% of total sales. This dominance is attributed to their extensive reach, wide product variety, and convenience for consumers. These retail formats provide easy access to a broad range of chocolate products, including mass-market, premium, and specialty offerings, making them a preferred choice for both everyday purchases and seasonal shopping. Strategic store layouts, high product visibility, and promotional campaigns further enhance consumer engagement and encourage impulse purchases. Additionally, supermarkets and hypermarkets utilize volume discounts, loyalty programs, and festive merchandising to appeal to both price-sensitive and premium-seeking buyers.

Online retail is emerging as the fastest-growing distribution channel in the European chocolate market, with a projected CAGR of 7.05% through 2031. This growth is driven by rapid digital adoption and changing consumer shopping behaviors. European consumers increasingly value the convenience, variety, and personalized experiences offered by e-commerce platforms, enabling them to browse, compare, and purchase chocolates from their homes. For example, according to the European Commission, 94% of individuals in Europe used the internet during the first three months of 2025, underscoring the widespread digital connectivity supporting online shopping growth [2]Source: European Commission, "E-commerce statistics for individuals", ec.europa.eu. Moreover, online retail allows chocolate brands to offer exclusive products, seasonal assortments, and premium or plant-based options that may not be available in traditional stores, attracting niche and premium-focused consumers.

Geography Analysis

The United Kingdom remains a key driver of European chocolate demand, accounting for 24.52% of the market share in 2025. This leadership is attributed to high consumer engagement, extensive retail penetration, and a well-established chocolate culture that emphasizes both everyday consumption and premium indulgence. United Kingdom consumers prioritize variety, quality, and innovation, prompting manufacturers to introduce new flavors, limited editions, and premium variants. Seasonal events such as Christmas, Easter, and Valentine’s Day further bolster the United Kingdom's contribution to European chocolate sales, with gifting and festive indulgence playing a crucial role in maintaining demand.

Spain is projected to be Europe’s fastest-growing chocolate market, with a CAGR of 6.91% through 2031. This growth reflects changing consumer behaviors and a rising interest in premium and specialty chocolates. Factors such as increasing urbanization, expanding retail networks, and the growing popularity of indulgent and health-focused chocolate options, including dark, single-origin, and plant-based varieties, are driving this trend. Spanish consumers are increasingly open to new formats and flavors, while promotional campaigns and seasonal gifting trends are further boosting consumption. This rapid growth positions Spain as a significant opportunity for chocolate manufacturers aiming to expand their presence in Southern Europe.

Germany, France, and Italy collectively account for a substantial share of European chocolate consumption, supported by strong cultural ties to chocolate and well-developed retail infrastructures. In Germany, approximately 9.09 million people purchased chocolate in 2024, according to IfD Allensbach, underscoring the country’s stable consumer base and consistent demand [3]Source: IfD Allensbach, "Number of people in Germany who bought chocolates", ifd-allensbach.de. France and Italy also exhibit strong consumption patterns, driven by traditional chocolate culture, premium gifting practices, and widespread availability in supermarkets, convenience stores, and specialty outlets. While these markets are mature, innovations in flavors, packaging, and ethical sourcing continue to sustain consumer interest and incremental growth, reinforcing their importance within Europe’s chocolate market.

Competitive Landscape

The European chocolate market is moderately concentrated, with a few multinational companies holding a significant share. Key players such as Mondelez International Inc., Ferrero International SpA, Mars, Incorporated, Nestlé S.A., and Chocoladefabriken Lindt & Sprüngli AG leverage their strong brand equity, extensive distribution networks, and diverse product portfolios to maintain their leadership in both mass-market and premium segments. These companies focus on product innovation, marketing initiatives, and strategic partnerships to meet consumer demand and foster loyalty in the mature European market.

Market competition is driven by innovation, premiumization, and consumer engagement. Leading companies differentiate themselves through unique flavor offerings, seasonal and limited-edition products, and high-quality packaging, catering to both everyday consumption and gifting occasions. Additionally, there is a growing emphasis on ethical sourcing and sustainability initiatives, such as Fairtrade and Rainforest Alliance certifications. These efforts not only enhance brand reputation but also align with increasing consumer demand for environmentally and socially responsible products. This strategic focus enables established brands to defend their market share while addressing competition from emerging local and niche chocolate manufacturers.

While established players dominate, the European chocolate market offers opportunities for innovation and new entrants. Functional chocolates, such as those infused with probiotics, collagen, or adaptogens, are gaining popularity among health-conscious consumers. However, regulatory clarity on health claims in this segment remains limited, providing room for differentiation. Similarly, personalized gifting solutions, supported by AI-driven flavor-matching algorithms and customizable packaging, are becoming increasingly popular as consumers seek unique and experiential products. By capitalizing on these trends, both established companies and startups can tap into high-growth niches, driving incremental market expansion and gaining competitive advantages in this moderately concentrated market.

Europe Chocolate Industry Leaders

-

Mondelez International Inc.

-

Ferrero International SpA

-

Mars, Incorporated

-

Nestlé S.A.

-

Chocoladefabriken Lindt & Sprüngli AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Ritter Sport launched four new chocolate varieties in Morrisons in the United Kingdom. The lineup includes Roasted Peanut, Caramel & Biscuit, as well as Duo variants, Sweet n Salty Duo and Coffee Duo.

- September 2025: Lindt & Sprüngli has introduced a new range of chocolate bars in the United Kingdom. The Les Grandes Fruit & Nut bar features premium ingredients, including roasted hazelnuts and raisins.

- July 2025: Cadbury introduced two new dark chocolate bars: Bournville Salted Caramel and Bournville Chopped Hazelnut. These additions enhanced the classic Bournville range by offering new textures and flavors, appealing to consumers seeking a contemporary variation of dark chocolate.

- May 2024: Arla Foods has entered into a licensing agreement with Mondelēz International to produce, distribute, and market chocolate milk under the Milka brand in Germany, Austria, and Poland.

Europe Chocolate Market Report Scope

The chocolate market encompasses the global industry involved in the production, distribution, and sale of chocolate products derived from cocoa beans. The chocolate market is segmented by product type, form, price range, ingredient type, distribution channel, and geography. Based on product type, dark chocolate, milk, and white chocolate. Based on form, the market is segmented into tablets and bars, molded blocks, pralines and truffles, and other forms. Based on price range, the market is segmented into mass and premium. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

By Product Type

| Dark Chocolate |

| Milk and White Chocolate |

By Form

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

By Price Range

| Mass |

| Premium |

By Ingredient Type

| Dairy-based |

| Plant-based |

| Single Origin |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Convenience Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Ingredient Type | Dairy-based |

| Plant-based | |

| Single Origin | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Online Retail Stores | |

| Convenience Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms