North America Building Information Modelling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

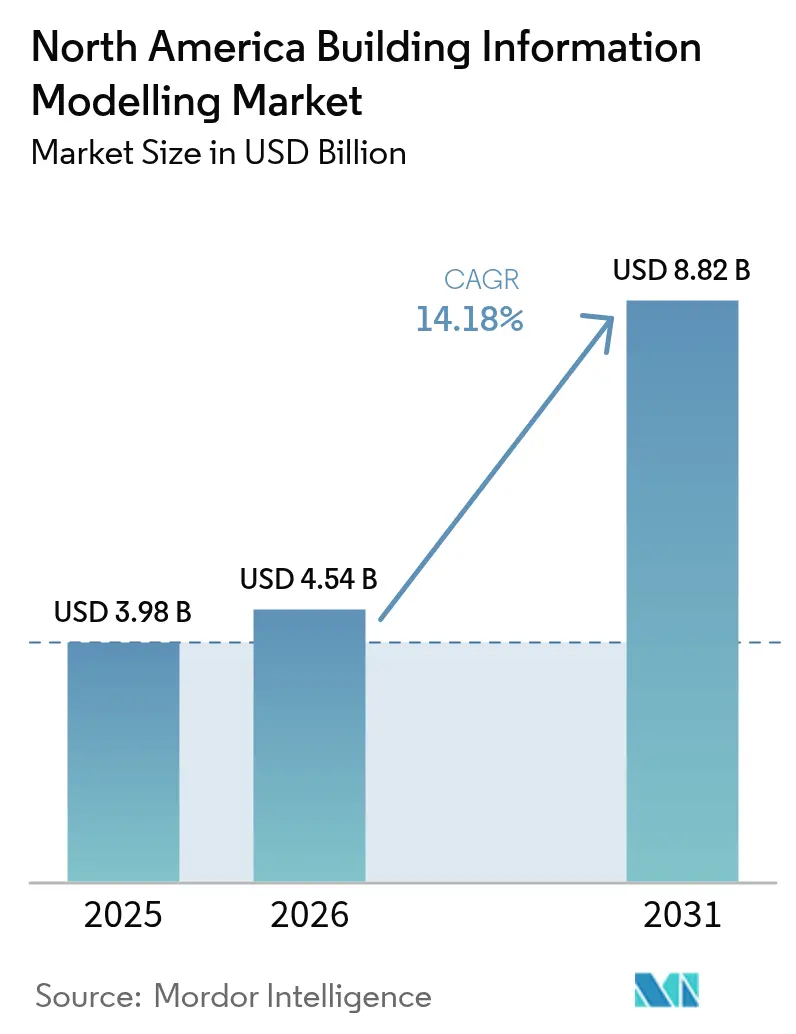

| Base Year Market Size (2025) | USD 3.98 Billion |

| Market Size (2026) | USD 4.54 Billion |

| Market Size (2031) | USD 8.82 Billion |

| Growth Rate (2026 - 2031) | 14.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Building Information Modelling Market Analysis by Mordor Intelligence

The North America Building Information Modelling market size was valued at USD 3.98 billion in 2025 and estimated to grow from USD 4.54 billion in 2026 to reach USD 8.82 billion by 2031, at a CAGR of 14.18% during the forecast period (2026-2031). Robust expansion is rooted in generative AI that automates design tasks, accelerating federal and state BIM mandates, and a push to retrofit existing buildings for decarbonization.[1]National Institute of Building Sciences, “US™ v4 | National Institute of Building Sciences,” nibs.org Cloud-native collaboration tools are widening access for small and medium enterprises, while insurers now offer premium discounts for BIM-centric risk modeling, further boosting adoption. Commercial real estate maintains the largest user base, yet residential construction posts double-digit growth as developers digitize workflows, and Mexico’s infrastructure boom positions the country as the fastest-growing geography.

Key Report Takeaways

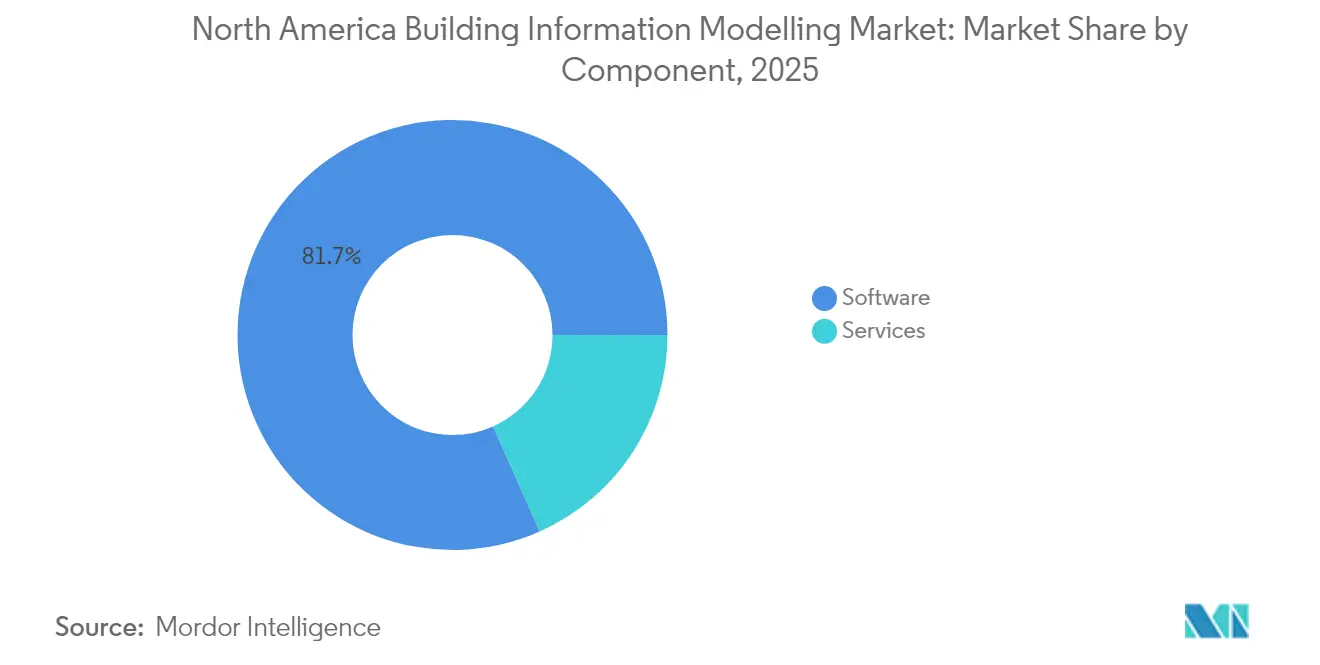

- By component, software led with 81.65% of the North America Building Information Modelling market share in 2025, while services are advancing at a 14.72% CAGR through 2031.

- By deployment mode, on-premise solutions held 63.15% share of the North America Building Information Modelling market size in 2025; cloud platforms exhibit the highest projected CAGR at 15.32% to 2031.

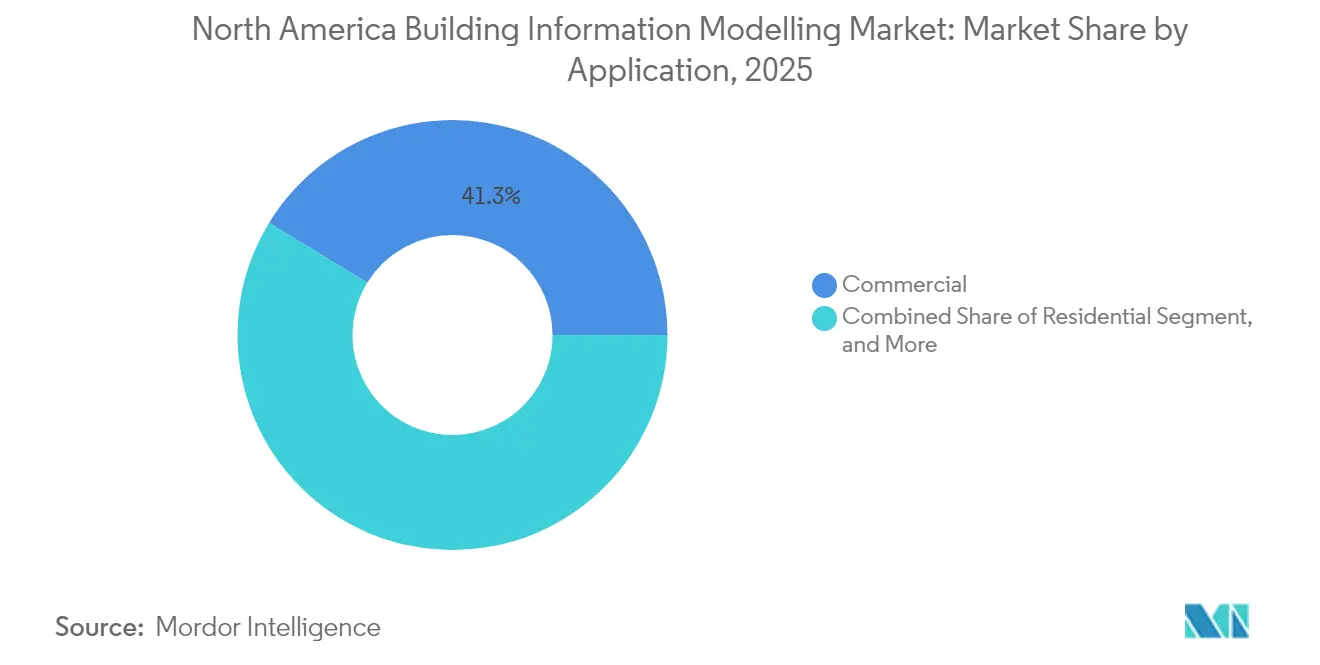

- By application, commercial construction accounted for 41.25% share of the North America Building Information Modelling market size in 2025 and residential projects are rising at a 15.74% CAGR through 2031.

- By project lifecycle phase, pre-construction and design captured 47.05% of the North America Building Information Modelling market share in 2025, whereas operations and maintenance record the steepest CAGR at 15.26% to 2031.

- By geography, the United States commanded an 80.75% share of the North America Building Information Modelling market size in 2025, and Mexico shows the fastest expansion at a 15.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Building Information Modelling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative AI-powered design optimization | +3.2% | United States tech hubs, early adopters in Mexico | Medium term (2-4 years) |

| Government BIM mandates and incentives | +2.8% | United States federal sector, Canadian provinces | Short term (≤ 2 years) |

| Rising retrofit demand for decarbonization | +2.1% | Urban cores across North America | Long term (≥ 4 years) |

| Cloud-native collaboration for SMEs | +2.4% | North American SMEs with spill-over from APAC precedents | Medium term (2-4 years) |

| Insurance premium discounts for BIM models | +1.8% | United States and Canada | Long term (≥ 4 years) |

| Digital-twin convergence with smart-city aid | +2.4% | Municipal programs in United States, Canada and Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generative AI-Powered Design Optimization Accelerates Workflow Automation

Generative AI features embedded in leading BIM tools automatically iterate structural and energy models, cutting project delivery time by up to 30%.[2]M. Zadeh et al., “Exploring BIM Implementation Challenges in Complex Renovation Projects,” MDPI.com Autodesk Forma and Graphisoft Archicad 28 include AI-driven documentation that speeds code checks, a benefit appreciated by 85% of Mexican firms pursuing competitiveness. Machine learning now scans historic project data to recommend material choices that improve energy intensity. Vendors employ cloud inference engines so even small laptops can harness advanced computation. Early adopters report fewer RFIs during construction because clash detection is executed at the concept stage, although firms must budget additional training hours to realize these gains.

Government BIM Mandates Create Compliance-Driven Adoption

The U.S. General Services Administration requires model-based submissions for all major public builds, pushing contractors toward full BIM workflows.[3]U.S. General Services Administration, “3D-4D Building Information Modeling,” gsa.gov Canada’s federal Collaborative Procurement framework sets BIM deliverable thresholds for projects above CAD 5 million. Several states and provinces supplement these rules with tax rebates on documented BIM execution plans, although inconsistent local codes still impose re-work. ISO 19650 alignment in both countries raises documentation quality and accelerates permit reviews. Contractors that cannot meet evolving mandates face exclusion from publicly financed opportunities, driving service demand for compliance audits and model validation.

Rising Retrofit Demand Drives Decarbonization-Focused Applications

North America’s aging building stock now represents a prime target for deep energy retrofits that rely on accurate as-built modeling. Owners use BIM to simulate photovoltaic fit-outs, window replacements, and HVAC overhauls that cut operating emissions. Laser scanning feeds point clouds into BIM tools, yet processing remains labor-intensive, challenging smaller contractors. Lenders increasingly link green finance approval to BIM-derived energy analyses that verify payback. Training programs funded by municipal climate initiatives aim to upskill trades so they can interpret digital models during retrofit execution.

Cloud-Native Collaboration Democratizes SME Access

Cloud platforms remove capital expenditure on high-end workstations, letting small firms subscribe to browser-based model editors that synchronize changes in real time. Surveys show 69% of Revit users are ready to migrate once security concerns are addressed. Data sovereignty questions persist, prompting some owners to mandate domestic data centers. Hybrid architectures are therefore popular, storing sensitive files on-premise while using the cloud for clash detection. Service marketplaces connect SMEs to freelance BIM coordinators, spreading specialist knowledge without full-time hiring costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Training and Cultural Change Costs | -2.1% | Global, particularly affecting SMEs | Short term (≤ 2 years) |

| Fragmented Building Codes Across United States States | -1.4% | US national, state-level variations | Medium term (2-4 years) |

| Cyber-Security Concerns Around Cloud BIM Repositories | -1.8% | North America and EU, cloud-dependent markets | Medium term (2-4 years) |

| IP Ownership Disputes in Multi-Stakeholder Models | -1.2% | Global, complex project environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Training and Cultural Change Costs Constrain SME Adoption

A BIM workstation can cost USD 10,000, while advanced user training surpasses USD 5,000 per employee. Smaller contractors often lack reserves for such outlays, slowing technology penetration beyond tier-one builders. Resistance to new workflows also persists because trades rely on familiar 2D drawings. Professional indemnity complexities arise when multiple parties edit a shared model, prompting legal reviews that add time and expense. Public grants partially offset costs, but many SMEs still prioritize near-term cash flow over digital investment.

Fragmented Building Codes Across United States Create Implementation Complexity

Each U.S. state enforces unique code amendments, forcing architects to configure bespoke BIM templates and rule-sets for compliance. This fragmentation undermines software economies of scale and complicates multi-state projects. Pilot efforts to digitize codes into machine-readable formats remain nascent. Contractors, therefore, maintain parallel execution plans, adding administrative overhead that erodes productivity gains. National standardization would raise BIM efficiency, yet requires coordination among thousands of local permitting bodies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Software Maturation

Software retained 81.65% of the North America Building Information Modelling market share in 2025 and has historically underpinned digital construction workflows. Continuous upgrades, such as AI-driven clash detection, sustain license renewals and support subscriptions. However, services are outstripping software with a 14.72% CAGR because implementation complexity drives organizations to outsource deployment, integration, and training. Consulting engagements range from project-specific modeling to enterprise-wide digital roadmaps, highlighting that technology alone cannot deliver full value.

Demand for tailored education programs illustrates the skills gap that limits internal execution capacity. Certification courses teach ISO 19650 compliance, data exchange protocols, and common data environment governance. Maintenance contracts also expand as owners migrate between on-premise and cloud solutions, requiring vendor-agnostic expertise to preserve data integrity. Consequently, services revenue is projected to narrow the gap with software by 2031, even though licenses will remain the foundation of the North America Building Information Modelling market.

By Deployment Mode: Cloud Acceleration Challenges On-Premise Dominance

On-premise systems still commanded 63.15% of the North America Building Information Modelling market size in 2025 due to established IT policies at large contractors. These environments offer direct control over sensitive intellectual property and integrate smoothly with legacy file servers. Yet cloud platforms are expanding at a 15.32% CAGR, propelled by rising remote collaboration demands and subscription pricing that lowers entry barriers. The hybrid approach, in which companies retain vault storage on-site while using cloud engines for rendering and coordination, is gaining popularity.

Cloud vendors emphasize zero-trust security and regional data centers to address owner concerns. Real-time model federation lets architects, engineers, and builders co-author files, shortening design iterations and reducing errors downstream. Payment flexibility is a compelling draw for SMEs that prefer operating expenses over capital expenditure. Over time, the cost of maintaining physical servers and the talent to administer them is expected to propel further migration toward fully hosted environments.

By Application: Residential Surge Contrasts Commercial Maturity

Commercial projects held 41.25% of the North America Building Information Modelling market size in 2025 and have long utilized digital coordination to manage complex MEP systems. Hospitals and higher education facilities employ BIM to achieve sustainability certifications and operational data handover. Conversely, residential construction posts the fastest 15.74% CAGR as single-family and multi-family developers adopt BIM to mitigate labor shortages and comply with stricter energy codes. Model-based quantity take-off improves budget certainty, appealing to lenders amid elevated borrowing costs.

Industrial and infrastructure sectors also leverage BIM for system-heavy facilities such as factories and rail networks. Mexico’s Tren Maya, for instance, mandates model-based documentation for all stations and track works, creating new opportunities for regional service providers. Public agencies increasingly require BIM for environmental impact assessments, spurring adoption even in smaller municipalities. Growing acceptance across these diverse applications underscores BIM’s versatility throughout North America.

By Project Lifecycle Phase: Operations Growth Reflects Digital Twin Convergence

Pre-construction and design dominated with 47.05% of the North America Building Information Modelling market share in 2025 because early-stage coordination underpins successful delivery. Value engineering, code compliance checks, and stakeholder visualization are well established. Operations and maintenance, however, lead growth at a 15.26% CAGR as owners connect models to sensor networks and facility management systems. Digital twins enable predictive maintenance that reduces downtime and energy consumption, extending BIM’s value beyond handover.

Structured data exchanges such as COBie v3 ease integration with computerized maintenance management systems. Asset owners can track equipment warranties, schedule inspections, and allocate capital budgets based on model intelligence. As the installed base of BIM-enabled assets expands, facility teams invest in cloud dashboards to monitor performance, driving recurring software and analytics revenue. This shift from project to lifecycle mindset marks a pivotal evolution in the North America Building Information Modelling market.

Geography Analysis

The United States accounted for 80.75% of the North America Building Information Modelling market size in 2025, supported by federal mandates that require native and IFC models on public projects. Major private owners also stipulate BIM deliverables, fostering a deep ecosystem of consultants and certified professionals. Despite dominance, state-level code variation hampers uniform workflows and inflates compliance costs.

Canada shows steady advancement backed by its Collaborative Procurement Initiative and the Canadian Practice Manual for BIM that align with ISO 19650. Provincial transport agencies integrate BIM and GIS to manage infrastructure lifecycles, and defense projects demonstrate sophisticated digital twin use cases. Yet inconsistent provincial codes mirror U.S. fragmentation, limiting nationwide economies of scale.

Mexico represents the fastest expansion with a 15.29% CAGR to 2031, driven by nearshoring, data center construction, and flagship infrastructure such as Tren Maya. International developers demand LEED and energy performance documentation that BIM readily supplies. Government entities progressively reference ISO standards for public tenders, bolstering local capacity. Cloud-ready SMEs in Mexico City and Monterrey use subscription software to compete for cross-border projects, signaling lasting momentum.

Competitive Landscape

Market concentration sits at a mid-level as long-standing leaders Autodesk, Bentley Systems, and Trimble continue to dominate core modeling domains while facing nimble challengers. Hexagon’s 2024 acquisition of Voyansi adds geospatial intelligence to its portfolio, and Nemetschek’s 2024 purchase of GoCanvas builds field data acquisition strength.[4]buildingSMART International, “buildingSMART Canada,” buildingsmart.org Bentley’s December 2024 deal for Cesium opens new 3D geospatial visualization avenues, underscoring a race to assemble end-to-end digital construction ecosystems.

AI-native startups target design generation, automated code checking, and energy optimization, often offering browser-based interfaces that reduce IT friction for SMEs. Interoperability remains a strategic differentiator; vendors promoting open standards such as IFC and COBie gain favor on multi-stakeholder projects. Service firms partner with software suppliers to bundle implementation and compliance support, generating holistic value propositions.

Insurers, lenders, and asset owners exert growing influence by embedding BIM deliverables into contracts, reshaping vendor roadmaps toward data transparency and lifecycle analytics. As subscription business models mature, incumbents must balance license revenue with managed services to defend share within the North America Building Information Modelling market. Mergers that streamline compliance, sustainability reporting, and cloud collaboration are likely through the forecast period.

North America Building Information Modelling Industry Leaders

Autodesk Inc.

Bentley Systems Incorporated

Trimble Inc.

Nemetschek SE

Dassault Systèmes SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Autodesk partnered with Nemetschek to enable seamless model exchange between Revit and Archicad, improving multi-vendor collaboration.

- December 2024: Bentley Systems acquired Cesium for USD 60 million, integrating 3D geospatial visualization into infrastructure BIM workflows.

- November 2024: Hexagon bought Voyansi for USD 45 million, enhancing reality capture and digital twin offerings.

- October 2024: Graphisoft released Archicad 28 in Mexico with AI-powered design and sustainability features.

North America Building Information Modelling Market Report Scope

Building information modeling (BIM) is a 3D model-based process for creating and managing information on a construction project across the project lifecycle. The important output of this process are the building information model, which is the digital description of every aspect of the built asset to manage the building infrastructure in a better way.

The scope of the study for the market is categorized into various applications of BIM, commercial, residential, and industrial. Also, the market is segmented by countries, including the United States and Canada.

North America building information modeling market is segmented by type (software, services), by deployment type (on-premise, cloud), by application (commercial, residential, industrial), and by country (United States, Canada). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Software | Design Authoring |

| Model Review and Coordination | |

| Simulation and Analysis | |

| Project Management | |

| Services | Consulting |

| Implementation and Integration | |

| Training and Certification | |

| Support and Maintenance |

| On-Premise |

| Cloud |

| Commercial | Office |

| Retail | |

| Healthcare | |

| Education | |

| Residential | Single-Family |

| Multi-Family | |

| Industrial | Manufacturing |

| Energy and Utilities | |

| Infrastructure | Transportation |

| Public Safety and Government Facilities |

| Pre-Construction/Design |

| Construction |

| Operation and Maintenance |

| United States |

| Canada |

| Mexico |

| By Component | Software | Design Authoring |

| Model Review and Coordination | ||

| Simulation and Analysis | ||

| Project Management | ||

| Services | Consulting | |

| Implementation and Integration | ||

| Training and Certification | ||

| Support and Maintenance | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By Application | Commercial | Office |

| Retail | ||

| Healthcare | ||

| Education | ||

| Residential | Single-Family | |

| Multi-Family | ||

| Industrial | Manufacturing | |

| Energy and Utilities | ||

| Infrastructure | Transportation | |

| Public Safety and Government Facilities | ||

| By Project Lifecycle Phase | Pre-Construction/Design | |

| Construction | ||

| Operation and Maintenance | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America Building Information Modelling market in 2026?

The market stands at USD 4.54 billion in 2026 with a 14.18% CAGR forecast to 2031.

Which segment is growing fastest within North America BIM?

Services are rising at 14.72% CAGR, reflecting demand for implementation, integration and training.

What deployment mode is gaining traction among SMEs?

Cloud platforms are growing 15.32% CAGR as subscription pricing lowers capital barriers and supports remote collaboration.

Why is Mexico the fastest-growing geography for BIM in the region?

Nearshoring, megaprojects like Tren Maya and increasing LEED certification requirements drive a 15.29% CAGR for Mexico through 2031.

How does generative AI influence BIM workflows?

AI automates design iterations, clash detection and documentation, shaving up to 30% from delivery timelines while enhancing energy performance modeling.

What is the main barrier preventing smaller firms from adopting BIM?

High upfront costs for hardware and specialized training, alongside cultural resistance to new workflows, limit SME adoption.

Page last updated on: