Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

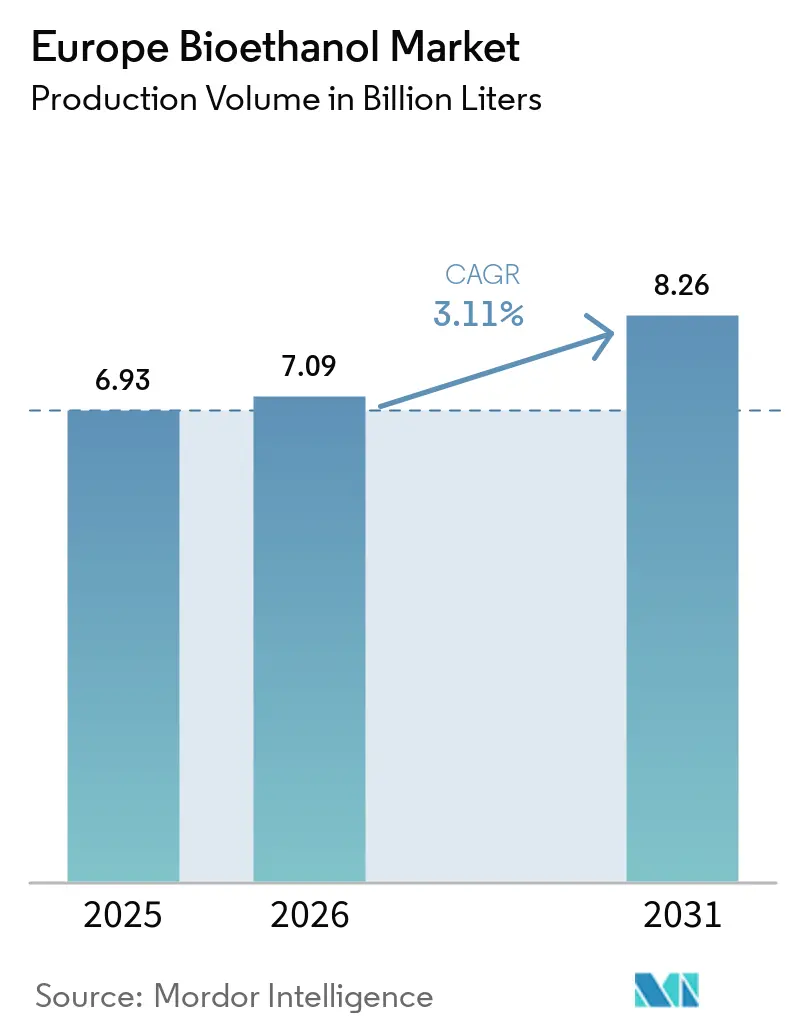

| Base Year Market Size (2025) | 6.93 Billion liters |

| Market Volume (2026) | 7.09 Billion liters |

| Market Volume (2031) | 8.26 Billion liters |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

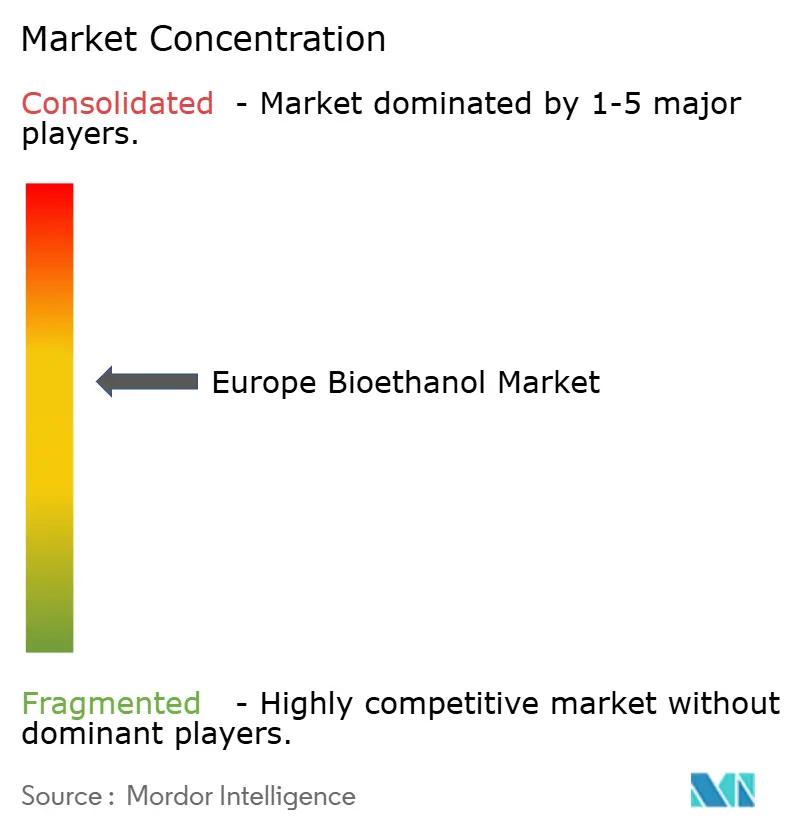

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Bioethanol Market Analysis by Mordor Intelligence

The Europe Bioethanol Market size in terms of production volume is expected to grow from 6.93 Billion liters in 2025 to 7.09 Billion liters in 2026 and is forecast to reach 8.26 Billion liters by 2031 at 3.11% CAGR over 2026-2031.

Robust RED III mandates, broader E10 and E85 adoption, carbon-pricing incentives, and early sustainable-aviation-fuel demand are expanding addressable volumes, although rising electric-vehicle penetration, feedstock-price volatility, and indirect land-use-change compliance temper upside potential.[1]European Commission, “Renewable Energy Directive III,” ec.europa.eu Integrated producers that monetize fermentation CO₂ and protein-rich co-products are widening their margin gap over legacy first-generation plants, while lignocellulosic pathways are moving from demonstration toward commercial scale, positioning second-generation ethanol as a durable value driver.[2]Verbio SE, “Annual Report 2025,” verbio.de Competitive intensity remains elevated because the top five players control just 45% of installed capacity, leaving room for regional specialists to capture premium niches, notably in spirits, pharmaceuticals, and alcohol-to-jet fuel.[3]CropEnergies AG, “Annual Report 2025,” cropenergies.com

Key Report Takeaways

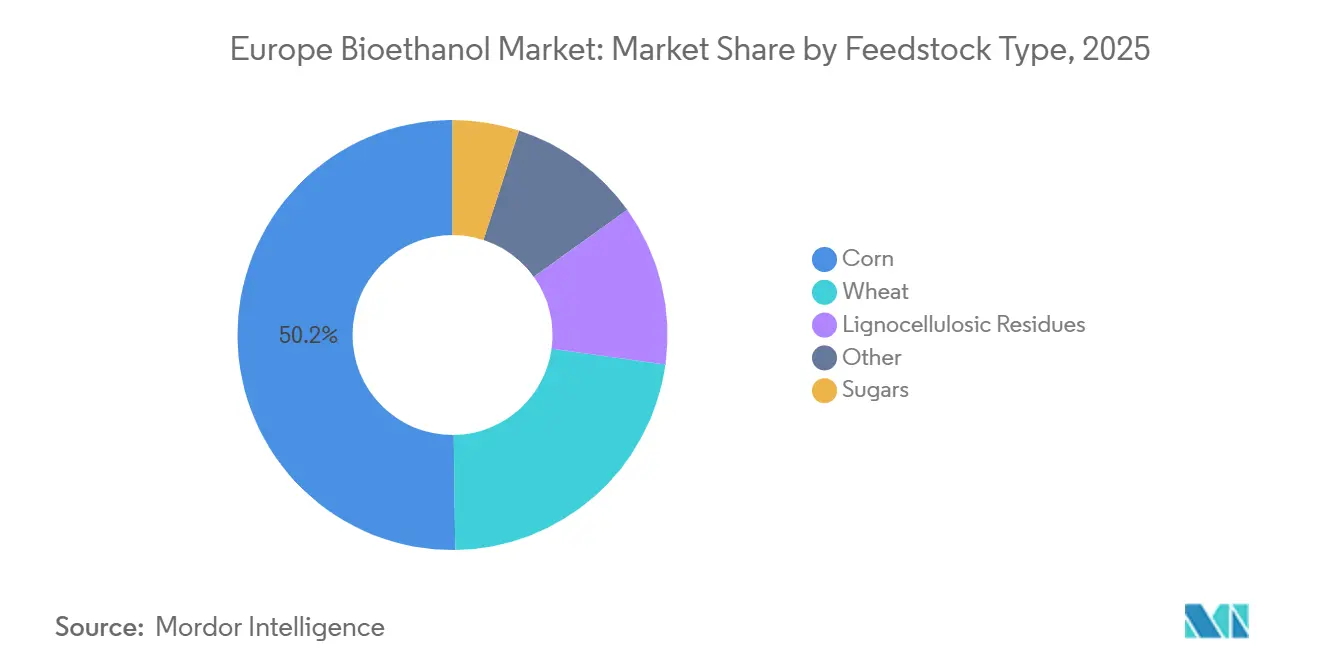

- By feedstock, Corn commanded 50.2% of the European bioethanol market share in 2025, while lignocellulosic residues are forecast to post the fastest 6.2% CAGR through 2031.

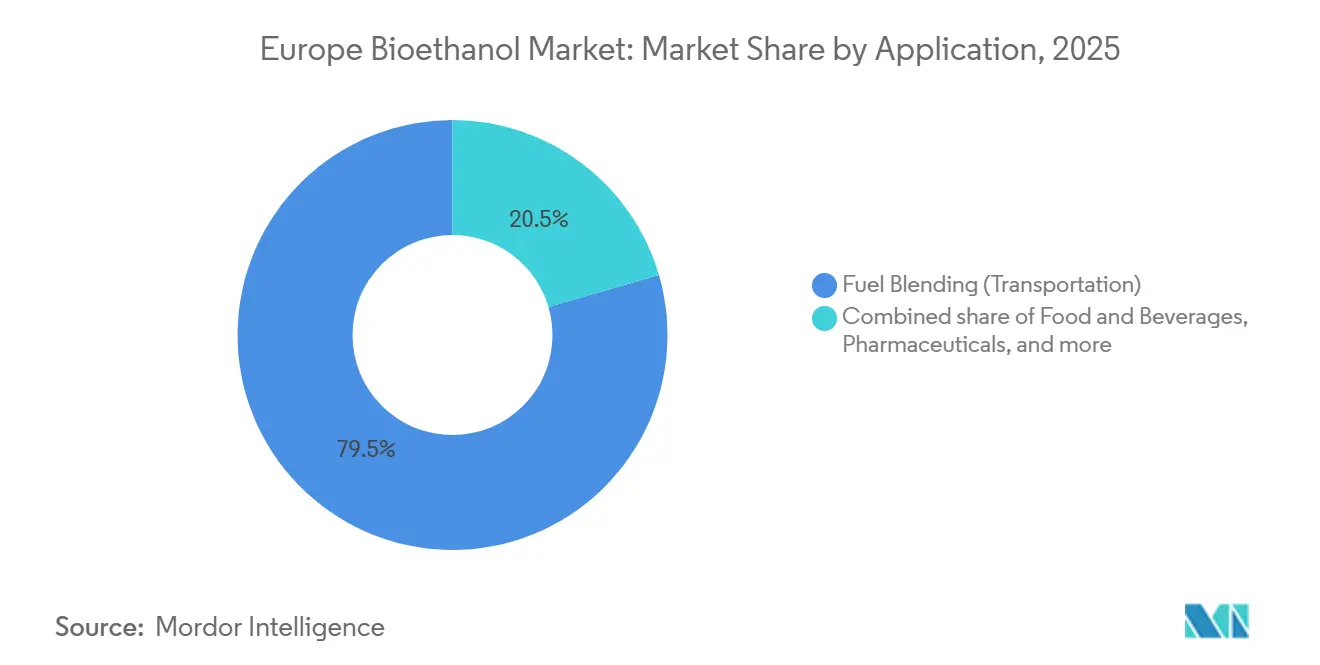

- By application, fuel blending retained 79.5% share of the European bioethanol market size in 2025, whereas food and beverages are projected to grow at a stronger 3.4% CAGR to 2031.

- By geography, France led with 19.9% volume share in 2025, while Nordic countries are expected to record the highest 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Bioethanol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RED III mandates raise renewable-fuel quotas | +0.9% | EU-wide, strongest in France, Germany, Netherlands | Medium term (2-4 years) |

| Roll-out of E10 / E85 across more countries | +0.6% | Poland, Spain, Italy, spillover to Balkans | Short term (≤ 2 years) |

| Carbon-pricing and GHG-credit premiums | +0.5% | Germany, Netherlands, Nordic region | Medium term (2-4 years) |

| Alcohol-to-jet pathway inclusion in SAF law | +0.4% | Hub airports in France, Netherlands, Germany | Long term (≥ 4 years) |

| Monetization of fermentation CO₂ | +0.3% | Netherlands, Belgium, Western Europe | Short term (≤ 2 years) |

| Protein-rich co-products | +0.2% | Germany, France, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

RED III Mandates Raise Renewable-Fuel Quotas

Revised RED III lifts the renewable share in transport to 29% by 2030, triggering incremental demand for 1.2 billion liters of ethanol if current blend levels persist.[4]European Commission, “Renewable Energy Directive III,” ec.europa.eu France and Germany have already published national transposition roadmaps that emphasize ethanol compliance, while Spain and Italy intend to finalize theirs in 2026. Advanced-biofuel sub-targets grant double counting for straw-based volumes, shifting capital toward second-generation plants that can lock in premium off-take contracts with obligated parties. Producers that certify low-ILUC residues therefore enjoy structural margin advantages, cushioning them against grain-price swings. This regulatory certainty underpins the steady expansion of the European bioethanol market.

Roll-Out of E10 / E85 Across Additional EU States

Poland completed nationwide E10 pump conversions in late 2024, adding 8,000 dispensers and lifting domestic bioethanol use by 15% year on year in 2025. Spain followed in early 2025 as Repsol and Cepsa upgraded 60% of their outlets, a change that is expected to absorb an extra 200 million liters by 2027. Germany launched a grant program to retrofit 2,000 stations for E85, broadening the flex-fuel network beyond France and Sweden. Carbon-credit transfers and lower excise taxes make E85 economically attractive, widening the price gap with E10 to €0.20 per liter in 2025. Expanded infrastructure removes blend-wall constraints, supporting the projected 3.11% CAGR of the European bioethanol market.

Carbon-Pricing and GHG-Credit Premiums Enhance Economics

EU ETS allowances averaged €85 per ton CO₂ in 2025, and bioethanol blenders capture tradable credits for lifecycle savings of 60–95%, translating to subsidies of €0.08–0.12 per liter. This cushion pushed E10 into cost parity with pure gasoline even without excise relief in Germany and the Netherlands. Smaller distillers lacking direct ETS access now partner with distributors to secure partial credit value, offsetting their selling price handicap. As Fit for 55 tightens caps, the incentive will persist, encouraging producers to invest in efficient fermentation and dehydration units. Carbon-pricing thus remains a pivotal tailwind for the European bioethanol market.

Alcohol-to-Jet Pathway Inclusion in ReFuelEU Aviation

ReFuelEU Aviation mandates 2% SAF by 2025, rising to 6% by 2030, and explicitly lists alcohol-to-jet as an eligible pathway. A SkyNRG-Neste venture in Rotterdam will convert 50,000 tons of bioethanol into SAF annually from 2027 under airline off-take deals, offering ethanol suppliers a margin-accretive outlet. SAF premiums of USD 800–1,200 per ton in 2025 underpin project economics. Capital intensity remains high, but first movers can lock in long-dated contracts that hedge against road-fuel demand erosion. This pathway diversifies revenue for the European bioethanol market and mitigates risks from electrification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock-price volatility and food-fuel debate | -0.5% | Grain-import-dependent Southern Europe | Short term (≤ 2 years) |

| ILUC-factor compliance costs | -0.3% | Central and Eastern Europe | Medium term (2-4 years) |

| High energy-price swings | -0.4% | Germany, Italy, Poland | Short term (≤ 2 years) |

| EV and e-fuel policy signals | -0.6% | Nordic region, Netherlands, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock-Price Volatility and Food-Versus-Fuel Debate

European wheat traded between €210 and €280 per ton in 2025, a 30% swing that compressed margins for plants lacking hedging capacity. Drought in Southern Europe rekindled the food-fuel debate as NGOs criticized the diversion of cereals to ethanol. RED III caps crop-based biofuels at 2020 levels, yet political scrutiny remains high in Spain and Italy, where bread-wheat prices spiked during mid-2025. Larger players lock multiyear grain contracts and build on-site storage, but small distillers without balance-sheet strength face margin squeezes that accelerate consolidation. Volatile feedstock, therefore, restricts upside for the European bioethanol market.

ILUC-Factor Compliance Increases Certification Costs

Stricter ILUC criteria under RED III require farm-level traceability, adding €2–3 per hectoliter in audit and monitoring fees. Fragmented landholdings in Central and Eastern Europe inflate compliance costs relative to consolidated French and German farms, hitting small-scale producers hardest. Certified low-ILUC volumes command price premiums, but not all costs can be passed through, cutting operating margins by 3–5% for crop-centric plants. This burden incentivizes shifts toward lignocellulosic feedstocks and strengthens the case for vertical integration, influencing capital flows within the European bioethanol market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Corn Dominates, But Lignocellulosic Residues are on the Rise

In 2025, corn accounted for 50.2% of bioethanol production in Europe, bolstered by extensive dry-mill facilities in Hungary, Romania, and Central Europe. This dominance underscores corn's pivotal role in Europe's bioethanol landscape. Meanwhile, lignocellulosic residues are projected to grow at a 6.2% CAGR through 2031. This surge is driven by producers ramping up advanced ethanol production from agricultural waste and forestry by-products, all in a bid to align with tightening decarbonization mandates. Wheat, a key feedstock in France, Germany, and the UK, enjoys advantages from its integration with milling infrastructure and adaptable feedstock economics. Sugars benefit from sugar beet processing and co-fermentation perks at facilities run by local agribusinesses. Additionally, other feedstocks encompass mixed biomass and specialized agricultural residues, processed at both pilot and commercial-scale facilities.

Second-generation output enjoys double-counting credits and commands price premiums that offset higher capex, eroding wheat’s margin advantage where carbon pricing is stringent. Verbio’s modular approach, integrating straw collection with existing distillation trains at EUR 150–200 million (~ USD 174-232 million) per 50,000-ton module, lowers investment hurdles compared with greenfield builds. CropEnergies will replicate the model at its Zeitz site, adding 30,000 tons of advanced capacity by 2027. While corn is set to command the largest share of Europe's bioethanol market until 2031, its dominance will wane as lignocellulosic residues capture an increasing share, propelled by carbon reduction goals and strategies for feedstock diversification.

By Application: Fuel Dominates, Spirits Premiumize

Fuel blending absorbed 79.5% of volume in 2025, sustained by E10 mandates, carbon-credit economics, and limited drop-in gasoline substitutes, reinforcing its anchor role in the European bioethanol market. Food and beverages are projected to rise at a 3.4% CAGR to 2031 as craft distillers and natural-extract manufacturers source non-GMO, traceable ethanol at 20–30% premiums over fuel grades. Pharmaceutical volumes normalized to around 3% post-pandemic but maintain a 40–50 € cent per liter price differential due to USP-grade specifications. Cosmetics and personal care represent a small yet growing niche, favoring grape-based and organic wheat ethanol that attracts the highest quality premiums. Industrial solvents and reagents round out the residual 5% with limited growth prospects absent carbon pricing in the petrochemical sector.

Transport volumes are capped by EV adoption and blend-wall limits, whereas non-fuel applications demonstrate mid-single-digit expansion and higher margins. Craft spirits output advanced 8% in 2025, reinforcing demand for provenance-certified ethanol sourced locally in Germany, France, and the United Kingdom. Pharmaceutical demand benefits from stricter EU GMP excipient rules that favor EU-made ethanol for supply-chain security. Premium cosmetics also create pull for organic and allergen-free grades. This divergence supports portfolio diversification, insulating the European bioethanol industry from the structural decline of the gasoline pool.

Geography Analysis

France held 19.9% of production in 2025 through Tereos and CropEnergies complexes near fuel-distribution hubs, ensuring logistical efficiency and strong domestic off-take. Germany followed at roughly 18%, leveraging Verbio’s straw-based modules and biogas cogeneration that lifts margin resilience. Nordic countries (Sweden, Finland, and Norway) are forecast to grow at a 6.8% CAGR through 2031 as waste-based double-counting makes residues cost-competitive; St1 ramped its Kajaani cellulosic plant to 40,000 tons in 2025. The United Kingdom, Spain, and Italy each account for 8–10%, supported by British Sugar, Abengoa legacy assets, and regional merchant distillers.

Poland and Russia supply a combined 12% volume with low-cost grain plants, yet rising ILUC certification burdens and limited carbon-credit access constrain their western exports. The Netherlands, although small in output, acts as a trading hub; Rotterdam handled 400 million liters of ethanol imports and re-exports in 2025, anchoring spot price discovery in Northwest Europe. Sweden’s reduction obligation and Finland’s waste focus support advanced ethanol premiums, further expanding the Nordic share. Western Europe exhibits slower growth due to mature infrastructure, while advanced-fuel mandates and CHP investments bolster competitiveness, shaping a two-tier Europe bioethanol market landscape.

Competitive Landscape

The Europe bioethanol market is moderately concentrated. The top five companies include CropEnergies, Tereos, Verbio, Pannonia Bio, and Lantmännen. Verbio achieved EBITDA margins 8–10 percentage points above peers by integrating straw feedstocks, biogas energy, and CO₂ capture, illustrating the premium accrued to advanced-fuel capabilities. CropEnergies and Tereos pivoted toward lignocellulosic expansions, each committing over €80 million to retrofit existing plants with Clariant’s Sunliquid technology, a move that protects market position as RED III doubles down on advanced fuels.

SkyNRG and Neste partnered to build a Rotterdam alcohol-to-jet facility that will source ethanol from European producers, signaling a new premium outlet where early supply agreements confer strategic leverage. Certification systems such as ISCC and REDcert evolved from compliance cost to market differentiator; producers with authenticated low-ILUC chains realized EUR0.05–0.08 (~USD 0.06-0.09) per liter price premiums, while uncertified rivals lost share. Four mergers or asset sales closed between 2024 and 2025 as capital requirements for 2G upgrades and energy efficiency forced weaker firms to exit or consolidate. Competitive advantage, therefore, centers on feedstock flexibility, energy self-sufficiency, and access to higher-value markets, elements that will shape share dynamics through 2031 in the European bioethanol market.

Europe Bioethanol Industry Leaders

CropEnergies AG

Vertex Bioenergy

Tereos SCA

Pannonia Bio Zrt.

Lantmännen Agroetanol

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: AGRANA and OMV piloted e-ethanol production in Austria, blending renewable hydrogen with fermentation CO₂ under a €12 million Horizon grant.

- September 2025: Associated British Foods (ABF) announced the closure of Vivergo, its Hull-based bioethanol plant, after failed talks with the UK government for support. This leaves Ensus’s Teesside plant, owned by CropEnergies, as the UK’s sole major bioethanol producer, though it has also warned of potential closure without urgent government action.

- September 2025: Avantium N.V. has partnered with Tereos and LVMH GAÏA to scale the production of Releaf®, a 100% renewable polymer made from plant-based feedstocks. Releaf® is used in packaging, fashion, and fibers.

- June 2025: Toyota is investing in sustainable bioethanol to reduce emissions from internal combustion engines. In partnership with Japanese manufacturers, it launched a pilot facility in Fukushima Prefecture to produce 60 kilolitres of second-generation bioethanol annually, using non-edible biomass like rice straw and forestry by-products.

Europe Bioethanol Market Report Scope

The bioethanol market involves the production, distribution, and consumption of bioethanol, a renewable fuel derived from biomass like sugarcane and corn. It is used in transportation, industrial solvents, pharmaceuticals, and beverages. Government mandates, renewable energy policies, environmental concerns, feedstock availability, and the global shift toward sustainable, low-carbon energy solutions drive market growth.

The European bioethanol market is segmented by feedstock, application, and geography. By feedstock, the market is divided among wheat, corn, sugars, lignocellulosic residues, and other. By application, the market is segmented into fuel blending, food and beverages, pharmaceuticals, cosmetics and personal care, and others. The report also covers the market size and forecasts for the European bioethanol market across major countries. For each segment, the market sizing and forecasts have been done based on volume (liters) for all the above segments.

By Feedstock

| Wheat |

| Corn |

| Lignocellulosic Residues |

| Sugars |

| Other |

By Application

| Fuel Blending (Transportation) |

| Food and Beverages (Spirits, Extracts) |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Others |

By Geography

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| NORDIC Countries |

| Netherlands |

| Poland |

| Russia |

| Rest of Europe |

| By Feedstock | Wheat |

| Corn | |

| Lignocellulosic Residues | |

| Sugars | |

| Other | |

| By Application | Fuel Blending (Transportation) |

| Food and Beverages (Spirits, Extracts) | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Netherlands | |

| Poland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe bioethanol market in 2026?

The Europe bioethanol market size is estimated at 7.09 billion liters in 2026.

Which feedstock holds the largest share in European ethanol production?

In 2025, corn dominated the output, accounting for 50.2%, driven by established dry-mill infrastructure, competitive feedstock availability, and strong demand for high-value co-products like distillers dried grains with solubles (DDGS).

What is driving second-generation ethanol investment?

RED III double counting, higher carbon-credit values, and lower enzyme costs are accelerating lignocellulosic projects such as Verbio's straw units and Clariant-licensed plants.

How will sustainable aviation fuel mandates affect ethanol demand?

ReFuelEU Aviation's alcohol-to-jet pathway creates an additional outlet that could absorb 70,000-100,000 tons of ethanol-derived SAF by 2030, offering producers margin-accretive diversification.

Which countries are expected to post the fastest growth?

The Nordic region is projected to expand at a 6.8% CAGR through 2031, propelled by waste-based blending mandates and new cellulosic capacity in Finland and Sweden.

Why are CO₂ capture projects important for distillers?

Selling food-grade CO₂ at €150–200 per ton adds €0.05–0.08 per hectoliter to margins, providing a hedge against feedstock and energy cost volatility.

Page last updated on: