Market Overview

| Study Period | 2020 - 2031 |

|---|---|

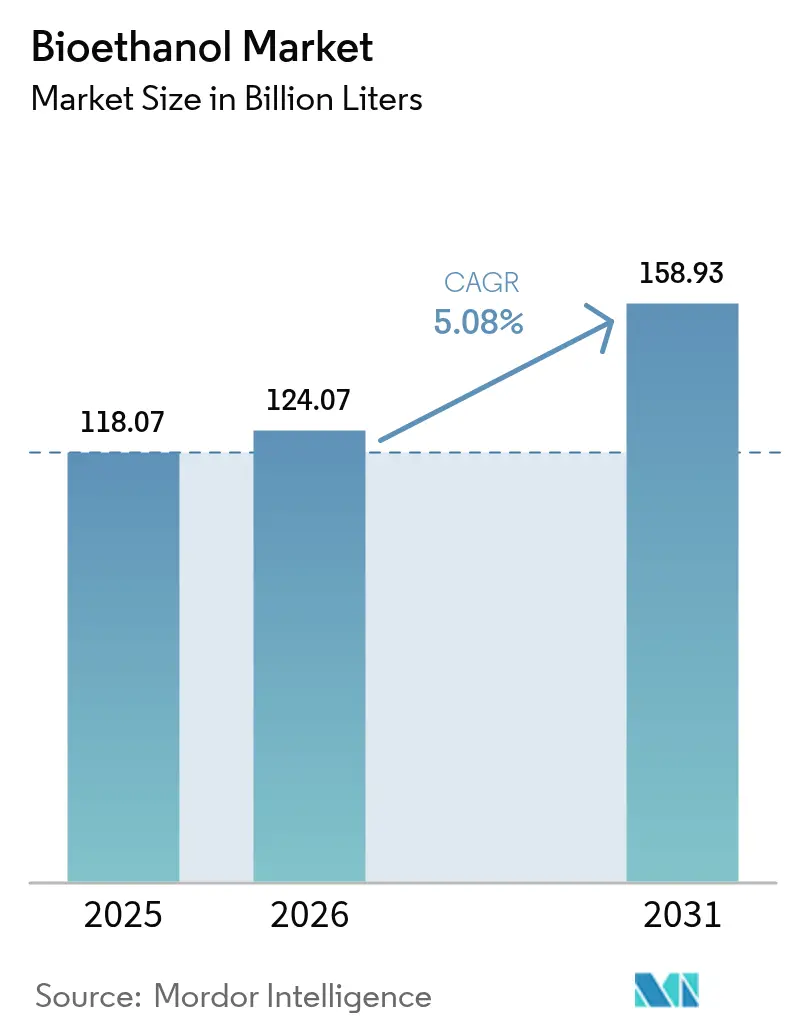

| Market Volume (2026) | 124.07 Billion liters |

| Market Volume (2031) | 158.93 Billion liters |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

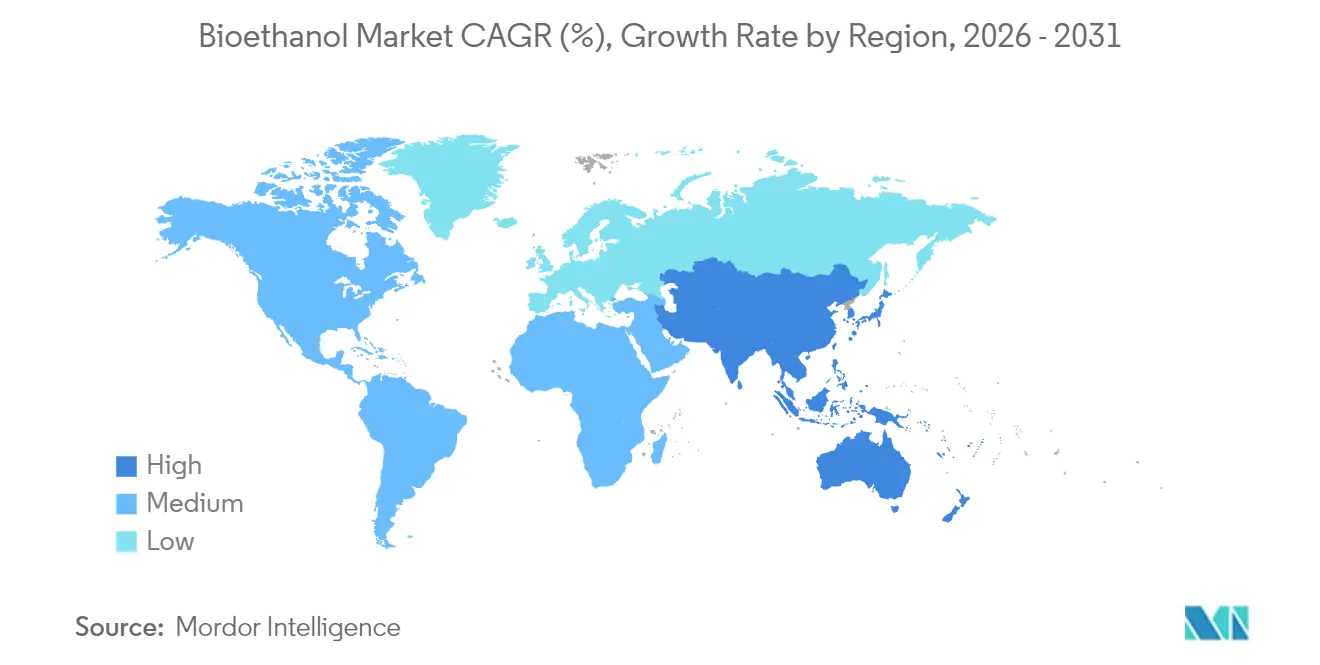

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioethanol Market Analysis by Mordor Intelligence

The Bioethanol Market size was valued at 118.07 billion litres in 2025 and estimated to grow from 124.07 billion litres in 2026 to reach 158.93 billion litres by 2031, at a CAGR of 5.08% during the forecast period (2026-2031). Continued policy backing for E10–E20 blends, growing interest in ethanol-to-jet fuel, and cost-advantaged feedstock supply underpin this trajectory even as light-duty vehicle electrification advances. North American corn-based capacity, Brazilian sugarcane flexibility, and fresh capital inflows from Middle Eastern investors reinforce supply security. Meanwhile, Asia-Pacific governments fast-track aggressive blending targets that deepen regional demand pools, and refiners pursue low-carbon ethanol to satisfy tightening ESG metrics. Together, these factors sustain the bioethanol market’s resilience against competing transport decarbonization pathways.

Key Report Takeaways

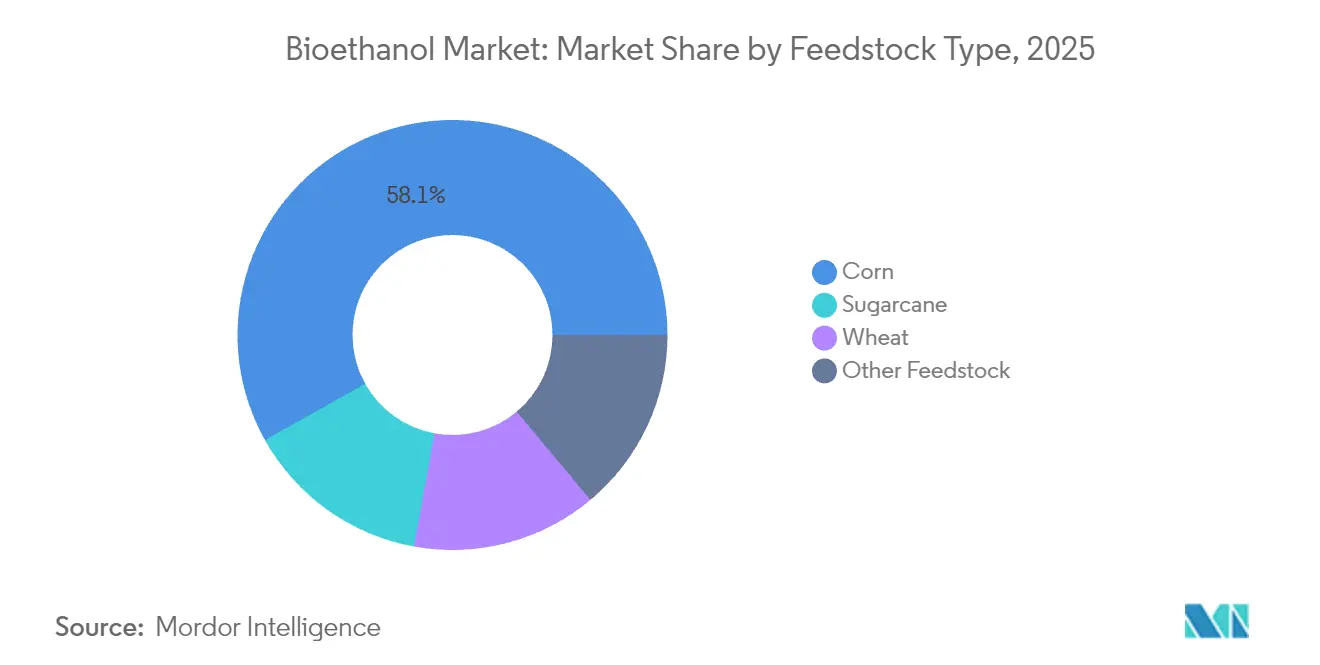

- By feedstock type, corn held 58.12% of the bioethanol market share in 2025, while wheat-based production is projected to expand at a 5.45% CAGR to 2031.

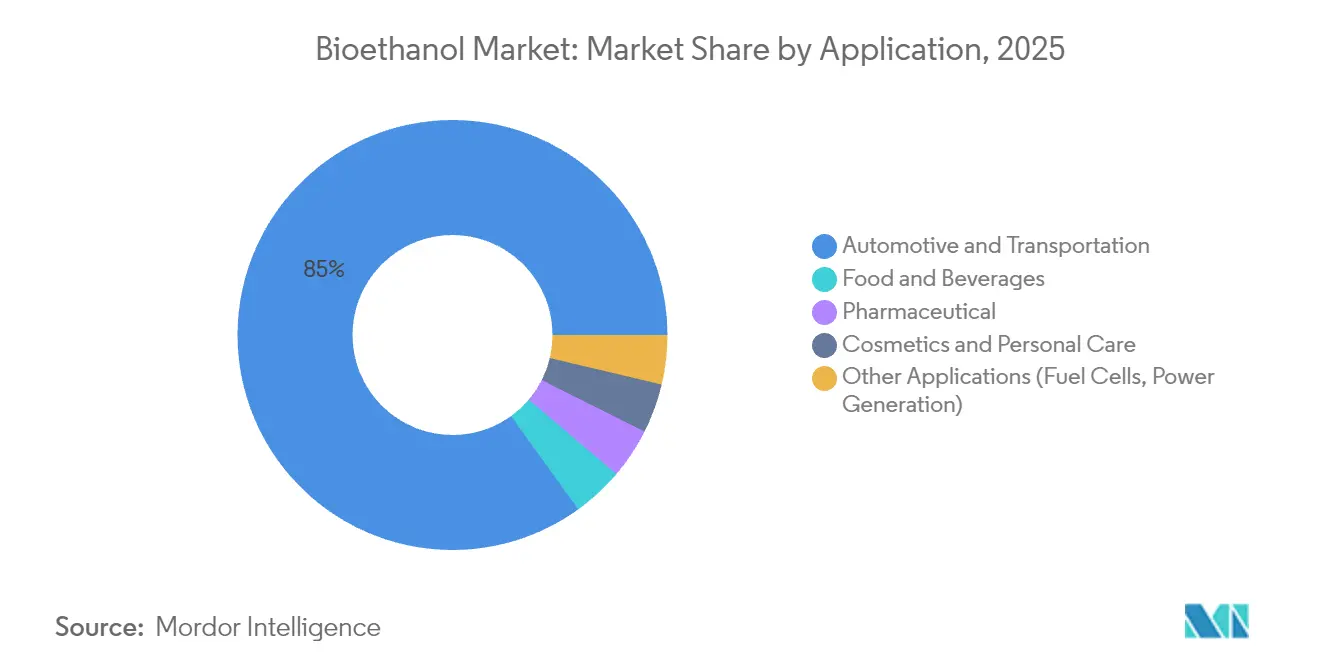

- By application, automotive and transportation dominated with 84.95% of the bioethanol market size in 2025, whereas food and beverages are forecast to grow at a 5.44% CAGR through 2031.

- By geography, North America captured 55.10% revenue share of the bioethanol market in 2025, while the Asia-Pacific region records the highest projected CAGR at 5.74% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioethanol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favourable global E10–E20 blending mandates | +1.8% | Global; early gains in Brazil, India, Japan | Medium term (2-4 years) |

| Carbon-reduction and ESG pressure on refiners | +1.2% | North America and EU; spill-over to APAC | Long term (≥ 4 years) |

| Feedstock cost advantage in U.S. corn and Brazil sugarcane | +0.9% | North America and South America core | Short term (≤ 2 years) |

| Octane demand spurring ethanol as aromatic substitute | +0.7% | Global; concentrated in developed markets | Medium term (2-4 years) |

| Airline demand for ethanol-to-jet SAF pathways | +0.4% | North America and EU; emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Favourable Global E10–E20 Blending Mandates

Strengthened blending requirements are creating predictable baseload demand that insulates the bioethanol market from crude price swings while locking in capacity expansion. Japan’s nationwide E10 roll-out and pilot E20 zones, Brazil’s 27% ceiling flexibility, and India’s accelerated 30% target together lift annual offtake volumes and encourage new plant investment[1]International Energy Agency, “Ordinance No 75/2015 on Ethanol Blending Mandate,” iea.org . Regulatory agencies back compliance through fuel-quality standards, domestic content rules, and import controls, ensuring blend targets translate into physical deliveries rather than paper credits. These policies turn the bioethanol market into a structural element of national energy security strategies even as electrification gains momentum.

Carbon-Reduction and ESG Pressure on Refiners

Refiners facing investor scrutiny and stringent carbon standards now view low-intensity bioethanol as a strategic differentiator instead of a mere compliance component. California’s 2024 Low Carbon Fuel Standard update tightened carbon benchmarks, rewarding supplies certified under schemes such as ISCC. The EU’s revised Renewable Energy Directive likewise privileges traceable, sustainably sourced ethanol. In response, companies like BP vertically integrated upstream via the USD 1.4 billion acquisition of Bunge Bioenergia, securing feedstock and lifecycle emission control in one step. Premium demand emerges in markets where renewable-content uptake exceeds mandate floors, sustaining price spreads favorable to lower-carbon producers.

Feedstock Cost Advantage in U.S. Corn and Brazil Sugarcane

Record U.S. corn yields, efficient dry-grind plants, and coproduct optimization grant American producers a cost buffer that shields margins when corn prices spike. Parallel advantages in Brazil arise from year-round sugarcane harvesting, cogeneration of power from bagasse, and growing corn-ethanol capacity that smooths seasonal supply gaps. USDA projects a 5% rise in planted corn acres for 2025, reinforcing feedstock availability. These dynamics position both regions as the bioethanol market’s swing suppliers, capable of expanding exports when other regions experience feedstock shortages.

Octane Demand Spurring Ethanol as Aromatic Substitute

Tighter air-quality rules phase down benzene, toluene, and xylene content in gasoline, prompting refiners to seek clean octane replacements. Ethanol’s 113 research octane number fills this gap while lowering toxic emissions, stimulating incremental demand unrelated to renewable-fuel quotas. High-performance vehicles in urban centers attract premium ethanol blends, and engine designs optimized for higher ethanol content bolster this pull. Consequently, octane-driven off-take offers the bioethanol market an additional hedge against declining gasoline volumes in mature economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid electrification of light-duty vehicles | -1.4% | North America and EU; expanding to APAC | Medium term (2-4 years) |

| Food-vs-fuel and land-use controversy | -0.8% | Global; acute in food-importing regions | Short term (≤ 2 years) |

| Stricter ILUC-based carbon-intensity scoring | -0.6% | EU and California; spreading elsewhere | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Light-Duty Vehicles

Soaring EV adoption trims gasoline demand ceilings in core markets. Norway hit 94% EV penetration for 2024 new car sales, China surpassed 35%, and the IEA forecasts a 30% global light-vehicle share by 2030. As a result, refiners face shrinking blend pools, compelling bioethanol producers to pivot toward aviation, heavy-duty transport, and export-led strategies. Regional demand divergence persists because emerging economies lag in vehicle electrification, creating opportunities for geographic diversification within the bioethanol market.

Food-vs-Fuel and Land-Use Controversy

India’s push to 30% blending flipped it from a corn exporter to an importer in 2024, inflating feed costs for poultry producers and intensifying scrutiny of first-generation biofuels. IFPRI warns that diverting food crops to fuel during tight grain supply cycles can exacerbate insecurity, spurring policymakers to recalibrate mandates. This narrative pressures governments to favor feedstock diversification toward residues and non-food crops, complicating investment decisions for conventional producers and tempering the bioethanol market’s growth in politically sensitive regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock Type: Corn Dominance Faces Wheat Innovation

Corn-based output contributed 58.12% of the bioethanol market size in 2025, anchored by the U.S. Midwest, Brazil’s Mato Grosso expansion, and well-established rail and barge logistics. Producers leverage enzyme advances and co-product valorization, notably distillers' grains for livestock feed and captured CO2 for beverages, to compress unit costs and improve carbon scores. Continuing investments in carbon capture and underground storage clusters across the Midcontinent further enhance lifecycle performance credentials.

Wheat ethanol is projected to record a 5.45% CAGR through 2031, the fastest growth among mainstream feedstocks. European players harness policy incentives for domestic grain diversification, while Australia’s bumper wheat cycles offer export opportunities. Rising protein premiums make wheat distillers' grains attractive to livestock feeders, offsetting higher starch costs. Technology breakthroughs enabling high-gravity fermentation and fractional distillation improve plant utilization rates, strengthening wheat’s competitiveness within the bioethanol market.

Other feedstocks, such as sugarcane, cassava, and emerging lignocellulosic sources, supply niche but strategic volumes that hedge against weather-induced crop swings. Brazilian sugarcane retains a structural cost edge via bagasse-fired cogeneration, while Indonesia’s nipa palm and Mexico’s agave pilots aim to unlock marginal-land production. Such diversification dampens price volatility and aligns with policymakers' pressure to minimize food-crop displacement.

By Application: Automotive Dominance with Food Sector Growth

Automotive and transportation end-uses absorbed 84.95% of total volume in 2025, cementing their status as the bioethanol market’s revenue spine. Mandated blend walls in the United States, Brazil, and the EU guarantee baseline demand even when oil prices fall. Refiners prize ethanol’s octane contribution, letting them comply with aromatic caps without costly refinery upgrades.

Food and beverages represent the fastest-expanding application, expected to grow at a 5.44% CAGR to 2031. Growth hinges on rising demand for premium spirits, natural flavor extracts, and fermentation substrates that require high-purity ethanol. Distillers benefit from flexible pricing linked to beverage-grade quality premiums, insulating them from fuel-ethanol price cycles. Pharmaceutical, cosmetics, and sanitizer uses add steady offtake backed by rigorous ISO and pharmacopeia standards that command stable margins inside the broader bioethanol market.

The nascent ethanol-to-jet fuel pathway opens an additional premium outlet. Airlines preferring drop-in solutions over radical aircraft redesigns underpin offtake agreements that finance new conversion plants. While still small in absolute liters, SAF potential reshapes producer economics by offering multiples of road-fuel prices for qualifying feedstocks, underscoring the application diversification underway.

Geography Analysis

North America maintained 55.10% of global volume in 2025 thanks to entrenched corn infrastructure, stable Renewable Fuel Standard targets, and supportive state-level Low Carbon Fuel initiatives. Producers integrate carbon capture, direct air capture, and pipeline networks that compress the carbon intensity of corn ethanol, qualifying it for high-value credit markets. Canada leverages wheat and corn feedstock clusters, whereas Mexico’s demand uptick absorbs U.S. exports, reinforcing continental trade flows that stabilize regional balance.

Asia-Pacific records the highest forecast CAGR at 5.74% through 2031 as India’s 30% blend target and China’s import appetite amplify consumption. Regional governments frame bioethanol expansion as rural income support and foreign-exchange savings, encouraging local investment in multi-feedstock biorefineries. Thailand, the Philippines, and Vietnam advance blend mandates aligned with agricultural modernization plans, while Indonesia pilots nipa-to-ethanol routes to sidestep food-crop constraints.

Europe emphasizes sustainability certification and favors residue-based ethanol that fulfills stringent greenhouse-gas savings thresholds. Quota systems in Germany and France anchor demand, and the United Kingdom’s Renewable Transport Fuel Obligation prioritizes SAF, indirectly boosting ethanol-to-jet pathways. South America, dominated by Brazil, attracts foreign capital, notably the UAE’s USD 13.5 billion commitment, to expand integrated assets that marry sugarcane, corn, and cogeneration. Middle East and Africa remain niche but rising, catalyzed by FAO programs for clean cooking solutions that position ethanol as a household energy alternative.

Competitive Landscape

The bioethanol industry is moderately fragmented. Gevo’s purchase of Red Trail Energy enlarged its North Dakota footprint and added onsite carbon sequestration expertise, illustrating the rising value of embedded CCS. Technology differentiation centers on enzyme cocktails that lift fermentation yield, advanced control systems using artificial intelligence for real-time energy optimization, and in-house carbon accounting platforms certified to ISO 14067. Producers racing toward ethanol-to-jet deployment secure offtake letters from airlines to underpin financing, with LanzaJet’s Georgia plant and Gevo’s Net-Zero 1 in South Dakota serving as early blueprints.

Bioethanol Industry Leaders

POET LLC

ADM

Valero

Raizen

Green Plains Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: India inaugurated its first bamboo-based bio-refinery at Golaghat district at Numaligarh Refinery Limited (NRL) to promote clean energy and reduce, dependence on fossil fuels.

- October 2024: BP p.l.c. finalized its USD 1.4 billion takeover of Bunge Bioenergia, adding 11 sugarcane mills and 1.2 billion liters of annual capacity.

- June 2024: Raizen opened its Piracicaba second-generation plant that converts 82,000 tons of bagasse into 42 million liters of cellulosic ethanol yearly.

Global Bioethanol Market Report Scope

Bioethanol is a clear, colorless liquid that is biodegradable and considered a green fuel. It is produced by fermenting sugar and starch-bearing plant yields like corn, sugarcane, and lignocellulosic biomass. Bioethanol is primarily used in the automotive industry as an octane enhancer for reducing engine knocking.

The Bioethanol Market is segmented by feedstock type (Sugarcane, Corn, Wheat, and Other Feedstock Types), Application (Automotive and Transportation, Food and Beverage, Pharmaceutical, Cosmetics and Personal Care, and other applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The report offers the market size and forecasts in volume (liters) for all the above segments.

By Feedstock Type

| Sugarcane |

| Corn |

| Wheat |

| Other Feedstock |

By Application

| Automotive and Transportation |

| Food and Beverages |

| Pharmaceutical |

| Cosmetics and Personal Care |

| Other Applications (Fuel Cells, Power Generation) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Feedstock Type | Sugarcane | |

| Corn | ||

| Wheat | ||

| Other Feedstock | ||

| By Application | Automotive and Transportation | |

| Food and Beverages | ||

| Pharmaceutical | ||

| Cosmetics and Personal Care | ||

| Other Applications (Fuel Cells, Power Generation) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast volumetric growth for global bioethanol through 2031?

Global volume is projected to rise from 124.07 billion liters in 2026 to 158.93 billion liters by 2031, reflecting a 5.08% CAGR.

Which region will add the most incremental liters of demand?

Asia-Pacific, driven by India’s 30 % blending target and sustained Chinese import demand, posts the highest CAGR at 5.74% through 2031.

How dominant is corn in current bioethanol output?

Corn accounts for 58.12 % of 2025 supply, making it the single largest feedstock within the global mix.

What segment beyond fuel offers the fastest revenue growth?

Food and beverages lead non-fuel applications, expanding at a 5.44 % CAGR on rising demand for beverage-grade and food-processing ethanol.

How are producers addressing carbon-intensity pressures?

Investments in carbon capture, sustainable feedstock certification, and ethanol-to-jet pathways allow producers to lower lifecycle emissions and access premium markets.

What forces could restrain future demand growth?

Accelerating electric-vehicle adoption in developed markets and mounting food-versus-fuel concerns may dampen gasoline-blend demand and policy backing.

Page last updated on: