Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.74 Billion |

| Market Size (2026) | USD 8.03 Billion |

| Market Size (2031) | USD 9.62 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

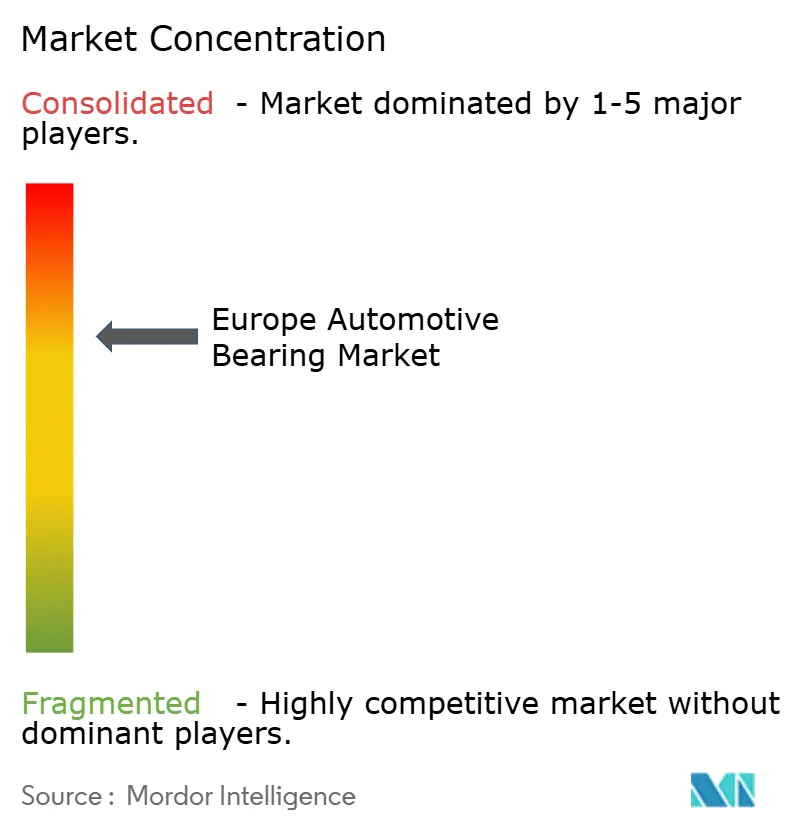

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Automotive Bearing Market Analysis by Mordor Intelligence

The European automotive bearing market size is expected to grow from USD 7.74 billion in 2025 to USD 8.03 billion in 2026 and is forecast to reach USD 9.62 billion by 2031 at 3.69% CAGR over 2026-2031. This outlook reflects the sector’s steady shift from internal-combustion to electric powertrains, where higher rotational speeds, electrical insulation, and tighter thermal windows are reshaping bearing specifications. The European Commission’s Euro 7 limits are accelerating demand for ultra-low-friction designs that slice both CO₂ and noise emissions. Rolling-element bearings remain the performance benchmark, while sensor-integrated “smart” variants are gaining traction in predictive maintenance programs. Germany anchors demand thanks to its premium vehicle production, but Spain, Poland, and the Czech Republic are capturing incremental volumes through new EV investments. On the supply side, steel price volatility and geopolitical tensions create margin headwinds, even as local circular economy rules expand opportunities for remanufactured products.

Key Report Takeaways

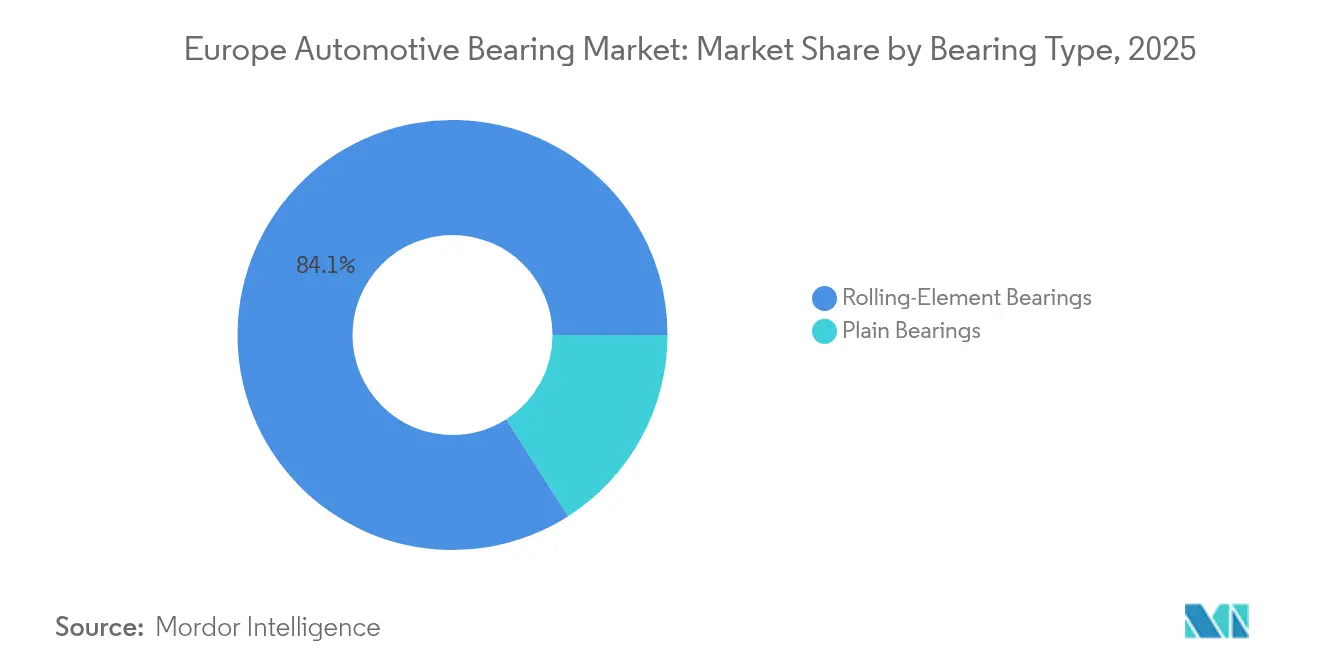

- By bearing type, rolling-element products led the European automotive bearing market, accounting for an 84.05% share in 2025. This category also posted the fastest growth rate of 4.15% through 2031.

- By material, steel held 53.74% of the European automotive bearing market share in 2025, while polymer and other advanced materials are projected to rise at a 4.32% CAGR to 2031.

- By vehicle type, passenger cars accounted for 72.62% of the European automotive bearing market size in 2025; light commercial vehicles are forecast to grow the quickest at 4.63% CAGR through 2031.

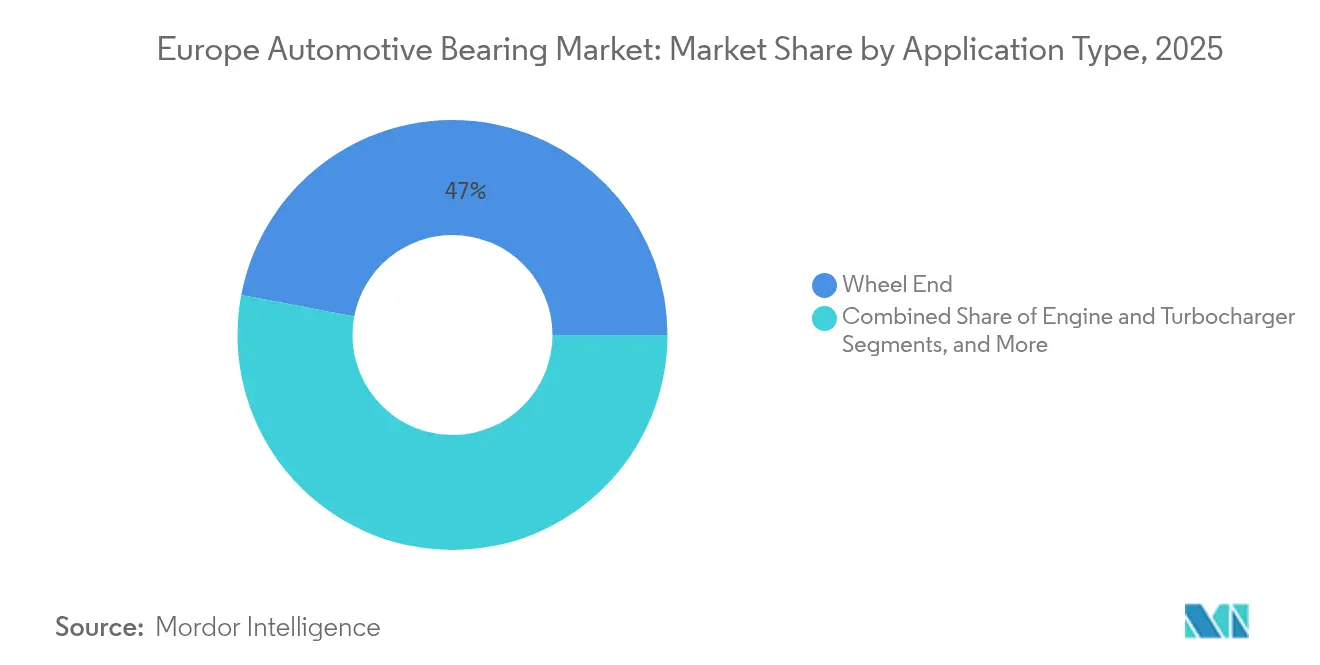

- By application, wheel-end systems accounted for 47.02% of the European automotive bearing market share in 2025. In contrast, driveline and transmission bearings are expected to expand at a 4.25% CAGR during the outlook period.

- By sales channel, the OEM business captured 62.74% of the European automotive bearing market in 2025, and the aftermarket segment is projected to advance at a 4.12% CAGR through 2031.

- By geography, Germany retained its top position with a 33.62% share of the European automotive bearing market in 2025, while Spain delivered the highest 3.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Bearing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Growth Needs Insulated Bearings | +1.2% | Germany, France, Netherlands, Nordic countries | Medium term (2-4 years) |

| EU Limits Push Low-Friction Designs | +0.9% | EU-wide, with early adoption in Germany, France | Short term (≤ 2 years) |

| European Production Recovery | +0.7% | Germany, Spain, Czech Republic, Poland | Short term (≤ 2 years) |

| Circular Economy Boosts Reman Bearings | +0.5% | EU-wide, strongest in Germany, Netherlands, France | Long term (≥ 4 years) |

| Smart Bearings for Predictive Maintenance | +0.4% | Germany, UK, France, premium vehicle segments | Medium term (2-4 years) |

| Additive Manufacturing of Polymer Cages | +0.2% | Germany, Netherlands, advanced manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising EV Adoption Demanding High-Speed Insulated Bearings

Europe's automotive bearing market suppliers must now engineer products for traction motors that regularly spin at 3,000–16,000 rpm, with top-tier designs exceeding 20,000 rpm. At such speeds, stray currents can pit steel raceways within 50,000 miles if no insulation is provided. OEMs mitigate the risk with multi-layer protection that blends ceramic elements, grounding clamps, and common-mode chokes. NSK’s deep-groove ball bearings, featuring proprietary insulation coatings, and Schaeffler’s hybrid ceramic solutions exemplify how vendors are adding electrical robustness without sacrificing load capacity[1]"High-Speed Bearings for Electric Vehicle Drivetrains," nsk.com. The shift increases the per-unit value, especially on high-voltage 800 V platforms, which intensifies concerns about current leakage. Germany and France account for the bulk of early EV volumes, but the Nordics serve as a growing testbed for cold-temperature validation.

Stringent EU CO₂ and Noise Limits Pushing Low-Friction Designs

Euro 7 rules, effective 2025, curb tailpipe CO₂ to 93 g/km for passenger cars and tighten brake-particulate and noise thresholds[2]"Euro 7 emissions standards for cars, vans, lorries and buses," ec.europa.eu. Bearing makers, therefore, prioritize surface engineering and lubricant compatibility with ultra-low-viscosity fluids as thin as 3.5 cSt at 100 °C. Diamond-like carbon coatings, advanced texturing, and mechanochemical finishing reduce low-speed wear by up to five times while damping NVH in near-silent EV cabins.

Sensor-Integrated “Smart” Bearings for Predictive Maintenance

IoT-enabled bearings embed temperature, vibration, and lubrication sensors that stream data to fleet dashboards, enabling condition-based maintenance and cutting unplanned downtime. SKF’s virtual sensor technology utilizes machine learning to infer bearing health from operating parameters, thereby eliminating the need for external hardware and reducing implementation costs. Schaeffler integrates resolvers and accelerometers into wheel-end units, providing rotational feedback for chassis control systems and maintenance alerts in a single assembly. European fleets average 12.4 years of service life and log 103,500 km annually, making predictive maintenance an attractive way to reduce roadside failures.

On-Demand Additive Manufacturing of Polymer Cages

Additive manufacturing using PEEK, PPS, and reinforced nylon permits complex cage geometries that streamline lubricant flow and trim weight. Research centers in Germany and the Netherlands have demonstrated 15% friction reductions by optimizing pocket geometry, results difficult to replicate via stamping or machining. Besides performance, on-demand printing reduces tooling lead times for prototype EV gearboxes and motorsport builds. Suppliers are trialing decentralized production hubs near OEM plants to reduce freight emissions and customs delays. Limitations remain—layer adhesion affects fatigue life, and high-temperature endurance still trails brass—but polymer cages hold promise for low-load e-pump bearings and steering-column units. The combined impact lifts the European automotive bearing market only modestly now but sets up a longer-term competitive edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -0.8% | EU-wide, particularly Germany, Italy, Spain | Short term (≤ 2 years) |

| Low-Cost Import Competition | -0.6% | EU-wide, strongest impact in commodity segments | Medium term (2-4 years) |

| Smart-Factory Cyber Shutdowns | -0.3% | Germany, Netherlands, advanced manufacturing regions | Short term (≤ 2 years) |

| EV Drivetrain Cuts Bearing Count | -0.4% | Germany, France, Netherlands, EV adoption leaders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Steel, Rare Alloys)

Hot-rolled coil prices yo-yoed in 2024, squeezing margins for bearing-grade steels that require precision metallurgy and vacuum degassing [3]"European Steel Industry Outlook," eurofer.eu. Specialty alloys containing rare-earth elements introduce additional volatility due to their concentrated global supply. The Carbon Border Adjustment Mechanism, while protecting EU steelmakers from carbon leakage, imposes additional compliance costs on imported raw materials. Smaller bearing manufacturers without scale to negotiate favorable supply agreements or maintain strategic inventory buffers face the most tremendous pressure. The restraint clips 0.8 percentage points from the growth of the European automotive bearing market in the short term.

Competition From Low-Cost Asian Imports

Chinese bearing exports to Europe rose in 2024, targeting aftermarket segments where price sensitivity outweighs brand loyalty. Asian producers have secured ISO certifications while maintaining labor-cost advantages, which has pressured European margins. The threat extends beyond commodity products as Chinese manufacturers develop capabilities in ceramic hybrids and sensor-integrated solutions. European vendors respond with investments in automation, product differentiation, and geographic diversification. Anti-dumping duties provide some protection but cannot fully offset the fundamental cost gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bearing Type: Rolling-Element Dominance Drives Innovation

Rolling-element bearings command 84.05% of the European automotive bearing market share in 2025 while simultaneously leading growth at 4.15% CAGR through 2031. Ball bearings within this category demonstrate particular strength in electric vehicle applications, where high-speed capabilities and electrical insulation properties address the unique requirements of traction motors operating at 10,000-20,000 rpm. Timken's research comparing tapered roller bearings to deep groove ball bearings in EV intermediate shafts reveals that application-weighted power losses are effectively equivalent under real-world conditions, despite conventional wisdom favoring ball bearings for efficiency.

Roller bearings, encompassing both cylindrical and tapered variants, are experiencing robust growth in commercial vehicle applications where higher load capacities and extended service intervals justify premium pricing. Cylindrical roller bearings benefit from their ability to handle pure radial loads with minimal friction, making them ideal for wheel-end applications in electric commercial vehicles. Tapered roller bearings are gaining traction in EV gearboxes due to their combined radial and thrust load capabilities, enabling more compact transmission designs that are critical for battery electric vehicle packaging constraints. Plain bearings, although representing a smaller market share, remain important in specialized applications such as turbocharger assemblies and engine auxiliaries, where their simple construction and high-temperature capabilities provide advantages over rolling-element alternatives.

By Material: Ceramic Integration Accelerates Performance

Steel bearings maintain the largest market share at 53.74% of the European automotive bearing market in 2025, leveraging established manufacturing processes and cost-effectiveness across mainstream automotive applications. However, polymer and other advanced materials are emerging as the fastest-growing segment, with a 4.32% CAGR through 2031, driven by weight reduction initiatives and specialized application requirements in electric vehicles. Silicon nitride ceramic bearings are gaining prominence in high-performance applications, offering superior hardness, lower weight, and electrical insulation properties that address bearing current issues in electric traction motors. Hyundai-Transys' research on silicon nitride ball bearings reveals critical manufacturing considerations, with hot isostatic pressing (HIP) treatments achieving 18.7% higher fracture toughness compared to standard sintering processes.

Ceramic and hybrid bearings, which combine ceramic rolling elements with steel raceways, offer optimal solutions for electric vehicle applications. This design prevents bearing current damage while maintaining mechanical performance, thanks to electrical insulation. These hybrid configurations block the flow of electrical current, which can cause pitting and premature failure in high-voltage electric drivetrains. Advanced polymer materials, including PEEK and reinforced nylon, enable additive manufacturing of customized bearing cages that optimize lubricant flow and reduce noise in quiet electric vehicles. The material selection increasingly considers lifecycle environmental impact, with EU circular economy regulations favoring materials that support remanufacturing and recycling. Graphene-infused lubricants and coatings represent emerging technologies that enhance bearing performance while supporting sustainability objectives. The transition toward lower-viscosity lubricants in EV applications places greater emphasis on bearing material properties and surface treatments to maintain adequate lubrication films under boundary lubrication conditions.

By Vehicle Type: Passenger Cars Lead, Commercial Vehicles Accelerate

Passenger cars dominate the European automotive bearing market with a 72.62% share in 2025, reflecting the segment's volume leadership and diverse bearing applications across engine, transmission, and chassis systems. Light commercial vehicles are emerging as the fastest-growing segment, with a 4.63% CAGR through 2031, driven by e-commerce growth, last-mile delivery expansion, and electrification initiatives that require specialized bearing solutions. The LCV segment's growth is particularly pronounced in urban areas, where emission regulations favor electric powertrains and bearing requirements differ significantly from those of traditional diesel applications. Electric LCVs typically operate with single-speed transmissions and high-torque electric motors that place different demands on bearing systems compared to multi-speed ICE powertrains.

Heavy commercial vehicles consistently demand high-capacity bearings, with wheel-end applications requiring extended service intervals and superior load-carrying capabilities. The HCV segment is experiencing gradual electrification, with hybrid powertrains creating complex bearing requirements that combine traditional ICE applications with electric motor support systems. Two-wheelers represent a specialized market with unique bearing requirements for high-speed applications and weight-sensitive designs, while off-highway vehicles in agriculture, construction, and mining demand bearings that can operate in harsh environments with extended maintenance intervals. Fleet operators' focus on total cost of ownership creates opportunities for premium bearing solutions that offer extended service life and predictive maintenance capabilities.

By Application: Wheel-End Leadership, Drivetrain Innovation

Wheel-end applications command 47.02% of the European automotive bearing market share in 2025, reflecting their critical safety function and the universal requirement across all vehicle types. Driveline and transmission applications emerge as the fastest-growing segment, with a 4.25% CAGR through 2031, driven by electrification trends that create new bearing requirements in single-speed reduction gearboxes and integrated motor-transmission units. Wheel-end bearings are evolving toward integrated solutions that combine bearing function with ABS sensors, temperature monitoring, and condition monitoring capabilities. These integrated hub units offer weight savings and enhanced reliability while enabling advanced vehicle dynamics control systems and predictive maintenance strategies.

Engine and turbocharger applications face declining demand in passenger vehicles due to electrification, but maintain importance in commercial vehicles and hybrid powertrains, where ICE components remain prevalent. Turbocharger bearings represent a specialized, high-performance segment that requires operation at extreme speeds and temperatures, with ceramic and hybrid bearing solutions gaining adoption. Steering and suspension applications benefit from the adoption of electric power steering, which eliminates hydraulic systems while creating new bearing requirements in electric assist motors and steering column assemblies. HVAC, alternator, and accessory applications are transforming as electric vehicles eliminate engine-driven accessories while introducing new electric systems for thermal management and battery cooling. The transition creates opportunities for bearings optimized for electric motor applications, including high-speed capability, electrical insulation, and enhanced sealing for liquid cooling systems. Advanced bearing technologies, including sensor integration and intelligent monitoring, are becoming standard in premium applications where condition-based maintenance provides operational advantages.

By Sales Channel: OEM Innovation, Aftermarket Resilience

OEM channels hold a 62.74% share of the European automotive bearing market in 2025, reflecting the importance of original equipment applications and the technical complexity of modern bearing specifications. The aftermarket emerges as the fastest-growing channel, with a 4.12% CAGR through 2031, benefiting from an aging vehicle population and the expansion of independent service networks. Independent aftermarket distributors are investing heavily in remanufacturing capabilities, with current remanufactured component sales expected to grow by 2030.

OEM channels benefit from direct relationships with vehicle manufacturers and access to technical specifications that enable the development of optimized bearing solutions for specific applications. The channel is transforming as OEMs increasingly specify integrated bearing solutions that combine multiple functions, such as bearing-sensor assemblies and bearing-seal combinations, thereby reducing assembly complexity and improving performance. The aftermarket is characterized by price sensitivity and brand competition, creating opportunities for both premium branded solutions and value-oriented alternatives. The channel dynamics are influenced by vehicle electrification, which reduces the demand for some conventional bearing applications while creating new requirements for specialized EV components and services.

Geography Analysis

Germany dominates the European automotive bearing market, holding a 33.62% share in 2025, leveraging its position as Europe's largest automotive manufacturer and an early adopter of electrification technologies. The country's automotive industry, anchored by BMW, Mercedes-Benz, Volkswagen Group, and Audi, drives demand for premium bearing solutions while fostering innovation in electric vehicle technologies. Germany's automotive production benefits from established supply chain networks and advanced manufacturing capabilities, while government incentives for electric vehicle production support continued market leadership. The country's focus on Industry 4.0 and smart manufacturing creates demand for sensor-integrated bearings and predictive maintenance solutions.

Spain emerges as the fastest-growing market, with a 3.92% CAGR through 2031, benefiting from significant foreign direct investment in electric vehicle manufacturing and battery production. The country's strategic position as a gateway to both European and North African markets, combined with competitive labor costs and government support for electrification, makes it an attractive destination for international automotive investments. France and Italy maintain substantial market positions, with France benefiting from Stellantis' production and Italy leveraging its strengths in the luxury and commercial vehicle segments. The United Kingdom, despite Brexit-related challenges, remains a key player due to its premium automotive sector and advanced engineering capabilities. Eastern European countries, including Poland and the Czech Republic, are gaining production share through cost competitiveness and proximity to German automotive clusters. The historical comparison between 2019-2024 and 2025-2030 growth rates shows acceleration in Southern and Eastern European markets, driven by production capacity expansion and electrification investments, while traditional automotive centers maintain steady growth supported by technology leadership and premium market positioning.

Competitive Landscape

The European automotive bearing market exhibits moderate concentration with intense competition among established global players and emerging technological disruptors. Market leadership remains concentrated among traditional bearing manufacturers, including SKF, Schaeffler Group, NSK, and Timken, who leverage extensive automotive relationships and technical expertise to maintain premium market positions. However, competitive dynamics are shifting as electrification creates new technical requirements and value propositions that challenge traditional competitive advantages.

Strategic patterns emphasize vertical integration and technology convergence, with bearing manufacturers expanding into adjacent technologies such as electric motors, power electronics, and sensor systems. NSK's development of integrated bearing-resolver solutions and SKF's virtual sensor technologies demonstrate how traditional bearing companies are evolving toward comprehensive system solutions. White-space opportunities exist in specialized EV applications, including high-speed motor bearings, electrical insulation solutions, and sensor-integrated smart bearings that enable predictive maintenance.

Emerging disruptors include Asian manufacturers that are rapidly developing advanced bearing technologies while maintaining cost advantages, as well as technology companies entering the automotive space through sensor integration and digital solutions. The use of artificial intelligence and machine learning for bearing design optimization, predictive maintenance, and manufacturing quality control is becoming a key differentiator, with companies investing heavily in digital capabilities to maintain competitive positions in an increasingly connected automotive ecosystem.

Europe Automotive Bearing Industry Leaders

-

NSK Ltd.

-

Schaeffler AG

-

NTN Corporation

-

AB SKF

-

The Timken Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: JTEKT Corporation has successfully transferred its European needle roller bearing (NRB) business. JTEKT struck a foundational deal with AEQUITA SE & Co. KGaA, a German investment firm, to hand over its NRB operations. This transfer encompasses three of JTEKT's consolidated subsidiaries, all of which are engaged in NRB manufacturing.

- October 2024: Schaeffler AG (Schaeffler) has successfully merged with Vitesco Technologies Group. Moving forward, the unified entity will be branded solely as “Schaeffler.” The business will be segmented into four divisions: E-Mobility, Powertrain & Chassis, Vehicle Lifetime Solutions, and Bearings & Industrial Solutions.

Europe Automotive Bearing Market Report Scope

The Europe Automotive Bearing Market Report is Segmented by Bearing Type (Plain Bearings, Rolling-Element Bearings including Ball Bearings and Roller Bearings with Cylindrical and Tapered variants), Material (Steel, Ceramic and Hybrid, Polymer and Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-Wheelers, and Off-Highway), Application (Wheel End, Engine and Turbocharger, Transmission and Driveline, Steering and Suspension, HVAC and Accessories), Sales Channel (OEM and Aftermarket), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

By Bearing Type

| Plain Bearings | ||

| Rolling-Element Bearings | Ball Bearings | |

| Roller Bearings | Cylindrical Roller | |

| Tapered Roller | ||

By Material

| Steel |

| Ceramic and Hybrid |

| Polymer and Others |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) |

| Two-Wheelers |

| Off-Highway (Agri/Construction/Mining) |

By Application / Position

| Wheel End |

| Engine and Turbocharger |

| Transmission and Driveline |

| Steering and Suspension |

| HVAC, Alternator and Accessories |

By Sales Channel

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Bearing Type | Plain Bearings | ||

| Rolling-Element Bearings | Ball Bearings | ||

| Roller Bearings | Cylindrical Roller | ||

| Tapered Roller | |||

| By Material | Steel | ||

| Ceramic and Hybrid | |||

| Polymer and Others | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles (LCV) | |||

| Heavy Commercial Vehicles (HCV) | |||

| Two-Wheelers | |||

| Off-Highway (Agri/Construction/Mining) | |||

| By Application / Position | Wheel End | ||

| Engine and Turbocharger | |||

| Transmission and Driveline | |||

| Steering and Suspension | |||

| HVAC, Alternator and Accessories | |||

| By Sales Channel | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Country | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

Key Questions Answered in the Report

What factors are driving growth in the European automotive bearing market?

The primary growth drivers include rising EV adoption requiring specialized high-speed insulated bearings, stringent EU emissions regulations pushing low-friction designs, recovery in vehicle production, and circular economy rules boosting remanufactured bearings. The market is projected to grow at 3.69% CAGR to reach USD 9.62 billion by 2031.

How is electrification changing automotive bearing requirements?

Electric vehicles demand bearings capable of operating at 3-5× higher speeds (10,000-20,000 rpm), with electrical insulation to prevent current damage, and compatibility with ultra-low viscosity fluids. This shift is driving adoption of ceramic hybrid bearings, DLC coatings, and sensor integration for condition monitoring.

Which bearing type dominates the European automotive market?

Rolling-element bearings command 84.05% market share and are growing at 4.15% CAGR through 2031. Within this category, ball bearings excel in electric motors while tapered roller bearings are gaining traction in EV gearboxes due to their combined radial and thrust load capabilities.

Which countries lead the European automotive bearing market?

Germany dominates with 33.62% market share due to its premium automotive manufacturing base.

Page last updated on: