Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

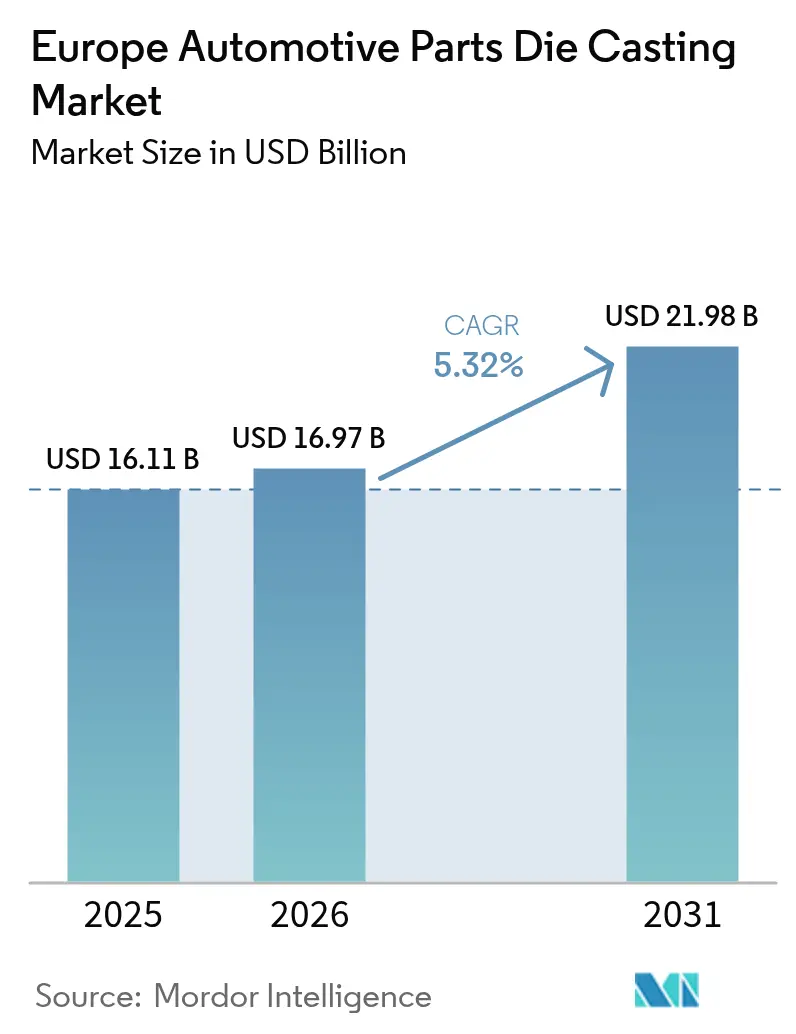

| Base Year Market Size (2025) | USD 16.11 Billion |

| Market Size (2026) | USD 16.97 Billion |

| Market Size (2031) | USD 21.98 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Parts Die Casting Market Analysis by Mordor Intelligence

The European automotive die casting market size was valued at USD 16.11 billion in 2025 and estimated to grow from USD 16.97 billion in 2026 to reach USD 21.98 billion by 2031, at a CAGR of 5.32% during the forecast period (2026-2031). Consistent electrification targets, a sharp pivot toward large structural “gigacast” parts, and the need for lightweight metals shape the current growth trajectory. Aluminum continues to anchor most volumes, yet magnesium and multi-stage vacuum high-pressure die casting (HPDC) record the highest growth as electric-vehicle (EV) programs demand porosity-free, weight-optimized castings. Parallel internal-combustion-engine (ICE) and battery-electric-vehicle (BEV) production keeps tooling revenue stable while allowing foundries to allocate capital toward EV-specific capabilities. Germany’s installed press capacity, Spain’s emerging EV assembly ecosystem, and tightening EU lifecycle-carbon regulations collectively reinforce supply-chain realignment and consolidation dynamics.

Key Report Takeaways

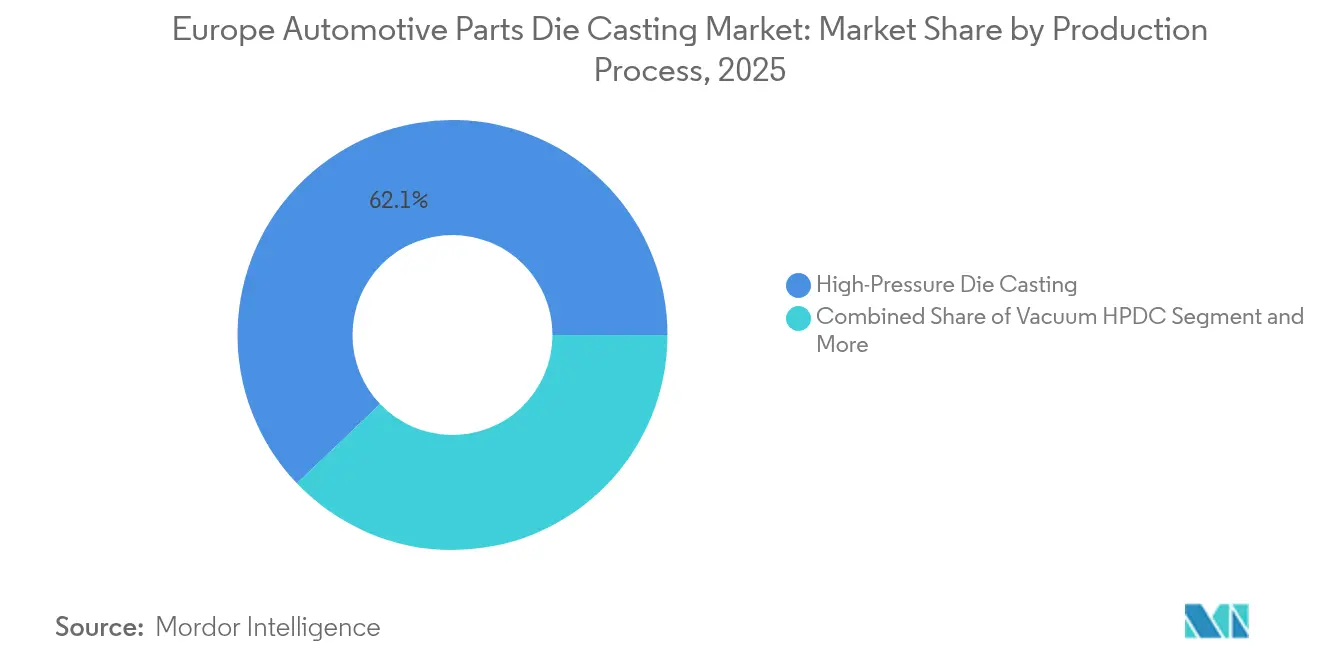

- By production process, high-pressure die casting led with 62.12% of the Europe automotive die casting market share in 2025, while vacuum HPDC is forecasted to advance at a 6.71% CAGR through 2031.

- By metal type, aluminum captured 75.12% share of the Europe automotive die casting market size in 2025; magnesium is projected to expand at a 9.25% CAGR between 2026 and 2031.

- By application, engine and powertrain parts retained a 39.40% share of the Europe automotive die casting market in 2025. In contrast, battery housings and e-drive casings are projected to post the fastest 11.22% CAGR to 2031.

- By vehicle type, passenger cars accounted for 70.65% of the Europe automotive die casting market share in 2025, while light commercial vehicles are projected to exhibit a 6.86% CAGR outlook.

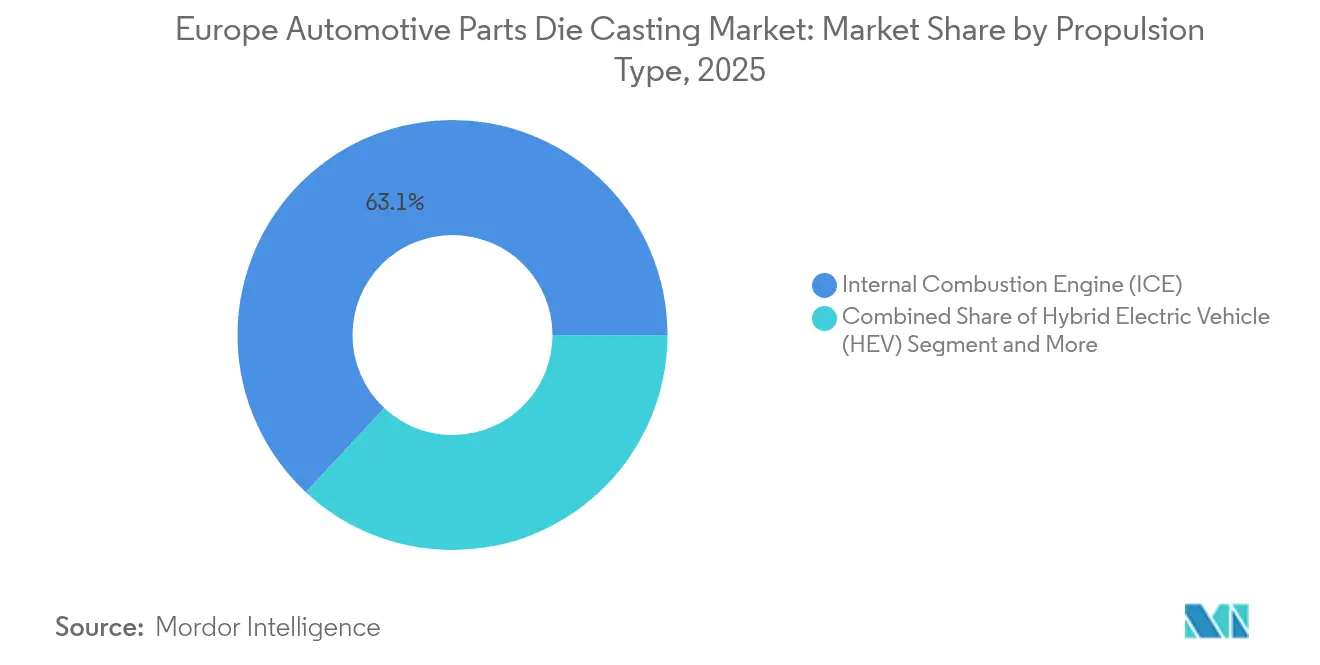

- By propulsion type, internal-combustion engines dominated, with 63.05% of the Europe automotive die casting market share in 2025; battery electric vehicles are accelerating at a 8.88% CAGR through 2031.

- By casting size, medium castings (1-10 kg) led with 48.92% share of the Europe automotive die casting market in 2025; mega-castings above 100 kg are projected to post the highest 9.31% CAGR by 2031.

- By country, Germany held 19.95% of the Europe automotive die casting market regional revenue in 2025, whereas Spain is expanding at the strongest 5.55% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Parts Die Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift "Gigacast" Structural Parts | +2.1% | Germany, France, Spain, Italy | Medium term (2-4 years) |

| CO₂ and Lifecycle-Carbon Regulations | +1.8% | EU-wide, DACH regions | Long term (≥ 4 years) |

| ICE–EV Parallel Production | +1.2% | Germany, France, Italy, CEE regions | Short term (≤ 2 years) |

| In-House Alloy Recycling Loops | +0.9% | Germany, France, Netherlands | Medium term (2-4 years) |

| Multi-Stage Vacuum HPDC | +0.7% | DACH regions, Northern Italy | Medium term (2-4 years) |

| Co-Development of Battery-Housing Castings | +0.6% | Germany, France, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Led Shift to Large “Gigacast” Structural Parts

European OEMs are adopting gigacasting to consolidate up to 100 smaller stampings into single 100 kg-plus aluminum structures, cutting weld points and floor-space requirements. Volvo’s Gothenburg plant and Mercedes-Benz’s Bremen line already operate presses exceeding 6,000 t clamping force. The transition elevates the share of mega-castings within the European automotive die casting market, encourages closer OEM-foundry engineering collaboration, and rewards suppliers capable of financing a large number of presses. While Tesla’s recent reconsideration of its next-generation gigacast layout underlines technical hurdles, European foundries continue investing in vacuum evacuation, crack-detection, and heat-treatment systems to meet OEM crash-performance targets. The capital intensity is accelerating regional consolidation because smaller family-owned shops struggle to fund megapress installations. Over the medium term, gigacasting is expected to lift press-tonnage utilization rates and broaden foundry revenue beyond traditional powertrain parts.

Stricter EU CO₂ and Lifecycle-Carbon Regulations

The Euro 7 framework, effective 2026, couples tailpipe limits with battery-durability and material-recycling thresholds, compelling OEMs to prioritize recycled low-carbon aluminum billets. Die casters, therefore, must record lifecycle assessments compliant with ISO 14040/14044 or risk losing sourcing bids[1]“Vehicle Emissions and Battery Durability (Euro 7): Technical Requirements and Certification Rules,” European Union, EUR-Lex, eur-lex.europa.eu. Foundries that already run closed-loop alloy recovery systems will achieve preferred-supplier status, whereas peers sourcing primary metal face margin dilution. The regulation also adds scope for non-exhaust particulates, driving brake, suspension, and body-in-white redesigns. These mandates provide multi-year demand visibility for porosity-free, thin-wall castings compatible with crash and corrosion criteria. Transition periods allow established regional foundries time to retrofit degassing stations and alternative fluxes, but laggards incur penalty fees or require joint ventures with material recyclers.

ICE–EV Parallel Production Extending Tooling Demand

European automakers maintain parallel ICE and BEV lines, stabilizing demand for engine blocks and transmission housings while BEV-specific parts ramp gradually. In 2024, more than 85% of passenger vehicles sold in the region still contained combustion engines, underpinning a sizeable installed base of high-tonnage tooling. This coexistence stretches amortization cycles, supporting the European automotive die casting market through predictable spare-part volumes even as OEMs deploy capital toward battery housing megacasts. Foundries leverage this window to retrain labor, pilot vacuum HPDC, and upgrade furnace alloys without losing core ICE cash flow. However, over-reliance on legacy volumes risks stranded assets once BEV penetration exceeds economic break-even for dedicated electric platforms, pushing management to monitor production-mix inflection points closely.

OEM Push for In-House Alloy Recycling Loops

Automakers across Germany, France, and the Netherlands implement closed-loop scrap collection to secure scrap quality, minimize CO₂ footprints, and reduce exposure to volatile primary metal prices. Under such agreements, foundries collect, sort, and remelt stamping or machining scrap into specification-compliant secondary billets, selling them back at a discount to primary ingot. The model alters profit pools: while overall casting revenue rises, material-margin retention narrows as OEMs internalize alloy value. Foundries that develop melt-shop analytics, impurity tracking, and automated scrap handling strengthen long-term contract stickiness. Facilities lacking space for dedicated remelt furnaces risk relegation to overflow work or face acquisition offers from vertically integrated OEM groups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility Vs Fixed-Price RFQs | -1.4% | EU-wide, particularly Germany | Short term (≤ 2 years) |

| PFAS and HF Gas Limits | -1.1% | EU-wide, DACH regions | Medium term (2-4 years) |

| Foundry Labour Shortages | -0.8% | Germany, Czech Republic, Poland, Austria | Long term (≥ 4 years) |

| OEM Re-Shoring Pressures | -0.6% | Germany, France, CEE regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Spot Aluminum-Price Volatility vs Fixed-Price RFQs

European cast-house margins widen or compress depending on the mismatch between LME spot quotes and 12- to 24-month RFQs secured with automakers. Recent energy-price spikes and potential trade sanctions threaten consistent billet availability, forcing foundries to either hedge positions at elevated premiums or absorb raw-material inflation. Smaller facilities with limited balance-sheet strength face liquidity strain, potentially accelerating consolidation. Some suppliers respond by incorporating adjustment clauses into new RFQs, though OEMs resist variable pricing to protect bill-of-materials forecasts. Inventory buffers offer temporary relief but tie up working capital and raise insurance costs, underscoring the need for dynamic procurement strategies.

Tightening PFAS and HF Gas Limits in EU Foundries

The proposed prohibition on per- and polyfluoroalkyl substances (PFAS) and tighter hydrogen-fluoride emissions rules threaten conventional die-release agents and fluxes essential for high-cycle HPDC lines. Foundries must test silicon-oxide, graphite, or water-borne substitutes, each with distinct viscosity and thermal-shock characteristics influencing filling speed and surface finish. Early adopters report marginal cycle-time penalties yet benefit from marketing “green-casting” credentials, aiding OEM sustainability scoring. Equipment retrofits such as catalytic after-burners or closed scrubber loops—require multi-million-euro outlays. Compliance costs weigh disproportionately on small job shops, potentially crowding them out of the European automotive die casting market over the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process Type: Vacuum HPDC Gains Momentum

High-pressure die casting retained a 62.12% European automotive die casting market share in 2025, thanks to its productivity advantage for high-volume parts. Vacuum HPDC, however, is forecast to outpace at a 6.71% CAGR, reflecting OEM acceptance of porosity-free structures for battery enclosures and chassis nodes. The European automotive die casting market size attributable to vacuum HPDC yields a direct gain in lightweight structural applications.

Rising clamping-force requirements motivate foundries to upgrade to multi-stage evacuation systems that reduce dissolved gases and enable post-weld heat treatment. Investments in real-time pressure monitoring shorten defect-detection feedback loops, reducing scrap times. Standard HPDC remains economical for engine block volumes, yet as ICE demand flattens, profit potential migrates to value-added gigacastings. Squeeze casting and semi-solid processes keep niche relevance for premium brake calipers, where superior mechanical properties offset cycle-time drawbacks. The shift in process mix illustrates how technical specifications, not just labor costs, define European competitiveness.

By Metal Type: Magnesium Accelerates Despite Aluminum Dominance

Aluminum commanded a 75.12% share of the European automotive die casting market size in 2025, given its balance of density, cost, and mature recycling paths. The segment captured a significant portion of the European automotive die casting market size, aided by circular-economy mandates that penalize virgin material. Magnesium, however, will post a 9.25% CAGR through 2031. Technological gains in alloy formulation attenuate corrosion concerns and allow thinner walls without sacrificing stiffness.

Battery-pack enclosures and steering-column brackets increasingly specify magnesium to offset cell weight, offering range benefits to BEVs. Zinc and specialty alloys serve infotainment housings and sensor brackets requiring dimensional accuracy rather than tensile strength. As Europe installs larger gigapresses, the alloy mix could widen further if structural magnesium alloys pass flammability tests. Supply security remains an open question because most primary magnesium originates outside the EU, but enhanced scrap-collection pathways mitigate part of the risk.

By Application Type: Battery Housings Drive Transformation

Engine and powertrain castings preserved a 39.40% share of the European automotive die casting market size in 2025, yet the segment will contract as BEVs displace ICE drivetrains. Battery housings and e-drive casings are expected to rise at an 11.22% CAGR by 2031, significantly increasing total revenue. This transition sees gigacast battery trays replacing multiple extrusions and sheet-metal assemblies, reducing assembly labor while improving thermal management.

Foundries capitalize by offering co-design services that integrate cooling channels directly into structural castings, lowering pack thickness and maximizing under-floor clearance. Transmission components decline in share but remain essential for plug-in hybrids and niche performance models. Structural body-in-white parts gain traction across all propulsion types, driven by EU crash mandates and lightweight incentives. The emerging mix reshapes tooling workflows from small-cell mold clusters toward large integrated die sets, redefining cost drivers and profit metrics.

By Vehicle Type: Commercial Vehicles Show Resilience

Passenger cars generated a 70.65% share of the European automotive die casting market size in 2025. Yet, light commercial vehicles are projected to record a 6.86% CAGR as e-commerce and urban-logistics fleets demand lightweight chassis parts. Fleet operators prioritize total cost of ownership, driving the commercial vehicle segment's interest in lightweight die-cast components for enhanced fuel efficiency and optimized payloads. While heavy commercial vehicles consistently demand die-cast components for engine and transmission applications, their electrification lags behind passenger cars, hindered by infrastructure challenges and range limitations.

Fleet operators focus on total cost of ownership, incentivizing high thermal-conductivity aluminum parts that improve brake cooling and extend pad life. Off-highway and agricultural equipment comprise a steady sub-segment relying on high-strength alloys for harsh duty cycles. The diversification across vehicle categories shields foundries from any single propulsion trend, though securing homologation for safety-critical commercial-vehicle parts entails stricter testing, adding lead-time to project pipelines.

By Propulsion Type: BEV Momentum Builds Gradually

In 2025, internal combustion engines (ICEs) strongly grip the European automotive die casting market, making up 63.05% of vehicle sales. This shows that while the shift to electric vehicles (EVs) is underway, it’s happening gradually. Battery electric vehicles (BEVs) are gaining momentum, expected to grow steadily at 8.88% annually from 2026 to 2031, thanks to better infrastructure and more model options. Foundries are feeling the impact of this shift, as demand for traditional ICE parts declines and EV-specific components rise, pushing them to rethink capacity and invest in new technologies.

At the same time, hybrid and plug-in hybrid vehicles act as a bridge, keeping demand alive for both conventional and electric drivetrain parts. Fuel-cell EVs remain a niche but promising area, offering opportunities for foundries with expertise in advanced materials and pressure systems. The growth of BEVs is being driven by improved battery tech, wider charging networks, and stricter regulations. Still, with ICEs continuing to dominate, foundries must stay flexible—supporting both legacy and emerging technologies to avoid risking short-term revenue while preparing for a more electric future.

By Casting Size: Mega-Castings Reshape Production

In 2025, medium-sized castings (weighing 1–10 kg) dominate the market with 48.92% share of the Europe automotive die casting market in 2025, thanks to their widespread use in traditional automotive parts like engine blocks and transmission housings. But the spotlight is shifting toward mega-castings, those over 100 kg, which are growing rapidly at a 9.31% annual rate from 2026 to 2031. This surge is driven by automakers like Tesla, Volvo, and Mercedes-Benz adopting gigacasting to simplify vehicle assembly and reduce the number of individual components. Meanwhile, small castings (under 1 kg) continue to serve precision roles in electronics and interiors, and large castings (10–100 kg) remain essential for structural and powertrain parts.

As casting sizes grow, foundries face new challenges that require serious investment in high-tonnage equipment and larger facilities. Producing mega-castings isn’t just about scale; it demands advanced skills in mold design, thermal control, and quality assurance to ensure these massive parts are structurally sound. This shift reflects a broader industry trend toward consolidation, aiming to cut costs and streamline production. However, it also means that only well-equipped foundries with the right expertise and resources will be able to compete in this evolving landscape.

Geography Analysis

Germany led the European automotive die casting market with a 19.95% revenue share in 2025, supported by an integrated supply ecosystem that locates foundries within a 200 km radius of major vehicle assembly plants. Domestic suppliers invest in multi-stage vacuum HPDC and gigacasting pilot cells to retain program awards from Volkswagen and Mercedes-Benz. Rising electricity costs and skilled-labor shortages challenge competitiveness, and the German automotive association expects up to 190,000 job losses by 2035 if reskilling does not keep pace with electrification. Foundries respond by expanding apprenticeship programs and co-financing renewable-power purchase agreements to stabilize operating costs.

France and Italy follow with mature foundry clusters; French policy incentives for aluminum recycling allow plants in regions such as Grand Est to claim low-carbon production credentials, which aligns with Euro 7 procurement frameworks. Italian suppliers across Lombardy and Emilia-Romagna continue exporting powertrain castings, but escalating gas prices compress margins. The United Kingdom maintains niche capabilities in magnesium casting and motorsport components, though customs-clearance delays add logistical overhead when shipping to continental OEMs.

Spain exhibits the fastest 5.55% CAGR, benefiting from EV assembly commitments in Catalonia and Valencia and wage structures that undercut northern peers. Tier-1 suppliers establish regional satellite units to serve battery-housing programs, leveraging government grants tied to the EU’s post-pandemic Recovery and Resilience Facility. Central and Eastern European (CEE) countries such as Poland and Czech Republic offer cost-competitive machining capacity; however, out-migration and low unemployment rates tighten labor pools, raising long-term wage trajectories. Norway and Sweden prioritize hydro-powered smelting of low-carbon primary aluminum, supplying billet for northern German and Danish foundries. Russian supply exits the market due to geopolitical sanctions, spurring billet imports from the Middle East and North America to balance demand.

Competitive Landscape

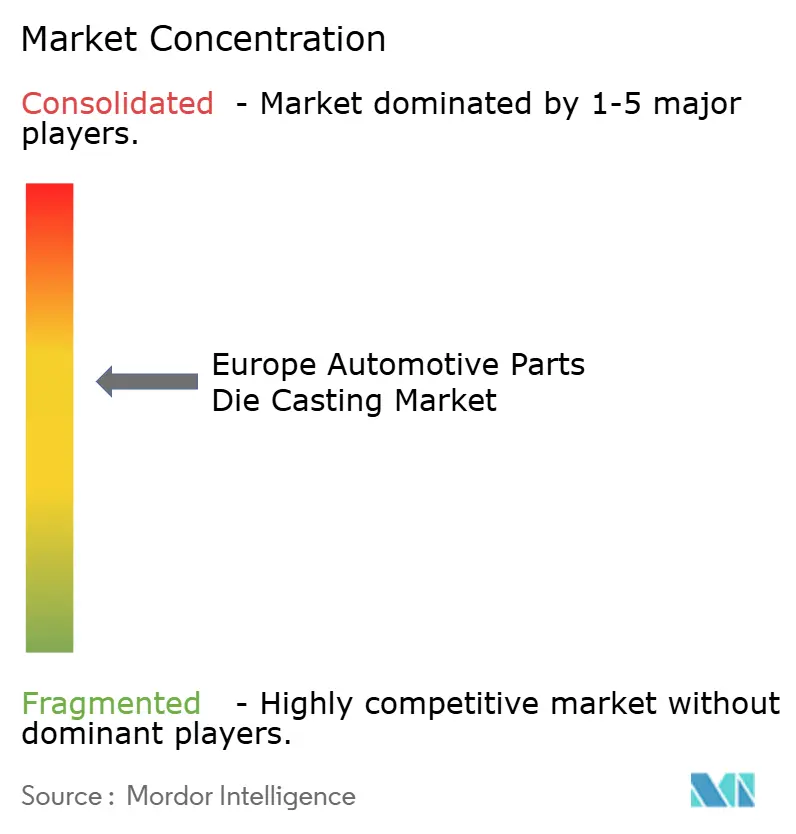

The European automotive die casting market remains moderately fragmented, with the top three players holding significant combined share, underscoring scope for consolidation. Market leaders deploy high-tonnage presses, vacuum-assisted dies, and closed-loop alloy recovery to secure multiyear EV platform awards. Medium-sized regional foundries differentiate through rapid prototyping, offering eight-week lead times for complex battery tray samples that larger competitors supply in twelve.

Strategic capital allocation gravitates toward gigapress installations, furnace digitalization, and inline computed tomography inspection. Leading firms partner with press manufacturers to co-develop die-lubrication systems that significantly cut cycle times. Vertical integration into machining and surface treatment secures additional margin while reducing logistics delays, which OEMs increasingly cite as contract-renewal criteria.

Consolidation momentum is evidenced by acquisitions in which well-capitalized groups absorb niche vacuum-HPDC specialists to access EV battery case intellectual property. Private-equity interest accelerates as steady EV-linked revenue streams offset the cyclicality traditionally linked to ICE demand. Meanwhile, Asian competitors establish joint ventures in Eastern Europe to circumvent trade barriers and exploit qualified labor at lower cost, introducing further pressure on incumbent pricing structures. Across the landscape, automation intensity and carbon-accounting transparency increasingly determine competitive fitness.

Europe Automotive Parts Die Casting Industry Leaders

Martinrea Honsel

Ryobi Die Casting

Georg Fischer

Rheinmetall Automotive

Buhler Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Novelis launched the first aluminum coil produced entirely from end-of-life scrap, claiming a 95% CO₂ reduction relative to primary metal and signaling a scalable closed-loop solution for European OEM programs.

- December 2024: Rheinmetall closed the purchase of Loc Performance Products for an enterprise value of USD 950 million, broadening its North American footprint in structural castings and advanced vehicle systems.

- November 2024: United Grinding agreed to acquire GF Machining Solutions, enhancing its position in ultra-precision equipment used to finish die casting molds for structural EV components.

- August 2024: Clarios announced EUR 200 million capacity investments across four European plants to increase advanced battery-technology output by 50% before 2026, bolstering demand for associated die cast battery enclosures.

Europe Automotive Parts Die Casting Market Report Scope

Automotive die casting uses a metal molding to produce parts from molten metal (die). The metal is then cooled and solidified into machined items such as engine blocks or gearboxes. This approach eliminates waste while saving manufacturers and customers time and money.

The Europe automotive parts die casting market has been segmented by production process type, application type, metal type, and by country. By production process type, the market is segmented into vacuum die casting, pressure die casting, and other production process types.By application type the market is segmented into engine parts, transmission components, structural parts, and other application types.By metal type the market is segmented into aluminum, zinc, and other metal types, and country the market is segmented into Germany, United Kingdom, France, Italy, Rest of Europe. The report offers the market size in value (USD) and forecasts for all the above segments.

By Production Process Type

| High-Pressure Die Casting (HPDC) |

| Vacuum HPDC |

| Squeeze Casting |

| Semi-Solid Metal Casting |

| Gravity and Low-Pressure Die Casting |

By Metal Type

| Aluminium |

| Zinc |

| Magnesium |

| Others (Cu-, Fe-based alloys) |

By Application Type

| Engine and Power-train Parts |

| Transmission Components |

| Structural and Body-in-White Parts |

| Battery Housings and e-Drive Casings |

| Chassis and Suspension Components |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Off-highway Vehicles |

By Propulsion Type

| Internal Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicle (BEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

By Casting Size

| Small (Below 1 kg) |

| Medium (1 to 10 kg) |

| Large (10 to 100 kg) |

| Mega-Castings (Above 100 kg) |

Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Production Process Type | High-Pressure Die Casting (HPDC) |

| Vacuum HPDC | |

| Squeeze Casting | |

| Semi-Solid Metal Casting | |

| Gravity and Low-Pressure Die Casting | |

| By Metal Type | Aluminium |

| Zinc | |

| Magnesium | |

| Others (Cu-, Fe-based alloys) | |

| By Application Type | Engine and Power-train Parts |

| Transmission Components | |

| Structural and Body-in-White Parts | |

| Battery Housings and e-Drive Casings | |

| Chassis and Suspension Components | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Off-highway Vehicles | |

| By Propulsion Type | Internal Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Battery Electric Vehicle (BEV) | |

| Fuel-Cell Electric Vehicle (FCEV) | |

| By Casting Size | Small (Below 1 kg) |

| Medium (1 to 10 kg) | |

| Large (10 to 100 kg) | |

| Mega-Castings (Above 100 kg) | |

| Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the European automotive die casting market?

The market is valued at USD 16.97 billion in 2026 and is projected to grow to USD 21.98 billion by 2031.

How quickly are battery housings expected to grow?

Battery housings and e-drive casings are forecast to register an 11.22% CAGR through 2031, making them the fastest-expanding application segment.

Which production process is gaining traction for EV structural parts?

Multi-stage vacuum HPDC is the fastest-growing process, advancing at a 6.71% CAGR as OEMs demand porosity-free castings.

Why is magnesium demand rising despite aluminum dominance?

Magnesium’s superior strength-to-weight ratio supports range gains in BEVs, driving a 9.25% CAGR between 2026 and 2031.

Which country shows the highest growth momentum in Europe?

Spain leads growth with a projected 5.55% CAGR as new EV assembly lines and government incentives attract supplier investment.

How will Euro 7 regulations affect die casters?

Euro 7 pushes foundries toward recycled low-carbon alloys and full lifecycle assessments, creating long-term demand for sustainable casting processes.

Page last updated on: