Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

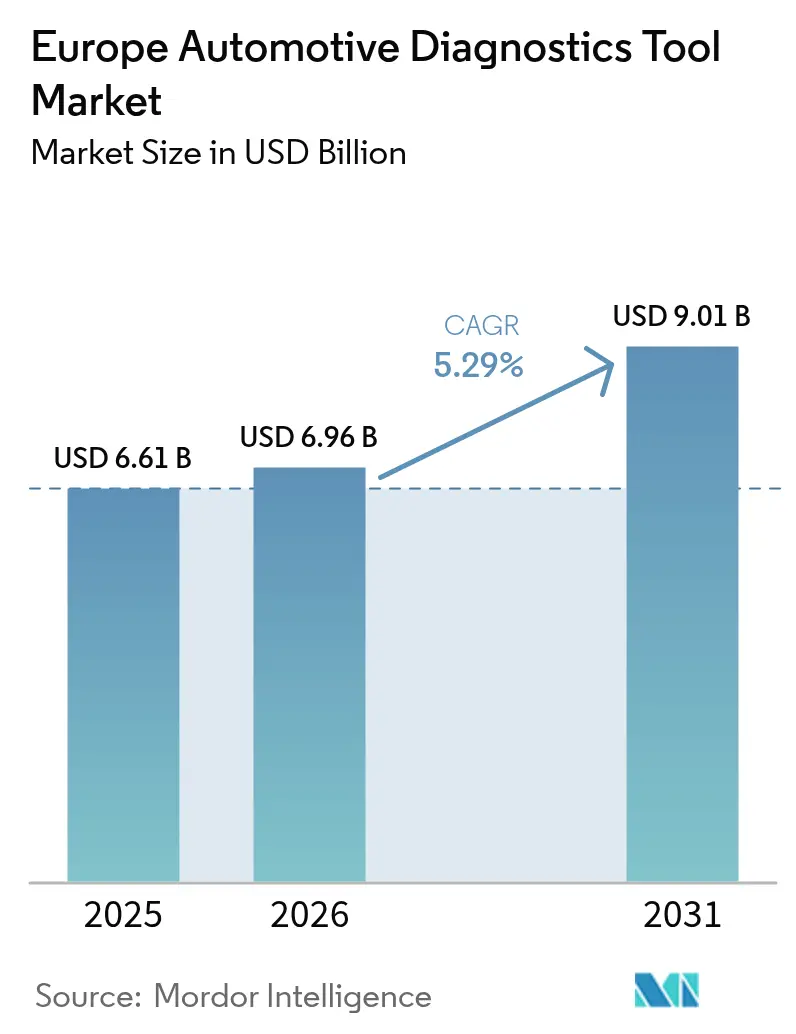

| Base Year Market Size (2025) | USD 6.61 Billion |

| Market Size (2026) | USD 6.96 Billion |

| Market Size (2031) | USD 9.01 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Diagnostics Tool Market Analysis by Mordor Intelligence

The Europe Automotive Diagnostics Tool Market size in 2026 is estimated at USD 6.96 billion, growing from 2025 value of USD 6.61 billion with 2031 projections showing USD 9.01 billion, growing at 5.29% CAGR over 2026-2031. Strong growth in the region is driven by the shift toward software-defined vehicles, the rapid adoption of electrified powertrains, and stricter Euro 7 emission limits that require more in-depth, data-rich diagnostics. Market momentum also draws support from the EU Right-to-Repair law, which equalizes data access for independent garages, as well as from the steady migration of workshops toward cloud-enabled service models. Established players introduce subscription offerings that bundle hardware, remote support, and continuous software updates to retain users and grow recurring revenue. At the same time, rising protocol fragmentation, cybersecurity obligations under GDPR, and the shortage of EV-qualified technicians temper adoption rates, requiring vendors to offer integrated training, secure gateways, and modular upgrade paths.

Key Report Takeaways

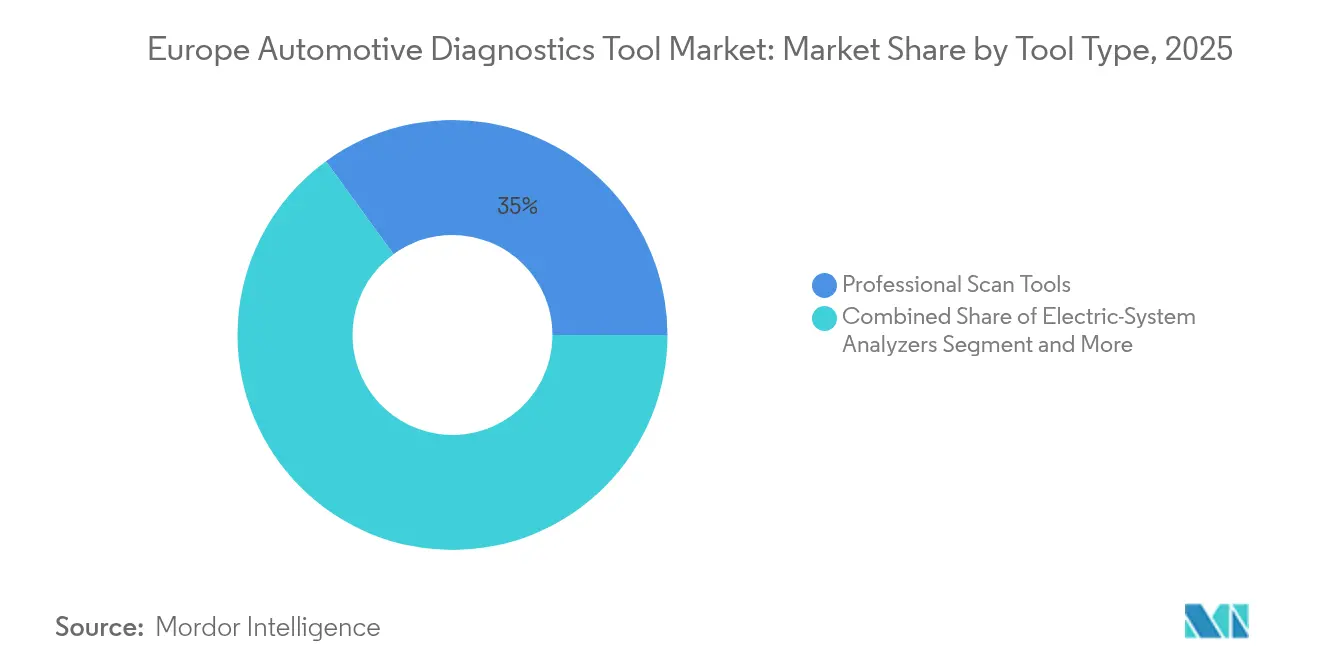

- By tool type, professional scan tools led with 35.02% of the European automotive diagnostic tools market share in 2025, while electric-system analyzers are projected to advance at a 5.41% CAGR to 2031.

- By vehicle type, passenger cars accounted for a 72.88% share of the European automotive diagnostic tools market size in 2025, and light commercial vehicles are on track for the fastest 5.41% CAGR through 2031.

- By propulsion, internal-combustion engines retained 63.70% of the European automotive diagnostic tools market size in 2025, but battery-electric platforms will log the highest 5.46% CAGR to 2031.

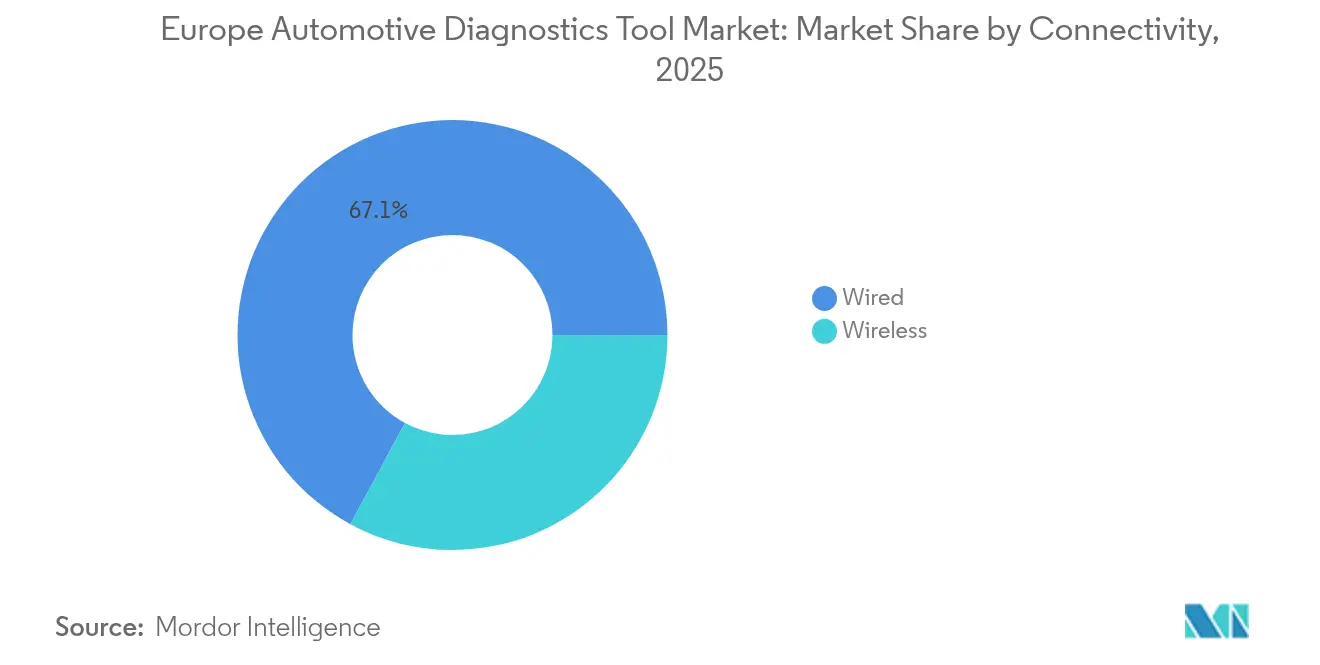

- By connectivity, wired solutions held 67.12% revenue share in 2025, even as wireless tools are forecast to grow at a 5.36% CAGR through 2031.

- By end user, OEM dealerships captured 52.85% share of the European automotive diagnostic tools market size in 2025, while fleet operators represent the fastest-growing constituency at a 5.43% CAGR.

- By country, Germany commanded 28.44% of 2025 revenue; the United Kingdom is set to lead growth at a 5.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Diagnostics Tool Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle Electronics Complexity Surge | +1.5% | Europe-wide, concentrated in Germany, France | Medium term (2-4 years) |

| Tightening Euro 6/7 Emission | +1.2% | EU27 + UK, strongest in urban centers | Short term (≤ 2 years) |

| Uptake Of EV/HEV Diagnostic Requirements | +0.8% | Nordic countries, Netherlands, Germany | Long term (≥ 4 years) |

| EU Right-To-Repair Data-Sharing Mandates | +0.6% | EU27, phased implementation | Medium term (2-4 years) |

| OTA-Update Failure Cost Containment | +0.4% | Premium vehicle markets, Germany, UK | Short term (≤ 2 years) |

| OEM SaaS Monetisation | +0.3% | Western Europe, dealership networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vehicle Electronics Complexity Surge

European cars now integrate multiple electronic control units, a five-fold increase over a decade ago, which forces workshops to adopt scanners capable of interrogating CAN, LIN, FlexRay, and Automotive Ethernet simultaneously. Tools must also verify over-the-air software updates and trace faults that span multiple domains, such as ADAS sensors feeding braking modules. Vendors respond by embedding AI to rank probable faults and to automate test routines that once required expert intervention. Workshops value devices coupled with cloud portals that push protocol updates weekly and allow remote experts to step in when technicians meet unfamiliar architectures. Demand therefore pivots toward integrated packages that combine ruggedized handhelds with browser-based dashboards and subscription billing [1]“Annual Report 2025,” Bosch Mobility Solutions, bosch.com .

Tightening Euro 6/7 Emission-Testing Rules

Euro 7, effective 2025, requires real-world driving emissions monitoring across a vehicle’s entire lifespan, shifting compliance documentation from annual checks to continuous in-service validation. Scan tools must log particulate filter efficiency, catalyst NOx performance, and sensor drift in real time while issuing harmonized reports accepted by national inspection databases. Independent garages require OEM-level access codes to reprogram emission systems after software updates or parts replacement. Portable measurement systems that verify compliance under actual road load conditions are gaining traction among fleet garages serving urban-delivery vans, where low-emission zone fines multiply quickly [2]“Proposal for Euro 7 Regulation,” European Commission, europa.eu.

Uptake of EV/HEV Diagnostic Requirements

Battery-electric and hybrid models reached one-fifth of new registrations in 2024, redirecting diagnostic priorities from fluids and mechanical wear to high-voltage isolation, battery health, and firmware integrity. Electric-system analyzers capable of electrochemical impedance spectroscopy and thermal imaging assessments are replacing conventional pressure testers. In addition to new hardware, garages buy VR-based simulators that allow trainees to practice safe battery teardown without real-world risk. Scan tools must read battery management system logs, compare firmware versions across distributed power electronics, and flag mismatches that impair fast-charging performance. Vendors offering turnkey safety certification, insulated probes, and regularly updated battery chemistry libraries gain share [3]“Equip Auto 2025 Press Release,” MAHLE Group, mahle.com .

EU Right-To-Repair Data-Sharing Mandates

Legislation now requires automakers to provide independent repair shops with the same diagnostic data, security certificates, and guided procedures as those given to franchised dealers. This levels the playing field and spurs adoption of multi-brand tools that can unlock OEM-specific functions, including advanced coding, immobilizer pairing, and ADAS calibration. Cloud vaults that host service manuals in multiple languages improve repair efficiency, while standardized pass-through interfaces simplify connections to secure gateways. Vendors that prove compliance auditing and encrypted data flows are favored by small workshops wary of GDPR penalties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex For Professional Scan Tools | -0.7% | Eastern Europe, independent workshops | Short term (≤ 2 years) |

| Shortage Of EV-Trained Technicians | -0.6% | Europe-wide, concentrated in rural areas | Medium term (2-4 years) |

| Cyber-Security & Data-Privacy Barriers | -0.5% | EU27, GDPR compliance regions | Medium term (2-4 years) |

| Protocol Fragmentation Interoperability Gaps | -0.4% | Multi-brand workshops, independent garages | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex For Professional Scan Tools

Integrated diagnostic stations, with prices varying fairly, are standard in small, family-run garages in Eastern European cities. Rapid technology cycles shorten depreciation periods, making outright purchase risky. While leasing and subscription packages reduce upfront cash outlay, they can double the total cost of ownership over a five-year horizon. Workshops, therefore, seek modular add-ons that augment existing devices rather than replace them entirely. Vendors showcasing backward-compatible probes, license key upgrades, and trade-in credits win contracts in cost-sensitive segments.

Cyber-Security & Data-Privacy Barriers

GDPR demands explicit customer consent for any telematics or diagnostic data stored beyond immediate repair needs, limiting cloud analytics. Tools must log user access, encrypt vehicle identifiers, and purge data on request. Achieving UNECE R155 cybersecurity certification adds months to development and requires continuous incident monitoring. Smaller suppliers struggle with these overheads, and garages wary of liability often favor on-premise solutions that never forward data outside the shop. Secure-by-design platforms that automate consent capture and anonymize files before transferring them to the cloud help ease concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Type: Professional Scanners Lead EV Transition

Professional scan tools held a 35.02% share of the European automotive diagnostic tools market in 2025, underscoring their role as the workshop’s central interface for multi-system troubleshooting. Revenue growth for this segment stems from the expansion of ECU programming features and AI-assisted fault trees, which shorten diagnostic times for complex electronics. Electric-system analyzers, while representing a smaller base, are expected to post a 5.41% CAGR as EV uptake accelerates in Nordic and Western European markets. The shift from mechanical to electrical architectures raises demand for high-voltage isolation testers and battery impedance meters coupled with cloud libraries of cell chemistries.

Professional scanners adapt by adding Ethernet ports, secure gateway authentications, and guided ADAS calibration workflows. Cloud dashboards record every session, allowing shop managers to audit technician efficiency and meet warranty compliance for franchised dealers. Electric-system analyzers differentiate themselves by offering insulated leads, Category III safety ratings, and integrated thermal imaging overlays that reveal cell imbalances in real-time. These features align with EU safety directives for handling batteries exceeding 60 V.

By Vehicle Type: Commercial Fleets Drive Innovation

Passenger cars accounted for 72.88% of the European automotive diagnostic tools market size in 2025, driven by the continent’s extensive private vehicle parc and the routine maintenance cycles associated with it. Demand in this segment centers on rapid throughput and broad brand coverage, making versatile scan tools a necessity. Light commercial vehicles, however, are projected to deliver a 5.41% CAGR, propelled by e-commerce logistics that depend on high vehicle availability. Fleet operators prefer telematics-integrated diagnostics that transmit fault data to centralized dashboards, enabling them to optimize service schedules. Medium and heavy trucks maintain a stable share, driven by safety-critical inspections and compliance with cross-border emissions regulations.

Commercial fleets are increasingly specifying API access, enabling diagnostic outputs to be fed directly into maintenance-management software. This integration allows for predictive part ordering and downtime forecasting. Light van operators in urban zones also require tools capable of instant Euro 7 emission verification to avoid penalties in low-emission zones.

By Propulsion: Electric Powertrains Reshape Requirements

Internal-combustion powertrains retained 63.70% of the European automotive diagnostic tools market share in 2025; however, their share is expected to decline each year as battery-electric models gain traction. EV-focused diagnostic demand grows at the fastest rate, with a 5.46% CAGR, requiring specialized safety gear and firmware interrogation functions that traditional scanners lack. Plug-in hybrids further complicate matters, necessitating dual-stack toolkits that can assess both spark-ignited and high-voltage components. Vendors invest in automatic VIN decoding to load the correct test scripts based on propulsion architecture, reducing human error.

Workshops must now measure battery state-of-health, verify cell balancing strategies, and ensure high-voltage interlock loops function correctly. Thermal runaway risk drives the purchase of infrared cameras integrated into diagnostic carts. For ICE vehicles, focus remains on combustion analysis, after-treatment performance, and turbocharger health. Suppliers bridge the transition by offering modular dongles that attach to legacy scanners and unlock EV routines, preserving prior investments. Training content covering safe disconnection procedures and OEM-specific battery pack layouts is often included with equipment bundles.

By Connectivity: Wireless Platforms Enable Remote Support

Wired interfaces accounted for 67.12% of revenue in 2025 because they deliver uninterrupted power and high data throughput. However, wireless diagnostic platforms are expected to register a 5.36% CAGR as workshops streamline workflows and reduce cable clutter. Bluetooth Low Energy and dual-band Wi-Fi chipsets enable handheld tablets to roam freely around vehicles while transmitting real-time data to cloud servers. Security remains paramount, so solutions incorporate token-based encryption and multi-factor authentication that comply with GDPR and UNECE R155.

The maturation of 5G across Western Europe unlocks low-latency connections that support live video assistance and over-the-air tool updates even in parking lots. Vendors bundle digital work orders that automatically populate from DTC codes, accelerating parts procurement. Wired solutions are not disappearing; instead, they evolve to include Ethernet over USB-C for high-bandwidth ADAS camera calibrations. Hybrid designs that auto-switch between wired and wireless modes offer workshops maximum flexibility and redundancy. As remote diagnostics become mainstream, service providers can triage faults off-site, reserving bay time for repairs rather than initial scans.

By End User: Fleet Operators Embrace Predictive Maintenance

OEM dealerships captured 52.85% of 2025 revenue, leveraging direct access to manufacturer data, security keys, and warranty administration portals. Their dominance persists because late-model vehicles still require brand-specific procedures, which are locked behind secure gateways. Nevertheless, fleet operators are expected to post the swiftest 5.43% CAGR as they integrate vehicle telematics with in-house service facilities. Predictive maintenance models built on continuous fault data reduce unscheduled downtime and save fuel, justifying investment in high-spec diagnostic stations.

Independent aftermarket garages remain essential in regions with large fleets of aging vehicles and offer competitive pricing on routine repairs. The Right-to-Repair mandate empowers them to access OEM data, elevating their role in complex electronic fixes. Tool providers cater to each user tier with differentiated license tiers: complete OEM programming for dealers, cross-brand functions for independents, and API-enabled dashboards for fleets. Training packages tailored to each profile, ranging from dealership-level ADAS alignment courses to fleet-centric battery-swap protocols, complement vendor offerings.

Geography Analysis

Germany generated 28.44% of 2025 revenue for the European automotive diagnostic tools market, reflecting its status as the region’s largest vehicle producer and the headquarters of several diagnostic innovators. Bosch, Continental, and Softing invest heavily in R&D, collectively spending a significant amount each year on mobility technologies, which stimulates domestic demand for cutting-edge workshop equipment. German garages were early adopters of Industry 4.0, integrating scanners with enterprise resource planning systems to streamline parts logistics and inventory management. The market, however, faces a slight drag from slower EV penetration relative to Nordic peers, which delays the complete transition to high-voltage-centric tools.

The United Kingdom is on course to log the fastest 5.34% CAGR through 2031, driven by consolidation in the fragmented repair sector and the rapid digitization of independent garages. Brexit severed some cross-border supply chains, prompting distributors to establish domestic inventory hubs and intensify online parts marketplaces. British workshops experiment with subscription-based diagnostics because flexible billing aligns with fluctuating bay utilization. Government incentives for the development of connected and autonomous vehicles have also spurred the adoption of cloud-enabled scanners that can validate software stacks unique to self-driving prototypes.

Consumer behavior also influences tool selection; nearly half of drivers research repair options online before booking, pushing garages to provide digital diagnostic reports that enhance transparency. Italy, despite reduced domestic production, remains a stronghold for component specialization, and its workshops increasingly prioritize EV-ready analyzers as Stellantis ramps up electrified models. The Nordic countries—Denmark, Sweden, Norway, and Finland—lead in EV density, thereby fostering early demand for battery-centric diagnostics. At the same time, Eastern Europe leans toward budget-conscious solutions optimized for older ICE fleets.

Competitive Landscape

The European automotive diagnostic tools market is moderately fragmented, yet consolidation is accelerating as leading vendors integrate hardware, software, and training into unified ecosystems. Bosch’s KTS series pairs with its Esitronic cloud portal, delivering weekly protocol updates and video support that deepen customer lock-in. Snap-on leverages its ZEUS tablet to offer guided component tests and remote-expert chat, charging monthly fees that turn occasional tool upgrades into recurring income. Continental’s Autodiagnos Drive targets telematics-connected fleets, providing continuous monitoring and predictive maintenance alerts without requiring a cable connection.

Asian entrants such as Autel and Launch inject price competition by bundling extensive model coverage at lower acquisition costs, pressuring incumbents to justify premiums through advanced analytics and secure gateways. Partnerships emerge between tool makers and training academies to fill the EV technician gap; for example, MAHLE collaborates with vocational schools to certify high-voltage competence using its TechPRO suite.

M&A activity focuses on acquiring software firms skilled in AI-driven fault prediction or cloud-native deployment, enabling vendors to expand features without extending development timelines. As diagnostic complexity continues to rise, value shifts from hardware margins to data services, compelling every market participant to refine cybersecurity postures and uptime guarantees.

Europe Automotive Diagnostics Tool Industry Leaders

Robert Bosch GmbH

Snap-On Inc.

Continental AG

Denso Corporation

Delphi Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: MAHLE unveiled the Digital ADAS 2.0 EXTRA calibration system and a major TechPRO 2 scanner update at Equip Auto in Paris, underscoring its focus on EV-ready diagnostics.

- October 2024: Autel introduced the MaxiSys 906 MAX tablet with expanded ADAS calibration functionality, marking a significant upgrade path for workshops using earlier 906 units.

Europe Automotive Diagnostics Tool Market Report Scope

An automotive diagnostic tool can detect and diagnose problems in a car's engine, transmission, brakes, and other systems. It can read error codes, perform system tests, reset warning lights, and provide detailed information about the vehicle's performance.

The European automotive diagnostics tool market has been segmented by offering, vehicle type, product type, workshop equipment, end user, and country. By offering, the report is segmented into diagnostic equipment/hardware and diagnostic software. By vehicle type, the report is segmented into passenger cars and commercial vehicles. By workshop equipment, the report is segmented into exhaust gas analyzer, wheel alignment equipment, paint scan equipment, dynamometer, headlight tester, fuel injection diagnostic, pressure leak detection, and engine analyzer. By end user, the report is segmented into automotive repair and maintenance shops, OEM dealerships, fleet management companies, and other end users. By country, the report is segmented into Germany, United Kingdom, France, Spain, Italy, Netherlands, and Rest of Europe.

By Tool Type

| OBD Scanners |

| Professional Scan Tools |

| Electric-System Analyzers |

| Pressure & Leak Testers |

| Code Readers |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

By Propulsion

| Internal Combustion Engine (ICE) |

| Battery-Electric Vehicle (BEV) |

| Hybrid & Plug-in Hybrid (HEV & PHEV) |

By Connectivity

| Wired |

| Wireless |

By End User

| OEM Dealerships |

| Independent Aftermarket Garages |

| Fleet Operators |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Russia |

| Rest of Europe |

| By Tool Type | OBD Scanners |

| Professional Scan Tools | |

| Electric-System Analyzers | |

| Pressure & Leak Testers | |

| Code Readers | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium & Heavy Commercial Vehicles | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Battery-Electric Vehicle (BEV) | |

| Hybrid & Plug-in Hybrid (HEV & PHEV) | |

| By Connectivity | Wired |

| Wireless | |

| By End User | OEM Dealerships |

| Independent Aftermarket Garages | |

| Fleet Operators | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What diagnostic capability do European workshops prioritize in 2025?

Secure ECU programming and high-voltage battery health analysis rank highest as EV adoption accelerates.

Which vehicle segment drives tool innovation the most strongly?

Light commercial fleets that rely on telematics-integrated diagnostics to reduce downtime are driving feature development.

How does Euro 7 influence equipment purchases?

Continuous real-time driving emission monitoring mandates compel garages to invest in scanners with enhanced data logging and compliance reporting capabilities.

Are wireless diagnostic tools displacing wired connections?

Wireless sessions proliferate, yet wired interfaces still dominate where uninterrupted power and high throughput are indispensable.

Why are subscription models gaining ground?

They convert one-off hardware sales into recurring revenue while ensuring workshops receive weekly protocol updates and remote support.

What limits adoption among small independents?

High upfront costs for professional equipment and cybersecurity compliance obligations remain key hurdles.

Page last updated on: