Europe Automotive Infotainment Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

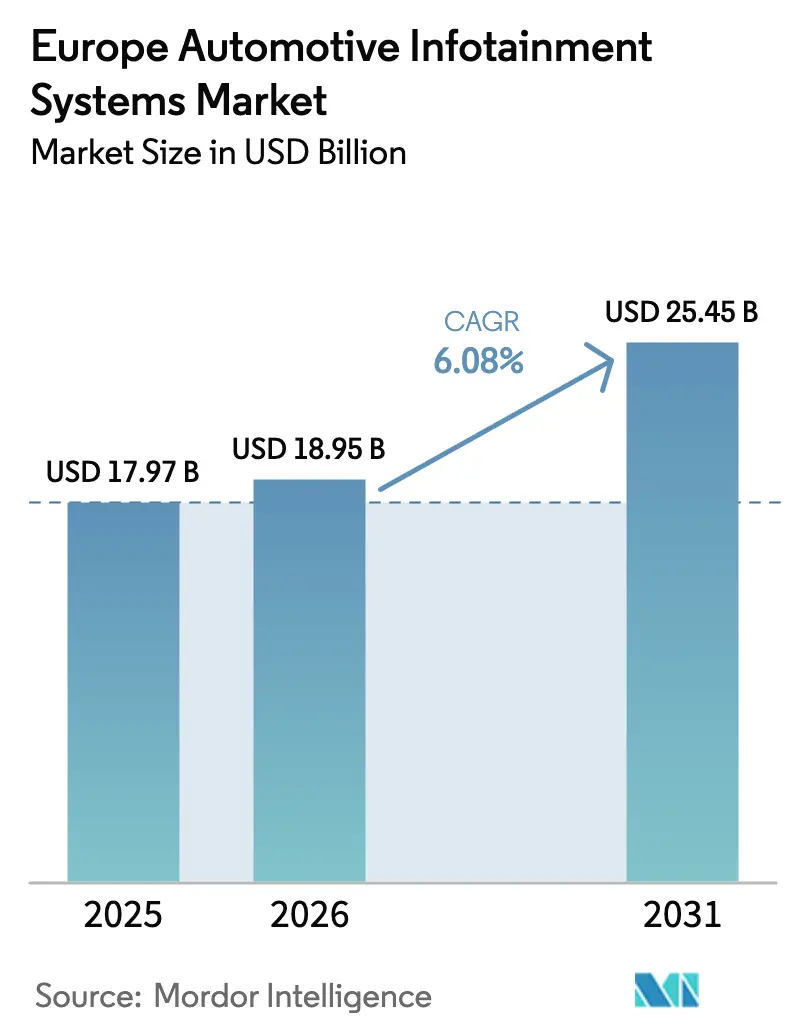

| Base Year Market Size (2025) | USD 17.97 Billion |

| Market Size (2026) | USD 18.95 Billion |

| Market Size (2031) | USD 25.45 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Automotive Infotainment Systems Market Analysis by Mordor Intelligence

The European automotive infotainment systems market size was valued at USD 17.97 billion in 2025 and estimated to grow from USD 18.95 billion in 2026 to reach USD 25.45 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031). This forward trajectory reflects rising battery electric vehicle penetration, tightening European safety mandates, and a shift in value from hardware to recurring software revenue within the European automotive infotainment systems market. Hardware prices are easing as display manufacturing scales, while 5G network slicing, open gateway APIs, and cloud-native operating systems intensify software differentiation across the European automotive infotainment systems market. German premium buyers continue to lead early adoption of large OLED screens and subscription bundles, yet low-cost Chinese battery electric vehicles with feature-rich cockpits now challenge incumbents, widening price-performance tension in the European automotive infotainment systems market.

Key Report Takeaways

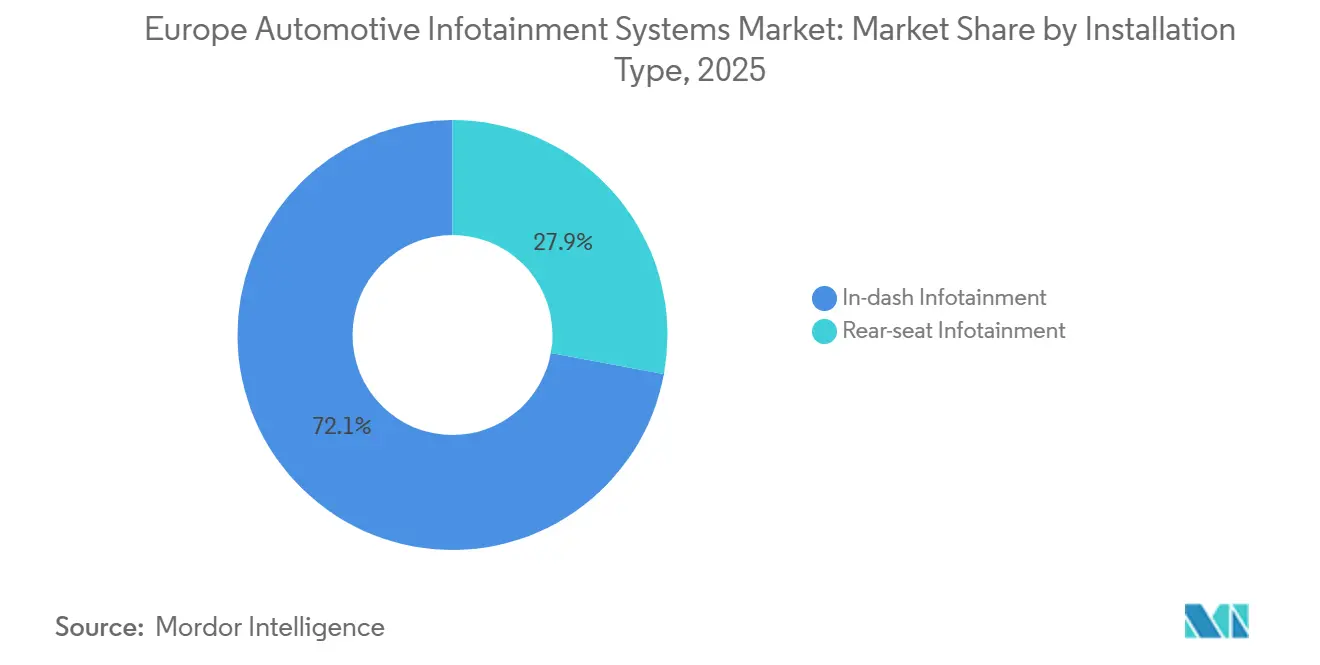

- By installation type, in-dash systems held 72.13% of the European automotive infotainment systems market share in 2025, while rear-seat systems are projected to increase at a 14.27% CAGR through 2031.

- By vehicle type, passenger cars accounted for 86.42% of the European automotive infotainment systems market share in 2025, and battery electric vehicles are forecast to advance at a 38.56% CAGR over the same period.

- By component, display modules commanded 48.29% of the European automotive infotainment systems market size in 2025, whereas operating-system software and apps are expected to grow at a 16.84% CAGR to 2031.

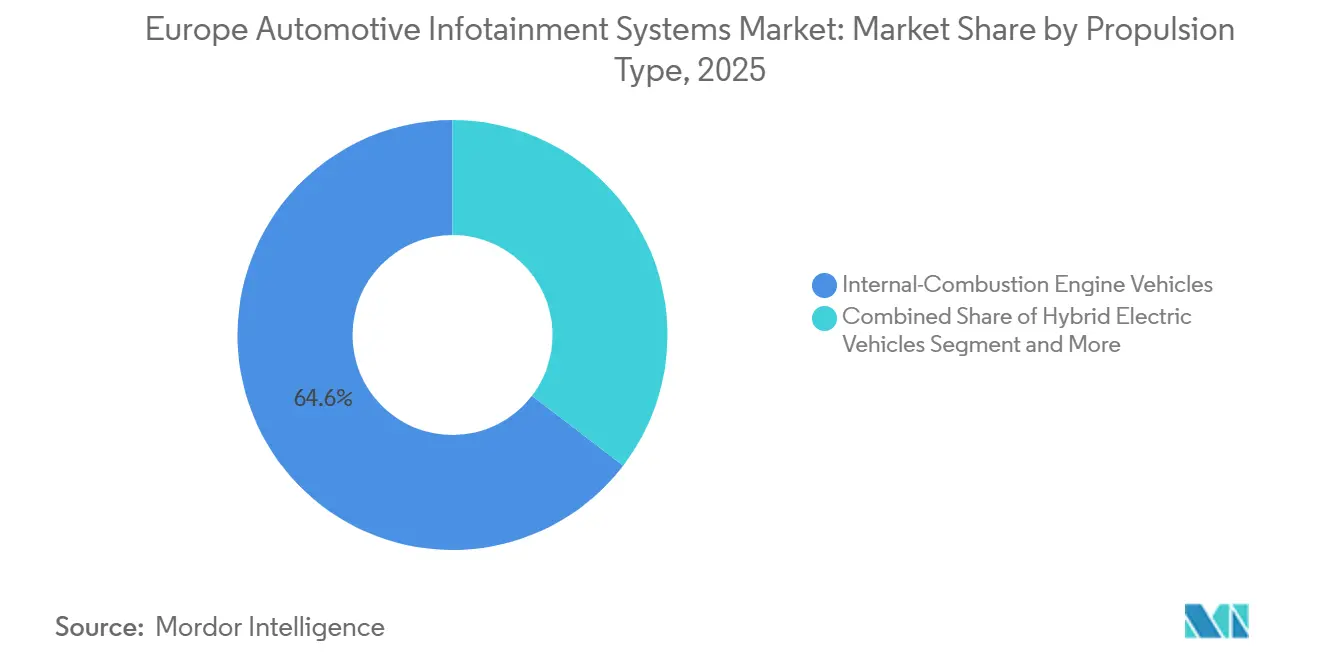

- By propulsion type, internal-combustion vehicles represented 64.58% of the European automotive infotainment systems market share in 2025, while battery electric vehicles are set to expand at a 38.41% CAGR through 2031.

- By connectivity generation, 4G LTE led with 61.37% of 2025 revenue and 5G connectivity is anticipated to register a 24.73% CAGR during the forecast window.

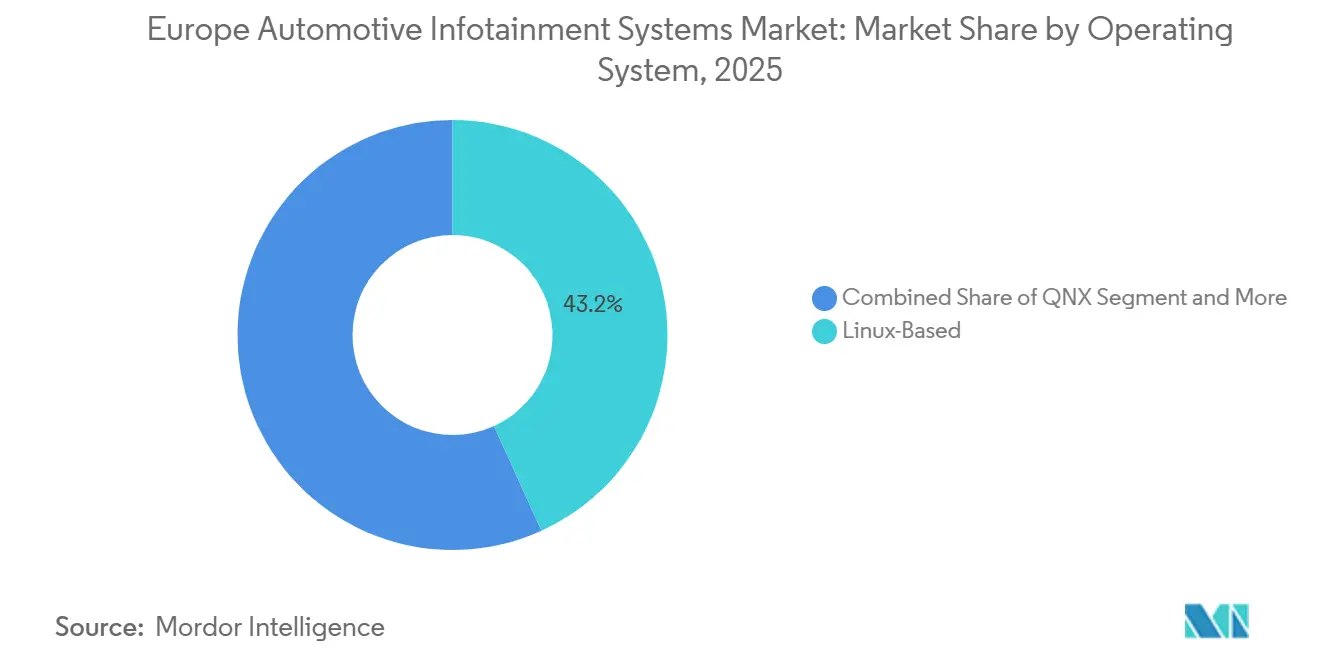

- By operating system, Linux-based platforms made up 43.18% of deployments in 2025 whereas Android Automotive OS is projected to climb at a 21.36% CAGR to 2031.

- By sales channel, original equipment manufacturer-installed systems dominated with 92.74% of the Europe automotive infotainment systems market share in 2025 while the aftermarket segment is poised to grow at a 12.48% CAGR through 2031.

- By geography, Germany generated 22.57% of regional revenue in 2025 and Spain is expected to post the fastest expansion at a 19.94% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Automotive Infotainment Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU eCall and Safety Telematics Mandate | +1.8% | EU-27, United Kingdom | Short term (≤ 2 years) |

| Surge in Electric Vehicle Adoption | +1.5% | Germany, France, Netherlands, Norway-adjacent | Medium term (2-4 years) |

| 5G Stand-Alone Roll-out | +1.2% | Urban Germany, France, Spain | Medium term (2-4 years) |

| Rising Consumer Demand for Smartphone-Like Cockpits | +1.1% | Western Europe, Poland, Czech Republic | Short term (≤ 2 years) |

| Open Gateway APIs Unlocking Cross-Operator QoS | +0.4% | Multinational fleets, premium OEMs | Long term (≥ 4 years) |

| Chinese Entry-Level BEVs Forcing Feature-Rich IVI | +0.3% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU eCall and Safety Telematics Mandate (Reg. 2018/858)

Regulation 2018/858 compels every new passenger car and light commercial vehicle sold in the EU to embed an automatic emergency-call module[1]"Regulation (EU) 2015/758 concerning type-approval requirements for the deployment of the eCall in-vehicle system based on the 112 service," EUR-Lex, eur-lex.europa.eu., anchoring baseline infotainment specifications to include 4G modems and GNSS receivers. Enforcement concluded in 2024, but original equipment manufacturers quickly expanded the mandated module into a revenue hub that layers predictive maintenance alerts, insurance telematics, and stolen-vehicle tracking onto the same hardware. Continental and Bosch now market white-label telematics-as-a-service packages that original equipment manufacturers rebrand inside their own mobility apps. A 2025 Commission assessment showed emergency-response times in rural areas fell 40%, reinforcing consumer acceptance of always-connected cockpits across the European automotive infotainment systems market.

Surge in EV Adoption Driving Energy-Aware Infotainment

Battery electric vehicles captured a significant share of EU passenger registrations in 2025, shifting cockpit priorities from entertainment to energy stewardship. Infotainment systems now integrate battery-thermal modeling, charging-station availability, and range-optimized routing. Volkswagen’s ID.Software 4.0 reserves 5G bandwidth via network slicing to keep charger data current, an upgrade that cut charging-related complaints 28% in Q4 2025. BMW’s 2026 Dutch pilot offers off-peak charging discounts when drivers let infotainment schedule battery sessions, recasting the cockpit as an energy-management console and strengthening stickiness inside the European automotive infotainment systems market.

5G Stand-Alone Roll-Out and Network Slicing for In-Car Data

5G stand-alone cores permit network slices that guarantee low latency for eCall traffic while freeing surplus bandwidth for passenger streaming. Deutsche Telekom, together with partners including BMW Group, Valeo, Ericsson, and Qualcomm Technologies, conducted real‑world demonstrations of 5G Standalone network slicing with controlled Quality of Service (QoS) to support automotive applications[2]"Automated driving with 5G Network Slicing and Quality of Service," Telekom, telekom.com.. GSMA’s 2026 Open Gateway APIs extend these slices across borders so a French vehicle roaming in Spain retains the same QoS contract. Premium OEMs embed the feature to differentiate connectivity, further elevating 5G demand in the European automotive infotainment systems market.

Rising Consumer Demand for Smartphone-Like Digital Cockpits

Buyers now expect seamless voice assistants, fluid touch response, and a wide app catalog mirroring their phones. Android Automotive OS delivers Google Maps, Assistant, and Play Store natively; Volvo, Renault, and Polestar expanded AAOS across full lineups by 2025. Stellantis forecasts USD 21.4 billion in annual software revenue by 2030, with infotainment subscriptions supplying 40%. As hardware commoditizes, the app ecosystem becomes the battleground inside the European automotive infotainment systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Large OLED/Mini-LED Displays | -0.9% | Germany, United Kingdom, France premium | Medium term (2-4 years) |

| Compliance Burden from UNECE R155/R156 Cyber Rules | -0.6% | EU-27, United Kingdom, Switzerland | Short term (≤ 2 years) |

| North-South Electric Vehicle and Connectivity Adoption Divide | -0.5% | Greece, Portugal, Romania rural | Long term (≥ 4 years) |

| Asian Semiconductor Supply Dependency | -0.4% | Pan-European | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Large OLED/Mini-LED Displays and HPC SoCs

LG Display has been supplying advanced flexible P‑OLED panels for Mercedes‑Benz’s MBUX Hyperscreen infotainment system used in EQS and other electric vehicles, supporting curved panoramic display designs across the dashboard[3]"LG and Mercedes-Benz Discusses Expanding "One LG Solution" Collaboration," LG ELectronics, lg.com.. NVIDIA’s DRIVE Orin SoC adds USD 500 per unit, limiting adoption to luxury trims. Mainstream brands such as Volkswagen capped display upgrades at 10 inches in 2025 to preserve margins, restraining premium-screen rollouts in the European automotive infotainment systems market.

Compliance Burden From UNECE R155/R156 Cyber Rules

Starting July 2024, all new vehicle models were required to demonstrate robust cybersecurity measures and secure over-the-air (OTA) channels. In a bid to comply with these stringent regulations, Continental has earmarked a significant portion of its budget for non-recurring engineering across its infotainment initiatives. Meanwhile, smaller suppliers are finding themselves ensnared in extended validation processes, pushing back their product launches in the competitive European automotive infotainment landscape. These regulations, introduced under UNECE R155/R156, aim to enhance vehicle safety and protect against potential cyber threats. As a result, companies are investing heavily in research and development to align with these compliance requirements and maintain their market position.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Installation Type: Rear-Seat Demand Outpaces In-Dash Maturity

In-dash units still held 72.13% revenue share in 2025, upheld by mandatory eCall connectivity, but single-digit growth underscores commoditization. Suppliers compete on integration cost, not screen size, as hardware converges on shared domain controllers. Rear-seat systems instead differentiate through content deals with Disney+ or Xbox Cloud Gaming, accelerating software subscriptions inside the European automotive infotainment systems market.

The rear-seat infotainment segment will climb at a 14.27% CAGR through 2031. Luxury original equipment manufacturers exploit long battery electric vehicle wheelbases to mount dual 11-inch touchscreens, wireless headsets, and gaming modes, delivering a lounge atmosphere. Chauffeur-driven executives in Germany, China, and the Middle East sustain this premium, while family-oriented MPVs in Spain and France expand addressable volumes.

By Vehicle Type: Passenger Cars Lead While BEVs Redefine UX

Passenger cars retained 86.42% share in 2025, anchored by 10.9 million EU registrations, yet battery electric vehicle variants of these cars will grow 38.56% a year. Energy-aware interfaces now display battery thermal state, regenerative-brake scores, and intelligent charging tips, features that elevate cockpit centrality within the European automotive infotainment systems market.

Commercial vans lag volumes but fast-track telematics for fleet optimization. The European Commission’s proposal to extend eCall to more than 3.5-ton trucks enlarges future demand. Medium-duty drivers require digital tachograph integration and real-time load analytics, nudging infotainment suppliers to tailor rugged HMI variants. Passenger-car dominance persists through 2031, yet light commercial vehicle digitization diversifies revenue streams across the European automotive infotainment systems industry.

By Component: Software Captures Value As Screens Plateau

Display modules represented 48.29% of 2025 revenue, but their CAGR trails 16.84% growth in operating-system software and apps. Original equipment manufacturers now embed app stores, cloud gaming, and feature-on-demand unlocks, turning the cockpit into a persistent revenue engine across the European automotive infotainment systems market.

Domain controller commoditization compresses hardware margins. Qualcomm and NXP ship turnkey reference boards that slash BOM by 18% for Visteon SmartCore customers. Subscription bundles, premium navigation, or in-car karaoke, generate >70% gross margin, shifting profitability toward software even while screens remain the largest absolute pool.

By Propulsion Type: Electrification Spurs Deep Integration

Internal combustion engine vehicles hold 64.58% of the European automotive infotainment systems market share in 2025, while battery electric vehicles surge at 38.41% a year. Their flat floors free cabin space for larger displays, and battery-aware HMI becomes mission-critical. Tesla’s “Camp Mode” sparked copycats from Ford and Volkswagen, illustrating how infotainment manages energy as much as entertainment.

Internal combustion engine vehicles dominate the installed base, but face subdued growth as the EU bans new sales by 2035. Hybrids plateau near 25% share by 2028, offering fewer unique infotainment hooks. Original equipment manufacturer differentiation pivots toward BEV-centric UX, cementing software-defined strategies in the European automotive infotainment systems market.

By Connectivity Generation: 5G Momentum Builds Despite Rural Lag

4G LTE led with 61.37% revenue in 2025, yet 5G stand-alone subscriptions will compound 24.73% annually. Original equipment manufacturers market 5G cockpits as “future-proof” and exploit slices to isolate safety telemetry from 4K streaming. Vodafone closed its German 3G network in 2024, forcing retrofit head units to upgrade or risk losing data.

Rural Greece and Romania still operate on patchy 4G, so original equipment manufacturers tier 5G as a premium option. The Commission’s 2030 corridor-coverage mandate will close gaps, making 5G the default baseline in the European automotive infotainment systems market by decade-end.

By Operating System: Android Automotive OS Scales Fastest

Linux derivatives held a 43.18% share in 2025, but Android Automotive OS alone will rise 21.36% per year. Google Maps' electric vehicle routing and Assistant voice control outweigh concerns about data sovereignty for several original equipment manufacturers. Volvo and Renault completed full-line Android Automotive OS (AAOS) rollouts by 2025, while Polestar commits through 2031.

QNX remains entrenched in safety clusters but recedes in infotainment. OEMs that crave data ownership, such as Volkswagen’s Cariad, continue adapting Automotive Grade Linux, balancing openness and brand experience. The operating-system battlefield shapes ecosystem control throughout the European automotive infotainment systems market.

By Sales Channel: Factory Fit Dominates, Aftermarket Finds Niches

Original equipment manufacturer installation covered 92.74% of 2025 shipments thanks to deep CAN and ADAS integration. Aftermarket vendors target aging fleets in Poland, Romania, and Bulgaria, pushing plug-and-play eCall dongles that win insurance discounts. Growth sits at 12.48% but remains niche.

Modern domain controllers unite HVAC, lighting, and ADAS on shared silicon, making later swap-outs costly. Nevertheless, enthusiast communities still retrofit 12-inch Android screens into decade-old Volkswagen Golfs, keeping a small but steady revenue pocket alive in the European automotive infotainment systems market.

Geography Analysis

Germany generated 22.57% of 2025 revenue, driven by Volkswagen, BMW, and Mercedes production volumes and a EUR 1,850 average infotainment spend per vehicle. High purchasing power sustains early adoption of OLED hyper-screens and 5G packages. Yet Chinese entrants opened local HQs in 2024 and price-damaged premium tiers, pressuring incumbent margins across the European automotive infotainment systems market.

Spain delivered the strongest trajectory, poised to post a 19.94% CAGR through 2031. Government PERTE VEC subsidies worth EUR 4.3 billion attracted Stellantis and Ford to base BEV lines near Valencia, pulling Visteon and Harman into new Barcelona and Madrid tech hubs. Infotainment demand follows production scale as suppliers localize just-in-time.

France, the United Kingdom, and Italy collectively hold a significant share. France leverages Renault-Nissan’s shared AAOS cockpit, reaching 1.2 million installs in 2025. The United Kingdom wrestles with a slower rural 5G rollout post-Brexit, tempering growth despite Nissan’s Sunderland Ariya output. Italy’s luxury niche commands high ARPUs with bespoke Maserati and Ferrari systems, albeit on small volumes.

Competitive Landscape

Continental, Bosch, Harman, Visteon, and Panasonic Automotive controlled a significant share of 2025 revenue, marking moderate concentration. Each pivots toward software-defined vehicle platforms that merge infotainment, ADAS, and telematics on shared compute, minimizing redundant ECUs. Semiconductor suppliers erode Tier-1 leverage: Qualcomm’s Snapdragon Digital Chassis won 28 European design slots by Q4 2025, while NVIDIA DRIVE Orin powers Mercedes and Volvo domain controllers.

Strategic moves include Bosch’s 2025 alliance with Microsoft for Azure-based voice processing, Continental’s 2024 acquisition of an AR HUD startup to enrich cockpit visuals, and Harman’s 2025 Madrid hub to accelerate AAOS integrations. Chinese Tier 1s such as Huawei IAS and Desay SV now pitch complete infotainment stacks with built-in AI assistants, targeting value-focused OEMs.

Regulatory readiness shapes vendor selection; ISO 21434 cyber certifications became a sourcing gate in 2025. Continental embedded UNECE R155 templates into its reference architecture, shaving OEM audit cycles by three months. Patent filings tilt to software: 60% of Continental’s 2024–2025 infotainment patents addressed secure OTA pipelines, underscoring the service-centric future of the European automotive infotainment systems market.

Europe Automotive Infotainment Systems Industry Leaders

-

Continental AG

-

Robert Bosch GmbH

-

Denso Corporation

-

Pioneer Corporation

-

AISIN CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Qualcomm Technologies confirmed a multi-year collaboration with Volkswagen to supply Snapdragon Digital Chassis platforms for the automaker’s next-generation software-defined vehicle architectures. The partnership will support infotainment, telematics, and ADAS processing, enabling connected cockpits with high-performance SoCs starting with 2027 model-year vehicles.

- January 2026: BMW unveiled its latest iDrive system, featuring a large touchscreen and integrated Amazon Alexa Plus voice assistant. The upgrade significantly enhances user experience, making the cockpit more interactive and connected across the brand’s lineup.

- September 2025: Harman International presented its latest cockpit innovations at IAA Mobility 2025, including modular telematics, AR-style displays, and enhanced connectivity solutions. The showcase highlighted the company’s push to integrate infotainment, driver monitoring, and software-defined services.

Europe Automotive Infotainment Systems Market Report Scope

Automotive infotainment is an in-vehicle device that provides entertainment and information to the driver and passengers. The system includes the integration of audio/video (A/V) interfaces, touchscreens, keypads, etc., for offering navigational services, hands-free phone connections, vehicle voice control, parking assistance, climate control, two-way communication tools, access to the internet, and other security services. These features help in increasing the operational efficiency of vehicles and improving safety and drivThe er experience.

The scope of the report includes Installation Type (In-dash Infotainment and Rear-seat Infotainment), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Medium and Heavy Commercial Vehicles), Component (Display/Touch-Screen Module, Head Unit/Domain Controller, Operating-System Software and Apps, and Connectivity ICs and Antenna Modules), Propulsion Type (Internal-Combustion Engine Vehicles, Hybrid Electric Vehicles, and Battery Electric Vehicles), Connectivity Generation (Legacy 2G/3G, 4G LTE, and 5G), Operating System (Linux-Based, QNX, Android Automotive OS, and Others), Sales Channel (OEM-Installed and Aftermarket), and Country (Germany, United Kingdom, France, Italy, Spain, Russia, and Rest of Europe). For each segment, market sizing and forecast have been done on the basis of value (USD Million).

| In-dash Infotainment |

| Rear-seat Infotainment |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Display/Touch-Screen Module |

| Head Unit/Domain Controller |

| Operating-System Software and Apps |

| Connectivity ICs and Antenna Modules |

| Internal Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Legacy 2G/3G |

| 4G LTE |

| 5G |

| Linux-Based (AAOS, AGL, etc.) |

| QNX |

| Android Automotive OS |

| Others (Proprietary, RTOS) |

| Original Equipment Manufacturer (OEM) Installed |

| Aftermarket |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Installation Type | In-dash Infotainment |

| Rear-seat Infotainment | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| By Component | Display/Touch-Screen Module |

| Head Unit/Domain Controller | |

| Operating-System Software and Apps | |

| Connectivity ICs and Antenna Modules | |

| By Propulsion Type | Internal Combustion Engine Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| By Connectivity Generation | Legacy 2G/3G |

| 4G LTE | |

| 5G | |

| By Operating System | Linux-Based (AAOS, AGL, etc.) |

| QNX | |

| Android Automotive OS | |

| Others (Proprietary, RTOS) | |

| By Sales Channel | Original Equipment Manufacturer (OEM) Installed |

| Aftermarket | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe automotive infotainment systems market in 2026?

The market stands at USD 18.95 billion in 2026 and is forecast to reach USD 25.45 billion by 2031.

Which installation type segment is the fastest-growing in Europe for automotive infotainment?

Rear-seat systems show the highest growth, advancing at a 14.27% CAGR through 2031.

What role does 5G play in European in-car infotainment?

5G enables network slicing that separates safety telemetry from passenger streaming, and 5G connections are projected to grow at 24.73% per year.

Why are battery electric vehicles critical to cockpit innovation?

BEVs require energy-aware interfaces for range and charging management, driving deep integration between the infotainment head unit and battery systems.

Which countries drive the most demand for advanced infotainment?

Germany leads revenue due to premium adoption, while Spain records the fastest growth because of aggressive EV manufacturing expansions.

Who are the leading suppliers in the European infotainment space?

Continental, Bosch, Harman, Visteon, and Panasonic Automotive collectively hold nearly half of 2025 market revenue.

Page last updated on: