Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

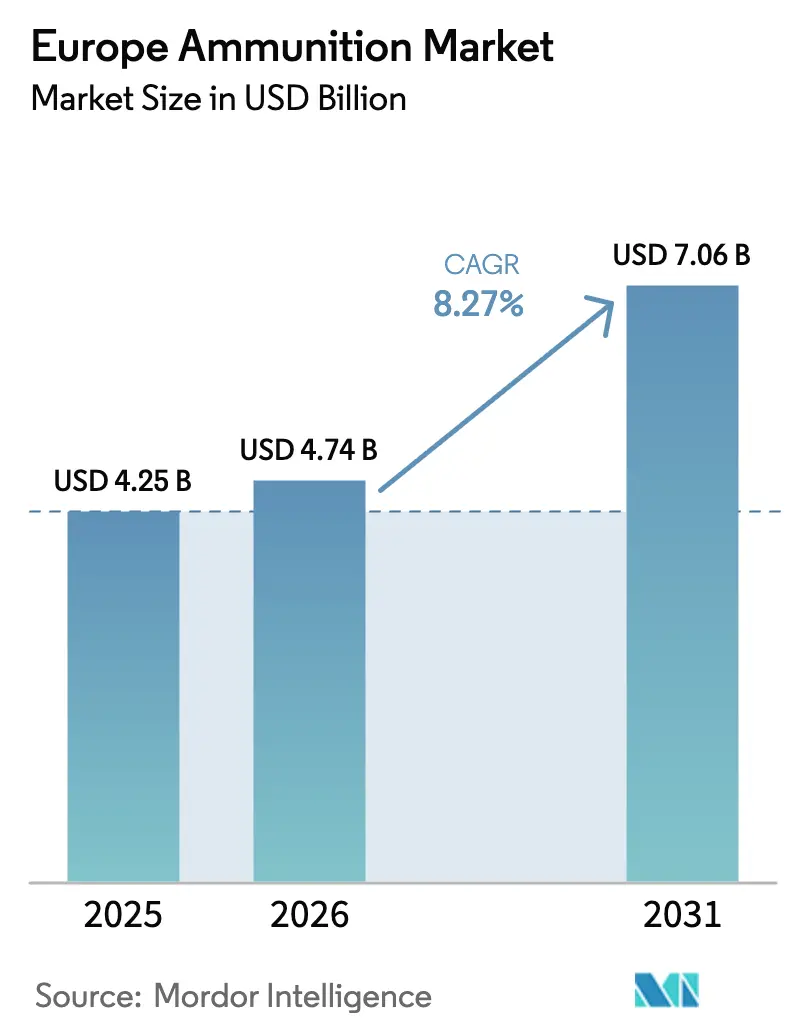

| Base Year Market Size (2025) | USD 4.25 Billion |

| Market Size (2026) | USD 4.74 Billion |

| Market Size (2031) | USD 7.06 Billion |

| Growth Rate (2026 - 2031) | 8.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ammunition Market Analysis by Mordor Intelligence

The Europe ammunition market size is expected to grow from USD 4.25 billion in 2025 to USD 4.74 billion in 2026 and is forecasted to reach USD 8.08 billion by 2031 at 11.24% CAGR over 2026-2031. Wartime consumption patterns stemming from the Russia-Ukraine conflict have shifted procurement priorities toward volume and readiness, reshaping the Europe ammunition market through multi-year contracting and urgent capacity additions. Industrial policy now favors assured production slots, sovereign control of key energy sources, and the distribution of manufacturing across multiple allied sites to reduce bottlenecks and logistics risk. Guidance-enabled munitions are gaining share for counter-battery and precision tasks, while unguided rounds remain the backbone for sustained ground operations. The result is an elevated baseline for orders that supports new lines for 155mm shells, propellants, and fuzes, which keeps the Europe ammunition market on a higher growth trajectory than before 2022.

Key Report Takeaways

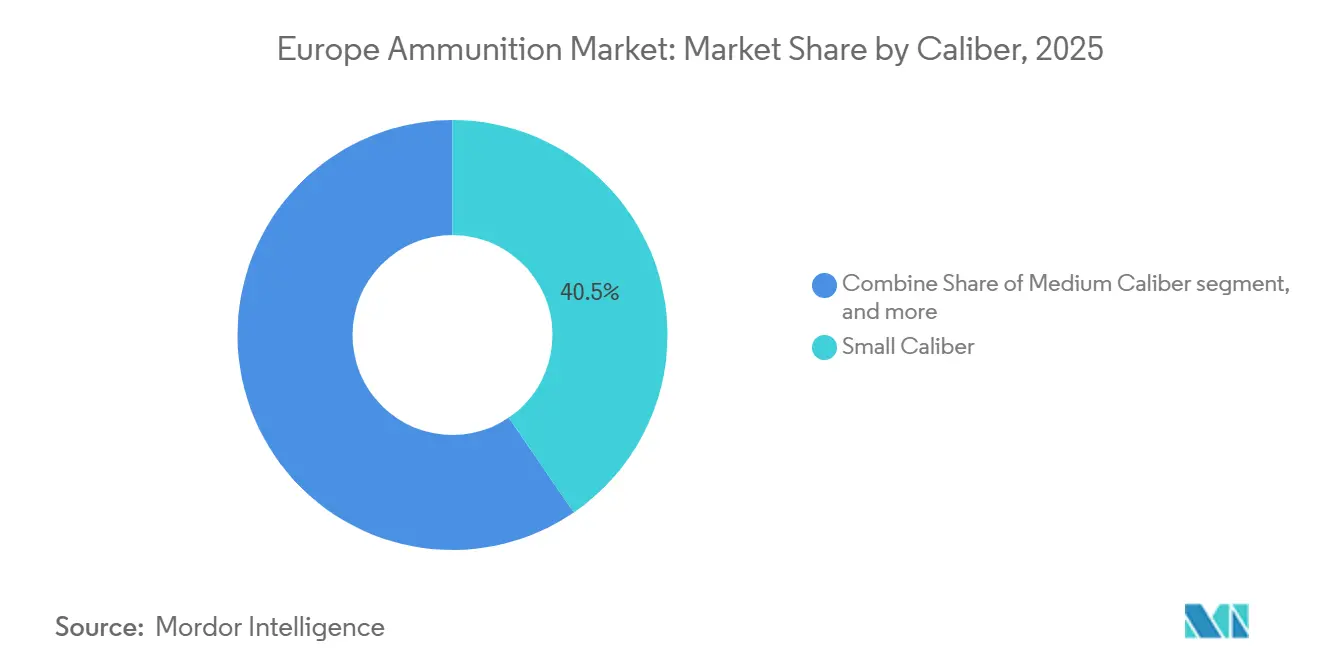

- By caliber, small caliber led with 40.47% revenue share in 2025, while large caliber is projected to expand at a 9.87% CAGR through 2031.

- By product, bullets and cartridges commanded a 63.68% share in 2025, and artillery shells and mortars are set to grow at a 10.67% CAGR between 2026 and 2031.

- By end-user, the military segment accounted for 78.93% of the market in 2025 and is projected to grow at an 11.21% CAGR through 2031.

- By platform, land-based systems accounted for 65.27% of demand in 2025 and are forecasted to grow at a 9.93% CAGR to 2031.

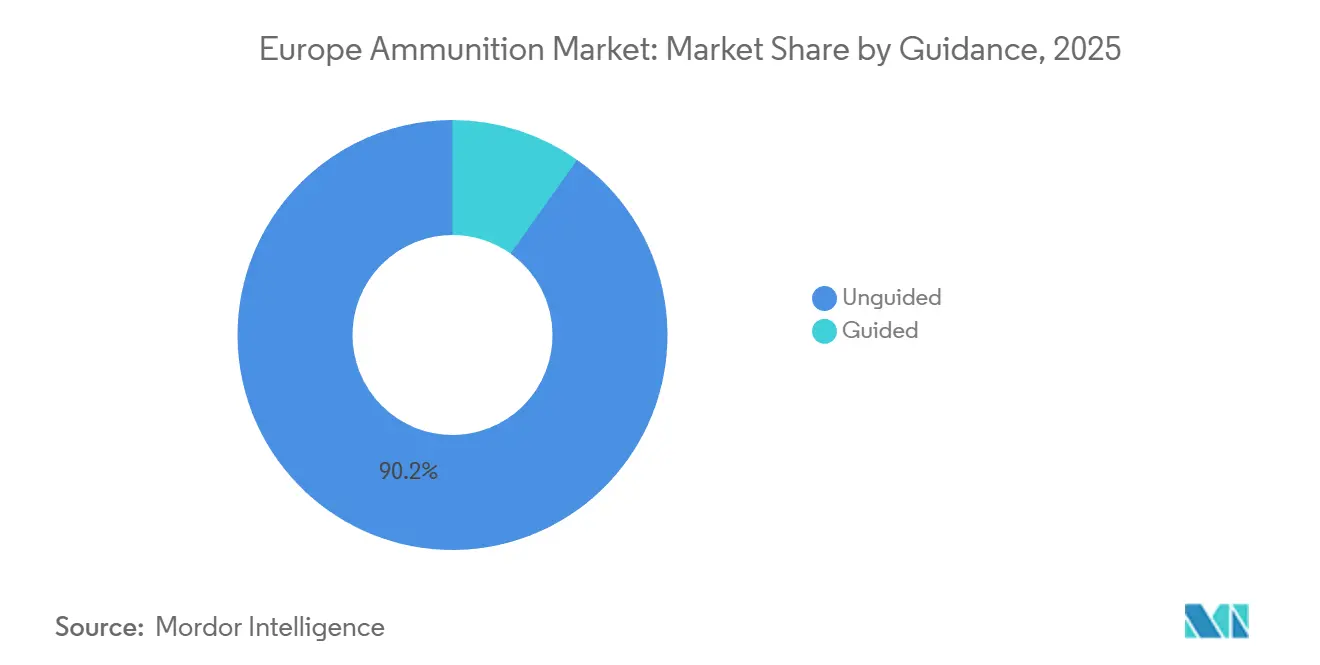

- By guidance, unguided munitions accounted for 90.15% of volumes in 2025, while guided ammunition is projected to grow at a 10.12% CAGR to 2031.

- By geography, the Rest of Europe led with a 31.96% share in 2025, while Russia is expected to be the fastest-growing region, with an 11.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Ammunition Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU/NATO stockpile replenishment accelerates artillery (155 mm) demand | +2.8% | Germany, France, Poland, Nordic countries | Medium term (2-4 years) |

| Multi-year European defense budgets and framework orders stabilize ammo demand | +1.9% | Global Europe, concentrated in major NATO contributors | Long term (≥ 4 years) |

| Rapid EU industrial ramp-up: new 155mm lines, propellant capacity, localization | +2.2% | Germany, France, Czech Republic, Poland, Spain | Medium term (2-4 years) |

| Shift to precision/guided and extended-range munitions across platforms | +1.4% | Western Europe core, spillover to Eastern NATO members | Long term (≥ 4 years) |

| Eastern Europe co-production and Ukraine licensing unlock new capacity nodes | +1.3% | Poland, Czech Republic, Romania, Bulgaria, Ukraine partnerships | Medium term (2-4 years) |

| Environmental shift to lead-free and synthetic propellants drives capex cycle | +0.9% | EU member states subject to REACH regulation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU/NATO Stockpile Replenishment Accelerates Artillery (155 mm) Demand

European inventories proved shallow in 2022, which triggered a shift from lean peacetime stocks to wartime readiness with specific artillery depth goals. The EU’s Act in Support of Ammunition Production and allied bilateral commitments set explicit round delivery targets for 155mm shells to rebuild stocks beyond immediate transfers to Ukraine. Defense ministries now treat ammunition depth as a formal readiness metric in NATO defense planning, which locks in recurring buys and contributes to structural demand.[1]NATO, “Defence Planning and Ammunition Readiness,” NATO, nato.int Governments accepted higher unit prices, co-financed brownfield expansions, and prioritized assured slots over competitive tendering, which aligns production tempo to the new stockpile baselines. This reconfiguration sustains a high-order floor and keeps capacity additions focused on 155mm, anchoring growth in the Europe ammunition market through 2031.

Multi-Year European Defense Budgets and Framework Orders Stabilize Ammo Demand

Budgeting practices shifted to multi-year appropriations and framework contracts, which offer visibility for suppliers making significant investments in energy and infrastructure lines. France’s 2024-2030 military program and Germany’s special fund structure ring-fence ammunition funding streams to simplify execution and accelerate awards. Nordic partners are aggregating orders through joint structures to pool demand, create scale, and reduce volatility in a historically cyclical category. This model aligns with the capital profile of ammunition plants, where fixed costs and safety compliance are high and payback periods are lengthy, thereby reducing demand shock risk for private operators. The result is predictable throughput and steadier utilization, which underpins the Europe ammunition market as national programs ramp and then sustain replenishment.

Rapid EU Industrial Ramp-Up, New 155mm Lines, Propellant Capacity, Localization

Large primes and mid-tier suppliers announced capacity expansions for shells, propellants, and energetics since 2022, with the focus on 155mm rounds.[2]Rheinmetall, “Artillery Ammunition Production Expansion,” Rheinmetall, rheinmetall.com Projects reactivate mothballed facilities, add automated filling lines, and localize propellant production, which reduces reliance on external suppliers for critical inputs. Eastern European plants are being refitted for NATO standards, utilizing existing explosive safety perimeters and site permits, which compresses approval cycles compared to greenfield builds. Distributed networks also lower cross-border licensing exposure for Class 1.1 materials and improve resilience against single-point failures. These steps raise effective output ceilings and strengthen the supply base, supporting sustained growth in the Europe ammunition market.

Shift to Precision/Guided and Extended-Range Munitions Across Platforms

Procurement is shifting a portion of indirect fires to guided and extended-range projectiles for standoff counter-battery and selective strike missions. Programs such as France’s KATANA and Germany-backed Vulcano expand range and accuracy for self-propelled howitzers that must operate outside enemy rocket artillery envelopes. Precision reduces rounds-per-target for high-value nodes, which eases logistics but raises unit cost, so forces employ mixed loads that combine unguided volume and guided first-round effects. Small-caliber airburst rounds for 30mm and 40mm are emerging for counter-UAS roles, although integration and cost limitations limit near-term fielding to specialized units. Adoption is steady because the operational advantages are clear, and this layered approach strengthens demand diversity within the Europe ammunition market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosives/powder bottlenecks (TNT, RDX, nitrocellulose) constrain output | -1.6% | Across Europe, particularly affecting new entrants | Short term (≤ 2 years) |

| Fragmented procurement and ammo standardization frictions increase costs | -1.1% | EU-wide, most acute in smaller NATO members | Medium term (2-4 years) |

| High energy prices and long tooling lead-times limit ramp speed | -0.8% | Energy-intensive production hubs in Germany, Italy, Spain | Short term (≤ 2 years) |

| Third-country export commitments divert EU capacity and keep prices elevated | -0.7% | Western Europe exporters, Germany, France, Belgium, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosives/Powder Bottlenecks (TNT, RDX, Nitrocellulose) Constrain Output

Energetics output for TNT and RDX runs well below historic peak capacity in Europe after decades of site closures and consolidation. Environmental restrictions reduced nitrocellulose production within the bloc, making spikes in demand harder to meet without imports from non-allied suppliers. Restarting mothballed energy lines requires safety reviews and new permitting, while brand-new plants face local opposition and high insurance costs. The tightest constraint shows up in 155mm melt-pour operations and insensitive munitions qualification, which prevents simple throughput gains from staffing or extra shifts.[3]NATO, “Insensitive Munitions and Qualification,” NATO, nato.int This bottleneck keeps supply below political targets in the near term and caps how fast the Europe ammunition market can scale.

Fragmented Procurement and Ammo Standardization Frictions Increase Costs

Divergent technical standards, testing protocols, and quality assurance requirements across national agencies limit scale economies for pan-European runs. STANAG baselines help, but national deviations for propellants, primers, and shelf-life testing force suppliers to qualify multiple variants per caliber. Smaller buyers struggle to justify unique specs yet hesitate to adopt larger nations’ standards, which keeps batch sizes small and inventory segmented. This environment favors large, vertically integrated players who can afford parallel qualifications and discourages mid-tier competitors from contesting multi-country frameworks. The result is a higher cost per unit and slower harmonization, which weighs on competitiveness in the Europe ammunition market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Caliber: Large-Caliber Artillery Drives Fastest Expansion

Small-caliber ammunition held 40.47% of the Europe ammunition market share in 2025, covering 5.56mm, 7.62mm, and 9mm rounds across military, law enforcement, and sporting uses. The large-caliber band is the fastest-moving caliber, with the Europe ammunition market size for large caliber projected to expand at a 9.87% CAGR from 2026 to 2031 as stockpile targets are reset. This shift reflects a transition from maintenance levels to wartime modeling, where artillery consumption rates dictate daily needs on a large scale. Manufacturers are aligning their products to NATO-standard 155mm, as well as legacy 152mm and 122mm lines, to serve both donors and frontline users. Incremental growth in small-caliber systems is tied to training hours and force structure, whereas medium-caliber systems track vehicle modernization, requiring more complex airburst and fuzing capabilities.

The caliber mix also mirrors platform doctrine and logistics realities seen in recent high-intensity operations. Heavy indirect fire needs are now prioritized based on counter-battery survivability, which places a premium on artillery depth and availability.[4]NATO, “Indirect Fire and Counter-Battery Lessons,” NATO, nato.int Medium caliber benefits from new infantry fighting vehicles that require programmable rounds and improved lethality against drones and light armor. Small-caliber pricing faces pressure as reformulation to lead-free standards proceeds and as legacy stocks re-enter the supply chain. At the same time, demand remains stable due to training cycles and sports shooting in select countries. The broader mix supports sustained investment in filling lines, fuzing, and case production, which reinforces capacity utilization in the Europe ammunition market.

By Product: Artillery Shells and Mortars See Strongest Demand Surge

Bullets and cartridges commanded 63.68% of the Europe ammunition market share in 2025, reflecting high run-rate volumes across services and civilian channels. Artillery shells and mortars are expected to grow at a 10.67% CAGR through 2031 as countries rebuild their indirect fire stocks and adapt to revised readiness benchmarks. Procurement concentration in 155mm high-explosive, extended-range, and rocket-assisted rounds accelerates to support counter-battery and broader maneuver operations. Mortars gain traction as battalion-level organic fires, reducing reliance on divisional assets in contested environments. Aerial bombs and grenades see steadier demand as air forces prioritize stand-off precision, not gravity munitions, in most planning scenarios.

The Europe ammunition industry is also retooling for greener materials in bullets and cartridges as lead phase-outs expand, which temporarily tightens supply during line transitions. Indirect fire rounds recover investment first because backlogs and strategic stock objectives are most clearly defined in that category. Law enforcement and sporting channels contribute consistent orders of bullets and cartridges, though volumes are small relative to military demand. Product complexity rises for indirect fires with extended range and improved fuzing, which supports higher unit values and longer qualification cycles across the Europe ammunition market.

By Guidance: Unguided Munitions Dominate, Guided Segment Accelerates

Unguided munitions represented 90.15% of 2025 volumes, a reflection that volume fire remains decisive in sustained ground campaigns. Guided categories are expected to expand at a 10.12% CAGR through 2031, as artillery and mortar projectiles incorporate GPS or INS kits for standoff and precision. Mixed loads are becoming the standard as forces match target values to round types, balancing cost, logistics, and collateral risk. France and Germany's programs for guided projectiles demonstrate the doctrinal move to extend range and limit counter-battery exposure. The Europe ammunition industry is also testing 30mm and 40mm airburst ammunition for counter-UAS missions to enhance first-shot effectiveness in mobile units.

Cost differentials remain large between guided and unguided rounds, so guided shares stay modest in most combat loads. Integration requires fire-control updates and new software baselines, which lengthen fielding cycles. Despite constraints, the operational benefits make guided munitions a durable growth niche within the broader Europe ammunition market. Demand signals are now clear enough to support steady investment in guidance kits and compatible fuzes that can scale across multiple platforms.

By End-User: Military Segment Sustains Double-Digit Growth

The military segment accounted for 78.93% in 2025 and is projected to grow at 11.21% CAGR through 2031, supported by stockpile mandates and framework contracts that guarantee take-or-pay volumes. Law enforcement purchases follow personnel growth and pistol fleet upgrades, while sporting demand varies according to regulations and participation rates. The Europe ammunition market size associated with military procurement is anchored by multi-year agreements that stabilize plant utilization and justify capital expenditures. National budgets now treat ammunition as a strategic inventory, marking a departure from earlier cost-minimizing approaches. Civilian demand remains small compared to military-run rates, so manufacturers plan their centers around defense programs to meet volume and scheduling needs.

Growth in military off-take also shapes supplier structure and capital allocation. Defense ministries are underwriting expansions to lift throughput and stockpile depth, which signals steady demand across the planning horizon. Revenue certainty enables suppliers to staff higher shift patterns and maintain surge capacity, thereby improving their responsiveness to future spikes. This structure supports resilience and keeps momentum in the Europe ammunition market during the forecast period.

By Platform: Land-Based Systems Command Investment Priority

Land-based platforms accounted for 65.27% of demand in 2025 and are forecast to grow at a 9.93% CAGR to 2031, reflecting the central role of artillery, mortars, and vehicle cannons in European defense concepts. Naval ammunition grows steadily with new frigates and patrol vessels, while airborne categories are smaller and skew to precision missiles rather than volume munitions. Land dominance stems from contested airspace and dense air defense, which elevate the importance of ground fires for tactical outcomes. Tank and howitzer reloads lead near-term procurement plans in several countries, with synchronized investments in propellants and fuzing to support range and survivability goals. The platform needs to align with the Europe ammunition industry's investment cycle, where land munitions receive priority in funding and capacity.

For navies and air forces, ammunition planning remains more measured and aligned to planned refits and integration projects. Maritime programs refresh magazines for modern 76mm and 127mm guns as new hulls are commissioned over the decade. Air arms allocate funding to sensors and electronic warfare, which narrows ammunition budgets to targeted missile programs with complex integration requirements. This balance favors land growth and keeps the output mix weighted to ground systems across the Europe ammunition market.

Geography Analysis

By Geography: Russia Leads Growth, Rest of Europe Holds Largest Share

The Rest of Europe held a 31.96% share in 2025, while Russia is forecasted to expand at an 11.30% CAGR through 2031 as domestic capacity replaces sanctioned imports and supports ongoing operations. The Europe ammunition market size for the rest of Europe reflects aggregated demand from Nordic members, the Balkans, Iberia, and neutral states that are revising posture and stockpiles. Major EU economies exhibit varying growth rates due to differences in industrial maturity, supplier base, and roles within NATO. Germany and Poland are scaling 155mm lines and co-production to distribute load and reduce transit and permitting risk for explosives.[5]MESKO, “Polish Ammunition Programs,” MESKO, mesko.com.pl France maintains an integrated supply chain for small, medium, and artillery ammunition, with state-aligned industry consolidation aimed at increasing scale and export strength.

The UK is rebuilding domestic production through public-private agreements that guarantee minimum volumes, thereby reducing its reliance on imports for critical types of ammunition. Italy and Spain grow at steadier rates as they maintain stocks and join joint frameworks that pool demand for better negotiations with suppliers. Russia’s trajectory is shaped by an autarkic policy that directs state-owned enterprises to expand production of artillery, mortars, and small arms for sustained operations. The geographic pattern highlights a market where more than 30 sovereign buyers maintain their own budgets and standards, generating opportunities for regional champions and complicating efforts to achieve scale. This structure continues to define the competitive landscape and procurement rhythms within the Europe ammunition market.

Competitive Landscape

Market structure is moderately concentrated in artillery and medium calibers, where scale, safety compliance, and energetic capabilities act as barriers; meanwhile, small calibers remain more fragmented, with regional producers. Rheinmetall, BAE Systems, KNDS, and Leonardo together control a significant revenue share and possess vertical integration covering explosives, propellants, projectile machining, and fuzing. Eastern European suppliers, such as MESKO and the Czechoslovak Group, expand their footprint through cost advantages and proximity to priority deliveries, including Soviet-standard calibers. Governments favor capacity assurance and sovereign access over the lowest price, which drives co-investment in new lines and more sole-source awards. This policy choice supports robust throughput and reinforces the Europe ammunition market during the forecast window.

Strategic moves highlight the new playbook. Rheinmetall completed a new 155mm plant under a framework deal with the Bundeswehr to secure utilization. KNDS secured a multi-year 155mm contract from France, with co-funding for propellant expansion at Eurenco. Nammo expanded nitrocellulose capacity to reduce import reliance, while BAE Systems reactivated production in England to rebuild domestic supply. Elbit Systems Europe invested in guided mortar capabilities in Italy to serve precision needs, and General Dynamics OTS won a multi-country 30mm order under an EDA framework. These moves reflect a rebalanced mix of volume-ground munitions and targeted precision rounds, which sustains breadth in the Europe ammunition market.

Technology and compliance remain focal points. Suppliers are prioritizing insensitive munitions standards and extended-range designs that utilize base bleed and rocket assist to achieve ranges exceeding 50 kilometers. Environmental regulation under REACH is driving a shift to lead-free small-caliber and alternative propellants, which necessitate new processes and more extended testing periods. White-space opportunities exist in guidance electronics and green energetics, where European vendors are scaling but still trail global leaders in some subcomponents. Additive manufacturing shows promise for select components; however, certification timelines are lengthy in this safety-critical category. Overall, policy-backed investment and framework contracting provide the backbone for capacity growth and product evolution across the Europe ammunition market.

Europe Ammunition Industry Leaders

BAE Systems plc

Rheinmetall AG

General Dynamics Corporation

Leonardo S.p.A.

KNDS N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Rheinmetall AG announced the completion of its new 155mm artillery shell production facility in Germany, with an annual capacity of 200,000 rounds. The facility is supported by a EUR 300 million (USD 349.57 million) German government co-investment and backed by a five-year framework contract from the Bundeswehr. The plant utilizes advanced robotic shell-filling systems, which enhance worker safety and improve throughput consistency.

- August 2025: KNDS N.V. secured a multi-year contract worth approximately EUR 1.20 billion (USD 1.40 billion) from the French Ministry of Armed Forces to supply 155mm artillery ammunition through 2030, with provisions for accelerated delivery if operational requirements increase. The agreement includes co-funding for the expansion of propellant capacity at Eurenco's facilities, a subsidiary of KNDS, in Sorgues.

- July 2025: Poland's state-owned MESKO signed a joint venture agreement with South Korea's Hanwha Defense to establish 155mm artillery shell production in Skarżysko-Kamienna, aiming to produce 100,000 rounds annually by 2027. The partnership combines Korean manufacturing technology with Polish labor and existing explosives infrastructure.

- June 2025: Nammo AS completed a EUR 180 million (USD 209.74 million) expansion of its nitrocellulose propellant production line in Raufoss, Norway, which increased European propellant capacity by approximately 25% and reduced reliance on non-NATO imports. The project received co-funding from Norway's MoD and NATO's Defence Production Action Plan.

Europe Ammunition Market Report Scope

Ammunition is a projectile shot, shattered, dropped, or exploded by any weapon or weapon system. Ammunition is used as a disposable weapon as well as a component of other weapons to have an impact on a target. Ammunition is used to direct a force to a certain target. To function, all mechanical weapons require some form of ammo. When input on functionality is obtained from the battlefield, enhancements, upgrades, and replacements are always being designed.

The Europe ammunition market is segmented by caliber, product, guidance, end-user, platform, and country. By caliber, the market is segmented into small-caliber, medium-caliber, large-caliber, and others. By product, the market is classified into bullets and cartridges, artillery shells and mortars, and aerial bombs and grenades. By guidance, the market is divided into guided and unguided. By end-user, the market is segmented into military, law enforcement, and civil and sports shooting. By platform, the market is segmented into land, naval, and airborne. The report also covers the market sizes and forecasts for the Europe ammunition market in major countries in the region. For each segment, the market size is provided in terms of value (USD).

By Caliber

| Small Caliber |

| Medium Caliber |

| Large Caliber |

| Others |

By Product

| Bullets and Cartridges |

| Artillery Shells and Mortars |

| Aerial Bombs and Grenades |

By Guidance

| Guided |

| Unguided |

By End-User

| Military |

| Law Enforcement |

| Civil and Sports Shooting |

By Platform

| Land |

| Naval |

| Airborne |

By Geography

| United Kingdom |

| France |

| Germany |

| Russia |

| Poland |

| Italy |

| Spain |

| Rest of Europe |

| By Caliber | Small Caliber |

| Medium Caliber | |

| Large Caliber | |

| Others | |

| By Product | Bullets and Cartridges |

| Artillery Shells and Mortars | |

| Aerial Bombs and Grenades | |

| By Guidance | Guided |

| Unguided | |

| By End-User | Military |

| Law Enforcement | |

| Civil and Sports Shooting | |

| By Platform | Land |

| Naval | |

| Airborne | |

| By Geography | United Kingdom |

| France | |

| Germany | |

| Russia | |

| Poland | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe ammunition market size in 2026 and its growth outlook to 2031?

The Europe ammunition market size is USD 4.74 billion in 2026, with a forecast value of USD 7.06 billion by 2031 at an 8.27% CAGR.

Which segments lead the Europe ammunition market by share and growth?

Bullets and cartridges lead by share at 63.68% in 2025, while artillery shells and mortars post the fastest growth at a 10.67% CAGR through 2031.

How is the guidance mix evolving in the Europe ammunition market?

Unguided munitions remain 90.15% of volumes, and guided rounds are growing at a 10.12% CAGR for standoff and precision roles.

Which end-user drives demand in the Europe ammunition market through 2031?

The military segment dominates with a 78.93% share in 2025 and an 11.21% CAGR to 2031, underpinned by multi-year contracts and stockpile mandates.

What geographic trends shape the Europe ammunition market’s demand?

Rest of Europe holds 31.96% share, and Russia grows fastest at 11.3% CAGR, while major EU economies scale 155mm capacity and co-production links.

What are the main constraints on the Europe ammunition market’s scaling plans?

Limited TNT, RDX, and nitrocellulose capacity and fragmented national procurement standards are the main near-term constraints on output and cost.

Page last updated on: