Aerospace & Defense

8th MayFeasibility Analysis for FBO Services in East Africa

3 Min Read

The Ammunition Market Report is Segmented by Caliber (Small Caliber, Medium Caliber, Large Caliber, and Others), Product (Bullets and Cartridges, Artillery Shells and Mortars, and More), Guidance (Guided and Unguided), End-User (Military, Law Enforcement, and More), Platform (Land, Naval, and Airborne), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

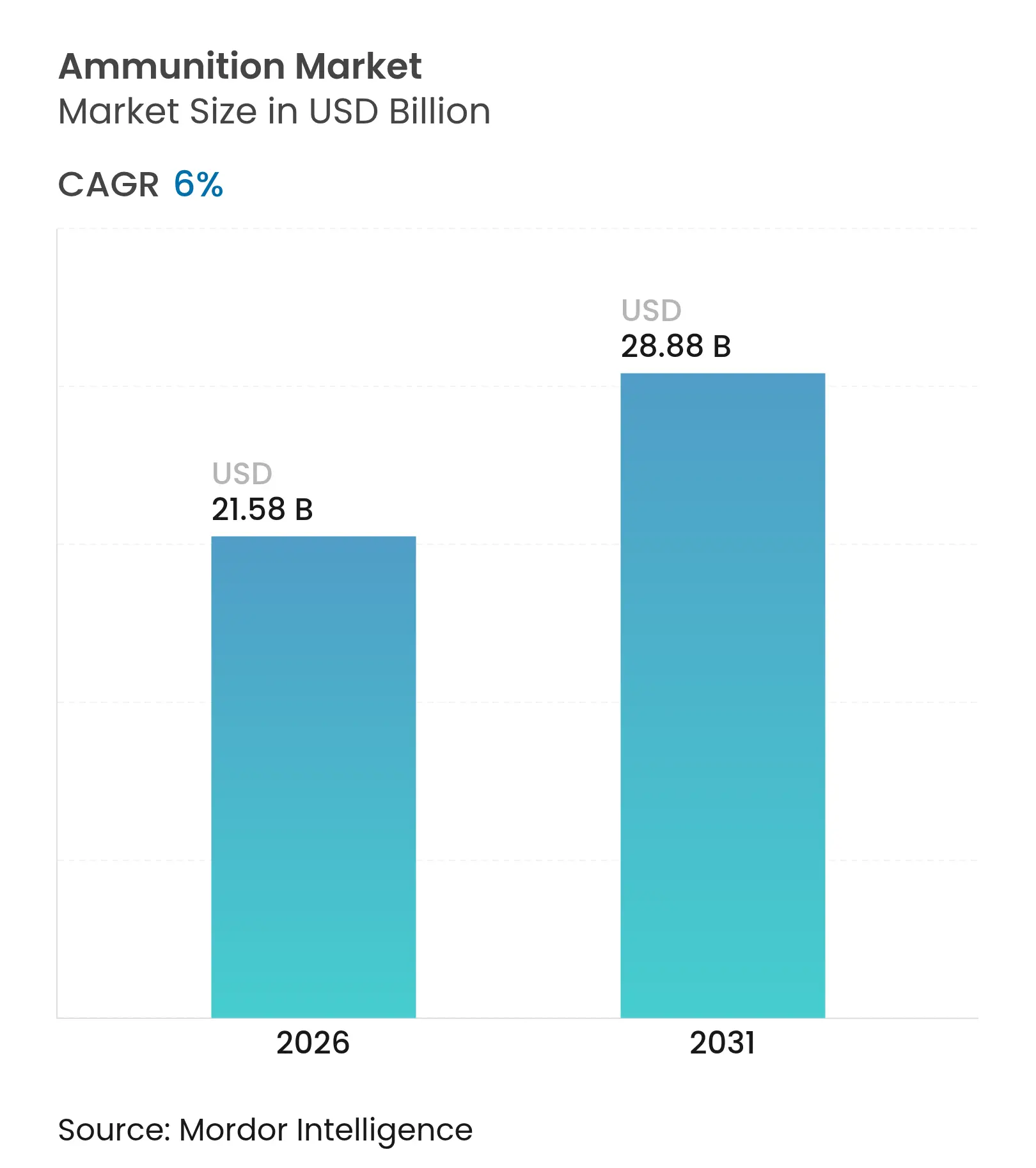

| Market Size (2026) | USD 21.58 Billion |

| Market Size (2031) | USD 28.88 Billion |

| Growth Rate (2026 - 2031) | 6.00 % CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The ammunition market size is expected to grow from USD 20.37 billion in 2025 to USD 21.58 billion in 2026 and is forecasted to reach USD 28.87 billion by 2031 at a 6.00% CAGR over 2026-2031. Solid multi-year procurement in the US, an EU-backed capacity-building program for 155mm shells, and widespread modernization programs across allied nations underpin this expansion. In 2026, North American buyers emphasize capacity additions for artillery, air-defense, and precision rounds, while European ministries of defense accelerate greenfield artillery plants to achieve industrial sovereignty. Premium pricing for programmable and monometal cartridges offsets higher compliance costs tied to lead-free mandates. Meanwhile, steady civilian participation and normalized retail inventories stabilize small-caliber volumes in the US.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Intensified NATO stockpile replenishment Intensified NATO stockpile replenishment | +1.8% | Europe core, spillover to North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Europe core, spillover to North America | Impact Timeline:Medium term (2-4 years) |

Increased defense spending and modernization driving market growth Increased defense spending and modernization driving market growth | +1.5% | Global, led by NATO and Indo-Pacific allies | Long term (≥ 4 years) | |||

Increased use of programmable air-burst and proximity-fuzed rounds in urban operations Increased use of programmable air-burst and proximity-fuzed rounds in urban operations | +0.9% | North America and EU, expanding to APAC | Medium term (2-4 years) | |||

Rising civilian concealed-carry adoption driving ammunition demand Rising civilian concealed-carry adoption driving ammunition demand | +0.6% | National (United States core, growth in select EU states) | Short term (≤ 2 years) | |||

Growing demand for modern artillery propellant systems Growing demand for modern artillery propellant systems | +1.0% | Global, urgent in Europe | Medium term (2-4 years) | |||

Shift to lead-free ammunition driving market growth Shift to lead-free ammunition driving market growth | +0.4% | North America and EU regulatory zones, early adoption in APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Intensified NATO Stockpile Replenishment Post-Ukraine War

NATO-aligned countries expand artillery and medium-caliber lines in 2026 as industry and government programs convert funding into stable production, evidenced by new European facilities that scale 155mm shells and 40mm telescoped rounds. Germany’s Unterlüß site opened in September 2025 and is scheduled to scale to artillery shells by 2027, with intermediate volume milestones in 2026, according to the company’s statements.[1]Rheinmetall AG, “A New Era at Rheinmetall: Ammunition Factory Opening in Unterlüß,” Rheinmetall, rheinmetall.com Belgium’s automated large-caliber machining and banding line is dedicated to 155mm shells, and nearly six months of 2026 output is allocated to Belgian Defence, signaling sovereign prioritization consistent with allied stockpile policies. Procurement data in the United States shows ammunition and munitions rebuild lines funded in the FY2026 account, sustaining replenishment cycles that backfill inventories and support training stocks. The Department of Defense budget materials also identify ammunition procurement and key supply-chain initiatives across the 2026 portfolio, which reinforce volume orders for shells and energetics to ensure readiness. Nordic governments have deepened regional coordination through a multi-country framework on deliveries, services, and surge capacity with a named supplier, aligning national reserve sharing with peak demand in crisis settings.

Increased Defense Spending and Modernization Driving Market Growth

The US FY2026 defense budget totals reflect continued emphasis on munitions arsenals, industrial-base expansion, and repeatable production of selected weapon systems that anchor upstream investment decisions. Congressional materials covering the FY2026 cycle highlight funding for Patriot, THAAD, Tomahawk, JASSM, LRASM, SM-3, and AMRAAM, which provides stable demand visibility for components, energetics, and assembly lines. Platform-centric contracts underscore how vehicle and artillery acquisitions pull associated ammunition demand, as seen in awards to produce additional M109A7 Paladin howitzers and M992A3 ammunition carriers for US Army formations.[2]BAE Systems, “BAE Systems Secures Programmable Ammunition Orders from Sweden and Finland,” BAE Systems, baesystems.com At the same time, US contracting records show production-scale awards for proximity-fuzed 30mm rounds tailored for counter-UAS missions, validating procurement of medium-caliber ammunition with specialized effects and guidance logic. Allied procurement in the Middle East adds further demand for bomb bodies and penetrators, with formal notifications confirming large-scale munitions packages that feed air-delivered stockpiles. Industrial-expansion announcements in the United States also target domestic production of nitrocellulose and triple-base propellants, which respond to prior bottlenecks in energetic materials and build long-term capacity for modular charge systems.

Rising Civilian Concealed-Carry Adoption Driving Ammunition Demand

The US industry data indicate a broad base of consumer participation that sustains demand for small-caliber training and concealed carry. In 2024, the sector reported millions of new owners and notable employment gains, providing a downstream sales channel for cartridges and components through 2025 and into 2026. New product introductions in 2026 continue to address performance niches, including long-range hunting and controlled-expansion designs, which reflect stable innovation pipelines at consumer-focused brands. Federal incentives for lead-free use on selected public lands also nudge a portion of demand toward monometal or non-toxic alternatives, which subtly shifts mix and pricing at the retail level. Stabilization in retail inventories reduces extreme spot shortages compared to prior surges, but law enforcement and federal agency training orders maintain a steady baseline for 9mm and other duty calibers. This civilian and public safety foundation complements military volume, which together underpins a balanced demand profile in the ammunition market.

Growing Demand for Modern Artillery Propellant Systems

Industrial set-ups in 2026 increasingly focus on energy material sovereignty, domestic nitrocellulose capacity, and modular charge production to enable sustained 155mm throughput. A US government-backed lease enables new domestic production of nitrocellulose and triple-base propellants that supply modular charge systems, which reduces exposure to imported feedstocks and transit risks. Company statements in Europe emphasize both shell bodies and powder lines as dual bottlenecks that must grow in tandem to meet allied replenishment objectives, prompting combined investments in forging, machining, and propellant chemistries. Government contracting data in the United States confirms active funding for artillery munitions across the FY2026 cycle, providing demand continuity for suppliers of charges, primers, and packaging operations. Allied Europe’s 155mm initiatives broaden the supplier base for propellant and charge components through new public-private partnerships, which add redundancy to cross-border supply during periods of elevated demand. These investments lift the resilience of artillery value chains in the ammunition market and reinforce expected volume growth through the end of the decade.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

DoD and MoD budget re-prioritization toward unmanned systems DoD and MoD budget re-prioritization toward unmanned systems | -0.7% | North America, Europe, APAC | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:North America, Europe, APAC | Impact Timeline:Medium term (2-4 years) |

Soaring nitrocellulose prices due to cotton supply shocks Soaring nitrocellulose prices due to cotton supply shocks | -0.5% | Global | Short term (≤ 2 years) | |||

Heightened ESG scrutiny on heavy-metal discharge at training grounds Heightened ESG scrutiny on heavy-metal discharge at training grounds | -0.3% | North America and EU, emerging in APAC | Long term (≥ 4 years) | |||

Civil export bans impacting US OEM sales to South America Civil export bans impacting US OEM sales to South America | -0.2% | Americas focus, indirect global effects | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

DoD and MoD Budget Re-Prioritization Toward Unmanned Systems

The US budget materials in 2026 prioritize a diverse set of capabilities, including attritable and low-cost weapons, which compete for funding with legacy ammunition inventories. Public reporting on reconciliation allocations highlights dedicated lines for one-way attack drones and affordable weapon efforts that draw on similar industrial skill sets and supply chains as traditional cartridges and shells. Allied governments are also standing up guided-rocket and missile assembly outside the United States, which diversifies suppliers while allocating resources toward precision weapons that may reduce short-term artillery buys. Across naval and air portfolios, 2026 funding covers multiple precision families that serve maritime strike and air defense missions, which pulls budget into high-technology lines at the expense of some unguided stockpiles. Industry responses include medium-caliber rounds designed for counter-UAS and multipurpose roles, keeping legacy guns relevant in a drone-saturated environment. The net effect restrains some conventional ammunition orders in the near term, although core artillery and small-caliber volumes remain essential for sustained operations and training in the ammunition market.

Soaring Nitrocellulose Prices Due to Cotton Supply Shocks

Energetic material bottlenecks and constraints on cotton-derived nitrocellulose have driven price and availability pressures since late 2024, which, in turn, have lifted the cost base for artillery charges and select propellant systems. European OEM actions to secure nitrocellulose sources and build strategic reserves aim to mitigate exposure to external supply disruptions, with public statements indicating dedicated investments into military-grade cellulose capacity. In the United States, new leases and facility plans are focused on domestic nitrocellulose and triple-base output for 155mm modular charges, which addresses a critical resilience gap. Public reporting also highlights increases in explosive fill prices for government buyers over the past several years, a signal that broader energetic markets have tightened. These dynamics pressure OEM margins and complicate end-user budget planning, even as 2026 funding supports rebuild initiatives.[3]U.S. Department of the Treasury, “Procurement of Ammunition, Army | Spending Profile,” USAspending, usaspending.gov The restraint moderates growth in the ammunition market until new Western energy capacity reaches a stable output level.

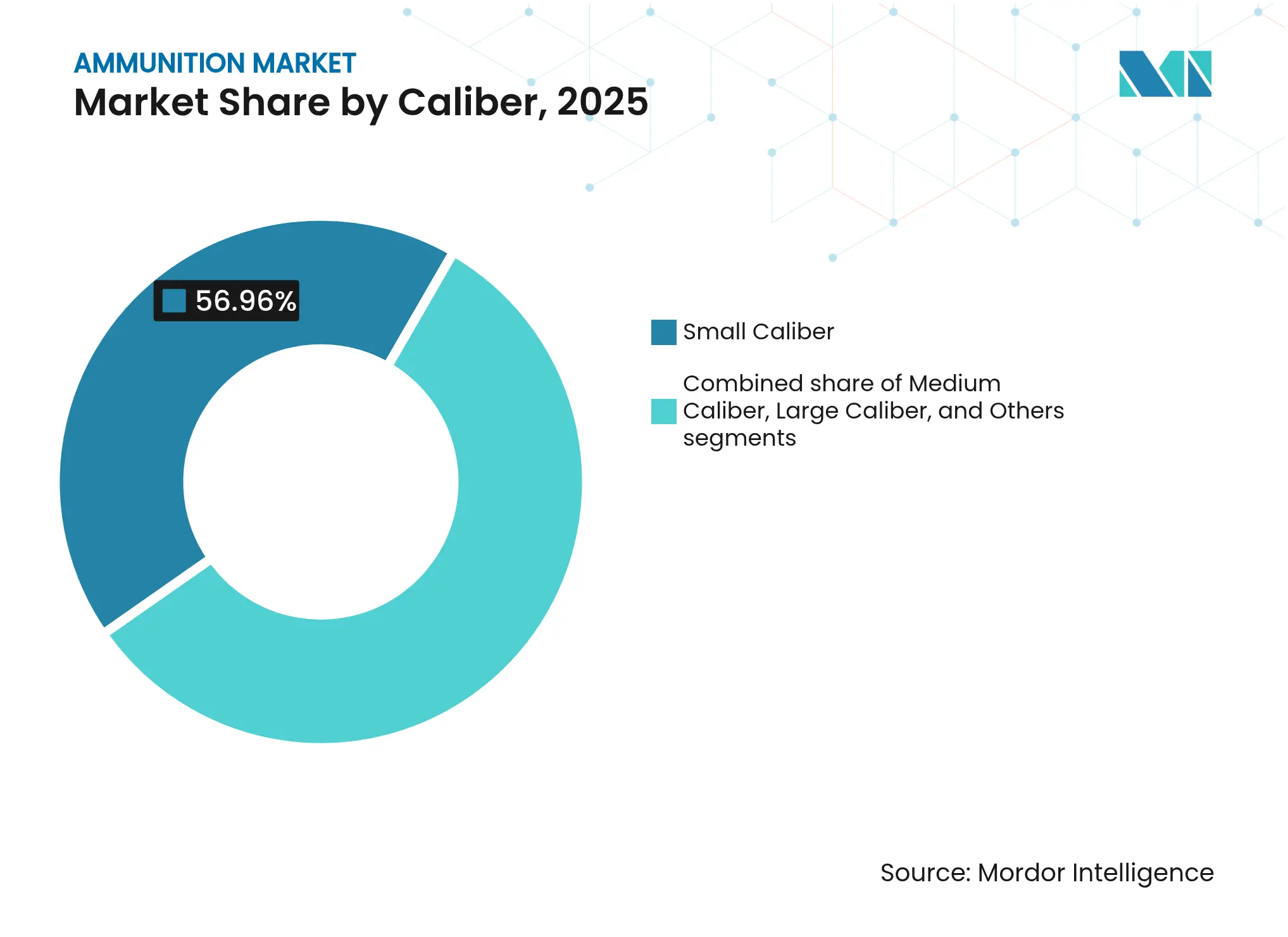

By Caliber: Small Caliber Commands Volume, Yet All Sizes Surge

Small-caliber ammunition accounted for 43.04% of the ammunition market in 2025 and is set to grow at a 6.25% CAGR through 2031 as civil, law enforcement, and military channels sustain parallel demand. New US consumers added in 2024 supported training and personal-defense purchases in 2025 and 2026, providing a broad retail base for small-caliber cartridges. On the defense side, polymer-cased .50-caliber programs reduced weight while improving heat resistance, supporting mobility and logistics benefits on expeditionary missions. Medium-caliber rounds progressed through program awards for F-35 users in Europe, including APEX combat and matched training variants, which confirms a robust pipeline in the 25mm class. European demand for 40mm telescoped ammunition increased with naval and land system deployments, which amplified production plans heading into 2026 and beyond. Large-caliber artillery remains a central priority, as US and European programs scale 155mm output and align propellant capacity to meet scheduled deliveries. These multi-caliber dynamics keep the ammunition market anchored in reliable volume segments while adding selective growth from premium medium-caliber rounds that address counter-UAS and base-defense tasks.

Small-caliber leadership is reinforced by the interoperability benefits of NATO standards around 5.56mm and 7.62mm cartridges, which support cross-border pooling and contract flexibility in allied training pipelines. Medium-caliber adoption benefits from integrated sensors and fire-control logic on land and maritime platforms, which improves lethality against drones and low-cost aerial threats. For large-caliber artillery, artillery body machining and propellant chemistry have both received investment attention to strengthen consistent throughput at Western sites in 2026. This mix of retail, training, and operational needs sustains balanced growth across calibers in the ammunition market, even as budgets also fund guided and unmanned systems. Within this segment, the ammunition industry continues to pursue lighter case materials and improved energetics to optimize logistics and reliability at scale.

Note: Segment shares of all individual segments available upon report purchase

By Product: Bullets and Cartridges Dominate, Yet Artillery Shells See Steepest Growth Acceleration

Bullets and cartridges held 60.81% of the ammunition market size in 2025 and are projected to advance at a 6.13% CAGR, supported by premium programmable options and steady small-caliber consumption. Northern European contracts for 40mm and 57mm programmable munitions demonstrate sustained demand for airburst and proximity-fuzed effects that counter drones, loitering munitions, and helicopters. Artillery shells and mortars drive replenishment workflows in Europe and the United States through FY2026, and contracting data confirms ongoing investment in 155mm projectiles and modular charges. The US Navy’s FY2026 budget supports artillery munitions procurement, which aligns with joint service needs to refresh expiring inventories and equip units for training cycles. Aerial bombs and grenades continue to benefit from fuze and guidance add-ons that enhance accuracy, allowing forces to extend the relevance of legacy stockpiles through modular kits. Foreign military sales in 2025 confirmed significant orders for bomb bodies and penetrators, a trend that supports steady demand for air-delivered munitions alongside artillery investment.

Digital interfaces between fuzes, propellants, and fire-control computers are now a more prominent part of product strategies, reflected in command-programmable cartridges designed for multi-mode effects. Western programs also consider submunition replacements where policy restricts cluster use, and public market surveys show interest in advanced 155mm submunitions at scale. OEMs and arsenals continue to expand 155mm load, assemble, and pack operations in the United States to achieve higher monthly throughput that aligns with training and operational needs. Overall, the ammunition market is shaped by replenishment-led demand in shells and mortars alongside growing premium niches in programmable cartridges, which together lift average selling prices without sacrificing volume. Within this segment, the ammunition industry continues to invest in fuze technology, insensitive munitions, and interface standards to create reliable, configurable effects.

By Guidance: Unguided Munitions Retain Share, Yet Precision Demand Reshapes Margins

Non-guided ammunition accounted for 92.12% of the ammunition market in 2025 and is expected to grow at a 5.99% CAGR, reflecting enduring demand for volume fire and training rounds where precision yields limited marginal gains. US budget lines in 2026 include artillery munitions and guidance kits that augment legacy shells rather than replace them outright, which confirms a blended path that preserves unguided volume. Guidance-kit programs like PGK improve accuracy for conventional shells at a lower cost than full-precision rounds, reinforcing a complementary rather than a substitutive relationship between guided and unguided inventories. Operational lessons have also emphasized electronic warfare resilience, which keeps demand for unguided rounds stable as forces hedge against GPS degradation in contested environments. These dynamics position unguided ammunition as the backbone of suppressive and area-target fires through 2031, while guided munitions fill high-value or time-sensitive strike roles.

Guided munitions maintain premium pricing and selective growth, with US appropriations supporting procurement for long-range anti-ship and air-launched systems in 2026. Experience with proximity-fuzed and airburst effects at medium caliber indicates that affordable programming can expand lethality without incurring full PGM costs, encouraging a nuanced mix across ground and maritime missions. Training requirements and safety rules reinforce steady purchases of unguided small-caliber loads across military and law enforcement agencies, which support the foundational volume in this segment of the ammunition market. Over the forecast period, suppliers that can flex between guided and unguided lines are best positioned to capture sustained orders and mitigate budget swings across programs.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

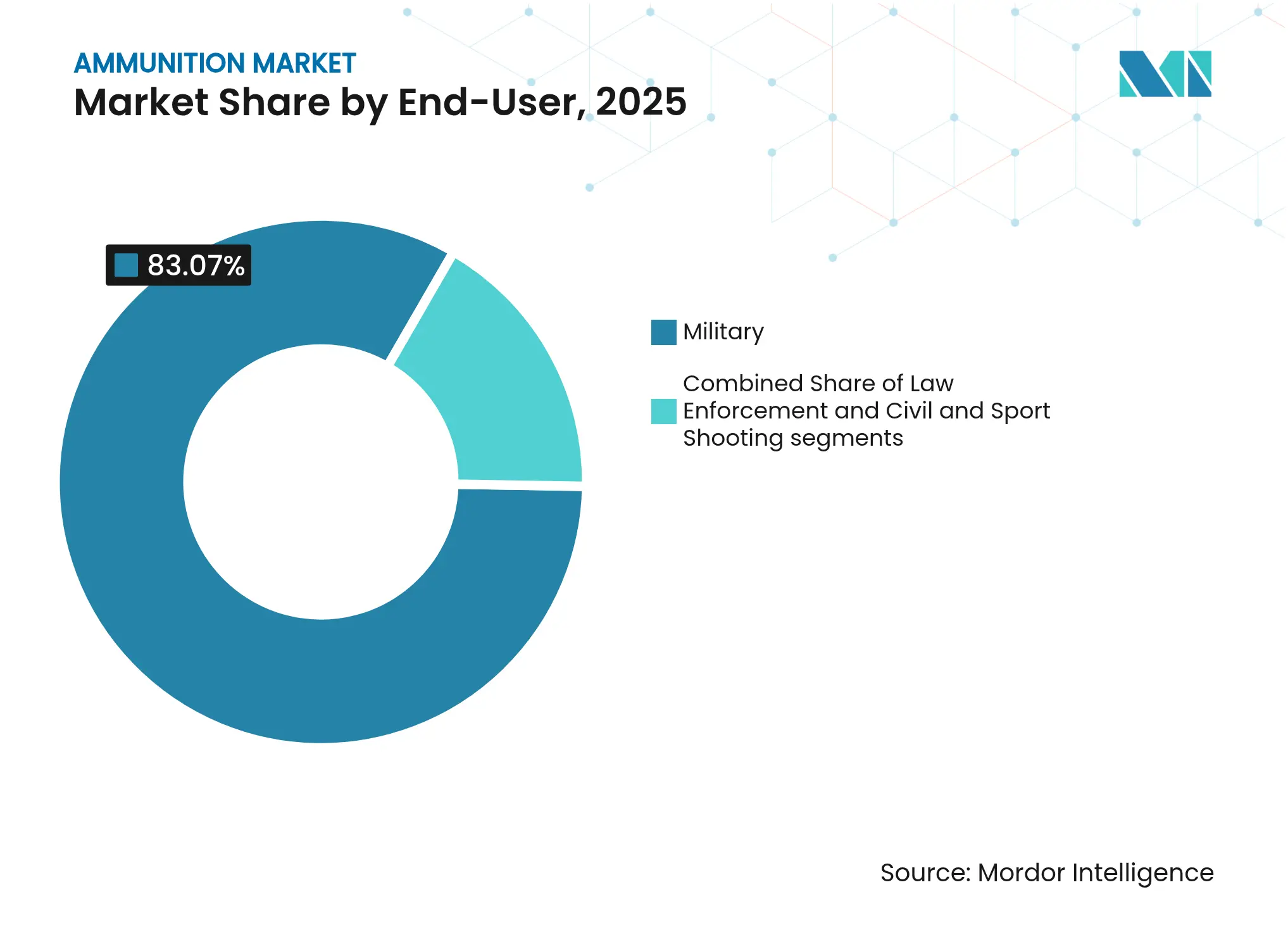

By End-User: Military Dominance Persists, Yet Civilian Segment Offers Margin Richness

Military users accounted for 83.07% of 2025 volumes and are projected to expand at a 6.22% CAGR through 2031, a profile that reflects multi-year budget authority and stockpile-rebuild priorities. US materials identify ammunition rebuild lines and supply-chain initiatives in FY2026, which reinforce long-run production signals to OEMs. Platform procurement, such as M109A7 Paladin howitzers and M992A3 ammunition carriers, strengthens the linkage between vehicle fleets and the associated artillery, mortars, and logistics munitions. Law enforcement sustains steady training demand with recurring orders for marking and duty loads, which buffer the channel against retail volatility. Civil and sports shooting has normalized from peak surges, but the base of new US participants added in 2024 continues to support retail volumes and conservation-linked excise flows.

Military demand is less sensitive to election cycles and consumer sentiment, which helps stabilize the ammunition market through 2026. In parallel, foreign military sales and bilateral programs confirm ongoing munitions deliveries, keeping air and artillery stockpiles at operational levels. The civilian channel remains shaped by localized carry laws, hunting participation, and retailer promotion strategies that seek to smooth demand through the year. Suppliers continue to balance runs across military and civil SKUs while managing common bottlenecks around powder and primers, which remain sensitive to defense-priority allocations. Within this end-user mix, the ammunition industry aligns production planning with defense calendars while keeping capacity for civilian and law enforcement commitments.

Note: Segment shares of all individual segments available upon report purchase

By Platform: Land Systems Command Share, Yet Naval and Airborne Segments Upgrade Faster

Land platforms held 68.05% in 2025 and are projected to grow at a 6.16% CAGR, a trajectory tied to artillery-centric doctrine and active 155mm programs across allied nations. Program awards in 2025 and 2026 for Paladin howitzers and ammunition carriers highlight sustained investment in tracked artillery systems and their resupply vehicles. Naval use cases include the procurement of torpedo components and 40mm telescoped ammunition for surface-vessel turrets, which extend programmable effects into maritime air-defense tasks. Air platforms continue to consume a high-value mix of cannon ammunition and guided weapons, with European F-35 users ordering 25mm APEX combat rounds and matched training munitions.

In 2026, land forces consume ammunition at rates consistent with high-intensity training and readiness cycles, and industrial planners allocate shell and charge capacity to match. Naval and shore-based air-defense roles reinforce the need for programmable 40mm and 57mm rounds, which have driven multi-year orders by Northern European customers. On the air side, gun ammunition for aircraft cannons and selected guidance kits for legacy inventories maintain relevance in permissive environments, even as advanced missiles dominate procurement headlines. This platform mix underscores sustained land-segment primacy in the ammunition market, while naval and air platforms retain specialty needs that command higher unit values. Across platforms, the ammunition industry invests in flexible manufacturing and inspection automation to support cross-segment throughput.

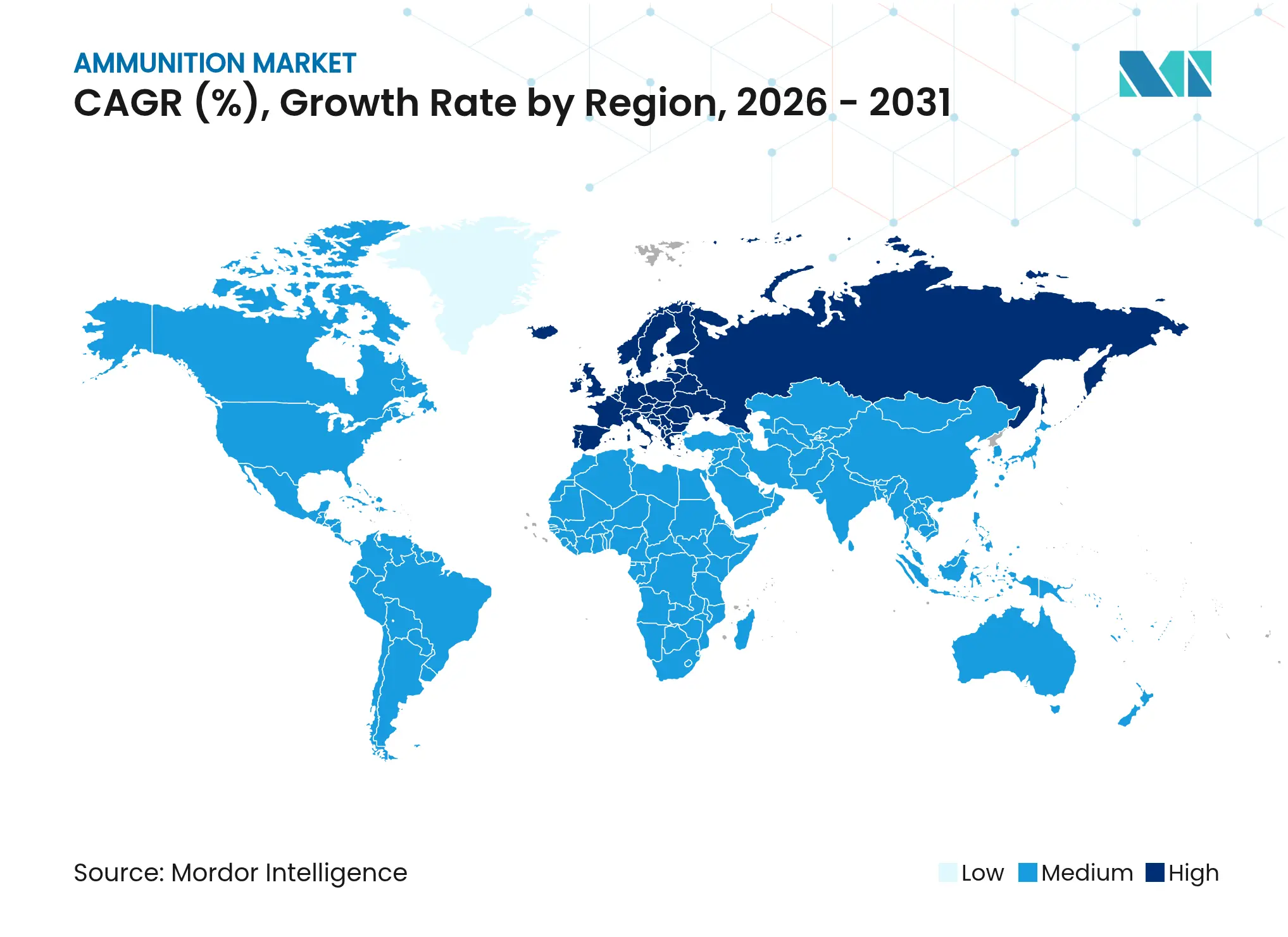

North America’s share of leadership with 47.31% in 2025 reflects the scale and continuity of US procurement, with FY2026 accounts funding artillery munitions, component lines, and rebuild programs that keep factories engaged throughout the year. Procurement records show repeat awards across calibers and product categories, indicating a balanced approach that sustains shells, cartridges, and specialty rounds for joint service use. The combination of vehicle platform orders, ammunition carriers, and ammunition rebuilds further raises production utilization at major OEM sites and at government-owned facilities that run energetics and loading operations. New energetic capacity planned under federal leases aims to reduce reliance on imported nitrocellulose and triple-base propellants, thereby improving resilience against supply disruptions and supporting long-term charge production for 155mm systems. In this context, the ammunition market benefits from predictable procurement, which enables multi-year capital planning and incremental workforce expansions.

Europe is the fastest-growing region, with a 9.48% CAGR, and 2026 marks a period of meaningful capacity ramp with fresh-shell machining units, new banding lines, and factory expansions designed around 155mm volumes. Announced volume milestones for 2026 and targeted run rates for 2027 reinforce a committed industrial policy focused on ammunition sovereignty, propelled by public-private financing and framework contracts. Complementary programs for 40mm telescoped ammunition highlight the role of programmable effects in airbase defense and naval applications, thereby increasing specialized demand beyond artillery. Regional defense cooperation agreements further standardize cross-border logistics and reserve sharing, speeding deliveries and helping meet national readiness targets in 2026. This trajectory expands Europe’s contribution to the global ammunition market and diversifies supply sources across allied nations.

Asia-Pacific partners pursue sovereign production and joint industrial ventures for rocket artillery and modular charges, which adds depth to allied supply chains while reflecting local doctrine and training needs. In the Middle East, formal notifications in 2025 confirm large munitions packages for air-delivered ordnance, which support steady supplier utilization and replenishment cycles through 2026. Africa and South America represent smaller demand pools, where export controls and local budgets shape the cadence of deliveries and may channel purchases toward training munitions over premium segments. Overall, North America retains the largest 2025 position, Europe leads growth through 2031, and Asia-Pacific and the Middle East add diversified demand. This pattern underpins a resilient global ammunition market in 2026.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

The ammunition market displays moderate concentration around a group of vertically integrated OEMs with capabilities across propellants, metal forming, and final assembly. Press statements show a clear push by leading European suppliers to secure supplies of energetic materials, including nitrocellulose, to mitigate exposure to external shocks while boosting regional artillery output. Factory openings in Germany and new machining lines in Belgium indicate concrete capacity gains for 155mm shells with defined production milestones for 2026 and 2027. In the United States, budget lines for FY2026 reinforce procurement for artillery, medium-caliber, and specialty rounds alongside selected guidance kits, which sustains multi-year visibility for tier-1 and tier-2 suppliers.

Strategic moves in 2026 emphasize industrial sovereignty and dual-use investments. A US government-approved plan for a new energetics facility at a government arsenal will produce nitrocellulose and triple-base propellants for 155mm modular charges, thereby reducing reliance on foreign feedstocks and bolstering long-term artillery supply. Northern European countries placed multi-year orders for programmable 40mm and 57mm munitions for counter-UAS and point-defense missions, nudging the mix toward higher-margin cartridges in this region. OEMs in Europe also expanded large-caliber machining and banding units with automated lines, allocating early 2026 capacity to sovereign orders, confirming a sequenced ramp for 155mm shells. This competitive posture favors suppliers with integrated energetics, deep forging, and automation that can flex between military and civil SKUs in a steady 2026 demand environment.

Program awards and public notifications underline a healthy pipeline across artillery, proximity-fuzed medium-caliber rounds, and air-delivered munitions. US procurement records confirm production awards for 30mm proximity rounds for counter-UAS roles with compatible chain guns, keeping medium-caliber lines active. Formal notifications to a Middle Eastern partner include significant bomb-body and penetrator quantities, which support aerospace-focused ordnance lines for multi-year delivery. Altogether, the ammunition market in 2026 rewards suppliers that can secure feedstocks, automate quality control, and deliver on schedule across artillery, programmable cartridges, and selected air-delivered product lines.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Ammunition Baseline Earns Trust

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 23.67 B (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 29.99 B (2025) | Global Consultancy A | Adds recreational ammo and uses list-price ASPs | ||

USD 35.83 B (2024) | Trade Journal B | Earlier base year and inclusion of rockets/missiles inflates value | ||

USD 75.27 B (2024) | Industry Association C | Bundles explosives and relies on arms-sales ratios without bottom-up checks |

Feasibility Analysis for FBO Services in East Africa

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.