Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

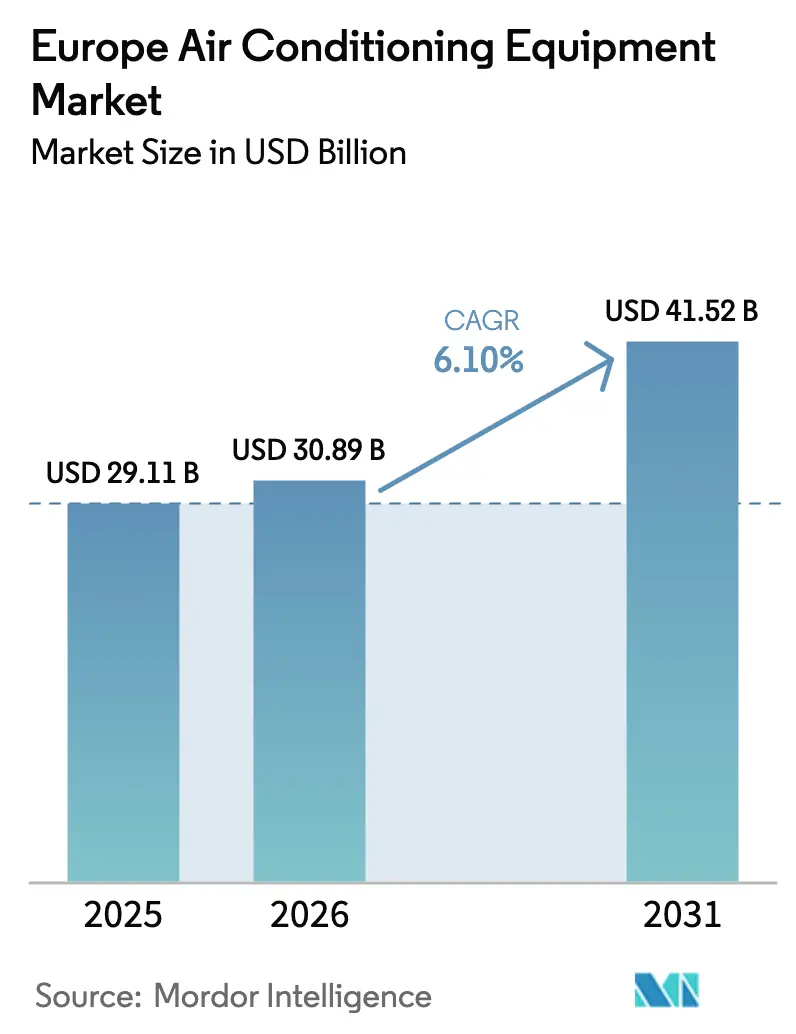

| Base Year Market Size (2025) | USD 29.11 Billion |

| Market Size (2026) | USD 30.89 Billion |

| Market Size (2031) | USD 41.52 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

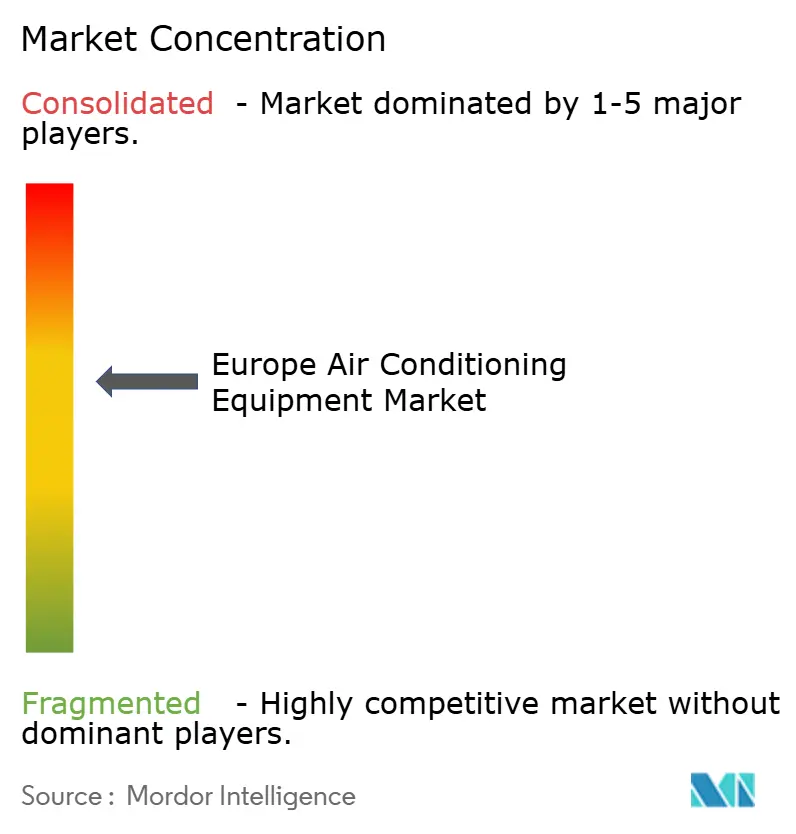

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Air Conditioning Equipment Market Analysis by Mordor Intelligence

Europe Air Conditioning Equipment Market size in 2026 is estimated at USD 30.89 billion, growing from 2025 value of USD 29.11 billion with 2031 projections showing USD 41.52 billion, growing at 6.1% CAGR over 2026-2031.

Rapid policy alignment with the EU Green Deal, stricter F-Gas quotas, and the REPowerEU goal of 60 million installed heat pumps by 2030 are creating an environment in which the Europe air conditioning equipment market consistently rewards energy-efficient, low-GWP technologies. Manufacturers that scaled natural-refrigerant product lines and secured inverter compressor capacity during 2024 now enjoy shorter lead-times, a competitive edge in public tenders, and higher average selling prices. The Europe air conditioning equipment market also benefits from a data-center construction wave in FLAP-D hubs, municipal heat-island programs in Southern capitals, and the growing popularity of HVAC-as-a-Service contracts among corporate facility managers. Direct-to-key-account sales are accelerating as large commercial buyers look to lock in specification packages that meet upcoming SEER thresholds without mid-project redesigns.

Key Report Takeaways

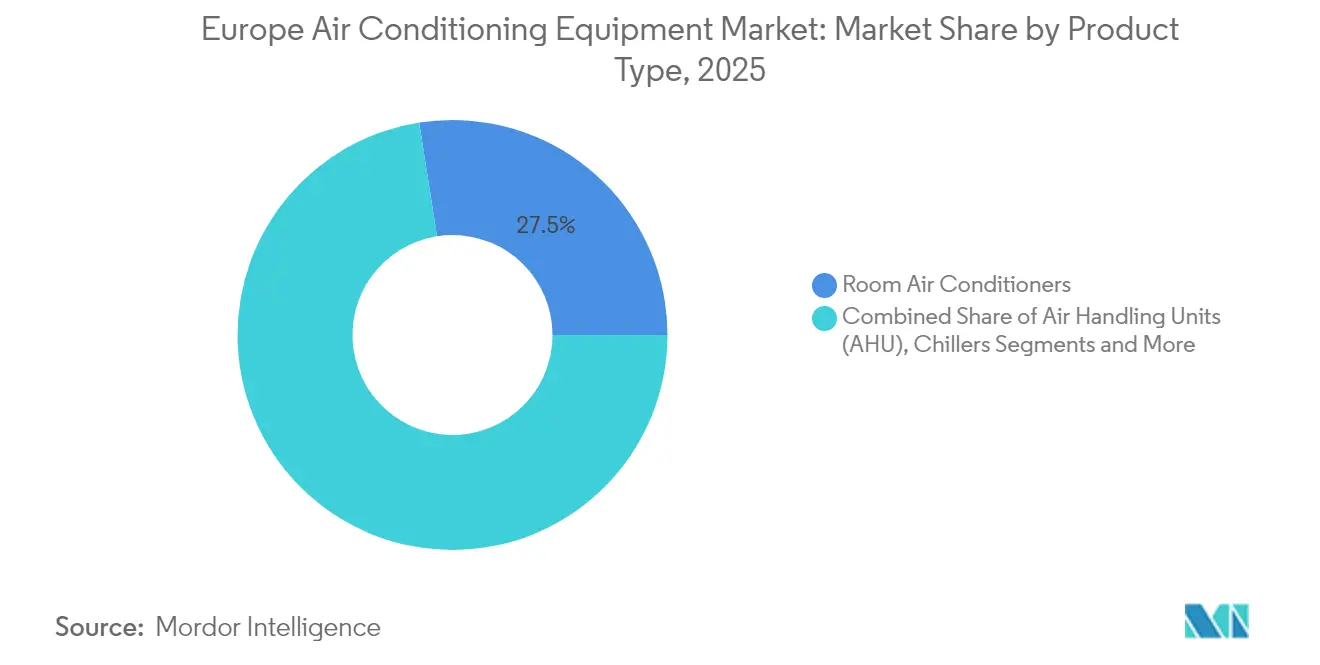

- By product type, Single-Split Systems led with 27.48% Europe air conditioning equipment market share in 2025, while Variable Refrigerant Flow (VRF) systems are expanding at a 9.15% CAGR through 2031.

- By technology, Non-Inverter systems controlled 67.95% of the Europe air conditioning equipment market size in 2025; Inverter technology records the highest CAGR at 8.85% through 2031.

- By geography, Germany commanded 17.12% share of the Europe air conditioning equipment market in 2025, whereas Spain registers the fastest growth at 8.15% CAGR to 2031.

- By end user, the residential segment accounted for 42.05% of the Europe air conditioning equipment market size in 2025 and data centers are growing at 10.65% CAGR.

- By distribution channel, indirect distribution captured 70.65% Europe air conditioning equipment market share in 2025; direct manufacturer-to-key-account sales are growing at 9.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Air Conditioning Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated Heat-Pump Uptake Driven by EU REPower Targets | +1.8% | EU-wide, strongest in Germany, Netherlands, Denmark | Medium term (2-4 years) |

| Rising Demand for Low-GWP Refrigerants Post F-Gas Revision | +1.2% | EU-wide, particularly Northern Europe | Short term (≤ 2 years) |

| Urban Heat-Island Mitigation Projects in Southern Europe | +0.9% | Spain, Italy, Southern France, Greece | Long term (≥ 4 years) |

| Data-Centre Expansion in FLAP-D Cities Boosting Precision Cooling | +1.1% | Frankfurt, London, Amsterdam, Paris, Dublin | Medium term (2-4 years) |

| Energy-Efficiency Renovation Wave Under EU Green Deal | +0.8% | EU-wide, strongest in Central and Eastern Europe | Long term (≥ 4 years) |

| HVAC-as-a-Service Contracts Gaining Traction Among Facility Managers | +0.4% | Western Europe, particularly UK, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Heat-Pump Uptake Driven by EU REPower Targets

Member-state mandates are converging on heat pumps as the primary replacement for fossil-fuel boilers, pushing annual installations toward 6 million units from 2025. Germany already approved heat pumps in 76% of new residential buildings in 2024. France is ramping domestic capacity to 1 million units per year by 2030, supported by reduced VAT, grant finance, and fast-track permitting. The European Commission’s Heat Pump Accelerator Platform is synchronizing incentive structures, giving manufacturers unprecedented demand visibility that anchors multi-year capex decisions. As the Europe air conditioning equipment market pivots toward hybrid heating-cooling equipment, suppliers with vertically integrated compressor and controls production gain the most leverage.[1]Clean Energy Wire, “Three in Four New German Buildings Approved in 2023 Will Come with Heat Pump,” cleanenergywire.org

Rising Demand for Low-GWP Refrigerants Post F-Gas Revision

Regulation (EU) 2024/573 bans refrigerants with GWP > 750 in new heat-pump systems from 2025. Manufacturers have responded swiftly: Daikin debuted CO₂ VRV lines for retail formats, and Mitsubishi Heavy Industries rolled out R-32 systems with 675 GWP. The quota cut from 42.9 million t CO₂-eq in 2025 to 9 million t by 2032 tightens HFC supply, accelerating adoption of propane and CO₂ alternatives. Service-provider networks now invest in technician up-skilling to handle flammable A3 refrigerants, further professionalizing after-sales markets and reinforcing brand loyalty across the Europe air conditioning equipment market.

Urban Heat-Island Mitigation Projects in Southern Europe

Cities such as Toulouse, Seville, and Athens allocate municipal budgets to large-scale shading, tree-planting, and climate-adaptive infrastructure. Toulouse’s “+fraiche” program earmarks EUR 10 million to add 100,000 trees and retro-fit public buildings with energy-efficient cooling. These initiatives translate into new orders for variable-speed rooftop units able to deliver comfort without inflating electricity peaks. The Europe air conditioning equipment market therefore finds a steady pipeline of public-sector tenders that prioritize seasonal efficiency and low-noise operation in dense urban cores.

Data-Centre Expansion in FLAP-D Cities Boosting Precision Cooling

Powerful AI workloads are proliferating across Frankfurt, London, Amsterdam, Paris, and Dublin, pushing computational-density targets above 100 kW per rack. Operators such as Equinix have launched Heat Export programs that repurpose waste heat for municipal pools and district networks. This model drives demand for high-lift, low-GWP chillers and rear-door heat exchangers. For suppliers, the Europe air conditioning equipment market offers double-digit growth where precision cooling adds up to 35% of data-center opex, making efficiency gains financially compelling.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent Seasonal Energy-Efficiency Ratio (SEER) Minimums Raising Costs | -0.7% | EU-wide, particularly Germany, Netherlands | Short term (≤ 2 years) |

| Supply-Chain Disruptions in Compressors & Micro-chips | -0.9% | Global impact, strongest in Eastern Europe manufacturing | Medium term (2-4 years) |

| Skilled-Labour Shortage for Low-GWP Refrigerant Handling | -0.6% | EU-wide, most acute in Northern and Central Europe | Medium term (2-4 years) |

| Rebound Energy-Consumption Concerns Limiting Subsidy Scope | -0.4% | Southern Europe, particularly Spain, Italy, Greece | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Seasonal Energy-Efficiency Ratio (SEER) Minimums Raising Costs

Ecodesign rules now require real-life efficiency testing rather than static lab values, a change that adds 7-10% to system development costs. Smaller OEMs struggle to finance additional R&D and certification, prompting consolidation and potentially reducing model choice in entry-level tiers of the Europe air conditioning equipment market. Tougher building codes further compress payback windows, delaying some replacement decisions among price-sensitive homeowners.[2]REHVA, “Requirements for Seasonal Efficiency for Air-Conditioning Units,” rehva.eu

Supply-Chain Disruptions in Compressors & Micro-chips

Shortages in steel, copper, and semiconductor controllers have lengthened lead-times, particularly for variable-speed compressors. Cylinder supply for A2L refrigerants R-454B and R-32 tightened in early 2025, forcing schedule shifts on major commercial projects. While tier-one manufacturers invest in regionalized sourcing and vertical integration, mid-tier brands face allocation risks that curb their ability to scale in the Europe air conditioning equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: VRF Systems Drive Premium Growth

Room Air Conditioners maintained 27.48% share of the Europe air conditioning equipment market in 2025 and continue to dominate replacement demand in small residential and light commercial spaces. VRF configurations, though starting from a lower base, post a 9.15% CAGR through 2031 by offering simultaneous heating and cooling with partial-load efficiencies that help building owners meet EPBD targets. Retail chains adopt multi-split designs to optimize limited façade space, while rooftop packaged units remain favored in out-of-town retail and logistics. Manufacturers adapt VRF lines to propane and CO₂, mitigating F-Gas quota exposure and differentiating on sustainability credentials.

The segment’s competitive focus is shifting toward controls interoperability and remote diagnostics. Integrated BMS features allow energy managers to visualize tenant usage and fine-tune setpoints, a capability that raises retention rates in HVAC-as-a-Service contracts. Portable spot coolers serve niche requirements such as emergency response and event venues, especially during severe heat waves in Southern capitals. Thermal storage add-ons extend nighttime renewable surplus into peak daytime cooling, underlining the Europe air conditioning equipment market’s alignment with broader grid-balancing objectives.

By Technology: Inverter Adoption Accelerates Efficiency Gains

Non-Inverter units retained 67.95% Europe air conditioning equipment market share in 2025, mainly in low-ticket residential channels. However, inverter solutions expand at 8.85% CAGR as falling component costs close the upfront-price gap. Variable-frequency drives reduce start-up current draw, enabling smaller electrical infrastructure and opening retrofit opportunities in heritage buildings with limited supply capacity. Utility rebate programs that reward seasonal efficiency further skew procurement toward inverter designs.

Manufacturers are integrating AI-based predictive algorithms that adjust compressor speed based on occupancy and weather forecasts. This software layer enhances the Europe air conditioning equipment market value proposition from pure hardware to data-driven services. Reliability concerns that once hindered inverter adoption are dissipating as refrigerant-cooled power electronics demonstrate 50,000-hour MTBF performance in field trials.

By Cooling Capacity: Mid-Range Systems Capture Commercial Demand

Systems rated >15-20 kW best match the cooling loads of small office blocks and supermarkets, creating a sweet spot for suppliers balancing cost and complexity. The ≤8 kW tier dominates new-build housing, boosted by incentives linked to the Building Energy Act in Germany. A typical air-to-air heat pump in this class covers both comfort cooling and primary heating, accelerating the heat-pump penetration rate inside the Europe air conditioning equipment market. Equipment >20 kW underpins data-center, hospital, and manufacturing applications where redundancy and close-control specifications justify premium pricing.

Energy-storage integration is rising in the >8-15 kW bracket, allowing prosumers to store solar surplus in chilled water or phase-change-material tanks. The feature lowers peak-grid demand charges and aligns with EU taxonomy alignment reporting, adding a financial kicker to the Europe air conditioning equipment market adoption curve.

By Refrigerant Type: Natural Refrigerants Gain Regulatory Momentum

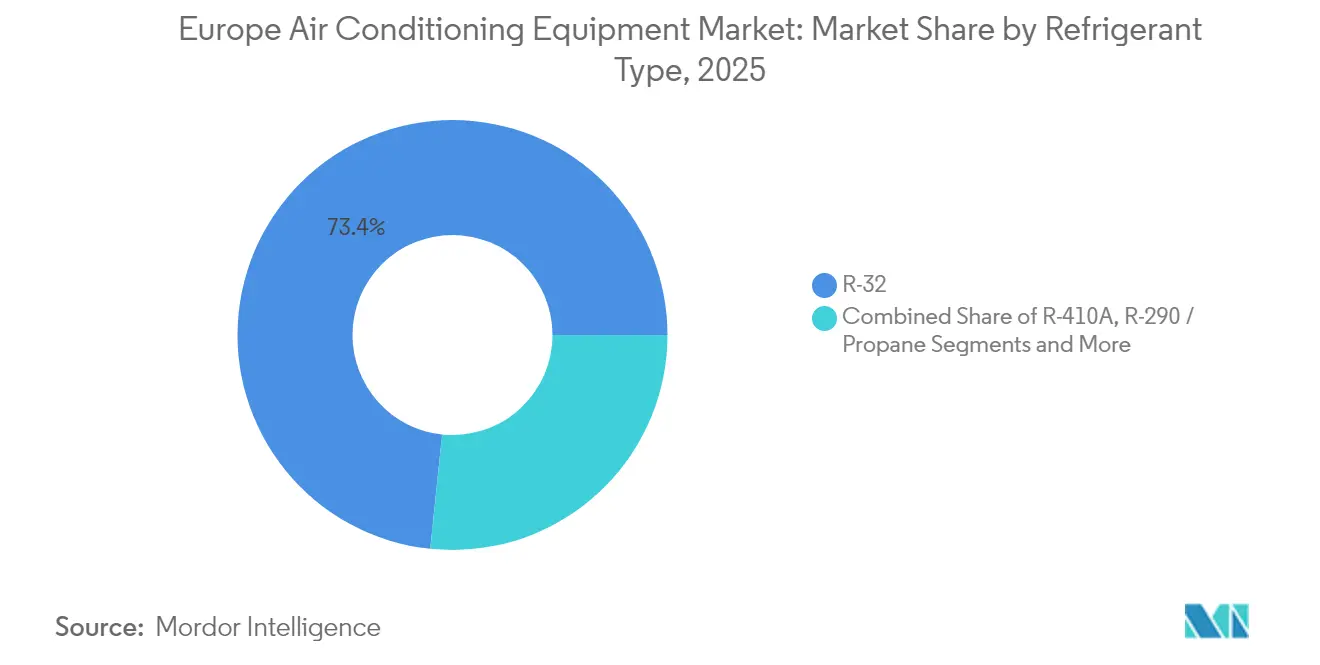

R-410A remains widespread in legacy stock but is locked out of new installations from 2025. R-32 acts as a transitional solution, offering 68% lower GWP yet meeting safety class A2L. Propane (R-290) is scaling in monobloc residential heat pumps, thanks to charge-limiting designs that meet IEC60285 updates. CO₂ (R-744) rapidly gains traction in supermarket and warehouse VRF networks because its GWP of 1 sidesteps phasedown tables completely. Hydro-Fluoro-Olefin blends such as R-1234yf cater to niche chiller retrofits where flammability constraints apply.

Technician certification requirements for flammable refrigerants are expanding training demand across the service ecosystem. Manufacturers running in-house academies capture share by reducing installation errors and warranty claims, reinforcing brand preference across the Europe air conditioning equipment market.

By End User: Data Centers Emerge as Growth Engine

Residential buildings still represent 42.05% of the Europe air conditioning equipment market size in 2025, sustained by renovation subsidies and consumer preference for integrated heating-cooling appliances. Data centers post an 10.65% CAGR as AI workloads drive rack densities and continuous thermal loads. Retail and co-working spaces seek flexible multi-zone systems that track fluctuating occupancy. Healthcare facilities tighten filtration and humidity control to comply with infection-prevention standards, making air-handling upgrades a recurrent budget line. Industrial process sectors such as food and pharma require temperature stability within ±1 °C, pushing demand for scroll and centrifugal chillers with rapid response times.

Hospitality operators leverage inverter heat pumps to cut operating costs and meet corporate sustainability goals, thereby improving asset valuations under green-bond frameworks. The heterogeneous requirement set creates room for specialized OEMs while ensuring that tier-one players with broad portfolios can cross-sell across the Europe air conditioning equipment market.

Geography Analysis

Germany leads the Europe air conditioning equipment market with a 17.12% revenue share in 2025, anchored by aggressive federal incentives and the Building Energy Act that mandates 65% renewable energy in new heating systems. The BAFA scheme has funded about 5,200 high-efficiency cooling projects, generating average energy savings of 40%. This ecosystem supports a robust installer network and underwrites order visibility for manufacturers.

Southern Europe registers the fastest growth. Spain, expanding at 8.15% CAGR, scales residential heat-pump retrofits and municipal cool-roof programs to curb Mediterranean heat stress. Italy’s Ecobonus and Superbonus tax credits spur whole-building renovations, with air-source heat pumps often bundled into façade upgrades. Urban heat-island strategies add incremental demand for precision rooftop units and district cooling loops, reinforcing double-digit growth prospects across the Europe air conditioning equipment market. Nordic countries showcase early adoption of cold-climate heat-pump technology. Denmark’s Heat Pump Pool offers subsidies of DKK 17,000-27,000 per system, catalyzing rural fuel-switch projects. Meanwhile, Poland is emerging as a manufacturing node: Aira’s EUR 300 million Wrocław factory will turn out 500,000 units annually, shortening lead-times into Central and Eastern Europe. Such regional supply additions lend resilience to the wider Europe air conditioning equipment market against global logistics disruptions

Competitive Landscape

Competitive Landscape

The Europe air conditioning equipment market is moderately consolidated, with scale advantages magnified by regulatory and supply-chain complexity. Samsung’s EUR 1.5 billion purchase of FläktGroup fortifies its presence in precision cooling and grants deeper reach into data-center end users. Bosch’s USD 8.1 billion acquisition of Johnson Controls-Hitachi’s residential HVAC arm nearly doubles its segment revenue and expands inverter heat-pump capacity inside the region. These moves compress the field of mid-size independents and accelerate platform-based product rationalization.

Technology differentiation centers on low-GWP refrigerants and smart-controls stacks. Daikin introduced CO₂ VRV systems, signaling that natural refrigerants can now power multi-split architectures traditionally reserved for HFCs. Mitsubishi Heavy Industries leverages R-32 adoption to balance performance with regulatory compliance. Suppliers with proprietary compressors and in-house electronics hedge against chip shortages that undermine delivery reliability elsewhere in the Europe air conditioning market.

Service capability is a decisive battleground. Panasonic’s acquisition of Poland-based Area Cooling expands regional service hubs, while Daikin’s takeover of Kylslaget and BKF Klima strengthens Nordic training infrastructure. OEMs that align installer accreditation with warranty tiers lock in annuity-like revenue and gather operational data that feeds back into product design, reinforcing first-mover advantages across the Europe air conditioning equipment market.

Europe Air Conditioning Equipment Industry Leaders

Daikin Industries Limited

Carrier Global Corporation

Johnson Controls–Hitachi Air Conditioning

Mitsubishi Electric Corporation

Panasonic Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung Electronics completed its EUR 1.5 billion acquisition of FläktGroup, marking the company's largest HVAC acquisition in eight years and positioning Samsung to capitalize on growing data center cooling demand driven by AI infrastructure expansion.

- March 2025: Daikin Europe launched its fourth-generation Altherma air-to-water heat pump series operating on natural refrigerant R-290 at ISH 2025, building on the success of over 1.3 million units sold across Europe.

- February 2025: The European Heat Pump Association launched a comprehensive refrigerant safety guidance project to address training requirements for technicians handling low-GWP refrigerants, responding to industry-wide skill shortages.

- December 2024: Mitsubishi Electric announced a USD 143.5 million investment to retrofit its Maysville, Kentucky factory for variable-speed compressor production, with manufacturing scheduled to begin in October 2027.

Europe Air Conditioning Equipment Market Report Scope

Europe Air Conditioning Equipment market is segmented By Type (Single Splits/Multi Splits, VRF, Air Handling Units, Chillers, Fans), By End User(Residential, Commercial, Industrial), and Country. The study further analyzes the overall impact of COVID-19 on the demand-side market dynamics and the ecosystem, in the near & short-term basis. The recent changes in trade scenario are also analyzed in the study.

By Product Type

| Room Air Conditioners | Window / Wall-Mounted Units |

| Portable / Spot Coolers | |

| Single-Split Systems | |

| Multi-Split Systems | |

| Variable Refrigerant Flow (VRF) Systems | |

| Rooftop Packaged Units | |

| Air Handling Units (AHU) | |

| Chillers | Centrifugal |

| Screw | |

| Scroll | |

| Fans and Ventilation Equipment | |

| Others (Evaporative Coolers, Thermal Storage, Etc.) |

By Cooling Capacity (kW)

| Less than 8 kW |

| 8 - 15 kW |

| 15 - 20 kW |

| Greater than 20 kW |

By Refrigerant Type

| R-32 |

| R-410A |

| R-290 / Propane |

| CO2 (R-744) |

| Hydro-Fluoro-Olefin (HFO-1234yf/ze) |

By Technology

| Inverter |

| Non-Inverter |

By End User

| Residential | |

| Commercial | Offices and Co-Working Spaces |

| Hospitality (Hotels, Resorts) | |

| Healthcare Facilities | |

| Retail and Shopping Centres | |

| Data Centres | |

| Industrial | Food and Beverage Processing |

| Pharmaceuticals and Cleanrooms |

By Distribution Channel

| Direct (Manufacturer to Key Accounts) |

| Indirect (Distributors / Installers / E-Commerce) |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Nordics (Sweden, Denmark, Norway, Finland) |

| Rest of Europe |

| By Product Type | Room Air Conditioners | Window / Wall-Mounted Units |

| Portable / Spot Coolers | ||

| Single-Split Systems | ||

| Multi-Split Systems | ||

| Variable Refrigerant Flow (VRF) Systems | ||

| Rooftop Packaged Units | ||

| Air Handling Units (AHU) | ||

| Chillers | Centrifugal | |

| Screw | ||

| Scroll | ||

| Fans and Ventilation Equipment | ||

| Others (Evaporative Coolers, Thermal Storage, Etc.) | ||

| By Cooling Capacity (kW) | Less than 8 kW | |

| 8 - 15 kW | ||

| 15 - 20 kW | ||

| Greater than 20 kW | ||

| By Refrigerant Type | R-32 | |

| R-410A | ||

| R-290 / Propane | ||

| CO2 (R-744) | ||

| Hydro-Fluoro-Olefin (HFO-1234yf/ze) | ||

| By Technology | Inverter | |

| Non-Inverter | ||

| By End User | Residential | |

| Commercial | Offices and Co-Working Spaces | |

| Hospitality (Hotels, Resorts) | ||

| Healthcare Facilities | ||

| Retail and Shopping Centres | ||

| Data Centres | ||

| Industrial | Food and Beverage Processing | |

| Pharmaceuticals and Cleanrooms | ||

| By Distribution Channel | Direct (Manufacturer to Key Accounts) | |

| Indirect (Distributors / Installers / E-Commerce) | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics (Sweden, Denmark, Norway, Finland) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe air conditioning equipment market?

The Europe air conditioning equipment market size totals USD 30.89 billion in 2026 and is projected to rise to USD 41.52 billion by 2031 at a 6.1% CAGR.

Which product category leads in market share?

Single-Split Systems hold the largest slice with 27.48% Europe air conditioning equipment market share in 2025, reflecting their popularity in residential and small commercial applications.

Why are VRF systems growing faster than other products?

VRF systems grow at a 9.15% CAGR because they deliver zone-specific control and meet stricter efficiency targets, making them attractive for offices, retail, and mixed-use buildings.

How is regulation affecting refrigerant choices?

EU Regulation 2024/573 bans new systems using refrigerants with GWP > 750 from 2025, driving rapid adoption of R-32, propane, and CO₂ across the Europe air conditioning market.

Which end-user segment shows the highest growth rate?

Data centers expand at 10.65% CAGR to 2031 due to surging AI workloads that require high-density, precision cooling solutions.

What role do heat-pump incentives play in market momentum?

National grants and reduced VAT, combined with the EU Heat Pump Accelerator Platform, sharply lower ownership costs and accelerate residential and commercial heat-pump adoption.

Page last updated on: