Market Overview

| Study Period | 2020 - 2031 |

|---|---|

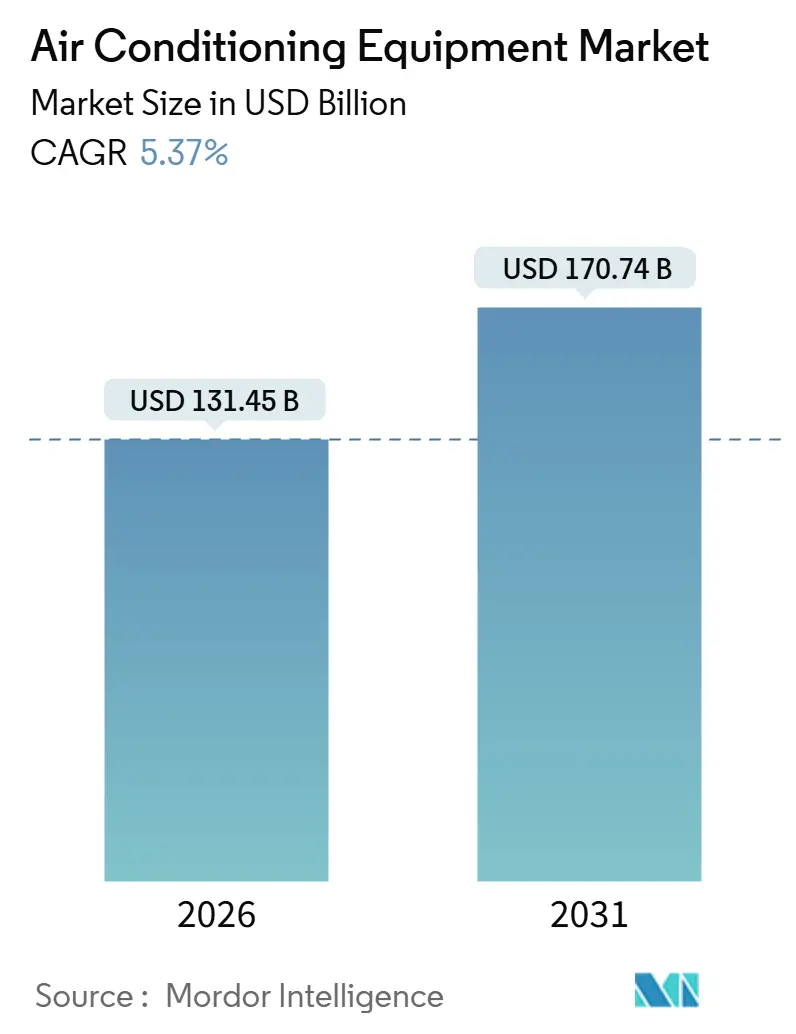

| Market Size (2026) | USD 131.45 Billion |

| Market Size (2031) | USD 170.74 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Conditioning Equipment Market Analysis by Mordor Intelligence

The air conditioning equipment market size is valued at USD 131.45 billion in 2026 and is projected to reach USD 170.74 billion by 2031, reflecting a 5.37% CAGR. The expansion is fueled by record heat waves, stricter energy-efficiency mandates, and hyperscale data-center growth. Variable refrigerant flow platforms are penetrating mixed-use towers, while inverter compressors dominate new residential demand. Rising commodity volatility is prompting vertical integration among leading manufacturers, and direct sales are reshaping procurement for large commercial projects.

Key Report Takeaways

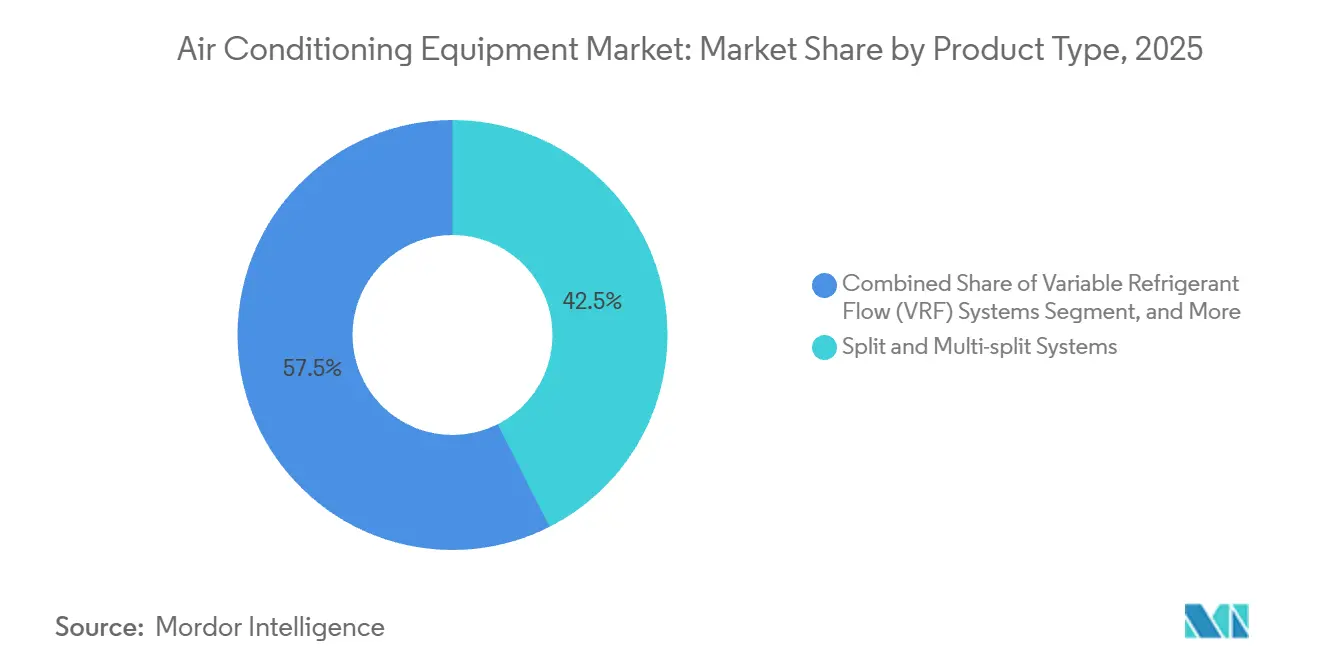

- By product type, split and multi-split systems led with 42.53% revenue share in 2025. However, variable refrigerant flow systems are advancing at a 6.73% CAGR through 2031.

- By technology, inverter systems captured 68.86% of the market share in 2025, and inverter platforms are expanding at a 6.53% CAGR through 2031.

- By end-user, residential accounted for 64.12% of the market share in 2025, while commercial is growing at a 6.85% CAGR to 2031.

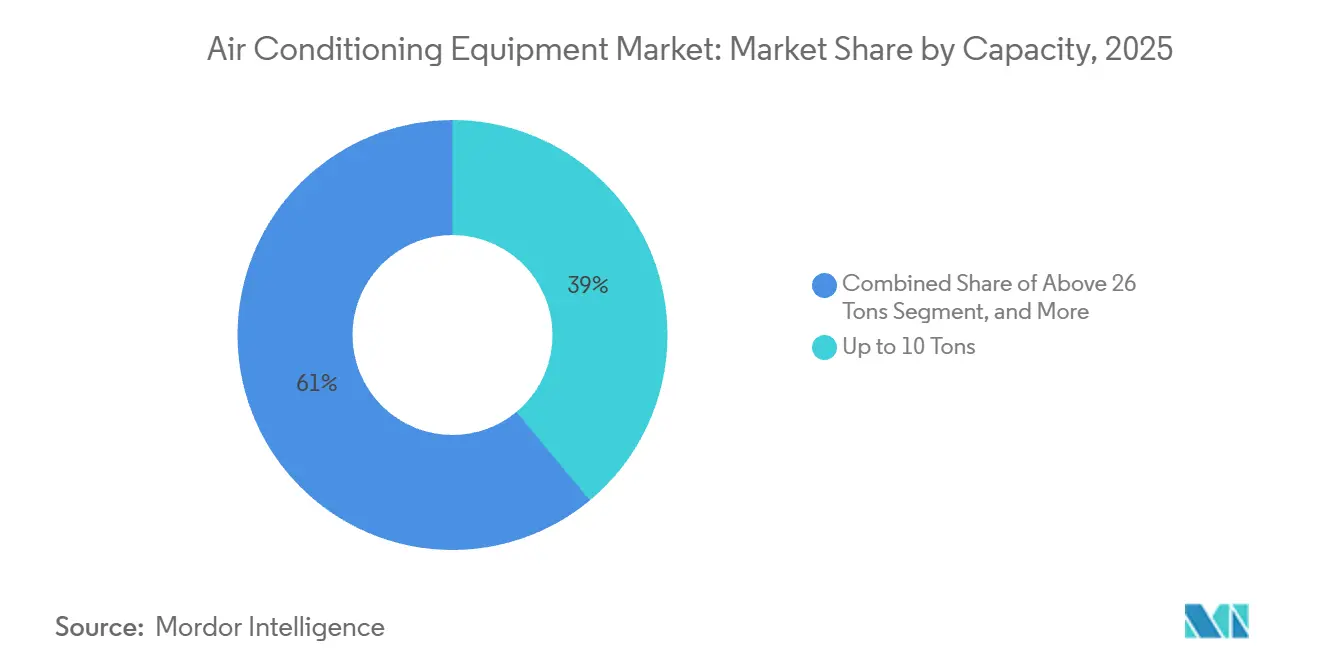

- By capacity, the up-to-10-tons segment accounted for 38.97% of 2025 revenue. While systems above 26 tons commanded a 7.51% CAGR forecast between 2026-2031.

- By distribution channel, dealer and retail stores accounted for 42.12% of 2025 sales, whereas direct sales are growing at a 7.79% CAGR.

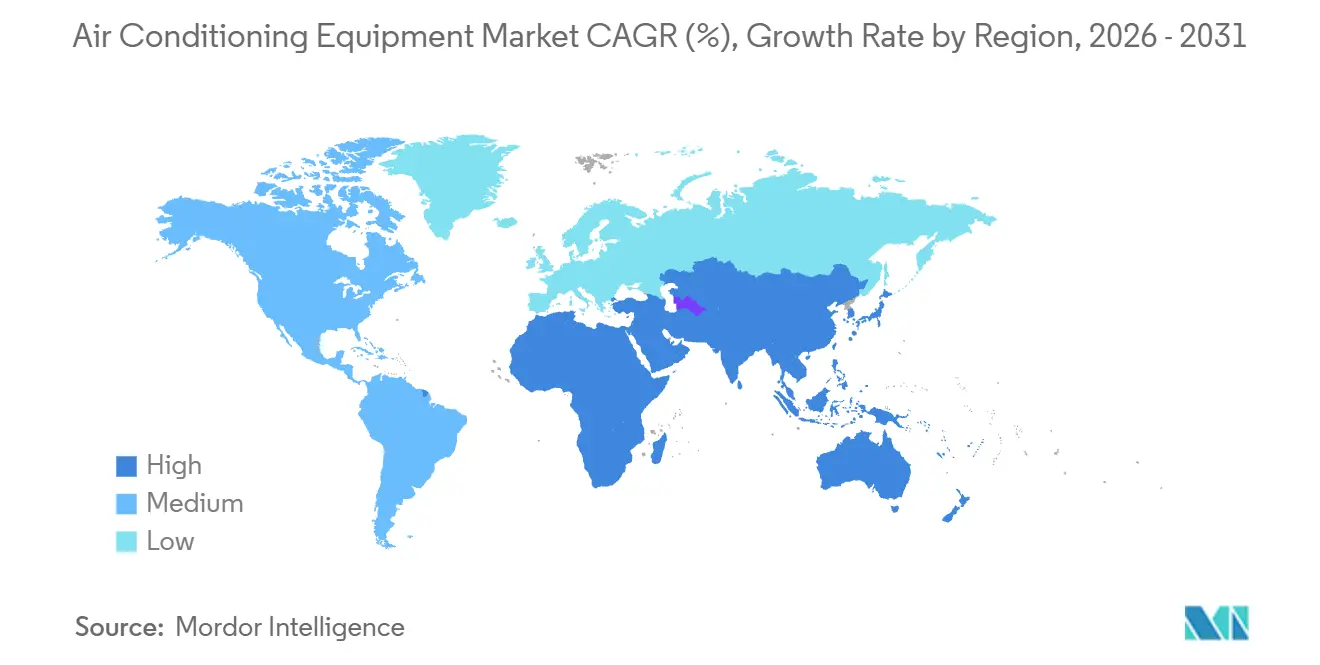

- By geography, Asia-Pacific led with 40.32% revenue share in 2025 and is projected to register an 8.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Air Conditioning Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Temperatures and Extreme-Heat Frequency | +0.9% | Global, with acute stress in Middle East, South Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Government Energy-Efficiency Standards and Cooling-Appliance Subsidies | +0.8% | North America, Europe, China, India | Medium term (2-4 years) |

| Urban High-Rise Construction Surge in Emerging Megacities | +0.7% | Asia-Pacific core (India, Indonesia, Philippines, Vietnam), spill-over to Middle East | Long term (≥ 4 years) |

| Edge and Hyperscale Data-Center Expansion Boosting Precision Cooling Demand | +0.6% | Global, concentrated in United States, China, Ireland, Singapore | Short term (≤ 2 years) |

| AI-Enabled Predictive-Maintenance Contracts Lowering Lifecycle Costs | +0.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing Demand for Off-Grid Solar-Powered Split AC Units in Power-Deficit Regions | +0.4% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Temperatures and Extreme-Heat Frequency

Climate records show 2024 as the hottest year to date, and the frequency of heat days above 40 °C is rising sharply in South Asia and the Middle East. Residential penetration is accelerating in tier-2 Indian cities, and hospitals in the Gulf are adding redundant chiller arrays to avert thermal shutdowns. [1]National Oceanic and Atmospheric Administration, “Global Climate Report 2024,” noaa.gov Higher cooling-degree days ensure sustained equipment replacement and capacity additions, keeping the air conditioning equipment market on an upward trajectory. Utilities in heat-stressed regions are also revising peak tariffs, incentivizing building owners to adopt high-efficiency VRF and inverter systems. Long-term climate projections pointing to 20-30% more cooling-degree days by 2040 translate into structural demand rather than cyclical replacement.

Government Energy-Efficiency Standards and Cooling-Appliance Subsidies

SEER2 thresholds in the United States, Ecodesign rules in the European Union, and upgraded GB 21455-2024 requirements in China collectively tighten minimum efficiency baselines. [2]U.S. Department of Energy, “SEER2 Standards for Residential Air Conditioners,” energy.gov Subsidy programs covering 20-30% of the incremental inverter cost in India and rebate schemes tied to seasonal energy-efficiency ratios in emerging Asia are closing the price gap with fixed-speed models. Manufacturers are rapidly shifting portfolios to inverter compressors, and component suppliers are scaling variable-speed drives, reinforcing the air conditioning equipment market’s technology transition. Tightened standards effectively shorten the obsolescence cycle for non-inverter units, creating a pull-through effect for higher-margin products.

Urban High-Rise Construction Surge in Emerging Megacities

Mixed-use towers exceeding 30 stories in Jakarta, Manila, and Ho Chi Minh City require centralized VRF or chilled-water systems because small window units cannot meet load diversity or floor-space constraints. [3]CBRE Asia-Pacific, “Asia-Pacific Real Estate Market Outlook 2025,” cbre.com Developers cite 8-12% gains in rentable area when duct-free VRF replaces bulky ducted alternatives. The construction pipeline in India’s National Capital Region and the Gulf states signals multi-year bulk orders, underpinning direct-sales channels and multi-year service contracts. As zoning rules allow more vertical density, demand tilts toward large-capacity outdoor condensers connected to dozens of indoor units, deepening the installed base for predictive service platforms.

Edge and Hyperscale Data-Center Expansion Boosting Precision Cooling Demand

Cloud providers have earmarked USD 120 billion for data-center builds in 2025, each facility consuming 20-50 MW and requiring precision cooling within a narrow 18-27 °C envelope. Liquid-cooling technologies such as direct-to-chip plates reduce fan energy up to 60%, opening premium niches for OEMs versed in refrigerant-neutral, modular packages. Edge sites in tier-2 cities require 100-500-ton modular chillers, enabling faster replacement cycles and higher aftermarket parts revenue. The segment’s double-digit growth provides an outsized contribution to overall gains in the air conditioning equipment market, despite its smaller volume base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper and Semiconductor Prices Squeezing OEM Margins | -0.6% | Global, acute in China, India, Southeast Asia manufacturing hubs | Short term (≤ 2 years) |

| Kigali Amendment-Driven Accelerated HFC Phase-Down Compliance Costs | -0.5% | Global, phased implementation with Article 5 countries facing 2029-2047 deadlines | Medium term (2-4 years) |

| Chronic Shortage of Certified HVAC Technicians for Inverter and VRF Systems | -0.4% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Grid Decarbonization Policies Favoring Passive and District-Cooling Alternatives | -0.3% | Europe, select Middle East cities, California, New York | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper and Semiconductor Prices Squeezing OEM Margins

Copper prices swung between USD 10,200 and USD 9,100 per metric ton in 2024, adding USD 3-8 to component costs per unit and compressing gross margins by up to 180 basis points. Semiconductor lead times for power modules reached 26 weeks, delaying inverter launches. Large players are hedging through vertical integration, exemplified by a Vietnamese copper-tube mill investment, whereas smaller brands without hedging capacity risk negative operating margins. Persistent volatility could dampen price-sensitive demand in emerging markets, limiting near-term growth in the air conditioning equipment market.

Kigali Amendment-Driven Accelerated HFC Phase-Down Compliance Costs

The Kigali Amendment mandates an 80% HFC reduction by 2047, and intermediate cuts take effect as early as 2029 in many Article 5 countries. Retooling a single compressor line for mildly flammable A2L refrigerants costs USD 15-25 million, and aggregate spending is estimated above USD 3 billion through 2027. Higher-pressure tubing, new safety sensors, and technician retraining elevate initial selling prices, risking demand deferral in price-sensitive markets. Compliance spending accelerates consolidation as regional brands exit, potentially reducing competition while also elevating barriers to new entrants in the air conditioning equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: VRF Systems Gain Share in Mixed-Use Towers

Variable refrigerant flow platforms generated a 6.73% CAGR outlook versus the overall 5.37%, making them the fastest-rising segment within the air conditioning equipment market size for the 2026-2031 window. Split and multi-split units still dominate revenue because single-room cooling prevails in emerging residential settings. Developers of 30-plus-story towers prefer VRF for zone control, energy recovery, and floor-space gains, reinforcing direct-sales relationships.

Expanded utility rebates, heightened energy codes, and falling inverter costs are compressing the price delta between traditional split units and VRF mini-modules. The ability to link up to 64 indoor fan-coils to a single outdoor unit supports high diversity loads in mixed-use floorplates. In parallel, packaged rooftop units advance steady replacement demand in North America’s light-commercial sector, while centrifugal and screw chillers (>500 tons) address pharmaceutical warehouses and semiconductor fabs that need sub-degree stability, adding diversity to the air conditioning equipment market.

By Technology: Inverter Dominance Reflects Regulatory and Cost Pressures

Inverter compressors secured 68.86% of 2025 shipments and are forecast to rise at a 6.53% clip, further raising their share of the overall air conditioning equipment market share by 2031. Non-inverter models linger in rural and rental stock but shrink annually as subsidy programs shrink incremental cost gaps.

Artificial-intelligence-enabled controllers now analyze weather, tariff windows, and occupancy in real time, trimming bills by another 8-12%. Demand-response integration allows building owners to monetize curtailed load. Fixed-speed systems remain viable in voltage-unstable zones of Africa and Latin America, yet global inverter penetration is projected above 80% by 2030, underpinned by scale economics and policy pressure.

By End-User: Commercial Segments Outpace Residential on Retrofit Wave

Residential demand still accounted for 64.12% of 2025 volume, but offices, hotels, and retail properties are forecast to expand faster, at a 6.85% CAGR, outpacing the air conditioning equipment market average. Retrofit cycles in North America and Europe are driven by carbon-intensity caps such as New York City’s Local Law 97.

Industrial expansion comes from semiconductor fabs in Arizona and Gujarat, and from cold-chain warehouses that require ±0.5 °C stability. VRF systems with heat recovery appeal to commercial landlords aiming for sustainability certifications, while ammonia chillers gain traction in cold-chain applications due to zero global-warming potential.

By Capacity: Above 26 Tons Expands on Data-Center and Pharma Demand

Large systems above 26 tons grow at 7.51% annually, the fastest among capacity brackets, buoyed by hyperscale data-center and pharmaceutical infrastructure investments. The 0-10-ton tier controlled 38.97% of 2025 revenue, serving homes and small offices.

Mid-range 11-26-ton units equip mid-rise apartments and boutique hotels, where compact rooftop chillers balance upfront cost versus floor-area efficiency. Large centrifugal chillers paired with free-cooling towers enable data-center PUE targets below 1.2, and modular arrays provide N+1 redundancy in vaccine cold chains, strengthening the air conditioning equipment market size.

By Distribution Channel: Direct Sales Surge on Bulk Developer Contracts

Dealer-retail outlets accounted for 42.12% of 2025 units, yet direct sales to developers and facility managers are forecast to grow at a 7.79% CAGR through 2031, boosted by turnkey procurement bundling equipment, analytics, and refrigerant transition services. Bulk contracts secure 15-25% volume discounts and lock in priority production slots during component shortages.

Online channels post double-digit gains in urban India and Southeast Asia, where e-commerce infrastructure and certified installer networks mature. Hybrid D2C portals allow consumers to configure systems online, then assign installations to local dealers, reshaping commission splits while sustaining service network density.

Geography Analysis

Asia-Pacific delivered 40.32% of 2025 revenue and is on pace for an 8.43% CAGR, outstripping every other region across the air conditioning equipment market. China’s growth moderates as tier-1 saturation rises, but India, Indonesia, and Vietnam continue double-digit installation growth driven by extreme heat and improved grid access. High-rise boom towns in Jakarta and Manila specify large VRF backbones, and Japan’s mature stock focuses on premium air-purification features. Australia’s commercial sector is retrofitting rooftop units to satisfy 2022 energy-efficiency code updates.

North America and Europe air conditioning equipment market expand 4-5% annually on replacement cycles, heat-pump adoption, and corporate net-zero targets. U.S. residential split-system shipments topped 8.2 million in 2024, while the Inflation Reduction Act continues to underwrite heat-pump retrofits. The European Union’s near-zero-energy mandate for non-residential buildings by 2030 pushes VRF upgrades in Germany, France, and the United Kingdom.

The Middle East and Africa register 6-7% growth. District-cooling networks in Dubai and Riyadh anchor large-capacity chiller demand, while off-grid solar splits penetrate power-deficient communities in Sub-Saharan Africa. South American markets grow 5-6%, led by Brazilian residential demand and Argentine commercial retrofits following electricity-subsidy phaseouts. Altogether, regional dynamics reinforce the diversified growth profile of the air conditioning equipment market.

Competitive Landscape

The market remains fragmented, with players including Daikin, Gree, Midea, Carrier, and others. To buffer copper and semiconductor volatility, leaders pursue vertical integration, as seen in tube-mill investments and compressor capacity expansions. Technology competition centers on inverter algorithms, low-GWP refrigerant readiness, and digital platforms such as OpenBlue that monetize demand-response flexibility.

Regional challengers like Haier, LG, and Fujitsu General compete on localized service and price in Asia and Latin America. Direct-to-consumer portals and subscription models disrupt traditional dealer margins. Patent filings around A2L refrigerant blends and sodium-ion battery-integrated solar ACs signal evolving areas of differentiation. Standards updates, notably ASHRAE 15 for leak detection, favor incumbents with established safety infrastructure, raising entry barriers for smaller brands.

Air Conditioning Equipment Industry Leaders

Daikin Industries, Ltd.

Bosch Thermotechnology GmbH

Mitsubishi Electric Corporation

LG Electronics Inc.

Carrier Global Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Daikin announced a USD 450 million capacity expansion at its Shiga VRF plant, targeting Q3 2026 commissioning.

- December 2025: Carrier closed the USD 13 billion Viessmann climate-solutions acquisition, aiming for USD 500 million cost synergies by 2027.

- November 2025: Gree opened a 5 million-unit inverter-split factory in Nanjing for Southeast Asian and Latin American export markets.

- October 2025: Trane partnered with Microsoft to install liquid-cooling systems across Azure data centers, achieving PUE below 1.15.

Global Air Conditioning Equipment Market Report Scope

Air conditioning equipment is designed to regulate temperatures and provide fresh air in rooms experiencing high temperatures and humidity, ensuring a comfortable indoor environment. The market study analyzes trends and opportunities for different types of air conditioning equipment, including split systems, variable refrigerant flow, air handling units, chillers, fan coils, indoor packaged units, and rooftop units, used across various end-user industries. Furthermore, the study examines the influence of macroeconomic factors on the market.

The Air Conditioning Equipment Market Report is Segmented by Product Type (Split and Multi-Split Systems, Variable Refrigerant Flow Systems, Packaged and Rooftop Units, and Chillers), Technology (Inverter Systems, and Non-Inverter Systems), End-User (Residential, Commercial, and Industrial), Capacity (Up to 10 Tons, 11-18 Tons, 19-26 Tons, and Above 26 Tons), Distribution Channel (Direct Sales, Dealer and Retail Stores, and Online), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Split and Multi-Split Systems |

| Variable Refrigerant Flow (VRF) Systems |

| Packaged and Rooftop Units |

| Chillers |

By Technology

| Inverter Systems |

| Non-Inverter Systems |

By End-User

| Residential |

| Commercial |

| Industrial |

By Capacity (Tons of Refrigeration)

| Up to 10 Tons |

| 11 - 18 Tons |

| 19 - 26 Tons |

| Above 26 Tons |

By Distribution Channel

| Direct Sales |

| Dealer / Retail Stores |

| Online |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Split and Multi-Split Systems | ||

| Variable Refrigerant Flow (VRF) Systems | |||

| Packaged and Rooftop Units | |||

| Chillers | |||

| By Technology | Inverter Systems | ||

| Non-Inverter Systems | |||

| By End-User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Capacity (Tons of Refrigeration) | Up to 10 Tons | ||

| 11 - 18 Tons | |||

| 19 - 26 Tons | |||

| Above 26 Tons | |||

| By Distribution Channel | Direct Sales | ||

| Dealer / Retail Stores | |||

| Online | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the air conditioning equipment market in 2031?

The air conditioning equipment market is forecast to reach USD 170.74 billion by 2031.

Which technology segment is growing fastest through 2031?

Inverter-based systems are projected to advance at a 6.53% CAGR through 2031.

How quickly are VRF systems expanding in the product mix?

VRF platforms are expected to post a 6.73% CAGR between 2026-2031, outpacing other product categories.

Which region leads in market share and growth rate?

Asia-Pacific holds the largest share at 40.32% of 2025 revenue and is expanding at an 8.43% CAGR.

Why are large-capacity (Above 26 Tons) systems gaining traction?

Hyperscale data-center builds and pharmaceutical cold-chain warehouses demand high-capacity chillers, driving a 7.51% CAGR for this bracket.

How are direct sales channels evolving?

Developers and facility managers increasingly sign multi-year turnkey contracts, causing direct procurement to grow at 7.79% CAGR through 2031.

Page last updated on: