Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

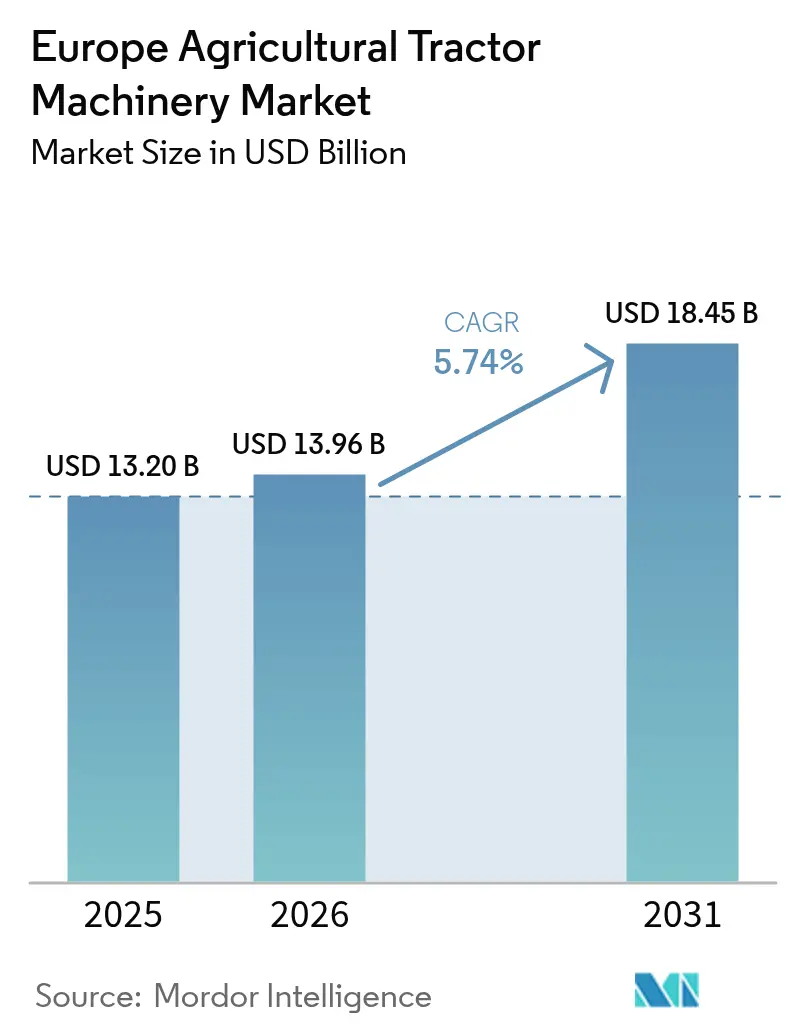

| Base Year Market Size (2025) | USD 13.2 Billion |

| Market Size (2026) | USD 13.96 Billion |

| Market Size (2031) | USD 18.45 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

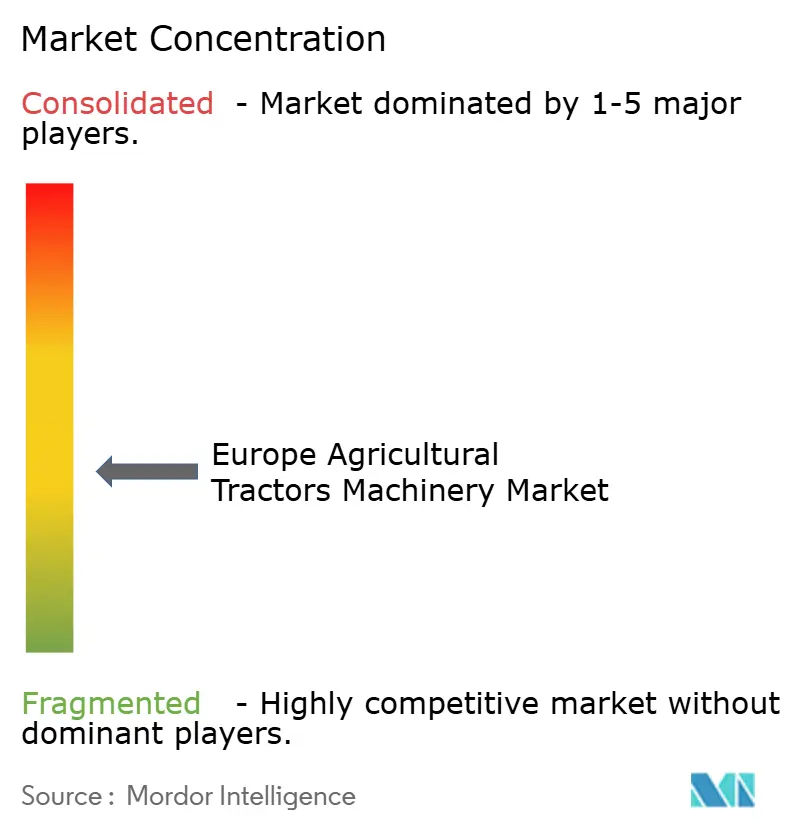

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The Europe agricultural tractor machinery market size was valued at USD 13.2 billion in 2025 and estimated to grow from USD 13.96 billion in 2026 to reach USD 18.45 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031). Demand gains stem from the European Union Common Agricultural Policy eco-schemes that underwrite precision-farming hardware, Stage V emissions compliance that accelerates fleet renewal, and persistent labor shortages that nudge farms toward automation[1]Source: European Commission, “CAP 2023-27 Eco-Scheme Overview,” agriculture.ec.europa.eu. Suppliers answer with powered, sensor-rich implements that integrate through the ISO 11783 (ISOBUS) protocol, while electrification pilots create a parallel pull for low-draw attachments compatible with battery tractors. At the same time, dealer inventory overhang from 2023, volatile commodity prices, and mixed-fleet interoperability frictions temper adoption in price-sensitive pockets of Central and Eastern Europe. Competitive intensity remains moderate because the top five vendors leave room for niche specialists that address strip-till, orchard under-vine mowing, or greenhouse applications.

Key Report Takeaways

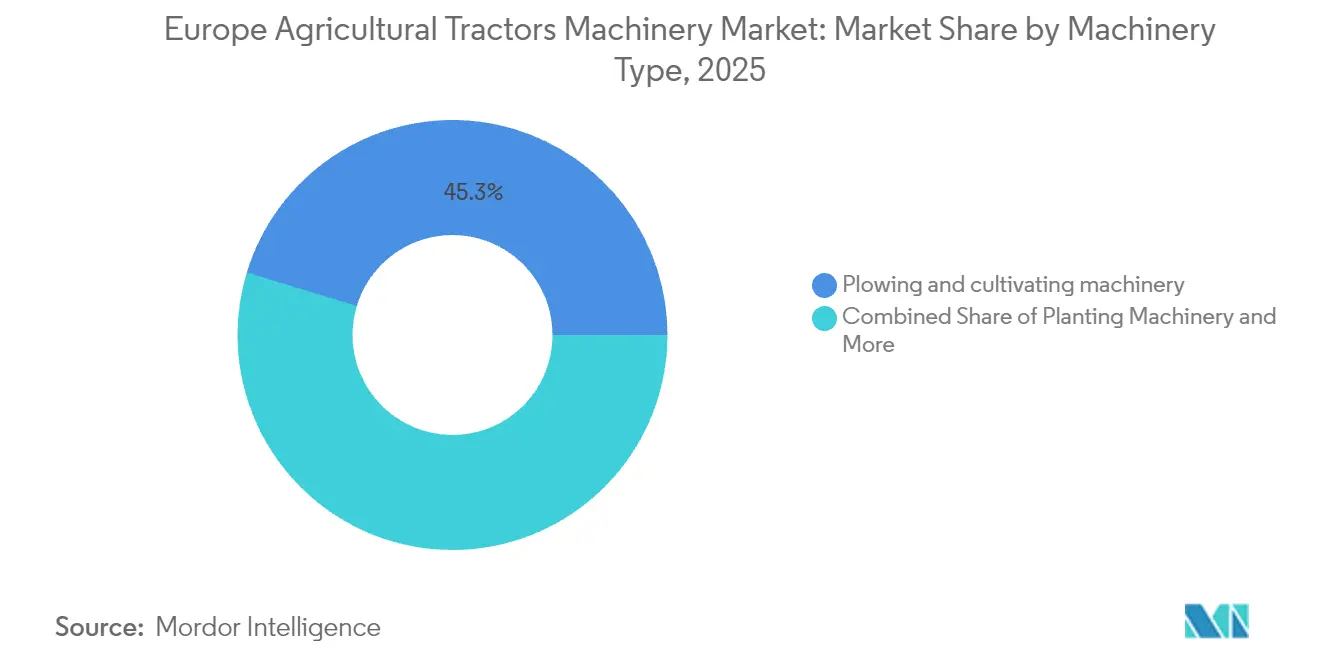

- By machinery type, plowing and cultivating machinery held 45.30% of the Europe agricultural tractor machinery market share in 2025, while planting machinery are advancing at a 7.66% CAGR through 2031.

- By geography, Germany accounted for 22.20% of regional revenue in 2025, while the Netherlands is forecast to post the fastest 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-farming subsidies under the EU Common Agricultural Policy (2025–2027 tranche) | +1.2% | Pan-European, with highest uptake in France, Germany, and Netherlands | Medium term (2–4 years) |

| Labor shortages accelerating automation demand in Western and Northern Europe | +1.0% | Germany, Netherlands, Denmark, Sweden, and United Kingdom | Short term (≤ 2 years) |

| Stage V emissions rules driving retrofit and replacement of PTO-efficient implements | +0.9% | EU27 plus United Kingdom, Norway, and Switzerland | Medium term (2–4 years) |

| Growth of controlled-traffic farming boosting demand for lightweight, wide-working-width tillage tools | +0.7% | United Kingdom, Germany, France, and Denmark | Long term (≥ 4 years) |

| Surge in vineyard and orchard mechanization in Mediterranean countries | +0.8% | Italy, Spain, France (southern regions), Portugal, and Greece | Medium term (2–4 years) |

| Emerging electric-tractor ecosystem requiring low-draw, ISOBUS-ready implements | +0.6% | Netherlands, Germany, Scandinavia, pilot zones in France and Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision-Farming Subsidies Under the EU Common Agricultural Policy (2025–2027 Tranche)

Mandatory eco-schemes now channel 25% of direct payments into proven input-efficiency projects, pushing farms to buy variable-rate planters, ISOBUS sprayers, and yield-mapping sensors. France, Germany, and Poland are moving toward such upgrades. Adoption lifts data-sharing, cooperative Terrena saw 38% of members stream implement telemetry in 2024, extending equipment life by 15%. Certification requirements favor ISO 11783-compliant brands and squeeze fringe suppliers out of subsidy eligibility, consolidating demand around a few large telematics ecosystems.

Labor Shortages Accelerating Automation Demand in Western and Northern Europe

Full-time farm employment in Germany fell 12% year on year in 2024. Horticulture in the Netherlands faces similar gaps, spurring take-up of robotic planters and vision-guided sprayers. Deere and Company reported a 47% jump in European shipments of its See and Spray system during 2024. Danish Agro deployed 15 autonomous mower-conditioner units that cut hay harvest labor costs by 30% while running day and night. The Europe agricultural tractor machinery market, therefore, tilts toward powered implements with embedded autonomy, widening the gap with legacy passive tools.

Stage V Emissions Rules Propelling Retrofit and Replacement of PTO-Efficient Implements

January 2024 enforcement of Stage V non-road mobile machinery rules reduces nitrogen oxides by up to 95% relative to Stage IV. Older implements lack the load-sensing electronics needed to sync with selective catalytic reduction dosing, pushing operators to newer PTO-efficient models. CNH Industrial’s Raven Autonomy platform links implement draft load to engine control and cut diesel-exhaust-fluid cost by EUR 4 (USD 4.2) per hectare in German trials. National retrofit grants in Italy and Spain, covering EUR 8,000 to EUR 15,000 (USD 8,500 to USD 15,900) per baler or forage harvester, shorten the replacement cycle in high-horsepower fleets.

Growth of Controlled-Traffic Farming Boosting Demand for Lightweight, Wide-Working-Width Tillage Tools

Controlled-traffic farming confines wheel tracks and curbs soil compaction by 70%[2]Source: Cranfield University, “Controlled-Traffic Farming Benefits 2024,” cranfield.ac.uk. United Kingdom adoption reached 18% of arable acres in 2024, aided by GBP 58 (USD 73) per hectare grants. Manufacturers answer with carbon-fiber tines and folding 12-meter cultivators. Väderstad’s TopDown TD 600 maintains 8 centimeter depth uniformity on rolling land and raised spring barley emergence by 9% in Danish trials. Large estates realize rapid paybacks while small farms struggle to fund the capital outlay.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dealer over-inventory since 2023 suppressing fresh orders through 2026 | -0.8% | Germany, France, United Kingdom, and Benelux | Short term (≤ 2 years) |

| High capital cost for smart implements on fragmented small holdings in Eastern Europe | -0.6% | Poland, Romania, Hungary, Bulgaria, and Baltic states | Medium term (2–4 years) |

| Complex interoperability standards (ISOBUS, TIM) delaying adoption among mid-size farms | -0.5% | Pan-European, acute in mixed-fleet operations | Medium term (2–4 years) |

| Volatile commodity prices lowering farmers' cash flow for discretionary equipment | -0.7% | Arable regions: Poland, Romania, France (Beauce), and Germany (Saxony) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dealer Over-Inventory Amassed Since 2023 Suppressing Fresh Orders through 2026

European dealers carried 9.2 months of implement supply at the start of 2024 versus a normal 5.5 months. BayWa posted EUR 340 million (USD 360 million) in unsold tillage and seeding stock, then cut 2025 purchase plans by 22%. French distributor InVivo similarly trimmed new orders 18% and pivoted to refurbishing used assets. Manufacturers extended payment terms to 180 days and offered consignment, but the margin squeeze still discourages dealers from stocking incremental models, slowing near-term growth in the Europe agricultural tractor machinery market.

High Capital Cost for Smart Implements on Fragmented Small Holdings in Eastern Europe

Average farm sizes are 11.2 hectares in Poland, 3.9 hectares in Romania, and 6.1 hectares in Bulgaria[3]Source: Eurostat, “Agricultural Census 2024,” ec.europa.eu/eurostat. A EUR 55,000 (USD 58,000) GPS precision seeder equals nearly five times the median annual income of a Polish arable farm, extending payback beyond normal planning horizons. Romania allocated budgets for shared-machinery grants yet saw less than 30% uptake due to co-financing hurdles. Fragmentation, therefore, bifurcates the Europe agricultural tractor machinery market into a high-tech core and a low-investment periphery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Planting Machinery Outpace Plowing and Cultivating Machinery

Plowing and cultivating machinery tools secured 45.30% of 2025 revenue in the Europe agricultural tractor machinery market. Planting machinery, aided by controlled-traffic mandates and real-time variable-rate algorithms, will grow at a 7.66% CAGR through 2031. French cooperative Axéréal documented a 12% reduction in seed cost per hectare after rolling out GPS section control across 85,000 hectares.

Planting machinery capture the fastest expansion because eco-scheme payments specifically reward reductions in seed waste. Lemken’s electric-meter Azurit planter sells at a 28% premium yet pays back within three seasons on farms above 500 hectares. Haying and forage machinery continue to serve the continent’s grassland but hinge on stable dairy and beef herds. Other specialty implements remain fragmented. The segment illustrates how subsidy rules and data capability shift profits toward powered, software-defined machines within the wider Europe agricultural tractor machinery market size.

Geography Analysis

Germany accounted for 22.20% of regional revenue in 2025, but moderate growth ahead. Stage V compliance drove a 14% spike in PTO-efficient baler sales during 2024, yet EUR 340 million (USD 360 million) in dealer stock keeps orders subdued until 2026. France secures eco-scheme allocations every year, which boosts purchases of precision seeders and sprayers. Wheat price volatility does dampen discretionary spending, though subsidies and insurance soften the blow.

Italy’s forecast growth rate relies on labor-saving vineyard tools in Piedmont, Veneto, and Tuscany, where manual work costs exceed EUR 1,200 (USD 1,270) per hectare. Maschio Gaspardo’s under-vine tiller shipments validate this trend. Spain pursues parallel moves in Andalusia and Catalonia under a subsidy that reimburses 40% of equipment spend. The United Kingdom experienced a 6% sales dip in 2024 as farms adjusted to new environmental land payments, although GBP 58 (USD 73) per hectare grants for controlled-traffic farming supported lightweight cultivator demand.

The Netherlands will log the region’s fastest 7.98% CAGR. Battery-electric tractors operate in dense greenhouse clusters, and nitrogen efficiency rules force rapid rollout of variable-rate fertilizer applicators. Central Europe grows more modestly because farm fragmentation inflates payback periods, yet large estates in western Poland and the Czech Republic deploy cutting-edge implements. Scandinavia leads autonomy pilots, highlighted by Danish Agro’s autonomous mower deployment, while the Balkans and Baltics continue to trail. These disparities reveal how the Europe agricultural tractor machinery market splits along both technology and purchasing-power lines.

Competitive Landscape

The top five suppliers, Deere & Company, CNH Industrial, AGCO Corporation, Kuhn Group, and Lemken, collectively hold modest percentage of 2025 revenue, placing the Europe agricultural tractor machinery market in a moderately concentrated state. Deere’s computer-vision See and Spray system lifted herbicide precision and boosted European shipments 47% in 2024. CNH Industrial’s Raven Autonomy links implement draft load to tractor controls and cuts diesel exhaust fluid spend by EUR 4 (USD 4.2) per hectare.

Interoperability gaps persist, with 38% of supposedly ISOBUS-ready implements failing cross-brand tests. Below the top tier, Väderstad, Pöttinger, Amazone, Kverneland Group, Horsch, and Maschio Gaspardo carve share in specific niches. Väderstad’s TopDown TD 600 improved spring barley emergence by nine per cent in Danish trials and secured large estate orders. Pöttinger’s Aerosem drill targets electric-tractor buyers with 22% lower draw, while Amazone and Kverneland Group push retrofit kits that add ISOBUS task control to legacy seeders.

French startup Ekylibre raised funds to scale an open-source farm-management platform that aggregates data from any ISO 11783 implement, and Deere purchased a minority position to strengthen its ecosystem. Strategic moves show that vendors combining proprietary innovation with open standards earn trust across mixed-brand fleets inside the Europe agricultural tractor machinery market.

Europe Agricultural Tractor Machinery Industry Leaders

CNH Industrial N.V.

AGCO Corporation

Kuhn Group

Lemken GmbH & Co. KG

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Horsch has introduced its latest cultivation and seeding machinery in Europe, highlighting innovations for efficiency and precision in modern farming. The launch underscores Europe’s role as a hub for advanced agricultural technology, with potential global spillover benefits.

- September 2025: Case IH has launched the Farmall A tractor with 110 HP in Europe, expanding its popular range. The new model emphasizes power, versatility, and efficiency to meet the needs of modern European farmers.

- April 2025: New Holland and MASCHIO GASPARDO have announced a new cooperation in Europe to distribute and supply crop preparation implements such as mowers, mower conditioners, tedders, and rotary rakes. The partnership will also co-develop future products, with MASCHIO GASPARDO leading engineering efforts to deliver innovative, customer-focused hay and forage solutions.

Europe Agricultural Tractor Machinery Market Report Scope

By Machinery Type

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Other Plowing and Cultivating Machinery | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery | |

| Sprayers | |

| Other Types |

By Country

| Germany |

| France |

| Italy |

| United Kingdom |

| Spain |

| Netherlands |

| Poland |

| Rest of Europe |

| By Machinery Type | Plowing and Cultivating Machinery | Plows |

| Harrows | ||

| Rotovators and Cultivators | ||

| Other Plowing and Cultivating Machinery | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Sprayers | ||

| Other Types | ||

| By Country | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the 2026 value of the Europe agricultural tractors machinery market?

The market is valued at USD 13.96 billion in 2026.

How fast will the market grow to 2031?

It is forecast to increase at a 5.74% CAGR, reaching USD 18.45 billion by 2031.

Which machinery type is expanding fastest?

Planting machinery is rising at a 7.66% CAGR through 2031.

Why is the Netherlands the fastest growing country market?

Dense greenhouse clusters, 50% co-financing for precision implements, and early adoption of electric tractors drive an 7.98% forecast CAGR.

Page last updated on: