Europe Agricultural Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Market Size (2025) | USD 26.5 Billion |

| Market Size (2030) | USD 32.60 Billion |

| Growth Rate (2025 - 2030) | 4.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Agricultural Tractor Market Analysis by Mordor Intelligence

The Europe agricultural tractor market size is valued at USD 26.5 billion in 2025 and is projected to reach USD 32.6 billion by 2030, registering a 4.2% CAGR over the forecast period. Persistently high labor costs, tightening Stage V emission rules, and accelerating electrification initiatives keep demand for modern equipment resilient even as farmer margins fluctuate. Medium-horsepower machines dominate because they fit the acreage profiles of most European farms, while precision-agriculture hardware integration stimulates replacement cycles rather than outright fleet expansion. OEMs (Original Equipment Manufacturers) counter cyclical demand by bundling financing with technology upgrades, smoothing order intake, and protecting dealer networks. Against this backdrop, the European tractor market continues to pivot toward battery-electric and autonomous capabilities while grappling with supply-chain volatility and component inflation.

Key Report Takeaways

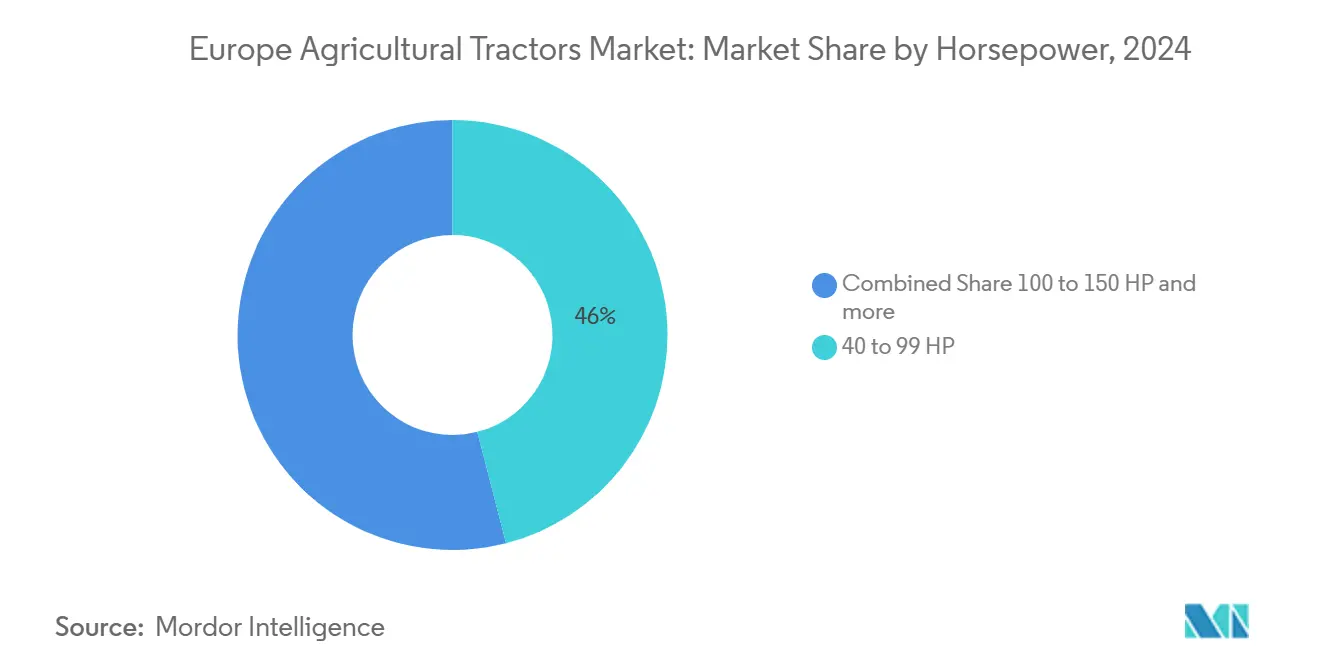

- By engine power, the 40-99 HP segment led with a 46.0% Europe agricultural tractor market share in 2024, the 100-150 HP class is forecast to grow at a 5.6% CAGR through 2030.

- By drive type, four-wheel drive tractors accounted for 64% of the Europe agricultural tractors machinery market share in 2024 and are expected to advance at a 6.2% CAGR from 2025 to 2030.

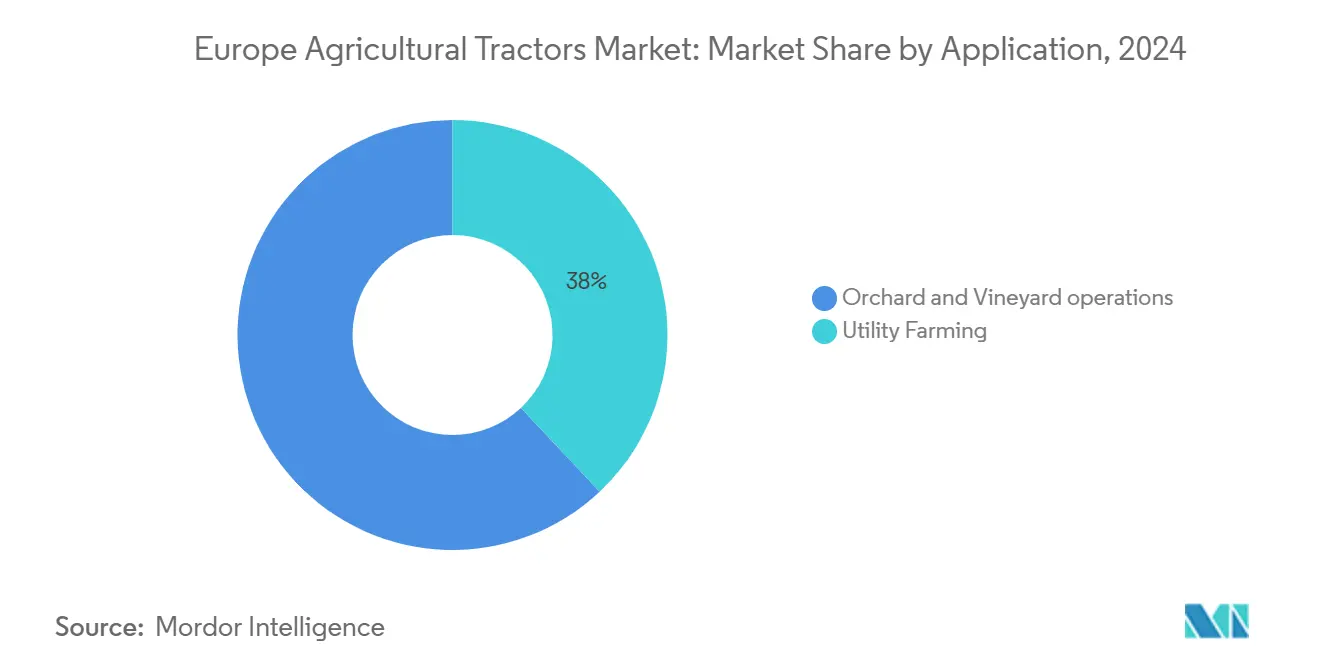

- By application, utility farming captured 38.0% of the Europe agricultural tractor market size in 2024, while specialty uses are projected to expand at a 7.5% CAGR.

- By geography, Germany held 19.5% of the Europe agricultural tractor market share in 2024, and Poland is poised for the fastest 6.4% CAGR through 2030.

Europe Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring farm-labor costs drive mechanization | +1.2% | Germany, the Netherlands, and France | Medium term (2-4 years) |

| European Union Common Agricultural Policy subsidies for tractor purchases | +0.8% | All European Union member states | Short term (≤ 2 years) |

| Precision-ag hardware integration (auto-guidance, ISOBUS) boosts replacement demand | +0.9% | Western and Eastern Europe | Medium term (2-4 years) |

| OEM (Original Equipment Manufacturer) financing schemes improve affordability for medium HP tractors | +0.6% | Germany, France, the United Kingdom, and the Netherlands | Short term (≤ 2 years) |

| Electrification roadmap under European Union Green Deal spurs R&D in battery-electric tractors | +0.5% | Germany, the Netherlands, and Denmark | Long term (≥ 4 years) |

| After-market autonomous retrofit kits unlock productivity for mid-size farms | +0.4% | Germany and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Farm-Labor Costs Drive Mechanization

Seasonal wages for field work nowadays exceed EUR 100 per day (USD 110), tightening operating budgets and forcing growers to mechanize routine tasks[1]Source: International Council on Clean Transportation, “European Stage V Standards,” theicct.org. Nearly 35% of European farmers are older than 65, limiting manual capacity and accelerating purchases of guidance-ready tractors that can operate longer shifts with fewer operators. Mid-range platforms benefit most because they pair maneuverability with enough power to cover additional hectares per hour. AGCO’s 2025 rollout of OutRun autonomous retrofit kits, for example, allows existing fleets to run unmanned during peak labor shortages, lowering per-acre labor costs and extending equipment life.

European Union Common Agricultural Policy Subsidies For Tractor Purchases

The 2021-2027 CAP allocates EUR 387 billion (USD 425.7 billion) for agriculture, with rural-development measures reimbursing up to 40% of new tractor costs. Planned reductions to EUR 300 billion (USD 330 billion) in the 2028-2034 cycle have prompted farmers to accelerate orders to secure current grant levels. Subsidy rules increasingly tie disbursements to Stage V compliance and precision-ag usage, effectively pulling advanced machines into the European tractor market ahead of normal replacement cycles. The policy's emphasis on environmental compliance increasingly links subsidy eligibility to Stage V emission standards and precision agriculture adoption, effectively mandating technology upgrades for continued financial support.

Precision-Ag Hardware Integration (Auto-Guidance, ISOBUS) Boosts Replacement Demand

ISOBUS has become the de facto plug-and-play standard, reducing integration hassles for mixed-brand implements [2]Source: AEF, “ISOBUS Overview,” aef-online.org. Tractor Implement Management systems nowadays automate downforce, seed spacing, and rate control, driving tangible yield gains that offset higher equipment costs within two seasons. High-speed ISOBUS trials promise real-time video and sensor streaming, which encourages growers to trade in older units lacking the bandwidth headroom for autonomous functions. As a result, the European tractor market gains a steady stream of tech-motivated replacements rather than relying solely on mechanical end-of-life triggers.

OEM (Original Equipment Manufacturer) Financing Schemes Improve Affordability For Medium HP Tractors

Elevated benchmark rates pushed conventional equipment loans past 9% in 2024. Captive finance arms responded with seasonal-payment leases and residual-value guarantees, making monthly costs predictable even in volatile commodity cycles[3]Source: CNH Industrial, “2023 Form 10-K,” cnh.com . Medium-horsepower models, which form the volume backbone of the European tractor market, see the greatest lift from these structures because purchase decisions hinge more on cash flow than on absolute price. These financing innovations also enable manufacturers to maintain production volumes during demand troughs by shifting inventory risk from dealers to captive finance arms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex versus volatile farm incomes | -1.8% | Italy, Spain, and Eastern Europe | Short term (≤ 2 years) |

| Component cost inflation and supply-chain volatility | -1.1% | All European Union member states | Medium term (2-4 years) |

| Stage V/VI emission rules raise engine complexity and cost | -0.7% | European Union-wide | Medium term (2-4 years) |

| Aging farmer demographics dampen long-term equipment demand | -0.5% | Germany, and Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex Versus Volatile Farm Incomes

Tractor list prices increased by 40%-60% in recent years due to raw material inflation and emission system upgrades. Farmers, facing uncertain crop returns, redirected funds to working capital needs, which increased the used equipment inventory by 40% in 2024. Small farm holdings, which represent a significant portion of the European tractor market, postponed new purchases or chose partial equipment refurbishments, reducing retail demand. The high capital requirements particularly affected smaller operations, where tractor purchases constitute a large portion of annual revenue, leading to farm consolidation or closure.

Component Cost Inflation and Supply-Chain Volatility

Global supply chain disruptions have elevated component costs across the agricultural machinery sector, with manufacturers reporting that logistics and production expenses significantly affect pricing structures throughout 2024. European OEMs (Original Equipment Manufacturers) import electronics and hydraulic castings from global suppliers, and freight delays and commodity swings introduced double-digit cost spikes throughout 2024. Tight semiconductor supply also pushed lead times for transmission controllers from eight to 26 weeks, causing production throttles that left dealers with inventory gaps. While most cost pressures pass through to end users, margins compress when price-sensitive growers resist new quotes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine power: Mid-Range Platforms Anchor a Versatile Fleet

The 40 to 99 HP segment commanded 46.0% market share in 2024, with this dominance reflecting European farm scale economics, where medium-sized operations require versatile tractors capable of diverse applications without excessive fuel consumption or operator complexity. The 100 to 150 HP category exhibits the fastest growth at 5.6% CAGR through 2030, driven by farm consolidation trends that favor higher-capacity equipment for expanded acreage coverage. AGCO’s Fendt 728 Vario became Germany’s top-registered tractor in 2024, illustrating the sweet spot of power and technology adoption. Precision-ag features such as variable-rate control and headland management are nowadays standard in this tier, bolstering productivity metrics that justify premiums even in tight financial cycles.

Smaller orchards and municipalities still rely on sub-40 HP units for maneuverability, but their growth trails the mid-range because specialty segments represent a niche share of arable land, above 150 HP, adoption clusters in large arable estates across Northern France and Central Germany, where high-drawbar tasks dominate. Rising total cost of ownership under Stage V rules tempers uptake, shielding the European tractor market from an outright shift toward very high horsepower machines.

By Drive Type: Four-Wheel Drive Extends Its Lead as Automation Spreads

Four-wheel drive platforms captured 64% of 2024 revenue within the Europe agricultural tractors machinery market size, reflecting their superior traction, higher hydraulic capacity, and compatibility with wide-working-width powered implements that dominate modern tillage and seeding operations. Adoption is heaviest on large arable estates in Germany, France, and the United Kingdom, where controlled-traffic farming protocols and Stage V emissions compliance favor tractors capable of delivering steady torque at lower engine speeds. The segment gains incremental lift from precision-agriculture subsidies that reward section-controlled planters, variable-rate sprayers, and other attachments that require four-wheel drive stability on slopes or under heavy loads. OEMs also pre-install ISO 11783 (ISOBUS) wiring harnesses and high-capacity alternators on four-wheel models, allowing growers to plug in sensor-laden implements without aftermarket upgrades.

Four-wheel drive tractors are projected to post a 6.2% CAGR through 2030, outpacing the broader market as electrification, autonomy, and high-speed planting technologies become mainstream. Battery-electric pilots now center on 60- to 120-kilowatt four-wheel platforms because the architecture distributes battery weight evenly across both axles, extending range and minimizing soil compaction. In Mediterranean vineyards and orchards, compact articulated four-wheel models maneuver more easily on terraced terrain, supporting the mechanization wave sweeping Italy, Spain, and Portugal. Two-wheel drive tractors, still favored on fragmented small holdings in Poland and Romania, will grow more slowly as these farms rely on contractor services or cooperative ownership for heavy fieldwork.

By Application: Utility Farming Drives Versatility Demand

Utility farming applications commanded 38.0% market share in 2024, reflecting European agriculture's diverse operational requirements that favor versatile tractors capable of multiple tasks over specialized equipment optimized for single applications. Utility farming's dominance also stems from European farm structure, where mixed operations require equipment flexibility rather than specialized optimization, explaining the continued preference for mid-range horsepower tractors with broad implement compatibility.

Specialty applications, including orchard and vineyard operations, demonstrate the fastest growth at 7.5% CAGR through 2030, driven by labor shortage pressures and precision agriculture adoption in high-value crop production. The application segmentation increasingly reflects technology integration patterns, with specialty crop producers leading electric tractor adoption due to noise restrictions in urban-adjacent operations and precise control requirements for delicate crop handling.

Geography Analysis

Germany anchors the European tractor market with a 19.5% share in 2024, although January 2025 registrations slid 19% year on year as growers delayed purchases amid commodity price softness. Strong domestic manufacturing, notably AGCO’s Marktoberdorf facility, supports local after-sales service and cements brand loyalty even during downturns. Fendt alone captured 25.2% of German registrations in 2024, highlighting the importance of localized product support and dealer density.

France ranks second in the market. The country benefits from diversified production of cereals in the north and specialty crops in the south, maintaining broad equipment demand. John Deere leads French registrations, supported by tailored CAP co-financing packages and an extensive parts network. Spain, while smaller, registered 8,763 new tractors in 2024, up 12.9% as modernization programs supported by regional funds offset drought-related yield risks.

Poland is the fastest-growing market with a projected 6.4% CAGR owing to European Union modernization grants and consolidation of fragmented farms. Medium-horsepower imports from Germany and Italy dominate early orders, but local assembly facilities are emerging to shorten lead times. Italy, confronting a 25% sales fall in Q1 2024, illustrates Southern Europe’s struggles with high capex and lower commodity margins. Farmers extend fleet life by retrofitting precision-spray booms rather than buying new units, slowing turnover.

Competitive Landscape

The European tractor market is moderately concentrated, with players including Deere and Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Claas KGaA mb. Product innovations, partnerships, and expansions are the prime strategies followed by these companies to increase their market share and improve their production capabilities using modern technologies. These companies are investing heavily in R&D and launching tractors that cater to the needs of farmers in this region. Kubota leverages compact-tractor strength for horticulture and municipal niches, while SDF exploits local presence in Italy and Germany to fill mid-power slots.

Rising R&D costs linked to Stage VI and electrification present barriers for smaller brands, fostering joint-technology ventures or supply agreements with battery specialists. Autonomous retrofit vendors represent an emergent threat, potentially decoupling brand loyalty from hardware and shifting value to software ecosystems. Technology deployment increasingly differentiates competitive positioning, with AGCO's OutRun autonomous retrofit kits launched in March 2025 to enable existing tractors from multiple manufacturers to operate unmanned, potentially disrupting traditional brand loyalty patterns.

The competitive landscape also reflects electrification race dynamics, where early market entry advantages accrue to manufacturers like Fendt with production-ready electric tractors, while laggards face technology catch-up costs and market share erosion. White-space opportunities emerge in precision agriculture integration, municipal applications, and autonomous operation capabilities, where traditional agricultural equipment manufacturers compete with technology companies entering from adjacent markets.

Europe Agricultural Tractor Industry Leaders

Deere and Company

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Claas KGaA mbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AGCO announced a EUR 87 million (USD 95.7 million) European Parts Distribution Centre in Amnéville, France. The facility enhances parts availability and delivery efficiency in the European tractor market, reducing equipment downtime for farmers and improving dealer service capabilities.

- June 2024: John Deere launched the 6M tractor series in Europe, offering models ranging from the compact 6M 95 to the powerful 6M 250. These tractors come with 4.5 or 6.8-liter engines, delivering up to 20 additional horsepower with intelligent power management (IPM).

- December 2023: The CNH Design team enhanced agricultural equipment through innovative design approaches. The German Design Council recognized these efforts by awarding the STEYR brand's Plus tractor series the 2024 German Design Award for Excellent Product Design in the Utility Vehicles category. The award acknowledged the tractor's integration of functionality, design, quality, and sustainability features.

Europe Agricultural Tractor Market Report Scope

| Less Than 40 HP |

| 40 to 99 HP |

| 100 to 150 HP |

| 151 to 200 HP |

| Above 200 HP |

| Two-Wheel Drive (2WD) |

| Four-Wheel Drive (4WD) |

| Utility Farming |

| Orchard and Vineyard operations |

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Russia |

| Poland |

| Rest of Europe |

| By Engine power | Less Than 40 HP |

| 40 to 99 HP | |

| 100 to 150 HP | |

| 151 to 200 HP | |

| Above 200 HP | |

| By Drive Type | Two-Wheel Drive (2WD) |

| Four-Wheel Drive (4WD) | |

| By Application | Utility Farming |

| Orchard and Vineyard operations | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe tractor market?

The Europe tractor market size stands at USD 26.5 billion in 2025.

Which horsepower range sells the most units in Europe?

Tractors rated 40-99 HP account for 46.0% of 2024 sales, reflecting medium-farm requirements.

Why are German farmers delaying new-tractor purchases in 2025?

Softer commodity prices and higher equipment prices pushed January 2025 registrations down.

Which country is the fastest-growing market for tractors in Europe?

Poland is forecast to expand at a 6.4% CAGR through 2030.

Page last updated on: