ERP Vendor Ecosystem And Marketplace Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.68 Billion |

| Market Size (2031) | USD 26.93 Billion |

| Growth Rate (2026 - 2031) | 16.26% CAGR |

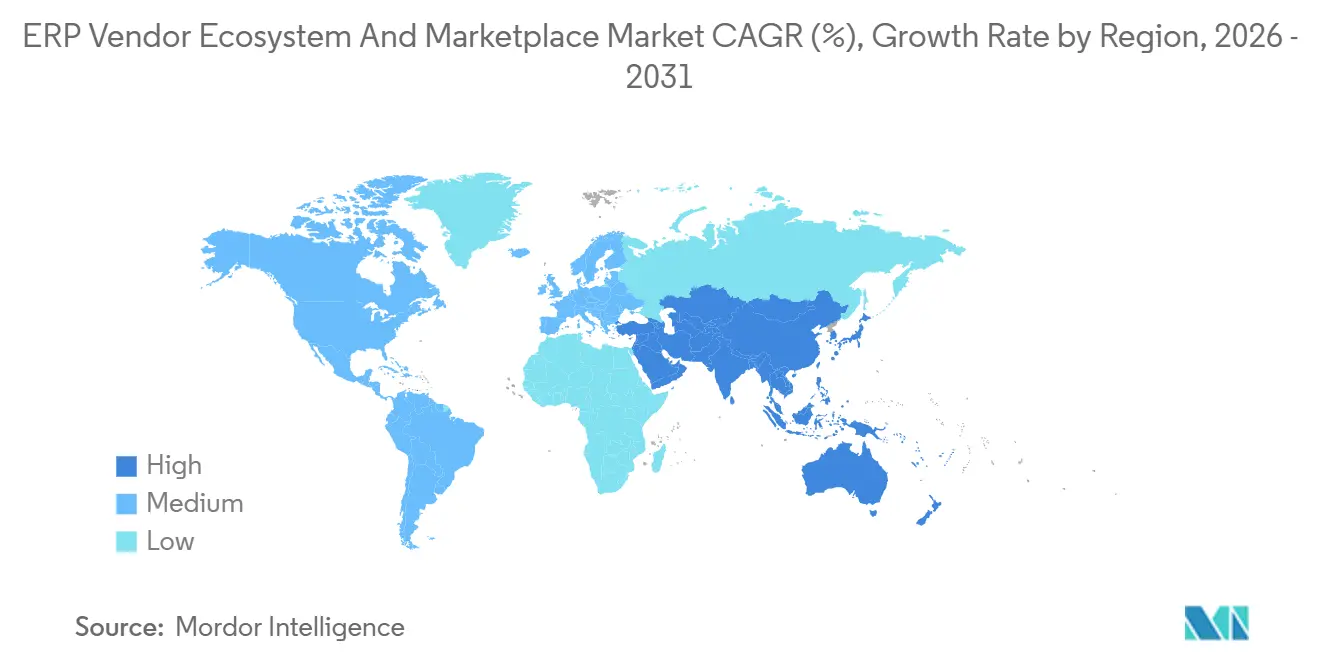

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ERP Vendor Ecosystem And Marketplace Market Analysis by Mordor Intelligence

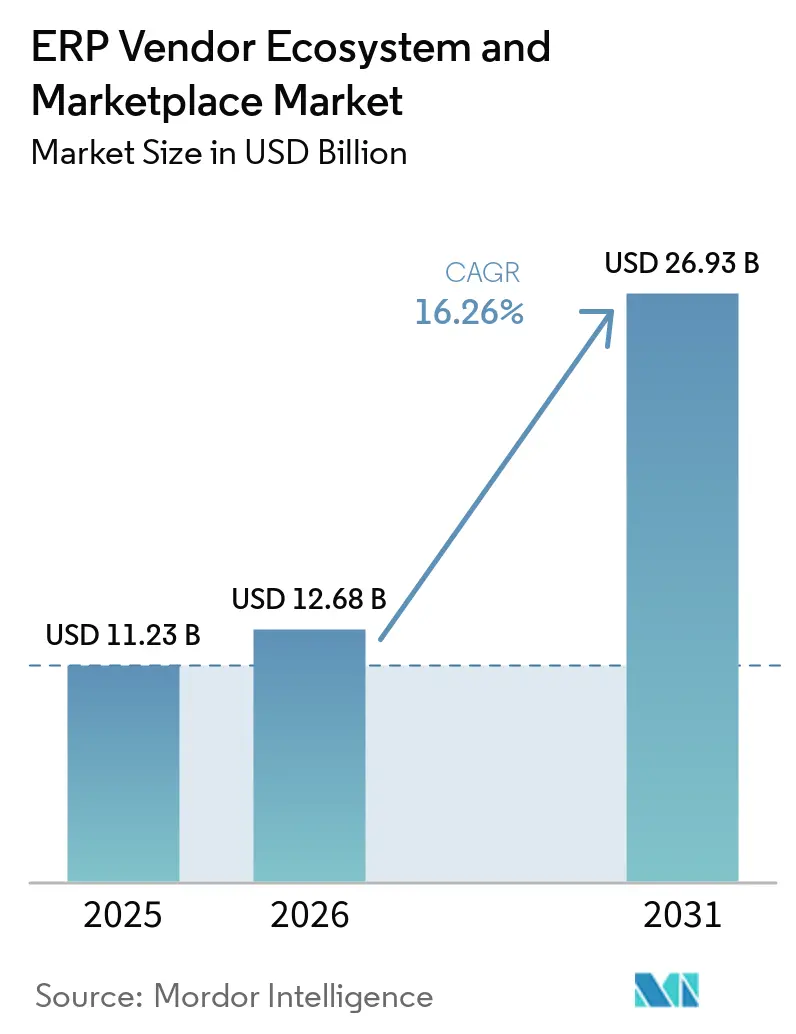

The ERP vendor ecosystem and marketplace market size is projected to be USD 11.23 billion in 2025, USD 12.68 billion in 2026, and reach USD 26.93 billion by 2031, growing at a CAGR of 16.26% from 2026 to 2031. Three structural shifts are accelerating expansion: the sunset of SAP ECC is forcing 18,000 licensees to re-platform, generative AI agents are automating finance and procurement workflows, and two-tier strategies let multinationals pair a headquarters suite with lighter systems at subsidiaries. Cloud adoption, already mainstream, is deepening through hybrid rollouts that keep sensitive ledgers on-premises while streaming analytics to public clouds. Simultaneously, consumption-based pricing and vertical templates are eroding the historical USD 500,000 implementation floor, widening the funnel for small and medium enterprises.

Key Report Takeaways

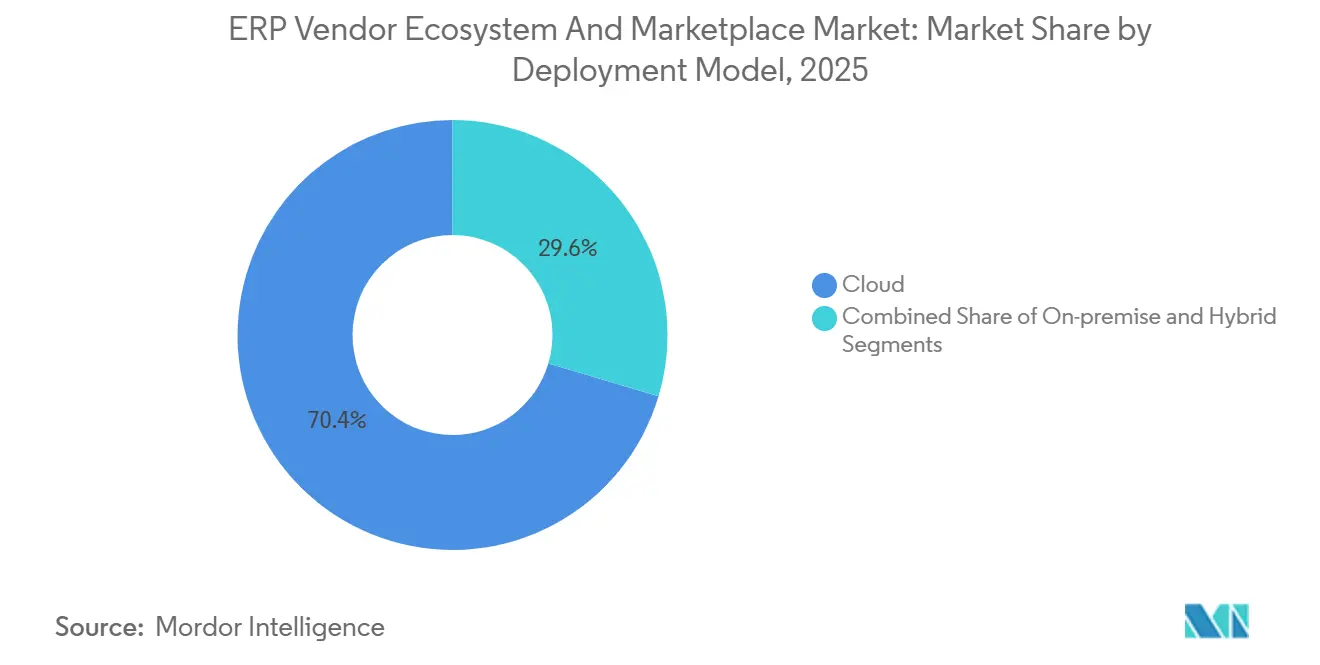

- By deployment model, cloud held 70.40% of the ERP vendor ecosystem and marketplace market share in 2025, whereas hybrid configurations are forecast to expand at a 19.90% CAGR through 2031.

- By organization size, large enterprises captured 62% of the ERP vendor ecosystem and marketplace market size in 2025, and small and medium enterprises are projected to grow at a 21.20% CAGR to 2031.

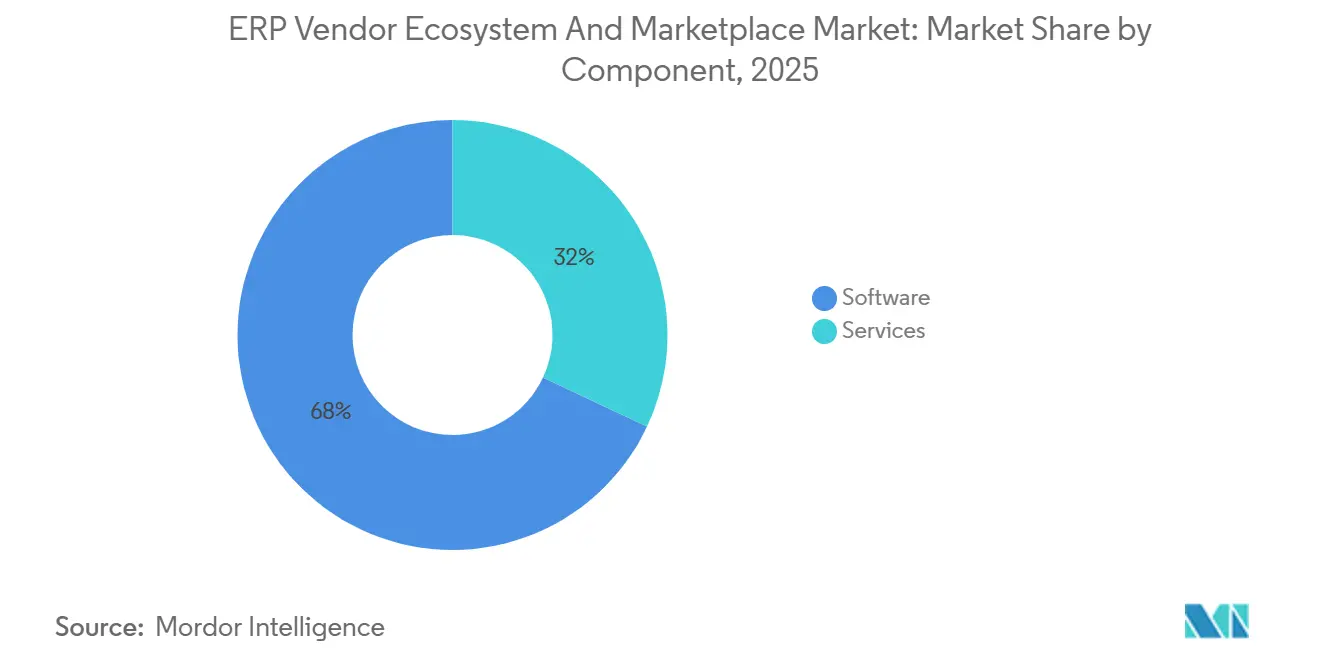

- By component, software modules accounted for 68% of spending in 2025, yet services revenue is growing faster at a 13.50% CAGR through 2031.

- By industry vertical, manufacturing led with 32% of ERP vendor ecosystem and marketplace market share in 2025, while healthcare and life sciences is advancing at a 12.60% CAGR to 2031.

- By geography, North America accounted for 37% of revenue in 2025, and Asia-Pacific is forecast to register the fastest regional CAGR at 14.00% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ERP Vendor Ecosystem And Marketplace Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SAP ECC 2027 End-of-Support Driving Replacement Cycles | +4.2% | Global, peaking in Europe and North America | Short term (≤ 2 years) |

| Adoption of AI-Embedded ERP Suites | +3.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Accelerating Cloud Adoption Among Enterprises | +3.1% | Global, fastest in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Demand for Integrated Supply-Chain Visibility | +2.5% | Global, focused on manufacturing hubs | Medium term (2-4 years) |

| Regulatory Mandates for Real-Time Financial Reporting | +1.9% | Europe, United States, emerging Asia-Pacific | Long term (≥ 4 years) |

| Two-Tier ERP Strategies Fueling Niche Vendor Growth | +1.5% | Multinationals with subsidiaries in South America and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SAP ECC 2027 End-of-Support Driving Replacement Cycles

SAP’s December 2027 support cutoff for ECC 6.0 is compressing a decade of migration activity into the next 24 months, creating a surge of license churn that benefits both SAP S/4HANA Cloud and rival suites. Implementation partners grew their certified headcount by double digits in 2025, yet vacancy rates above 20% are inflating day-rates for experienced consultants, pushing enterprises toward low-code migration kits distributed through vendor marketplaces.[1]SAP Newsroom, “SAP S/4HANA Cloud Public Edition 2411 Innovations,” sap.com Oracle and Workday exploited the fatigue by offering time-limited discounts and fee waivers, luring defectors that prefer greenfield deployments over brownfield conversions. [2]Oracle Corporation, “Oracle Launches AI Agents for Fusion Cloud Applications,” oracle.com

Adoption of AI-Embedded ERP Suites

Generative AI is recasting ERP from a passive system of record into an autonomous decision cockpit. Oracle’s AI Agent Marketplace ships bots that reconcile invoices and predict demand, trimming finance closings from 10 days to 3 days in early pilots. Microsoft Copilot for Dynamics 365 uses natural-language prompts to automatically post journals, reducing month-end labor hours by 30%. [3]Microsoft Corporation, “New Agents in Microsoft 365 Unlock Business Value,” microsoft.com SAP’s Joule assistant lets buyers renegotiate contract terms in chat rather than e-mail threads, catalyzing a new ecosystem of prompt-engineering consultancies. Growing API traffic between ERP cores and data lakes is stressing legacy middleware, accelerating uptake of event-driven integration platforms.

Accelerating Cloud Adoption Among Enterprises

A significant percentage of ERP workloads now operate in public or private clouds, and this percentage continues to grow. The primary appeal of cloud delivery lies in its capability to convert capital expenditures into manageable operating expenses. Additionally, integrated marketplaces within these platforms simplify the process of acquiring extensions. Currently, several enterprises utilize at least one cloud-based business application. Furthermore, several of these enterprises rely on services from two or more hyperscalers. This ongoing trend requires ERP vendors to develop expertise in cross-cloud data replication and to implement unified identity governance systems. The cost-saving potential of cloud ERP is significant: it reduces upfront hardware and software expenses by 60%, thereby enabling organizations to allocate resources toward analytics initiatives and AI pilot projects. [4]Financial Times Staff, “Cloud ERP Migration Trends,” ft.com

Demand for Integrated Supply-Chain Visibility

Disruptions from 2020 to 2023 exposed blind spots in siloed ERP stacks. Modern suites embed control towers that stream IoT telemetry and logistics manifests into a single ledger, letting planners reroute shipments or swap suppliers in real time. Oracle added blockchain-provenance tracking for 40,000 automotive components, while SAP pre-wired logistics networks, such as project44, into Integrated Business Planning, lowering stockouts by one-quarter in consumer-goods pilots. Logistics giants like DHL now bundle ERP subscriptions with freight contracts, signaling a convergence of software and physical supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Costs and Budget Overruns | -2.8% | Global, most acute among firms with 100-1,000 employees | Short term (≤ 2 years) |

| Data Security and Privacy Concerns in Cloud ERP | -2.1% | Europe (GDPR) and Asia-Pacific (China Cybersecurity Law) | Medium term (2-4 years) |

| Shortage of ERP-Qualified Implementation Talent | -1.6% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Interoperability Challenges in Composable Architectures | -1.3% | Early adopters of multi-vendor stacks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs and Budget Overruns

Total cost of ownership for a 500-employee manufacturer moving to SAP S/4HANA Cloud averages USD 2.8 million over five years, and deployments still overshoot budgets by up to 50% when data cleansing and change management are underestimated. In response, vendors rolled out fixed-price quick-start bundles that cap customization requests, lowering the barrier to entry yet compressing partner margins. Smaller consultancies are merging to achieve scale, and self-service migration tools are proliferating inside marketplaces to limit human billable hours.

Data Security and Privacy Concerns in Cloud ERP

Multi-tenant designs remain suspect in jurisdictions with strict data-sovereignty rules. The GDPR fines enterprises up to 4% of global revenue for improper transfers, prompting SAP to maintain 14 regional data centers in Europe, while China’s Cybersecurity Law confines ledgers to domestic hyperscalers, raising hosting costs by one-quarter. Local champions such as TOTVS and Ramco capitalize on the anxiety by offering single-tenant national-cloud options at higher per-user fees, slowing multinational rollouts that rely on global templates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Configurations Outpace Pure Cloud

Hybrid architectures held 9% of 2025 spending but are expanding at a 19.90% CAGR, the fastest among deployment models. Enterprises anchor transaction databases on-premises for latency or regulatory reasons and shuttle analytics and collaboration modules to hyperscalers, achieving a near 40% cost relief compared with pure on-premises landscapes. Vendors are pivoting: SAP’s RISE service now orchestrates mixed topologies for 35% of S/4HANA clients, Oracle Cloud at Customer packages public-cloud software in an on-site appliance, and Azure Stack extends Dynamics 365 to edge factories, responses that deepen the ERP vendor ecosystem market penetration in regulated industries.

The ERP vendor ecosystem and marketplace market size advantage remains with cloud at 70.40% in 2025, yet momentum is firmly with hybrid. Marketplace sales skew heavier in hybrid estates; customers average 4.1 add-ons compared with 3.2 for pure cloud, because integration accelerators are required to bridge on-prem and cloud services.

By Organization Size: Mid-Market Disruption Accelerates

Large organizations accounted for 62% of 2025 revenue, but the small and medium cohort is expanding at a 21.20% CAGR, nearly double the headline rate. Consumption-based pricing now lets a USD 50 million manufacturer roll out a financial core for under USD 100,000 in year one, eroding the historical barrier. Two-tier strategies intensify the shift: conglomerates keep SAP or Oracle at headquarters but provision Odoo or Acumatica at plants in Southeast Asia, reducing per-site fees by 60% and lifting ERP vendor ecosystem and marketplace market share for mid-market specialists.

The ERP vendor ecosystem and marketplace market-size tailwind for small and medium enterprises stems from modularity. Odoo ships 40 vertical packs that deploy in four weeks, and Rootstock leverages Salesforce-native objects to unite CRM and ERP without custom connectors. Large-enterprise renewals are slowing, but they remain the profit core: average contract value still tops USD 5 million, cushioning incumbents while they court smaller logos.

By Component: Services Margin Expansion Reshapes Economics

Software modules retained 68% of revenue in 2025, yet services billings are increasing faster at 13.50% CAGR because composable stacks demand perpetual integration. Enterprises spend 40% of total ownership on post-go-live custom work, up from 25% under monolithic on-prem models. Deloitte and Accenture bundle licenses, hosting, and 24/7 support into managed-service subscriptions that carry 35% gross margins, double the old time-and-materials benchmark. Independent vendors monetize connector packs through marketplaces. SAP Store payouts climbed 40% to USD 1.2 billion in 2025, cementing services as the revenue engine of the ERP vendor ecosystem industry.

Marketplace economics also pressure software pricing: Oracle and SAP introduced transaction-based tiers that meter API calls, smoothing entry for new adopters but reducing predictability of renewals. The ERP vendor ecosystem's software market share is therefore expected to tick down by 2 points by 2031, even as absolute software dollars rise.

By Industry Vertical: Healthcare Disrupts Manufacturing Dominance

Manufacturing-led spending with 32% in 2025, buoyed by Industry 4.0 projects that mesh CNC telemetry with work-order costing. Yet healthcare and life sciences, helped by interoperability rules in the 21st Century Cures Act, are on a 12.60% CAGR glide path, narrowing the gap. Banks modernize core ledgers to support instant payments, and retailers overlay omnichannel stock visibility by adding ERP modules that reconcile e-commerce orders every 15 minutes.

The ERP vendor ecosystem and marketplace market size for healthcare rose sharply after cloud vendors certified HIPAA-compliant regional data centers, and best-of-breed EHR connectors in marketplaces halved integration timelines. Manufacturing remains resilient; the sector consumes 50% of new hybrid ERP nodes, but its share will drift lower as regulated service industries digitize.

Geography Analysis

North America accounted for 37% of 2025 revenue, thanks to its dense partner network and rapid cloud adoption. The United States construction labor crunch is spurring adoption of mobile ERP modules that clock worker hours and materials on site, cutting back-office headcount 30%. Canada’s 796 SAP-certified firms, many of which are bilingual in Quebec, support localized rollouts that comply with dual-jurisdiction tax codes. Mexico’s nearshoring wave is driving demand for multi-currency consolidation between maquiladora subsidiaries and their U.S. parents.

Asia-Pacific is the fastest climber at 14.00% CAGR. Digital India forces 120,000 suppliers onto cloud ERP by 2027, and China’s substitution drive toward Kingdee and Yonyou re-shapes the vendor mix even while multinationals cling to SAP global templates. Japanese mid-market manufacturers are now migrating ECC to the cloud to cut maintenance payroll by 40%. Indonesia, Vietnam, and Thailand together account for 18% CAGR as e-commerce giants spur demand for real-time inventory.

Europe contributes 28% of revenue. The European Single Electronic Format requirement, effective September 2026, obliges 12,000 listed firms to embed XBRL tags, prompting upgrades to reporting modules. Germany’s Mittelstand runs two-tier deployments, and France is migrating from AS/400 legacies under ECC support deadlines. In South America, TOTVS dominates the mid-market through localized tax engines, while Vision 2030 public projects galvanize demand in the Middle East. Africa remains nascent, yet records lift from mobile-first public-sector tenders.

Competitive Landscape

While SAP, Oracle, and Microsoft continue to dominate the revenue landscape, their once-unassailable grip is gradually weakening. The increasing adoption of two-tier ERP strategies and composable architectures is creating opportunities for emerging competitors to challenge the incumbents. Oracle, capitalizing on its innovative offerings such as Copilot and AI agents, achieved an impressive 21% year-on-year growth in its cloud ERP segment for fiscal 2025. Meanwhile, Odoo and ERPNext are disrupting the mid-market by offering competitively priced solutions at USD 20 per user per month, effectively capturing significant market attention and undercutting established players.

IFS is strategically focusing on the aerospace and defense sectors, while Epicor is strengthening its presence in the automotive and distribution industries. The market is witnessing a shift in priorities, with API ecosystems gaining more importance over traditional functional breadth. Workday, recognizing this trend, has partnered with Boomi to deliver 200 pre-built connectors, enhancing integration capabilities. At the same time, Rootstock is promoting its Salesforce-native manufacturing suites, emphasizing their hybrid cloud functionalities to meet evolving customer needs.

New opportunities are emerging in specialized micro-verticals, including construction job costing, restaurant franchise management, and hybrid-cloud orchestration for regulated data. Additionally, there is a growing demand for API-first approaches to assemble best-of-breed technology stacks. Open-source disruptors are redefining their business models by focusing on monetizing hosting services rather than traditional licensing. Furthermore, established vertical SaaS providers, such as Procore, are expanding their offerings by integrating ERP solutions into their workflow platforms, leveraging their existing customer bases to drive growth and enhance value propositions.

ERP Vendor Ecosystem And Marketplace Industry Leaders

Oracle Corporation

SAP SE

Microsoft Corporation

Workday, Inc.

Sage Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Oracle launched its AI Agent Marketplace with autonomous agents for procurement, accounts payable, and demand planning, recording 70% faster invoice cycles and 30% better forecast accuracy.

- January 2026: SAP released S/4HANA Cloud Public Edition 2411 with embedded Joule AI, 120 new APIs, and enhanced multi-currency consolidation.

- December 2025: Microsoft made Copilot for Dynamics 365 Finance and Supply Chain Management generally available, hitting 40% customer adoption in one quarter.

- November 2025: Workday and Boomi unveiled 200 connectors that cut integration labor by half for composable architectures.

Global ERP Vendor Ecosystem And Marketplace Market Report Scope

The ERP Vendor Ecosystem and Marketplace refers to the ecosystem of enterprise software providers, third-party developers, system integrators, and service providers that collectively support, extend, and commercialize Enterprise Resource Planning (ERP) platforms through integrated marketplaces and partner networks.

The ERP Vendor Ecosystem and Marketplace Report is Segmented by Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises and SMEs), Component (Software and Services), Industry Vertical (Manufacturing, Retail and E-Commerce, and Other Industry Verticals), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Software Modules |

| Services |

| Manufacturing |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Banking, Financial Services and Insurance |

| Professional Services |

| Public Sector |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Component | Software Modules | |

| Services | ||

| By Industry Vertical | Manufacturing | |

| Retail and E-commerce | ||

| Healthcare and Life Sciences | ||

| Banking, Financial Services and Insurance | ||

| Professional Services | ||

| Public Sector | ||

| Other Industry Verticals | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the ERP vendor ecosystem market be by 2031?

It is projected to reach USD 26.93 billion by 2031, expanding at a 16.26% CAGR from 2026 to 2031.

What segment is growing fastest within ERP deployment models?

Hybrid configurations are forecast to rise at a 19.90% CAGR as firms blend on-premises control with cloud analytics.

Which region delivers the strongest growth through 2031?

Asia-Pacific is set to post the highest regional CAGR at 14.00%, propelled by government mandates and new industrial capacity.

Why are small and medium enterprises adopting ERP more rapidly now?

Consumption-based pricing, vertical templates, and lower implementation floors allow firms with under USD 50 million revenue to deploy modern suites economically.

How is generative AI changing ERP operations?

AI agents automate tasks like invoice matching, journal entry creation, and demand forecasting, cutting cycle times by up to 70% and freeing staff for analytical work.

What restrains ERP cloud migration in Europe and Asia-Pacific?

Strict data-sovereignty laws such as GDPR and the China Cybersecurity Law oblige vendors to run localized clouds, elevating cost and deployment complexity.

Page last updated on: