ERP Security And Compliance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

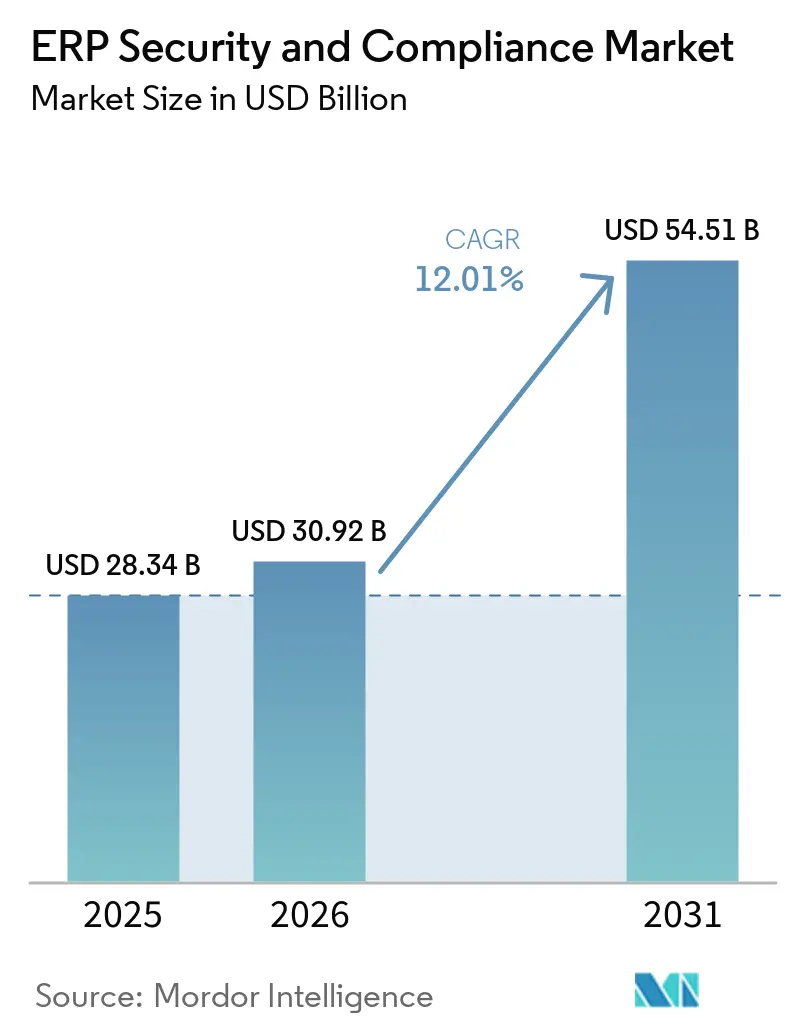

| Market Size (2026) | USD 30.92 Billion |

| Market Size (2031) | USD 54.51 Billion |

| Growth Rate (2026 - 2031) | 12.01% CAGR |

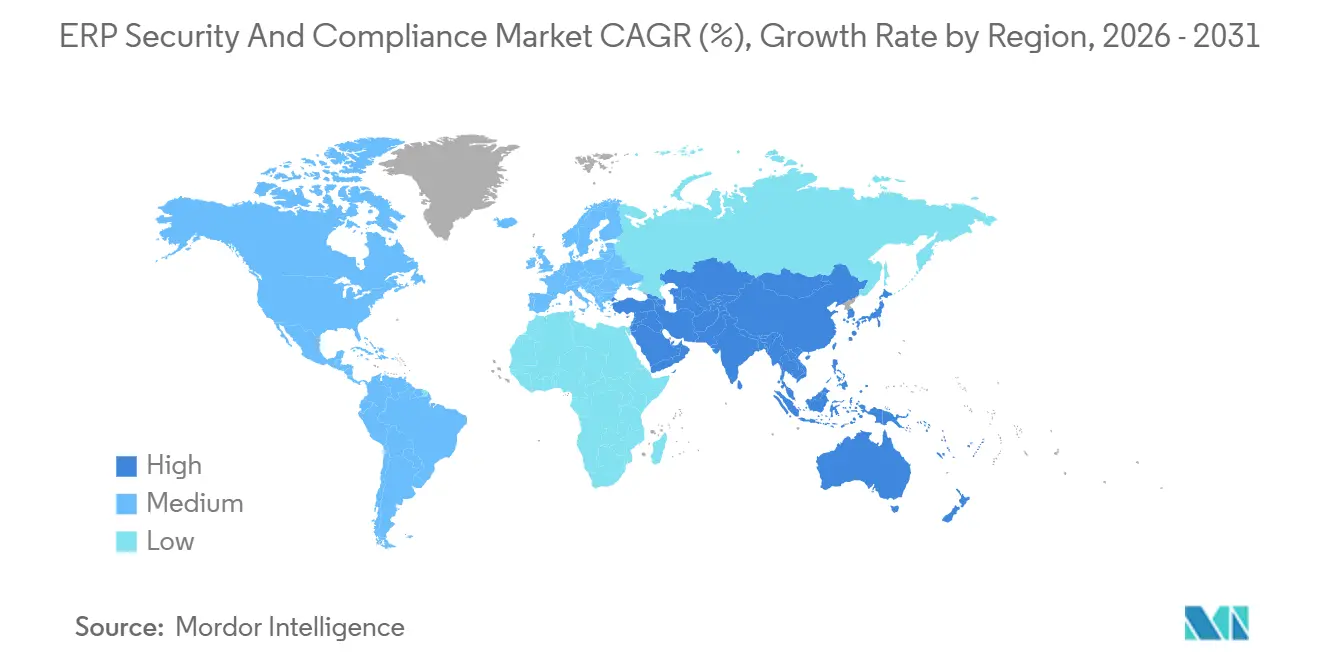

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ERP Security And Compliance Market Analysis by Mordor Intelligence

The ERP security and compliance market size is projected to expand from USD 28.34 billion in 2025 and USD 30.92 billion in 2026 to USD 54.51 billion by 2031, registering a CAGR of 12.01% between 2026 and 2031. Heightened board-level scrutiny of cyber risk, a 32% surge in identity-based attacks in 2025, and the rapid lift-and-shift of core ERP workloads into software-as-a-service environments are reshaping investment priorities. Organizations are pivoting from periodic point-in-time audits to continuous controls monitoring that blends behavioral analytics, segregation-of-duties (SoD) rules, and automated remediation. Competitive advantage now hinges on embedding artificial-intelligence detection inside live financial processes without triggering costly re-implementations of SAP, Oracle, or Microsoft instances. Service-led value creation is accelerating in parallel, as overstretched security teams outsource configuration, rule-set tuning, and 24/7 monitoring to managed security providers. The ERP security and compliance market continues to evolve as regulatory bodies tighten breach notification timelines, auditors demand real-time evidence, and threat actors target hybrid multi-cloud estates that blur traditional perimeter lines.

Key Report Takeaways

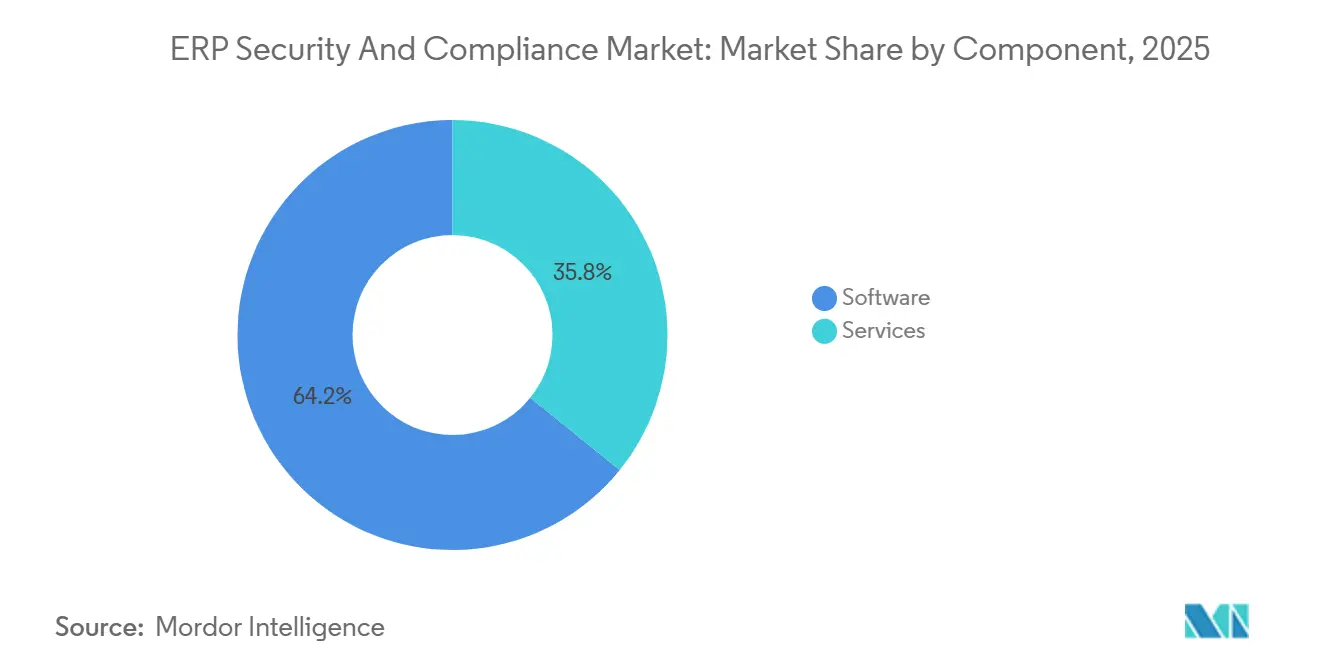

- By component, software led with 64.20% revenue share in 2025, while services are advancing at a 16.80% CAGR through 2031.

- By deployment mode, cloud captured 58.50% of the ERP security and compliance market share in 2025 and is expanding at a 18.30% CAGR through 2031.

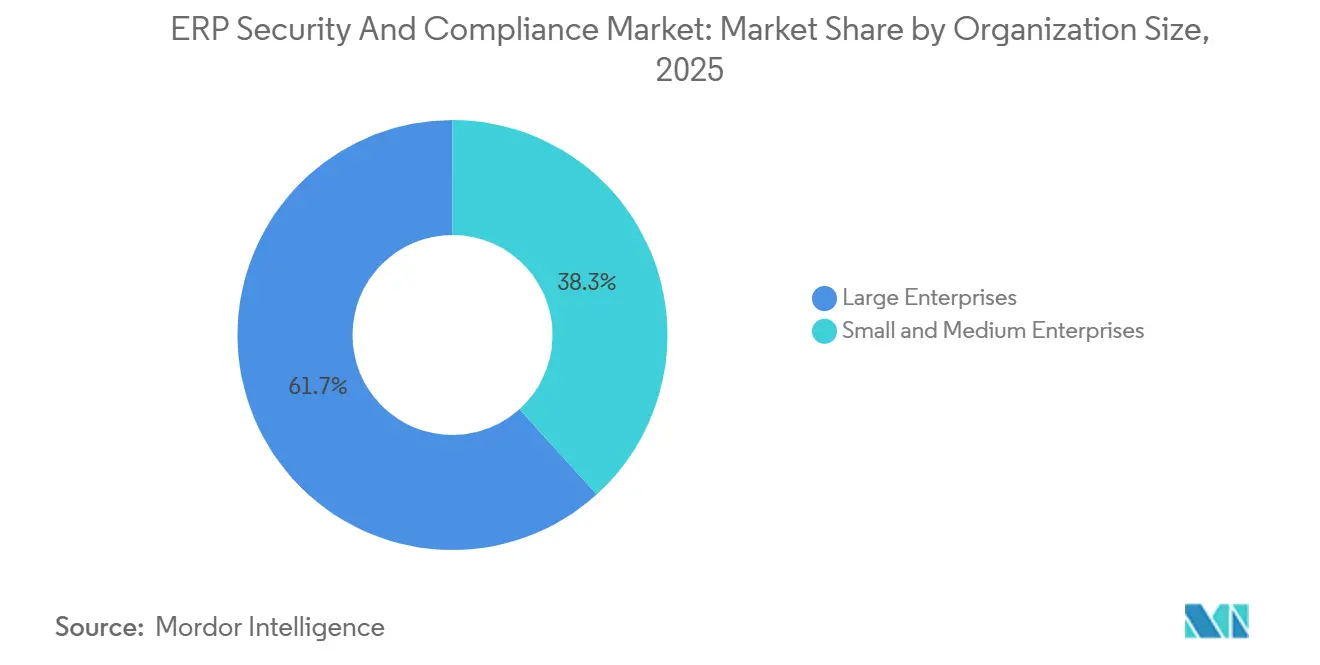

- By organization size, large enterprises held 61.70% of the ERP security and compliance market in 2025, whereas small and medium enterprises are growing at a 17.90% CAGR through 2031.

- By end-use industry, manufacturing accounted for 22.40% of 2025 revenue, while healthcare is forecast to grow at a 19.40% CAGR through 2031.

- By geography, North America retained 34.10% share in 2025; Asia-Pacific is poised to register the fastest 17.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ERP Security And Compliance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Cloud-Based ERP Deployments | +3.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Escalating Regulatory Compliance Requirements Across Industries | +2.8% | Global, high in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rising Incidence of Insider Threats and Data Breaches in ERP Environments | +2.5% | Global | Short term (≤ 2 years) |

| Growing Need for Centralized SoD Management in Multi-ERP Landscapes | +2.0% | North America, Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Integration of AI-Driven Behavioral Analytics for Real-Time Risk Scoring | +1.5% | North America and Europe, early uptake in Asia-Pacific | Medium term (2-4 years) |

| Demand for Continuous Controls Monitoring Tied to ESG Assurance | +1.2% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Cloud-Based ERP Deployments

Three out of four enterprises ran at least one cloud ERP instance in 2025, but the shared-responsibility model blurs accountability between vendor and customer for access governance. Multi-tenant architectures expose application programming interfaces that adversaries weaponize, while voice-phishing accounted for 23% of cloud compromises in 2025.[1]Mandiant, “M-Trends 2026,” MANDIANT.COM The U.S. Securities and Exchange Commission now compels public companies to disclose material cyber incidents within four business days, forcing boards to scrutinize ERP role design and SoD hygiene. Continuous monitoring that ingests user-behavior telemetry and flags privilege escalations in real time is emerging as a board-level requirement. Vendors that automate the mapping of roles to business-process risk scenarios gain purchase precedence because they cut audit preparation from weeks to hours.

Escalating Regulatory Compliance Requirements Across Industries

PCI DSS v4.0 became compulsory in March 2025, adding 64 new requirements that strengthen authentication and require quarterly penetration testing in ERP-linked cardholder environments.[2]PCI Security Standards Council, “PCI DSS Version 4.0,” PCISECURITYSTANDARDS.ORG Europe’s Corporate Sustainability Reporting Directive extends oversight to non-financial data, obliging finance teams to reconcile ESG metrics with general ledger entries. Banks' face Basel III operational resilience proofs that map critical business services to ERP modules, creating steady demand for automated evidence generation. Auditors in North America are increasingly rejecting manual SoD attestations and moving toward continuous digital substantiation. Together, the multifaceted mandates ensure sustained purchasing momentum for the ERP security and compliance market as firms seek to unify controls across financial and sustainability disclosures.

Rising Incidence of Insider Threats and Data Breaches

Average insider threat costs reached USD 17.4 million per incident in 2025.[3]Ponemon Institute, “Cost of Insider Threats Report 2025,” PONEMON.ORG The Cl0p ransomware group exploited the Oracle E-Business zero-day CVE-2025-61882 to siphon procurement data before encryption. The median dwell time was 14 days, allowing attackers to disable logs and manipulate financial data. Only 52% of intrusions were caught internally, underscoring detection gaps and elevating demand for AI-driven user-behavior analytics. Manufacturing enterprises, which rely on ERP systems to orchestrate production schedules and supplier payments, saw a 40% year-over-year spike in targeted attacks, cementing the business case for proactive risk scoring embedded in the ERP transaction layer.

Growing Need for Centralized SoD Management

Aggregated entitlements often breach SoD policies even when each platform appears compliant in isolation. Oracle Access Governance applies machine learning to recommend least-privilege roles and flag toxic role combinations, pushing the market toward policy orchestration layered on top of heterogeneous ERP stacks.[4]Oracle, “Access Governance,” ORACLE.COM Enterprises that consolidate SoD oversight report 30% fewer audit findings and 25% faster financial close cycles, underscoring tangible return on investment for unified entitlement management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Integration and Implementation Costs | -2.1% | Global, heavy on SMEs | Short term (≤ 2 years) |

| Shortage of Skilled ERP Security Professionals | -1.8% | Global, acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Overlapping IGA and PAM Toolsets Creating Purchase Decision Paralysis | -1.0% | North America and Europe | Short term (≤ 2 years) |

| Vendor Consolidation Limiting Best-of-Breed Options for Niche Compliance Needs | -0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration of AI-Driven Behavioral Analytics

AI-based anomaly engines now parse millions of ERP transactions per hour, correlating unusual posting times, location anomalies, and peer-group deviations to generate real-time risk scores. Early adopters in North America and Europe cite a 60% reduction in false-positive alerts relative to rule-centric systems, freeing analysts to investigate high-fidelity threats. Onapsis’s Agentic Gateway showcases large-language-model summarization that turns forensic signals into plain-English incident narratives, enabling finance and audit staff to validate alerts without cybersecurity jargon. AI explainability is also moving up the regulatory agenda, with European watchdogs exploring guidance that requires clear audit trails for machine-generated access decisions, further boosting investment in transparent behavioral engines.

Demand for Continuous Controls Monitoring Linked to ESG Assurance

Investors and regulators alike expect verifiable ESG statements that roll into financial filings. Continuous controls monitoring aligns sustainability data such as scope-3 emissions or supplier diversity metrics with core ERP ledgers. Europe leads maturity after the Corporate Sustainability Reporting Directive, yet North American firms are fast followers as the Securities and Exchange Commission weighs climate-disclosure obligations. Automated reconciliation of environmental, social, and governance data streams with financial closings reduces manual spreadsheet use and accelerates quarterly reporting, positioning continuous monitoring as a dual compliance and efficiency lever.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Software in Growth Velocity

Software dominated the ERP security and compliance market in 2025, yet the narrative is shifting. Enterprises have already purchased core SoD engines and continuous controls dashboards; now they crave the expertise to operationalize them. Services revenue, consulting, implementation, and managed detection, grows at 16.80% CAGR, reflecting this pivot. Advisory engagements increasingly incorporate business-process reengineering to ensure SoD enforcement aligns with ISO 27001:2022 risk-based principles, while managed-service subscriptions bundle 24/7 alert triage and quarterly access attestations.

Software vendors, meanwhile, race to lower the total cost of ownership through low-code API orchestration. Pathlock’s August 2025 link-up with Microsoft Sentinel demonstrates how ERP-centric anomalies can feed directly into existing security operations workflows, eliminating the need for separate SIEM dashboards. Over the forecast horizon, platform vendors will embed AI-assisted configuration that guides customers through context-aware role definitions, further closing the skills gap and sustaining software renewal momentum inside the ERP security and compliance market.

By Deployment Mode: Cloud Dominates Share and Velocity

Cloud deployments accounted for 58.50% of 2025 revenue and continue to outpace alternatives as financial-management, supply-chain, and human-capital-management suites migrate to Oracle Fusion Cloud, SAP S/4HANA Cloud, and Microsoft Dynamics 365. The ERP security and compliance market size tied to cloud instances is forecast to increase at an 18.30% CAGR through 2031 as SaaS ERP becomes the default choice for greenfield installations. FedRAMP’s 325-control moderate baseline serves as a benchmark well beyond U.S. federal agencies, prompting private enterprises to insist on equivalent coverage. Continuous API log ingestion, serverless agents, and in-memory analytics deliver minute-level anomaly detection, collapsing mean-time-to-detect from days to minutes.

On-premises estates persist in the defense and critical infrastructure sectors, where data sovereignty rules and air-gapped networks require local hosting. Maintenance costs escalate as vendors funnel research and development toward cloud-native feature sets. Hybrid deployments, which splice on-premise financial modules with cloud-based talent systems, introduce cross-identity complexities that force security teams to manage entitlements across at least two directories. Unified dashboards that consolidate risk postures across modes are now table stakes in request-for-proposal scoring.

By Organization Size: SMEs Accelerate Adoption Despite Resource Constraints

Large enterprises accounted for 61.70% of 2025 spending because their multi-instance landscapes and global audit exposure demand advanced controls. However, the small and medium enterprise segment is the fastest-growing slice of the ERP security and compliance market, with 17.90% CAGR projected through 2031. Cloud pricing tiers reduce upfront hardware costs and align expenses with user counts, but subscription fatigue looms when identity governance, privileged-access management, and ERP security modules each require separate contracts.

Vendors respond by bundling core and advanced features, introducing guided setup wizards, and offering managed service overlays that offload 24/7 monitoring. SMEs thus gain enterprise-grade protection without staffing a security operations center, fueling expansion into mid-market niches.

By End-Use Industry: Healthcare Surges on Regulatory Tailwinds

Manufacturing accounted for 22.40% of 2025 revenue because production schedules, supplier payments, and quality records reside in ERP systems that adversaries target to cause operational disruption. Industrial ransomware attacks surged, with ransom demands. In response, manufacturers invest in real-time anomaly detection that flags suspicious changes to the bill of materials or production parameters before damage cascades.

Healthcare, although smaller today, is the fastest-growing vertical, with a 19.40% CAGR. HIPAA’s January 2025 rule update mandates multi-factor authentication on every electronic protected health information access, compresses breach-notification timelines to 72 hours, and drives immediate budget reallocation toward continuous monitoring. Hospitals and insurers now integrate SoD enforcement into electronic medical record workflows, ensuring clinicians cannot both order and self-approve high-risk medications. Retailers wrestle with PCI DSS v4.0’s 64 new requirements, financial institutions juggle Basel III and Sarbanes-Oxley, and public agencies procure only FedRAMP-authorized solutions; each mandate feeds specialized feature demand inside the ERP security and compliance market.

Geography Analysis

North America remains the largest regional slice at 34.10% in 2025, anchored by Sarbanes-Oxley audits, deep cybersecurity vendor benches, and aggressive cloud ERP adoption among Fortune 500 companies. Artificial-intelligence anomaly engines gain traction first in this region, producing lighthouse implementations that global subsidiaries later replicate. Mergers and acquisitions among mid-cap players spark new ERP instances and consolidation efforts, both of which require fresh SoD review.

Asia-Pacific posts the fastest 17.20% CAGR, driven by Japan’s spike in credential-stuffing incidents, India’s data-protection statute, and Singapore’s amended Personal Data Protection Act that levies fines of SGD 1 million (USD 750,000) for delayed breach notifications. Chinese data-localization rules compel multinationals to deploy in-country ERP stacks, in which local CSPs partner with international security vendors to satisfy dual compliance requirements. Skill shortages are acute, so managed service providers fill gaps, accelerating SaaS security adoption.

Europe grows steadily as GDPR fines escalate, crossing EUR 2.1 billion (USD 2.3 billion) in 2025. The NIS2 directive widens the definition of critical infrastructure to include digital service providers, adding transportation and logistics to the compliance roster. South America’s trajectory reflects the influence of Brazil’s Lei Geral de Proteção de Dados and Argentina’s consent-centric data-protection law. The Middle East and Africa trail in spend but experience double-digit growth as sovereign-cloud initiatives and National Institute of Standards and Technology model-led frameworks require ERP-layer controls merged with national cyber-defense strategies.

Competitive Landscape

The ERP security and compliance market demonstrates a moderate level of fragmentation. Organizations such as Pathlock, Appsian, SafePaaS, and Onapsis concentrate on delivering ERP-centric risk analytics solutions. On the other hand, companies like SailPoint, Saviynt, and Delinea enhance their core identity governance systems by incorporating ERP modules. The market witnessed an acceleration in consolidation during 2025-2026, marked by Pathlock's acquisition of Appsian and Delinea's purchase of StrongDM. These strategic moves aimed to expand zero-trust security coverage across databases and middleware.

Additionally, Onapsis introduced the Agentic Gateway, an advanced AI-driven solution designed to enhance threat detection while providing natural-language explanations to assist security operations teams in decision-making. In the current landscape, technological differentiation is increasingly reliant on federated identity gateways, which play a critical role in enforcing Segregation of Duties (SoD) across complex hybrid IT environments. Vendors that achieve certifications such as FedRAMP, ISO 27001:2022, and SOC 2 Type II gain a significant advantage in procurement processes, particularly when targeting public-sector organizations and Fortune 500 enterprises.

Meanwhile, small and medium-sized enterprises (SMEs) represent a largely untapped market segment. Platforms that come pre-configured with rule sets and offer subscription-based monitoring services are particularly appealing to finance teams operating with constrained resources, as they provide cost-effective and efficient compliance solutions.

ERP Security And Compliance Industry Leaders

Pathlock Inc.

Appsian Security Inc.

Onapsis Inc.

Delinea Inc. (Fastpath)

SafePaaS Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Delinea acquired StrongDM, unifying privileged-access management across ERP and infrastructure.

- March 2026: Onapsis launched Agentic Gateway, an autonomous threat-hunting suite for SAP and Oracle landscapes.

- January 2026: Onapsis appointed regional vice presidents for Europe, Middle East, and Asia-Pacific to accelerate go-to-market expansion.

- October 2025: Netwrix enhanced its 1Secure platform with AI-based data-loss-prevention modules linked to Active Directory Certificate Services.

Global ERP Security And Compliance Market Report Scope

The ERP Security and Compliance market encompasses software solutions and associated services that protect Enterprise Resource Planning (ERP) systems, ensure data integrity, and enable compliance with regulatory, industry, and organizational requirements.

The ERP Security and Compliance Market Report is Segmented by Component (Software and Services), Deployment Mode (On-premise, Cloud, and Hybrid), Organization Size (Large Enterprises and Small and Medium Enterprises), End-use Industry (Manufacturing, Banking Financial Services and Insurance, Healthcare, Retail and E-commerce, Government and Public Sector, IT and Telecom, and Other End-use Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| On-premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Banking, Financial Services and Insurance |

| Healthcare |

| Retail and E-commerce |

| Government and Public Sector |

| IT and Telecom |

| Other End-use Industries |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East |

| Africa |

| By Component | Software |

| Services | |

| By Deployment Mode | On-premise |

| Cloud | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-use Industry | Manufacturing |

| Banking, Financial Services and Insurance | |

| Healthcare | |

| Retail and E-commerce | |

| Government and Public Sector | |

| IT and Telecom | |

| Other End-use Industries | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East | |

| Africa |

Key Questions Answered in the Report

How fast is the ERP security and compliance market expected to grow through 2031?

It is projected to advance at a 12.01% CAGR from 2026 to 2031, reaching USD 54.51 billion in value.

Which deployment mode is gaining the most traction?

Cloud deployments lead with 58.50% share in 2025 and are expanding at an 18.30% CAGR as enterprises shift core workloads to SaaS ERP.

Why is healthcare the quickest-expanding end-use sector?

HIPAAs 2025 mandate for multi-factor authentication and 72-hour breach reporting drives 19.40% CAGR growth in healthcare spending on ERP security.

What primary factor restrains adoption among SMEs?

High initial integration costs, sometimes surpassing annual IT security budgets, deter small and medium enterprises despite cloud price elasticity.

Which region is forecast to record the highest growth rate?

Asia-Pacific is set to achieve a 17.20% CAGR, fueled by rising cybercrime exposure and stricter data-protection statutes in Japan, India, and Singapore.

Page last updated on: