Enzymatic Recycling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

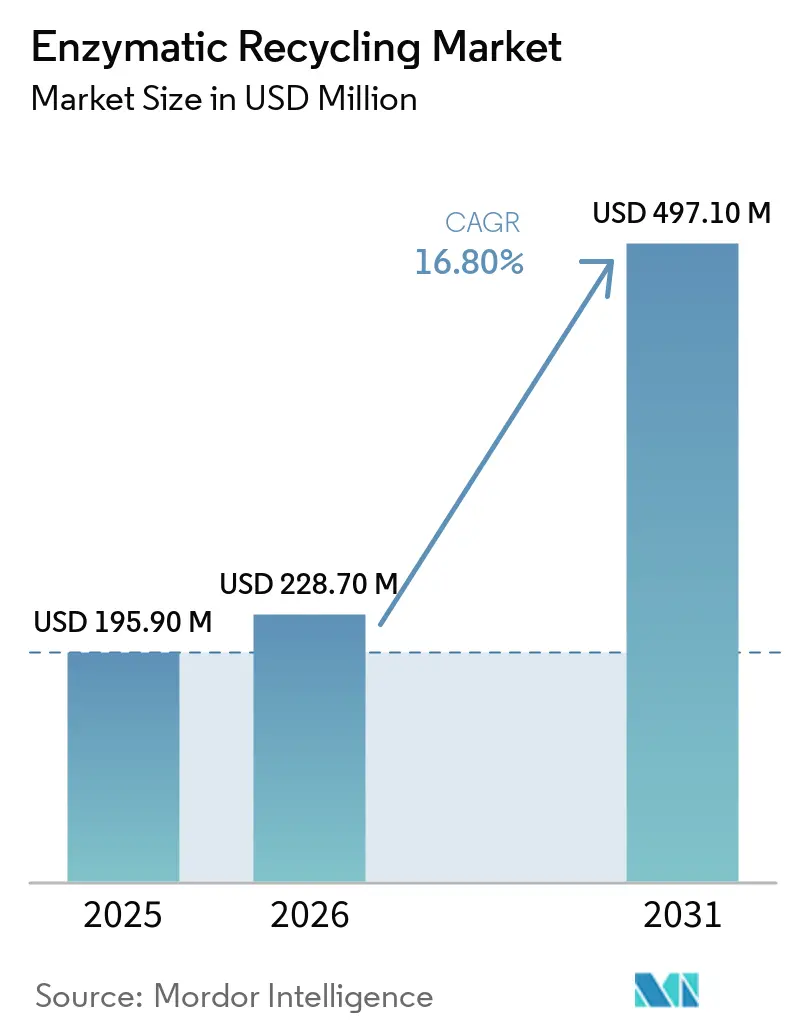

| Market Size (2026) | USD 228.70 Million |

| Market Size (2031) | USD 497.10 Million |

| Growth Rate (2026 - 2031) | 16.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enzymatic Recycling Market Analysis by Mordor Intelligence

The Enzymatic Recycling Market size is projected to expand from USD 195.90 million in 2025 and USD 228.70 million in 2026 to USD 497.10 million by 2031, registering a CAGR of 16.80% between 2026 to 2031.

The shift from pilots to commercial deployment is supported by audited process innovations that push enzyme-recycled PET below United States virgin PET price benchmarks, reinforcing cost-based adoption in the enzymatic recycling market. Steady policy momentum in the European Union and rising public funding in the United States are compressing time-to-scale for first movers, improving offtake certainty, and reducing project-finance risk premia across the enzymatic recycling market. Multi-enzyme systems and immobilized formats now complement high-performance hydrolases, driving productivity gains while addressing contamination and reuse needs in continuous operation. Competitive intensity remains moderate-to-high as pioneers lock in brand agreements and exclusive enzyme supply, while regional challengers scale with public grants and industrial consortia, setting the stage for faster penetration from 2026 onward.

Key Report Takeaways

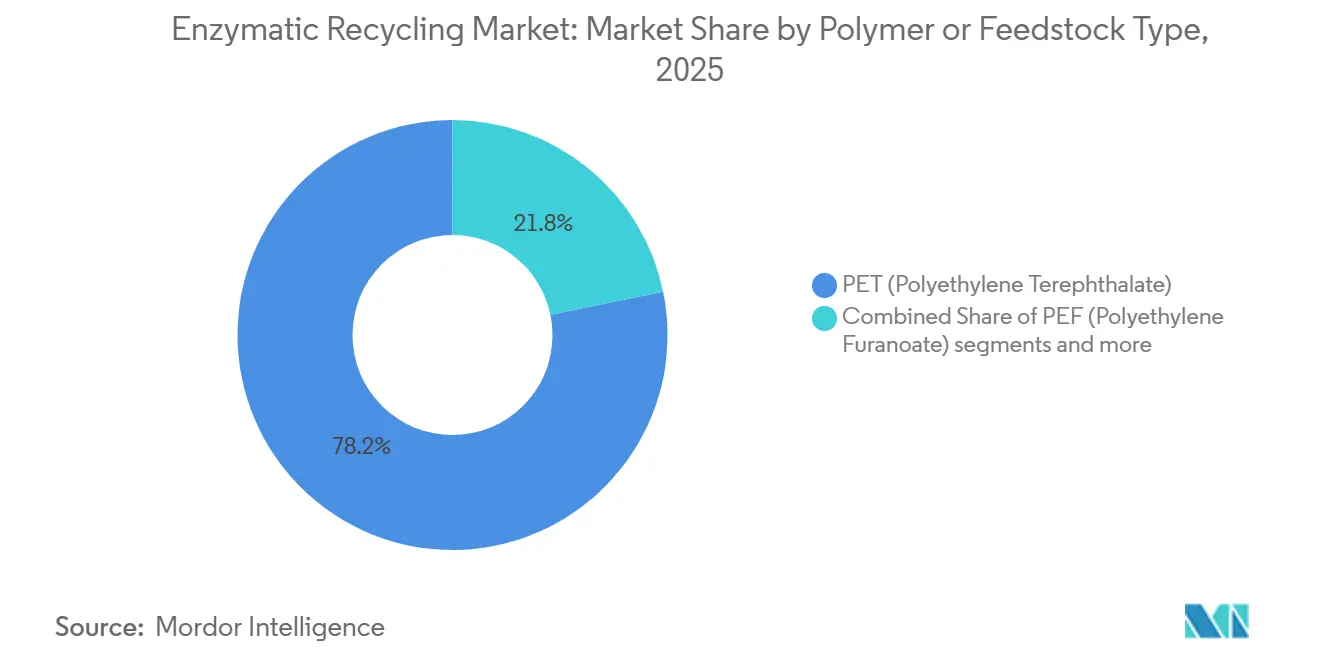

- By polymer/feedstock type, PET (Polyethylene Terephthalate) accounted for 78.2% of the enzymatic recycling market share in 2025 and is projected to grow at a CAGR of 18.7% through 2031.

- By enzyme type, hydrolases accounted for 74.32% of the enzymatic recycling market size in 2025, while oxidoreductases are forecast to expand at a 19.2% CAGR to 2031.

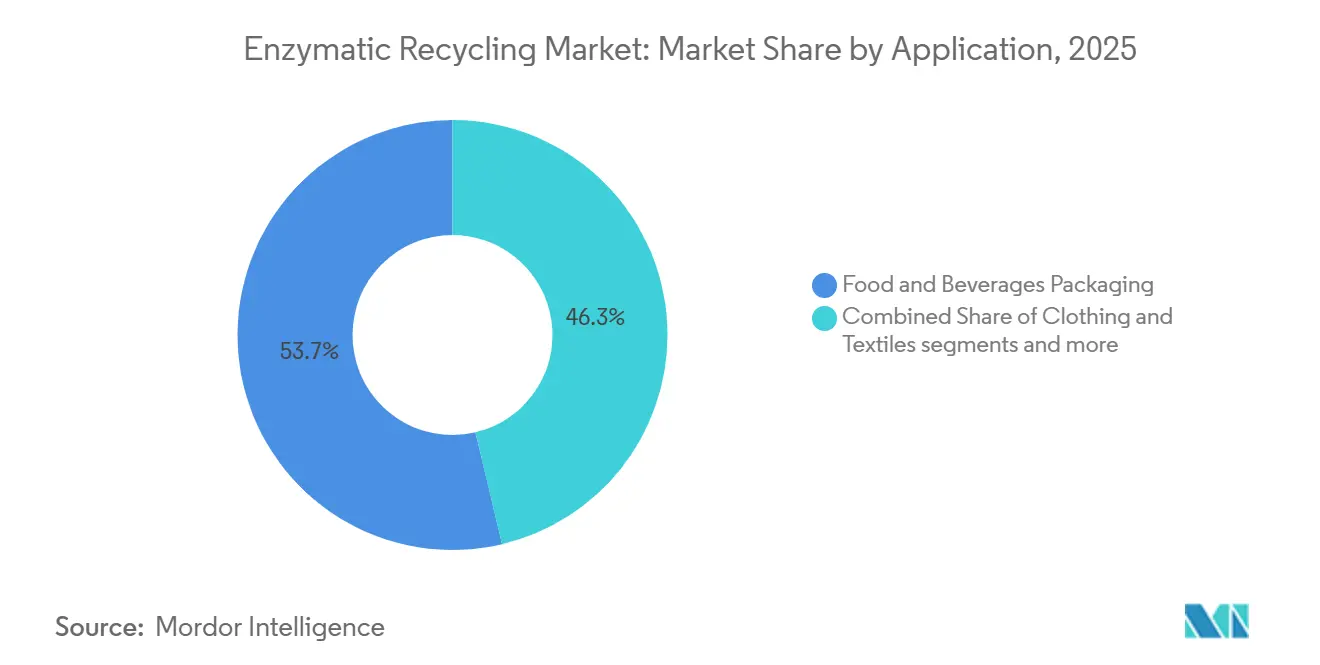

- By application, food & beverages packaging accounted for 53.7% in 2025, with clothing & textiles projected to advance at a 20.7% CAGR through 2031.

- By technology, biocatalysis via free enzymes held 68.9% in 2025, while immobilized enzyme systems are set to grow at a 21.7% CAGR to 2031.

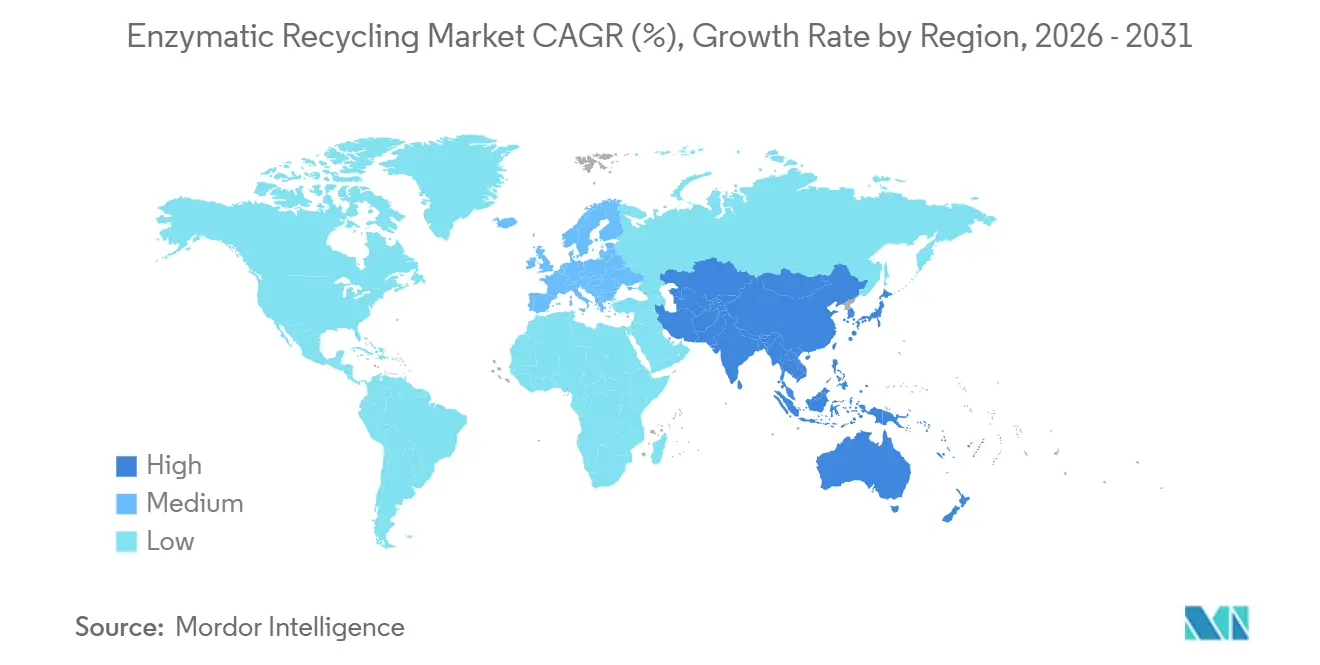

- By geography, Europe led with a 38.7% share in 2025, and Asia-Pacific is projected to post a 22.4% CAGR through 2031 in the enzymatic recycling market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Enzymatic Recycling Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic Advantages Over Virgin Plastic Production as Technology Scales | +3.8% | Regional, with early parity in Asia and potential EU cost advantages | Long term (≥ 4 years) |

| Stringent Environmental Regulations on Plastic Waste Management | +3.2% | Global, with early gains in EU and North America | Medium term (2-4 years) |

| Growing Corporate Sustainability Commitments and Net-Zero Targets | +2.8% | Global, led by multinational brands in Europe, North America, and Asia | Long term (≥ 4 years) |

| Technological Breakthroughs in Enzyme Engineering and Biocatalysis | +2.6% | Global, concentrated in leading R&D hubs in the U.S., EU, Japan, and China | Medium term (2-4 years) |

| Increasing Availability of Venture Capital and Strategic Funding | +2.5% | North America and Europe core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Rising Consumer Preference for Sustainable and Circular Products | +2.1% | Global, strongest in Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Advantages Over Virgin Plastic Production as Technology Scales

Peer-reviewed process designs and validated pilots now place enzyme-recycled Polyethylene Terephthalate (PET) within or below the cost band of virgin PET, accelerating adoption in the enzymatic recycling market. In 2025, National Renewable Energy Laboratory (NREL) and collaborators reported USD 1.51 per kilogram for enzyme-recycled PET versus USD 1.87 per kilogram for United States domestic virgin PET, enabled by substrate amorphization, ammonium-hydroxide pH control, and lower energy demand for recovery. At commercial scale, operators project cost-parity ranges in which policy-linked premiums and Extended Producer Responsibility (EPR) fee modulation can secure attractive margins under real-world feedstock conditions. As carbon pricing and border adjustments expand, the comparative advantage of low-temperature, solvent-light enzymatic depolymerization grows against fossil incumbents. These gains compound when paired with the reuse of immobilized enzymes, which spreads catalyst costs across multiple cycles and increases reactor productivity. Together, these improvements turn prior aspirations into bankable economics at first-commercial plants.

Stringent Environmental Regulations on Plastic Waste Management

Tightening global rules on recycled content and extended producer responsibility are raising the structural floor for demand in the enzymatic recycling market. The EU Single-Use Plastics Directive requires 25% recycled content in PET beverage bottles in 2025 and 30% by 2030, and in 2025, the Commission opened a consultation on counting chemically recycled content in bottles, signaling regulatory pathways for advanced recycling[1]European Commission, “Commission Consults on New Rules for Chemically-Recycled Content in Plastic Bottles,” European Commission, europa.eu. France added a EUR 1,000-per-tonne bonus (approximately USD 1,080 per tonne) for biorecycled plastics in sensitive-contact packaging in September 2025, improving modeled margins for food-grade enzymatic rPET. China advanced national standards and roadmaps for recycled plastics in 2025, positioning enzymatic depolymerization within chemical recycling development phases. These policy signals encourage long-term offtake, support financing for first-of-commercial facilities, and reinforce the emissions and purity advantages that differentiate enzyme-based routes. As regulators refine end-of-waste rules and traceability frameworks, certified chain-of-custody can translate directly into procurement criteria that favor enzymatic monomers.

Growing Corporate Sustainability Commitments and Net-Zero Targets

Public commitments in sustainability reports and investor communications are converting into pre-sales and long-horizon purchasing agreements that de-risk scale-up for the enzymatic recycling market. In 2025 and 2026, Carbios disclosed multi-year brand contracts and targeted 70% plant pre-sales for Longlaville, aligning financing with projected utilization before commissioning[2]Carbios, “CARBIOS Maintains Its Commitment to Build the Longlaville Plant and Adjusts Its Timeline,” Carbios, carbios.com. These offtakes enable project finance structures to proceed with narrower interest spreads and help absorb output as facilities ramp from pilot to steady-state volumes. Consortia and bilateral brand agreements support guaranteed feedstock and predictable revenue, while quality specifications for virgin-equivalent monomers accelerate qualification in regulated packaging. Corporate sustainability teams are integrating recycled-content key performance indicators into executive compensation, which sustains procurement even during swings in virgin resin pricing. These factors extend visibility into the late 2020s for capacity planning and underpin the learning-curve effects that lower unit costs as volumes scale.

Technological Breakthroughs in Enzyme Engineering and Biocatalysis

Accelerated protein engineering and computational design are converting research-grade enzymes into industrial tools for the enzymatic recycling market. Japan’s Kirin, Shizuoka University, and the Institute for Molecular Science reported PET2-21M with roughly 95% depolymerization of bottle-grade PET powder in 24 hours at 60°C, plus scalable yeast-based production of PET2-14M-6Hot near 690 mg/L. Nagoya University boosted cutinase activity by 69% using a simple alkyl-chain modification that enhances PET surface adsorption, opening formulation paths beyond genetic edits. Chinese research teams disclosed a double-mutant enzyme that degrades polyester-type polyurethane up to 10 times faster than the wild type, widening the substrate scope beyond PET. EU consortia such as WHITECYCLE and UPLIFT standardized performance metrics and scaled pilots, improving transferability of lab success into industry trials. These advances shorten development cycles and lift conversion performance under moderate temperatures, which suits both batch and continuous plant designs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure and Long Payback Periods | -2.4% | North America and Asia-Pacific, moderate in Europe | Medium term (2-4 years) |

| Competition from Established Chemical Recycling Technologies | -2.2% | Global, with entrenched pyrolysis assets in EU and U.S. | Medium term (2-4 years) |

| Limited Substrate Scope and Polymer Type Compatibility | -1.8% | Global, acute in polyolefin-intensive regions | Long term (≥ 4 years) |

| Enzyme Production Costs and Supply Chain Complexities | -1.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Long Payback Periods

First-commercial enzymatic depolymerization plants require heavier capex than mechanical recyclers, placing a premium on offtakes, policy support, and finance blending to make returns viable in the enzymatic recycling market. Carbios disclosed EUR 230 million (approximately USD 248 million) for its Longlaville build and moved into 2026, needing to close the final portion while targeting a 2028 start, which underlines the timeframes involved in engineering, procurement, and construction. Chinese projects show staged capex with 10,000-tonne anchor lines designed to de-risk later expansions, a pattern that spreads fixed costs but delays full economies of scale. Payback horizons remain sensitive to gate fees, enzyme costs, and recycled-content premiums, which tie outcomes to regulatory continuity. Financing certainty improves when brands sign multi-year offtakes before groundbreak, yet interest-rate cycles still influence project timing.

Competition from Established Chemical Recycling Technologies

Enzymatic depolymerization competes with mechanical recycling for clean streams and with chemical routes for mixed waste and offtakes, which diffuses investment and slows utilization in the enzymatic recycling market. Mechanical routes hold the lowest cost for clear bottles, while pyrolysis and solvent-based polyester renewal claim mixed-feedstock tolerance at larger installed scales. Policy frameworks that treat all advanced recycling equivalently under mandates can weaken differentiation based on low-temperature operation and monomer purity. Where mass-balance accounting expands, certification choices will influence brand claims and purchasing, shaping the share captured by enzymatic offtakes. Competitive dynamics will be defined by cost parity with virgin resin and clarity on recycled-content attribution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer/Feedstock Type: PET Dominance with Bio-Based Polymers Gaining Traction

PET (Polyethylene Terephthalate) dominates the enzymatic recycling market, accounting for a 78.2% market share in 2025, and is projected to grow at a CAGR of 18.7% through 2031, driven by its strong compatibility with enzymatic processes and well-established collection systems. The market continues to rely on PET’s ester linkages, moderate processing conditions, and consistent availability of bottle-grade feedstocks that meet quality specifications at scale. Ongoing innovation is further expanding PET applications into more complex streams such as colored PET and textile-derived waste, where enzymatic recycling can unlock higher recovery value and differentiation.

At the same time, advancements in enzymes for polyurethane and polyamide, including early developments in nylon 6,6 recycling, are gradually expanding the industry’s long-term substrate scope. However, these segments remain at an early stage and face scaling challenges related to enzyme stability and mixed-material handling. As a result, PET is expected to remain both the largest and fastest-growing segment in the near term, anchoring commercialization while supporting incremental diversification across emerging polymer types.

By Enzyme Type: Hydrolase Primacy with Multi-Enzyme Systems Advancing

Hydrolases accounted for 74.32% in 2025, driven by consistent performance on PET and improved kinetics at industrially relevant temperatures. The enzymatic recycling market continues to benefit from cutinase and PETase derivatives tuned through directed evolution and process-informed design. Oxidoreductases are the fastest-growing group, with a 19.2% CAGR through 2031, as operators trial cascades to pre-treat contamination and co-process challenging waste streams. Standardized benchmarks in EU consortia improved cross-lab comparability and accelerated translation into pilot systems. These shifts keep hydrolases central while expanding the toolkit for mixed substrates and continuous operation within the enzymatic recycling industry.

The enzymatic recycling market for hydrolases remains the largest, while oxidoreductases gain ground toward future multi-enzyme architectures in industrial reactors. Immobilization strategies improve reuse and stabilize catalytic activity, complementing native hydrolase strengths and supporting a lower cost per cycle. As datasets grow and models improve, more enzymes will meet performance thresholds for industrial qualification, widening substrate compatibility and use cases. In parallel, supplier capacity and formulation advances will be essential to meet the volume and shelf-stability needs of early commercial plants.

By Application: Food & Beverages Packaging Leads, Textiles Surge as Fiber-to-Fiber Gains Momentum

Food & beverages packaging led with 53.7% in 2025, supported by strong collection, food-contact clearances, and brand procurement aligned to recycled-content targets. Regulatory pathways for rPET in food-contact provide a repeatable channel for qualified monomers to re-enter high-value packaging. Clothing & textiles are the fastest-growing application, projected to grow at a 20.7% CAGR, as fiber-to-fiber routes move from pilots to demonstration scale. European policy on separate textile collection improves feedstock flows for enzymatic depolymerization and supports rapid learning cycles in the textile industry. These conditions extend packaging leadership while opening a second major demand center in apparel and performance textiles.

Textile offtakes and performance validations are expanding, which supports scale-up plans that complement packaged-goods demand in the enzymatic recycling market. As brands test fiber strength and dye affinity, enzyme-monomer quality becomes a decisive factor for premium collections. Automotive and construction remain smaller today, with PU and technical polyester progress likely to shape medium-term adoption. The balance of evidence indicates a two-pillar demand structure for the next five years, anchored in packaging and ramping textiles.

By Technology: Free Enzyme Systems Lead, Immobilized Enzyme Systems Propel Productivity Gains

Free enzyme systems accounted for 68.9% of the enzymatic recycling market in 2025, driven by operational simplicity and compatibility with existing fermentation economics. Meanwhile, immobilized enzyme systems are projected to grow at a CAGR of 21.7% through 2031, supported by their ability to improve enzyme reuse, process stability, and productivity efficiency. The enzymatic recycling market favors hybrid flows that pair pre-treatment to reduce crystallinity with optimized enzyme kinetics to boost throughput. As immobilization materials improve and tie-in costs fall, the technology mix will shift toward higher uptime and lower catalyst intensity per tonne. Together, these formats expand the operational playbook for early commercial plants.

The enzymatic recycling market will remain dominated by free-enzyme systems in the near term, while immobilized systems will close gaps through proven reuse factors. Optimization focus is shifting from single-parameter lab gains to integrated, plant-level metrics where uptime, energy intensity, and monomer yield define outcomes. Supplier partnerships and exclusive agreements affect technology choices and standard operating procedures as licensees seek predictable performance. This dynamic will guide reactor design and cost curves across the 2026–2031 horizon.

Geography Analysis

Europe held 38.7% in 2025, reflecting strong policy mandates and early public financing for first-of-a-kind plants in the enzymatic recycling market. EU rules on recycled content in PET beverage bottles, and 2025 consultations on counting chemically recycled inputs frame a clear pathway for advanced recycling contributions. France’s bonus for biorecycled plastics in sensitive-contact packaging enhances economics for food-grade applications and has supported brand adoption. Carbios advanced financing for a 50,000-tonne Longlaville facility, confirming the objective of starting production in 2028 and illustrating Europe’s front-runner in commercialization. EU-funded projects such as WHITECYCLE and PET-Rezya have deepened cross-border collaboration on enzyme libraries and specialty feedstocks, such as flame-retardant PET.

Asia-Pacific is the fastest-growing region with a projected 22.4% CAGR to 2031, propelled by China’s standards advances, new textile-focused enzymatic PTA capacity in Tianjin TEDA, and strategic licensing for PET depolymerization. Japan’s research output has been pivotal, with PET2-21M and related heat-resistant enzymes demonstrating high conversion at moderate temperatures and scalable expression. These factors create an innovation-to-industry corridor that supports faster commercialization across packaging and textiles. Regional integration of textile and petrochemical value chains further compresses feedstock and logistics costs, which accelerates plant ramp-up.

North America is gaining momentum through the BOTTLE Consortium and DOE support, which have enabled cost and energy breakthroughs. Academic and national lab collaboration with industry has improved process economics, giving developers a stronger foundation for pilot-to-demonstration transitions through 2026–2028. Food-contact precedents for recycled PET support adoption in packaging when quality is proven, and traceability is documented. State-level EPR initiatives are evolving, and harmonization will influence investment pacing and offtake structures.

Competitive Landscape

The enzymatic recycling market is moderately consolidated in nature, with moderate-to-high competitive intensity as a handful of leading players secure enzyme supply, Intellectual Property (IP) positions, and brand offtakes while challengers scale regionally. Carbios and partners advanced financing for the Longlaville plant and disclosed multi-year brand commitments to anchor early utilization. EU projects WHITECYCLE and PET-Rezya strengthen Europe’s technical base, particularly for specialty inputs like flame-retardant textiles. In parallel, Asia’s textile-focused capacity and licensing activity are positioning local firms as fast followers in the PET and PTA routes.

Technology differentiation is shifting from enzyme activity alone to integrated solutions that combine pre-treatment, optimized biocatalysts, and purification tuned for food-grade outputs. Advances in immobilization and process design are helping reduce catalyst intensity and stabilize performance under continuous operation. Strategic moves include brand-led offtakes in apparel and packaging, public funding to anchor first-commercial plants, and standardized validation under EU programs, all of which underpin bankability. Developers who deliver cost parity with virgin resin and a verified chain of custody will consolidate early advantage.

North America’s public-lab ecosystems, anchored by BOTTLE, are translating research into industry-ready processes that cut both operating costs and energy intensity, helping close the gap with incumbents. Europe’s early policy clarity and funding reinforce a licensing-led expansion strategy, while Asia’s cost base and capacity commitments support rapid buildouts in PTA-focused textile recycling. The net effect is a multi-regional race where speed to first-commercial plants and offtake lock-in will determine share capture through 2031.

Enzymatic Recycling Industry Leaders

Samsara Eco

Carbios

Epoch Biodesign

Yuantian Biotechnology

Novonesis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Carbios reported significant financing progress for the Longlaville PET biorecycling plant, targeting production start in H1 2028 with EUR 42.5 million (approximately USD 46 million) in confirmed public funds and the remaining financing expected to close by Q3 2026.

- February 2026: Fraunhofer IGCV and partners completed PET-Rezya on enzymatic recycling of flame-retardant PET textiles, scaling decomposition and repolymerization of TPA for aviation applications.

- September 2025: France enacted a EUR 1,000 per tonne (USD 1,080 per tonne) bonus for bio-recycled plastics in sensitive-contact packaging, supporting the cost competitiveness of enzymatic rPET.

- July 2025: Japan’s IMS, Shizuoka University, and Kirin Holdings announced PET2-21M with approximately 95% depolymerization of bottle-grade PET powder in 24 hours at 60°C and scalable expression near 690 mg/L.

Global Enzymatic Recycling Market Report Scope

The Enzymatic Recycling Market Report is Segmented by Polymer/Feedstock Type (Polyethylene Terephthalate and more), Enzyme Type (Hydrolases and more), Application (Food & Beverages Packaging, Clothing & Textiles, and more), Technology (Free Enzyme Systems, Immobilized Enzyme Systems, and more), and Geography (North America, Europe, and more). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

| PET (Polyethylene Terephthalate) |

| PEF (Polyethylene Furanoate) |

| PE (Polyethylene) |

| PU (Polyurethane) |

| Others |

| Hydrolases |

| Oxidoreductases |

| Lyases |

| Isomerases/Ligases/Transferases |

| Others |

| Food & Beverages Packaging |

| Clothing & Textiles |

| Automotive |

| Construction |

| Consumer Goods & Electronics |

| Others |

| Free Enzyme Systems |

| Immobilized Enzyme Systems |

| Whole-Cell Biocatalysis |

| Hybrid Processes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| SouthEast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Polymer/Feedstock Type | PET (Polyethylene Terephthalate) | |

| PEF (Polyethylene Furanoate) | ||

| PE (Polyethylene) | ||

| PU (Polyurethane) | ||

| Others | ||

| By Enzyme Type | Hydrolases | |

| Oxidoreductases | ||

| Lyases | ||

| Isomerases/Ligases/Transferases | ||

| Others | ||

| By Application | Food & Beverages Packaging | |

| Clothing & Textiles | ||

| Automotive | ||

| Construction | ||

| Consumer Goods & Electronics | ||

| Others | ||

| By Technology | Free Enzyme Systems | |

| Immobilized Enzyme Systems | ||

| Whole-Cell Biocatalysis | ||

| Hybrid Processes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| SouthEast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the enzymatic recycling market size and projected growth to 2031?

The enzymatic recycling market size is USD 228.7 million in 2026 and is projected to reach USD 497.1 million by 2031 at a 16.8% CAGR.

Which polymer type leads and which grows the fastest in enzymatic recycling?

Polyethylene Terephthalate leads with a 78.2% share in 2025 and is also the fastest-growing polymer segment, projected to expand at a CAGR of 18.7% during 2026–2031.

What region leads and which region will grow the fastest through 2031?

Europe leads with 38.7% in 2025, and Asia-Pacific is projected to grow the fastest at a 22.4% CAGR.

Which application accounts for the largest share today?

Food & beverages packaging accounts for 53.7% in 2025 due to strong collection and food-contact clearances.

Page last updated on: