AI-Integrated Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

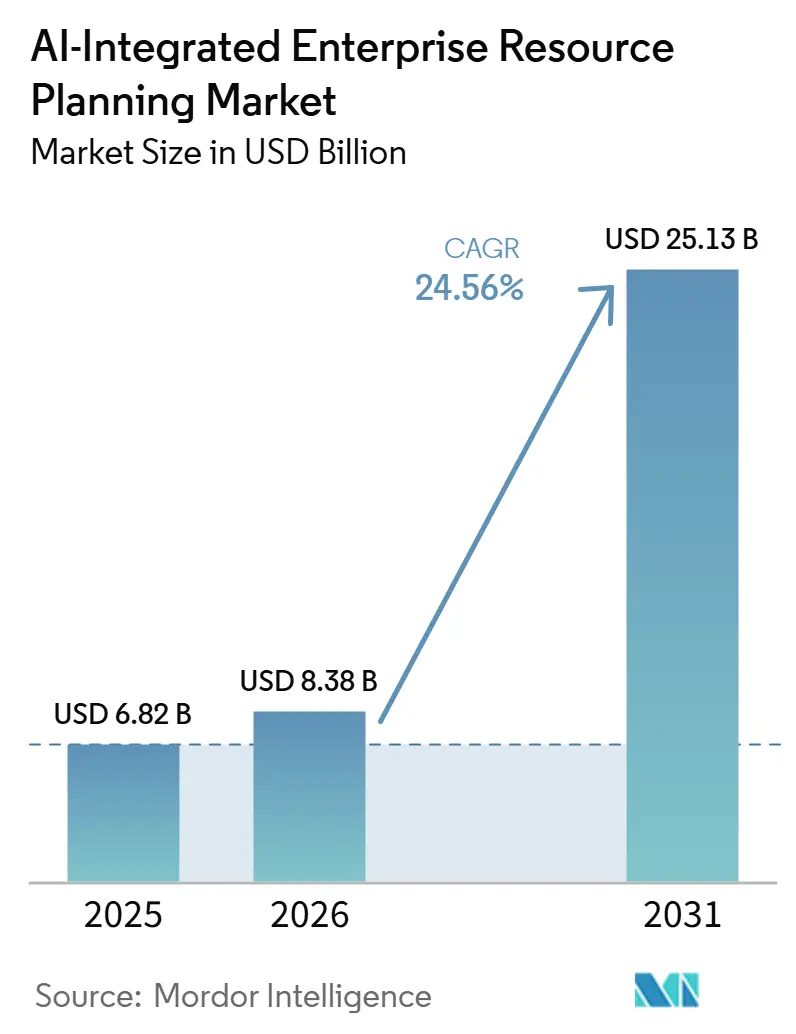

| Market Size (2026) | USD 8.38 Billion |

| Market Size (2031) | USD 25.13 Billion |

| Growth Rate (2026 - 2031) | 24.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

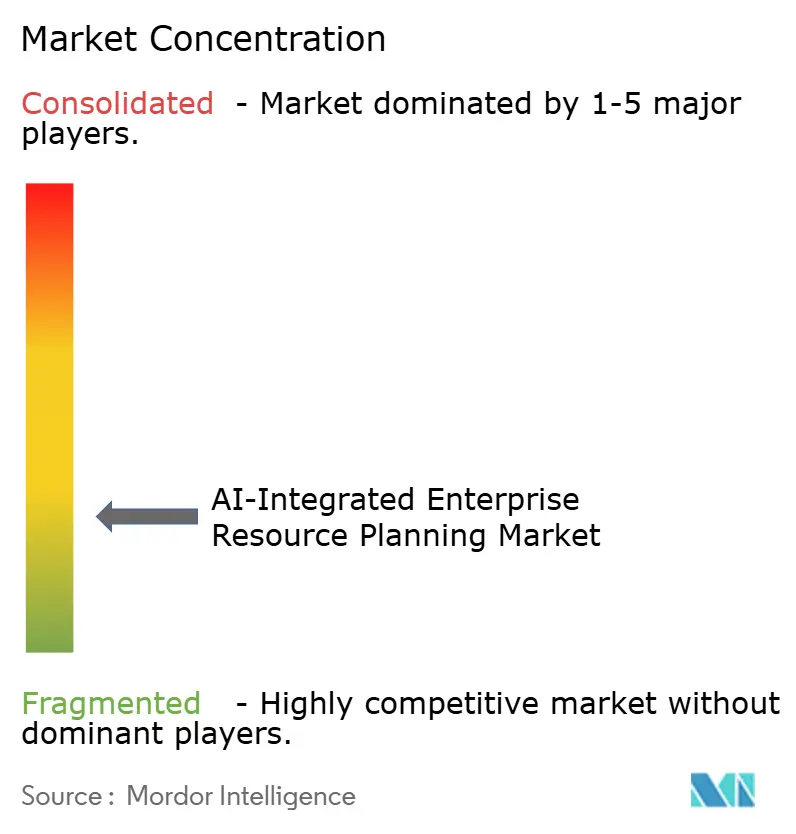

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Integrated Enterprise Resource Planning Market Analysis by Mordor Intelligence

The AI-integrated enterprise resource planning market size is expected to increase from USD 8.38 billion in 2026 to reach USD 25.13 billion by 2031, growing at a CAGR of 24.56% over 2026-2031. Organizations are accelerating upgrades as cloud-native suites embed predictive intelligence that automates exception handling and reconfigures workflows in real time. On-premise customers extend existing investments with edge-deployed models, while greenfield adopters choose multitenant SaaS to avoid infrastructure costs. Vendors are bundling conversational copilots and autonomous finance agents exclusively in cloud subscriptions, which pulls mid-market buyers into the ecosystem even when budgets are tight. Supply-chain volatility, labor shortages, and government digital-transformation incentives reinforce adoption, turning the AI-integrated enterprise resource planning market into a strategic priority across every region and industry.

Key Report Takeaways

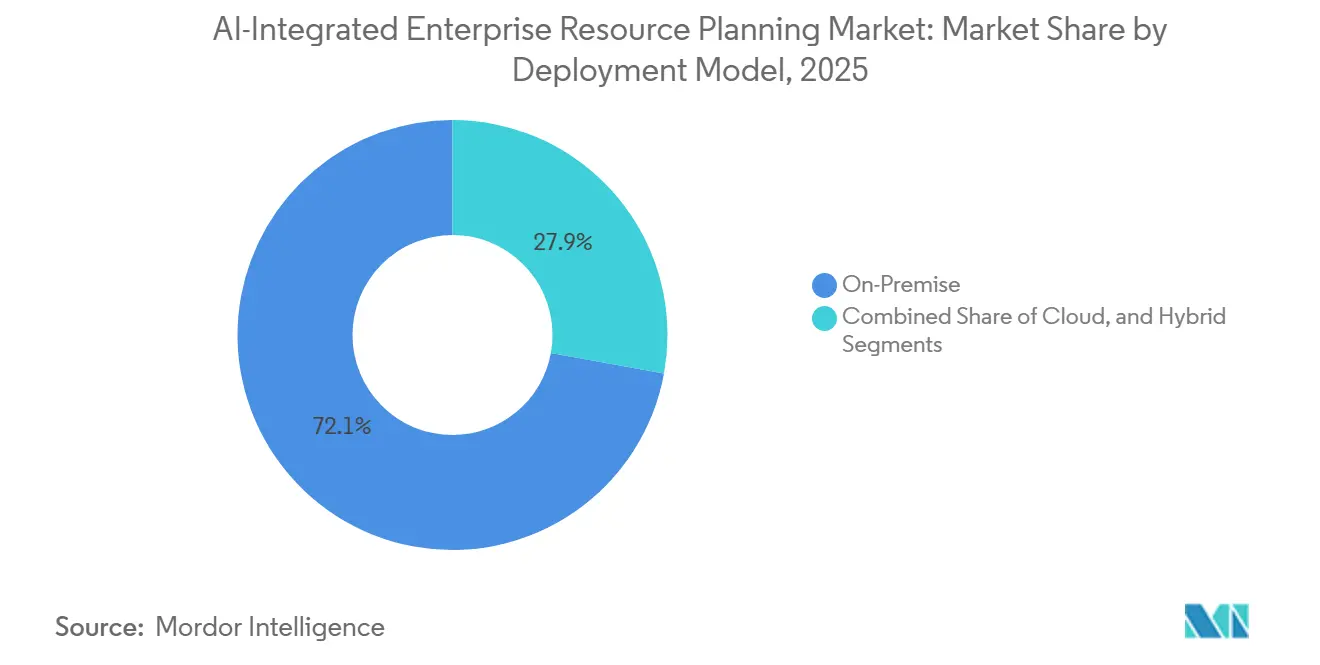

- By deployment model, on-premise installations commanded 72.13% of the AI-integrated enterprise resource planning market share in 2025, whereas cloud deployments are advancing at a 25.16% CAGR through 2031.

- By enterprise size, large enterprises accounted for 67.48% of revenue share in 2025, yet small and medium enterprises are projected to expand at a 25.13% CAGR between 2026 and 2031.

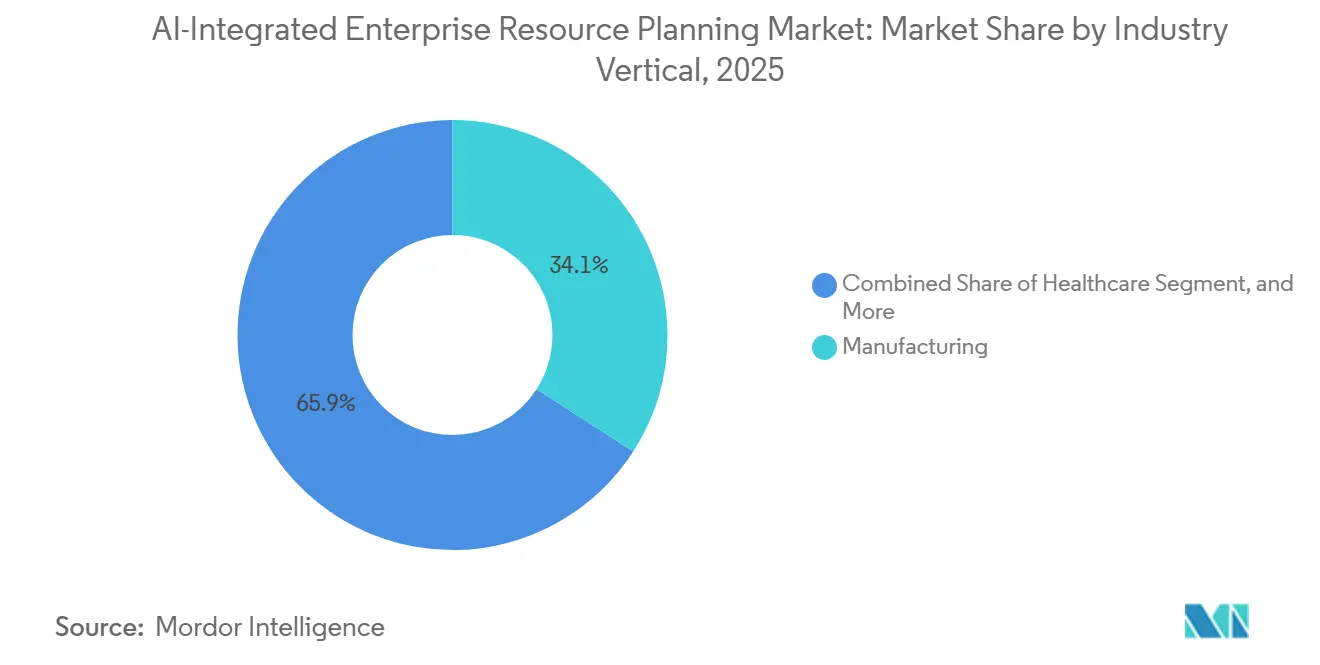

- By industry vertical, manufacturing led with 34.11% revenue share in 2025, while healthcare is poised to grow at a 25.96% CAGR to 2031.

- By business function, finance and accounting accounted for 26.31% of spending in 2025; inventory and work-order management is forecast to grow at a 25.76% CAGR through 2031.

- By geography, North America dominated with 37.89% revenue share in 2025; Asia-Pacific is projected to accelerate at a 25.56% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Integrated Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Migration to Cloud-Native ERP with Embedded AI | +5.2% | Global, with early concentration in North America and Western Europe | Medium term (2-4 years) |

| Demand for Real-Time Predictive Analytics in Supply Chain Disruptions | +4.8% | Global, particularly Asia-Pacific manufacturing hubs and North America retail | Short term (≤ 2 years) |

| Two-Tier ERP Adoption among Multinational Subsidiaries | +3.9% | North America and Europe headquarters with Asia-Pacific and South America subsidiaries | Medium term (2-4 years) |

| AI-Driven Reduction in Implementation Time and Cost | +4.1% | Global, with highest uptake in mid-market segments across all regions | Short term (≤ 2 years) |

| Mid-Market Appetite for Composable Low-Code ERP Modules | +3.6% | North America, Europe, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Government Digital Transformation Mandates and Incentives | +3.4% | Asia-Pacific (Japan, India), Middle East (UAE), North America (United States, Canada) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Migration to Cloud-Native ERP With Embedded AI

Global corporations typically maintain a single instance of SAP S/4HANA or Oracle Fusion at their headquarters while equipping subsidiaries with lighter, more agile cloud suites such as NetSuite or Microsoft Dynamics 365 Business Central.[1] Oracle Corporation, “Oracle Announces AI Agents for Fusion Cloud Applications,” ORACLE.COM This hub-and-spoke architecture balances global financial consolidation with localized operational flexibility. Pre-configured templates streamline deployment by packaging manufacturing, distribution, or service workflows, enabling regional entities to achieve go-live in less than 4 months. This is a significant improvement over the year or more typically required for a full-scale rollout. Additionally, nightly synchronization ensures compliance with transfer pricing regulations, while local teams retain the ability to modify procurement rules without triggering corporate-level change control processes. This approach allows organizations to maintain centralized oversight while fostering adaptability at the regional level.

Demand for Real-Time Predictive Analytics in Supply Chain Disruptions

Manufacturers and retailers are increasingly integrating external signals such as port-congestion updates, extreme-weather alerts, and geopolitical indices directly into their planning engines to enhance operational efficiency. These predictive models enable businesses to proactively reschedule production, reroute freight, and rebalance safety stock, preventing shortages from escalating into larger disruptions. For instance, automotive and consumer-electronics companies that have implemented real-time visibility platforms connected to AI-integrated enterprise resource planning market deployments have successfully reduced planning cycles by one-third. Additionally, these companies have significantly reduced expedited shipping costs, demonstrating the tangible benefits of such integrations. This emerging practice is transforming traditional dashboards from merely providing descriptive views into advanced prescriptive engines capable of autonomously executing corrective actions, thereby streamlining decision-making processes and improving overall supply chain resilience.

Two-Tier ERP Adoption Among Multinational Subsidiaries

Global corporations typically maintain a single instance of SAP S/4HANA or Oracle Fusion at their headquarters to centralize operations and ensure consistency across the organization. At the same time, they empower their subsidiaries by deploying lighter cloud-based suites such as NetSuite or Microsoft Dynamics 365 Business Central. This hub-and-spoke structure is designed to strike a balance between global financial consolidation and the flexibility required for local operations. Pre-packaged templates for manufacturing, distribution, or services workflows enable regional entities to implement these systems efficiently, reducing the go-live timeline to under four months compared to the year or more typically needed for a full-scale rollout. Additionally, nightly synchronization ensures compliance with transfer pricing regulations while allowing local teams to modify procurement rules without triggering corporate-level change controls. This approach enhances operational efficiency while maintaining regulatory and organizational alignment across all levels of the business.

AI-Driven Reduction in Implementation Time and Cost

Automated configuration assistants meticulously analyze chart-of-account spreadsheets and generate ready-to-deploy setups tailored to organizational needs. These tools streamline the setup process, reducing manual effort and minimizing errors. Additionally, robotic test frameworks simulate and execute thousands of transactions, identifying potential defects and inconsistencies well before go-live dates. This proactive approach significantly reduces the risk of deployment issues. Consequently, organizations experience a 25-35% reduction in adoption costs, with payback periods shortening to less than twelve months. Furthermore, managed service providers enhance these systems by integrating predictive diagnostics, which identify and address performance bottlenecks before they escalate. This allows organizations to optimize their IT resources, reallocating skilled labor from routine maintenance tasks to more strategic, high-value analytics and decision-making processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Data-Security and Compliance Concerns in Regulated Industries | -2.8% | Global, with acute pressure in Europe (GDPR), North America (HIPAA, SOX), and Asia-Pacific (emerging data localization laws) | Short term (≤ 2 years) |

| Integration Complexity with Legacy and Edge Systems | -2.4% | North America and Europe (aging on-premise infrastructure), Asia-Pacific (heterogeneous vendor ecosystems) | Medium term (2-4 years) |

| Shortage of AI-Skilled ERP Implementation Talent | -1.9% | Global, with most severe gaps in Asia-Pacific and South America | Long term (≥ 4 years) |

| Vendor Lock-In and Escalating Subscription Costs | -1.7% | Global, affecting mid-market and large enterprises equally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Data-Security and Compliance Concerns in Regulated Industries

Healthcare and banking entities are required to demonstrate that training data remains confined within approved jurisdictions and that audit trails comply with regulations such as GDPR, HIPAA, or SOX. This ensures that sensitive data is handled securely and transparently. However, to address regulatory concerns, many organizations implement parallel manual reviews alongside AI-generated journal entries. These reviews are intended to build trust with regulators but often undermine the efficiency gains promised by AI automation. To overcome these challenges, emerging federated-learning techniques offer a potential solution by enabling local model training without transferring sensitive data across jurisdictions.[2]United Arab Emirates Federal Tax Authority, “E-Invoicing Mandate,” TAX.GOV.AE Despite its promise, the adoption of federated learning at scale remains limited, as few enterprise suites have successfully operationalized it.

Integration Complexity With Legacy and Edge Systems

Large manufacturers use programmable logic controllers (PLCs) and supervisory control systems that generate data in proprietary formats, making seamless integration with enterprise resource planning (ERP) systems challenging. To enable predictive maintenance agents to effectively communicate with ERP work-order modules, translation layers are often required. These layers are typically custom-coded, which adds complexity and increases the integration cost. In many cases, the budgets allocated to integration efforts can exceed the cost of the core software itself. Additionally, each new interface introduced during integration increases the potential for cybersecurity vulnerabilities, creating further risks for manufacturers. While low-code integration hubs have emerged as a solution to simplify some of these challenges, they come with their own set of issues, including additional licensing fees and governance requirements, which manufacturers must carefully manage to ensure operational efficiency and security.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: On-Premise Resilience Amid Cloud Momentum

On-premises installations retained 72.13% of 2025 revenue because regulated enterprises keep sensitive records within corporate firewalls and require millisecond-level response times for shop-floor equipment. The AI-integrated enterprise resource planning market size for cloud deployments, however, is projected to climb at a 25.16% CAGR to 2031. Vendors reserve the most advanced copilots for SaaS editions, so financial controllers often champion gradual module migrations even when core ledgers stay on-site.

Hybrid approaches combine local data lakes with cloud analytics sandboxes. Asian organizations in countries with stringent data-residency laws increasingly store personal data on sovereign clouds while pushing anonymized datasets to global regions for AI training. As more proofs of concept succeed, boardrooms become more comfortable staging sensitive workloads off-premises during non-business hours, accelerating broader migration waves across the AI-integrated enterprise resource planning market.

By Component: Services Surge as AI Complexity Rises

Large manufacturers use programmable logic controllers (PLCs) and supervisory control and data acquisition (SCADA) systems that generate data in proprietary formats. These systems are critical for automating and monitoring industrial processes, but the data they produce often requires translation layers to be compatible with enterprise resource planning (ERP) systems. These translation layers, frequently custom-coded, are essential for enabling predictive maintenance agents to seamlessly integrate with ERP work-order modules. However, the development and maintenance of these layers can significantly increase integration budgets, often surpassing the costs of the core software itself. Additionally, each new interface introduced into the system poses a potential cybersecurity risk, as vulnerabilities can arise from poorly secured connections or outdated protocols.

To address these challenges, low-code integration hubs have emerged as a solution to simplify connecting disparate systems. These hubs reduce the need for extensive custom coding, allowing businesses to streamline integration efforts and lower associated costs. However, while they alleviate some of the pain points, they also come with their own set of challenges, including additional licensing fees and the need for robust governance frameworks to ensure compliance and security. As a result, manufacturers must carefully evaluate the trade-offs between traditional custom-coded solutions and low-code platforms to optimize their operations while mitigating risks.

By Enterprise Size: SME Acceleration Reshapes Vendor Priorities

Large enterprises commanded 67.48% of global spend in 2025 due to multi-module footprints, but small and medium enterprises will expand at a 25.13% CAGR through 2031. Entry-level SaaS editions start at under USD 50 per user per month and include AI copilots that auto-populate purchase orders or suggest credit limit increases. As SMEs adopt these tools, vendors diversify go-to-market playbooks with self-service onboarding and marketplace extensions, broadening the AI-integrated enterprise resource planning market.

For incumbents, the challenge is avoiding one-size-fits-all interfaces. NetSuite and SAP Business ByDesign now ship vertical templates that require only parameter tweaks rather than code changes, letting a 75-employee medical-device maker go live in 90 days. Large-enterprise cycles remain slower due to multi-year budget approval and change management, yet once committed, they procure additional AI modules that amplify ticket size.

By Industry Vertical: Healthcare Overtakes Manufacturing in Growth Velocity

Manufacturing led 2025 revenue at 34.11% because discrete producers rely on ERP to coordinate multi-tier supply chains, ensuring seamless operations and minimizing inefficiencies. These systems enable manufacturers to optimize production schedules, manage inventory levels, and streamline supplier interactions. Yet healthcare’s forecast CAGR of 25.96% positions it as the fastest-growing buyer group. Hospitals are increasingly automating prior-authorization checks and leveraging predictive analytics to anticipate claims denials, thereby significantly reducing revenue cycle delays and improving cash flow management. The AI-integrated enterprise resource planning market for manufacturing continues to expand, but growth moderates as early adopters shift their focus from core modules to advanced edge analytics, which provide deeper insights and enhanced decision-making capabilities.

Retail and distribution sectors are using AI-driven demand planning tools to minimize stockouts and improve inventory turnover, ensuring customer demand is met efficiently. Meanwhile, BFSI institutions are embedding real-time fraud-detection models into settlement workflows, thereby enhancing security and reducing financial risks. Energy utilities are adopting predictive-maintenance agents that analyze IoT sensor data streams, enabling them to proactively address equipment issues and extend asset lifespans. Across sectors, the integration of embedded intelligence is transforming ERP systems from traditional back-office record-keeping tools into dynamic platforms that provide real-time operational guidance, driving efficiency and innovation in business processes.

By Business Function: Inventory and Work-Order Management Leads Functional Growth

Finance and accounting remained the highest-spending function in 2025 with 26.31% share, but inventory and work-order management will grow fastest at a 25.76% CAGR. IoT sensors close work orders automatically when machines signal task completion, and demand-forecasting agents suggest replenishment quantities before safety stocks are breached. As predictive quality models mature, manufacturers expect double-digit defect reductions without new capital equipment, enlarging the AI-integrated enterprise resource planning market.

Human-resource modules integrate skills-matching AI that recommends personalized upskilling paths, helping organizations reduce voluntary attrition by aligning employee growth with business needs. These modules also provide real-time insights into workforce trends, enabling better decision-making for talent management. Similarly, customer-relationship modules embed advanced sentiment analysis tools that identify at-risk accounts by analyzing customer interactions and feedback. This triggers proactive outreach strategies, improving customer retention and satisfaction rates. The functional boundaries between these modules are increasingly overlapping, as a single AI model can now process and analyze diverse datasets, including HR leave trends, supplier lead times, and e-commerce traffic. This integration allows businesses to dynamically recalculate production plans on an hourly basis, ensuring operational efficiency and responsiveness to changing market demands.

Geography Analysis

North America accounted for 37.89% of 2025 revenue, driven by public-sector modernizations and aggressive cloud migrations across retail and healthcare. United States federal programs alone represent multi-billion-dollar deals that span a decade. Canadian cloud-first procurement rules further expand the addressable AI-integrated enterprise resource planning market and fuel consulting engagements that localize data-residency controls. Mexico’s nearshoring boom entices automotive suppliers to adopt two-tier architectures linking local plants with U.S. headquarters.

Asia-Pacific is set to record a 25.56% CAGR from 2026-2031, the fastest pace worldwide. Japanese subsidies help small manufacturers offset license fees, Indonesian data-localization laws push global vendors to open domestic regions, and Indian tax-digitization mandates accelerate mid-market upgrades. Chinese regulations require in-country data centers, steering deals to joint ventures between global publishers and domestic hyperscalers. Australia and South Korea emphasize cybersecurity and disaster recovery certifications, further expanding regional budgets.

Europe grows more slowly because fragmented compliance rules prolong decision cycles. The United Kingdom’s multi-department SAP migration illustrates the complexity of cross-agency programs. German manufacturers add AI agents to track carbon footprints in line with new border-adjustment mechanisms, while French health systems adopt cloud ERP only after local hosting becomes available. Spain and Italy accelerate e-invoicing upgrades, and the Nordics emphasize green-data-center sourcing. South America, the Middle East, and Africa collectively represent a smaller but fast-closing gap, especially where governments introduce real-time e-invoice mandates that require embedded tax logic.

Competitive Landscape

Five global vendors, SAP, Oracle, Microsoft, Workday, and Infor, control roughly 60% of worldwide revenue, giving the AI-integrated enterprise resource planning market a moderate concentration. Each expands through vertical clouds that bundle pre-trained models, curated data sets, and partner ecosystems tailored to manufacturing, healthcare, or government. Oracle markets autonomous finance agents, SAP ships Joule natural-language copilots, and Microsoft leverages Power Platform for citizen-developer extensions.

Mid-market challengers such as Acumatica, Zoho, Odoo, and Sage pursue open APIs and modular pricing. Their agility resonates with SMEs that demand quick time-to-value and avoid long contracts. Epicor’s 2025 acquisition spree adds depth in building-materials distribution, while IFS, QAD, and Plex refresh manufacturing suites with embedded quality-inspection agents. Patent filings for explainable AI, federated learning, and anomaly detection rise sharply as vendors defend intellectual property.

Strategic alliances multiply, SAP and Accenture invest in industry accelerators, Oracle partners with Fujitsu and NTT Data for local-language deployments, and Infor teams with Siemens to ingest factory-floor IoT streams. Low-code platforms OutSystems and Mendix integrate connectors that feed custom apps back into ERP cores, blurring lines between packaged software and bespoke development. Subscription-pricing models evolve toward usage-based tiers that meter AI-inference calls, introducing new optimization levers for CIOs.

AI-Integrated Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Workday, Inc.

Infor, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Oracle released autonomous finance agents for Fusion Cloud ERP that auto-reconcile invoices and score supplier risk, claiming a 40-50% reduction in manual tasks.

- January 2026: SAP and Accenture announced a USD 1.5 billion program to co-develop industry AI accelerators for manufacturing, retail, and healthcare clients.

- December 2025: Microsoft enhanced Dynamics 365 Copilot to generate sales quotes and upsell recommendations, driving 22% year-over-year growth in cloud revenue.

- November 2025: Workday finalized its USD 1.8 billion purchase of Evisort, embedding contract-intelligence AI into procurement and finance workflows.

Global AI-Integrated Enterprise Resource Planning Market Report Scope

The AI-Integrated Enterprise Resource Planning (ERP) market refers to ERP solutions and associated services that embed artificial intelligence (AI) capabilities to automate, optimize, and enhance business processes across organizations. AI integration enables predictive analytics, intelligent automation, real-time decision-making, and personalized insights within ERP suites, helping enterprises improve operational efficiency, reduce costs, and enhance customer and employee experiences.

The AI-Integrated Enterprise Resource Planning Market Report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Component (Software, and Services), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, Healthcare, Retail and Distribution, IT and Telecom, Government and Utilities, and Other Industry Verticals), Business Function (Finance and Accounting, Human Resource Management, Supply Chain and Logistics, Customer Relationship Management, Inventory and Work Order Management, and Other Business Functions), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Software |

| Services |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| BFSI |

| Healthcare |

| Retail and Distribution |

| IT and Telecom |

| Government and Utilities |

| Other Industry Verticals |

| Finance and Accounting |

| Human Resource Management |

| Supply Chain and Logistics |

| Customer Relationship Management |

| Inventory and Work Order Management |

| Other Business Functions |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| Saudi Arabia | ||

| Rest of Middle East | ||

| South Africa | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Component | Software | ||

| Services | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Industry Vertical | Manufacturing | ||

| BFSI | |||

| Healthcare | |||

| Retail and Distribution | |||

| IT and Telecom | |||

| Government and Utilities | |||

| Other Industry Verticals | |||

| By Business Function | Finance and Accounting | ||

| Human Resource Management | |||

| Supply Chain and Logistics | |||

| Customer Relationship Management | |||

| Inventory and Work Order Management | |||

| Other Business Functions | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| Saudi Arabia | |||

| Rest of Middle East | |||

| South Africa | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving rapid cloud adoption of AI-enabled ERP platforms?

Pre-trained intelligence agents embedded in SaaS editions cut deployment times to under nine months and eliminate large capital expenditures, making cloud attractive across company sizes.

Which industry is projected to grow fastest in adopting AI-integrated ERP?

Healthcare is forecast to expand at a 25.96% CAGR through 2031 as hospitals automate revenue-cycle tasks and meet interoperability mandates.

How are small and medium enterprises benefiting from AI-ERP?

Low monthly subscriptions include copilots that automate purchase orders and cash-flow forecasts, reducing administrative overhead and providing enterprise-grade insight without large IT teams.

Why do on-premise deployments still dominate revenue?

Regulated sectors and manufacturers retain sensitive data and latency-critical workflows on site, giving on-premise solutions 72.13% market share in 2025 despite cloud momentum.

What is the main restraint on AI-ERP expansion in financial services?

Strict compliance frameworks such as SOX require explainable audit trails for machine-generated journal entries, slowing full automation until governance tools mature.

How concentrated is vendor competition?

The top five publishers account for about 60% of global revenue, indicating moderate concentration with ample opportunity for regional and vertical specialists.

Page last updated on: