Procurement Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

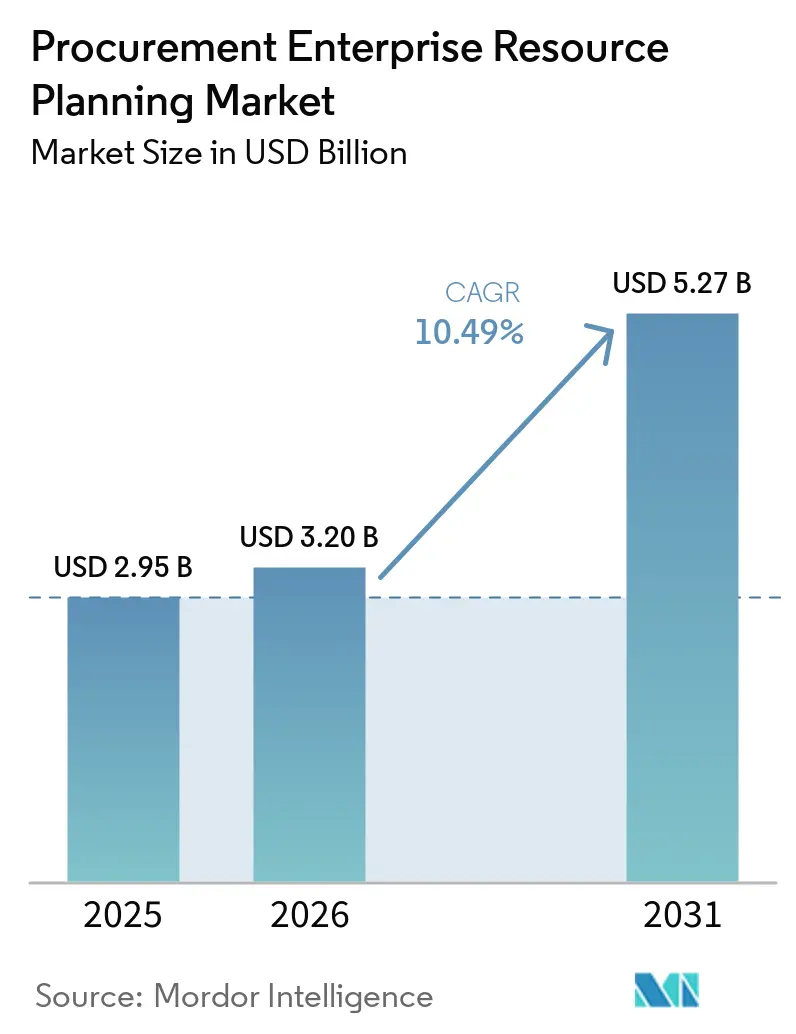

| Market Size (2026) | USD 3.20 Billion |

| Market Size (2031) | USD 5.27 Billion |

| Growth Rate (2026 - 2031) | 10.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Procurement Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Procurement Enterprise Resource Planning(ERP) market size is projected to be USD 3.20 billion in 2026 and reach USD 5.27 billion by 2031, growing at a CAGR of 10.49% over 2026-2031. Enterprises are prioritizing integrated source-to-settle platforms that replace manual requisitions, embed artificial intelligence for real-time spend visibility, and automate supplier-risk scoring. Cloud deployment dominates because subscription pricing avoids large capital outlays, accelerates rollout across distributed operations, and simplifies quarterly feature upgrades. Contract Lifecycle Management is advancing faster than traditional Procure-to-Pay modules because automated obligation tracking prevents value leakage at renewals, and AI models now extract key terms from legacy PDFs in seconds. On the demand side, small and medium enterprises are embracing low-code procurement suites that shorten implementation from months to weeks, while large enterprises continue to consolidate point solutions into unified data models that enforce governance across every subsidiary. Agentic bots and tokenized payment rails are further transforming the Procurement ERP market by compressing sourcing cycle time and enabling real-time cross-border settlement.

Key Report Takeaways

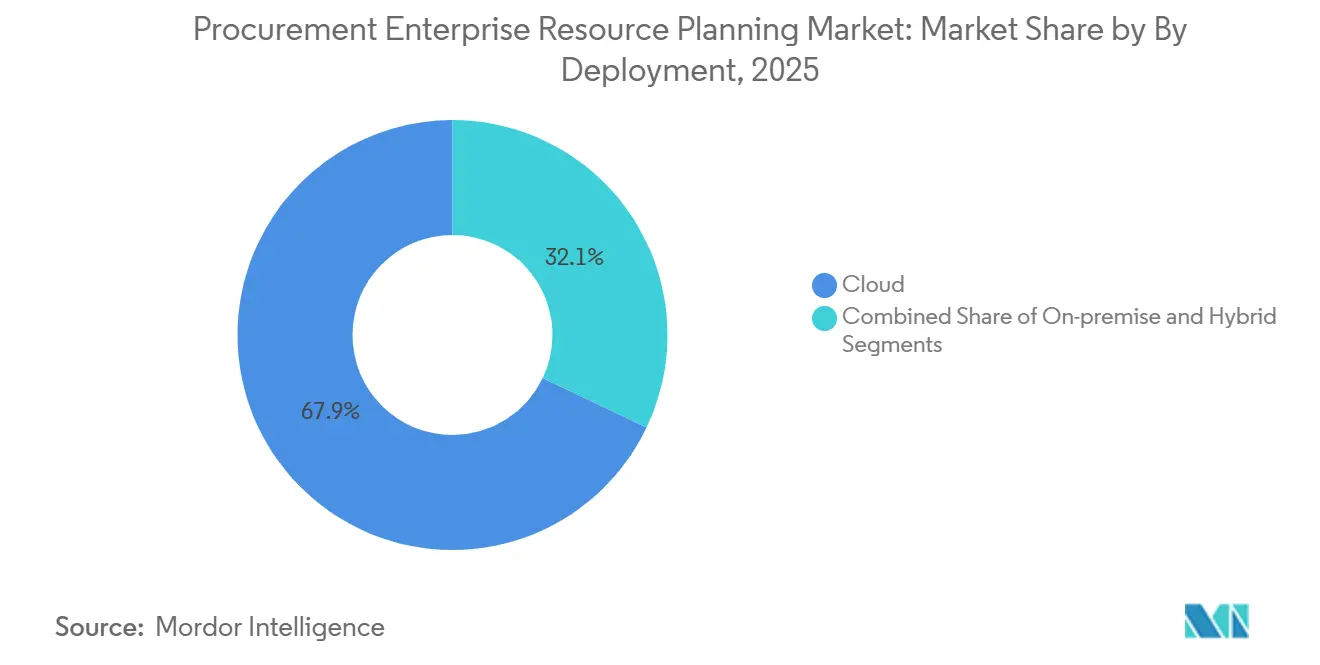

- By deployment mode, cloud solutions captured 67.92% of the Procurement ERP market revenue share in 2025, while hybrid deployments are forecast to expand at a 10.81% CAGR through 2031.

- By module, Procure-to-Pay accounted for 55.12% of the Procurement ERP market in 2025, yet Contract Lifecycle Management is projected to grow at a 11.01% CAGR over 2026-2031.

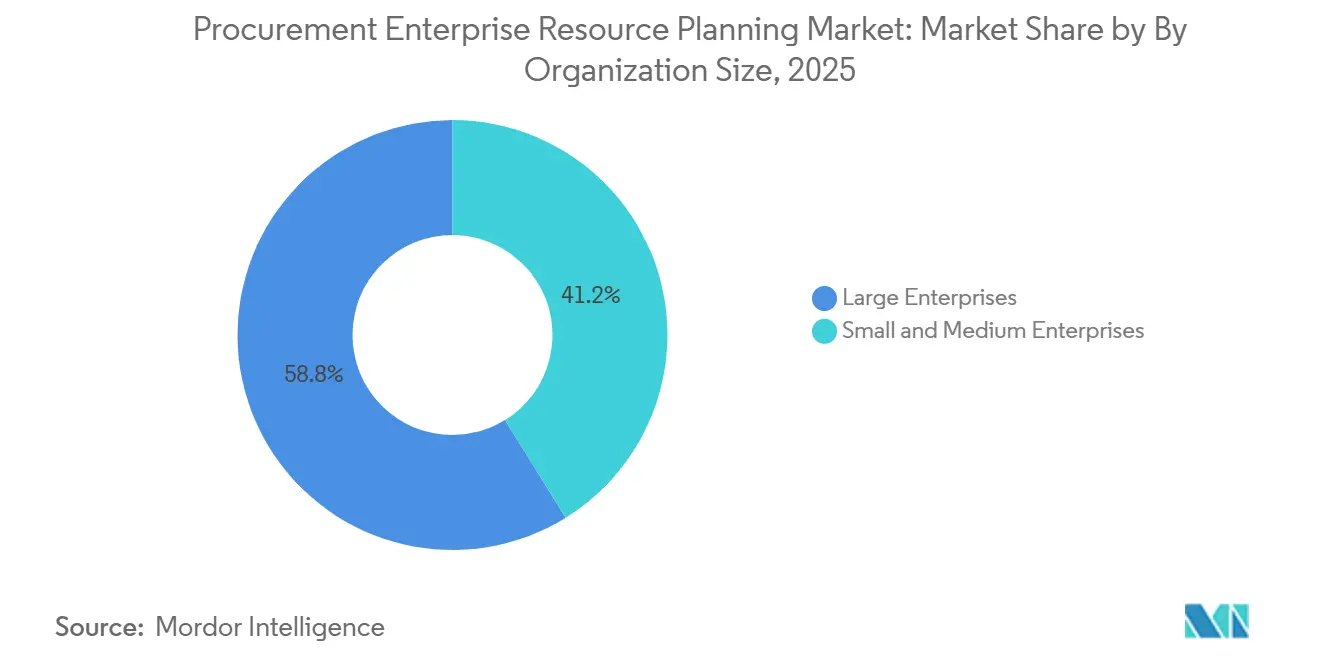

- By organization size, large enterprises accounted for 58.82% of 2025 spending, whereas small and medium enterprises are expected to record a 10.50% CAGR to 2031.

- By end-user industry, retail and e-commerce led with 20.12% revenue share in 2025, while healthcare and pharmaceutical procurement are advancing at a 11.79% CAGR to 2031.

- By geography, North America held 33.64% of the Procurement ERP market share in 2025, and Asia-Pacific is forecast to expand at a 10.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Procurement Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of Cloud-Based Procurement Suites | +2.80% | Global, North America and Europe | Medium term (2–4 years) |

| Integration of AI and ML for Spend Analytics and Supplier Risk Scoring | +2.30% | Global, North America and Asia-Pacific | Medium term (2–4 years) |

| Rising Demand for End-to-End Source-to-Pay Automation Among Large Enterprises | +1.90% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Increasing Regulatory Emphasis on Supply-Chain Transparency and ESG Compliance | +1.60% | Europe and North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Cross-Border Tokenized Payment Rails Enabling Real-Time Supplier Settlement | +0.90% | Global trade corridors | Long term (≥ 4 years) |

| Agentic Procurement Bots Reducing Sourcing Cycle Time in Mid-Market Firms | +1.00% | North America, Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Cloud-Based Procurement Suites

Cloud deployment frees enterprises from hardware refresh cycles and supports elastic scaling during demand spikes. Subscription economics cut upfront license costs, making advanced capabilities accessible to mid-market buyers. Multi-tenant architectures deliver quarterly AI enhancements without disruptive upgrades, and industry examples show 40% reductions in cycle time after migrating multiple legacy systems. Seasonal sectors benefit from cloud elasticity, which curbs overprovisioned compute during off-peak months, improving the total cost of ownership.

Integration of AI and ML for Spend Analytics and Supplier Risk Scoring

Machine-learning engines mine purchase orders, delivery performance, and external risk data to generate dynamic supplier scorecards. Early adopters report considerable cost savings in the first year after consolidating tail spend. Natural-language processing automatically extracts payment terms and penalty clauses, creating centralized obligation calendars that trigger proactive renegotiations. Agentic AI routinely drafts low-value purchase orders and routes approvals, allowing category managers to focus on strategic sourcing.

Rising Demand for End-to-End Source-to-Pay Automation Among Large Enterprises

Unified data models now link supplier negotiations directly to downstream invoice matching, allowing finance teams to reconcile accruals in real time. Real-time visibility also enforces preferred-supplier policies automatically, stopping off-contract purchases before approval. Manufacturers synchronize procurement with production schedules, triggering material orders when inventory drops below safety stock. Regulatory audits further spur adoption because complete digital trails demonstrate compliance with anti-corruption and conflict-mineral rules.

Increasing Regulatory Emphasis on Supply-Chain Transparency and ESG Compliance

Directives in the European Union and climate-disclosure rules in the United States require companies to collect supplier-level carbon and labor-practice data.[1]European Commission, “Corporate Sustainability Due Diligence Directive,” ec.europa.eu Procurement ERP vendors are embedding third-party ESG feeds so buyers can filter suppliers by carbon intensity or diversity credentials at the RFP stage. Healthcare and pharmaceutical firms must now verify that active ingredients are sourced from certified facilities, driving higher demand for traceable procurement workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy ERP Integration Complexity and High Migration Costs | -1.40% | Global, acute in mature ERP regions | Medium term (2–4 years) |

| Persistent Data Security and Privacy Concerns in Cloud Deployments | -1.10% | Global, heightened in Europe and regulated sectors | Medium term (2–4 years) |

| Shortage of Procurement-Tech Talent to Configure AI Workflows | -0.80% | Global, tight labor markets | Short term (≤ 2 years) |

| Algorithmic Bias Risks in AI-Driven Supplier Selection Engines | -0.60% | Global, regulatory scrutiny in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy ERP Integration Complexity and High Migration Costs

Decades-old systems store procurement data in proprietary formats, forcing costly custom pipelines that can consume 40% of the budget and extend cutover beyond 18 months. Duplicate supplier records and bespoke workflows must be cleansed or rebuilt, while just-in-time manufacturers fear downtime penalties during transition. Those factors delay cloud adoption and slow the overall growth of the Procurement ERP market.

Persistent Data Security and Privacy Concerns in Cloud Deployments

Multi-tenant environments pose confidentiality risks for sensitive supplier pricing data. Regulations such as GDPR require regional data centers and encryption that meets strict cross-border transfer rules.[2]GDPR, “GDPR Compliance Framework,” gdpr.eu High-profile breaches in 2024 exposed purchase-order volumes, highlighting reputational damage. Regulated industries often deploy hybrid models to keep critical workflows on-premise, reducing cloud benefits and dampening platform uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Adoption Drives Market Expansion

Cloud-based solutions commanded 67.92% of the Procurement ERP market share in 2025. Buyers are shifting to subscription models that convert capital expenses into predictable operating expenses and accelerate rollout across subsidiaries. Vendors now bundle AI-powered spend dashboards and collaboration tools that depend on always-connected architectures, reinforcing cloud preference. On-premises deployments persist where national security or sovereign data rules prohibit external hosting. Hybrid topologies, offered under programs like RISE with SAP, allow gradual module migration, mitigating disruption risk and supporting compliance.

Hybrid models appeal to companies balancing strict audit mandates with the need for scalable innovation. Pharmaceutical firms often keep ingredient sourcing on-premises while moving indirect procurement to the cloud, while manufacturers process latency-sensitive data at local edge nodes before synchronization. Vendors that support seamless data flow across environments position themselves for additional growth in the Procurement ERP market.

By Module: Contract Lifecycle Management Gains Momentum

Procure-to-Pay retained 55.12% of 2025 revenue thanks to its foundational role in automating requisition-to-payment processes. However, Contract Lifecycle Management is growing at a 11.01% CAGR because AI text-extraction prevents missed renewals and uncaptured escalators. Modern platforms link CLM directly to requisition creation, turning negotiated terms into executable purchase orders without manual re-keying, which protects negotiated savings.

Spend-analysis engines forecast category demand and identify tail-spend consolidation, while supplier-management portals centralize third-party risk scores. Source-to-Contract suites now digitize the entire RFP life cycle, capturing auditable records that meet internal control requirements. This modular breadth enables enterprises to scale into strategic functionality as the Procurement ERP market maturity increases.

By Organization Size: SMEs Narrow the Digital Divide

Large organizations contributed 58.82% of 2025 spending because they must harmonize supplier data and enforce global governance. Their platforms integrate with warehouse and transportation systems, handling millions of purchase orders each year. Small and medium enterprises are forecast to grow at a 10.50% CAGR as vendors price modules by transaction volume and offer low-code packages that eliminate the need for external consultants.

SMEs thus access analytics and compliance tools once limited to Fortune-level budgets, improving competitiveness and supplier leverage. Industry-specific templates reduce complexity, and embedded marketplaces let SMEs transact with vetted suppliers instantly, accelerating Procurement ERP market penetration in the mid-tier.

By End-User Industry: Regulation Spurs Healthcare Uptake

Retail and e-commerce led 2025 adoption with 20.12% share, using ERP-linked inventory data to automate replenishment during flash sales and holiday peaks. Healthcare and pharmaceutical firms are advancing at a 11.79% CAGR due to serialization mandates that require digital traceability from ingredient to patient. ERP systems now automatically capture lot numbers and chain-of-custody data, ensuring regulatory compliance.

Manufacturers synchronize material orders with sensor-driven production lines, while BFSI sectors emphasize robust audit trails for anti-money-laundering compliance. Public-sector bodies use configurable rules to meet tender transparency laws, and energy companies tie procurement to asset-maintenance schedules, ensuring critical spares are available when turbines or transformers require service, broadening the Procurement ERP market reach across verticals.

Geography Analysis

North America accounted for 33.64% of 2025 revenue, driven by mature ERP ecosystems and stringent transparency rules that compelled unified procurement processes. Climate-disclosure mandates drive the adoption of platforms that record supplier-level carbon emissions, and Canadian forced-labor laws require annual due diligence reports captured by ERP audit trails.[3]FDA, “Drug Supply Chain Security Act Requirements,” fda.gov Mexico’s nearshoring wave further stimulates cross-border procurement suites that integrate customs documentation and quality metrics.

Asia-Pacific is the fastest-growing region at a 10.76% CAGR. Chinese and Indian manufacturers digitize procurement to meet export standards and reduce cycle times, while Japanese firms embed supplier performance into Industry 4.0 quality dashboards. Emerging Southeast Asian economies deploy multi-language, tax-compliant procurement portals to support rising foreign investment, and tokenized payment rails ease supplier settlement across fragmented banking networks.

Europe’s market is shaped by directives mandating human rights and environmental assessments. German automotive giants manage thousands of tier-two suppliers on ERP platforms to track ESG metrics, and United Kingdom companies must reconcile divergent UK and EU compliance after Brexit.[4]Coupa, “European Automotive Manufacturer Partnership Announcement,” coupa.com France’s anti-corruption law drives conflict-of-interest checks at supplier onboarding. Procurement modernization is also accelerating in South America, the Middle East, and Africa as governments adopt e-tender portals and multinationals extend global suites to local subsidiaries, broadening the Procurement ERP market footprint.

Competitive Landscape

The Procurement ERP market is moderately concentrated. SAP, Oracle, and Workday leverage broad ERP footprints to cross-sell procurement modules, while specialists such as Coupa, Jaggaer, and Ivalua differentiate through rapid innovation and vertical depth. Mid-tier vendors Basware, Zycus, and GEP target niche workflows with pre-configured templates that shorten deployment.

AI integration is the primary battleground, with vendors embedding generative models for contract summarization, RFP drafting, and conversational spend queries. Partnerships like SAP and Microsoft integrate large language models to recommend savings initiatives. Blockchain features, including tokenized payments and supplier credential verification, are emerging differentiators that challenge legacy architectures.

Marketplaces embedded within ERP suites create additional revenue streams from transaction fees and supplier advertising, intensifying rivalry. Disruptors focusing on autonomous procurement execution pressure incumbents to modernize code bases dating back decades. Vendors offering flexible deployment, robust ESG analytics, and integrated financing options are best positioned to capture incremental Procurement ERP market share as global digital maturity rises.

Procurement Enterprise Resource Planning Industry Leaders

SAP SE

Coupa Software Incorporated

Oracle Corporation

GEP Worldwide LLC

Jaggaer LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SAP completed the first live deployment of generative AI-assisted RFP drafting for a European aerospace supplier, reducing document preparation time by 60%.

- February 2025: Workday reported that Fairview Health Services consolidated 14 legacy systems onto Workday Procurement, cutting requisition-to-order cycle time by 40%.

- January 2025: Oracle launched Fusion Cloud Procurement 26A with AI contract summarization that highlights renewal dates and penalty clauses.

- December 2024: SAP debuted its next-generation Ariba cloud suite with predictive analytics that flag maverick buying before discounts erode.

Global Procurement Enterprise Resource Planning Market Report Scope

The Procurement Enterprise Resource Planning (ERP) market comprises integrated software solutions that streamline and optimize an organization’s sourcing, purchasing, supplier management, and spend control processes. These systems enhance visibility, compliance, cost efficiency, and supplier collaboration across the procurement lifecycle, enabling organizations to transition from transactional purchasing to strategic sourcing and spend management.

The Procurement Enterprise Resource Planning Report is segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Module (Procure-to-Pay, Source-to-Contract, Contract Lifecycle Management, Spend Analysis, Supplier Management, and Other Modules), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Manufacturing, Retail and E-commerce, Healthcare and Pharmaceutical, Banking Financial Services and Insurance, Information Technology and Telecom, Government and Public Sector, Energy and Utilities, and Other Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa).

| Cloud |

| On-Premise |

| Hybrid |

| Procure-to-Pay (P2P) |

| Source-to-Contract (S2C) |

| Contract Lifecycle Management (CLM) |

| Spend Analysis |

| Supplier Management |

| Other Modules |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Manufacturing |

| Retail and E-commerce |

| Healthcare and Pharmaceutical |

| Banking Financial Services and Insurance (BFSI) |

| Information Technology and Telecom |

| Government and Public Sector |

| Energy and Utilities |

| Other Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Deployment Mode | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Module | Procure-to-Pay (P2P) | |

| Source-to-Contract (S2C) | ||

| Contract Lifecycle Management (CLM) | ||

| Spend Analysis | ||

| Supplier Management | ||

| Other Modules | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-User Industry | Manufacturing | |

| Retail and E-commerce | ||

| Healthcare and Pharmaceutical | ||

| Banking Financial Services and Insurance (BFSI) | ||

| Information Technology and Telecom | ||

| Government and Public Sector | ||

| Energy and Utilities | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Procurement ERP market by 2031?

The market is forecast to reach USD 5.27 billion by 2031.

Which deployment mode is growing fastest within Procurement ERP?

Cloud solutions are expanding at a 9.81% CAGR because subscription pricing and quarterly AI upgrades drive adoption.

Why is Contract Lifecycle Management gaining traction?

CLM prevents value leakage by automating obligation tracking, fueling a 9.01% CAGR between 2026-2031.

Which region is expected to record the highest growth rate?

Asia-Pacific is projected to grow at 10.50% annually through 2031 as manufacturers digitize procurement.

How are mid-market firms shortening sourcing cycles?

Agentic bots automate low-value purchases, cutting cycle time from 8 days to 36 hours and freeing staff for strategic tasks.

What regulatory trends influence Procurement ERP investments?

ESG reporting mandates and climate-disclosure rules require platforms that capture supplier-level carbon, labor and governance data.

Page last updated on: