Project-Based Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.80 Billion |

| Market Size (2031) | USD 4.65 Billion |

| Growth Rate (2026 - 2031) | 10.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Project-Based Enterprise Resource Planning Market Analysis by Mordor Intelligence

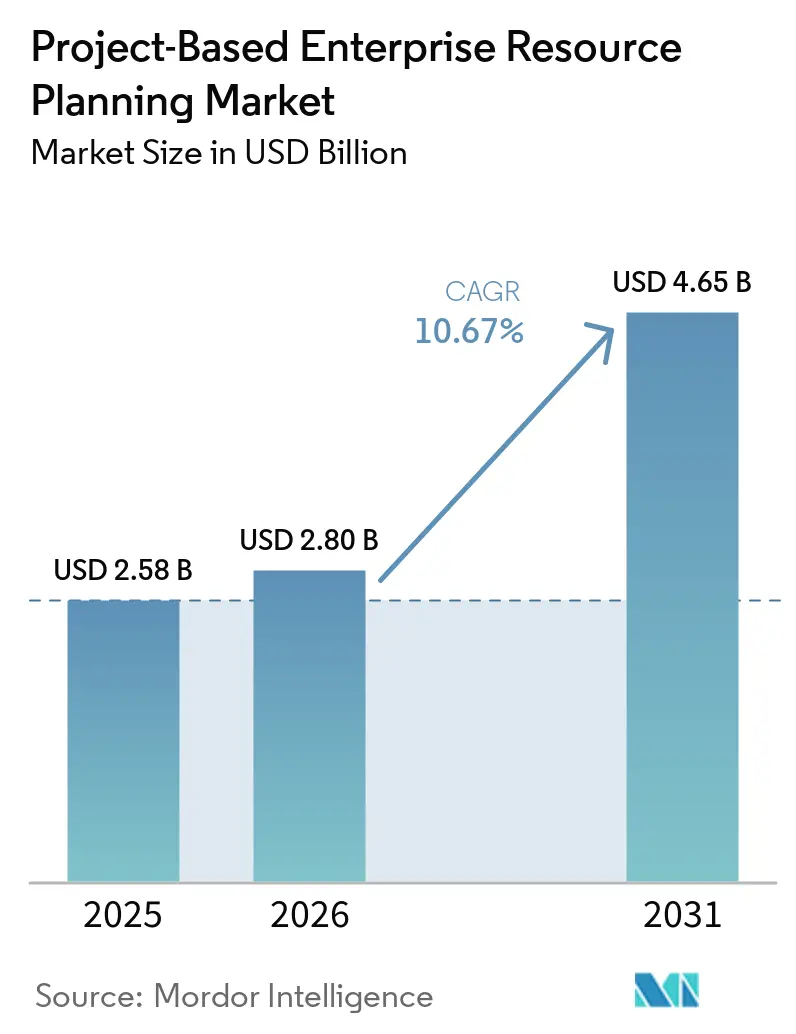

The Project-Based Enterprise Resource Planning (ERP) market size is projected to expand from USD 2.58 billion in 2025 and USD 2.80 billion in 2026 to USD 4.65 billion by 2031, registering a CAGR of 10.67% during 2026-2031. Demand is accelerating as project-centric businesses replace legacy finance and scheduling tools with unified platforms that offer real-time cost visibility, mobile collaboration, and embedded artificial intelligence. Cloud and hybrid deployments already account for more than 70% of new implementations, reflecting buyers’ preference for rapid upgrades and lower infrastructure overhead. Large enterprises continue to anchor spending, yet the overall Project-Based ERP market is increasingly influenced by small and medium enterprises that benefit from subscription pricing and pre-configured templates. Vendors that combine project accounting, resource planning, and compliance reporting in a single environment are capturing wallet share as organizations seek shorter implementation cycles and lower total cost of ownership.

Key Report Takeaways

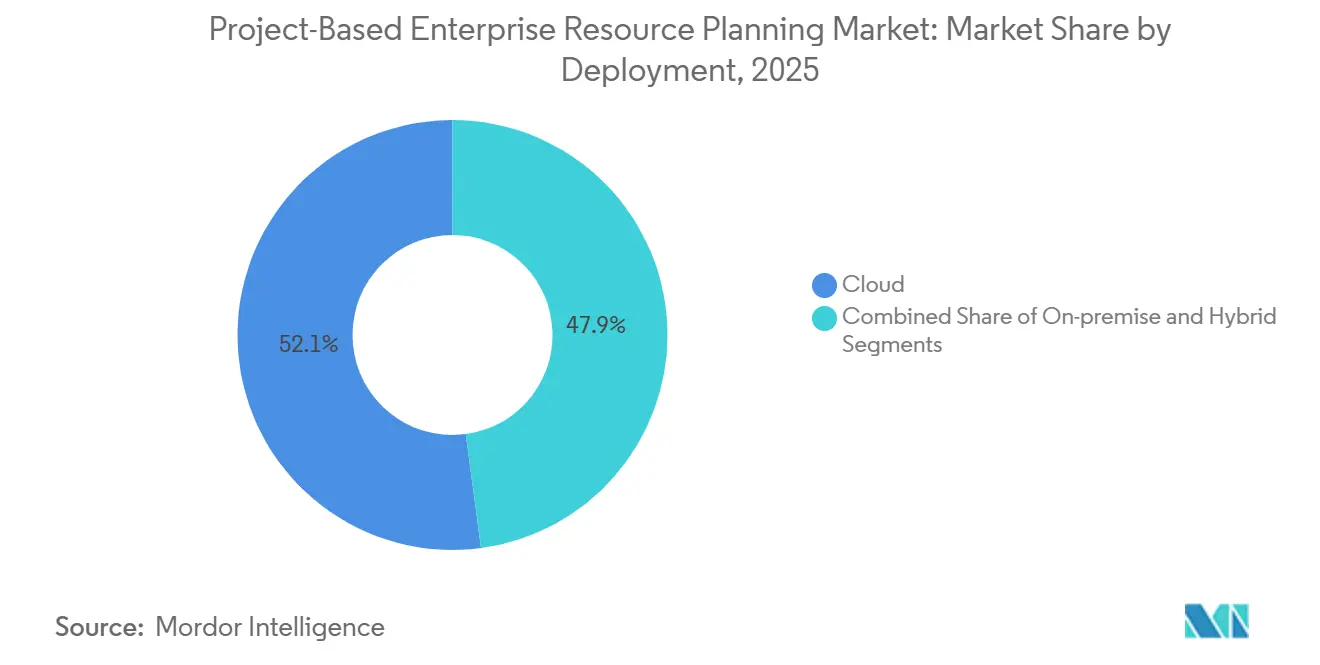

- By deployment mode, cloud and SaaS solutions commanded 52.12% of the Project-Based ERP market share in 2025, while hybrid architectures are forecast to expand at a 17.80% CAGR through 2031.

- By organization size, large enterprises held 60.29% revenue share in 2025, whereas small and medium enterprises are advancing at a 15.60% CAGR to 2031.

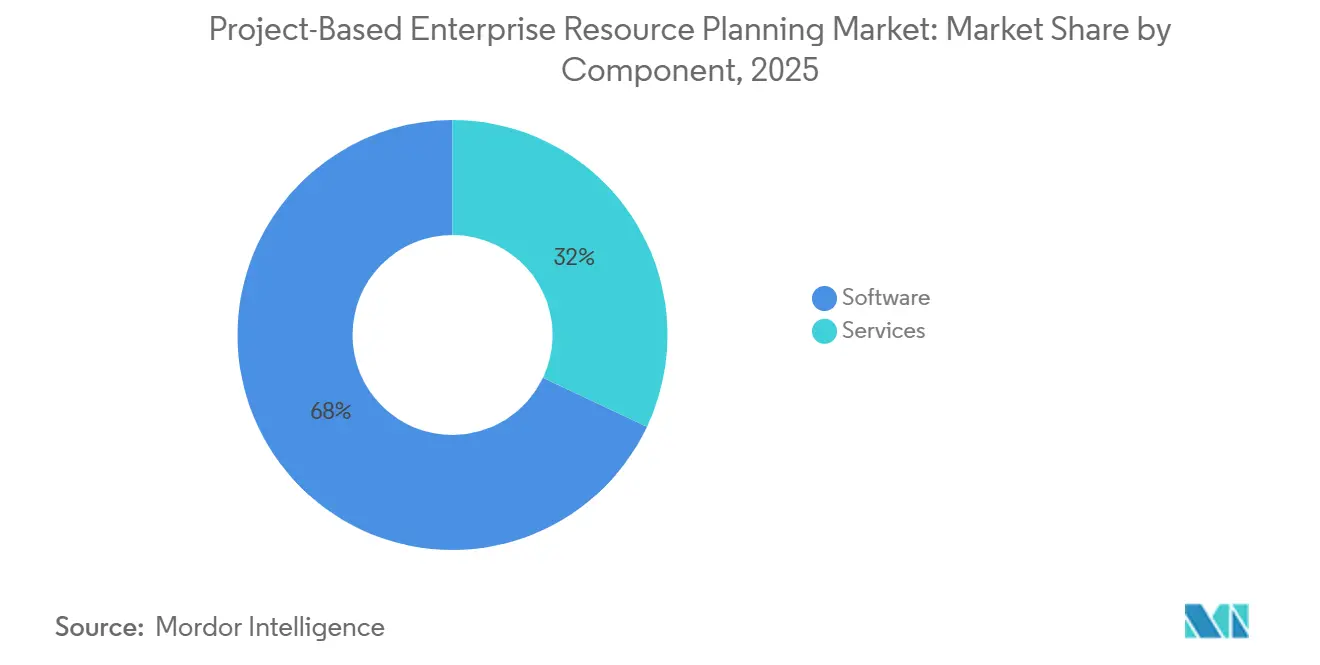

- By component, software accounted for 67.98% of the Project-Based ERP market size in 2025, and services are growing at a 14.90% CAGR through 2031.

- By end-user industry, construction and engineering led with 24.65% revenue share in 2025, while healthcare is projected to post an 18.40% CAGR to 2031.

- By geography, North America dominated with 34.26% share of the Project-Based ERP market in 2025, and Asia-Pacific is the fastest-growing region at 13.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Project-Based Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of Remote Work and Distributed Project Teams | +2.3% | Global, North America and Europe | Short term (≤ 2 years) |

| Transition to SaaS and Subscription-Based Pricing Models | +3.1% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Integration of AI-Driven Project Analytics | +2.8% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Growing Complexity of Compliance in Project Accounting | +1.6% | Europe, North America, Middle East | Long term (≥ 4 years) |

| Demand for Unified Bid-to-Cash Visibility Across Projects | +2.4% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Rising Investment in Public Infrastructure Megaprojects | +1.9% | Asia-Pacific, Middle East, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption Of Remote Work And Distributed Project Teams

Remote and hybrid work models became permanent in 2025, forcing companies to retire on-premises systems that rely on VPN access and desktop clients. Cloud-native Project-Based ERP market platforms now ship with mobile interfaces that let field engineers submit timecards and approve change orders from any device, cutting approval cycles by 40% in aerospace and professional-services pilots.[1]Microsoft Corp., “Dynamics 365 Project Operations and Teams Integration Cuts Approval Times,” microsoft.com Billable utilization climbs when time entries are captured within hours, protecting margins that would otherwise be eroded by manual delays. Buyers increasingly prefer vendors that embed chat, document management, and workflow approvals directly inside the ERP rather than through third-party tools. This consolidation simplifies user training and reduces integration overhead, making remote collaboration a key purchase criterion. As a result, solution providers that optimize experiences for distributed teams are winning competitive bids.

Transition To SaaS And Subscription-Based Pricing Models

The Project-Based ERP market is shifting decisively toward subscription contracts as vendors announce sunset dates for on-premises releases. Epicor’s January 2026 roadmap gives customers four years to migrate, a deadline that compresses decision cycles and accelerates cloud adoption.[2]Epicor Software Corp., “Epicor Announces Final On-Premises Feature Releases,” epicor.com SaaS eliminates server hardware costs, yet it converts capital expenditure into recurring operating expense that can exceed perpetual-license amortization over long horizons. Firms that value continuous feature updates and elastic user scaling find the trade-off attractive, whereas organizations with stable headcounts must carefully evaluate lifetime subscription totals. Migration windows are pushing even risk-averse industries to accelerate data-conversion projects, reinforcing double-digit growth in cloud revenue across the Project-Based ERP market.

Integration Of AI-Driven Project Analytics

Artificial intelligence is moving from dashboards into day-to-day operations. SAP embeds generative AI in S/4HANA Finance to create narrative KPI briefings, freeing controllers from manual report preparation.[3]SAP SE, “How S/4HANA Finance Improves Working Capital and Cash Flow Forecasting,” sap.com IFS released Digital Workers that autonomously manage material replenishment, helping field-service firms reclaim technician hours valued at USD 3 million annually. Sage added Copilot features that surface late-shipment risks, reducing exception reviews by 30%. These capabilities enable managers to address cost overruns and schedule slippage proactively instead of retrospectively. Companies lagging in AI adoption risk losing bids to rivals that promise predictive delivery dates and real-time status dashboards, making AI functionality a differentiator in the Project-Based ERP market.

Growing Complexity Of Compliance In Project Accounting

Regulatory demands continue to multiply across industries. European Union Medical Device Regulation, CMS interoperability mandates in U.S. healthcare, and regional data-protection laws all require granular audit trails within project financials. Organizations must link budgets, change orders, and revenue milestones to verify adherence to ASC 606, IFRS 15, and local tax statutes. Cloud platforms with built-in compliance tooling reduce manual reconciliation and audit preparation. Vendors that provide automated document retention, electronic signature workflows, and region-specific reporting templates draw interest from highly regulated sectors, reinforcing share gains for compliance-centric offerings in the Project-Based ERP market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Switching Costs from Legacy ERP Platforms | -1.8% | Global, North America and Europe | Medium term (2-4 years) |

| Shortage of Skilled Project-ERP Implementation Specialists | -1.4% | Global, acute in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Data Security Concerns in Multi-Tenant Cloud Environments | -0.9% | Europe, North America, regulated sectors globally | Medium term (2-4 years) |

| Budget Constraints in SMEs Amid Macroeconomic Uncertainty | -1.2% | Global, South America and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Switching Costs From Legacy ERP Platforms

Migrating historical data, rebuilding custom integrations, and training users can consume 18-24 months and overrun budgets by 30% in complex carve-outs. A mid-sized engineering firm replacing a 15-year-old Deltek instance must map legacy cost codes and maintain audit trails for active contracts during cutover. NetSuite’s SuiteSuccess and Unit4’s low-code configuration help compress timelines, yet the investment hurdle deters risk-averse CFOs. Until accelerated implementation frameworks prove reliable at scale, high switching costs will temper adoption velocity in parts of the Project-Based ERP market.

Shortage Of Skilled Project-ERP Implementation Specialists

Demand for consultants with project accounting, revenue recognition, and vertical-specific expertise significantly outstrips supply. Large integrators often prioritize marquee transformations, leaving mid-market customers to compete for limited talent pools. The scarcity of skilled labor inflates day rates and stretches timelines, especially in the Asia-Pacific region, where project-based industries are expanding rapidly. Vendors respond with partner enablement programs and prebuilt accelerators to reduce customization needs, yet the skills gap remains a structural constraint on the Project-Based ERP industry’s growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Architectures Balance Control And Agility

Hybrid configurations are expanding at 17.80% CAGR through 2031 as enterprises pair private-cloud databases with public-cloud collaboration modules. Cloud installations captured 52.12% of the Project-Based ERP market share in 2025, confirming buyer confidence in vendor-managed security and automatic upgrades. A construction conglomerate might hold sensitive financials on private infrastructure but place mobile field-service and analytics workloads in public SaaS to support site engineers. The Project-Based ERP market size for on-premises deployments is shrinking as vendors limit innovation to cloud editions, yet it persists in defense and critical infrastructure accounts that require air-gapped networks.

Organizations choosing deployment models assess total cost across subscription, data egress, and integration charges versus the flexibility to scale. Microsoft’s tiered Dynamics 365 options and SAP’s RISE program encourage phased migrations that reduce operational risk. Hybrid offerings that allow incremental module shifts appeal to firms burdened by heavily customized legacy stacks. Consequently, hybrid remains the fastest-growing slice of the Project-Based ERP market as businesses seek both compliance and rapid innovation.

By Organization Size: SMEs Close The Functionality Gap

Large enterprises held a 60.29% share of the Project-Based ERP market in 2025, yet small and medium enterprises are growing at a 15.60% CAGR through 2031. Subscription pricing removes capital barriers: a 200-person architectural firm can deploy core modules for USD 50,000-100,000 in year one, a fifth of historical on-premises costs. Net at Work’s January 2026 purchase of BHE Consulting underscores integrator interest in mid-market growth. Modular licensing lets SMEs add procurement or analytics when revenue allows, aligning software expense with contract inflows.

Professional services, construction, and IT consultancies lead adoption because margins depend on real-time capture and prompt billing. Currency fluctuations and macroeconomic volatility still curb adoption in South America and Africa, but vendors that offer flexible payment terms and regionally hosted data centers are reducing barriers. As capabilities once reserved for global enterprises become accessible, SMEs will exert growing influence on functional roadmaps within the Project-Based ERP market.

By Component: Services Revenue Accelerates With Complexity

Software accounted for 67.98% of Project-Based ERP market revenue in 2025, yet services, implementation, integration, and managed support are growing at a 14.90% CAGR. A mid-tier engineering group may spend USD 150,000 on first-year licenses but USD 200,000-300,000 on consultants to map legacy project structures, build reports, and connect Salesforce opportunity data. The Project-Based ERP market size attached to services reflects the scarcity of specialized talent and the intricacy of multi-system landscapes.

Service providers bifurcate between global integrators that marshal thousands of consultants for enterprise rollouts and niche boutiques that target vertical regulations such as the U.S. Federal Acquisition Regulation. Partnerships like the March 2026 IFS-UKG alliance integrate workforce management with ERP systems to eliminate duplicate data entry, thereby shortening overall deployment time. Managed services grow as SMEs offload system monitoring and patching, enabling business units to focus on delivery rather than infrastructure maintenance.

By End-User Industry: Healthcare Outpaces Traditional Segments

Construction and engineering-led deployments accounted for 24.65% of deployments in 2025, grounded in job costing and subcontractor billing needs. However, healthcare is surging at a 18.40% CAGR because hospital expansions, clinical trials, and medical device development require granular project tracking to satisfy regulators. The Project-Based ERP market share allocated to healthcare projects is expected to expand as the European Union Medical Device Regulation and U.S. CMS rules require precise cost allocation and auditability.

Other sectors exhibit distinct needs. Professional services firms monitor utilization, aerospace contractors adhere to government cost standards, and oil and gas operators oversee decades-long capital projects. Manufacturing embraces engineer-to-order workflows that convert every sales order into a mini-project with a unique bill of materials. Government and utilities leverage ERP to align multi-year infrastructure budgets with public procurement rules. Vendors that deliver configurable industry accelerators without heavy customization costs are positioned to win cross-vertical share.

Geography Analysis

North America accounted for 34.26% of the Project-Based ERP market revenue in 2025, owing to mature ecosystems, high IT budgets, and a concentration of defense and professional services. U.S. federal agencies adopted enterprise project management software to track capital programs, while Canadian and Mexican manufacturers integrated ERP systems to coordinate nearshore supply chains. A deep bench of certified consultants and early AI experimentation helps the region maintain leadership.

Asia-Pacific is growing fastest, with a 13.70% CAGR through 2031. China’s Belt and Road projects, India’s electronic invoicing mandates, and ASEAN manufacturing expansion are fueling robust demand. Australia and New Zealand have high deployment rates in mining, and Japan is upgrading its ERP systems to support smart-factory initiatives. Talent shortages and diverse data-residency laws are driving regional cloud zones and accelerating hybrid models.

Europe balances opportunity with regulatory headwinds. GDPR, sustainability reporting, and the Medical Device Regulation elevate compliance requirements, steering buyers toward platforms with built-in audit capabilities. Germany, the United Kingdom, France, and Italy dominate spend across automotive, aerospace, and engineering. The Middle East invests in megaprojects tied to diversification agendas, seeking ERP that supports joint ventures and Islamic finance. South American growth is localized to Brazil and Argentina due to currency volatility, and Africa’s uptake is led by South Africa and Nigeria in mining and telecom despite infrastructure gaps.

Competitive Landscape

The Project-Based ERP market is moderately fragmented. Enterprise incumbents Oracle, SAP, and Microsoft command global reach and broad functionality, competing against specialists such as Deltek, IFS, and Unit4 that excel in government contracting, asset-intensive industries, and professional services. IFS’s 2025 Softeon acquisition merged warehouse execution and robotics orchestration with Industrial AI, underscoring a strategy to deliver end-to-end operational intelligence.[4]ERP Today, “IFS Completes Softeon Acquisition,” erp.today

Oracle demonstrated 83% faster invoicing after its own SAP S/4HANA deployment, evidence that vendors showcase internal wins to validate value propositions. Mid-market disruptors Acumatica and Unit4 deploy embedded payments and AI-driven planning to offer lower total cost than legacy suites. Compliance certifications such as ISO 27001 and SOC 2 are baseline requirements for regulated verticals, driving vendors to harden security and transparent incident response.

Implementation capacity shapes go-to-market: suppliers invest in low-code toolkits, partner academies, and pre-built vertical templates to mitigate consultant shortages and accelerate customer time-to-value.

Project-Based Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Deltek, Inc.

IFS AB

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: IFS and UKG formed a partnership to combine IFS ERP with UKG Pro workforce management, targeting customers that manage large project-based labor forces.

- February 2026: Sage hosted the Xperienc3 event in Granada, highlighting Sage X3 cloud enhancements, AI integrations, and mobile extensions for manufacturers and distributors.

- January 2026: Net at Work acquired BHE Consulting to bolster Sage and Acumatica implementation capacity across construction, manufacturing, and wholesale distribution.

- January 2026: Vena Solutions acquired Acterys to create a Microsoft-native orchestrated planning environment that unifies Excel-based planning with Power BI analytics.

Global Project-Based Enterprise Resource Planning Market Report Scope

The Project-Based Enterprise Resource Planning (ERP) market comprises integrated software solutions that plan, execute, and manage project-centric operations, with revenue, costs, and resources directly tied to specific projects. These systems enable organizations to streamline project accounting, resource allocation, budgeting, time tracking, and project delivery, ensuring improved visibility, cost control, and on-time project execution.

The Project-Based ERP Market Report is Segmented by Deployment Mode (On-Premise, Cloud/SaaS, Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises), Component (Software, Services), End-User Industry (Construction and Engineering, Professional Services, Aerospace and Defense, Government and Utilities, Healthcare, IT and Telecom, Manufacturing, Oil and Gas, Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa).

| On-Premise |

| Cloud/SaaS |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Software |

| Services |

| Construction and Engineering |

| Professional Services |

| Aerospace and Defense |

| Government and Utilities |

| Healthcare |

| IT and Telecom |

| Manufacturing |

| Oil and Gas |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Mode | On-Premise | |

| Cloud/SaaS | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Component | Software | |

| Services | ||

| By End-User Industry | Construction and Engineering | |

| Professional Services | ||

| Aerospace and Defense | ||

| Government and Utilities | ||

| Healthcare | ||

| IT and Telecom | ||

| Manufacturing | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will spending on project-centric ERP reach by 2031?

The Project-Based ERP market size is projected to reach USD 4.65 billion by 2031 on a 10.67% CAGR trajectory.

Which region is forecast to grow the fastest?

Asia-Pacific leads regional growth with a 13.70% CAGR driven by infrastructure investment and regulatory digitization.

What drives small and medium enterprise adoption?

Subscription pricing, pre-configured templates, and modular licensing allow SMEs to access advanced functionality without heavy capital expenditure.

Why are hybrid deployments gaining attention?

Hybrid architectures blend on-premises control for sensitive data with public-cloud agility for collaboration, expanding at 17.80% CAGR through 2031.

Which vertical will outpace others in growth?

Healthcare is expected to expand at an 18.40% CAGR as hospitals and device makers adopt ERP to meet stringent compliance mandates.

How are vendors mitigating implementation talent shortages?

Suppliers invest in partner academies, low-code configurators, and industry accelerators to reduce reliance on scarce specialized consultants.

Page last updated on: