App Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

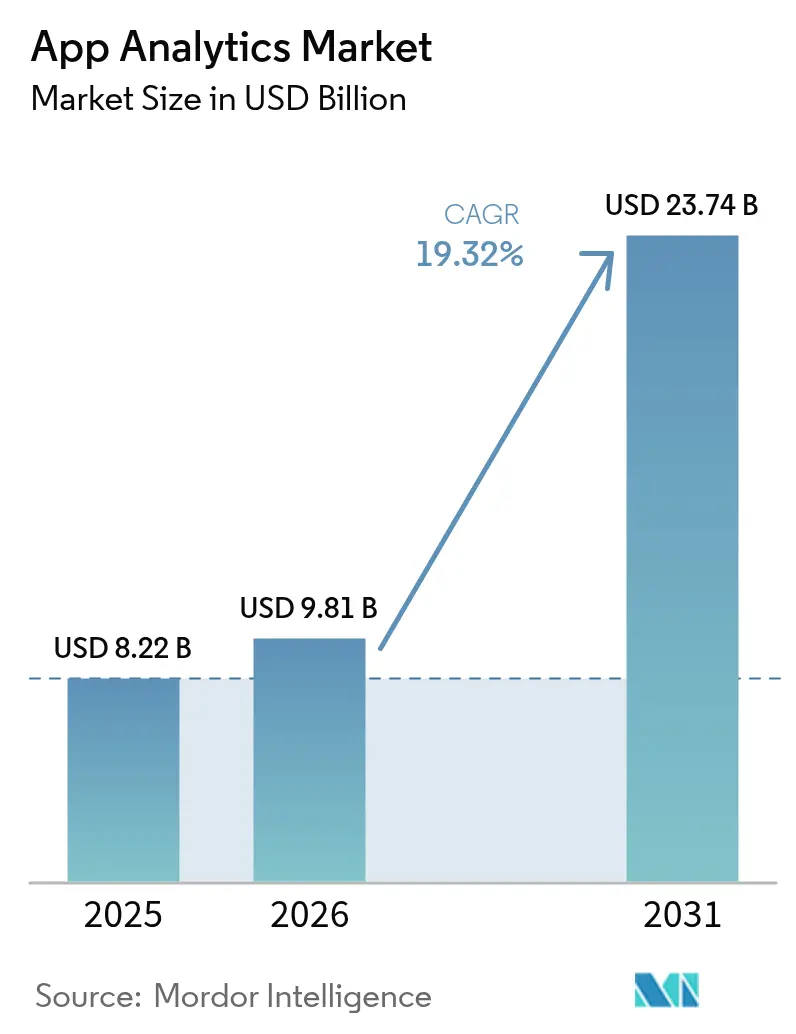

| Market Size (2026) | USD 9.81 Billion |

| Market Size (2031) | USD 23.74 Billion |

| Growth Rate (2026 - 2031) | 19.32% CAGR |

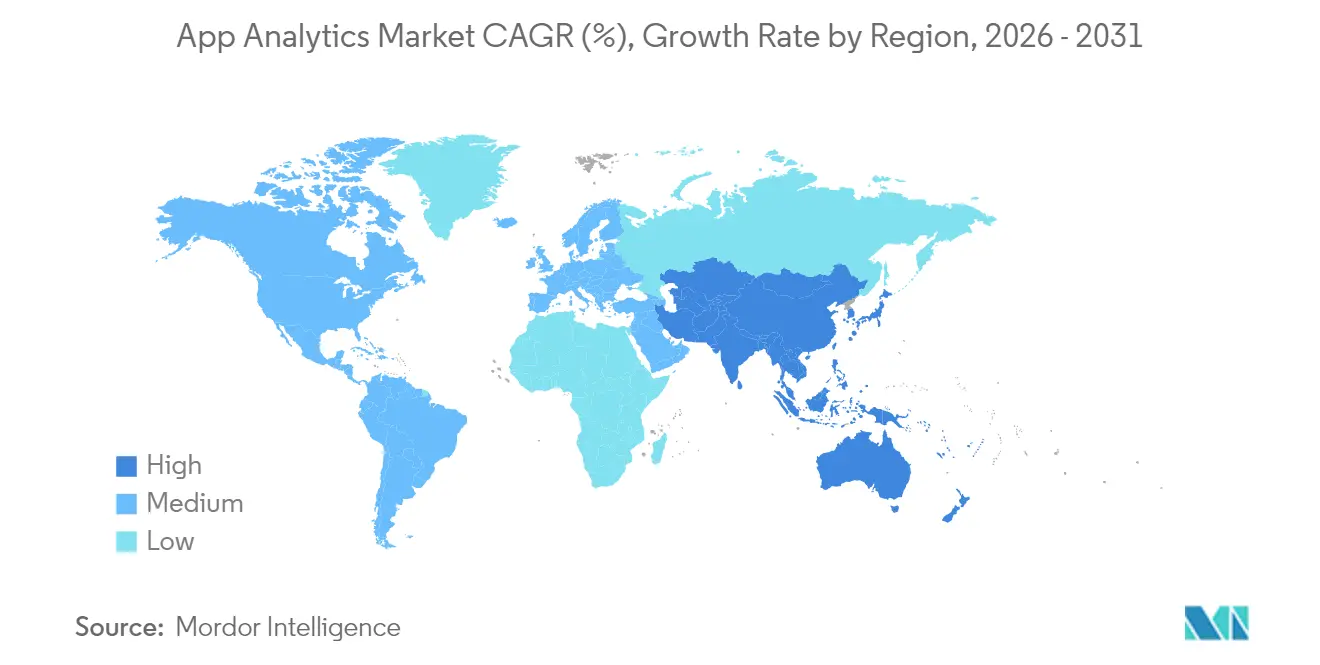

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

App Analytics Market Analysis by Mordor Intelligence

App Analytics market size in 2026 is estimated at USD 9.81 billion, growing from 2025 value of USD 8.22 billion with 2031 projections showing USD 23.74 billion, growing at 19.32% CAGR over 2026-2031. This rapid expansion is propelled by enterprises treating in-app insight platforms as mission-critical infrastructure that anchors customer experience, monetization, and compliance strategies. Accelerated 5G deployment shortens data-collection-to-decision cycles, while privacy-preserving architectures unlock user-level understanding without breaching regulations. Real-time behavioral insight now guides pricing, retention, and fraud controls across industries, prompting a wave of edge-enabled solutions that cut latency and cloud costs. Competitive intensity rises as incumbents integrate AI-driven modules and specialist vendors position privacy-first toolkits, giving CIOs a wider but more complex partner universe.

Key Report Takeaways

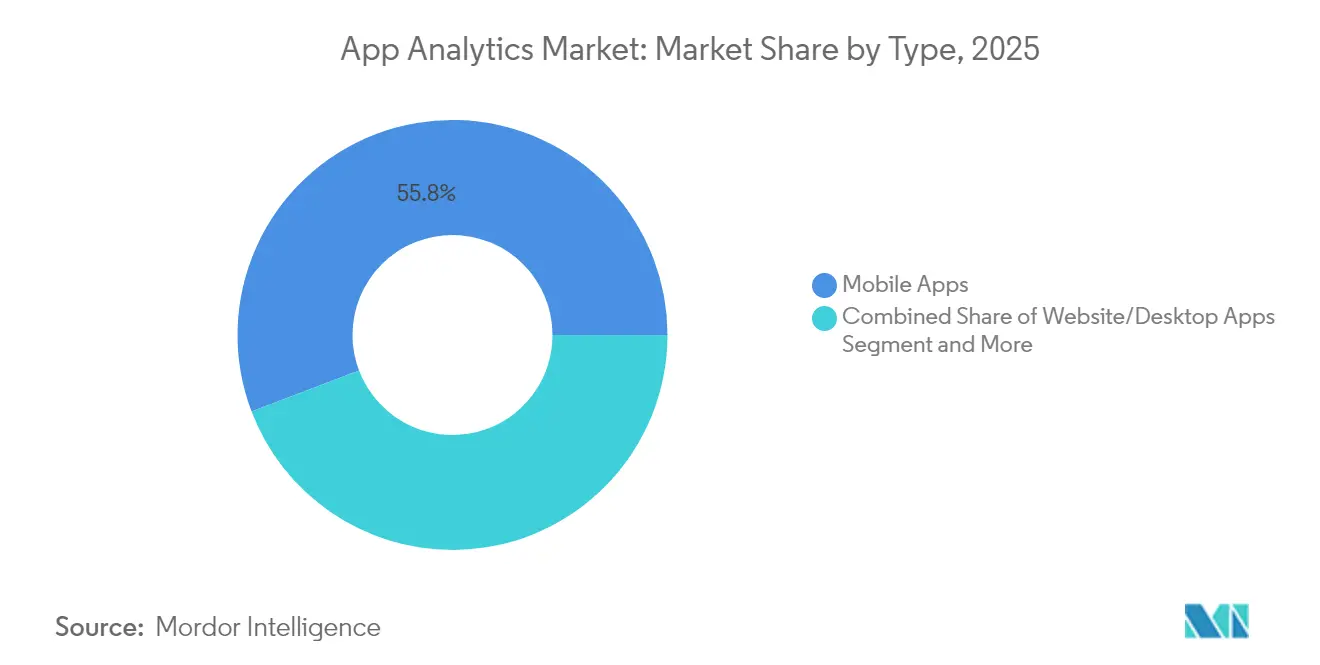

- By type, Mobile Apps led with 55.78% revenue share in 2025, while Progressive Web Apps are projected to expand at a 21.90% CAGR through 2031.

- By application, Marketing and Advertising Analytics accounted for 40.75% of the app analytics market share in 2025, whereas User Behaviour and Navigation Analytics is advancing at a 21.25% CAGR.

- By deployment model, Cloud retained 56.61% of the app analytics market size in 2025, and Hybrid deployment is forecast to grow at a 21.65% CAGR to 2031.

- By organisation size, Large Enterprises held 59.72% of the app analytics market share in 2025, while Small and Medium Enterprises are growing at a 22.45% CAGR through 2031.

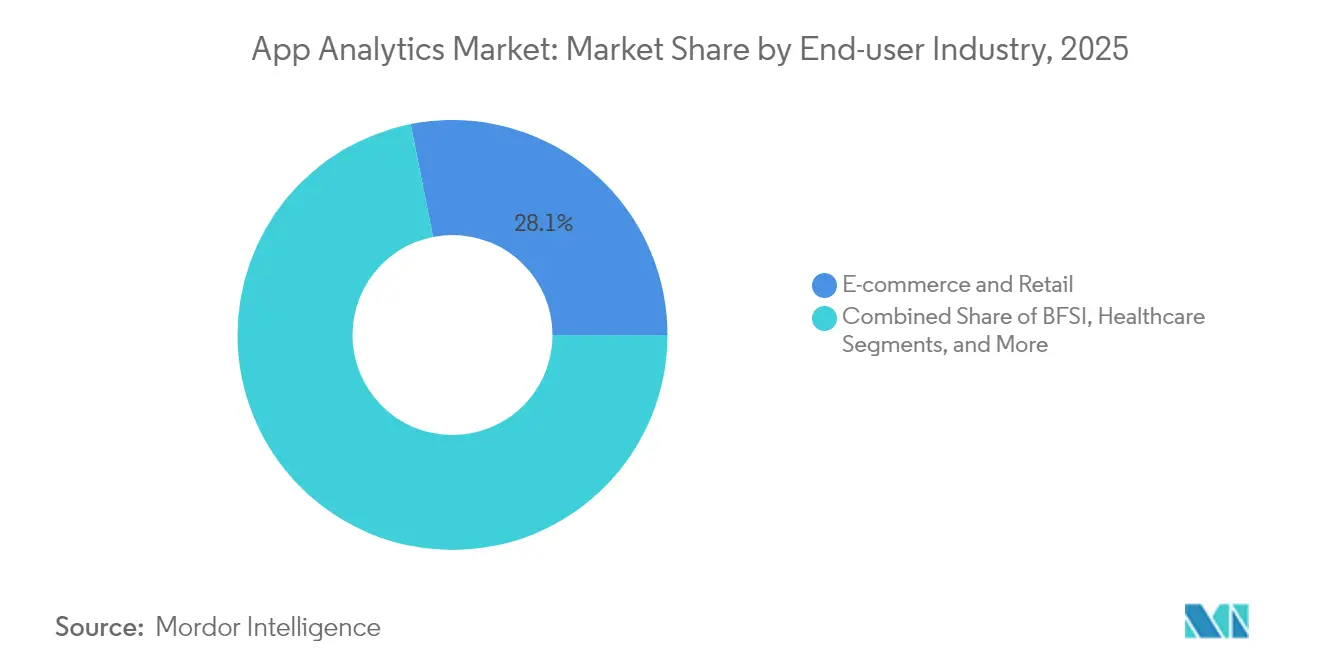

- By end-user industry, E-commerce and Retail commanded 28.12% revenue share in 2025, whereas Healthcare is projected to record a 20.74% CAGR to 2031.

- By geography, North America captured 35.74% revenue in 2025, and Asia-Pacific is set to post a 20.98% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global App Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising app usage across industries | +4.2% | Global | Medium term (2-4 years) |

| Rapid 5G roll-out & smartphone penetration | +3.8% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Time-spent on mobiles driving CX analytics | +3.1% | North America & EU | Medium term (2-4 years) |

| Privacy-preserving analytics as edge | +2.9% | Global | Long term (≥ 4 years) |

| Demand for edge & real-time analytics | +2.6% | North America & APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising App Usage Across Industries

Enterprises well beyond retail now embed mobile interfaces into production, logistics, and field-service workflows. Volkswagen’s AI-enabled mobile monitoring trimmed factory expenses by EUR 1 billion (USD 1.13 billion) through analytics-guided optimization, illustrating how manufacturing, healthcare, and utilities rely on specialized SDKs for offline sync, IoT hooks, and compliance reporting. [1]Adrian Staar et al., “An In-Depth Case Study of Volkswagen’s AI Integration,” CEUR Workshop Proceedings, ceur-ws.org As traditional B2B firms view mobile front ends as the chief client touchpoint, the app analytics market unlocks new vertical-specific modules that monetize operational data and expand supplier ecosystems.

Rapid 5G Roll-out and Smartphone Penetration

Ultra-low-latency 5G networks enable edge engines that pre-process behavior data on the device, cutting round-trip delays by up to 90% for gaming, streaming, and AR companies. [2]International Journal of Computing and Engineering, “The Impact of Edge Computing on Real-Time Data Processing,” carijournals.org Asia-Pacific, where smartphone penetration tops 85% in urban China, South Korea, and Japan, sees predictive content delivery and real-time fraud detection become standard. These millisecond insights directly uplift retention and in-app spend, strengthening the economic case for advanced telemetry inside every release cycle.

Time-spent on Mobiles Driving CX Analytics

Users spent 4.2 trillion hours in apps last year, yielding dense, high-velocity data streams that power churn-prediction and micro-moment personalization. Banking leaders applying deep text analytics boosted fraud-detection efficiency by 35% and saved USD 15 million annually through automation. Retailers harness heat maps and session replays to shrink stockouts by 40% and fine-tune recommendations in minutes, proof that behavior telemetry converts directly into margin protection.

Privacy-preserving Analytics as Competitive Edge

Apple’s App Tracking Transparency cut identifiable traffic by 55 percentage points in the United States, forcing brands to rethink identity strategies. Firms investing in differential privacy and federated learning not only pass audits but also court user trust that drives engagement. HIPAA-compliant builds cost USD 100,000–1.25 million, a hurdle that squeezes smaller rivals and nudges buyers toward turnkey, privacy-first suites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened data-privacy & security concerns | -2.8% | Global | Long term (≥ 4 years) |

| Stringent global data-protection laws | -2.1% | North America & EU | Medium term (2-4 years) |

| Apple ATT & death of device IDs | -1.9% | Global | Short term (≤ 2 years) |

| Uncertain ad-measurement post-cookie | -1.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Data-privacy and Security Concerns

Default SDKs often siphon user identifiers without developer visibility, triggering reputational damage and fines when uncovered. Building consent layers, encryption routines, and synthetic-data pipelines inflate timelines and budgets, especially for SMEs that already cite maintenance and training as top barriers. Market growth slows where legal complexity diverts resources from feature delivery to compliance checklists.

Stringent Global Data-protection Laws (GDPR/CCPA)

Fines of up to 4% of global revenue under GDPR drive risk-averse procurement and prolonged due diligence. CCPA-style regimes demand deletion workflows and granular consent logs, increasing the total cost of ownership. Cross-border projects stall while legal teams align policies, pushing some firms toward regionalized data centers that raise operating overheads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Progressive Web Apps Accelerate Platform Convergence

Mobile Apps retained 55.78% of 2025 revenue, underscoring their entrenched role in user engagement. Yet Progressive Web Apps are set for a 21.90% CAGR through 2031 as businesses seek a single-code-base reach without app-store friction. Intershop’s PWA deployment integrates Google Tag Manager and Matomo to refine conversion funnels, demonstrating parity with native telemetry.

The app analytics market now values platform-agnostic tracking so that product teams follow users from browser to install without losing attribution. Service workers enable offline event caching, and unified APIs let analysts compare session depth regardless of container. Vendors that unify mobile, PWA, and desktop pipelines expand wallet share as clients retire channel-specific dashboards. This fluidity cements the app analytics market as the analytics backbone for omnichannel journeys.

By Application: User Behavior Analytics Drives Retention Focus

Marketing and Advertising Analytics held a 40.75% share in 2025, but User Behaviour and Navigation tools will grow fastest at 21.25% CAGR. The shift mirrors rising acquisition costs and the superior ROI of retention. Session heatmaps, funnel drop-off alerts, and predictive churn models now ship as standard modules. Retail pilots using live clickstream feedback saw 40% inventory accuracy gains that flowed directly into margin expansion.

Forward-looking buyers demand platforms that stitch acquisition, engagement, and monetization metrics into one view. Expect packages that pair ad-source attribution with deep in-product behavior scoring so that teams can suppress spend on low-LTV cohorts. The app analytics market size for behavior-centric platforms is forecast to widen further as subscription and marketplace operators pivot budgets toward lifetime-value safeguards.

By Deployment Model: Hybrid Solutions Bridge Sovereignty and Scale

Cloud deployment captured 56.61% revenue in 2025, reflecting the appeal of zero-infrastructure onboarding. However, Hybrid configurations are on a 21.65% CAGR trajectory because regulators and CFOs push data-gravity and cost-governance agendas. AI-enabled FinOps tools that flag cost anomalies in multi-cloud estates gain prominence.

Hybrid orchestration sends sensitive payloads to on-prem or national clouds while bursting heavy compute to hyperscalers, blending compliance with elasticity. Vendors scoring wins are those offering policy-aware routing, single-pane monitoring, and unified billing. Consequently, the app analytics market share of pure-cloud-only products erodes in regulated sectors, whereas adaptable hybrids win new logos in healthcare and finance.

By End-user Industry: Healthcare Transformation Accelerates Digital Analytics

E-commerce and Retail commanded 28.12% revenue in 2025, but Healthcare is the fastest mover at 20.74% CAGR as telehealth and digital therapeutics mature. FDA clearance for apps like PanopticAI’s smartphone pulse monitor underlines regulatory appetite for mobile diagnostics. These approvals mandate HIPAA-grade analytics pipelines, spurring specialist platforms that package audit trails and consent ledgers out of the box.

Hospital networks allocate budgets to predictive readmission models and remote-patient monitoring dashboards. Vendors equipped with de-identification, cohort-building, and longitudinal outcome reporting secure contracts in a segment where data integrity stakes are life-critical. As funding such as Innovaccer’s USD 275 million round shows, capital flows to niche players capturing this vertical’s deep compliance moat.

By Organisation Size: SME Democratization Drives Market Expansion

Large Enterprises held 59.72% revenue in 2025, yet SMEs will expand at 22.45% CAGR thanks to no-code interfaces and usage-based pricing. OECD’s D4SME survey found 39% of small firms now deploy AI within analytics workflows, up from 26% a year earlier.

Barriers remain: 40% cite maintenance cost, 39% lack training. Vendors respond with guided setup wizards, embedded education modules, and partner ecosystems of fractional data scientists. Government grants and tax credits further lower entry thresholds. As democratization widens, the app analytics industry sees rising long-tail adoption that offsets slower growth in saturated large-enterprise accounts.

Geography Analysis

North America contributed 35.74% of 2025 revenue, aided by venture capital outlays that poured USD 33.9 billion into generative-AI tooling, many of which embed real-time in-app telemetry. Regulatory clarity encourages experimentation, yet new state-level privacy acts add integration overhead. Canada’s manufacturing digitization and Mexico’s export-oriented plants also fuel industrial analytics demand, supporting steady regional growth.

Asia-Pacific is the fastest-growing arena at 20.98% CAGR, underpinned by smartphone ubiquity and public-sector digital-first mandates. China’s mobile content market is racing toward USD 302.5 billion in 2030 at 29.5% CAGR. Japan’s services-export boom and India’s 143% leap in food-and-dining app downloads illustrate how sector-specific surges translate into telemetry volume spikes.

Europe balances innovation with governance. GDPR compliance drives adoption of differential privacy and federated learning, giving European vendors an exportable advantage as other regions impose similar restrictions. Germany’s Industry 4.0 programs, the UK’s open-banking wave, and France’s health-data hubs all demand analytics that fuses domain specificity with strict residency. Eastern Europe supplies cost-efficient engineering talent, anchoring provider R&D centers.

Competitive Landscape

The app analytics market remains moderately fragmented. Google, Apple, and Adobe leverage platform ecosystems, while AppsFlyer, Mixpanel, and Amplitude carve niches in attribution, product, and behavioral analytics. WIPO data shows generative-AI analytics patents exploding 800% since 2017, feeding USD 4.4 trillion in yearly economic value. M&A activity centers on privacy tech and vertical modules; large vendors prefer bolt-ons over greenfield builds.

Regulatory costs act as a moat: smaller entrants must absorb legal overhead before feature velocity. Niche providers differentiate via edge deployment or zero-copy compute, courting clients that fear vendor lock-in. Meta’s patent portfolio around real-time ad bidding sets a benchmark for latency-sensitive insight pipelines. White-space persists in sector-specific suites for healthcare, manufacturing, and public services. Victory will hinge on marrying AI-powered prediction, iron-clad privacy, and hybrid orchestration at a price point palatable to SMEs.

App Analytics Industry Leaders

AppsFlyer Ltd.

Kochava Inc.

Google LLC

Amazon Web Services, Inc.

Adobe Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Catchpoint released Mobile RUM built on OpenTelemetry to deepen real-user monitoring across code and network layers.

- May 2025: MongoDB teamed with Langtrace AI to bolster AI observability by embedding database performance metrics.

- April 2025: Adobe’s 2025 AI & Digital Trends report showed 79% of executives plan higher analytics investment.

- March 2025: Sensor Tower noted 11% YoY growth in food-and-beverage app downloads, nearing 2 billion worldwide.

- February 2025: PanopticAI obtained FDA clearance for pulse-rate measurement via iPhone camera, highlighting mobile-first clinical analytics.

- February 2025: AWS and General Catalyst unveiled an AI-powered healthcare partnership aiming for predictive care and operational savings.

- January 2025: OECD’s D4SME survey revealed 39% of SMEs already employ AI applications, citing cost and skills constraints.

- January 2025: Innovaccer secured USD 275 million to expand healthcare data analytics capabilities, underscoring investor confidence in vertical platforms.

- December 2024: WIPO reported generative-AI patent families rose from 733 in 2014 to 14,000 in 2023, a harbinger for analytics IP battles.

Research Methodology Framework and Report Scope

Market Definition and Key Coverage

Our study defines the app analytics market as all licensed or subscription cloud and on-premise platforms that collect, process, and visualize usage, performance, revenue, and marketing data for mobile, web, and progressive web applications across industries worldwide. According to Mordor Intelligence, market values are expressed in constant 2025 dollars, covering platform fees and associated managed services.

Scope Exclusion: We purposely exclude stand-alone crash loggers and simple ad-tag scripts lacking a unified analytics dashboard.

Segmentation Overview

- By Type

- Mobile Apps

- Website/Desktop Apps

- Progressive Web Apps

- By Application

- Marketing/Advertising Analytics

- Revenue Analytics

- In-app Performance Analytics

- User Behaviour & Navigation Analytics

- By Deployment Model

- Cloud

- On-premise

- Hybrid

- By End-user Industry

- BFSI

- E-commerce and Retail

- Media and Entertainment (incl. Social and Gaming)

- Travel and Hospitality

- IT and Telecom

- Healthcare

- Government and Public Sector

- Manufacturing

- Other End-user Industries

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed platform product managers, digital marketers in retail and BFSI, and CIOs across North America, Europe, and Asia-Pacific to validate usage ratios, contract norms, and forward spending intentions.

Desk Research

We map demand using GSMA Intelligence mobile connections, ITU broadband penetration, OECD digital economy datasets, and Apple and Google developer statistics. Company filings, investor decks, and news from Dow Jones Factiva refine vendor splits, while D&B Hoovers gauges enterprise footprints and Questel patent counts flag emerging tracking techniques. Additional open data supported verification.

Market-Sizing & Forecasting

A top-down model converts the global smartphone and web user base into an addressable app pool, applies primary-verified penetration, and then we multiply by benchmarked average revenue per app, while supplier roll-ups and channel checks offer bottom-up reasonableness. Core variables include monthly active apps per enterprise, events per session, cloud cost per million events, mobile ad spend share, and privacy enforcement timelines. Multivariate regression on smartphone growth, app downloads, and digital ad spend produces the 2025-2030 curve, with proxy ratios bridging data gaps.

Data Validation & Update Cycle

Outputs pass anomaly flags, peer review, and senior sign-off. The model refreshes annually, with interim updates triggered by major funding, pricing, or policy shifts.

Why Mordor's App Analytics Baseline Earns Stakeholder Trust

Published estimates often differ because publishers vary scope, price trajectories, and refresh cadence. Our disciplined boundaries and yearly recalibration give decision-makers a consistent yardstick.

Key gap drivers elsewhere include exclusion of desktop analytics, inclusion of broader performance monitoring tools, and differing ASP paths.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.22 B (2025) | Mordor Intelligence | N/A |

| USD 6.25 B (2025) | Global Consultancy A | Omits desktop and hybrid-app analytics |

| USD 9.44 B (2025) | Industry Association B | Bundles wider performance monitoring software |

These contrasts show that clear scope, transparent variables, and frequent validation make Mordor's baseline the dependable starting point for strategy planning.

Key Questions Answered in the Report

What is the current size of the app analytics market?

The app analytics market is valued at USD 9.81 billion in 2026 and is projected to reach USD 23.74 billion by 2031.

Which region is expanding the fastest?

Asia-Pacific is the fastest-growing region, forecast to record a 20.98% CAGR through 2031 on the back of widespread 5G adoption and digital-first policies.

Which deployment model is gaining ground over cloud-only setups?

Hybrid deployment is growing at 21.65% CAGR as enterprises blend on-prem sovereignty with public-cloud scalability.

Why are Progressive Web Apps important to future growth?

PWAs provide native-like experiences without app-store barriers and are forecast to expand at 21.90% CAGR, encouraging platform-agnostic analytics.

How are privacy regulations affecting vendor selection?

Regulations such as GDPR and CCPA elevate demand for privacy-preserving architectures, favoring vendors that ship differential privacy and consent-management features by default.

What factors limit analytics adoption among SMEs?

OECD research lists maintenance costs and employee training time as primary hurdles, although simplified SaaS models are gradually lowering these barriers.

Page last updated on: