Mobile Application Testing Services (MATS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

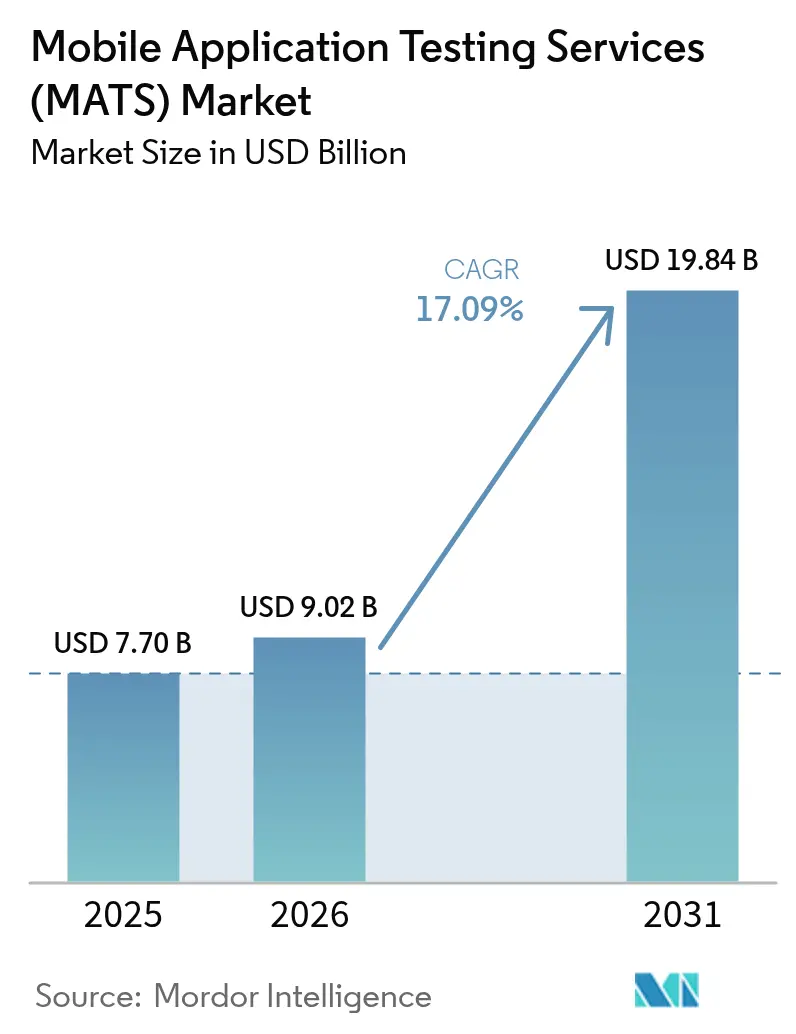

| Market Size (2026) | USD 9.02 Billion |

| Market Size (2031) | USD 19.84 Billion |

| Growth Rate (2026 - 2031) | 17.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Application Testing Services (MATS) Market Analysis by Mordor Intelligence

The mobile application testing services market size is expected to grow from USD 7.70 billion in 2025 to USD 9.02 billion in 2026 and is forecast to reach USD 19.84 billion by 2031 at 17.09% CAGR over 2026-2031. Strong demand stems from enterprises baking continuous quality checks into DevOps pipelines, tighter security regulations, and the race to deliver flawless customer experiences on an ever-wider range of 5G-enabled smartphones. The shift from manual, release-end testing to real-time quality assurance has raised expectations for specialized partners that can automate at scale, provide deep domain expertise, and cover vast device matrices. Automated and crowd-sourced approaches now coexist to balance velocity with real-world coverage, while compliance-driven industries such as BFSI and healthcare fuel robust spend on security and accessibility validation. Vendors that fuse AI-assisted test creation with cloud-based device farms are winning share as clients seek faster feedback loops and lower total cost of ownership.

Key Report Takeaways

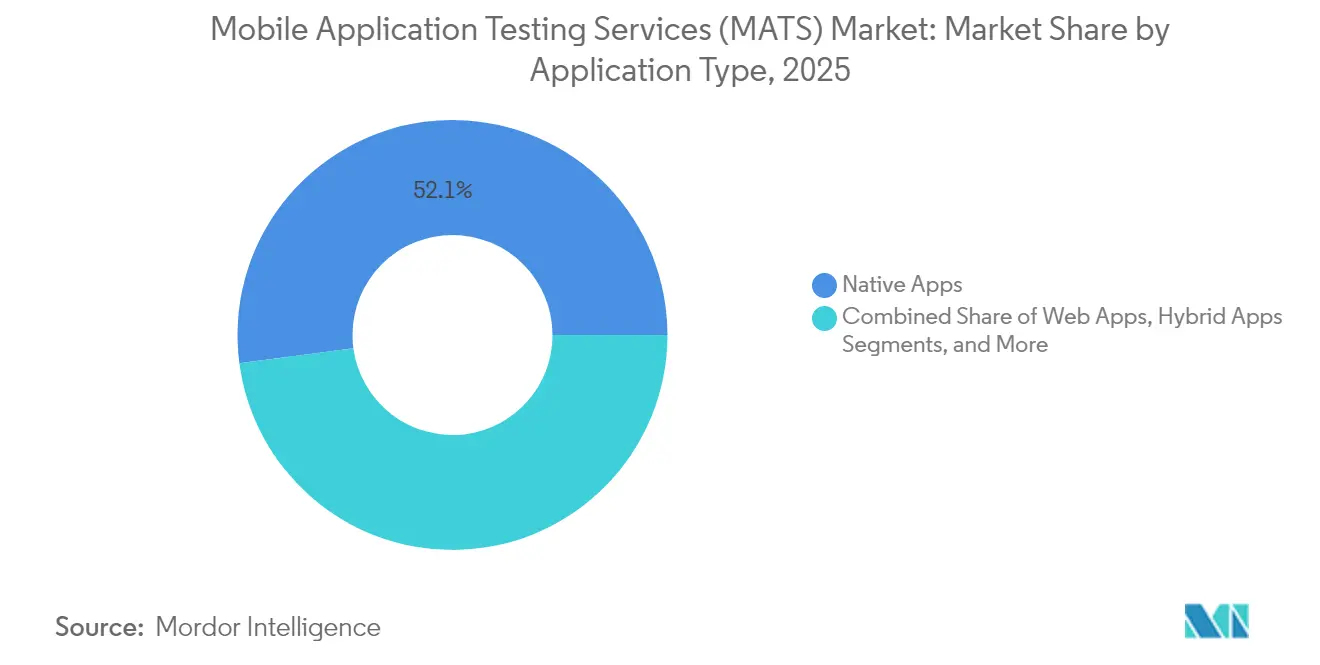

- By application type, native apps led with 52.10% of the mobile application testing services market share in 2025, whereas progressive web apps are advancing at an 18.15% CAGR through 2031.

- By service type, functional testing commanded 41.30% of the mobile application testing services market size in 2025; security and penetration testing is projected to expand at 17.95% CAGR.

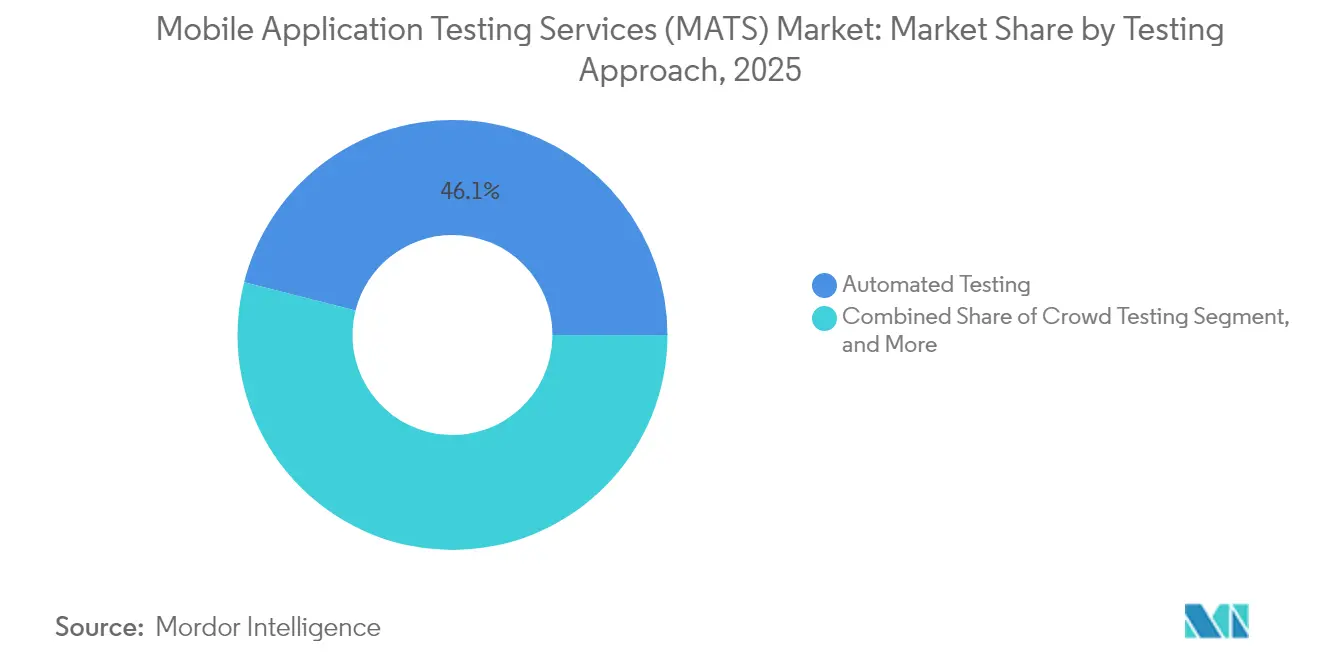

- By testing approach, automated testing captured 46.05% share of the mobile application testing services market size in 2025, while crowd testing records the fastest 18.02% CAGR.

- By end-user industry, BFSI accounted for 28.30% share of the mobile application testing services market size in 2025; healthcare and life sciences is growing at 17.62% CAGR.

- By geography, North America maintained 37.10% share in 2025 in the mobile application testing services, yet Asia-Pacific is set to post a 17.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Application Testing Services (MATS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global smartphone penetration | +3.2% | APAC leadership, global reach | Medium term (2-4 years) |

| Agile/DevOps shift demanding continuous test | +4.1% | North America and EU lead, global adoption | Short term (≤ 2 years) |

| AI/ML, AR/VR, 5G rich-experience apps | +2.8% | Developed markets worldwide | Long term (≥ 4 years) |

| Stronger mobile security and privacy rules | +3.5% | EU and North America primary | Medium term (2-4 years) |

| OEM push for in-vehicle infotainment testing | +1.9% | North America, EU, China auto hubs | Long term (≥ 4 years) |

| Sustainability KPIs for battery/CO₂ testing | +1.3% | EU leadership, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Smartphone Penetration Accelerates Testing Demand

Smartphone adoption in India, Indonesia, and the Philippines climbed sharply in 2025 as the average 5G handset fell below USD 200, spawning thousands of localized apps targeting varied network conditions and lower-spec devices. For suppliers to this mobile application testing services market, the result is a surge in compatibility workloads across fragmented Android forks where OEM tweaks often break core functions.[1]Rakesh Thampi, “A Guide to Mastering Battery Drain Testing,” HeadSpin, headspin.io Device coverage must span multiple chipset vendors and screen sizes, pressuring service providers to expand real-device clouds and refine test-case prioritization. Enterprises unable to maintain these device matrices in-house increasingly outsource, creating recurring revenue streams for pure-play testing firms.

Rapid Shift to Agile and DevOps Demanding Continuous Testing

Fortune 500 developers now push code to production dozens of times a day, dissolving the wall between development and quality. Testing therefore moves upstream, runs in parallel with every commit, and feeds go/no-go gates in CI/CD pipelines. Vendors that plug AI-assisted script generation into Jenkins, GitLab, and Azure DevOps see stronger win rates because they compress feedback cycles from hours to minutes.[2]“Applause Announces Acquisition by Vista Equity Partners,” Applause, applause.com The mobile application testing services market prizes such partners for lowering mean time to remediation and supporting the “fail-fast” ethos central to digital product teams.

Proliferation of AI/ML, AR/VR and 5G Rich-Experience Apps

Generative AI chatbots, AR shopping assistants, and low-latency gaming streaks rely on edge computing and multi-camera input, introducing state-space explosions beyond traditional test permutations. Service providers now model neural-network drift, sensor fusion accuracy, and radio-handover scenarios that saturate conventional lab setups. Leaders in the mobile application testing services market deploy synthetic data, 5G network emulation, and hardware-in-the-loop rigs to validate such experiences at scale, giving clients confidence to launch demanding real-time services.

Growing Regulatory Push for Mobile App Security and Privacy

The European Accessibility Act, enforced in June 2025, and evolving GDPR case law have transformed security and accessibility tests from best practice into legal necessity. Health, finance, and public-sector apps must document conformance to EN 301 549, WCAG 2.1, and stringent encryption standards before app-store submission. Providers that deliver audit-ready evidence packages, penetration tests, and threat-model overlays gain premium pricing power, particularly among U.S. banks seeking EU passporting rights post-launch.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device-lab infrastructure costs | -2.1% | Global, hurts smaller vendors | Short term (≤ 2 years) |

| Android fragmentation erodes automation ROI | -1.8% | Global, strongest in APAC | Medium term (2-4 years) |

| In-app ad-tech SDK complexity adds flakiness | -1.2% | Consumer apps worldwide | Short term (≤ 2 years) |

| Limited test-data privacy for GenAI testing | -0.9% | EU and North America focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Infrastructure and Device-Lab Investment Costs

A lab with 1,000 real devices spanning iOS and 20 Android OEMs can cost USD 6 million to build and USD 50,000 per month to refresh. Smaller providers cannot amortize these outlays across enough clients, curbing their ability to compete on price. Cloud device farms alleviate capex but introduce opex tied to hourly usage and geographic data-center fees. This restraint slows new-entrant growth in the mobile application testing services market and accelerates M&A as niche players seek scale advantages.

Fragmented Device/OS Ecosystem Complicates Automation ROI

Android 14 behaves differently on Samsung One UI, Xiaomi HyperOS, and Oppo ColorOS. The same XPath locator can fail across skin variants, forcing script rewrites and ballooning maintenance hours. Enterprises often allocate 40% of automation budgets to handle fragmentation, diluting ROI versus iOS. Service partners with dynamic locator strategies and AI-based element detection mitigate, but not eliminate, the drag on the mobile application testing services market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Type: Native Apps Dominate Despite PWA Acceleration

Native apps held 52.10% of the mobile application testing services market share in 2025, underscoring enterprise reliance on platform-level performance and camera, GPS, or biometric APIs. The segment’s durability keeps demand high for Swift, Kotlin, and Jetpack Compose test specialists who validate deep device integrations. Progressive web apps, expanding at 18.15% CAGR, require cross-browser conformance testing and service-worker validation that differ from native test patterns. Their rise encourages providers to offer unified test suites blending browser and device farms, thereby broadening total addressable spend within the mobile application testing services market.

PWAs also attract mid-sized retailers and SaaS vendors seeking a single code-base strategy. Testing partners must therefore prove capability in offline caching, push-notification integrity, and installability across Chromium forks and WebKit. As bandwidth improves, enterprises expect near-native UX, raising the bar for load-time and animation smoothness benchmarks. Firms that can deliver side-by-side performance analytics for native versus PWA builds gain influence over tech-stack decisions, increasing wallet share.

By Service Type: Security Testing Accelerates Amid Functional Dominance

Functional testing represented 41.30% of the mobile application testing services market size in 2025 as UI verification and regression suites remained table stakes across all industries. Yet security and penetration testing grows at 17.95% CAGR, propelled by financial institutions extending zero-trust policies to every software component. Providers bundling OWASP MASVS compliance audits with API fuzzing and runtime app self-protection checks shorten remediation cycles and justify premium fees.

Expanded privacy laws and high-profile breaches elevate budget priority for mobile pentests that simulate device rooting, network-layer interception, and malicious SDK inclusion. Vendors that feed findings into DevSecOps dashboards and retest patches automatically in CI/CD pipelines demonstrate tangible risk-reduction ROI. This pull through boosts their cross-sell of managed vulnerability management and red-team services, raising average contract value across the mobile application testing services industry.

By Testing Approach: Automation Leads While Crowd Testing Surges

Automation commanded 46.05% share of the mobile application testing services market size in 2025 as enterprises codified regression packs in Java, Kotlin, or JavaScript. AI-generated scripts now cut authoring time by 60%, although maintenance challenges persist amid device churn. Crowd testing’s 18.02% CAGR shows organizations valuing organic user feedback across networks, locales, and accessibility contexts that labs cannot replicate. Platforms that pre-qualify testers, encrypt PII, and stream session replays directly into issue trackers convert episodic pilots into annual subscriptions.

Blended strategies are becoming typical. A retailer, for example, may run nightly automated smoke suites on 200-device clouds, then trigger weekend crowd sprints focused on promotional flows in top-five target countries. Providers fluent in orchestration and data hygiene occupy a strategic niche, steering more spend toward the mobile application testing services market as clients offload coordination complexity.

By End-User Industry: BFSI Leadership Challenged by Healthcare Growth

BFSI retained 28.30% share of the mobile application testing services market size in 2025. Mobile banking failures carry direct monetary losses and regulatory fines, compelling exhaustive functional, security, and accessibility tests before every release. Providers that map test cases to PSD2, SOC 2, and PCI-DSS controls become trusted risk partners rather than commoditized vendors, solidifying multi-year engagements.

Healthcare and life sciences, expanding at 17.62% CAGR, embody the next frontier. FDA guidance requires evidence of clinical safety, data integrity, and interoperability for mobile medical apps, lifting test-case volume and documentation rigor. Testing partners that blend HIPAA-grade data isolation with domain-expert clinical validation tap higher bill rates. As remote patient monitoring, telehealth, and digital therapeutics scale, healthcare is poised to challenge BFSI’s dominance in the mobile application testing services market.

Geography Analysis

North America generated 37.10% of 2025 revenues, leveraging deep DevOps adoption and strict compliance mandates. U.S. banks and payers rolled out real-time fraud-detection apps that need 24×7 security scans, while digital-native brands outsource regression suites to manage bi-weekly release cadences. Canadian demand centers on healthcare digitization and provincial accessibility laws, sustaining premium for bilingual testing coverage across English and French apps.

Asia-Pacific posts the strongest 17.82% CAGR through 2031. India’s fintech and social-commerce boom prompts large-scale crowd campaigns across 15 regional languages and myriad low-cost handsets. China’s super-app ecosystems require providers versed in mini-program architectures and domestic compliance, creating two-track engagements covering both domestic and export builds. Mature 5G rollouts in Japan and South Korea elevate AR/VR app workloads, expanding the device lab footprint for vendors in the mobile application testing services market.

Europe shows steady growth underpinned by regulation. The European Accessibility Act and GDPR fine regime convert accessibility and privacy checks into non-negotiable budget lines. Germany leads demand via automotive OTA-update testing, while the U.K. remains strong in finance despite post-Brexit regulatory divergence. Nordic clients emphasize sustainability metrics, asking suppliers to report test-lab carbon intensity, a nascent differentiator within the mobile application testing services industry.

Competitive Landscape

The market is moderately fragmented. Global IT-services majors, Accenture, TCS, Wipro, bundle testing with transformation deals, leveraging offshore talent for scale. Pure-play platforms such as BrowserStack and Sauce Labs anchor differentiation in cloud device coverage and developer UX, frequently courting SMBs and agile squads. Mid-tier specialists like Applause focus on crowd models that deliver authentic user feedback at speed.

Consolidation accelerated after Vista Equity Partners acquired Applause in late 2024 and BrowserStack bought Bird Eats Bug in January 2025. Private-equity backing fuels R&D into AI-powered defect clustering and self-healing test cases. Tech-driven deals also aim to assemble end-to-end quality suites spanning planning, execution, observability, and analytics. Simultaneously, smaller regional vendors seek vertical niches, sustainability testing or automotive infotainment, to command premium margins.

Competitive advantage now hinges on three pillars: real-device breadth, AI-driven efficiency, and regulatory fluency. Vendors delivering continuous quality dashboards that merge functional, security, and ESG telemetry gain stickiness. The top five hold roughly 45% of global revenue, indicating mid-level concentration yet room for specialist challengers in the mobile application testing services market.

Mobile Application Testing Services (MATS) Industry Leaders

Accenture PLC

Capgemini SE

EPAM Systems Inc.

Cognizant Technology Solutions Corporation

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BrowserStack acquired Bird Eats Bug and introduced Bug Capture, promising 30% faster debugging through instant session replays.

- November 2024: Vista Equity Partners purchased Applause, arming the crowd-testing pioneer with expansion capital.

- July 2024: Tricentis announced the takeover of SeaLights to deepen AI-powered quality intelligence across CI/CD pipelines.

- July 2024: QA Wolf raised USD 36 million to scale its managed QA offering for web and mobile apps.

Global Mobile Application Testing Services (MATS) Market Report Scope

Mobile application testing service allows the application developer to test and interact with the Android and iOS simultaneously or other platform apps, along with web and hybrid apps, on many devices. It also allows the developers to reproduce issues on a device in real time. The application developer can view logs, videos, screenshots, and performance data to pinpoint and fix problems and improve the quality before releasing the app. It enables fast development-to-market time and addresses issues impacting end-user adoption.

The mobile application testing services (MATS) Market is segmented by application type (native, web, hybrid), end-user industry (gaming, travel and tourism, BFSI, retail, healthcare), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Native Apps |

| Web Apps |

| Hybrid Apps |

| Progressive Web Apps (PWA) |

| Functional Testing Services |

| Performance and Load Testing Services |

| Security and Pen-Testing Services |

| Compatibility and UX Testing Services |

| Test Automation Services |

| Manual Testing |

| Automated Testing |

| Crowd / Crowd-source Testing |

| Gaming |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Travel and Hospitality |

| Media and Entertainment |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application Type | Native Apps | ||

| Web Apps | |||

| Hybrid Apps | |||

| Progressive Web Apps (PWA) | |||

| By Service Type | Functional Testing Services | ||

| Performance and Load Testing Services | |||

| Security and Pen-Testing Services | |||

| Compatibility and UX Testing Services | |||

| Test Automation Services | |||

| By Testing Approach | Manual Testing | ||

| Automated Testing | |||

| Crowd / Crowd-source Testing | |||

| By End-User Industry | Gaming | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Travel and Hospitality | |||

| Media and Entertainment | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the mobile application testing services market in 2031?

The market is expected to reach USD 19.84 billion by 2031, reflecting a 17.09% CAGR.

Which region is growing fastest for mobile application testing services?

Asia Pacific shows the highest growth, poised for a 17.82% CAGR through 2031 driven by rising smartphone adoption and digital transformation.

Which application type currently holds the largest share?

Native apps lead with 52.10% share thanks to their platform-specific performance advantages.

Why is security testing demand accelerating?

Escalating cyber threats and stringent regulations are boosting security and penetration testing, the fastest-growing service at 17.95% CAGR.

Which end-user sector spends the most on mobile application testing?

BFSI remains the largest spender, accounting for 28.30% of 2025 revenue due to its zero-tolerance stance on transaction failures.

Page last updated on: