Market Overview

| Study Period | 2020 - 2031 |

|---|---|

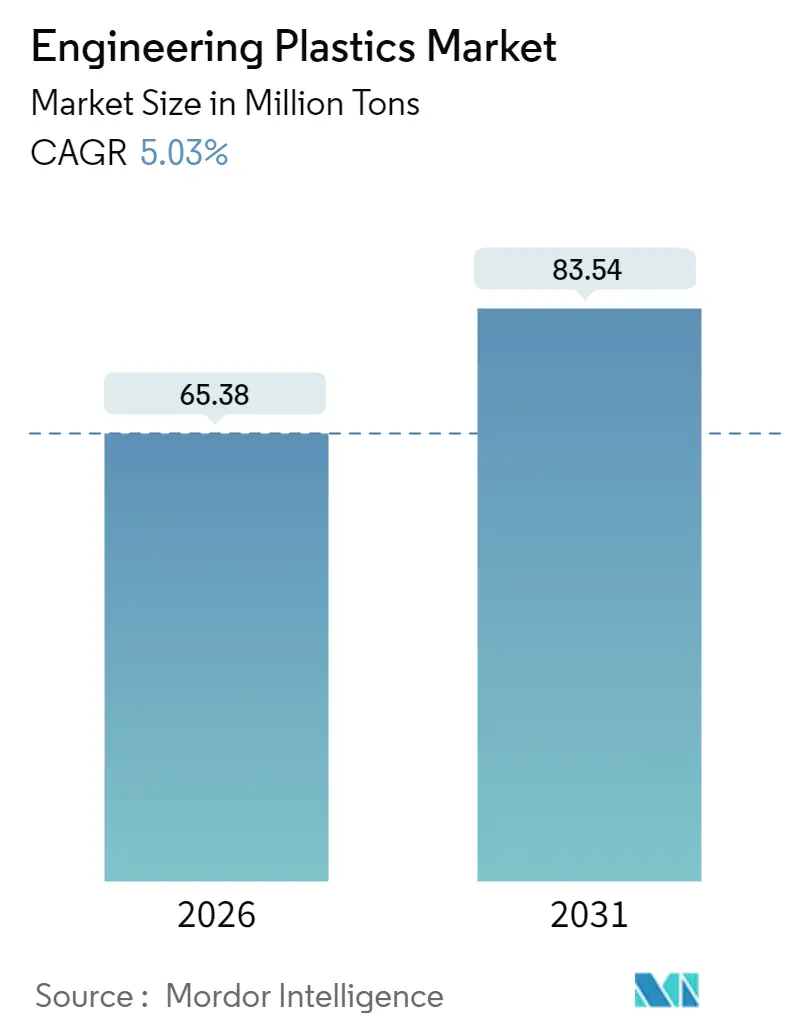

| Market Volume (2026) | 65.38 Million tons |

| Market Volume (2031) | 83.54 Million tons |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Engineering Plastics Market Analysis by Mordor Intelligence

The Engineering Plastics Market was valued at 62.25 million tons in 2025 and estimated to grow from 65.38 million tons in 2026 to reach 83.54 million tons by 2031, at a CAGR of 5.03% during the forecast period (2026-2031). Demand stems from lightweighting programs across the mobility and aerospace sectors, the electrification of vehicles and industrial equipment, and the growing adoption of semiconductor fabrication, all of which reward materials that offer high strength-to-weight ratios and geometric freedom. Sustained capital spending on Asia-Pacific capacity, the emergence of chemical recycling at a commercial scale, and regulatory pushes for fuel economy and carbon reduction further reinforce growth momentum.

Key Report Takeaways

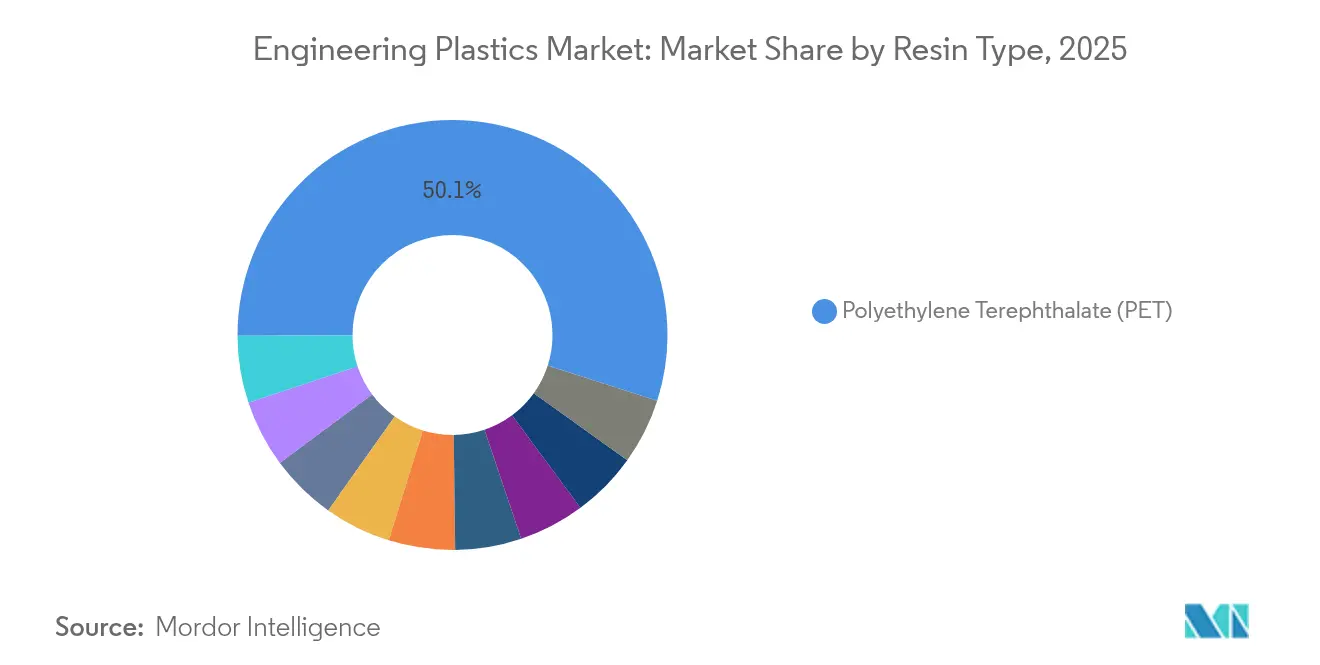

- By resin type, polyethylene terephthalate (PET) held 50.05% of the Engineering Plastics market share in 2025. Fluoropolymers are projected to post the fastest 7.34% CAGR through 2031.

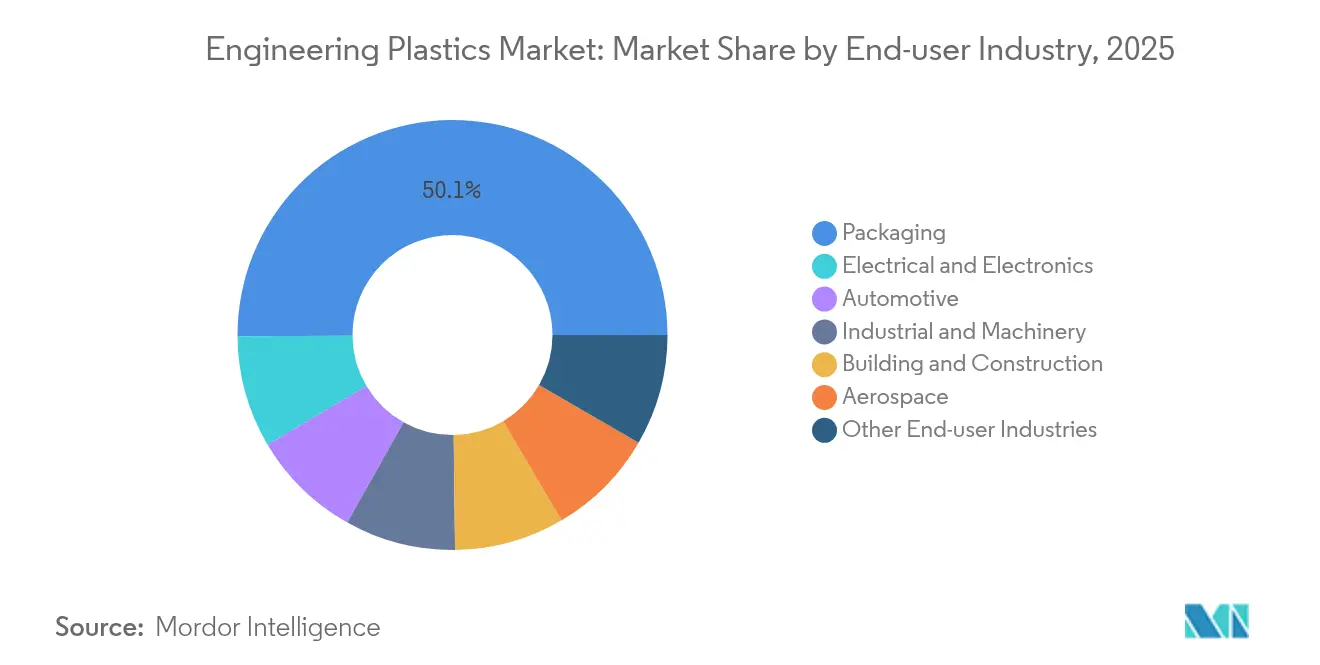

- By end-user industry, packaging led with a 50.10% share in 2025. Electrical and electronics applications are forecasted to expand at a 6.98% CAGR between 2026 and 2031.

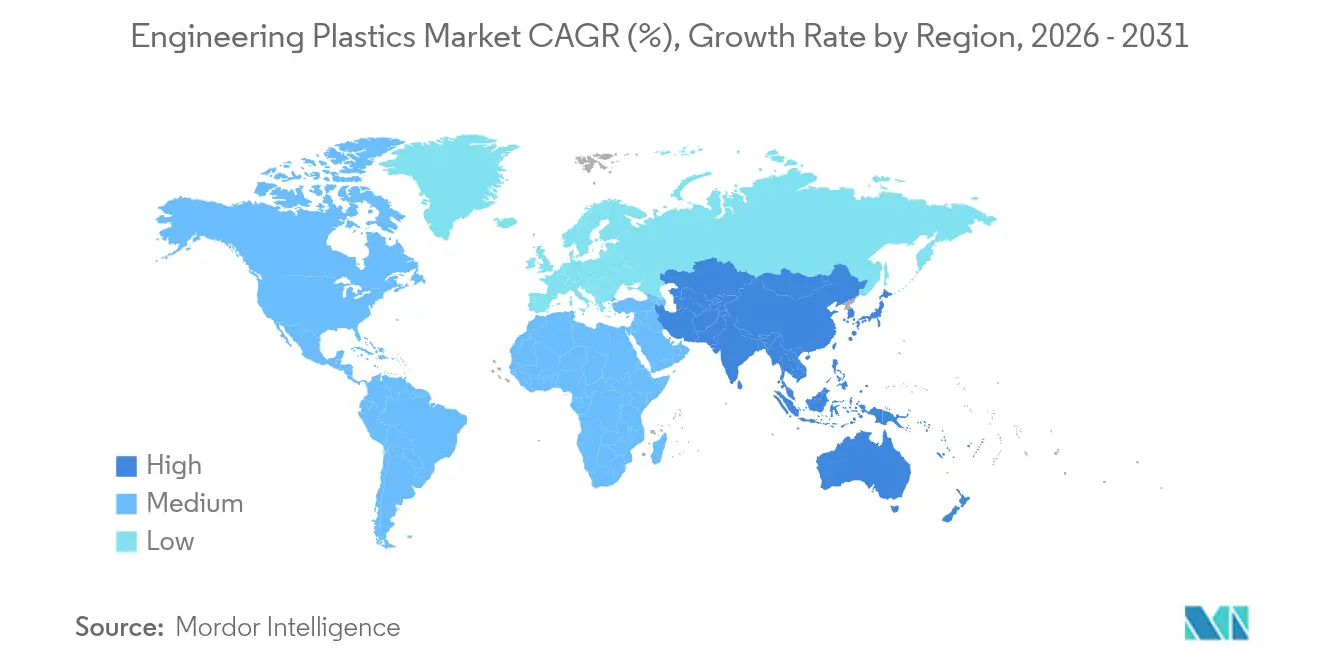

- By geography, the Asia-Pacific region commanded a 55.10% share in 2025 and is projected to advance at a 5.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Engineering Plastics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting Push in Mobility and Aerospace | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Electrification-led Demand Spike | +0.9% | APAC core, spill-over to North America and Europe | Short term (≤ 2 years) |

| APAC Manufacturing Migration | +0.8% | Asia-Pacific, particularly China and India | Long term (≥ 4 years) |

| EV Battery Module Housings Adoption | +0.7% | Global, led by China and North America | Medium term (2-4 years) |

| Chemical-recycling Supply Boosts | +0.4% | North America and Europe initially | Long term (≥ 4 years) |

| OEM Switch to Bio-based PA/PTT | +0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Lightweighting Push in Mobility and Aerospace

Automotive fuel-economy mandates, such as the US CAFE target of 54.5 mpg by 2025, intensify OEM (original equipment manufacturer) focus on weight reduction, and every 10% mass cut yields 6-8% efficiency gains[1]U.S. Department of Energy, “Vehicle Technologies Office: Lightweighting Materials,” energy.gov. Aircraft programs illustrate parallel dynamics: the Boeing 787 achieved 22% fuel savings with 50% composite content, while the Airbus A350 utilizes 53% composites to achieve a similar effect[2]Boeing, “787 Dreamliner Program Fact Sheet,” boeing.com. Carbon-fiber-reinforced thermoplastics gain share because they can be reheated and recycled, unlike thermosets, and automated fiber placement lowers cycle times. Wind-turbine blades now consume larger volumes of carbon fiber than the aerospace industry, with 100-meter blades trimming mass by 38% compared to glass-fiber designs. These successes raise confidence among OEMs evaluating polymer-based structures for wheels, seating, and secondary aircraft structures.

Electrification-Led Demand Spike

High-voltage electric vehicles require enclosures that offer robust flame retardancy and dielectric strength, pushing polyphenylene sulfide, polyether ether ketone, and glass-filled polyamide consumption upward[3]Tesla, “Optimus: Full-Scale Humanoid Robot,” tesla.com . Robotics lines such as Tesla’s Optimus prototype highlight PEEK’s longevity under continuous duty, validating higher-end grades for actuators. Semiconductor fabs scaling for AI chips adopt liquid-crystal polymers for fine-pitch connectors that remain dimensionally stable above 260 °C, preserving signal integrity during lead-free reflow. The migration from 400-V to 800-V EV (electric vehicle) architectures amplifies dielectric stress, prompting OEMs to specify insulation with comparative tracking index (CTI) values above 600. Meanwhile, thermal-runaway barriers increasingly incorporate polycarbonate-siloxane blends to prevent heat propagation without resorting to heavy metallic shields.

APAC Manufacturing Migration

Chinese players, such as Wanhua Chemical and BASF China, have commissioned multi-hundred-kiloton lines near downstream auto and electronics clusters, thereby lowering logistics costs and enhancing technical collaboration. India’s 2024 Production-Linked Incentive scheme covers advanced polymers, unlocking foreign investment for brownfield debottlenecking and greenfield sites. Regional specialization extends to talent: Taiwanese processors offer micro-molding expertise critical for camera modules and sensor housings. Environmental compliance also influences siting decisions, as stricter EU carbon tariffs prompt export-oriented producers to adopt the best-available control technologies from the outset. The net result is a resilient supply base that will anchor the engineering plastics market in the Asia-Pacific region for the long haul.

EV Battery Module Housings Adoption

Battery-pack casings require simultaneous structural strength, dielectric isolation, and vent-gas management, attributes that can be achieved with glass-reinforced polyamide and polycarbonate blends, which offset the weight of aluminum designs by 15-20 kg. Structural battery concepts combine load-bearing composite skins with solid-state electrolyte layers, and early tests using polyvinylidene fluoride matrices meet ionic-conductivity benchmarks while surviving crash pulses. Fire-safety protocols, such as UL 94 V-0, necessitate halogen-free flame retardants that maintain efficacy over a wide temperature range, from −40°C to 120°C, prompting suppliers to commercialize red phosphorus-stabilized polybutylene terephthalate grades. Ultrasonic welding compatibility reduces the fastener count, yielding 5-7% cost savings in high-volume packs. As scale rises, OEMs increasingly negotiate long-term pricing indexed to resin feedstock costs to manage volatility.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Monomer Price Volatility | -0.8% | Global, particularly Asia-Pacific | Short term (≤ 2 years) |

| Packaging Regulations Tightening | -0.6% | Europe and North America | Medium term (2-4 years) |

| Fluorspar-linked Fluoropolymer Shortage | -0.4% | Global | Medium term (2-4 years) |

| Metal AM Substitution Threat | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Monomer Price Volatility

Propylene and ethylene prices track crude swings because Asian crackers rely heavily on naphtha; a USD 10/bbl oil jump can increase propylene costs by USD 90/ton, compressing converters’ margins when selling into fixed-price OEM contracts. China’s styrene monomer capacity reached 21.51 million tons in H1 2025, accounting for 49% of the global supply and triggering spot price collapses below cash costs for high-cost producers. Tariff escalations between major economies further distort trade flows, forcing rapid output cuts at styrene-based ABS and polycarbonate plants. Volatility particularly stings high-performance resins such as polyimide, whose specialized dianhydride monomers command 4-5× commodity feedstock prices, limiting the ability to pass on surges in tight downstream markets.

Packaging Regulations Tightening

The EU Packaging & Packaging Waste Regulation proposes 30% recycled content by 2030 for contact-sensitive applications, adding qualification burdens for virgin resin suppliers. Parallel moves to phase out bisphenol A in food-service items challenge polycarbonate lines; while non-BPA resins exist, they impose tooling upgrades and pre-drying steps that slow cycle times. Pending PFAS restrictions threaten certain fluoropolymer coatings unless they are deemed “essential,” creating demand uncertainty for PVDF used in flexible food packaging. Extended producer responsibility fees elsewhere in North America are pressuring converters to redesign multilayer films toward mono-material platforms, potentially diverting spending from engineering-grade solutions and trimming incremental growth.

Segment Analysis

By Resin Type: PET Dominance Faces Fluoropolymer Disruption

Polyethylene terephthalate (PET) maintained a commanding 50.05% engineering plastics market share in 2025, driven by ubiquitous demand for beverages and rigid packaging. Yet the segment contends with plateauing single-use volumes and mounting recycled-content targets that require process investments. Polyamide blends are gaining renewed traction as automakers opt for bio-based PA11 to reduce scope 3 emissions without compromising tensile strength. Fluoropolymers, although comprising only a mid-single-digit slice of the engineering plastics market, post the fastest 7.34% CAGR because their unrivaled chemical and thermal resistance support aerospace wire coatings and sub-7 nm chip making.

Polysulfones, PEEK (Polyetheretherketone or Polyether Ether Ketone), and liquid-crystal polymers are suitable for niche applications where melting points exceed 280°C and continuous-use temperatures surpass 240°C. Polycarbonate endures scrutiny for BPA (Bisphenol A) in foodware but retains dominance in glazing and consumer electronics housings due to its impact resilience. Polyoxymethylene offers machining ease for gears and window lifters, while styrene copolymers bridge the gap between commodity ABS (Acrylonitrile Butadiene Styrene) and specialty blends, making them a go-to for appliance frames that require balanced toughness and cost.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Electronics Acceleration Challenges Packaging Leadership

Packaging captured a 50.10% share in 2025, buoyed by the production of PET bottles and rigid containers for household goods. Regulatory headwinds, however, prompt brands to evaluate monomaterial flexibles and paper composites, tempering volume growth after 2026. Electrical and electronics exhibit the strongest 6.98% CAGR, driven by AI server demand and miniaturized 5G hardware that utilizes LCP (Liquid Crystal Polymer) connectors and PPS (Programmable Power Supply) sockets, capable of withstanding reflow temperatures of up to 280°C.

Automotive programs adopt engineering thermoplastics for instrument panels, under-hood components, and newly critical battery enclosures. Aerospace sustains a smaller but lucrative niche, paying premiums for flight-certified grades that meet FAR 25.853 flammability thresholds. Industrial machinery relies on Polyoxymethylene (POM) and glass-filled PA to replace cast metals in pump impellers and conveyor parts, citing their superior corrosion resistance and quieter operation. Building and construction utilizes UV-stabilized PC sheets and weatherable Polymethyl Methacrylate (PMMA) for skylights and façades, demonstrating that the engineering plastics market continues to broaden beyond its historical strongholds.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Asia-Pacific region led with a 55.10% engineering plastics market share in 2025 and is expected to expand at a 5.38% CAGR through 2031, driven by the build-out of Chinese and Indian capacities, accelerating EV adoption, and sustained electronics export demand. Chinese styrene production, already 49% of global output, reinforces regional price leadership, while state policies encourage high-value polymer self-sufficiency. India leverages tax credits and import duty relief to draw multinational molders eyeing southern automotive hubs. Japan focuses on ultra-high-purity polymers for semiconductor photomasks, demonstrating the region’s spectrum from volume to value.

North America enjoys robust demand from the commercial aerospace sector and an expanding battery-manufacturing corridor that stretches from Michigan to Georgia. Legislative support for advanced recycling, including the US Internal Revenue Code § 45Z clean-fuel credits applicable to chemical recycling outputs, incentivizes innovation in the circular economy. Europe champions sustainability leadership through the Green Deal, spurring R&D in bio-based PA and chemically recycled polycarbonate, although high power costs and PFAS debates weigh on fluoropolymer capacity additions.

South America sees incremental growth tied to automotive localization in Brazil and Argentina, yet remains net-import-reliant for high-performance grades. Middle East & Africa emerge as investment destinations following ADNOC’s vertical integration move, which positions the region as a potential net exporter of specialty engineering resins once Covestro capacity synergies materialize. Across all regions, the globalization of supply chains means that engineering plastics market size evolves in lock-step with downstream manufacturing shifts rather than mere resin production footprints.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The Engineering Plastics market is moderately fragmented. The vertical integration of major players, including BASF, SABIC, DuPont, Covestro AG, Celanese Corporation, and Lanxess AG, into feedstocks, compounding, and downstream formulations enables them to capture margins across the entire value chain. ADNOC’s USD 16 billion acquisition of Covestro folds polycarbonate, MDI, and TPU expertise into a petrochemical powerhouse, potentially shifting competitive dynamics. New entrants capitalize on EV battery housings and structural composite stacks, often partnering with mold-in-place battery integrators. Start-ups with proprietary siloxane-based heat-dissipation fillers have won contracts for 2026 model-year inverter casings. As the engineering plastics market shifts toward circularity, alliances between resin majors and chemical recyclers are proliferating, promising closed-loop supply for high-purity grades and stabilizing long-term margins.

Engineering Plastics Industry Leaders

SABIC

BASF

DuPont

Covestro AG

Celanese Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Arkema unveiled plans for a new Rilsan Clear transparent polyamide unit at its Singapore facility. With an investment of approximately USD 20 million, the unit is slated to commence operations in the first quarter of 2026. This move will triple Arkema's global Rilsan Clear transparent polyamides production capacity.

- January 2025: Covestro AG invested significantly in its Hebron, Ohio site, pouring in a low triple-digit million Euro amount. This expansion will see the construction of multiple new production lines and infrastructure dedicated to producing customized polycarbonate compounds and blends.

Global Engineering Plastics Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Fluoropolymer, Liquid Crystal Polymer (LCP), Polyamide (PA), Polybutylene Terephthalate (PBT), Polycarbonate (PC), Polyether Ether Ketone (PEEK), Polyethylene Terephthalate (PET), Polyimide (PI), Polymethyl Methacrylate (PMMA), Polyoxymethylene (POM), Styrene Copolymers (ABS and SAN) are covered as segments by Resin Type. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.By Resin Type

| Fluoropolymer | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinylfluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub Resin Types | |

| Liquid Crystal Polymer (LCP) | |

| Polyamide (PA) | Aramid |

| Polyamide (PA) 6 | |

| Polyamide (PA) 66 | |

| Polyphthalamide | |

| Polybutylene Terephthalate (PBT) | |

| Polycarbonate (PC) | |

| Polyether Ether Ketone (PEEK) | |

| Polyethylene Terephthalate (PET) | |

| Polyimide (PI) | |

| Polymethyl Methacrylate (PMMA) | |

| Polyoxymethylene (POM) | |

| Styrene Copolymers (ABS, SAN) |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Resin Type | Fluoropolymer | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | ||

| Polytetrafluoroethylene (PTFE) | ||

| Polyvinylfluoride (PVF) | ||

| Polyvinylidene Fluoride (PVDF) | ||

| Other Sub Resin Types | ||

| Liquid Crystal Polymer (LCP) | ||

| Polyamide (PA) | Aramid | |

| Polyamide (PA) 6 | ||

| Polyamide (PA) 66 | ||

| Polyphthalamide | ||

| Polybutylene Terephthalate (PBT) | ||

| Polycarbonate (PC) | ||

| Polyether Ether Ketone (PEEK) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyimide (PI) | ||

| Polymethyl Methacrylate (PMMA) | ||

| Polyoxymethylene (POM) | ||

| Styrene Copolymers (ABS, SAN) | ||

| By End-User Industry | Aerospace | |

| Automotive | ||

| Building and Construction | ||

| Electrical and Electronics | ||

| Industrial and Machinery | ||

| Packaging | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- End-user Industry - Packaging, Electrical & Electronics, Automotive, Building & Construction, and Others are the end-user industries considered under the engineering plastics market.

- Resin - Under the scope of the study, consumption of virgin resins like Fluoropolymer, Polycarbonate, Polyethylene Terephthalate, Polybutylene Terephthalate, Polyoxymethylene, Polymethyl Methacrylate, Styrene Copolymers, Liquid Crystal Polymer, Polyether Ether Ketone, Polyimide, and Polyamide in the primary forms are considered. Recycling has been provided separately under its individual chapter.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF