Diisononyl Phthalate (DINP) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

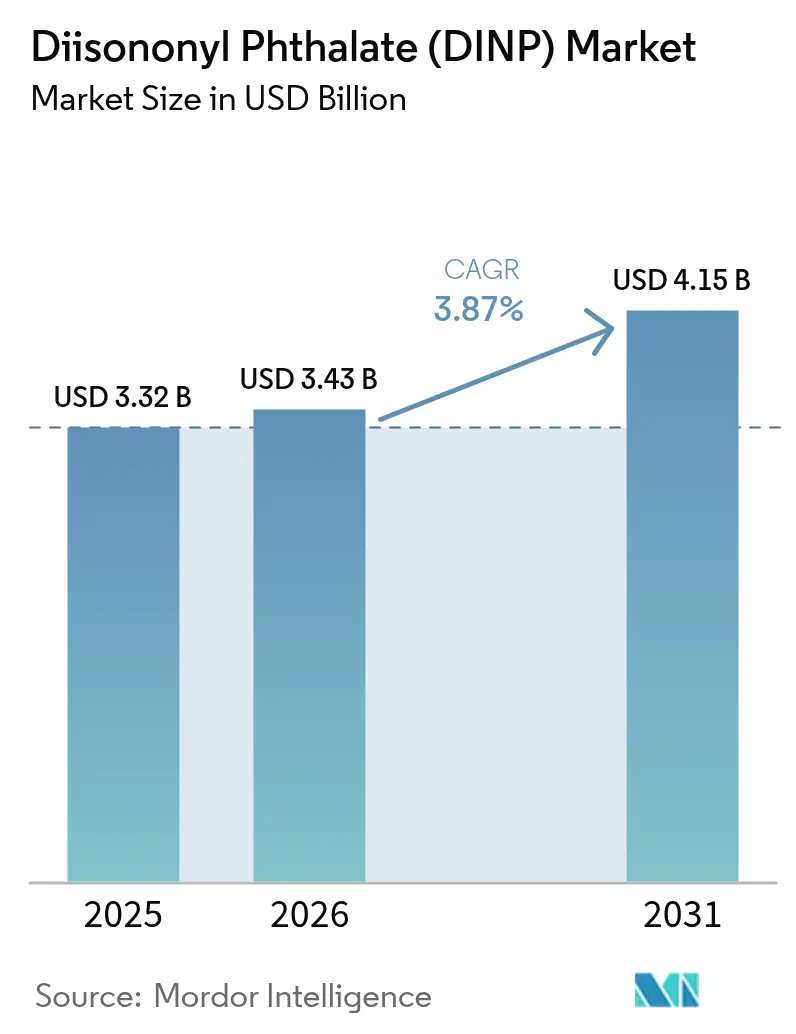

| Market Size (2026) | USD 3.43 Billion |

| Market Size (2031) | USD 4.15 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diisononyl Phthalate (DINP) Market Analysis by Mordor Intelligence

The Diisononyl Phthalate Market size is expected to grow from USD 3.32 billion in 2025 to USD 3.43 billion in 2026 and is forecast to reach USD 4.15 billion by 2031 at a 3.87% CAGR over 2026-2031. Robust infrastructure spending in Asia-Pacific, the rebound of global light-vehicle production, and steady demand for flexible PVC compounds support this expansion, even as end users in North America and Europe accelerate trials of non-phthalate substitutes. Construction projects in China, India, and the ASEAN bloc continue to pull in large volumes of PVC flooring, conduit, and piping, while 5G roll-outs are creating a niche for fire-retardant DINP grades that satisfy IEC 60332 flame benchmarks. Producers are therefore navigating a two-track environment: servicing price-sensitive growth regions with traditional DINP while allocating fresh capital toward low-migration chemistries for regulated markets. Competitive intensity remains moderate because backward-integrated capacity in Asia and incremental debottlenecking in Europe keep supply aligned with demand growth.

Key Report Takeaways

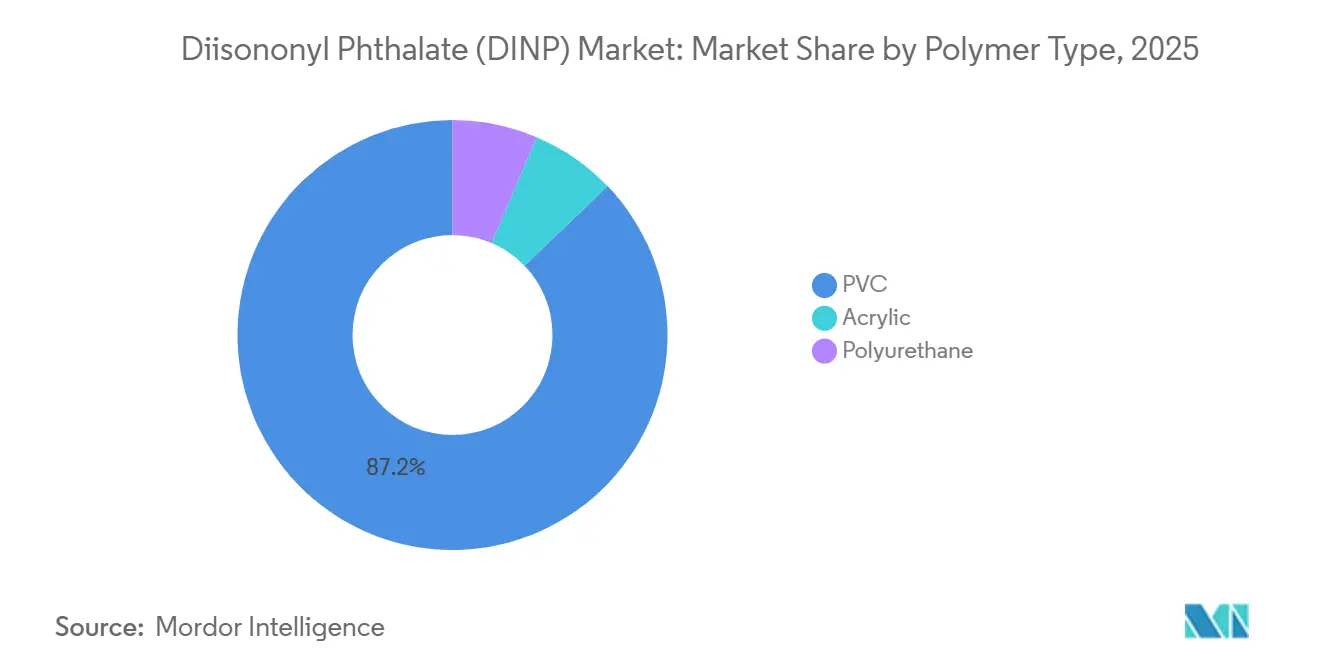

- By polymer type, PVC led with 87.19% of the Diisononyl Phthalate market share in 2025 and is progressing at a 4.09% CAGR through 2031.

- By application, floor and wall coverings accounted for 30.41% of the Diisononyl Phthalate market size in 2025 and are expanding at a 4.31% CAGR to 2031.

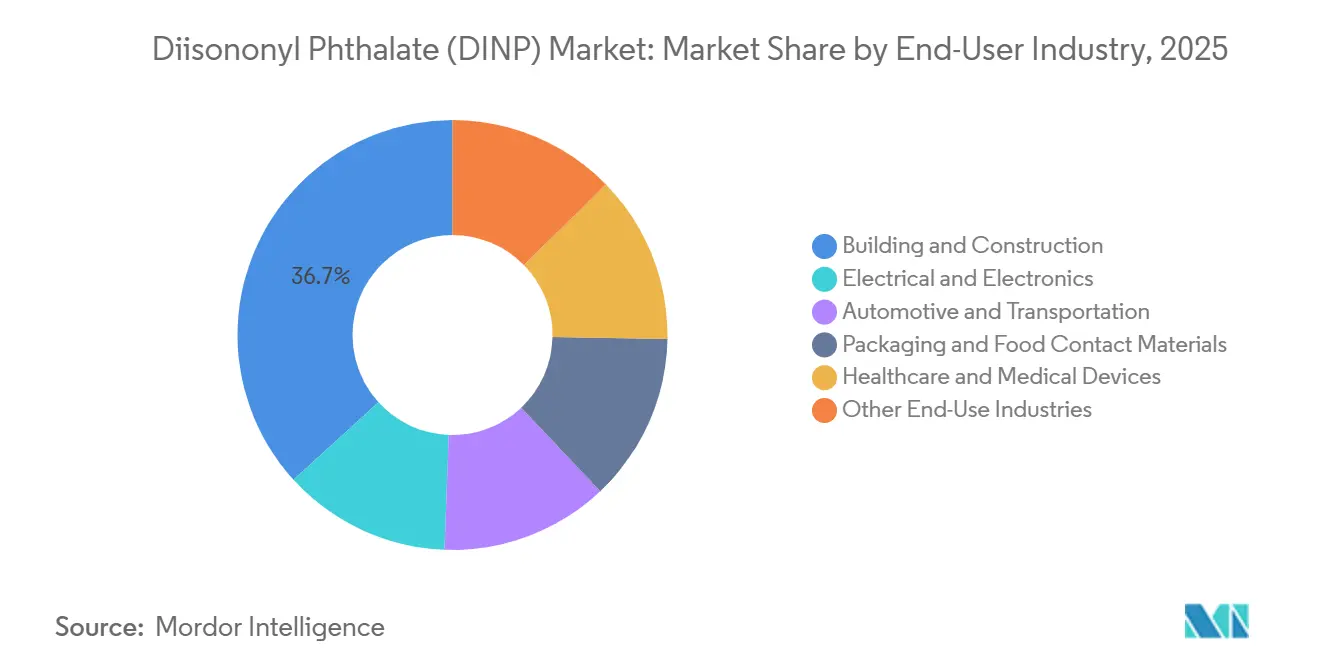

- By end user industry, building and construction captured 36.75% of the Diisononyl Phthalate market share in 2025; the segment is advancing at the highest recorded CAGR of 4.62% during the forecast window.

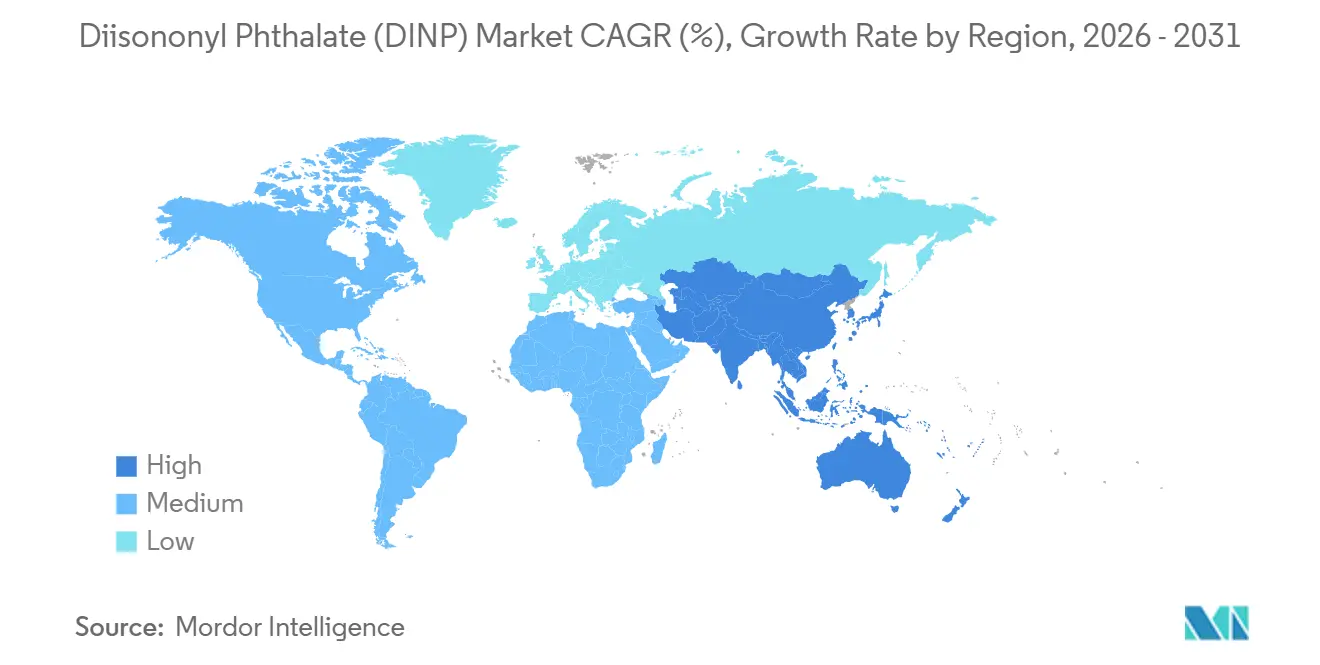

- By geography, Asia-Pacific held a dominant 59.26% revenue share in 2025; the region is on track to grow at a 4.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Diisononyl Phthalate (DINP) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for flexible PVC | +0.8% | Global, with APAC core accounting for 59.26% share | Medium term (2–4 years) |

| Expansion of building and construction sector | +0.7% | APAC (China, India, ASEAN), Middle East | Long term (≥4 years) |

| Rising consumption in electrical wire and cable insulation | +0.6% | Global, spill-over to MEA and South America | Medium term (2–4 years) |

| Post-COVID recovery of automotive production and lightweight interiors | +0.5% | North America, Europe, APAC (China, Japan, South Korea) | Short term (≤2 years) |

| Fire-retardant DINP grades for 5G high-frequency cables | +0.3% | North America, Europe, APAC urban centers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Flexible PVC

DINP continues to dominate as the primary plasticizer for flexible PVC, outpacing both bio-based and terephthalate alternatives in terms of cost-performance balance. In early 2025, China's chemical fixed-asset investments saw a year-on-year increase, directing funds into integrated ethylene-VCM-PVC hubs that capitalize on feedstock advantages. In 2024, Petronas Chemicals launched an isononyl alcohol unit in Malaysia, securing a captive feedstock that stabilizes DINP output against market fluctuations. Projections indicate global polymer demand will surge, with PVC consistently holding a steady market share. Consequently, the Diisononyl phthalate market is poised to maintain its PVC-centric focus throughout the forecast period.

Expansion of Building and Construction Sector

Emerging Asia's infrastructure-driven growth is bolstering the consumption of PVC in construction. India's National Infrastructure Pipeline emphasizes metro lines, affordable housing, and industrial corridors, all of which highlight the use of flexible PVC flooring and conduits. ASEAN grapples with a staggering infrastructure deficit. Moreover, local procurement regulations tend to prioritize immediate costs, inadvertently favoring DINP-plasticized products. In early 2025, China witnessed a surge in water-conservancy investments, leading to a spike in orders for plasticized PVC pipes. Meanwhile, a February 2025 revision by the European Commission to its Ecolabel sets limits on phthalate content in indoor flooring, underscoring a growing demand for non-phthalate alternatives in Europe.

Rising Consumption in Electrical Wire and Cable Insulation

As telecom densification and electrification surge, the demand for medium-voltage cables, known for their flexibility and fire resistance due to DINP, has risen. Projections indicate that the global fiber-optic cable market will more than double by 2035, subsequently boosting the demand for plasticized jacketing. In a move to bolster the industry, India rolled out its production-linked incentive scheme, spurring the establishment of new cable capacities. Meanwhile, to adhere to stringent national fire codes, China's high-speed rail corridors are utilizing DINP-blended, halogen-free cables. Given these developments, compounders are increasingly viewing the Diisononyl phthalate market as a crucial component of the electrification supply chain.

Post-COVID Recovery of Automotive Production and Lightweight Interiors

Global light-vehicle output bounced back in 2024 and is set to top in 2026. Automakers favor DINP-modified PVC skins for instrument panels, door trims, and seating because the additive delivers a competitive combination of softness, low VOC emissions, and fire safety. Japan’s export of automotive parts rose year-on-year in Q1 2025, and Hyundai earmarked a significant amount for electrification that will require cabin materials meeting ISO 12219-1 thresholds. This rebound reinforces the Diisononyl phthalate market outlook in transportation interiors.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny and health-risk assessments | -0.4% | North America, Europe, with spillover to APAC export-oriented manufacturers | Medium term (2–4 years) |

| Accelerated switch to bio/non-phthalate plasticizers | -0.4% | Europe, North America, Japan; emerging in urban China | Long term (≥4 years) |

| EU green-procurement criteria limiting VOC-rich flooring | -0.3% | Europe (Germany, France, Scandinavia), with indirect influence on North America public-sector tenders | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny and Health-Risk Assessments

In January 2025, the U.S. EPA's risk evaluation approved most uses of DINP. However, it raised concerns over spray applications, compelling producers to either enhance controls or pivot to alternatives[1]United States EPA, “Final Risk Evaluation for DINP,” epa.gov. California's AB 2300 mandates a DINP phase-out in intravenous bags for pediatric care and for adults. This pushes medical converters to consider alternatives like cyclohexane or citrate. In June 2024, the EU Scientific Committee on Health recommended a reduced migration ceiling. Following this, Regulation 2026/245, enacted in February 2026, imposed stricter limits on food contact[2]European Commission, “Regulation 2026/245 on Plasticizers,” europa.eu . These compliance demands are straining research and development budgets and complicating global supply chains, thereby moderating the growth rate of the Diisononyl phthalate market.

Accelerated Switch to Bio/Non-Phthalate Plasticizers

Non-phthalate plasticizers are steadily diminishing the market share of DINP in Europe and North America. Eastman’s Dominator is making strides in the resilient flooring sector, emphasizing the importance of LEED points. Meanwhile, Evonik is expanding its DINCH offerings, targeting OEMs in the toy and medical device sectors, aligning with REACH Annex XVII regulations. BASF’s Hexamoll DINCH is securing contracts in the baby-care film segment. In a notable industry shift, Teknor Apex's acquisition of Danimer Scientific in July 2025 underscores the trend of mid-tier compounders moving towards bio feedstocks. Collectively, these strategic maneuvers are steering purchasing decisions away from the Diisononyl phthalate market, especially in applications with stringent regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: PVC Holds Dominance while Alternatives Emerge

PVC represented 87.19% of 2025 volume in the Diisononyl phthalate market and is forecast to expand at a 4.09% CAGR to 2031. As a result, the market size of Diisononyl phthalate, closely tied to PVC, is poised to rise in tandem with construction demand in the Asia-Pacific region. In a strategic move, integrated producers in China and Malaysia leverage captive isononyl alcohol streams, allowing them to navigate feedstock volatility and maintain healthy margins. On the other hand, while acrylic and polyurethane together command a modest share, they are gradually gaining traction in coatings and sealants that demand lower glass-transition temperatures without compromising on hardness. In Europe, a phthalate limit in indoor coatings is steering the industry towards adipate and citrate alternatives. However, in the cost-sensitive APAC region, DINP usage remains steady.

The Diisononyl phthalate market presents a dual narrative: while PVC applications lead in volume, niche specialty formulas in acrylics and polyurethanes carve out smaller, yet lucrative, margins. Looking ahead, producers foresee a gradual decline in DINP usage within EU and U.S. polymer systems. Yet, this dip is expected to be balanced by modest increases in regions like South Asia and the Middle East, where economic factors make substitutions less appealing. Thus, while the Diisononyl phthalate market remains firmly rooted in PVC, it must navigate and adapt to regional compliance differences.

By Application: Flooring Retains Lead, Cables Accelerate

Floor and wall coverings held 30.41% of 2025 demand and are expected to post a 4.31% CAGR, supported by residential projects and retrofit activity. As India expands its metro systems and Indonesia pushes for public housing, both nations are increasingly opting for PVC flooring. This trend has bolstered the Diisononyl phthalate market size. However, Europe's Ecolabel cap is steering public tenders towards terephthalate or bio-based solutions, leading global suppliers to adopt a dual-portfolio strategy.

Wire and cable insulation, constituting a notable share of total plasticizer consumption, is reaping benefits from the 5G roll-out and grid hardening initiatives. The Diisononyl phthalate market's foothold in this segment is strengthened by formulations compliant with international standards. This segment's expansion outpaces that of flooring. While films, sheets, and coated fabrics command a combined share, they grapple with stringent regulatory oversight concerning food contact and consumer safety. Despite this diversification in application demand, flooring and cables remain pivotal to the Diisononyl phthalate market's trajectory.

By End-User Industry: Construction Dominates, Healthcare Faces Substitution

Building and construction captured 36.75% of 2025 revenue, and the segment records the highest expected CAGR at 4.62% to 2031. China's investment in water-conservancy infrastructure surged, driven by flood-control and irrigation projects requiring plasticized PVC piping. India's infrastructure budget prioritizes urban metro systems, affordable housing, and industrial corridors, all utilizing flexible PVC materials. Southeast Asian nations face significant infrastructure financing gaps, favoring DINP-plasticized PVC due to cost-focused procurement rules. In contrast, Europe's green-procurement standards are steering demand toward phthalate-free flooring, requiring dual product portfolios from producers.

Electrical and electronics benefit from 5G infrastructure deployment, driving demand for fire-retardant DINP grades. Automotive and transportation sectors are recovering, boosting demand for DINP-plasticized components. Packaging faces challenges from stricter EU regulations, while healthcare is under pressure to phase out DINP in medical devices, prompting validation of alternatives. Other sectors, including toys and sporting goods, face stringent safety directives limiting phthalate content.

Geography Analysis

Asia-Pacific contributed 59.26% of global revenue in 2025 and is on track for a 4.22% CAGR to 2031. In the first two months of 2025, China invested heavily in infrastructure, with water-conservancy projects witnessing a notable year-on-year increase. For FY 2024-25, India set aside substantial funds for infrastructure, and its electronics PLI scheme led to a significant boost in cable production. ASEAN countries grapple with a major infrastructure shortfall, with a pronounced preference for DINP-based PVC, as budgets lean towards capital expenditures rather than life-cycle costs. Petronas’s INA unit, operational since 2024, bolsters supply security in Southeast Asia. Meanwhile, Japan and South Korea, driven by automaker demands for stringent cabin-air-quality standards, are focusing on premium low-VOC applications.

North America and Europe, while accounting for a considerable portion of 2025's consumption, are witnessing slower growth, largely due to stringent health regulations. The U.S. EPA’s risk assessments, coupled with California’s phased-out pediatric care, are curtailing volumes in medical applications. Simultaneously, EU Ecolabel regulations are limiting DINP usage in indoor flooring. Yet, these regions continue to import cost-effective DINP for industrial uses and products destined for export, ensuring a steady demand.

South America and the Middle-East-Africa make up the remaining portion of the market value. Brazil’s housing incentives, alongside Saudi Arabia’s Vision 2030-driven hospitality surge, are sustaining demand for DINP in flooring. Additionally, Egypt’s ambitious water-and-sanitation initiative is boosting the usage of PVC pipes. Despite price sensitivities and a more lenient enforcement landscape, local buyers are upholding DINP specifications, solidifying the market's presence.

Competitive Landscape

The diisononyl phthalate market is moderately consolidated. White-space innovation centers on fire-retardant DINP grades for 5G cabling and medical formulations meeting ISO 10993 without the full cost of DINCH. Chinese independents gain feedstock efficiency from integrated clusters but lack research and development heft for specialty niches. Overall, strategy revolves around safeguarding core Diisononyl phthalate market earnings while capturing premium margins in regulated replacements.

Diisononyl Phthalate (DINP) Industry Leaders

Exxon Mobil Corporation

BASF

Evonik Industries AG

LG Chem

UPC Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The United States Environmental Protection Agency (EPA) completed risk evaluations for Diisononyl Phthalate (DINP) under the Toxic Substances Control Act (TSCA). The evaluations identified unreasonable health risks for workers exposed to spray-applied products containing these chemicals. Following these findings, the EPA must implement risk management measures to address the identified hazards.

- October 2023: BASF signed a technology licensing agreement with Ningbo Refining and Chemical Co. Ltd (NZRCC) to use its proprietary oxo-technology for isononyl alcohol (INA) production. INA, an essential component in manufacturing Diisononyl Phthalate (DINP), strengthens BASF's DINP supply chain.

Global Diisononyl Phthalate (DINP) Market Report Scope

Diisononyl Phthalate (DINP) is produced industrially by esterification of phthalic anhydride with isononyl alcohol. Diisononyl Phthalate (DINP) is used for a variety of applications in different industries.

The diisononyl phthalate (DINP) market is segmented by polymer type, application, end-user industry, and geography. By polymer type, the market is segmented into PVC, acrylic, and polyurethane. By application, the market is segmented into floor and wall coverings, coated fabrics, consumer goods, films and sheets, wires and cables, and other applications. By end-user industry, the market is segmented into building and construction, electrical and electronics, automotive and transportation, packaging and food contact materials, healthcare and medical devices, and other end-use industries. The report also covers the market size and forecasts for the market in 19 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| PVC |

| Acrylic |

| Polyurethane |

| Floor and Wall Coverings |

| Coated Fabrics |

| Consumer Goods |

| Films and Sheets |

| Wires and Cables |

| Other Applications |

| Building and Construction |

| Electrical and Electronics |

| Automotive and Transportation |

| Packaging and Food Contact Materials |

| Healthcare and Medical Devices |

| Other End-Use Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Polymer Type | PVC | |

| Acrylic | ||

| Polyurethane | ||

| By Application | Floor and Wall Coverings | |

| Coated Fabrics | ||

| Consumer Goods | ||

| Films and Sheets | ||

| Wires and Cables | ||

| Other Applications | ||

| By End-User Industry | Building and Construction | |

| Electrical and Electronics | ||

| Automotive and Transportation | ||

| Packaging and Food Contact Materials | ||

| Healthcare and Medical Devices | ||

| Other End-Use Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Diisononyl phthalate market by 2031?

It is expected to reach USD 4.15 billion by 2031, growing at a 3.87% CAGR from USD 3.43 billion in 2026.

Which polymer type dominates DINP consumption?

PVC accounts for 87.19% of the 2025 volume and retains the top spot through the forecast period.

How significant is the Asia-Pacific region in terms of DINP demand?

Asia-Pacific generated 59.26% of global revenue in 2025 and is growing at a 4.22% CAGR.

How are regulations affecting DINP usage in medical devices?

California’s AB 2300 and new EU migration limits are pushing suppliers to phase out DINP in intravenous bags and tubing by 2035 at the latest.

Page last updated on: