Grid-Scale Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 111.08 Billion |

| Market Size (2031) | USD 323.68 Billion |

| Growth Rate (2026 - 2031) | 23.85% CAGR |

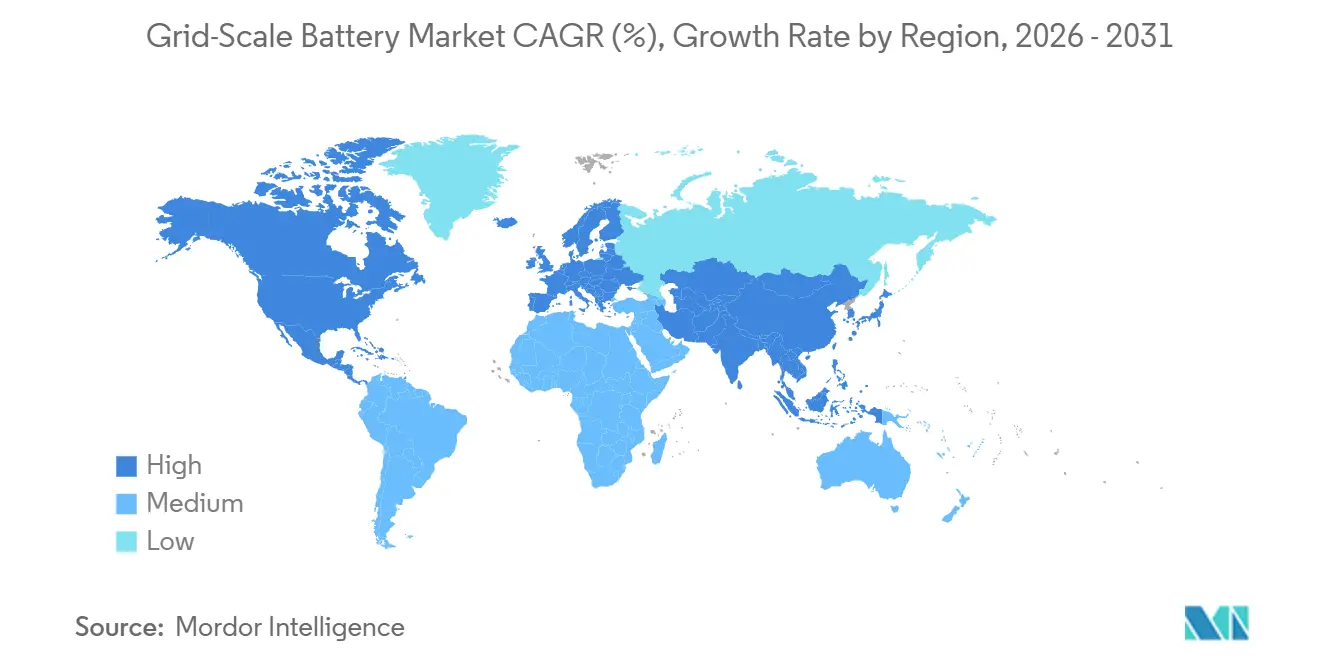

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

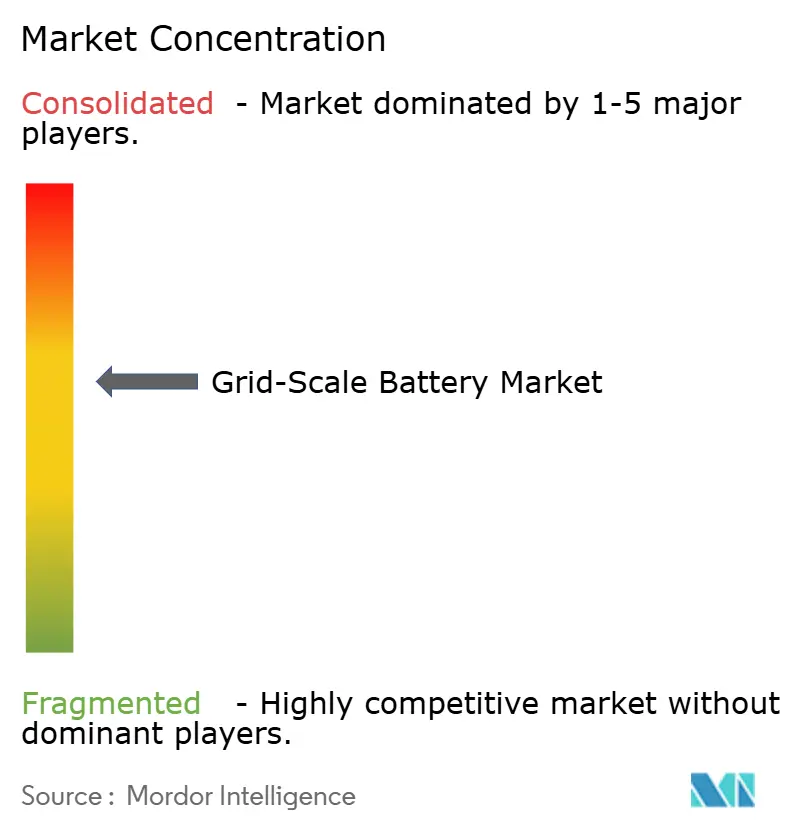

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grid-Scale Battery Market Analysis by Mordor Intelligence

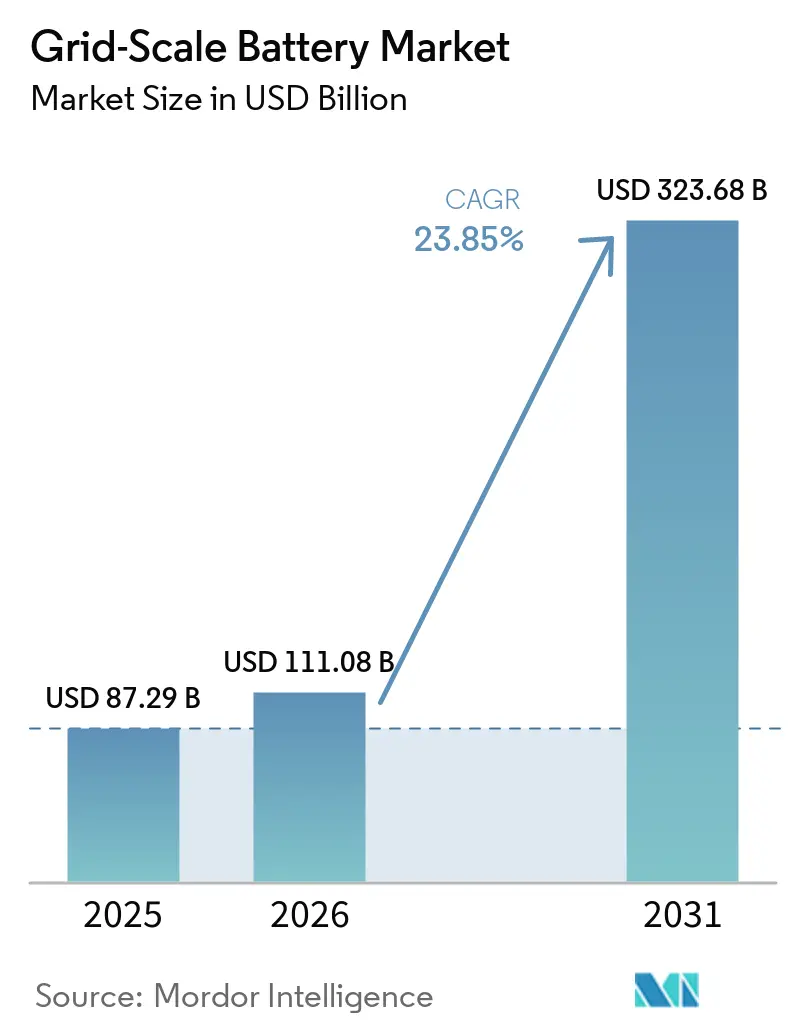

The Grid-Scale Battery Market size was valued at USD 87.29 billion in 2025 and is estimated to grow from USD 111.08 billion in 2026 to reach USD 323.68 billion by 2031, at a CAGR of 23.85% during the forecast period (2026-2031).

Strong lithium-ion cost declines, policy tailwinds such as the U.S. Inflation Reduction Act, and mandatory storage requirements in China and the European Union are accelerating utility procurement cycles. Competition is polarizing around vertically integrated manufacturers that own cell, pack, and software capabilities, while pure-play integrators differentiate through grid-forming inverters and advanced controls. Revenue stacking across energy, capacity, and ancillary services is maturing, creating durable cash-flow profiles that attract infrastructure investors. Supply-chain resilience is emerging as a decisive advantage because mineral bottlenecks and fire-safety rules are reshaping chemistry selection and plant design.

Key Report Takeaways

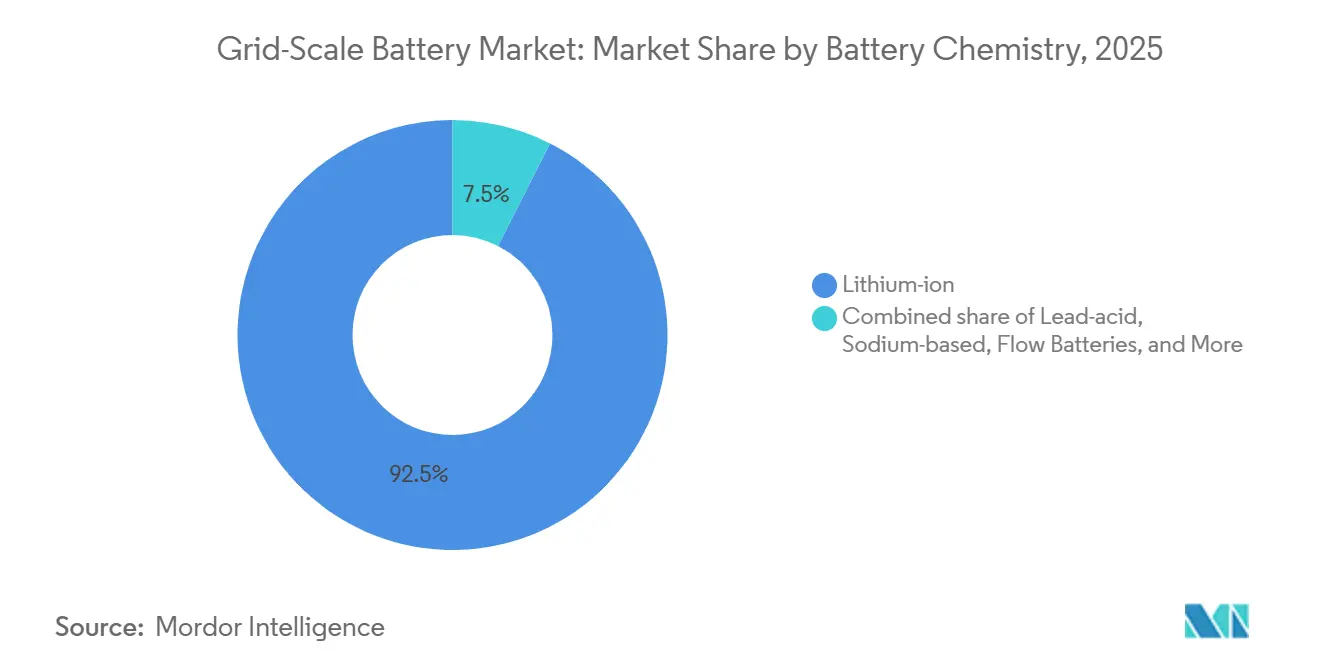

- By battery chemistry, lithium-ion technologies led with 92.5% revenue share in 2025, while lithium-iron-phosphate is projected to grow at 24.2% CAGR through 2031.

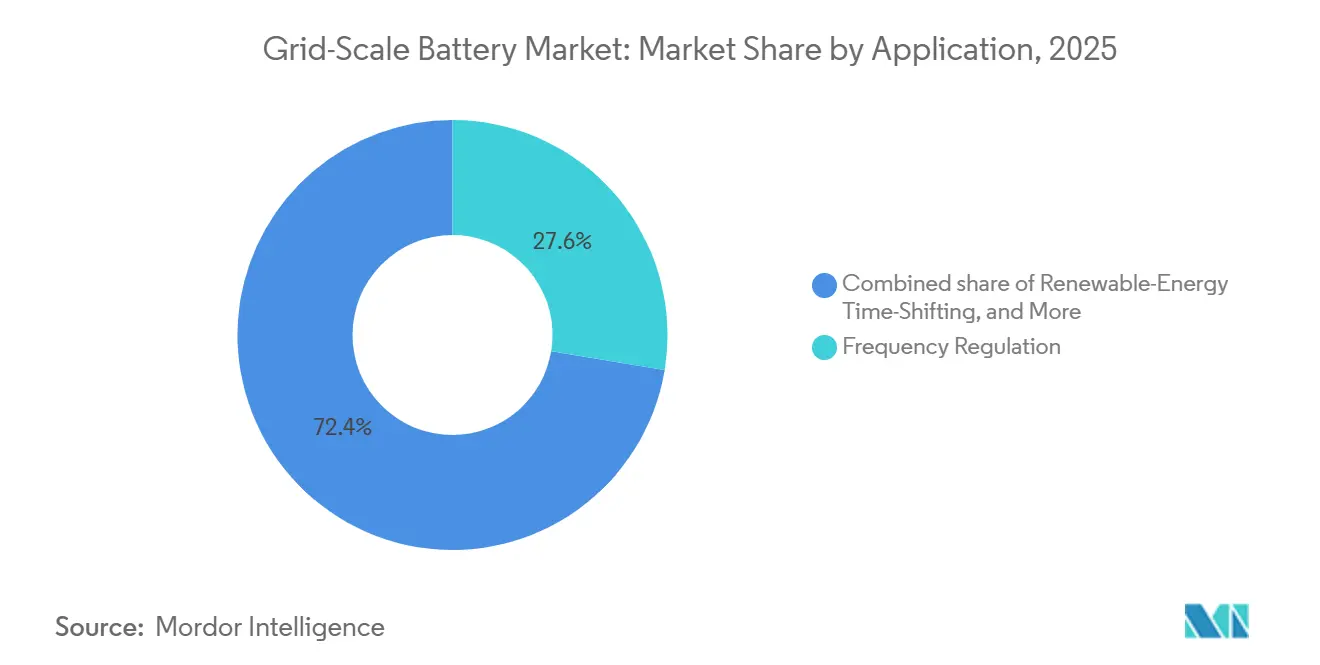

- By application, frequency regulation held 27.6% of the global grid-scale battery market share in 2025, whereas renewable-energy time-shifting is expected to expand at a 26.3% CAGR to 2031.

- By geography, Asia-Pacific commanded 47.4% of 2025 deployments and is expected to advance at a 25.4% CAGR to 2031, driven by China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Grid-Scale Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion battery costs | +6.2% | Global with peaks in North America, Europe, China | Medium term (2-4 years) |

| Renewable-energy integration mandates | +5.8% | EU, China, India, emerging ASEAN and Latin America | Long term (≥ 4 years) |

| Grid reliability and resiliency needs | +4.1% | North America, Australia, Nordic Europe | Short term (≤ 2 years) |

| Favorable policy incentives | +4.7% | North America, EU core, spillover to Middle East and South America | Medium term (2-4 years) |

| Hybrid solar-plus-storage PPAs & revenue stacking | +3.4% | North America, Australia, Spain, Italy | Medium term (2-4 years) |

| Data-center microgrids demand firm clean power | +2.9% | North America, EU, early in Singapore and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Battery Costs

Pack prices for lithium-iron-phosphate cells fell to USD 89 per kWh in 2025, a 36% reduction from 2023 as Chinese gigafactories reached 95% yield, pushing four-hour systems below natural-gas peaker costs in carbon-priced markets. CATL’s high-density Qilin architecture shaved 12% from balance-of-system expenses and enabled brownfield retrofits at retired coal sites. Emerging sodium-ion products priced near USD 60 per kWh broaden the chemistry mix for long-duration storage. The glidepath signals USD 70 per kWh by 2028, eroding the cost edge of pumped hydro and compressed-air options.

Renewable-Energy Integration Mandates

China’s rule that wind and solar plants pair 10-20% storage triggered 18 GW of battery orders in 2025 and sliced curtailment rates in high-renewable provinces below 3%.[2]National Energy Administration of China, “Storage Requirements for New Wind and Solar,” nea.gov.cn India now requires two-hour firming for renewable certificates, adding 6 GW of demand, while the EU’s Renewable Energy Directive III will necessitate 45 GW of co-located storage by 2030. Standardized testing under IEC 62933 is lengthening commissioning timelines but secures finance by de-risking performance.

Grid Reliability and Resiliency Needs

Texas and California implemented rules valuing dispatchable capacity after recent blackouts, directing 17 GW of procurements toward batteries between 2024 and 2026.[3]Federal Energy Regulatory Commission, “Reliability Standards Update,” ferc.gov Australia classified grid-forming batteries as system-strength assets, unlocking separate capacity payments and enabling remote deployments. Utilities now pay more for availability than for pure energy, with capacity and ancillary revenue moving from 30% of project cash flow in 2023 to half in 2026.

Favorable Policy Incentives

The U.S. Inflation Reduction Act slashed the after-tax cost of a 100 MW / 400 MWh plant from USD 60 million to USD 36 million, cutting payback from nine to 5.5 years.[4]U.S. Department of Energy, “Inflation Reduction Act Battery Storage Guidance,” energy.gov EU grants and concessional loans encourage local content, while Saudi Arabia’s hydrogen program mandates 4 GW of storage. These incentives reshape supply chains toward regional production even at an 8-12% cost premium.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral supply-chain constraints | -3.8% | Global, acute in Australia, Chile, DRC | Medium term (2-4 years) |

| Battery storage safety and fire-risk concerns | -2.1% | North America, Europe, South Korea | Short term (≤ 2 years) |

| Interconnection-queue bottlenecks | -2.6% | United States, India, Spain, Italy | Medium term (2-4 years) |

| Ancillary-service revenue cannibalization | -1.9% | California, Texas, Australia, UK, Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Supply-Chain Constraints

Lithium demand exceeded supply by 200,000 t in 2025, lifting spot prices 50% into early 2026 despite previous softening. Australian and DRC permitting delays reinforced a pivot toward cobalt-free chemistries and stimulated early adoption of sodium-ion and iron-air formats, which captured 3% of installations.

Battery-Storage Safety and Fire-Risk Concerns

Thermal-runaway incidents in South Korea, California, and Germany cost USD 120 million and led to UL 9540A and NFPA 855 rules that add 15-20% to project footprints. Insurance premiums rose to 60%, favoring vertically integrated suppliers that can self-insure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Safety-Driven Shift Toward LFP Gains Momentum

Lithium-ion products dominated the global grid-scale battery market with 92.5% share in 2025. Within this umbrella, lithium-iron-phosphate captured most new orders because regulators in California and Germany now prefer chemistries that pass stringent fire-propagation tests. The segment’s 24.2% CAGR through 2031 makes it the primary driver of global grid-scale battery market growth. Sodium-ion and vanadium-flow systems are carving out a niche for eight-hour and longer applications where energy density matters less than mineral independence and calendar life.

Growth in lithium-iron-phosphate lowers average energy density but improves thermal stability, cutting insurance premiums while satisfying UL 9540A requirements. The global grid-scale battery market size for lithium-ion technologies is projected to climb from USD 97 billion in 2026 to USD 281 billion by 2031 at a 24% CAGR. Metal-air and solid-state concepts remain experimental yet attract R&D funding as utilities seek alternatives to lithium supply risk. Regulations such as IEC 62933 and NFPA 855 tighten qualification, accelerating chemistry diversification across the global grid-scale battery industry.

By Application: Time-Shifting Leads Commercial Value Creation

Frequency regulation represented 27.6% of global grid-scale battery market revenue in 2025, reflecting the first wave of utility deployments. However, renewable-energy time-shifting is now advancing at a 26.3% CAGR, outpacing the overall market and absorbing surplus solar and wind during midday troughs. The global grid-scale battery market share for frequency regulation is expected to fall below 20% by 2031 as multi-hour systems pivot toward energy arbitrage and firm capacity products.

Corporate adopters such as data-center operators use batteries for peak shaving and power-quality support, adding a predictable revenue layer that improves debt service coverage. Transmission and distribution deferral, while niche today, benefits rural networks in Australia and the U.S. Midwest, where upgrade costs exceed USD 1 million per mile. Black-start and grid-forming capabilities are increasingly embedded in procurement specifications, cementing their role in resilience strategies and broadening the opportunity set for integrators across the global grid-scale battery market.

Geography Analysis

Asia-Pacific led the global grid-scale battery market with 47.4% of 2025 installations, and its 25.4% CAGR to 2031 stems from China’s 25 GW build in 2025 and India’s new ancillary-services rules. The region benefits from domestic supply chains that buffer mineral price shocks and from mandates that bundle storage with renewables, creating predictable order books for CATL, BYD, and Gotion High-Tech. Chinese provincial curtailment fell below 3% as required storage ratios reduced oversupply events, reinforcing policy momentum.

North America surged after the Inflation Reduction Act unlocked USD 20 billion in announcements during 2024-2025. Texas and California account for over two-thirds of capacity additions, encouraged by resilience standards and clean-firm mandates. Data-center procurement in Virginia, Oregon, and Arizona is catalyzing six-hour systems that guarantee 24/7 clean power. UL 9540A and NFPA 855 rules standardize safety, extending project timelines but lifting investor confidence. The global grid-scale battery market size attributable to North America is forecast to rise from USD 29 billion in 2026 to USD 85 billion in 2031, equal to a 23% CAGR.

Europe is modernizing its grid with Germany, Spain, and the Nordics at the forefront. The EU Net-Zero Industry Act’s 90 GW battery-manufacturing target and concessional loans accelerate regional supply chains. Transmission operators require dynamic stability studies for inverter-based resources, spurring demand for grid-forming capabilities. Eastern Europe and the Mediterranean are early in the adoption curve but view storage as a hedge against renewable curtailment and rising gas prices. Collectively, these factors sustain 22% annual growth across the global grid-scale battery market in Europe through 2031.

Competitive Landscape

Market power is concentrating around CATL, BYD, and Tesla, which combine cell supply, pack assembly, and proprietary energy-management platforms. Their scale permits aggressive pricing that undercuts integrators reliant on spot-market cells, while in-house software captures up to 70% of system value. Fluence and Wärtsilä remain competitive through grid-forming inverters and performance guarantees that appeal to transmission operators seeking inertia and black-start services.

Long-duration storage represents fertile ground for challengers. ESS Tech’s iron-flow battery won a 500 MW award in Australia, and Ambri’s liquid-metal pilot demonstrated multi-day storage in Massachusetts. These systems sidestep lithium and cobalt constraints, meeting safety codes without thermal-runaway risk. Corporations with net-zero pledges are signing 15-year contracts that assure minimum cycling, creating stable cash flows attractive to pension funds and sovereign wealth investors.

Patent filings covering advanced thermal management and inverter control jumped after 2024, reflecting an innovation race to satisfy stricter UL 9540A, IEC 62933, and NFPA 855 requirements. Compliance creates barriers for small entrants yet offers incumbents a moat if they can certify faster. Overall, the competitive dynamics reinforce 6% market concentration on the proprietary 1-10 scale, as the top three suppliers together command roughly two-thirds of annual shipments.

Grid-Scale Battery Industry Leaders

Tesla (Megapack)

Fluence

Sungrow Power Supply

CATL

Wärtsilä

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NUVVE Japan plans to deploy a 2 MW/8 MWh grid-scale battery energy storage system in Mino City, Gifu Prefecture, by November 2026. Utilizing the Nuvve Platform and Sungrow technology, the system will contribute to grid stability, enable market participation, and generate revenue streams while expanding Nuvve’s energy storage presence in Japan.

- October 2025: Energy Vault announced the acquisition of the 150 MW/300 MWh SOSA Energy Center battery energy storage system in Texas under its Asset Vault platform. Construction is scheduled to begin in Q4 2025, with operations targeted for Q1 2027. The project aims to support renewable energy integration, enhance grid resilience, and expand the company's grid-scale storage portfolio.

- August 2025: Peak Energy launched the first grid-scale sodium-ion battery energy storage system in a U.S. pilot project in collaboration with utilities and independent power producers. Featuring a passive cooling design, the system reduces operational costs and improves reliability, representing a significant step toward scalable and cost-effective sodium-ion storage solutions that support grid resilience.

- July 2025: Honeywell completed the acquisition of the Li-ion Tamer business from Nexceris to improve early off-gas detection for lithium-ion battery systems. This acquisition enhances safety monitoring for grid-scale battery storage, renewable energy systems, and EV infrastructure, addressing the growing risks of thermal runaway as energy storage demand increases.

Global Grid-Scale Battery Market Report Scope

The grid-scale battery market encompasses the global industry involved in the development, manufacturing, deployment, and operation of large-scale battery energy storage systems (BESS) designed to store and supply electricity directly to power grids.

The global grid-scale battery market report is segmented by battery chemistry (lithium-ion (LFP, NMC, NCA), lead-acid, sodium-based (NAS, Sodium-ion), flow batteries (Vanadium, Iron, Zinc-Br), and other emerging chemistries (Metal-air, Solid-state)), application (frequency regulation, energy arbitrage/bill management, load shifting and peak shaving, renewable-energy time-shifting, transmission and distribution deferral, and black-start and grid-forming support), and geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD billion).

| Lithium-ion (LFP, NMC, NCA) |

| Lead-acid |

| Sodium-based (NAS, Sodium-ion) |

| Flow Batteries (Vanadium, Iron, Zinc-Br) |

| Other Emerging Chemistries (Metal-air, Solid-state) |

| Frequency Regulation |

| Energy Arbitrage/Bill Management |

| Load Shifting and Peak Shaving |

| Renewable-Energy Time-Shifting |

| Transmission and Distribution Deferral |

| Black-Start and Grid-Forming Support |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Chemistry | Lithium-ion (LFP, NMC, NCA) | |

| Lead-acid | ||

| Sodium-based (NAS, Sodium-ion) | ||

| Flow Batteries (Vanadium, Iron, Zinc-Br) | ||

| Other Emerging Chemistries (Metal-air, Solid-state) | ||

| By Application | Frequency Regulation | |

| Energy Arbitrage/Bill Management | ||

| Load Shifting and Peak Shaving | ||

| Renewable-Energy Time-Shifting | ||

| Transmission and Distribution Deferral | ||

| Black-Start and Grid-Forming Support | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will grid-scale batteries become by 2031?

The global grid-scale battery market size is forecast to reach USD 323.68 billion by 2031 at a 23.85% CAGR from 2026 to 2031.

Which battery chemistry is growing fastest?

Lithium-iron-phosphate leads with a projected 24.2% CAGR through 2031 due to safety advantages and falling costs.

Why are hybrid solar-plus-storage contracts popular?

Stacking energy, capacity, and renewable-credit revenue raises project returns by roughly 4 percentage points compared with standalone solar.

How are policy incentives shaping storage economics?

The U.S. IRA's 30% tax credit and EU low-interest loans cut payback periods to about 5-6 years for four-hour systems.

What limits storage deployment in the United States?

Interconnection queues now average more than five-year wait times, delaying about 2.6 TW of proposed generation and storage.

Are long-duration alternatives to lithium emerging?

Yes, sodium-ion, iron-flow, and liquid-metal batteries captured a combined 3% of 2025 installations, targeting eight-hour or longer use cases.

Page last updated on: