Lithium-ion Battery For Electric Vehicle Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

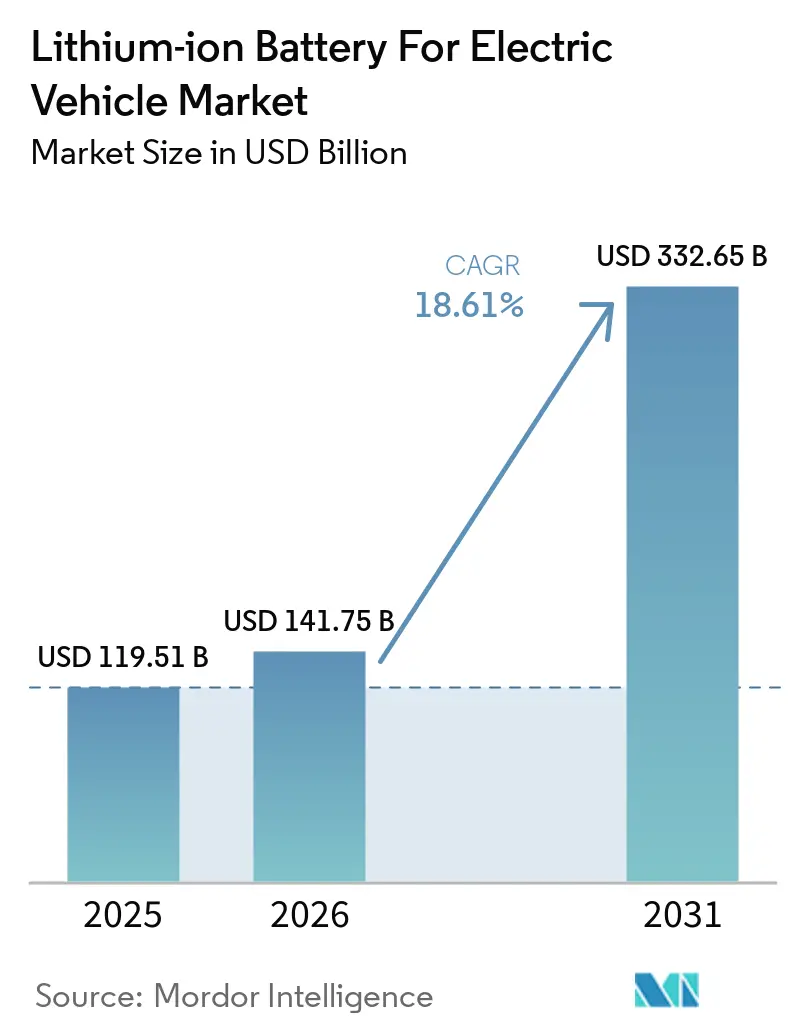

| Market Size (2026) | USD 141.75 Billion |

| Market Size (2031) | USD 332.65 Billion |

| Growth Rate (2026 - 2031) | 18.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

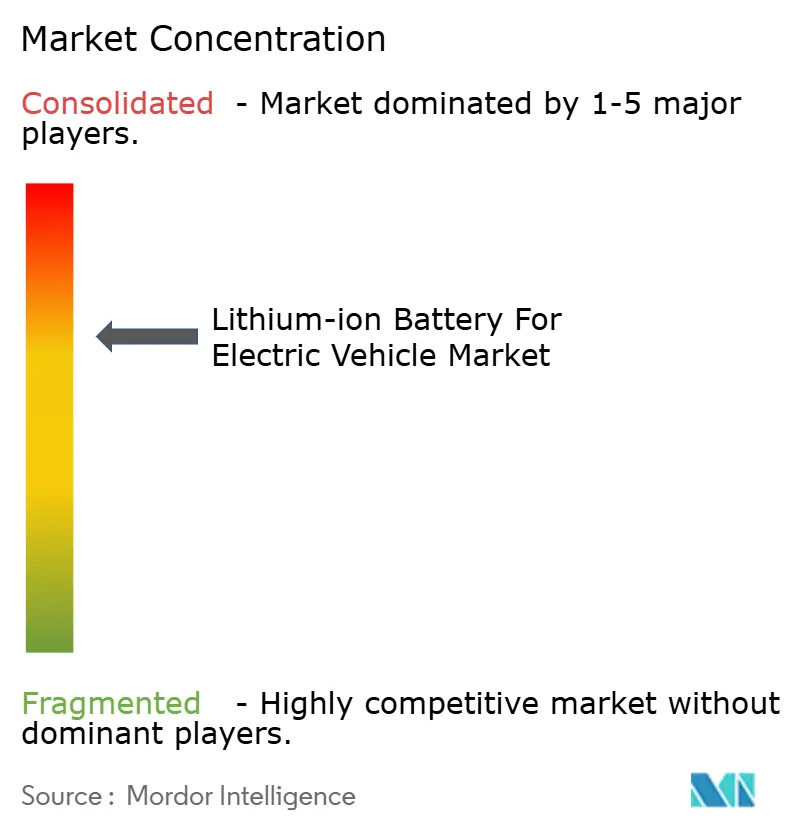

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lithium-ion Battery For Electric Vehicle Market Analysis by Mordor Intelligence

Lithium-ion Battery For Electric Vehicle Market size in 2026 is estimated at USD 141.75 billion, growing from 2025 value of USD 119.51 billion with 2031 projections showing USD 332.65 billion, growing at 18.61% CAGR over 2026-2031.

Automakers are shifting from outsourced cells to in-house gigafactories, compressing supply-chain risk while chasing pack costs below USD 80/kWh that unlock price parity with internal-combustion cars. Policy incentives in the United States, the European Union, and India have redirected nearly USD 100 billion toward on-shore cell plants, diluting Asia’s historic dominance and supporting a cascade of joint-venture announcements.(1)“Biden’s Climate Law Spurs U.S. Battery-Factory Boom,” energy.gov Meanwhile, rapid heavy-truck electrification mandates, 800-V platform adoption, and LFP’s cobalt-free cost edge are widening the addressable customer base, especially in two-wheelers and delivery vans. Competitive pressure is intense: vertically integrated OEM programs such as Tesla’s 4680 and BYD’s Blade are squeezing mid-tier suppliers’ gross margins below 10%, triggering consolidation and accelerating gigafactory scale-ups.

Key Report Takeaways

- By battery chemistry, lithium-iron-phosphate captured 44.65% share of China’s passenger segment in 2025, and solid-state prototypes are forecast to post a 30.90% CAGR through 2031.

- By cell format, prismatic designs commanded 47.55% share in 2025, yet pouch cells are growing fastest at 22.80% CAGR as European automakers favor flexible packaging.

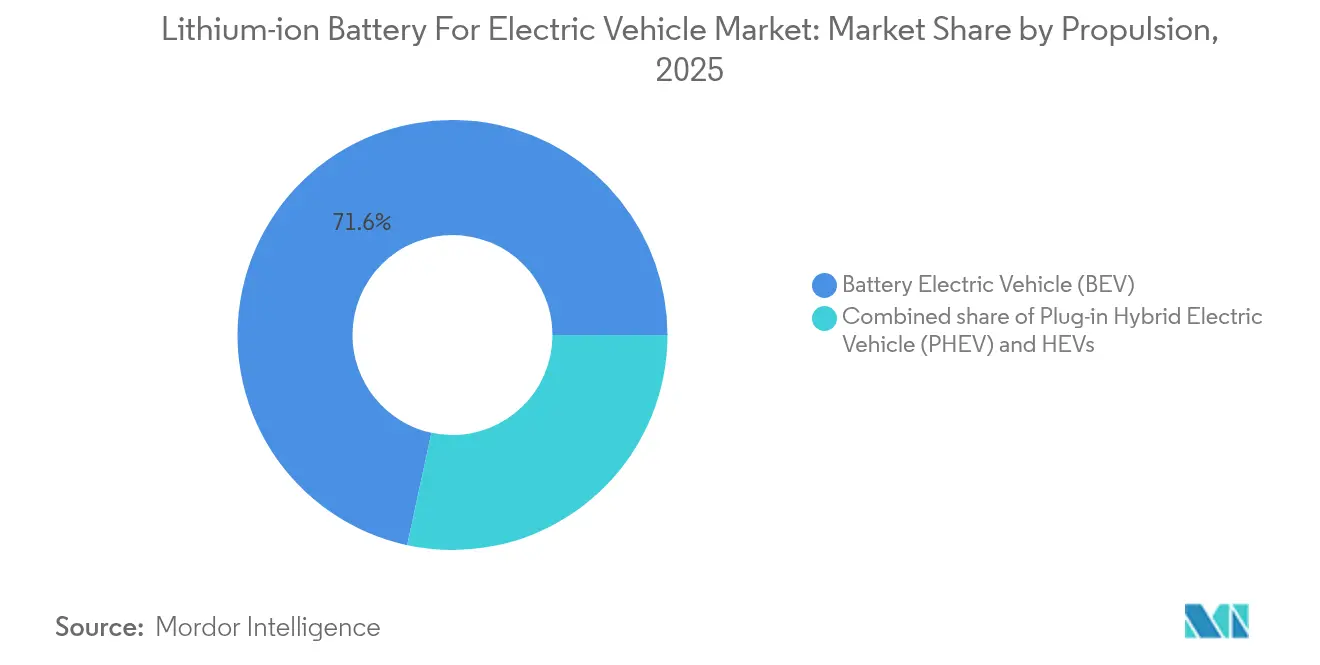

- By propulsion, battery electric vehicles accounted for 71.62% of 2025 cell demand, expanding at a 21.15% CAGR that eclipses plug-in hybrids.

- By vehicle type, passenger cars retained 70.12% volume in 2025, while two- and three-wheelers are scaling at a 31.20% CAGR through 2031 on the back of India’s swap-station rollout.

- By geography, Asia-Pacific led with 50.35% of the Lithium-ion battery market share in 2025, while North America is poised for the fastest 22.05% CAGR to 2031 as IRA subsidies spur local capacity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lithium-ion Battery For Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining pack prices below USD 80/kWh by 2029 | +4.20% | Global, strongest in North America, EU | Medium term (2-4 years) |

| Heavy-duty truck electrification mandates | +3.80% | China, EU, United States | Short term (≤2 years) |

| OEM vertical integration | +3.50% | China, North America | Medium term (2-4 years) |

| On-shoring gigafactories via subsidies | +4.10% | North America, Europe, India | Long term (≥4 years) |

| 800-V fast-charging architectures | +2.70% | Europe, North America, China premium | Medium term (2-4 years) |

| LFP cost edge in price-sensitive 2W/3W markets | +3.90% | India, ASEAN with spillover to Africa | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Battery Pack Prices Below USD 80/kWh by 2029

Average pack costs fell to USD 115/kWh in 2024, down 14% year-on-year, driven by lithium carbonate deflation and gigafactory scale. Chinese LFP bids dipped to USD 95/kWh, enabling unsubsidized entry-level cars across Asia. Tesla projects USD 70/kWh by 2026 on its 4680 program, underscoring the captive-supply arbitrage available to vertically integrated OEMs.

Rapid Electrification Mandates for Heavy-Duty Trucks

China, the EU, and the United States have aligned timelines that push battery-electric trucks toward mainstream sales. China requires 50% zero-emission heavy-truck registrations in tier-1 cities by 2030, the EU is targeting a 90% emissions cut by 2040, and the U.S. EPA calls for 40% Class 8 battery-electric sales by 2032. Each tractor needs up to 400 kWh, amplifying cell demand far beyond passenger-car averages.

OEM Vertical Integration Driving Captive Cell Demand

BYD’s FinDreams supplied every battery for 3 million vehicles in 2024, Tesla’s Texas line is scaling toward 100 GWh by 2026, and Geely’s Zeekr introduced its Golden Brick LFP pack, all showcasing the pivot to in-house cell strategies. These moves erode purchasing volumes for contract manufacturers and compress negotiated pricing to single-digit margins.

Geopolitical Race to On-Shore Gigafactories

The U.S. Inflation Reduction Act gives USD 35/kWh cell production credits, the EU Battery Joint Undertaking co-funds 12 sites, and India’s PLI subsidizes 40 GWh of new capacity. Localization reduces shipping costs and tariff exposure while improving compliance with emerging traceability rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | –2.8% | Global, especially Europe, North America | Short term (≤2 years) |

| Solid-state and sodium-ion cannibalization risk | –1.9% | Japan, Europe | Long term (≥4 years) |

| ESG scrutiny on Chinese supply chains | –1.5% | Europe, North America | Medium term (2-4 years) |

| Battery-fire recalls in emerging markets | –1.3% | Asia-Pacific, Middle East, Africa | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Lithium carbonate collapsed 85% between January and December 2024, forcing miners such as Albemarle to throttle Australian output. Nickel sulfate swung 46% during the same period, squeezing NMC producers’ margins, whereas LFP suppliers faced relatively stable input costs. European cell makers, importing 90% of battery-grade lithium hydroxide, are especially exposed to currency risk.

Solid-State and Sodium-Ion Commercialization Risk

QuantumScape’s solid-state prototype achieved 800 Wh/L energy density in 2024 validation, promising 500-mile range sedans by 2028.(2)QuantumScape Corp., “Q4 2024 Shareholder Letter,” quantumscape.com CATL’s 2024 sodium-ion launch sliced 30% off material costs but carried a 20% energy-density penalty, aligning with short-range urban vehicles. Successful scaling of either technology could strand billions in liquid-electrolyte assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Dual Disruption Looms

In 2025, lithium NMC, LFP, and NCA held 90.87% of demand inside the Lithium-ion battery for electric vehicle market. NMC rules premium 400-mile models despite a 20-30% cost premium, while LFP now owns 44.65% of China’s passenger segment due to cobalt-free stability. Sodium-ion debuted for entry-level applications, and solid-state cells are projected at a 30.90% CAGR toward 2028 commercialization. The Lithium-ion battery market size for LFP alone is on track to surpass USD 124.7 billion by 2031 as Asian scooters and buses adopt the chemistry. Yet, if solid-state production costs fall under USD 120/kWh, incumbent liquid-electrolyte gigafactories face accelerated depreciation.

The Lithium-ion battery for the electric vehicle market must therefore manage a dual-front threat. Solid-state promises 60% higher energy density that challenges nickel-rich NMC in long-range segments, while sodium-ion undercuts LFP in cost-sensitive fleets. Producers are diversifying cathode portfolios, with SVOLT commercializing cobalt-free NMX to hedge against ESG scrutiny. Regulators’ carbon-footprint disclosure rules intensify chemistry selection; low-emission cathodes earn procurement preference in Europe beginning 2025.

By Cell Format: Structural Benefits Drive Prismatic Leadership

Prismatic cells delivered 47.55% of 2025 shipments within the Lithium-ion battery for electric vehicle market. BYD’s Blade integrates long prismatic units into the chassis, removing module housings and cutting weight by 15%. CATL’s Qilin achieves 255 Wh/kg pack density by embedding coolant channels within sidewalls. In contrast, cylindrical designs like Tesla’s 4680 held a 35.25% share and excel at automated production; tabless electrodes lower internal resistance by 50% to support 5-minute fast charging.

Pouch cells, at 17.20% share, are forecast for 22.80% CAGR through 2031 as BMW’s Neue Klasse favors flexible footprints that maximize cabin space. The Lithium-ion battery market size tied to pouch formats could reach USD 60 billion by decade-end as European gigafactories ramp up. Regional bias is evident: Asia champions prismatic, North America leans cylindrical, and Europe eyes pouch, forcing suppliers to maintain multi-format lines or risk customer attrition.

By Propulsion: BEV Centricity Simplifies Platforms

Battery electric vehicles generated 71.62% of 2025 cell demand and are growing at a 21.15% CAGR, accelerating the Lithium-ion battery for electric vehicle market. Each BEV uses 65 kWh on average, quadrupling PHEV needs and driving volume concentration. Ford, Stellantis, and Mercedes-Benz have published timelines to exit plug-in hybrids before 2030, simplifying cell qualification to one or two chemistries per OEM. In Latin America and Southern Europe, charging gaps keep PHEVs relevant, yet their share declines steadily as public charging builds out.

The Lithium-ion battery market share for BEV-specific cells reached 71.62% in 2025 and is forecast to reach near 79% by 2031, signaling contracting revenue pools for hybrid-only suppliers. Dedicated BEV platforms improve purchasing economies: Tesla’s unified cell order book yielded 15% lower prices than multi-propulsion rivals in 2024.

By Vehicle Type: Two-Wheeler Momentum

Passenger cars absorbed 70.12% of 2025 volume, but two- and three-wheelers are racing ahead at 31.20% CAGR, a key growth lever inside the Lithium-ion battery for electric vehicle market. Ola Electric’s swap-station network proved swappable LFP packs can remove home-charging barriers, while Indonesia’s similar deployments target 15 million annual motorcycle sales.

Light commercial vehicles, electrifying for e-commerce logistics, are running at a 18.62% CAGR as operators like Amazon lock in high-capacity van orders. Medium and heavy trucks, though only 6.15% of 2025 cell demand, will balloon once China’s 50% zero-emission rule and the EU’s 90% CO₂ cut blend into fleet procurement cycles. Region-specific chemistry splits remain: LFP dominates buses and two-wheelers; NMC holds premium sedans; emerging sodium-ion can capture intra-city delivery bikes by late decade.

Geography Analysis

Asia-Pacific accounted for 50.35% of the Lithium-ion battery for electric vehicle market in 2025, with China’s 550 GWh installed capacity dwarfing Europe and North America combined. Regional CAGR of 20.92% persists through 2031 as India’s PLI-backed plants and Southeast Asia’s two-wheeler boom raise cell offtake. China’s vertically integrated chain, covering 70% of global lithium refining, provides a 15-20% cost advantage versus import-dependent rivals.

North America’s IRA incentives underpin a 22.05% CAGR. Announced U.S. capacity reached 80 GWh in 2024, led by Tesla, GM-LG, Ford-SK, and Panasonic projects scheduled for 2025-2027 commissioning. Domestic sourcing requirements reshape supply deals, encouraging Asian giants to license technology locally to capture credits.

Europe follows at 19.35% CAGR on the back of the EU Battery Regulation and EUR 3.2 billion of joint-undertaking co-funding, which lifted the pipeline to 700 GWh in 2024. Northvolt, ACC, and CATL’s Hungarian site illustrate cost-competitive continental sourcing that erodes Chinese export margins.

South America and the Middle East-Africa collectively stood at 8.25% share but are accelerating. Brazil’s Stellantis line and Saudi Arabia’s Ceer venture target 2026 starts, creating early footholds for localized supply. Regional adoption focuses on buses and ride-hailing fleets where fuel savings are immediate.

Mordor Intelligence provides coverage of the lithium-ion battery for electric vehicle market across other key regional markets, including North America, Asia, Middle East and Africa, Europe, and South America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Kingdom and France incorporating local coverage and market participation, as required.

Competitive Landscape

The Lithium-ion battery for the electric vehicle market remains moderately concentrated. CATL, BYD, LG Energy Solution, Panasonic Energy, and Samsung SDI delivered 68% of 2024 output, yet vertical OEM entrants such as Tesla, Geely, and BYD increasingly displace third-party vendors. Chinese leaders wield 15-20% cost advantages via captive cathode and anode processing, prompting Western cell makers to differentiate on low-carbon credentials and patented fast-charging formats.

Strategic plays center on 800-V platforms, cobalt-free cathodes, and recycling loops that reclaim lithium and nickel at 80-90% efficiencies. Redwood Materials’ Nevada plant, fully operational in 2024, feeds 100 GWh of cathode precursor into Panasonic’s Kansas line at up to 30% material-cost savings. Patent activity supports the next transition: Toyota, Samsung SDI, and QuantumScape accounted for 60% of solid-state separator filings in 2024.

Margins bifurcate. BYD and Tesla post 25-30% gross margins from pack-to-vehicle integration, whereas independent cell makers slip below 10% as contract volumes fragment. European challengers leverage renewable-powered plants to win ESG-sensitive orders; Northvolt secured USD 15 billion in customer commitments by guaranteeing carbon-neutral cells.

Lithium-ion Battery For Electric Vehicle Industry Leaders

Panasonic Corporation

Samsung SDI Co., Ltd.

Contemporary Amperex Technology Co. Ltd (CATL)

Tianjin Lishen Battery Joint-Stock Co., Ltd.

LG Energy Solution Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CATL has introduced the Naxtra sodium-ion battery platform. These batteries are designed as a cost-effective alternative to lithium iron phosphate (LFP) packs for electric vehicles (EVs), offering reliable cold-weather performance and fast charging capabilities.

- September 2024: Northvolt obtained a USD 5 billion U.S. DOE loan guarantee for a 60 GWh Quebec facility serving GM and Volkswagen.

- August 2024: BYD’s FinDreams signed Ford for 45 GWh of LFP cells annually from 2026, marking Ford’s first Chinese supply pact.

- July 2024: Samsung SDI and GM broke ground on a USD 3.5 billion Indiana JV for 35 GWh of prismatic NMC output by 2026.

Global Lithium-ion Battery For Electric Vehicle Market Report Scope

A lithium-ion battery for electric vehicles (EVs) is a rechargeable battery commonly used to power electric cars and other electric vehicles. This battery technology is known for its high energy density, long cycle life, and lightweight design. It enables efficient storage and delivery of electrical energy. Lithium-ion batteries contain cells containing an anode, cathode, separator, and electrolyte. These batteries offer a high power-to-weight ratio, excellent energy efficiency, and reduced self-discharge compared to other rechargeable batteries, making them a preferred choice for modern electric vehicles.

Battery Chemistry, Cell Format, Propulsion Type, and Vehicle Type segments the Lithium-ion Battery for Electric Vehicles Market. By Battery Chemistry, the Market is Segmented by Lithium-ion (Nmc, Lfp, Nca), Emerging (Solid-state, Li-S, Na-ion), Lead-acid, and Nickel-metal-hydride. By Cell Format, the Market is Segmented Into Cylindrical, Prismatic, and More. By Propulsion Type, the Market is Segmented Into BEV, PHEV, and HEV. By Vehicle Type, the Market is Segmented Into Passenger Cars, Light Commercial Vehicles, Medium and Heavy Trucks, Buses and Coaches, and Two and Three-wheelers.

The report also covers the market size and forecasts for the lithium-ion battery for the electric vehicle market across major regions in terms of revenue in USD for all the above segments.

| Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) |

| Lead-acid |

| Nickel-metal-hydride |

| Cylindrical |

| Prismatic |

| Pouch |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Battery Chemistry | Lithium-ion (NMC, LFP, NCA) | |

| Emerging (Solid-state, Li-S, Na-ion) | ||

| Lead-acid | ||

| Nickel-metal-hydride | ||

| By Cell Format | Cylindrical | |

| Prismatic | ||

| Pouch | ||

| By Propulsion | Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Trucks | ||

| Buses and Coaches | ||

| Two and Three-wheelers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Lithium-ion battery for electric vehicle market in 2031?

The market is forecast to reach USD 332.65 billion by 2031, expanding at an 18.61% CAGR from 2026.

Which battery chemistry is growing fastest through 2031?

Solid-state prototypes and sodium-ion cells are collectively projected to post a 30.90% CAGR as they move from pilot to commercial scale.

How do U.S. IRA incentives affect cell manufacturing economics?

The IRA provides up to USD 35/kWh in production credits, often offsetting higher U.S. labor costs and accelerating domestic gigafactory plans.

Why are two-wheelers important for future battery demand?

India and Southeast Asia are electrifying scooters rapidly, with LFP packs enabling sub-USD 1,500 retail prices and 30%+ annual growth.

What risks could slow Lithium-ion battery adoption after 2028?

Commercial success of solid-state or sodium-ion technologies could cannibalize liquid-electrolyte demand, while raw-material price swings and ESG audits add near-term uncertainty.

Which companies dominate global capacity today?

CATL, BYD, LG Energy Solution, Panasonic Energy, and Samsung SDI together hold roughly 68% of installed output, though OEM vertical integration is slowly diluting that share.

Page last updated on: